additional mathematics(napi)

DESCRIPTION

addmath dooTRANSCRIPT

ADDITIONAL MATHEMATICS

PROJECT WORK

2/2012

PRICE INDEX

NAME : MOHD HANAFI BIN SAIF

I/C NUM : 950320-13-5617

TEACHER : GOH PEI SHIEN

SCHOOL : KOLEJ D.P.A.H ABDILLAH

CONTENTS

NUMBER CONTENTS PAGE

1 ACKNOWLEDGEMENT

2 OBJECTIVE

3 INTRODUCTION

4 PART A

5 PART B

6 PART C

7 PART D

8 FURTHER

EXPLORATION

9 REFLECTION

ACKNOWLEDGEMENT

Alhamdulillah, thank you Allah for giving the will to do my additional mathematics project.

Secondly, I would like to thank the principal of Kolej Datu Patinggi Abang Haji Abdillah,

Puan Hajah Mastura binti Haji Anuar for giving the permission to do my Additional

Mathematics Work. I also like to thank my Additional Mathematics teacher, Mdm Goh Pei

Shien for the guide and giving useful and important information for me to complete this

project work. Besides that, I would like to thank my parents for their support and

encouragement. Last but not least, a special thank to Azfierol and Lexley for their help and

cooperation in searching information and completing this project work.

OBJECTIVE

The aims of carrying out this project work are:-

to apply and adapt a variety of problem-solving strategies to solve problems;

to improve thinking skills;

to promote effective mathematical communication;

to develop mathematical knowledge through problem solving in a way that increases

students interest and confidence;

to use the language of mathematics to express mathematical ideas precisely;

to provide learning environment that stimulates and enhances effective learning;

to develop positive attitude towards mathematic

INTRODUCTION

A bank is a financial institution and a financial intermediary that accepts deposits and

channels those deposits into lending activities, either directly or through capital markets. A

bank connects customers that have capital deficits to customers with capital surpluses.

Due to their critical status within the financial system and the economy generally, banks

are highly regulated in most countries. Most banks operate under a system known asfractional

reserve banking where they hold only a small reserve of the funds deposited and lend out the

rest for profit. They are generally subject to minimum capital requirements which are based

on an international set of capital standards, known as the Basel Accords.

The oldest bank still in existence is Monte dei Paschi di Siena, headquartered in Siena, Italy,

which has been operating continuously since 1472.

HISTORY

Banking in the modern sense of the word can be traced to medieval and

early Renaissance Italy, to the rich cities in the north like Florence, Venice and Genoa.

The Bardi and Peruzzi families dominated banking in 14th century Florence, establishing

branches in many other parts of Europe. Perhaps the most famous Italian bank was

the Medici bank, set up by Giovanni Medici in 1397. The earliest known state deposit

bank, Banco di San Giorgio (Bank of St. George), was founded in 1407 at Genoa, Italy.

ORIGIN OF THE WORD

The word bank was borrowed in Middle English from Middle French banque, from

Old Italian banca, fromOld High German banc, bank "bench, counter". Benches were used as

desks or exchange counters during the Renaissance by Florentine bankers, who used to make

their transactions atop desks covered by green tablecloths.

One of the oldest items found showing money-changing activity is a silver Greek drachm coin

from ancient Hellenic colony Trapezus on the Black Sea, modern Trabzon, c. 350–325 BC,

presented in theBritish Museum in London. The coin shows a banker's table (trapeza) laden

with coins, a pun on the name of the city. In fact, even today in Modern Greek the word

Trapeza (Τράπεζα) means both a table and a bank.

Another possible origin of the word is from the Sanskrit words (ब्यय) 'byaya' (expense) and

'onka' (calculation) = byaya-onka. This word still survives in Bangla, which is one of the

Sanskrit's child languages. ব্যা��য় + অঙ্ক = ব্যা��ঙ্ক . Such expense calculations were the biggest

part of mathmetical treaties written by Indian mathmeticians as early as 500 B.C.

FIXED DEPOSIT ACCOUNT

A Fixed Deposit (also known as FD) is a financial instrument provided by Indian banks

which provides investors with a higher rate of interest than a regular savings account, until the

given maturity date . It may or may not require the creation of a separate account. It is known

as a Term Deposit in the Canada, Australia, New Zealand and the US and as Bond in United

Kingdom. they are considered to be very safe investments. Term Deposits in India is used to

denote a larger class of investments with varying levels of liquidity. The defining criteria for a

Fixed Deposit is that the money cannot be withdrawn for the FD as against Recurring

Deposit or Demand deposit before maturity. Some banks may offer additional services to FD

holders such as loans against FD certificates at competent interest rates. Its important to note

that banks may offer lesser interest rates under uncertain economic conditions. The interest

rate varies between 4 and 11 percent. The tenure of an FD can vary from 10, 15 or 45 days to

1.5 years and can be as high as 10 years. These investments are safer than Post Office

Schemes as they are covered under Deposit Insurance & Credit Guarantee Scheme of India.

They also offer Income tax and Wealth tax benefits.

AUTO RENEWABLE

The automatic renewal of deposits will be done for the principal amount only in the case of

non-cumulative deposit schemes like STD, FD, Unit, Facility (Fixed deposit scheme) and for

maturity value for cumulative deposits like RIP , Cash Certificates and Facility (Reinvestment

Plan).

PART A

by Geometric Progression Solution

Tn = arn-1 r = Tn+1

T n a = 50 000

BANK A

Monthly auto renewable

r – 100+3.10

100 T13 – 50 000 x 1.031013-1

– 103.10

100 - 50 000 x 1.031012

– 1.0310 - 72 123.03397

- 72 123.00

Three months auto renewable

r – 100+3.15

100 T5 - 50 000 x 1.03155-1

– 103.15

100 - 50 000 x 1.30154

– 1.0315 - 56 603.9754

-56 603.00

Six months auto renewable

r – 100+3.20

100 T3 - 50 000 x 1.0323-1

– 103.2100

- 50 000 x 1.0322

– 1.032 - 53 251.20

Twelve months without withdrawal

r – 100+3.25

100 T2 – 50 000 x 1.03252-1

– 103.25

100 - 50 000 x 1.03251

– 1.0325 - 51 625.00

BANK B

Monthly auto renewable

r – 100+3.00

100 T13 – 50 000 x 1.030013-1

- 103100

- 50 000 x 1.030012

– 1.0300 - 71 288.04434

- 71 288.00

Three months auto renewable

r – 100+3.05

100 T5 – 50 000 x 1.03055-1

– 103.05

100 - 50 000 x 1.03054

- 1.0305 - 56 384.79279

- 56 384.80

Six months auto renewable

r – 100+3.10

100 T3 – 50 000 x 1.03103-1

r – 103.10

100 - 50 000 x 1.03102

r- 1.0310 - 53 148.05

-53 148.00

Twelve months auto renewable

r – 100+3.15

100 T2 – 50 000 x 1.03152-1

r – 103.15

100 - 50 000 x 1.03151

r – 1.0315 - 51 575.00

BANK C

Monthly auto renewable

r – 100+3.00

100 T13 – 50 000 x 1.030013-1

r – 103100

- 50 000 x 1.030012

r – 1.0300 - 71 288.04434

- 71 288.00

Three months auto renewable

r – 100+3.05

100 T5 – 50 000 x 1.03055-1

r – 103.05

100 - 50 000 x 1.03054

r – 1.0305 - 56 384.79279

- 56 384.80

Six months auto renewable

r – 100+3.10

100 T3 – 50 000 x 1.03103-1

r – 103.10

100 - 50 000 x 1.03102

r – 1.0310 - 53 148.05

- 53 148.00

Twelve months auto renewable

r – 100+3.20

100 T2 – 50 000 x 1.0322-1

r – 103.20

100 - 50 000 x 1.0321

r – 1.032 - 51 600.00

PERIOD BANK A BANK B BANK C

MONTHLY RENEWABLE 72 123.00 71 288.00 71 288.00

THREE MONTHS RENEWABLE 56 604.00 56 384.80 56 384.80

SIX MONTHS RENEWABLE 53 251.00 53 148.00 53 148.00

TWELVE MONTHS

RENEWABLE

51 625.00 51 575.00 51 575.00

Therefore, I will choose Bank A because the interest of Bank A is higher than Bank

B and Bank C.

PART B

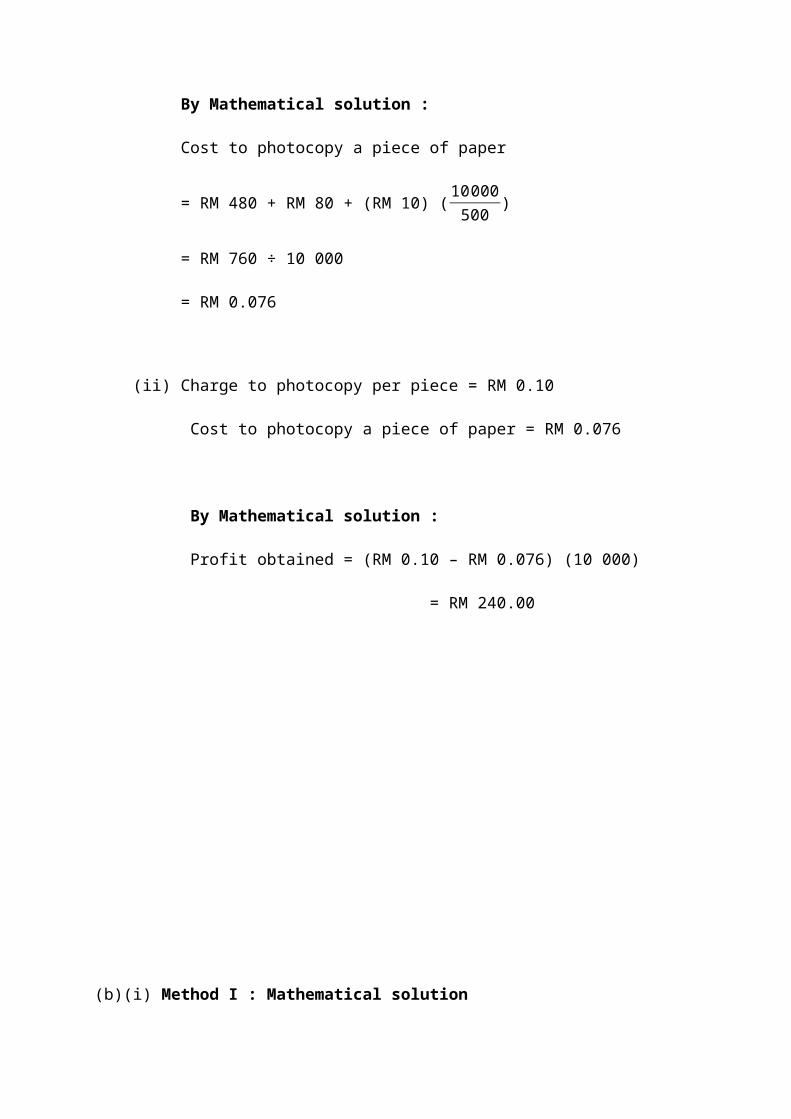

(a)(i) Rental for photocopy machine per month = RM 480.00

Cost for a rim of paper (500) = RM 10.00

Price of a bottle of toner (10 000 pieces of paper) = RM 80.00

By Mathematical solution :

Cost to photocopy a piece of paper

= RM 480 + RM 80 + (RM 10) (10 000

500)

= RM 760 ÷ 10 000

= RM 0.076

(ii) Charge to photocopy per piece = RM 0.10

Cost to photocopy a piece of paper = RM 0.076

By Mathematical solution :

Profit obtained = (RM 0.10 – RM 0.076) (10 000)

= RM 240.00

(b)(i) Method I : Mathematical solution

Cost to photocopy a piece of paper in year 2013

= RM 500+RM 100+RM 240

10 000

= RM 0.084

Percentage increase

= ( 0.084−0.076

0.076 ) × 100%

= 10.53%

Method II : Price Index solution

I = PP

× 100 , Ī = ∑ IW∑W

Price Index, I Weightage, W

Rental 6256

25

Toner 125 5

Paper 120 12

Ī = (625 ) (25 )+(125 ) (5 )+(120 ) (12 )

¿¿25+5+12

¿

= 25015

252

= 111.17

Therefore, percentage increase

= ( RM 0.076 × 111.17

100 ) - 0.076 × 100%

= 10.53%

(ii) Method by Quadratic Expression :

Pieces of paper should cooperative photocopy

0.1x – 10 000 (0.084) = 240

0.1x – 840 = 240

0.1x = 1080

x = 10800.1

x = 1080

(iii) Profit obtained = ( RM 0.10 ) ( 10 000) – ( RM 0.084 ) ( 10 000)

= RM 1 000 – RM 840

= RM 160

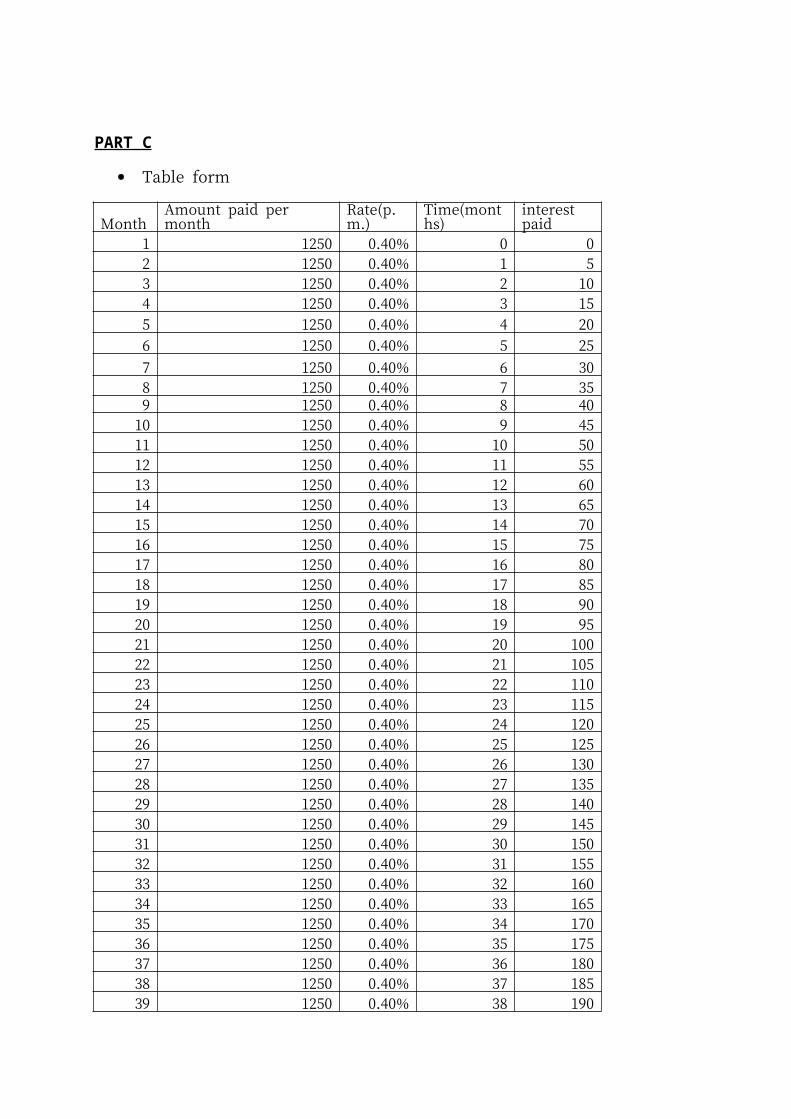

PART C

Table form

Month Amount paid per month Rate(p.m.) Time(months) interest paid1 1250 0.40% 0 02 1250 0.40% 1 53 1250 0.40% 2 104 1250 0.40% 3 15

5 1250 0.40% 4 20

6 1250 0.40% 5 25

7 1250 0.40% 6 308 1250 0.40% 7 359 1250 0.40% 8 40

10 1250 0.40% 9 4511 1250 0.40% 10 5012 1250 0.40% 11 5513 1250 0.40% 12 6014 1250 0.40% 13 6515 1250 0.40% 14 7016 1250 0.40% 15 7517 1250 0.40% 16 8018 1250 0.40% 17 8519 1250 0.40% 18 9020 1250 0.40% 19 9521 1250 0.40% 20 10022 1250 0.40% 21 10523 1250 0.40% 22 11024 1250 0.40% 23 115

25 1250 0.40% 24 12026 1250 0.40% 25 12527 1250 0.40% 26 13028 1250 0.40% 27 13529 1250 0.40% 28 14030 1250 0.40% 29 14531 1250 0.40% 30 15032 1250 0.40% 31 15533 1250 0.40% 32 16034 1250 0.40% 33 16535 1250 0.40% 34 17036 1250 0.40% 35 17537 1250 0.40% 36 18038 1250 0.40% 37 18539 1250 0.40% 38 19040 1250 0.40% 39 19541 1250 0.40% 40 20042 1250 0.40% 41 20543 1250 0.40% 42 21044 1250 0.40% 43 21545 1250 0.40% 44 22046 1250 0.40% 45 22547 1250 0.40% 46 23048 1250 0.40% 47 23549 1250 0.40% 48 24050 1250 0.40% 49 24551 1250 0.40% 50 25052 1250 0.40% 51 25553 1250 0.40% 52 26054 1250 0.40% 53 26555 1250 0.40% 54 27056 1250 0.40% 55 27557 1250 0.40% 56 28058 1250 0.40% 57 28559 1250 0.40% 58 29060 1250 0.40% 59 29561 1250 0.40% 60 30062 1250 0.40% 61 30563 1250 0.40% 62 31064 1250 0.40% 63 31565 1250 0.40% 64 32066 1250 0.40% 65 32567 1250 0.40% 66 33068 1250 0.40% 67 33569 1250 0.40% 68 34070 1250 0.40% 69 345

71 1250 0.40% 70 35072 1250 0.40% 71 35573 1250 0.40% 72 36074 1250 0.40% 73 36575 1250 0.40% 74 37076 1250 0.40% 75 37577 1250 0.40% 76 38078 1250 0.40% 77 38579 1250 0.40% 78 39080 1250 0.40% 79 39581 1250 0.40% 80 40082 1250 0.40% 81 40583 1250 0.40% 82 41084 1250 0.40% 83 41585 1250 0.40% 84 42086 1250 0.40% 85 42587 1250 0.40% 86 43088 1250 0.40% 87 43589 1250 0.40% 88 44090 1250 0.40% 89 44591 1250 0.40% 90 45092 1250 0.40% 91 45593 1250 0.40% 92 46094 1250 0.40% 93 46595 1250 0.40% 94 47096 1250 0.40% 95 47597 1250 0.40% 96 48098 1250 0.40% 97 48599 1250 0.40% 98 490

100 1250 0.40% 99 495101 1250 0.40% 100 500102 1250 0.40% 101 505103 1250 0.40% 102 510104 1250 0.40% 103 515105 1250 0.40% 104 520106 1250 0.40% 105 525107 1250 0.40% 106 530108 1250 0.40% 107 535109 1250 0.40% 108 540110 1250 0.40% 109 545111 1250 0.40% 110 550112 1250 0.40% 111 555113 1250 0.40% 112 560114 1250 0.40% 113 565115 1250 0.40% 114 570116 1250 0.40% 115 575

117 1250 0.40% 116 580118 1250 0.40% 117 585119 1250 0.40% 118 590120 1250 0.40% 119 595

Total Interest paid 35700

Money is still left after the loan has been paid out for the period of ten years.Hence, keeping the RM 150 000 in a fixed deposit account then borrow the RM 150 000 from a bank is a better way to expand the store-room.

PART D

Compound interest means interest that accrues on the initial principal and the accumulated interest of a principal deposit, loan or debt.Compounding of interest allows a principal amount to grow at a faster rate than simple interest, which is calculated as a percentage of only the principal amount.

Simple Interest means a quick method of calculating the interest charge on a loan. Simple interest is determined by multiplying the interest rate by the principal by the number of periods.

Where: P is the loan amountI is the interest rate N is the duration of the loan, using number of periods

. Simple Interest

Years Principal Rateinterest earned

1 50000 5% 25002 50000 5% 50003 50000 5% 75004 50000 5% 100005 50000 5% 125006 50000 5% 150007 50000 5% 175008 50000 5% 200009 50000 5% 22500

10 50000 5% 2500011 50000 5% 27500

12 50000 5% 3000013 50000 5% 3250014 50000 5% 3500015 50000 5% 3750016 50000 5% 4000017 50000 5% 4250018 50000 5% 4500019 50000 5% 4750020 50000 5% 5000021 50000 5% 5250022 50000 5% 5500023 50000 5% 5750024 50000 5% 6000025 50000 5% 6250026 50000 5% 6500027 50000 5% 6750028 50000 5% 7000029 50000 5% 7250030 50000 5% 75000

Compound InterestYears Principal Rate Amount interest

1 50000 3.50% 51750 1,750

2 50000 3.50%53561.2

5 3,561

3 50000 3.50%55435.8

9 5,436

4 50000 3.50%57376.1

5 7,376

5 50000 3.50%59384.3

2 9,384

6 50000 3.50%61462.7

7 11,463

7 50000 3.50%63613.9

6 13,614

8 50000 3.50%65840.4

5 15,840

9 50000 3.50%68144.8

7 18,145

10 50000 3.50%70529.9

4 20,530

11 50000 3.50%72998.4

9 22,998

12 50000 3.50%75553.4

3 25,553

13 50000 3.50% 78197.8 28,198

14 50000 3.50%80934.7

3 30,935

15 50000 3.50%83767.4

4 33,767

16 50000 3.50% 86699.3 36,699

17 50000 3.50%89733.7

8 39,734

18 50000 3.50%92874.4

6 42,874

19 50000 3.50%96125.0

7 46,125

20 50000 3.50%99489.4

4 49,489

21 50000 3.50%102971.

6 52,972

22 50000 3.50%106575.

6 56,576

23 50000 3.50%110305.

7 60,306

24 50000 3.50%114166.

4 64,166

25 50000 3.50%118162.

2 68,162

26 50000 3.50%122297.

9 72,298

27 50000 3.50%126578.

4 76,578

28 50000 3.50%131008.

6 81,009

29 50000 3.50%135593.

9 85,594

30 50000 3.50%140339.

7 90,340

Therefore, it is better to save in the compound interest plan account for long-term savings and simple interest for short-term savings.

FURTHER EXPLORATION

a = 500

r = 8.0100

n = ?

Tn > 5 000 arn-1 > 5 000

( 8−0100

+ 1)n-1 > 5 000

5 000 × (1.08)n-1 > 5 000 log10 (1.08)n-1 > log10 10 (n-1) log10 1.08 > log10 10

n-1 > log 1010

log 101.08 n-1 > 29.92 n > 30.92 n > 31

REFLECTION

I have done many researches throughout the internet and discussing with a friend who have helped me a lot in

completing this project. Through the completion of this project, I have learned many skills and

techniques. This project really helps me to understand more about the uses of index number in our

daily life.This project also helped expose the techniques of application of additional mathematics in real life

situations.

While conducting this project, a lot of information that I found. I have learnt how to calculate interest

rates per annum by using index number. Besides, I also had learn some moral values that I’d practiced. This

project had taught me be more responsible to complete the work given by teachers.

Apart from that, this project encourages the student to work together and share their knowledge. It is

also encourage student to gather information from the internet, improve thinking skills and promote effective

mathematical communication. I also enjoy doing this project during holiday. My friends and I do it together to

discuss the solution of the question and it had tighten our friendship.