actuarial methods slides

TRANSCRIPT

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 1/23

Actuarial Methods in theActuarial Methods in the EUEUGroupe Consultatif Groupe Consultatif

PaulPaul ThorntonThornton

DavidDavid CollinsonCollinsonMichael LucasMichael Lucas

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 2/23

Format of theFormat of the Groupe Consultatif Groupe Consultatif

reportreport

nn Commentary and overview of retirementCommentary and overview of retirement

benefits and funding vehicles, actuarialbenefits and funding vehicles, actuarial

methods and assumptionsmethods and assumptions

nn Country by country descriptionCountry by country descriptionnn Definition of actuarial methodsDefinition of actuarial methods

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 3/23

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 4/23

Typical actuarial calculationsTypical actuarial calculations

nn Calculation of past service funding positionCalculation of past service funding position

nn Calculation of cost and contributionsCalculation of cost and contributions

nn Analysis of demographic and economicAnalysis of demographic and economic

experienceexperience

nn Calculation of early retirement factorsCalculation of early retirement factors

nn Calculation of commutation factorsCalculation of commutation factorsnn Asset/Liability modellingAsset/Liability modelling

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 5/23

The focus for today's sessionThe focus for today's session

nn The calculation of the past service fundingThe calculation of the past service funding

position….influenced byposition….influenced by – – Regulation/supervisionRegulation/supervision

– – TaxTax

– – AccountingAccounting

– – Funding vehicleFunding vehicle egeg life assurance or pension fundlife assurance or pension fund

nn The past service funding position is a comparison of The past service funding position is a comparison of

– – Technical provisionsTechnical provisions

– – Fund assetsFund assets

The funding target in each country is a result of a mixture of

influences, not least common practice. There is variation both

The funding target in each country is a result of a mixture of

influences, not least common practice. There is variation both

within and between countries.

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 6/23

Valuation of assetsValuation of assets

nn Market value - Austria, Belgium, NetherlandsMarket value - Austria, Belgium, Netherlands

(some funds), Norway (accounting purposes),(some funds), Norway (accounting purposes),

Portugal, Spain, UKPortugal, Spain, UK

nn Discounted income value - Cyprus, Ireland,Discounted income value - Cyprus, Ireland,UK (use is generally declining)UK (use is generally declining)

nn Average market value - Cyprus, Ireland, UKAverage market value - Cyprus, Ireland, UK

(not common)(not common)

nn Book value - Denmark, Finland, GermanyBook value - Denmark, Finland, Germany

From an actuarial perspective the valuation of assets should be

consistent with the valuation of the liabilities (technical provisions)

and the expected return on assets assumption

From an actuarial perspective the valuation of assets should be

consistent with the valuation of the liabilities (technical provisions)

and the expected return on assets assumption

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 7/23

Technical provisionsTechnical provisions

nn The amount of the technical provisions isThe amount of the technical provisions is

dependent ondependent on

– – Actuarial funding methodActuarial funding method – – Economic assumptions (Discount rate, salaryEconomic assumptions (Discount rate, salary

inflation, price inflation, social security inflation)inflation, price inflation, social security inflation)

– – Demographic assumptions (RetirementDemographic assumptions (Retirementage,mortality,turnover,disability,partners issues)age,mortality,turnover,disability,partners issues)

– – The benefits valuedThe benefits valued egeg discretionary benefitsdiscretionary benefits

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 8/23

Most commonly used actuarialMost commonly used actuarial

funding methodsfunding methods

nn Projected Unit Method Projected Unit Method --

Belgium, Cyprus, Germany (commercial accounting),Belgium, Cyprus, Germany (commercial accounting),Ireland, Netherlands (commercial accounting), SpainIreland, Netherlands (commercial accounting), Spain

and United Kingdom andand United Kingdom and IASIAS/US/US GAAPGAAP

nn Current Unit Method Current Unit Method - Finland, Netherlands, Norway,- Finland, Netherlands, Norway,SwitzerlandSwitzerland

nn Attained Age Method Attained Age Method - Austria, Germany (infrequent),- Austria, Germany (infrequent),

Ireland (infrequent)Ireland (infrequent)

nn Entry Age Method Entry Age Method -Germany and Austria (Infrequent)-Germany and Austria (Infrequent)

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 9/23

X

DBO

X+1

Servicecost

Projected

0 Service

Salary

Current

Benefit

Pension accrualPension accrual

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 10/23

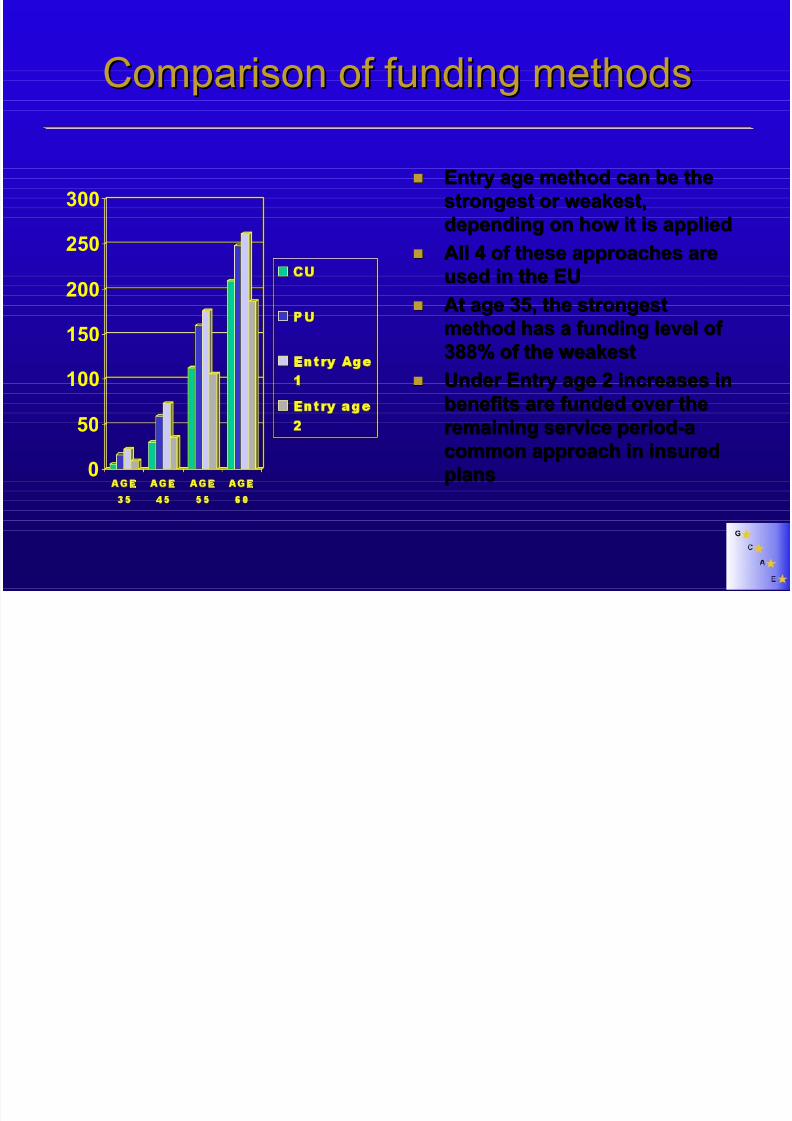

Comparison of funding methodsComparison of funding methods

0

50

100

150

200

250

300

AGE

35

AGE

45

AGE

55

AGE

60

CU

PU

Entry Age

1

Entry age

2

nn Entry age method can be theEntry age method can be the

strongest or weakest,strongest or weakest,depending on how it is applieddepending on how it is applied

nn All 4 of these approaches areAll 4 of these approaches are

used in theused in the EUEU

nn

At age 35, the strongestAt age 35, the strongestmethod has a funding level of method has a funding level of

388% of the weakest388% of the weakest

nn Under Entry age 2 increases inUnder Entry age 2 increases in

benefits are funded over thebenefits are funded over the

remaining service period-aremaining service period-a

common approach in insuredcommon approach in insured

plansplans

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 11/23

Factors affecting choice of methodFactors affecting choice of method

nn Tax restrictions eg Germany, maximum funding inTax restrictions eg Germany, maximum funding in

NetherlandsNetherlands

nn Supervisory minimum funding levels eg Netherlands,Supervisory minimum funding levels eg Netherlands,

Belgium, UKBelgium, UK

nn Accounting standards eg FRS17, IAS19, FAS87,Accounting standards eg FRS17, IAS19, FAS87,

local accounting ruleslocal accounting rules

nn

Nature of fundNature of fund

egeg

'open' or 'closed''open' or 'closed'

nn Funding vehicleFunding vehicle egeg pension fund or life insurancepension fund or life insurance

nn Past custom and practicePast custom and practice

The role and responsibilities of the actuary varies across the EU, with

significant variation in the extent to which actuaries have professional

The role and responsibilities of the actuary varies across the EU, with

significant variation in the extent to which actuaries have professional

freedom or must follow detailed rules and regulations

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 12/23

Economic assumptionsEconomic assumptions

nn Single defined discount rate used egSingle defined discount rate used eg

Germany, Netherlands, Sweden, Finland,Germany, Netherlands, Sweden, Finland,

SwitzerlandSwitzerland

nn Full set of assumptions applied eg Belgium,Full set of assumptions applied eg Belgium,Cyprus, Ireland, UK and Spain plusCyprus, Ireland, UK and Spain plus

applications of US GAAP and IAS19applications of US GAAP and IAS19

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 13/23

Example single discount ratesExample single discount rates

nn Austria - 6.0% for book reserve tax calculationsAustria - 6.0% for book reserve tax calculations

nn Finland - 3.5% to 4.25% for pension fundsFinland - 3.5% to 4.25% for pension funds

nn Germany - 6.0% for book reserve calculationsGermany - 6.0% for book reserve calculations

nn Netherlands - 4.0%Netherlands - 4.0%nn Slovenia - 4.0%Slovenia - 4.0%

nn Norway - 3.0% or 4.0%Norway - 3.0% or 4.0%

nn Sweden - 3.75%Sweden - 3.75%

nn Switzerland - 4.0%Switzerland - 4.0%

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 14/23

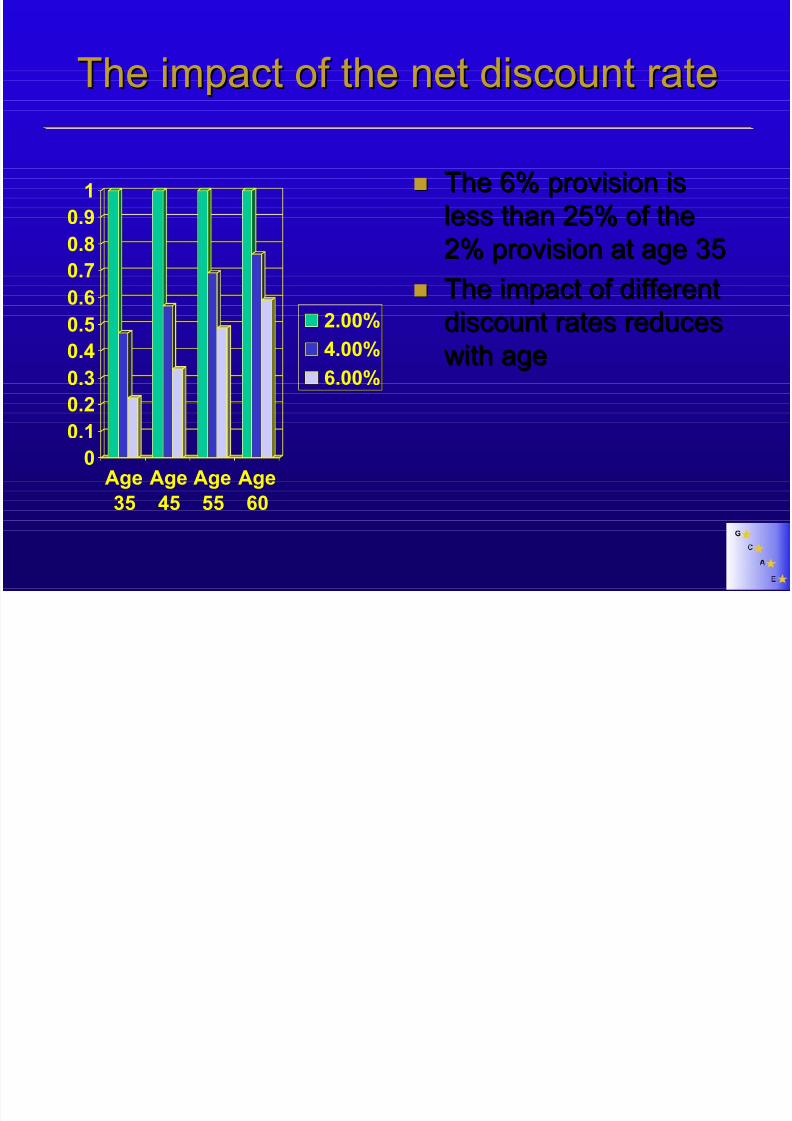

The impact of the net discount rateThe impact of the net discount rate

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

Age

35

Age

45

Age

55

Age

60

2.00%

4.00%

6.00%

nn The 6% provision isThe 6% provision is

less than 25% of theless than 25% of the2% provision at age 352% provision at age 35

nn The impact of differentThe impact of different

discount rates reducesdiscount rates reduceswith agewith age

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 15/23

Demographic assumptionsDemographic assumptions

nn Practice ranges from full complete set of Practice ranges from full complete set of

demographic assumptions to consideringdemographic assumptions to considering

mortality and retirement onlymortality and retirement only

nn Practice varies from using standard tablesPractice varies from using standard tablesspecified in regulations to complete freedomspecified in regulations to complete freedom

of choice for the actuary (eg UK/Ireland)of choice for the actuary (eg UK/Ireland)

nn In most countries standard mortality tablesIn most countries standard mortality tables

developed either through population or other developed either through population or other

censuses are usedcensuses are used

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 16/23

Comparison of pensioner mortalityComparison of pensioner mortality

12

12.5

13

13.5

14

14.5

15

15.5

16

Bum

Fa

Gma Ia

y NSn

Swe U

PV of pension at 65

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 17/23

What benefits are valued?What benefits are valued?

nn Under many pension plans there are optionsUnder many pension plans there are options

available for the employeeavailable for the employee egeg retirement ageretirement age

nn Under many pension plans there are optionsUnder many pension plans there are options

available for the employer/fundavailable for the employer/fund egegdiscretionary pension increasesdiscretionary pension increases

The extent to which these options/choices are built into the

calculation of the technical provisions will affect the security provided

to members

The extent to which these options/choices are built into the

calculation of the technical provisions will affect the security provided

to members

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 18/23

The possible impact of valuing optionsThe possible impact of valuing options

(early retirement and pension increases)(early retirement and pension increases)

8

910

11

12

13

14

15

16

Provision at age 60

Deferred pensionfrom 65

Deferred pensionwith increases

Immediate pension

Immediate pensionwith increases

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 19/23

The development of accountingThe development of accounting

standardsstandards

nn 10 years ago - only10 years ago - only SSAP24SSAP24????

nn Now - currently IAS19 gaining wide recognition andNow - currently IAS19 gaining wide recognition and

useuse

nn Expanded use of US GAAP by European companiesExpanded use of US GAAP by European companies

listed on the New York Stock Exchangelisted on the New York Stock Exchange

nn Further development of country specific accountingFurther development of country specific accounting

standards, for example,standards, for example, RJ271RJ271 in the Netherlandsin the Netherlands

and Swedish accounting standardsand Swedish accounting standards

nn Replacement of SSAP24 byReplacement of SSAP24 by FRS17FRS17

nn

Increasing emphasis onIncreasing emphasis on 'Transparancy''Transparancy' of accountingof accountinginformation on pension plansinformation on pension plans

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 20/23

Overall trend of accountingOverall trend of accounting

standardsstandards

nn Move to market based approach for valuing assetsMove to market based approach for valuing assets

nn Move to market related discount rate that reflectsMove to market related discount rate that reflects

long-term, high quality corporate bond yieldslong-term, high quality corporate bond yields

nn Move to straight line approach for amortisation of Move to straight line approach for amortisation of

gains and lossesgains and losses

nn Move to Projected Unit MethodMove to Projected Unit Method

nn

Move to more complete actuarial assumptions setsMove to more complete actuarial assumptions setswith each assumption specified individually rather with each assumption specified individually rather

than implicitly through the use of a net discount ratethan implicitly through the use of a net discount rate

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 21/23

ConclusionsConclusions

nn Different actuarial funding methodsDifferent actuarial funding methods

nn Different approaches to setting actuarialDifferent approaches to setting actuarial

assumptionsassumptions

nn Different assumptions usedDifferent assumptions usednn Different approaches to valuation of assetsDifferent approaches to valuation of assets

nn

Different approaches to setting demographicDifferent approaches to setting demographicassumptionsassumptions

nn Different approaches to valuing options andDifferent approaches to valuing options and

choiceschoices

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 22/23

ConclusionConclusion

nn Being fully funded under the new EU directive onBeing fully funded under the new EU directive on

pensions will mean different things in differentpensions will mean different things in differentcountriescountries

8/3/2019 Actuarial Methods Slides

http://slidepdf.com/reader/full/actuarial-methods-slides 23/23

Actuarial Methods in theActuarial Methods in the EUEUGroupe Consultatif Groupe Consultatif

PaulPaul ThorntonThornton

DavidDavid CollinsonCollinson

Michael LucasMichael Lucas