adb catalyzing microfinance for the poor business planning reading... · adb catalyzing...

TRANSCRIPT

Bank of Lao PDR Asian Development Bank

ADB Catalyzing Microfinance for the Poor

Business Planning Training for MFIs Reading Materials

1

Table of Contents SESSION 1: INTRODUCTION TO BUSINESS PLANNING ................................................................................. 2 SESSION 2: ENVIRONMENTAL ANALYSIS ......................................................................................................... 4 SESSION 3: CLIENTS AND MARKETS ................................................................................................................... 7 SESSION 4: PRODUCTS AND SERVICES ............................................................................................................. 10 SESSION 5: PORTFOLIO PLANNING ................................................................................................................... 14 SESSION 6: HUMAN RESOURCE MANAGEMENT ........................................................................................... 16 SESSION 7: MARKETING & PROMOTION ......................................................................................................... 19 SESSION 8: SOCIAL PERFORMANCE MANAGEMENT .................................................................................. 23 SESSION 9: FINANCIAL PLANNING .................................................................................................................... 26

2

Session 1: Introduction to Business Planning 1. What is business planning? A business plan is a plan that enables an organisation to look ahead, allocate resources, focus on key points, and prepare for problems and opportunities. Business planning is about results. You need to make the contents of your plan match your purpose. Unfortunately, many people think of business plans only for starting a new business or applying for business loans. But they are also vital for running a business, whether or not the business needs new loans or new investments. Businesses need plans to optimize growth and development according to priorities. Business Planning incorporates both strategic and operational planning for achieving outreach and sustainability. Strategic Planning enables us to define broad institutional goals for the future based on an assessment of the current situation. Operational planning allows us put those goals into action by detailing specific activities, their costs and the sources of income that will be received as a result. In order to be sustainable, an MFI must be financially self sufficient. It therefore needs to operate as a business. Sure it can have social objectives as well as financial ones, but the financial sustainability imperative makes it a business. And every business needs a plan. 2. The elements of a business plan

Microfinance business plans contain the same elements as for any business. Plan formats and outlines may vary, but generally a plan should include the following components:

1) Organisational Profile: summarises the history, mission, structure etc. of the organisation.

2) Environmental Analysis: frames the economic, regulatory and business environment in which you operate

3) Market Analysis: you need to know your market, customer needs, where they are, how to reach them, etc.

4) Products and Services: describes your savings and loan products and any other services you are providing, or plan to provide.

5) Portfolio / Outreach Plan: your expected level of activity for each product / service. This generates your financial plan, and determines your resource needs, so is critical to the planning process.

6) Human Resource Management: describes the staffing structure and the key roles and responsibilities, as well plans for staff development.

7) Marketing & Promotion: To be successful, people need to know about your services. Who will you target and how?

8) Social Performance Management: Non-profit agencies have a social agenda, how will poverty, gender and other social objectives be tracked and managed?

9) Financial Analysis: Identifies your funding sources, presents the balance sheet and projected Profit and Loss and Cash Flow tables.

2. Components of the organisational profile

3

The first section of the business plan is the Organisational Profile. This contains the following elements:

1. Background – brief history of organisation 2. Mission – brief mission statement 3. Goals / Objectives – lists your organisational goals 4. Organisational Structure - governance and legal structure, management &

staffing 5. Clients / beneficiaries – identifies your main clients / beneficiaries 6. Activities & Services – describes what your organisation does / offers

Mission & Objectives A Mission Statement is a declaration of organisational purpose. A good mission statement should state:

• What issues the institution is trying to address • How the institution responds to these issues • Who the intended clients are

Two example mission statements

1) To deliver best practice economic and social development programs 2) To reduce poverty by providing training in business development that enables the

poor to improve their businesses Which of these do you think is better? Why?

Organisational goals / objectives reflect how the institution intends to pursue its mission with specific statements about:

• The core activities • The outreach goals / objectives • The impact goals / objectives • The institutional goals / objectives

Here are some examples of organisational goals / objectives: 1. To deliver efficient and affordable savings and credit services to poor rural households 2. To reach at least 10,000 households with savings services 3. For 50% of member households to move out of poverty within 3 years of joining 4. To maintain at least 70% of women clients and staff 5. To be financially self-sufficient Note that these are different to operational objectives, which are more specific and will be developed later in the business plan. Examples of operational objectives are: 1. To extend savings and credit services to five new villages by December 2008 2. To commence using a computerized MIS by July 2009 3. To complete client surveys with at least 200 clients by October 2008 4. To recruit and train two new field officers by December 2008 5. To grow the outstanding loan portfolio to $10,000 by December 2009

4

Session 2: Environmental analysis 1. Why complete an environmental analysis? What do we mean by ‘microfinance

environment’? The microfinance environment includes a range of factors such as: economic, business /

competition, social / cultural, legal and regulatory, and political environment.

For the purpose of the business plan we are going to focus on just a few of these: economic; regulatory; and other service providers.

The environmental analysis should help to clarify the key areas that the MFI needs to consider in order to achieve its goals in the face of external factors.

2. Economic considerations

In this section we consider the local economic environment. Consider how economic factors may affect their business as an MFI.

Some examples of important economic factors are: • Inflation • Main income sources for target clients • Growth sectors / economic opportunities • Paid employment levels • Existence of cash economy at local level

Now consider how each of these factors may influence decisions you make about the way

you run your MFI. For example: • Product design – loan terms, repayment frequency, loan uses • Interest rates charged on loans, and paid on savings • Geographic areas to target for expansion • Economic sectors to target for expansion • Particular types of clients to target • The pace of growth

3. Regulatory framework

The regulatory framework that an MFI operates within comprises a range of different laws

and regulations. Some examples of regulatory factors are: • business registration • legal system • financial accounting requirements • standards for reporting • capital requirements

The Bank of Lao has specific regulations for MFIs, comprising: Savings & Credit Unions, Deposit –Taking MFIs, and Non Deposit-Taking MFIs. You should be familiar with the regulations that apply to your organization.

4. Competition & Partnerships

COMPETITORS: Every business, even an NGO-MFI, is in competition with others. It is very important to know who are our main competitors in order to offer competitive products and services, as well as marketing strategies. For example, if the competition is too strong you may choose not to enter certain markets / areas.

5

You should list your competitors, and their strong points and weak points. Here is an example:

Competitors Strenghts (+) Weaknesses (-) 1. Village fund Low interest rates, fast

approval, familiarity, convenient

Small loan sizes, limited capital, weak management, no savings services

2. Money lender Fast approval, no paperwork, familiarity, convenient

Small loan sizes, not always available, no savings service, high interest rate charges

3. APB Branch infrastructure, plenty of capital, low interest loans

Difficult to access loans, paperwork, too far away, inconvenient

‘PARTNERS’. Partnering with other organisations can help your MFI to achieve its goals, improve your performance, increase outreach. These partners could be any company, organization or government agency that can assist you in your work. Ask participants to list some of their existing or potential partners.

For each partner, identify how they will support you, and how you will support them. Here is

an example:

Partners How they can support me How I can support them Village committee Mobilise villagers, arrange

meetings, promotion Provide useful services, help reduce poverty

Agricultural extension service Provide ag training to clients, more successful businesses

Pay travel and per diems for staff; take photos and report on benefits to community

Now take a look back at your Competitors. Are there any competitors that could become

Partners? Discuss ways that MFIs could potentially work with their competitors in a partnership arrangement.

For example: an MFI might use the APB branch to deposit the monthly savings, which could be deposited by a Village Committee member. This might save the MFI staff having to attend all meetings.

For any competitors that do not become partners, you need to consider how you will

compete. What will you do to ensure that your products / services are more attractive than those of you competition?

5. Major risks and assumptions Whenever we develop a plan or strategy, we should be aware of the assumptions we are

making, and the risks we are facing. We will begin by looking at the risks and assumptions regarding the economic environment.

Refer back to the list of economic considerations. And list examples of risks or assumptions relating to these items. For example:

i. Market for silk continues to grow ii. Inflation does not increase above 15% p.a.

6

Now add more risks and assumptions relating to competition and partnership. For example: iii. APB is willing to open group savings account iv. Competitor MFI does not start offering savings services

7

Session 3: Clients and Markets

1. Understanding markets and clients Understanding markets and clients helps a microfinance institution develop the

capacity to serve those clients in ways that expand outreach, achieve greater impact, and enhance institutional sustainability.

Learning more about clients’ needs and preferences helps an MFI to develop new products and delivery channels, or refine existing ones.

While we often think we know what clients want / need, our assumptions are not always correct. In the past, many MFIs implemented a certain methodology without proper consideration of what their clients wanted. Nowadays, MFIs around the world have learned that – just like any business – they need to put their clients first. This means identifying and responding to their needs and preferences.

MFI staff will often get informal feedback from clients, but it is also important to use more structured means of gaining client feedback. Some common methods that MFIs use to gain client feedback and suggestions are:

• Structured surveys • Focus group discussions • Suggestion boxes (placed at the branch or at the village meeting)

2. Who are the target markets?

What do we mean by ‘markets’? A “market segment” is a group of clients with similar needs that are different from those of other groups. Often we choose to disaggregate market segments by geographic location, or by economic activity. Why look at market segments? Since a market segment is a group of people with similar needs, they often require a similar product or service. For example, an MFI may identify two main market segments: agriculturalists and traders.

Assessing the volume of demand for products will inform management of whether the specified market is likely to be cost efficient for the MFI: this is critical to the future viability of the organisation. Before entering a new market, it is important to consider key features of each segment:

The estimated size of the market The overall level of demand for financial services Significant market trends – is the market increasing or decreasing?

This information should feed directly into your MFI’s portfolio planning. So, how can we collect this kind of information? Secondary data in the form of government statistical data, industry reports, and donor studies may be a cost effective way of gathering such information. In your analysis of the market you should identify the sources of data and any assumptions made to arrive at your conclusions.

3. What are the needs and preferences of the target clients?

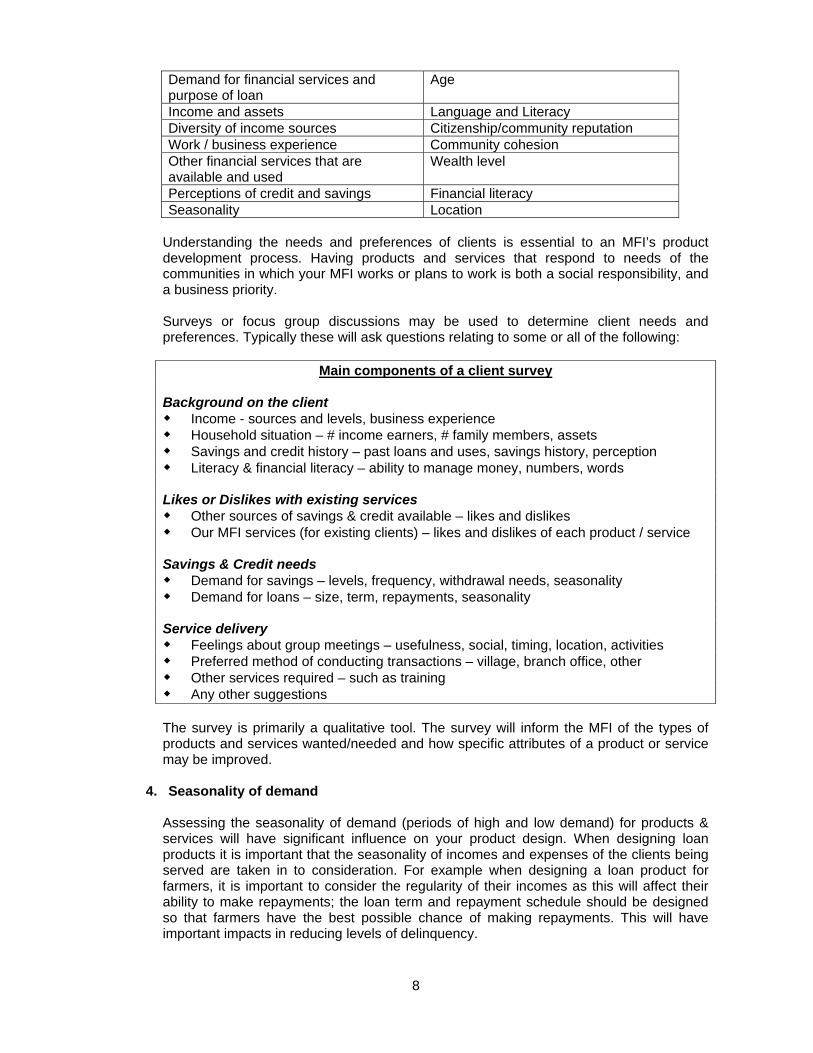

Once we have identified the market segments in which we work, it is important to understand more fully the different types of clients we serve. We should analyse the key characteristics of current and/ or potential clients. Consider both their economic and personal traits. This information will come from data collected through client surveys. Economic characteristics Personal & social characteristics Business type Gender

8

Understanding the needs and preferences of clients is essential to an MFI’s product development process. Having products and services that respond to needs of the communities in which your MFI works or plans to work is both a social responsibility, and a business priority. Surveys or focus group discussions may be used to determine client needs and preferences. Typically these will ask questions relating to some or all of the following:

Main components of a client survey Background on the client

Income - sources and levels, business experience Household situation – # income earners, # family members, assets Savings and credit history – past loans and uses, savings history, perception Literacy & financial literacy – ability to manage money, numbers, words

Likes or Dislikes with existing services

Other sources of savings & credit available – likes and dislikes Our MFI services (for existing clients) – likes and dislikes of each product / service

Savings & Credit needs

Demand for savings – levels, frequency, withdrawal needs, seasonality Demand for loans – size, term, repayments, seasonality

Service delivery

Feelings about group meetings – usefulness, social, timing, location, activities Preferred method of conducting transactions – village, branch office, other Other services required – such as training Any other suggestions

The survey is primarily a qualitative tool. The survey will inform the MFI of the types of products and services wanted/needed and how specific attributes of a product or service may be improved.

4. Seasonality of demand

Assessing the seasonality of demand (periods of high and low demand) for products & services will have significant influence on your product design. When designing loan products it is important that the seasonality of incomes and expenses of the clients being served are taken in to consideration. For example when designing a loan product for farmers, it is important to consider the regularity of their incomes as this will affect their ability to make repayments; the loan term and repayment schedule should be designed so that farmers have the best possible chance of making repayments. This will have important impacts in reducing levels of delinquency.

Demand for financial services and purpose of loan

Age

Income and assets Language and Literacy Diversity of income sources Citizenship/community reputation Work / business experience Community cohesion Other financial services that are available and used

Wealth level

Perceptions of credit and savings Financial literacy Seasonality Location

9

5. Putting it into practice The MFI that serves two types of clients, agriculturalists and traders, may choose to conduct two different types of surveys, one for each group. The agriculturalists may be interviewed through group surveys after harvest time, while the traders are interviewed individually at their place of business. Following the survey, the MFI may for example choose to define or refine two different loan products:

Agriculture loans: 6 month term (based on crop cycle), monthly interest payments, and lump sum repayment of principal at end of term (when harvest comes in)

Trading loan: variable terms (3-12 months), equal monthly installments of principal plus interest (since have regular cash flow)

Don’t forget the dropouts! In addition to surveying existing and potential clients, it is also important to talk to those who have dropped out. From both a business and a social perspective, it is preferable for an MFI to retain its existing clients rather that to always have to find new clients to replace the ones who are leaving. In order to improve client retention, you have to know why they are leaving and what you can do to avoid this.

10

Session 4: Products and Services

1. What do we mean by ‘Products’ and ‘Services’ in Microfinance?

MFIs typically offer their clients a range of products. A product is a specific item that you may choose to use. Here are some examples of typical microfinance products: • Savings products

Savings Product 1: Transaction account; Savings Product 2: 6-month term deposit account

• Loan products Loan Product 1: Agriculture loan Loan Product 2: Regular loan

• Insurance products Insurance Product 1: Death insurance Insurance Product 2: Crop insurance

In addition to these products, an MFI may also provide a range of services. Services involve the MFI performing work. For example: • Remittance services

e.g. client deposits money in one village and sends to a relative in another village • Skills training

e.g. coffee growing, IPM, sewing • Business training

e.g. doing market assessments, financial planning • Financial literacy training

e.g. how to calculate interest rates People often use the terms ‘products’ and ‘services’ almost interchangeably. For example, we may talk about savings services, or insurance services. One service offered by an MFI may be to provide a savings product. It really doesn’t matter which terms you use, as long as you provide what your clients need! 2. Developing new or existing products – the process

It is important that MFIs undertake a systematic process in developing or refining their loan or savings products. Products and services should be designed and delivered in such a way that they meet the current and evolving needs and preferences of the clients. Note: this section provides you with background information on how to develop new products or refine existing products. This is for your information only, you do not need to define this process in the business plan. There are 4 main steps to developing a product, which can be understood as a cycle:

2. Design

3. Testing

1. Market Research

4. Evaluating new product

refine design

11

1. Market Research: In the last session we talked about the importance of understanding markets and clients through market research activities like client surveys so that the products and services are designed to be popular and successful. 2. Design: We use the information gained from market research to design the product. Design will take into consideration the various product attributes described below. Costing and pricing of products is an important factor in product design; Effective interest rates have to be high enough for the MFI to become financially self sufficient once scale is reached. 3. Testing: Ideally you should test the new product with a sample group of clients before launching into on a large scale. Make sure you specify how you will evaluate this trial, so that later you will be able to determine whether or not the trial was successful. 4. Evaluating new product: Collect information and analyse the results to see how successful the product was with the sample group. Did the product satisfy your own objectives? Did it meet the needs of the client? What did the client dislike about the new product? Refine product: based on your evaluation of the test of the new product you can decide whether any further modifications are needed.

3. Key product attributes The products and services section of the business plan gives a description of the products and services that will be provided. Any new or planned products should be clearly specified. Each product has different attributes or features, which is what distinguishes it from other products. Also, loan products will have different types of attributes to savings products. We summarise the main attributes of savings and loan products below. Loan product attributes:

1. Size range: what is the size of the loan? This might be a fixed amount, but more likely, an amount within a range, i.e. $100-200

2. Term: Refers to the maturity or length of time until final repayment on a loan. 3. Repayment frequency: how often does the loan principle (and interest) need to be

repaid? Weekly, monthly? 4. Collateral/guarantee:

Collateral = assets pledged to secure the repayment of a loan, i.e. property. Guarantee = A pledge (could be by another person) to cover the payment of debt or to perform some obligation if the person liable fails to make repayments.

5. Interest rate (state period and flat or declining): Interest rate period = the period of time over which the interest rate is applicable i.e. 24% interest over 12 months term is the same as saying 2% interest rate per month. Which method of interest rate calculation do you use? Flat or declining interest rate method? (see box over page)

6. Current portfolio size: what is the total value of all your loans?

12

Saving Product attributes: 1. Minimum deposit: what is the minimum amount that a client must have in their

account while their account is active (usually opening deposit)? 2. Frequency of deposit: how often does the client have to make deposits into their

account? 3. Withdrawal conditions: what are the conditions (requirements set by the MFI) on

withdrawing from the account? Are there any restrictions on the customer accessing their money, i.e. maximum amount allowed to be withdrawn, maximum number of times money can be withdrawn?

4. Interest rate: how is the interest earned on savings calculated? how often does it get paid on the balance?

5. Current portfolio size: what is the total savings your MFI is currently holding?

4. MFI Services Separate from its products (savings, loans, insurance), an MFI may provide ‘services’. Services can be financial or non financial. Typical financial services offered by MFIs include:

Financial Literacy Training Remittance/Money Transfer

Typical non financial services offered by MFIs include:

Business/Livelihoods Training/Advice Business Development Services: Education (literacy, numeracy, other) Health (usually linked to a healthcare provider)

Below is an example of the products and services offered by TYM MFI:

Interest Rate Calculation Methods – Flat vs. Declining Balance:

1. Flat Rate: Interest is charged on initial loan amount rather than outstanding loan balance.

2. Declining Balance: Interest is charged on outstanding loan balance at a given point in time, so interest amount is different for every period.

For example, a 1-year loan of 600,000 kip at 12% p.a. interest, with quarterly installments of principal:

1. Using the Flat Rate method, total interest payable = 12% * 600,000 = 72,000 kip. 2. Using the Declining Balance method, total interest payable = (12%/4 * 600,000)

+ (12%/4 * 450,000) + (12%/4 * 300,000) + (12%/4 * 150,000) = 36,000 kip If the loan principal is all paid in one lump sum at the end of the loan term, then there is no difference in interest payable between the Flat and Declining Balance methods. Where instalments of principal are made, the declining balance method results in around half the interest rate cost of the flat method.

13

Example: TYM is a non bank financial institution in Vietnam. The bank provides the following products:

� Loans � Voluntary Savings � Insurance

It provides the following services also: � Business Development Services � Health � Education/ Training � Consulting

5. Action Plan

If your MFI is planning to develop or refine its products or services (the product attributes and/or the delivery process), you should develop an action plan that clearly defines:

the organisation’s planned objectives for product/service modification the specific activities your organisation must undertake to achieve it’s objectives, the person responsible for taking those actions a timeframe within which the action will be completed

Below is an example of an action plan: Product/Service

Objective Specific Activities Person

Responsible

Complete By (date)

1 To introduce a new loan product to meet the needs of farmers i.e. agriculture loan

1. Conduct market research with farmers in Rong Village 2. Design the loan product based on market research finding 3. Test new product 4. Evaluate and make necessary modifications to design of new product

1. Lara Jones (Snr. Loan officer) 2. Bob Smith (Operations officer) 3. Lara Jones (Snr. Loan officer) 4. Bob Smith (Operations officer)

1st April 2009 1st June 2009 1st July 2009 1st Dec 2009

2

3

4

5

.

14

Session 5: Portfolio Planning

1. What is Portfolio Planning?

A microfinance portfolio refers to the total value of the products being offered: i.e. Loan Portfolio = the total amount of loans outstanding; Savings Portfolio = the total amount of savings deposited at the MFI. Why it is important to plan a portfolio? How far ahead should we plan?

• Planning future numbers of clients helps us to plan our expansion of operations e.g. moving into new villages, hiring new staff, increasing expenses

• Planning the value of a portfolio tells us how much our interest income will be on loans, and how much our interest expenses will be on savings

• Planning the value of money coming in and going out helps us to plan for cash flow. We have to make sure we always have enough cash on hand to fund our portfolio and our operational expenses

• MFIs usually like to plan their portfolio for 2-3 years into the future, so that they can plan their future operations. Usually you should plan as far ahead as needed to reach full cost recover (i.e. total income exceeds total expenses)

2. Portfolio Quality

MFIs talk about portfolio quality. The quality of a loan portfolio is determined by the rate of delinquency among customers i.e. the percentage of loans that are not repaid. Gross Loan Portfolio: All outstanding principal of all active loans (i.e. current, delinquent and restructured loans, but not loans that have been written off). It does not include interest receivable. Arrears: the amount of repayments that are due but have not yet been paid. Current Portfolio: the outstanding value of all loans that do not have any instalment of principal past due. It does not include accrued interest. Delinquent Loan: a loan that has repayments due but not yet paid. Portfolio at Risk: Unpaid principal balance of all delinquent loans / Total outstanding portfolio Loan default: refers to when a borrower cannot or will not repay his/her loan and when the MFI no longer expects to receive repayment, although it keeps trying to recover it.

3. Loan Loss Provisioning A loan loss provision is an amount of money set aside to cover potential future loan losses. The longer a loan is overdue, the greater the provision. Loans that have been rescheduled (i.e. loan terms extended) require a higher level of provisioning than regular loans, since these are already considered to be risky.

15

BoL requires MFIs to provision on the following basis: Aging Status Reserve (Percent)

Regular Portfolio Rescheduled Portfolio Current loans 1% 25% Loans past due 31-90 days 25% 25% Loans past due 91-180 days 50% 50% Loans past due > 180 days 100% 100% Loans in legal recovery 100% 100% Loan Loss Provision: an amount expensed on the Income and Expenses Statement. It increases the Loan Loss Reserve Loan Loss Reserve: a balance sheet account that represents the amount of outstanding principal that is not expected to be recovered by an MFI. It is a credit balance on the asset side of the balance sheet (a ‘negative asset’), and reduces the outstanding portfolio. Microfinance organizations typically establish a loan loss reserve equal to 2-5% of the value of their active portfolios. Loan write-off: when an MFI decides that it is unlikely to receive a repayment, it removes the outstanding value of the loan from its overall loan portfolio. It uses the loan loss reserve to pay for this. Loan write-offs occur only as an accounting entry. They do not mean that recovery should not be pursued. They decrease the reserve and the outstanding portfolio

4. Delinquency Management Zero delinquency is:

a reasonable and obtainable target an attitude the whole organisation must adopt… if it is to become a reality. the result of a purposeful decision by the organisation

Understanding causes of delinquency:

can be internal (controllable) and external (uncontrollable but a response can be planned)

internal causes: image of MFI; bad MIS; inappropriate products and delivery mechanisms; poor staff skills and/or morale

external causes: government policies, natural disaster; economic conditions; personal crises.

It is important for the management of an MFI to consider the internal factors of delinquency and to put in place measures that respond to any issues that may arise. All staff should be conscious of delinquency and its causes and the MFI should manage its delinquency in a structured manner with loan officers reporting delinquency and management reviewing its causes and providing appropriate solutions.

16

Session 6: Human Resource Management

1. Why include human resources in the business plan?

An MFI’s most important asset is its staff. So it is important to consider staffing and management when we are preparing a business plan. In order to be effective, staff must be competent, trained, and motivated. It is also important to make sure you have the right number and type of staff. Too many staff leads to inefficiencies while too few staff leads to inadequate attention to procedures and detail. All of this must be planned to ensure that you are managing your human resources optimally.

2. Organisational Structure

When considering human resources, the first place to start is with an organisational chart. This enables you to see at a glance your overall staffing situation, including:

o The major groupings such as branches and sections o The total number of staff, as well as the numbers in each section / branch o The number of managers compared to the number of other staff o The relationships between personnel (lines of authority and communication), and

whether you have a very hierarchical or flat organisational structure. o Gaps in staffing that need to be filled

The organisational chart can serve as a tool for employees to understand how and where they fit into the mission of the institution. You can draw your organisational chart any way you like. Some organisations place the Managing Director in the middle, others at the top, or even at the bottom. Draw your chart in the way that makes the most sense to you.

3. Staffing

An efficient organisation should have clear roles and responsibilities. Every staff member (from the Managing Director to the Driver) should have a job description. The job description should state:

o The general and specific tasks that the staff member is required to perform o Who they report to o How they will be assessed o Incentives for good performance

Pay levels and working conditions should also be written down, either in the job description or a separate letter of employment. If you do not have written job descriptions for all of your staff then start now! In your business plan, summarise the key roles and responsibilities for each type of position (e.g. credit officer) listed in your organisational chart. Another key aspect of human resource management is regular performance review. This should take place at least once per year (or more often). It provides an opportunity for staff to hear from what their manager thinks of their performance – what they are doing well and what they need to improve. It also provides an opportunity for the manager to hear the thoughts, concerns and suggestions of their staff. Performance should always be assessed according to the job description. It is not fair to judge someone by standards that they are not aware of. The performance review is a good time to review job descriptions, as well as wage levels.

17

The productivity of staff can be measured in a variety of ways. Some simple measures of staff productivity are:

o Field officer caseload = no. of clients per field officer o Field officer portfolio = loan (or savings) portfolio per field officer o Clients to staff ratio = total no. of clients / total number of staff

When preparing your business plan, be sure to indicate your plans for future staffing. What staff do you plan to recruit in the future – what skills and qualifications do they need? You will also need to consider the costs involved when you are preparing your financial projections.

4. Staff Incentive Schemes Many MFIs use staff incentive schemes to encourage good performance from staff members. Incentives are not an entitlement – they should only reward good performance. Typical incentives include financial reward, i.e. a bonus. A well-designed performance-based staff incentive scheme (bonus scheme) can have positive and powerful effects on the productivity and efficiency of MFI operations. To be effective, such schemes must be transparent and fair. Staff incentive schemes take different forms and each has its own advantages and disadvantages:

Individual: incentive payout made to each person individually Group based: incentive payout made to a team of people Profit sharing schemes: incentive payout made to individuals depending on overall

profit gains of organization Employee Stock Ownership Plan: staff members own share capital Pensions benefits and other contributions Non-financial benefits: such as promotion, training and recognition (e.g. employee of

the month) Remember that your incentive scheme should match your organizational goals. For example, with regard to loan portfolio it is important to have both growth and quality. The most common incentives schemes apply to:

o The number of new clients this period o The value of new loans disbursed this period o Portfolio quality (PAR or other measure) o MFI or branch-level profit this period

The following are some considerations you should keep in mind when designing a performance based Staff Incentive Scheme:

Timing: typically staff should become eligible for participation in bonus schemes approximately six months after joining the organization

Frequency of Incentive Payout: ideally these incentive payouts should be monthly or frequently enough to relate the reward to particular efforts.

Weight of Bonus in Total Remuneration: In practice, for effective incentive schemes the weight of the bonuses for credit officers typically ranges from 20% up to 50% of total compensation.

Examples of Staff Incentive Schemes: Acleda Bank, Cambodia Staff incentive schemes:

1. Annual Merit Pay – based on achievement of annual goals / targets

18

2. Profit Centre Bonus (if RoE>20%)

3. 400 employees hold approx. 6% of share capital

Banco Ademi, Dominican Republic

Staff incentive schemes:

1. Performance-based monthly bonus for loan officers

2. Profit sharing: 10% of annual profits distributed to all employees

3. Employee Stock Ownership Plan (ESOP): Staff hold 20% of share capital and have a seat on the Board of Directors

5. Staff training & development

Every existing and new staff member should have opportunities for training and career development. It is therefore important to have a staff training and development plan.

The training plan might include a pre-service / induction training programme: comprising training on operating rules, policies and procedures of the MFI, and an introduction to the work ethic and philosophy of the organisation.

In-service training should be provided to upgrade the skills and knowledge of employees in specific areas such as products and services; internal controls; systems and procedures; reporting; savings and loan account administration; branch accounting and Management Information System; Delinquency management etc.

The organisation should identify who is responsible for managing training activities and who the training activities could be provided by. An outline of these plans should be provided in the business plan.

6. Action Plan

It is recommended that you devise an action plan that clearly defines the specific activities your organisaiton must undertake to achieve its human resource management objectives. This action plan may cover such activities as:

o Plans for recruitment of new staff o Changes to organisational structure o Employee performance review / job description review o Reviews of incentive schemes o A staff retreat or other activity o

When preparing an action plan be sure to identify the person responsible for each action and a timeframe within which the action will be completed.

19

Session 7: Marketing & Promotion

1. What is marketing? A broad definition: Marketing is the way an institution engages with the various markets it serves or would like to serve.

Marketing focuses on what the market values, rather than what the institution wants to provide: The production concept: “Make it and it will sell” The product concept: “Make it well and it will sell.” The selling concept: “Promote it well and it will sell.” The marketing concept: “Make something the market values and it will sell.” Marketing brings together information from internal and external sources to determine the best answers to the following questions:

• Which products and services are needed and will be bought? • What price is acceptable to clients? • How can products and services be sold in the most efficient and effective

manner? • Which information channel is best able to reach clients to make the product

known, valued and demanded? We have already discussed client needs and preferences in Session 3, and products in Session 4, so this session will focus on how an MFI effectively reaches clients with information about its products and services. Remember that marketing is more than selling and promotion of products. It is the customer focus of the whole organization. 2. Marketing for MFIs Why do MFIs need to do marketing?

“Financial viability is dependent on client satisfaction.”

In places where microfinance is relatively new, MFIs typically put little effort into marketing since they often have no competition. But in places where MFIs compete with each other for the same clients, marketing is quickly becoming a critical concern of MFIs. Increasing competition requires MFIs to put more energy into retaining and finding new customers. 3. The Marketing Mix

Marketing comprises a ‘mix’ of 8 different features. Read about each of these below. For each product or service you offer, you should specify each of the following, and compare this with your competitors. Feature Details Product (design)

Includes specific product features, opening/minimum savings balances, withdrawal terms, loan terms, loan disbursement times, collateral or guarantees, repayment structures

Price Includes the interest rate, withdrawal costs, loan fees, pre-payment

20

Feature Details penalties, prompt payment incentives, transaction costs and other fees and discounts.

Promotion Includes advertising, public relations, direct marketing, publicity, and all aspects of sales communication.

Place Refers to distribution and making sure that the product/service is available where and when it is wanted. This includes such options as field workers or agents, branches, working with informal sector financial service providers, etc.

Positioning Is the effort by the MFI to occupy a distinct competitive position in the mind of the target customer. This could be in terms of low price, security of savings, quick turnaround time, professional service, etc. It is a perception.

Physical Evidence

This is what makes the MFI and its invisible, intangible services visible. It includes the presentation of the product, how the branch physically looks, whether it is tidy or dirty, newly painted or decaying, the appearance of the brochures, posters and passbooks, etc.

People Includes how the clients are treated by the people involved with delivering the product – in other words the staff of the MFI.

Process Includes the way or system through which products and services are delivered: the queues/waiting involved, forms to be completed etc.

Source: MicroSave

4. Key Aspects of Marketing “The most important thing is to improve the amount and quality of attention

given to the client.” FUPACODE, Paraguay

Marketing is a continuous process that includes planning, implementing and evaluating performance. MFI marketing involves studying clients and developing products to meet their needs. It takes into consideration the competitive market, determines the position of the institution in that market, and promotes products to potential clients. Carrying out these activities effectively often requires a specific marketing plan. Market & Client Analysis Marketing begins with the clients, by identifying potential markets and then surveying clients to determine their specific needs and desires. These steps were covered in Session 3. Competitive Analysis By studying the competition, an MFI can be informed about the types of financial services that are offered by its competitors. The level and type of competition will affect how the MFI decides to position itself strategically in the market.

Strategic Planning and Positioning Assemble all of the market information you have and determine how best to place to your organization within that market. i.e. what image would you like to convey?

Promotion and Outreach Communications

ACLEDA in Cambodia conducts regular questionnaires with 100 micro and small

enterprises and 100 small and medium sized enterprise clients at each of its

branches every year.

SEWA Bank in India and Fundación Mario Santo Domingo in Colombia offer corresponding social services along with

their credit product to create a competitive edge.

21

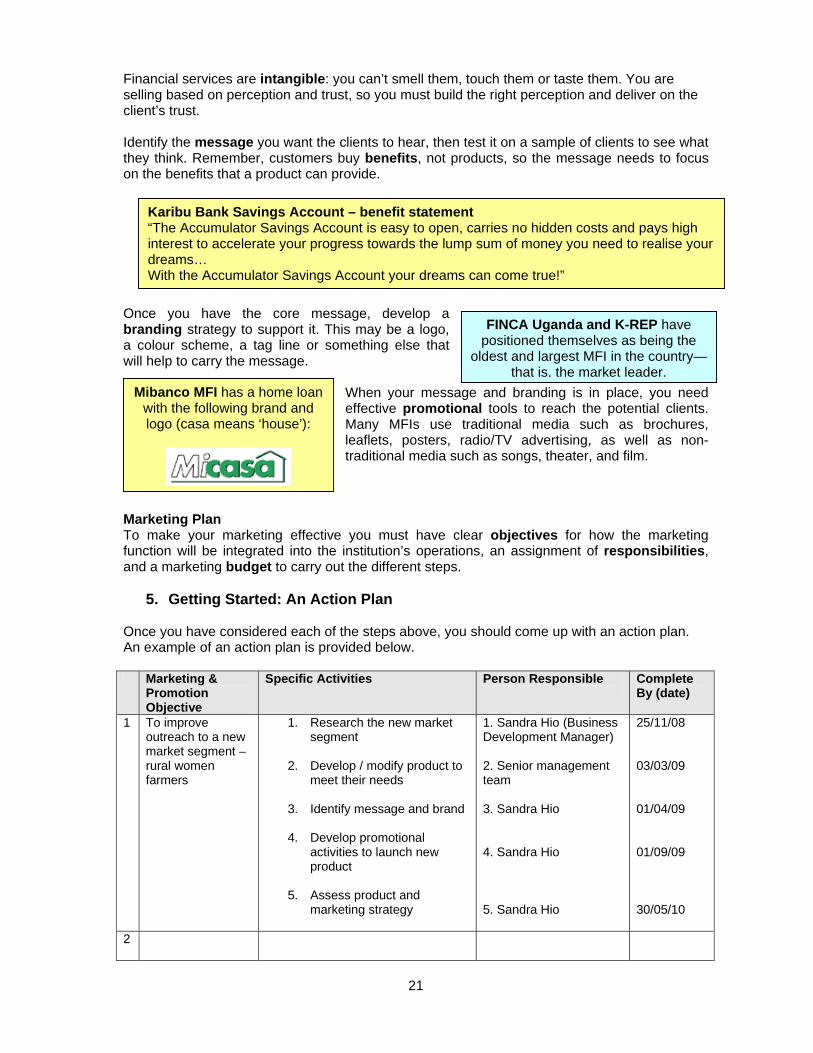

Financial services are intangible: you can’t smell them, touch them or taste them. You are selling based on perception and trust, so you must build the right perception and deliver on the client’s trust. Identify the message you want the clients to hear, then test it on a sample of clients to see what they think. Remember, customers buy benefits, not products, so the message needs to focus on the benefits that a product can provide.

Once you have the core message, develop a branding strategy to support it. This may be a logo, a colour scheme, a tag line or something else that will help to carry the message.

When your message and branding is in place, you need effective promotional tools to reach the potential clients. Many MFIs use traditional media such as brochures, leaflets, posters, radio/TV advertising, as well as non-traditional media such as songs, theater, and film.

Marketing Plan To make your marketing effective you must have clear objectives for how the marketing function will be integrated into the institution’s operations, an assignment of responsibilities, and a marketing budget to carry out the different steps.

5. Getting Started: An Action Plan Once you have considered each of the steps above, you should come up with an action plan. An example of an action plan is provided below. Marketing &

Promotion Objective

Specific Activities Person Responsible

Complete By (date)

1 To improve outreach to a new market segment – rural women farmers

1. Research the new market segment

2. Develop / modify product to

meet their needs 3. Identify message and brand 4. Develop promotional

activities to launch new product

5. Assess product and

marketing strategy

1. Sandra Hio (Business Development Manager) 2. Senior management team 3. Sandra Hio 4. Sandra Hio 5. Sandra Hio

25/11/08 03/03/09 01/04/09 01/09/09 30/05/10

2

FINCA Uganda and K-REP have positioned themselves as being the

oldest and largest MFI in the country— that is, the market leader.

Karibu Bank Savings Account – benefit statement “The Accumulator Savings Account is easy to open, carries no hidden costs and pays high interest to accelerate your progress towards the lump sum of money you need to realise your dreams… With the Accumulator Savings Account your dreams can come true!”

Mibanco MFI has a home loan with the following brand and logo (casa means ‘house’):

22

3

23

Session 8: Social Performance Management

1. What is social performance management?

Social performance management = an ongoing process which involves setting clear social objectives, monitoring and assessing progress towards achieving these, and using this information to improve overall organisational performance.

Most microfinance institutions (MFIs) have explicit social goals within their mission

statements, but often these are not managed actively. Social performance needs to be managed and reported as systematically as your

financial performance. Social Performance Management can help your MFI stay focused on its mission and

maximise both aspects of its performance – financial and social.

An example of Pro Mujer’s social objectives

Social goal Social objective

Offer services to women who live in conditions of socioeconomic exclusion

At all times, 95-98% outreach to women, percentage of men no higher than 5%

At the end of 2008, at least 50% of new clients will be below the poverty line

Expand coverage to 15 medium-sized towns by the end of 2008

Offer integrated services to satisfy the needs of the target clientele

By the end of 2008, to reach an average loan amount of $241.

Achieve a retention rate of 95% by the end of 2008

Establish, by the end of 2008, 3 new alliances with institutions to offer additional services to clients

Lead towards the sustainability of clients, their families and communities

Increase client income by at least 15%, by the end of 2008.

Increase of clients' participation in social organisations by 15%.

Increase of 5% in school attendance of clients’ children.

Clients’ savings will average $85 by the end of 2008

2. Assessing social performance

Unlike financial performance which can be assessed with the use of statistical data provided from within the organisation (financial reports), social performance is much more qualitative in nature and therefore requires a more qualitative approach to data collection. Best practice market-led microfinance should assess client satisfaction on an on-going basis. Client satisfaction reports are also the most appropriate way for an organisation to

24

assess its social performance against its pre-defined social objectives. As described in Step 3: Clients and Markets, client surveys and focus group discussions are simple methods that any organisation can employ to obtain such information. Remember: Client satisfaction surveys and focus group discussions should:

be undertaken in a participatory manner MFI staff should consider various formats of interviewing, including the introduction

of games, use of visual tools that will encourage more of a more qualitative analysis.

An example of Pro Mujer’s monitoring process:

Pro Mujer uses the following information sources to evaluate its progress towards its social goals:

Client monitoring and evaluation: assess client satisfaction and reasons for client exit. Use suggestion boxes, exit mini-surveys, staff and client feedback.

Social development services quality monitoring system: this tool looks at the quality of health and training services, and staff attention to clients. When complete, it will be integrated into the MIS.

Monitoring of client poverty levels External social rating reports and impact assessment, conducted

every two to three years

When planning your social performance monitoring, ask yourself:

1. What tools/methods will you use to measure social performance? 2. How often will you collect data? 3. Who will undertake data collection and analysis of the data? 4. Are you already collecting this data? 5. How will you monitor gender inequalities?

3. Assessing social & poverty impact, incl. gender considerations

In addition to looking at the organisation’s performance, it is important for an MFI to evaluate the impact it is having on its clients. MFI’s activities have various types of impact on its clients:

social impact (relationships); human impact (health, education); natural impact (access to land, water, infrastructure); physical impact (ownership of productive and non-productive assets); financial impact (income levels, levels of savings, access to finance).

An organisation’s assessment should also consider the extent to which gender inequalities have been addressed and have changed. MFIs should use qualitative tools such as client survey, interviews, focus group discussions to collect data on the impact of products and services.

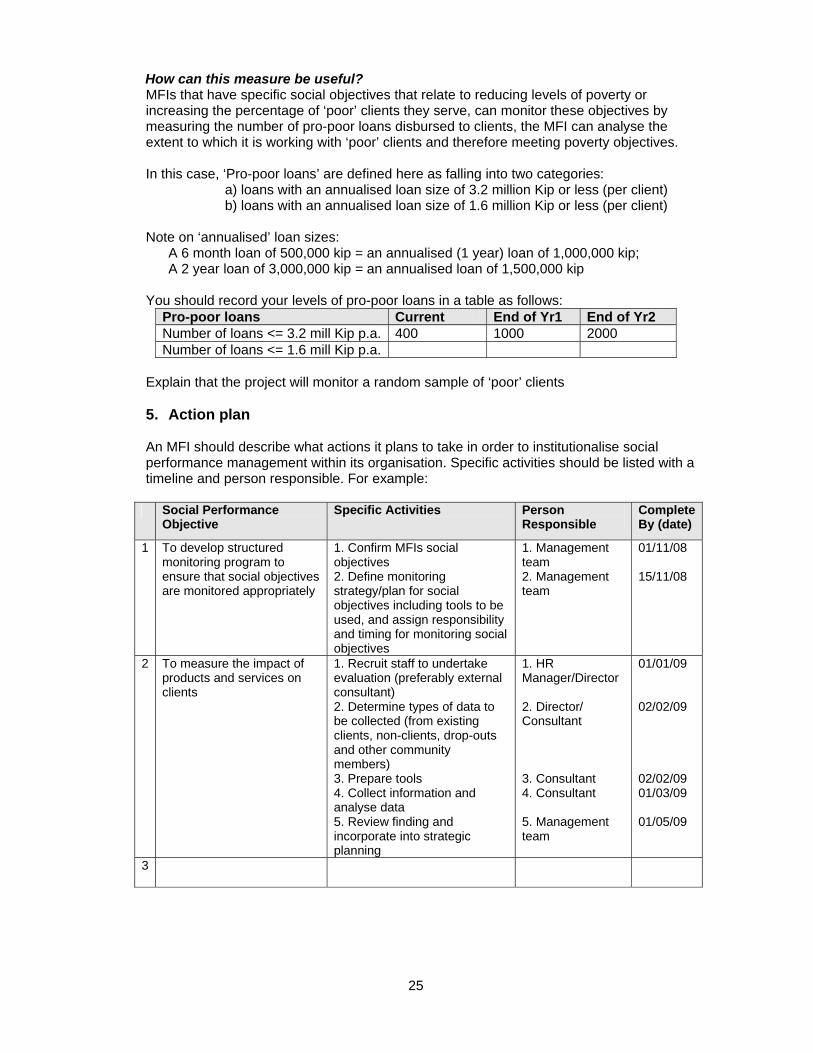

4. Social Performance Measurement: Pro-poor loans A ‘pro-poor loan’ is a loan that is designed to meet the needs of the poor (defined within a specific context).

25

How can this measure be useful? MFIs that have specific social objectives that relate to reducing levels of poverty or increasing the percentage of ‘poor’ clients they serve, can monitor these objectives by measuring the number of pro-poor loans disbursed to clients, the MFI can analyse the extent to which it is working with ‘poor’ clients and therefore meeting poverty objectives.

In this case, ‘Pro-poor loans’ are defined here as falling into two categories:

a) loans with an annualised loan size of 3.2 million Kip or less (per client) b) loans with an annualised loan size of 1.6 million Kip or less (per client)

Note on ‘annualised’ loan sizes:

A 6 month loan of 500,000 kip = an annualised (1 year) loan of 1,000,000 kip; A 2 year loan of 3,000,000 kip = an annualised loan of 1,500,000 kip

You should record your levels of pro-poor loans in a table as follows: Pro-poor loans Current End of Yr1 End of Yr2 Number of loans <= 3.2 mill Kip p.a. 400 1000 2000 Number of loans <= 1.6 mill Kip p.a.

Explain that the project will monitor a random sample of ‘poor’ clients 5. Action plan An MFI should describe what actions it plans to take in order to institutionalise social performance management within its organisation. Specific activities should be listed with a timeline and person responsible. For example:

Social Performance Objective

Specific Activities Person Responsible

Complete By (date)

1 To develop structured monitoring program to ensure that social objectives are monitored appropriately

1. Confirm MFIs social objectives 2. Define monitoring strategy/plan for social objectives including tools to be used, and assign responsibility and timing for monitoring social objectives

1. Management team 2. Management team

01/11/08 15/11/08

2 To measure the impact of products and services on clients

1. Recruit staff to undertake evaluation (preferably external consultant) 2. Determine types of data to be collected (from existing clients, non-clients, drop-outs and other community members) 3. Prepare tools 4. Collect information and analyse data 5. Review finding and incorporate into strategic planning

1. HR Manager/Director 2. Director/ Consultant 3. Consultant 4. Consultant 5. Management team

01/01/09 02/02/09 02/02/09 01/03/09 01/05/09

3

26

Session 9: Financial Planning

1. Income & Expenditure Projections

To help us plan future operations we need to know what income and expenditure we expect to incur. The easiest way to do this is by estimating our average monthly income and expenditure, then projecting this forward. If you are planning 2 or 3 years ahead then remember to factor in price rises each year.

Major income items Typical sources of MFI income are:

Interest received on loans Fees charged to clients Interest received on bank and other investments

Major expenditure items Typical MFI expenditure items are as follows:

Portfolio expenses such as interest paid on savings Loan loss provision expense Financing expenses such as interest paid on MFI borrowings Staffing expenses (branch and head office staff salaries) Other branch and head office operational expenses, such as rent, stationary,

postage, utilities, consumables, insurance, repairs & maintenance, fuel for vehicles, vehicle maintenance, travel and per diem, training/workshops, marketing, recruitment, audit and external accounting support, legal and licensing costs

Depreciation of fixed assets Taxes

Depreciation expense: When you purchase fixed assets (such as a motorbike) you do not record the purchase value of the item as an expense. Instead you add the asset to the balance sheet. Over time the value of the asset will reduce, so you need to reduce the value of the asset in the balance sheet. We do this by recording depreciation. Each month or year, an MFI should depreciate a percentage of the original value of the asset. This is recorded as an expense in the income statement.

Depreciation Example: An MFI purchases a motorbike for $2,000. The useful life of the motorbike is 4 years. So the MFI will record a depreciation expense of 25% ($500) each year for 4 years.

2. Sources of funds & Balance Sheet

Sources of Funds

MFIs typically access funding from a variety of sources and these should be clearly identified in the financial planning section of the business plan.

The following is a list of some common sources of funds for MFIs:

• Investor Capital: this refers to shares or other capital invested in the institution.

27

• Donations/Grants: these can be cash or in kind donations (i.e. office space, seconded staff, legal services etc). Donations/grants are usually made by government, international aid agencies, international NGOs or individuals)

o Restricted grant funding can only be used for a specified purpose o Unrestricted grant funding can be used for any area of MFI operations

• Savings: these may be deposited by members (those who have paid some membership fee) or non members (other clients)

• Borrowing: these are wholesale loans taken by the MFI. Loans may be available from government, international agencies or banks.

• Retained earnings: this is the accumulated profit made by the MFI. Retained earnings or reserves = the profit in the Incomes Statement.

All of these sources of funding should be recorded in and accessible from the MFI’s balance sheet. Balance Sheet The balance sheet shows an organisation’s assets, liabilitities and equity (owner capital) at a specific point in time. The relationship between these items must always be: Assets = Liabilities + Owner Equity

Assets

• Cash and deposits • Loans • Fixed Assets • Other assets

Liabilities • Customer deposits • Other borrowed funds • Other liabilities

Owner Equity • Shares • Reserves and Funds • Retained Earnings

When conducting financial planning, start with your current balance sheet. Then use your income, expense and portfolio projections to plan what your future balance sheet will look like. This will enable you to plan the right mix between debt, capital and assets. If for example, your projected balance sheet tells you that you need to raise more capital next year, then you need to make plans to achieve this.

3. Projected cash-flow statement Cash flow is critical to all businesses, especially businesses that specialise in managing cash! You should always have a cash flow projection for at least 1 year ahead. A cash flow statement = a financial statement that shows a company's incoming and outgoing money (sources and uses of cash) during a time period (often monthly or quarterly). Remember that cash in does not equal income, and cash out does not equal expenses. There are other sources of money coming in and out such as loans and savings. Here as examples of typical cash flows for an MFI:

28

Money in: income, deposits, repayments, other borrowings Money out: expenses, withdrawals, loan disbursements, repayment of borrowings

The cash flow statement is useful in determining the short and medium-term viability of a MFI, particularly its ability to pay bills.You should make sure you always have enough cash to pay for your near-term expenses and outgoings.

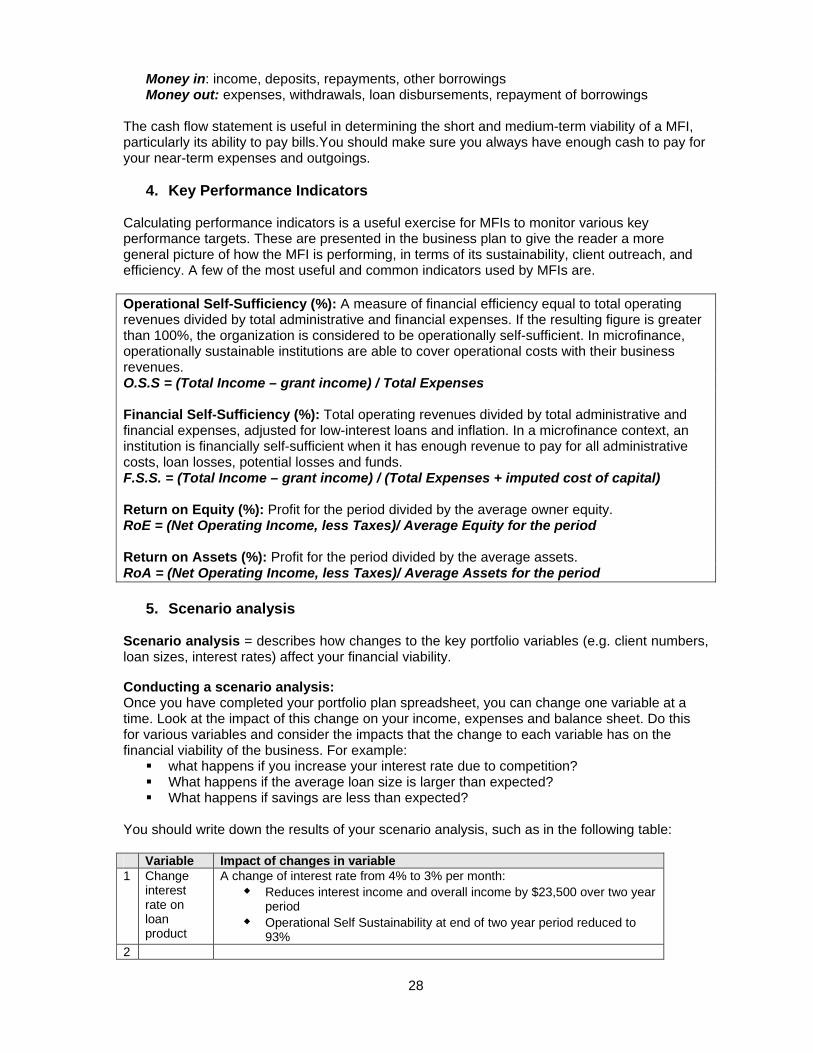

4. Key Performance Indicators Calculating performance indicators is a useful exercise for MFIs to monitor various key performance targets. These are presented in the business plan to give the reader a more general picture of how the MFI is performing, in terms of its sustainability, client outreach, and efficiency. A few of the most useful and common indicators used by MFIs are. Operational Self-Sufficiency (%): A measure of financial efficiency equal to total operating revenues divided by total administrative and financial expenses. If the resulting figure is greater than 100%, the organization is considered to be operationally self-sufficient. In microfinance, operationally sustainable institutions are able to cover operational costs with their business revenues. O.S.S = (Total Income – grant income) / Total Expenses Financial Self-Sufficiency (%): Total operating revenues divided by total administrative and financial expenses, adjusted for low-interest loans and inflation. In a microfinance context, an institution is financially self-sufficient when it has enough revenue to pay for all administrative costs, loan losses, potential losses and funds. F.S.S. = (Total Income – grant income) / (Total Expenses + imputed cost of capital) Return on Equity (%): Profit for the period divided by the average owner equity. RoE = (Net Operating Income, less Taxes)/ Average Equity for the period Return on Assets (%): Profit for the period divided by the average assets. RoA = (Net Operating Income, less Taxes)/ Average Assets for the period

5. Scenario analysis Scenario analysis = describes how changes to the key portfolio variables (e.g. client numbers, loan sizes, interest rates) affect your financial viability. Conducting a scenario analysis: Once you have completed your portfolio plan spreadsheet, you can change one variable at a time. Look at the impact of this change on your income, expenses and balance sheet. Do this for various variables and consider the impacts that the change to each variable has on the financial viability of the business. For example:

what happens if you increase your interest rate due to competition? What happens if the average loan size is larger than expected? What happens if savings are less than expected?

You should write down the results of your scenario analysis, such as in the following table: Variable Impact of changes in variable1 Change

interest rate on loan product

A change of interest rate from 4% to 3% per month: Reduces interest income and overall income by $23,500 over two year

period Operational Self Sustainability at end of two year period reduced to

93% 2

29

3

5. Key risks and assumptions

It is important to consider the financial risks that your organisation faces in the years to come. This may be based on your scenario analysis as well as your own consideration of risks facing the MFI.

Major Risks & Assumptions – Financial1 Loan delinquency 2 Fraud, corruption and misuse of funds (by clients or staff) 3 Higher than expected operating costs 4 Unreasonable rental demands from office owners 5 Poor management and investment of funds 6 7 8 9 10

Finally, consider your overall business operations and list any other major risks or assumptions that you are facing as an institution. Below are some examples:

Major Risks & Assumptions - Other1 Power supply problems 2 Theft, robbery and attacks 3 Assumes inflation rate of 3% 4 Portfolio at Risk (> 30 days) = 1%5 Staffing structure = 5 in total, 1 director, 1 finance manager, 3 loan officers 6 7 8 9 10

Congratulations! You now have the knowledge required to complete each of the key steps in preparing a business plan. Be sure to discuss your business plan with all stakeholders and make adjustments based on their feedback. Most importantly, take a step back and consider whether your business plan is realistic and achievable. Once you have agreed on your business plan, the next step is to make it reality! Be sure to refer back to your business plan regularly to track your progress on each of the items.