adrri journal of arts and social...

TRANSCRIPT

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

1

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6,No.6(1), September, 2014

The Effects of Activity-Based Lending on SMES in Ghana: A Case Study of Stanbic Bank

Ghana Limited, Tamale Branch.

Alhassan Baba Andani1 and Abdul-Mumuni Yussif2

1Lecturer, Department of Languages and Liberal Studies, Tamale Polytechnic

E-mail:[email protected] Tel: (233) 0202301331/0247716454

2Stanbic Bank Ghana Limited. Email: [email protected] Tel: 0541256095

1Correspondence: [email protected]

Received: 31st August, 2014 Revised: 24th September, 2014 Published Online: 30th September, 2014

URL: http://www.journals.adrri.org/

[Cite as: Alhassan, B. A. and Abdul-Mumuni, Y. (2014). The Effects of Activity-Based Lending on SMES in Ghana:

A Case Study of Stanbic Bank Ghana Limited, Tamale Branch. ADRRI Journal of Arts and Social Sciences, Ghana:

Vol. 6, No. 6(1), Pp. 1-11, ISSN: 2343-6891, 30th September, 2014.]

Abstract

The study sought to evaluate the effects of activity-based lending on SMEs in Ghana, with the Tamale

branch of Stanbic Bank Ghana as case study. The sources of materials for the study were both primary

and secondary. Primary data was collected by the use of a structured questionnaire designed and

administered to Top Management and business owners of SMEs and Staff of Stanbic Bank Ghana

Limited, Tamale Branch. The study found that there were different types of funding the bank offers to

SMEs for activity-based projects. It was revealed that despite high interest rates, SMEs continue to borrow

from the banks. Regarding factors affecting SMEs access to lending in Ghana, improper record keeping

affects SMEs, lack of entrepreneurial skills affects owners of SME businesses as well as interest rate

effects. On the issue of moral hazards, the result shows that Stanbic Bank experiences moral hazards

when the bank is unable to discern on borrowers. Based on the findings, it is recommended that more

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

2

working capital could be provided to SMEs to enable the sector to have relatively higher working capital

credit facilities to be able to operate effectively. It is suggested that entrepreneurial skills and training on

proper book keeping be given to SMEs to enhance their development and growth. It also recommended

that proper action plan should be developed for loans collection so as to reduce legal actions taken

against SMEs.

Keywords: activity-based lending small and medium sized enterprises (SMEs), economic liberalization

INTRODUCTION

Small and Medium sized Enterprises (SMEs) constitute a large source of industrial employment

in Ghana. It is assumed that the poorer income sections of Ghana benefit when Small and

Medium sized Enterprises (SMEs) have better access to finances because they help in alleviating

poverty by creating more jobs and wages to the employed (Emeni and Okafor 2008).The actual

performance of SMEs, however, varies depending on: the comparative economic efficiency, the

macro-economic policy atmosphere and the specific elevation policies pursued for their benefit.

In Ghana, SMEs contribute about 85% of manufacturing employment and account for about

92% of businesses (Steel and Webster, 1991). Given the seminal role of SMEs to the economy of

Ghana, various regimes of government since independence, have focused on various

programmes and spent immense amount of money with the primary goal of evolving this

segment of the economy, theses have not brought any substantial results as evident in the

present state of the SMEs in the country (Abor, 2005).

Also, the process of economic liberalization and market reforms as a result of international

trade agreements has opened up the Ghanaian economy to international struggle. SMEs are

now facing stiff competition from multinational companies after the liberalization of the

Ghanaian economy in the early part of 1980s. They have to revitalize their marketing and

promotional strategies and galvanize support from government, NGOs and other investors to

endure. In order to expand the mutual level of entrepreneurship and competitiveness of local

SMEs, Ghana need to increase access to capital and newer technologies. However, according to

Mensah (2004) the most important factor constraining the growth of SMEs is the lack of finance

and that SMEs and formal financial institutions in Ghana have had a history of mutual caution

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

3

in dealing with one another. This is due to high non-payment degrees on the part of SMEs and

stringent and restrictive conditions for acquiring loans on the part of banks.

The World Bank’s Doing Business Report has thus ranked Ghana at a dismal 115 out of 178

economies in ease of access to credit (World Bank/ IFC, 2008). The causes according to Dinye

(1991) can be traced to the doorsteps of both the firms and the financial institutions.

At the firm’s level, lack of experience in dealing with financial institutions, lack of credit history,

low levels of management involvement, failure to prepare corporate strategies and difficulty in

meeting collateral requirements are the underlying reasons that explain why entrepreneurs are

unable to access credit from the banks. At the bank level, the high managerial cost of transacting

business with the micro and small scale industries entrepreneurs and the high risk associated

with loans contracted out to them account for the inability of the banks to advance credit to

micro and small scale industries as expected.

The non-financial problems relate to the empowering atmosphere within which they operate

and accessibility of set-up. With respect to situation where interest rates are high, heavy tax

burden, lack of access to market information and lack of inter-industry linkages between

agriculture and industry are some of the factors militating against their operations. These create

a financing gap for SMEs to operate effectively. The present condition equally is deteriorating

by the global credit crunch which affected the ability of financial institutions, government and

donor agencies to provide the needed credit facilities to SMEs. A very large segment of the

rural and business community still has little or no access to financial services.

The SMEs lending market currently uses a corporate lending approach as financial institutions

have difficulties in servicing the wide-reaching SME sector. The government has instituted a

number of interventions to improve access to SME credit, such as Ghana Investment Fund

(GIF), the Export Development and Investment Fund (EDIF), Micro Finance and Small Loans

Centre, the Venture Capital Trust Fund (VCTF) and the National Board for Small Scale

Industries (NBSSI) Credit schemes. These policies aimed at making credit facilities easily

accessible to SMEs.

Section 13 of the Loans Act of 1970 (Act 335) empowers the Government of Ghana (GoG) to

provide government guarantee to any external financiers who wish to advance funds to any

Ghanaian organisation and the terms of such facility require the provision of guarantee from

the government. Guarantee facilities are contingent liabilities of the Government. The onus for

repaying the facility lies with the borrower and not the Government.

Although Government in exercise of the relevant provision in the loans Act, has provide

guarantee to a number of bilateral and multilateral organisations in the past on behalf of

selected Ghanaian organisations in both the Private and Public sectors of the economy, no

targeted SME guarantee facilities has been introduced.

Activity-based lending is where credit is given to a customer of bank based on particular

activity the business wants to undertake or use the money for. It begins with cost structure of

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

4

the action the business intends to undertake. This lending type was established from activity-

based costing technique which was developed to measure the cost of production or action more

accurately in multi-product production system. In this research, the researcher used activity-

based lending since that gives more detailed statement on the cost of operations in which the

credits are given.

In view of that, this study is conducted to assess the effects of activity-based lending on Small

and Medium Sized Enterprises in Ghana, concentrating on SMEs who receive loads from

Tamale branch of Stanbic Bank Ghana Limited and sought to achieve the following objectives.

1. To identify the various types of activity-based lending to SMEs in Ghana

2. To examine the effects of lending policy on SMEs in Ghana

3. To assess the factors that affect SMEs access to lending in Ghana

4. To examine the decision-making process of lending to SMEs

This research is designed to provide answers to the following research questions:

1. What are the various types of activity-based lending to SMEs in Ghana?

2. What are effects of lending policy on SMEs in Ghana?

3. What are factors that affect SMEs access to lending in Ghana?

4. What is the decision-making process of lending to SMEs?

This study would be useful to identify innovative options and institutional arrangements that

would serve as an input for policy makers, politicians, government agencies and bankers in

formulating activity-based lending policy to SMEs. In the light of the unavailability of literature

to similar study in the developing countries of which Ghana is one, findings of this study would

contribute to the literature availability in the country. In addition, the findings of the study

would increase the understanding of the bank lending decisions on activity-based lending to

SMEs. The research focuses on the effects of activity-based lending on Small and Medium sized

Enterprises in Ghana, considering Stanbic bank branch of Tamale. The study covers SMEs in

Tamale Metropolitan narrowing to those receiving activity-based lending from Tamale branch

of Stanbic bank. The study is restricted to the effects of activity-based lending on SMEs in

Tamale Metropolis in the Northern Region of Ghana.

LITERATURE REVIEW

Abor and Quartey (2010) indicated that the issue of what constitutes a small or medium

enterprise is a major concern in the literature. Different authors have usually given different

definitions to this group of corporate. Small and Medium sized Enterprises (SMEs) have

certainly not been secured with the explanation of problem that is usually associated with

concepts which have many mechanisms. The definition of firms by size varies among

researchers. Some attempt to use the capital assets while others use skill of labour and turnover

level. Others have defined SMEs in terms of their legal status and method of production. Storey

(1994) tries to sum up the danger of using size to define the status of a firm by stating that in

some sectors all firms may be regarded as small, whilst in other sectors there are possibly no

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

5

firms which are small. The Bolton Committee (1971) first formulated an ‚economic‛ and

‚statistical‛ definition of a small firm. Under the ‚economic‛ definition, a firm is said to be

small if it meets the following three criteria: it has a relatively small share of their market place;

it is managed by owners and not through the medium of a formalized management structure;

and it is independent, in the sense of not forming part of a large enterprise.

Under the ‚statistical‛ definition, the Committee suggested the following criteria the size of the

small firm sector and its impact on the a country’s GDP, contribution to job creation and export

business; the extent to which the small firm sector’s economic contribution has changed over

time; and applying the statistical definition in a cross-country comparison of the small firms’

economic contribution.

The European Commission (EC) defined SMEs basically in term of the number of employees are

firms with 0 to 9 employees - micro enterprises; 10 to 99 employees - small enterprises; and 100

to 499 employees - medium enterprises. Thus, the SME sector is comprised of enterprises

(except agriculture, hunting, forestry and fishing) which employ less than 500 workers. In effect,

the EC definitions are based solely on employment rather than a multiplicity of criteria.

Secondly, the use of 100 employees as the small firm’s upper limit is more appropriate, given

the increase in productivity over the last two decades (Storey, 1994). Finally, the EC definition

did not assume the SME group is similar; that is, the definition makes a distinction between

micro, small, and medium-sized enterprises.

The UNIDO also defines SMEs in terms of number of employees by giving different

classifications for industrialized and developing countries (Elaian, 1996). The definition for

industrialized countries is given as follows: Large - firms with 500 or more workers; Medium

firms with 100-499 workers; and Small - firms with 99 or less workers. The classification given

for developing countries is as follows: Large - firms with 100 or more workers; Medium -

firms with 20-99 workers; Small - firms with 5-19 workers; and Micro - firms with less than 5

workers. It is perfect from the several definitions that there is not all-purpose consensus over

what creates an SME. Definitions vary across industries and also across countries. It is

significant now to examine definitions of SMEs given in the context of Ghana.

Kayanula and Quarter (2000) specified that there have been many definitions given to small-

scale enterprises in Ghana but the most commonly used criterion is the number of employees of

the enterprise. In applying this definition, confusion often arises in respect of the arbitrariness

and cut off points used by the various authorised foundations. In its Industrial Statistics, the

Ghana Statistical Service (GSS) considers firms with fewer than 10 employees as small-scale

enterprises and their counterparts with more than 10 employees as medium and large-sized

enterprises. Kayanula and Quarter (2000) again stated that, unluckily the GSS in its national

accounts measured companies with up to 9 employees as SMEs. The value of fixed assets in the

firm has also been used as an alternative criterion for defining SMEs. However, the National

Board for Small Scale Industries (NBSSI) in Ghana applies both the ‚fixed asset and number of

employees‛ criteria. It defines a small-scale enterprise as a firm with not more than 9 workers,

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

6

and has plant and machinery (excluding land, buildings and vehicles) not exceeding10 million

Ghanaian cedis. The Ghana Enterprise Development Commission (GEDC), on the other hand,

uses a 10 million Ghanaian cedis upper limit definition for plant and machinery. It is important

to caution that the process of valuing fixed assets poses a problem. Secondly, the continuous

depreciation of the local currency as against major trading currencies often makes such

definitions outdated (Kayanula and Quartey, 2000).

In Ghana, Steel and Webster (1991) and Osei et al (1993) used an employment cut-off point of

30 employees in the definition of small-scale enterprises in Ghana. Nevertheless, Osei et al

(1993), classified small-scale enterprises into three categories, namely: micro - employing less

than 6 people; very small - employing 6-9 people; and small - between 10 and 29 employees.

A more recent definition is the one given by the Regional Project on Enterprise Development

Ghana manufacturing survey paper classified firms into: micro enterprise, less than 5

employees; small enterprise, 5 - 29 employees; medium enterprise, 30 – 99 employees; large

enterprise, 100 and more employees (Teal, 2002).

SMEs are very significant to the economic success for most countries and their citizens and in

recent time have been observed to employ an increasing proportion of the work force of most

countries. There is a fast growth in the number of privately owned small and medium-sized

companies worldwide; however, this category of business is plagued by several issues that

deter this growth. A key challenge for most SMEs is the problem financing, according to Da

Silva .et al (2007). All small firms live under tight liquidity constraints, therefore making finance

a major problem for them.

According to Ogujiuba et al (2004) generating an entrepreneurial idea is one thing but accessing

the necessary finance to translate such ideas into reality is another. Many novel entrepreneurial

ideas have been known to die simply because their originators could not fund them, and banks

could not be convinced that they were worth inverting in. Finance, whether owned or

borrowed, is needed to expand so as to maximize profit and given the nature of SMES, there is a

need for financing. SMEs generally have four key funding requirements: i. initial infrastructure

investments, ii. Lump operations costs, iii, next-step expansion, and iv. unexpected

opportunities requiring quick access to funds. Despite what the funding requirement maybe,

SMES often prioritize the source of financing from internal (cash flow or entrepreneur’s own

capital) to external, according to relative availability and (opportunity) cost (Ogujiuba, Ohuche

and Adenuga 2004). This is because for most firms, the internal funds are always insufficient to

undertake the required level of transactions for profitable projects hence the cell for external

finance to fill the finance gap.

Theoretically, a number of analytical paradigms have attempted to explain the complexities and

practicalities involved in small-firm financing. As early as the Mac Millan Report in 1931, there

has been recognition that British small firms suffer from what is termed the, finance gap‛. In a

first -world setting like that in the UK, this situation arises when is termed the grown to a size

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

7

where the use of short-term finance is maximized, but the firm is not big enough to access

capital-market funds. By contrast, in developing countries it is probable that such a finance gap

arises at even earlier stages of the enterprise’s lifecycle (South African reserve bank in a report

conducted by the Task Group of the Policy Board for Financial Service and Regulation 2004)

The problem of bank financing to SMEs has been persistent for many years in the country with

both parties actively responsible for the lack of SMES financing: SMES because of their shortfalls

in meeting the classic requirements of the banking sector and banks because they could

mobilize more resource in order to penetrate the SMES segment, basically both parties share the

blames of the problem as both the other.

Traditionally dominated the financial systems, leaving little leeway for SMEs seeking

alternatives financial to bank loans; hence a close look at behaviour from the bank and to

reveals a number reason explaining the behaviour from the bank. For the purpose of this thesis,

will these be categorized under three broad heading;

i. A poor macroeconomics environment

ii. Lack of basic infrastructure facilities

iii. Internal structuring problems of SMEs

The most common form of bank financing used by small businesses is the overdraft. It is a

facility where a bank allows the customer to overdraw his or her account up to an amount

agreed upon. The customer draws down only parts of the line of credit as the need arises, so

that redundant borrowings are unnecessary. This facility is normally given to finance the

working capital requirements of a business, such as holding of stocks, extension of credit to

buyers, and for operating expenses. Interest is charged on the amount overdrawn, and for the

period of its use. The advance may be repaid as inflows of cash to the business occur. Cressy

(1992) cites a number of reasons for the use of overdraft as a major form of bank financing.

First, it is flexible and overcomes the need to extend a series of separate short-term loans.

Second, it allows the customer some insurance against subsequent deteriorating in his or her

credit rating. Finally, it can help in overcoming the moral hazard commonly associated with

lending under asymmetric information.

Financing of small businesses can also be made available through term loans. These are

generally medium to long-term loan facilities used largely for the purchase of major assets or

for permanent increases in working capital. The maturity can be as long as 10 years, and thus

these loans can expose the banks to potential default risks over a long period. Typically, these

loans are amortised by periodic instalment payments. These payments can be on a monthly,

quarterly, half-yearly or yearly basis, depending on the purpose for which the loans are given,

the repayment ability of the business borrowers, and the total repayment period of the

loans. This form of financing is, however, generally provided by the commercial banks against

landed property.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

8

METHODOLOGY

The researchers employed both quantitative and qualitative data in assessing the effects of

activity-based lending on Small and Medium sized Enterprises in Ghana, with a particular

interest in the role that Stanbic Bank Ghana Limited plays in the growth of SMEs in the country.

The population of the study included Small and Medium sized Enterprises and top

management of Stanbic bank Tamale branch.

The purposive sampling method was employed in sampling the respondents to identify the

effects of activity-based lending on SMEs in Ghana. Simple random method was also employed

in sampling the Stanbic bank staff, each is chosen randomly and entirely by chance, such that

each individual has the same probability of being chosen. One hundred (97) respondents were

used for the study, including SMEs and some staff of Stanbic bank in Tamale.

Table1 Distribution of Respondents

Respondents Sampled Respondents

Small and Medium sized Enterprises 76

STANBIC Bank Officials 21

Total 97

Source: Field survey June, 2013

Since the objective of this study is to get general picture of the effects of activity-based lending

on Small and Medium sized Enterprises in Ghana and using Stanbic Bank Ghana Limited

Tamale branch as a case study, both quantitative and qualitative research approaches were

suitable and were selected in that direction.

The data for this study were gathered through the use of primary and secondary sources.

The Researchers also used a combination of structured questionnaires and interviews. In order

to collect reliable and valid information, the researchers contacted SMEs and employees of

Tamale branch of Stanbic Bank. Primary data were collected using questionnaires.

The study also made use of secondary sources of information. This included books, internet

search, articles, and journals among others. This helped to identify how others have defined and

measured key concepts, the data sources that others used and this helped to discover how the

research project is related to the work of others.

A descriptive statistics was found to be an ideal analysis technique for this study and

subsequently used in ascertaining the effects of activity-based lending on SMEs in Ghana with

reference to Tamale branch of Stanbic bank Ghana Ltd.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

9

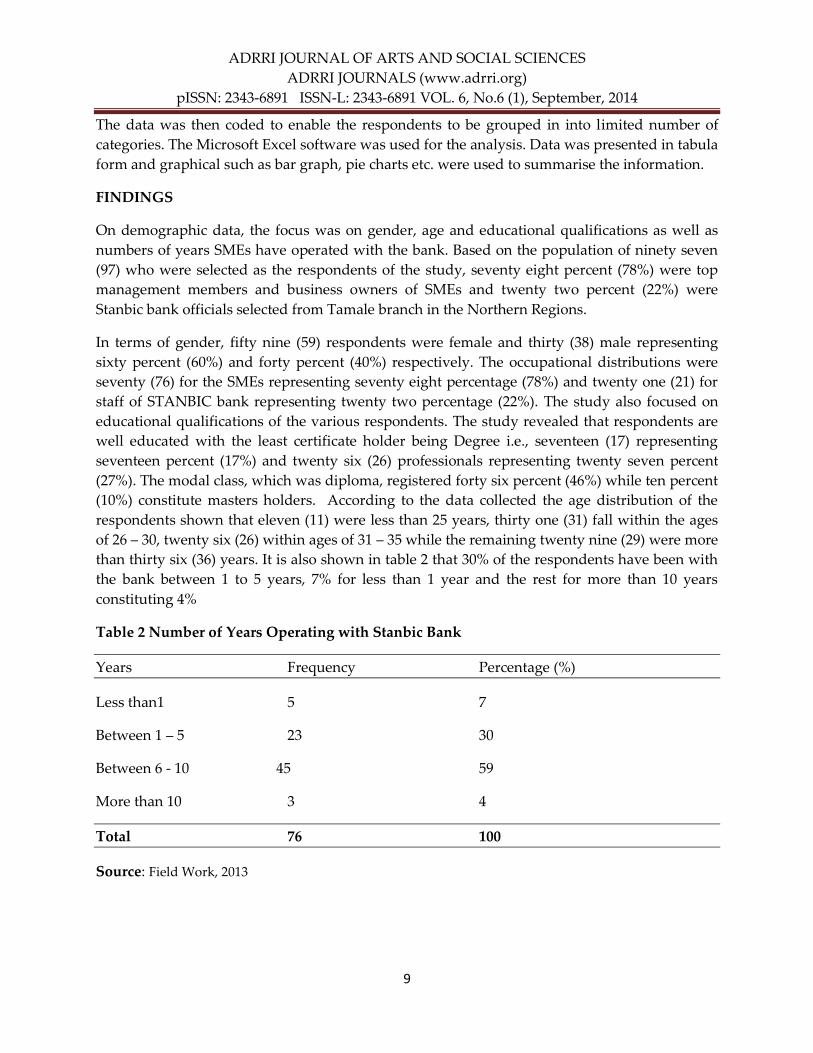

The data was then coded to enable the respondents to be grouped in into limited number of

categories. The Microsoft Excel software was used for the analysis. Data was presented in tabula

form and graphical such as bar graph, pie charts etc. were used to summarise the information.

FINDINGS

On demographic data, the focus was on gender, age and educational qualifications as well as

numbers of years SMEs have operated with the bank. Based on the population of ninety seven

(97) who were selected as the respondents of the study, seventy eight percent (78%) were top

management members and business owners of SMEs and twenty two percent (22%) were

Stanbic bank officials selected from Tamale branch in the Northern Regions.

In terms of gender, fifty nine (59) respondents were female and thirty (38) male representing

sixty percent (60%) and forty percent (40%) respectively. The occupational distributions were

seventy (76) for the SMEs representing seventy eight percentage (78%) and twenty one (21) for

staff of STANBIC bank representing twenty two percentage (22%). The study also focused on

educational qualifications of the various respondents. The study revealed that respondents are

well educated with the least certificate holder being Degree i.e., seventeen (17) representing

seventeen percent (17%) and twenty six (26) professionals representing twenty seven percent

(27%). The modal class, which was diploma, registered forty six percent (46%) while ten percent

(10%) constitute masters holders. According to the data collected the age distribution of the

respondents shown that eleven (11) were less than 25 years, thirty one (31) fall within the ages

of 26 – 30, twenty six (26) within ages of 31 – 35 while the remaining twenty nine (29) were more

than thirty six (36) years. It is also shown in table 2 that 30% of the respondents have been with

the bank between 1 to 5 years, 7% for less than 1 year and the rest for more than 10 years

constituting 4%

Table 2 Number of Years Operating with Stanbic Bank

Years Frequency Percentage (%)

Less than1 5 7

Between 1 – 5 23 30

Between 6 - 10 45 59

More than 10 3 4

Total 76 100

Source: Field Work, 2013

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

10

The types of finance to Small and Medium Sized Enterprises

The study revealed that Stanbic bank gives loan to the agriculture sector. This was confirmed by

majority (62) of the respondents agreeing to the statement. The study also discovered that

Stanbic bank provides fixed term loans to SMEs in the area under study. It was realised seventy

eight percent (78%) of the respondents strongly agree to the statement Stanbic bank offers fixed

term loan to SMEs, twenty percent (20%) also agree while only two percent of (2%) of the

respondents were uncertain to the statement. It was further obtained from the results that

Stanbic bank grants revolving term loan to the SMEs in the area under investigation. Based on

the findings, it was indicated that almost all the respondents in aggregate disconfirmed the

statement that home loan is one of the largest investments Stanbic bank offer to SMEs. Table 3

indicates that ninety seven percent (97%) out of the seventy six (76) respondents agree to the

statement that the bank provides vehicle and asset finance facility to finance the purchase of

moveable assets while three percent (3%) of the respondents were not sure with the statement.

These findings approve the statement as posted at the website of the bank.

Table 3: The bank provides vehicle and asset finance facility to finance the purchase of

moveable assets

Years Frequency Percentage (%)

Strongly Agree 0 0

Agree 74 97

Uncertain 2 3

Disagree 0 0

Strongly Disagree 0 0

Total 76 100

Source: Field work, 2013

The effects of funds on Small and Medium Sized Enterprises

It was found from the study that the bank was not being restrained from giving loans to SMEs.

The study revealed that majority of the respondents disagrees to the statement. It was revealed

that eighty percent (80%) representing sixty one (61) of the respondents were uncertain to the

statement , five (5) each for strongly agree and agree, three (3) for disagree while two (2) for

strongly disagree representing seven percent (7%) each for strongly agree and agree, four

percent (4%) and three percent (2%) for agree and strongly disagree respectively. It was further

noticed that majority of the responses shown that they were not sure whether they (borrowers)

find it tough paying back loans. It was revealed that interest rate does not scare SMEs from

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

11

borrowing from the bank. The study further indicates that Stanbic bank loans have positive

impact on the businesses of SMEs in the study area.

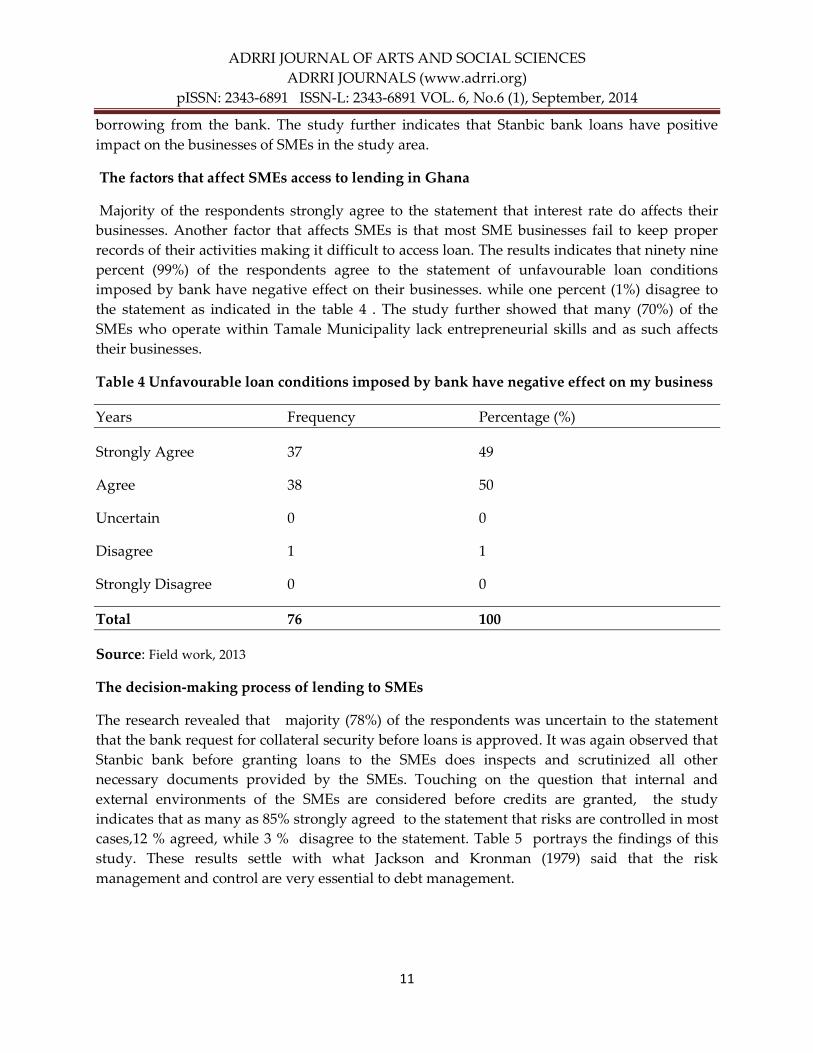

The factors that affect SMEs access to lending in Ghana

Majority of the respondents strongly agree to the statement that interest rate do affects their

businesses. Another factor that affects SMEs is that most SME businesses fail to keep proper

records of their activities making it difficult to access loan. The results indicates that ninety nine

percent (99%) of the respondents agree to the statement of unfavourable loan conditions

imposed by bank have negative effect on their businesses. while one percent (1%) disagree to

the statement as indicated in the table 4 . The study further showed that many (70%) of the

SMEs who operate within Tamale Municipality lack entrepreneurial skills and as such affects

their businesses.

Table 4 Unfavourable loan conditions imposed by bank have negative effect on my business

Years Frequency Percentage (%)

Strongly Agree 37 49

Agree 38 50

Uncertain 0 0

Disagree 1 1

Strongly Disagree 0 0

Total 76 100

Source: Field work, 2013

The decision-making process of lending to SMEs

The research revealed that majority (78%) of the respondents was uncertain to the statement

that the bank request for collateral security before loans is approved. It was again observed that

Stanbic bank before granting loans to the SMEs does inspects and scrutinized all other

necessary documents provided by the SMEs. Touching on the question that internal and

external environments of the SMEs are considered before credits are granted, the study

indicates that as many as 85% strongly agreed to the statement that risks are controlled in most

cases,12 % agreed, while 3 % disagree to the statement. Table 5 portrays the findings of this

study. These results settle with what Jackson and Kronman (1979) said that the risk

management and control are very essential to debt management.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

12

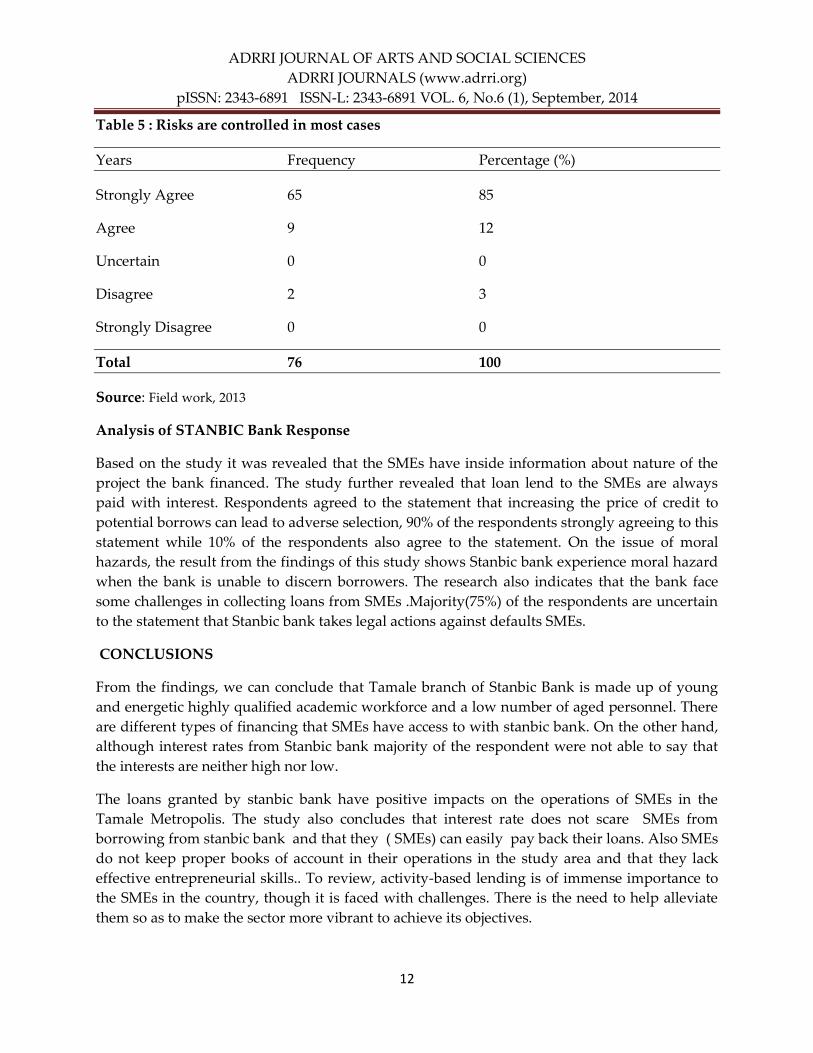

Table 5 : Risks are controlled in most cases

Years Frequency Percentage (%)

Strongly Agree 65 85

Agree 9 12

Uncertain 0 0

Disagree 2 3

Strongly Disagree 0 0

Total 76 100

Source: Field work, 2013

Analysis of STANBIC Bank Response

Based on the study it was revealed that the SMEs have inside information about nature of the

project the bank financed. The study further revealed that loan lend to the SMEs are always

paid with interest. Respondents agreed to the statement that increasing the price of credit to

potential borrows can lead to adverse selection, 90% of the respondents strongly agreeing to this

statement while 10% of the respondents also agree to the statement. On the issue of moral

hazards, the result from the findings of this study shows Stanbic bank experience moral hazard

when the bank is unable to discern borrowers. The research also indicates that the bank face

some challenges in collecting loans from SMEs .Majority(75%) of the respondents are uncertain

to the statement that Stanbic bank takes legal actions against defaults SMEs.

CONCLUSIONS

From the findings, we can conclude that Tamale branch of Stanbic Bank is made up of young

and energetic highly qualified academic workforce and a low number of aged personnel. There

are different types of financing that SMEs have access to with stanbic bank. On the other hand,

although interest rates from Stanbic bank majority of the respondent were not able to say that

the interests are neither high nor low.

The loans granted by stanbic bank have positive impacts on the operations of SMEs in the

Tamale Metropolis. The study also concludes that interest rate does not scare SMEs from

borrowing from stanbic bank and that they ( SMEs) can easily pay back their loans. Also SMEs

do not keep proper books of account in their operations in the study area and that they lack

effective entrepreneurial skills.. To review, activity-based lending is of immense importance to

the SMEs in the country, though it is faced with challenges. There is the need to help alleviate

them so as to make the sector more vibrant to achieve its objectives.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

13

RECOMMENDATIONS

In view of the findings of the research, it was realized that bank lending forms an integral part

of SMEs growth and development of the country; its running and operation leave much to be

desired. Based on the findings the following recommendations are made:

The types of finance to Small and Medium Sized Enterprises

Based on the finding, it was realized that there were different types of finance to SMEs that have

positive impact on their operation. However, the results disapproved that home loan is one of

the largest investments the bank offer to SMEs. In view of that, it is recommended that bank

should maintain that as credit for home will make it difficult for the SMEs to repay back such

loans. This is because loans given to SMEs are to be used to work in order to gain profit so as to

enable them repay. It rather suggested that more working capital could be provided to SMEs to

enable them have the needed relatively higher working capital requirement to operate

effectively. It is hoped that would give the SMEs skills to development and growth.

The effects of funds on Small and Medium Sized Enterprises

Based on the study, it was found that the bank was not being restrained from giving loans to

SMEs. It was further noticed that majority of the responses shown that they were not sure

whether they (borrowers) find it tough paying back loans. It was revealed that interest rate does

not scare SMEs from borrowing from the bank. The research also shows that loans are

insufficient to operate with and the result of the study further indicates that loans SMEs receive

from Stanbic bank have positive impact on their businesses. Based on the findings, it is

therefore recommended that bank should provide sufficient loans to SMEs to be able to operate

effectively. It is commended that where particular SME is found not to be credit worthy some

kind of restrains should be imposed on the SME. Suggestion is again give that interest rate

should not scare the SMEs from obtaining loans from the bank.

The factors that affect SMEs access to lending in Ghana

From the work it was revealed that interest rates were high. The findings again indicate that

duration for repayment of loan is short. The study also revealed that unfavourable loan

conditions imposed by bank have negative effect on SMEs. It was further revealed SME

businesses fail to keep proper records of their activities making it difficult to access loan for

their operations. From the study, it was again observed that Stanbic bank loans have positive

impact on SMEs. Based on the observations stated above from the findings, it is commended

that the bank should review its interest rate policy on activity-based lending to SMEs to enable

SMEs to have some kind of comfort in paying the loan with interest. It is also recommended

that conditions imposed on SMEs should be favourable. Suggestion is given that bank should

train and develop the SMEs on how to keep proper books of accounts as this would make them

take track of expenses as well other activities regarding their operations.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

14

The decision-making process of lending to SMEs

The research revealed that majority (78%) of the respondents was uncertain to the statement

that the bank request for collateral security before loans is approved. It was again observed that

Stanbic bank before granting loans to the SMEs does inspects and scrutinized all other

necessary documents provided by the SMEs. Touching on the question that internal and

external environments of the SMEs are considered before credits are granted, the study

indicates that as many as 85% strongly agreed to the statement that risks are controlled in most

cases,12 % agreed, while 3 % disagree to the statement Based on the findings, it therefore

suggested that bank make sure to scrutinize the document of the SMEs to make sure they are

truly registered businesses and that the document also bears the names of those registered them

using to contract loans. It is further commended that collateral security requirement should be

encouraged so that in case of default they can make up for it.

Analysis of STANBIC Bank Response

Based on the study, the following observations were noticed; that the SMEs have inside

information about nature of the project the bank financed and that loan lend to the SMEs are

always paid with interest and it also noted that increasing the price of credit to all potential

borrows can lead to adverse selection. On the issue of moral hazards, the result from the

findings of this study shows Stanbic bank experience moral hazard when the bank is unable to

discern borrowers. The research also identified that the bank face challenges in collecting loans

from SMEs and that majority were uncertain to the statement that Stanbic bank takes legal

actions against defaults SMEs.

Based on these findings, it is therefore recommended that stanbic bank should develop a

strategy that will ensures that such challenges the bank face in collecting loans back will be

reduced. It again suggested that in order minimise the problem of moral hazards, the bank

should be able to determine a credit worthy customer before loans are approved. It also

recommended that proper action plan should be developed for loans collection so as to reduce

legal actions taken against SMEs.

Recommendation for further research

The research has brought to fore the effects of activity-based lending on SMEs in Ghana. To

enhance this development, extensive research should be conducted to determine a model on

how such effects could be well managed to ensure that bank loans sustain the SMEs in the

Tamale Metropolis and Ghana as a whole.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

15

REFERENCE

Abor, J. (2005). The effect of capital structure on profitability: an empirical analysis of listed

firms in Ghana. 6(5), 438-445.

Abor, J. and N. Biekpe, (2006), ‚Small Business Financing Initiatives in Ghana‛, Problems and

Perspectives in Management, 4(3), pp. 69-77.

Alexander Keith (1992). Facilities Risk Management, Facilities, Vol. 10 No. 4, pp. 14-18, MCB

University Press, 0263-2772.

Allayannis, G. and Weston, J.P. (1999), ‘The use of Foreign Currency Derivatives and Firm

Market Value’, Working Paper, University of Virginia.

Ang, J.J. and McConnel, J. (1982), ‘The Administrative Cost of Corporate Bankruptcy: A Note’,

Journal of Finance, Vol. 37, pp. 219-26.

Avery, R. B., Bostic, R. W. & Samolyk, K. A. (1998) The Role of Personal Wealth in Small

Business Finance, Journal of Banking and Finance, 22,1019-1061.

Bank for International Settlement, (2001), ‘Overview of The New Basel Capital Accord’,

http://www.bis.org/publ/bcbsca02.pdf

Badu, Y.A., Daniels, K., Kenneth, N., and Amagoh, F., (2002), ‚An empirical analysis of net

interest cost, the probability of default and credit risk premium: a case study using the

com-monwealth of Virginia‛, Managerial finance; Vol. 28 No. 4.

Berlin, M. & Mester, L. J. (1998) On the Profitability and Cost of Relationship Lending,

Journal of Banking and Finance, 22,873-897.

Blackwell, D. & Winters, D. B. (1998) Banking Relationships and the Effect of Monitoring on

Loan Pricing, Journal of Financial Research, 20,275-289.

Bolton Report (1971) Report of the Committee of Enquiry on Small Firms, Cmnd. 4811,

London: HMSO.

Byrne, J., (2000), ‚Bringing banking risk up to date‛; Balance Sheet, Vol. 8, No. 6.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

16

Carlstrom, C.T. and Samolyk, K.A. (1995), ‘Loan Sales a Response to Market-Based Capital

Constraints’, Journal of Banking and Finance, 19, 627-646.

Cassell, C. & Symon, G. (1994) (eds) Qualitative Methods in Organizational Research,

London: Sage.

Cebenoyan, A.S. and Strahan, P.E. (2001), ‘Risk Management, Capital Structure and Lending

at Banks’, The Working Paper Series, Financial Institutions Centre, University of

Pennsylvania.

CGC (1973) Annual Report, Kuala Lumpur: Credit Guarantee Corporation.

Dahiya, S., Puri, M. and Saunders, A. (2000), ‘Bank Borrowers and Loan Sales: New Evidence

on the Uniqueness of Bank Loans’, Working Papers, NYU.

Demsetz, R.S. and Strahan, P.E. (1997), ‘Diversification, Size and Risk at Bank Holding

Companies’, Journal of Money, Credit and Banking, 29, 300-313.

De Vaus, D. (2002). Surveys in Social Research (5th ed.). London: Routledge

Eccles, R., Herz, R., Keegan, M., Phillips, D. (2001), ‚The risk of risk‛; Balance sheet; Vol. 9,

No.3.

Emeni, F.K. and Okafor, C. (2008), ‚Effects of bank mergers and acquisitions on small business

lending in Nigeria‛, African Journal of Business Management2 ( 9): 146-156.

Gorton, G.B. and Haubrich, J.G. (1990), ‘The Loan Sales Market’ Research in Financial

Services, 2, 85-135.

Guimon, J. (2005), ‘Intellectual capital reporting and credit risk analysis, Journal of

Intellectual Capital, Vol. 6, No.1.

Hinson R. (2004), ‘The Importance of Service Quality in Ghana’s banking Sector’, the

Marketing Challenge, Vol. 7, Issue 3, pp. 16-18.

Houston, J. James, C. and Marcus, D. (1996), ‘Capital Market Frictions and the Role of Internal

Capital Markets in Banking’, Journal of Monetary Economics, 35, 389-411.

Jayaratne, J. and Morgan, D.P. (1999), ‘Capital Market Frictions and Deposit Constraints on

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

17

Bank’, Journal of Money, Credit Banking.

Jensen, M., and W. Mecklin (1976) ‚Theory of the Firm: Managerial Behaviour, Agency Costs,

Ownership Structure‛ Journal of Financial Economics, 3, 305-60.

Kayanula, D., and Quartey, P., (2000). ‚The Policy Environment for Promoting Small,

Medium Enterprises in Ghana and Malawi,‛ Finance and Economic Research

Programme Working Paper Series 15. Institute of Development Policy Management

(IDPM), University of Manchester.

Mainelli, M. (2002), ‘Industrial strengths; operational risk and banks’, Balance Sheet; Vol. 10,

No. 3.

Mensah, S. (2004), A review of SME financing schemes in Ghana. UNIDO Regional Workshop

of Financing SMEs, 15-16 March, Accra.

Mintton, B.A and Schrand, C. (1999), ‘the Impact of Cash Flow Volatility on Discretionary

Investment and the Cost of Debt and Equity Financing’, Journal of Financial

Economics, 54, 423-460.

Myers, S. C. (1977), Determinants of corporate borrowing: 1. 5(2), 147-175.

OECD (2008), Measuring the impacts of ICT using official statistics, OECD, Paris

OECD (2004), ICT, E-BUSINESS AND SME, Paris

Warner, J. (1977), ‘Bankruptcy Costs: Some Evidence’, Journal of Finance, Vol. 32, pp. 337-47.

Smith, C. & Warner, J. (1979) On Financial Contracting: An Analysis of Bond Covenants,

Journal of Financial Economics, 7,117-162.

Storey, D. J. (1994) New Firms Growth and Bank Financing, Small Business Economics, 6,139-

150.

Yin, R.K (1994), Case Study Research: Design and Methods, applied Social Research

Methods Series, 2nd Ed. Sage Publishing, Newbury parl California.

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

18

APPENDIX

Population and sample of selected categories of respondents

The sample size for each of the category or group was determined with DeVaus (2002) formula

below:

21 aN

Nn

Where n = sample size, N= population universe and ‘a’ is the confidence level. The formula

adopted a confidence level of 90% and the margin of error is therefore 10% which is acceptable

in social science research. The break down for each of the group is calculated as follows:

Small and medium sized Enterprises:

N=312

21.03121

312n

12.31

312n

12.4

312n 76n

STANBIC Bank Officials:

26N

21

26.1

26

261

26

1.0261

262

nnnn

ADRRI JOURNAL OF ARTS AND SOCIAL SCIENCES

ADRRI JOURNALS (www.adrri.org)

pISSN: 2343-6891 ISSN-L: 2343-6891 VOL. 6, No.6 (1), September, 2014

19

This academic research paper was published by the Africa Development and Resources

Research Institute’s Journal of Arts and Social Sciences. ADRRI JOURNALS are double blinded,

peer reviewed, open access and international journals that aim to inspire Africa development

through quality applied research.

For more information about ADRRI JOURNALS homepage, follow: http://journal.adrri.org/aj

CALL FOR PAPERS

ADRRI JOURNALS call on all prospective authors to submit their research papers for

publication. Research papers are accepted all yearly round. You can download the submission

guide on the following page: http://journal.adrri.org/aj/

ADRRI JOURNALS reviewers are working round the clock to get your research paper

published on time and therefore, you are guaranteed of prompt response. All published papers

are available online to all readers world over without any financial or any form of barriers and

readers are advice to acknowledge ADRRI JOURNALS. All authors can apply for one printed

version of the volume on which their manuscript(s) appeared.