administrative regulations and rulings chapter 4

Post on 21-Dec-2015

224 views

TRANSCRIPT

Administrative Regulations and RulingsChapter 4

What do We Need to Know About “Authorities”

What they areTheir sourceWhere to find themHow to use them

What We Must Determine• Their

reliability

Administrative Regs and Rulings (Second Primary Source)

• Treasury and IRS PronouncementsRegulations

Revenue Rulings

Revenue Procedures

Letter Rulings

Regulations

Are the IRS’s / Treasury’s official interpretation of the IRC

§7805(a) “Except where such authority is expressly given by this title to any person other than an officer or employee of the Treasury department, the Secretary shall prescribe all needful rules and regulations for the enforcement of this title, including all rules and regulations as may be necessary by reason of any alteration of law in relation to internal revenue.”

Regulations

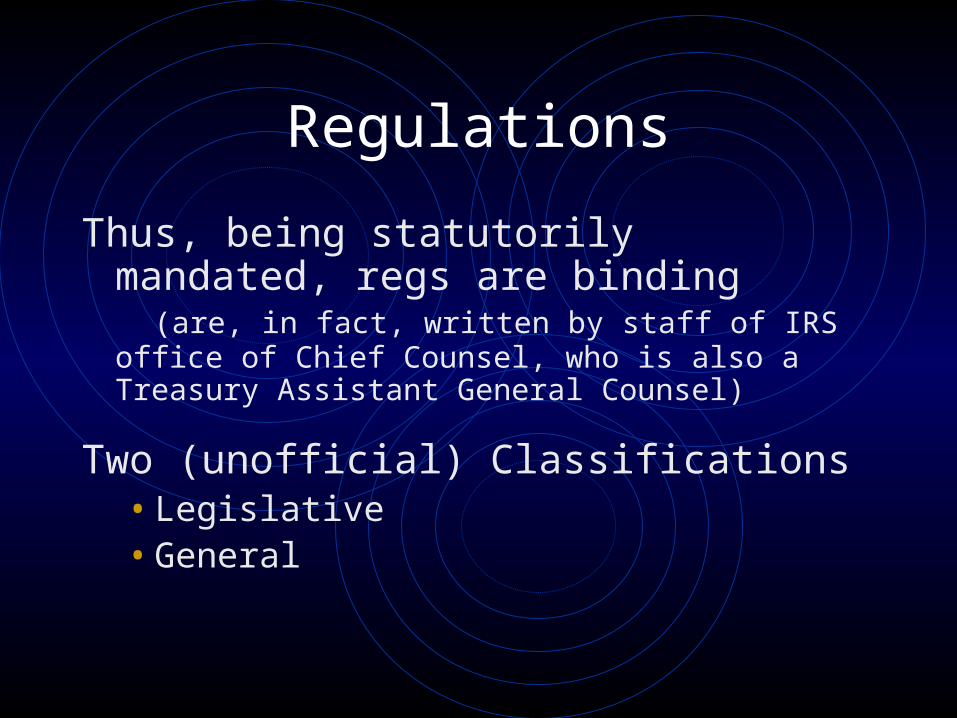

Thus, being statutorily mandated, regs are binding

(are, in fact, written by staff of IRS office of Chief Counsel, who is also a Treasury Assistant General Counsel)

Two (unofficial) Classifications • Legislative• General

Regulations Legislative

Written by Treasury at direction of Congress, essentially carrying out a law making function (Congress does not want to address the detail and complexities of the issue), and

• Have the effect of law.• Have the greatest precedential value of

any Treasury pronouncement.

Legislative Regulations (cont’d) Examples

• §135 – exclusion if interest on certain U.S. Savings Bonds

• “(4) Regulations

• The Secretary may prescribe such regulations as may be necessary or appropriate to carry out this section, including regulations requiring record keeping and information reporting.”

Legislative Regulations (cont’d) Examples

• §385 – distinguished debt from equity in “thinly capitalized” corporations.

• “(a) Authority to prescribe regulations -

• The Secretary is authorized to prescribe such regulations as may be necessary or appropriate to determine whether an interest in a corporation is to be treated for purposes of this title as stock or indebtedness (or as in part stock and in part indebtedness).”

Regulations General

• All other• Supreme Court views as having the force

and effect of law, unless they conflict with the statute [Maryland Casualty Co., 251 US 342 (1920)]

• Although binding, they are subject to challenge, but challenger bears the burden of proof

Regulations General (cont’d)

Authorized by §7805(a)• “(a) Authorization • Except where such authority is expressly given by

this title to any person other than an officer or employee of the Treasury Department, the Secretary shall prescribe all needful rules and regulations for the enforcement of this title, including all rules and regulations as may be necessary by reason of any alteration of law in relation to internal revenue.”

Regulations General (cont’d)

Are Treasury’s Official interpretation of the Statute

Are issued first as Proposed regs (w/o yet having the effect of law)

When finally issued, are issued as a Treasury Decision (TD)

Note: Distinguish from Temporary Regs, discussed later

Proposed Regulations

Regulations are first issued in proposed formatAre published in the Federal Register, and in the IRB.Public has 30-days to commentTreasury may then hold hearings for public testimony (depends on comments received)Then, Treasury may change, issue as proposed again, or issue as a Treasury Decision

Proposed Regulations (cont’d)

Do not have effect of law, but are important in thatthey give a clue to IRS’ position, andwhat could be the final published position and

guidance

Treasury Decision

Regulations, when issued in final form after public circulation and comment, hearings held if deemed necessary, and revised based on public comment and hearings, are issued as a Treasury Decision.

Temporary Regulations

(Distinguish from Proposed Regulations)Responsive to new law – for immediate guidance to

taxpayersEffective immediately upon publication – not

subject public comment or hearingsFully in effect and must be followed until

superceded (IRS issues in proposed format simultaneously)

Expires 3 years after issuance (§7805) (However, superceding regulations not always ready).

Regulations

• Effective Date -• “Retroactivity of regulations. -- • (1) In general. -- • Except as otherwise provided in this subsection,

no temporary, proposed, or final regulation relating to the internal revenue laws shall apply to any taxable period ending before the earliest of the following dates:

• (A) The date on which such regulation is filed with the Federal Register.(cont’d)

Regulations

• Effective Date – (cont’d)• (B) In the case of any final regulation, the

date on which any proposed or temporary regulation to which such final regulation relates was filed with the Federal Register.

• (C) The date on which any notice substantially describing the expected contents of any temporary, proposed, or final regulation is issued to the public.”

Regulations (cont’d)

• Reg. §1.482-1(b)(4)• 1 = Income tax

(20= Estate, 25 = Gift, 31 = Employment, 301 = Procedural matters, etc.)

• 482-1 = Regulation number corresponds to IRC §)

• (b) = Paragraph

• (4) = Subparagraph

Revenue Rulings

• Second most important administrative source.

• Official position of the IRS (no hearings)• Favorable to TP – IRS is bound to follow, at all levels• If unfavorable, all divisions of IRS are bound, except

Appeals Division not bound.

• Deals with a specific fact situation.• Public need for guidance with a specific fact situation.• But the need for public hearings and formal regs are not

justified.

Revenue Rulings (cont’d)

• Distinguish from Regulations• No public hearings or requests for comment• Limited to specific fact situation

• Effective Date - It may state. Generally, being interpretative, is retroactive.• If contradictory to previous position, and• unfavorable to taxpayers, will be prospective.

• Are reliable and may be cited as authority.

Revenue Rulings (cont’d)

• Format• Issue

• Facts

• Law and Analysis

• Holding

Revenue Rulings (cont’d)

• Cite:• (Temp) Rev. Rul. 02-34, 2002-62 I.R.B. 58

• 02 = year

• 34= consecutive number of the ruling (published that year)

• 2002 = year (again)

• 62 = consecutive number of IRB’s volume

• I.R.B. = Internal Revenue Bulletin

• 58 = page number

Revenue Rulings (cont’d)

• (Perm) Rev. Rul. 02-34, 2002-1 C.B. 373

• 02 = year

• 34 = consecutive number of ruling published that

year

• 2002-1 = year/volume of C.B.

• C.B. = Cumulative Bulletin

• 373 = page number

Revenue Procedure

• Guidance regarding procedures. How to…. such as:• Request a Private Letter Ruling

• Request approval to change accounting method

• Etc.

• Cite – same as Revenue Ruling, except is a Procedure.

Letter Rulings

• Prepared in Several Formats• Private Letter Rulings

• Determination Letters

• Technical Advice Memorandums

Letter Rulings (cont’d)

• Are not published by the IRS• Are available through FOIA

• In sanitized format to protect the identity of the requester

• Most tax services have them and publish most of them

• Again, all are sanitized

• Reliability very limited except to requester - §6110• But provides good insight into IRS position

Private Letter Ruling (PLR)

• Is a great opportunity for TPs contemplating a significant transaction – especially if it may controversial tax-wise

• Is requested by a specific TP contemplating a proposed transaction, with a specific fact situation, and wanting the assurance of the tax results before entering into the transaction.

• TPs and practitioners may request as a “comfort ruling,” where they know the answer, but want confirmation.

PLR (cont’d)

• If the IRS foresees a response unfavorable to the requester, they may• Offer an opportunity for a conference to

discuss, either by telephone or a personal conference in Washington, D.C.

• Make suggestions to revise the transaction that would bring more favorable results.

(PLR’s are issued by the IRS’ National Office)

PLR (cont’d)

• Very reliable to the requester only.• But, for research purposes, provides good

insight into IRSs position

• May not be relied upon by the requester if the facts presented were inaccurate/incomplete, or

• If the actual facts or transaction differs from those presented.

PLR (Cont’d)

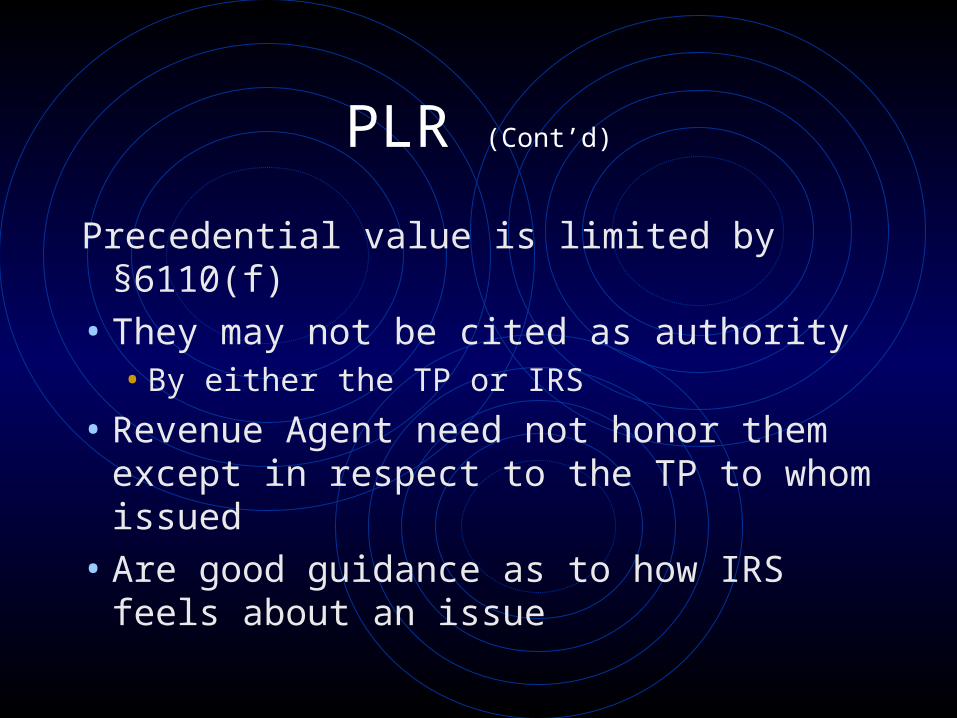

Precedential value is limited by §6110(f)

• They may not be cited as authority• By either the TP or IRS

• Revenue Agent need not honor them except in respect to the TP to whom issued

• Are good guidance as to how IRS feels about an issue

PLR (cont’d)

• Significantly, is among the “substantial authorities” listed in Reg. §1.6662-4(d)(3)(iii) – the TP may rely on it to avoid some penalties

PLR (cont’d)

If IRS receives repeated requests regarding particular or similar transactions, they may issue a Revenue Ruling

Determination Letter

Generally:

• Issued locally (formerly District Director)

• Deals with issues/transactions not exceptionally complex or controversial

• After the fact, completed transactions

• Usually pension plan qualification, exempt organization.

Determination Letters (cont’d)

• Are not published. May be available through FOIA.

Technical Advice Memorandum (TAM)

• Issued by the NO upon request of an Internal Revenue Agent or the TP during an administrative proceeding.

• After the fact, completed (closed) transaction.

• Facts must be established.• TP may request a conference if a proposed

response is unfavorable.

PLRs and TAMs

• If the NO receives requests for guidance in the nature of PLRs or TAMs with respect to any particular type of transaction indicating the need for guidance to the public, they may issue a Revenue Ruling.

Acquiescence

• The Commissioner of Internal Revenue may issue an “Acquiescence” or “Non-Acquiescence” to a decision of the Tax Court, meaning that the IRS agrees or disagrees with the TC’s decision.

• Are published (as a list in IRB / CB’s, and are included in the case cite by some publishers

Acquiescence (cont’d)

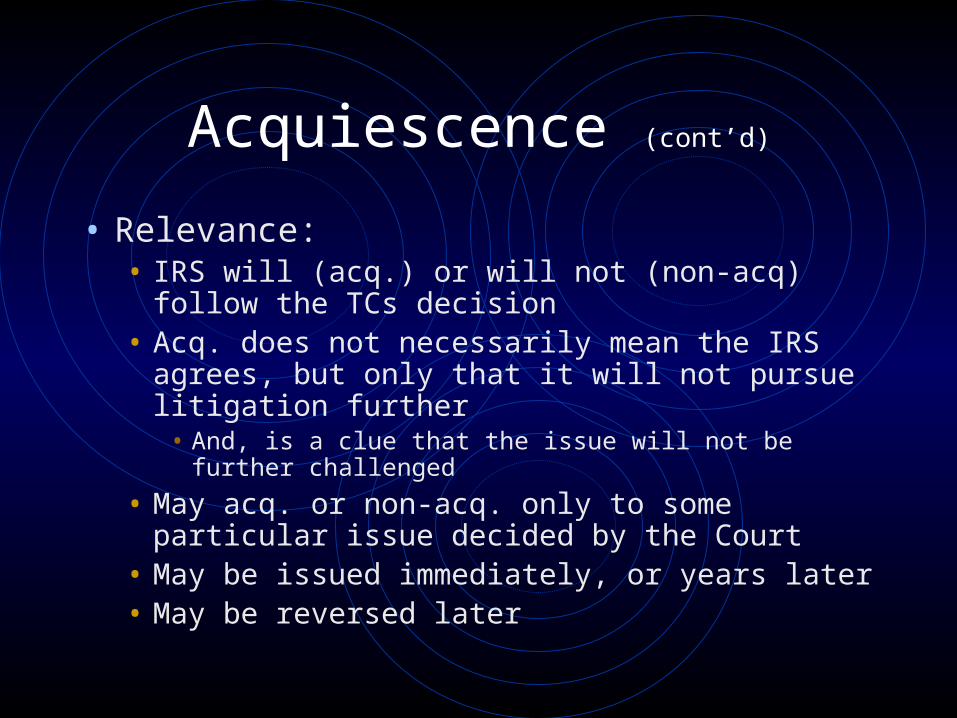

• Relevance:• IRS will (acq.) or will not (non-acq) follow the TCs

decision• Acq. does not necessarily mean the IRS agrees, but

only that it will not pursue litigation further• And, is a clue that the issue will not be further challenged

• May acq. or non-acq. only to some particular issue decided by the Court

• May be issued immediately, or years later• May be reversed later

Acquiescence (cont’d)

• Are NOT driven, as the text states, by litigation costs.

Action on Decision

• Is an analysis of a decision in a case decided unfavorable to the IRS, somewhat similar to a Court Case Brief, generally written by the Area Counsel trial attorney. It’s purpose is to recommend action regarding unfavorable result, e.g., appeal, acquiesce, await a better case for litigation, or simply no further action. Relevance ??

Internal Revenue Bulletins Cumulative Bulletins

• Internal Revenue Bulletin – a periodic publication in which IRS publishes its pronouncements, and other documents:

New Public Laws Committee Reports

Revenue Rulings Revenue Procedures

Treasury Decisions New Treaties

• Etc.

Internal Revenue Bulletins Cumulative Bulletins (cont’d)

• Internal Revenue Bulletins are accumulated into a Cumulative Bulletin, generally twice a year, but may be more or less depending upon the volume of pronouncements issued

Questions?