advanced certificate program on international financial ... · oriental bank of commerce, hindustan...

TRANSCRIPT

Advanced Certificate Program on

International Financial Reporting

Standards

(IFRS) – Implementation and Compliance

KPMG IN INDIA

Ver 1.1

2© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Content

About the program

Program Modules

Know your Program Director

About KPMG IFRS practice

Synchronous Learning - NIIT Imperia

Other Details

This program is jointly provided by KPMG in India and NIIT Imperia

Recent Developments

3© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

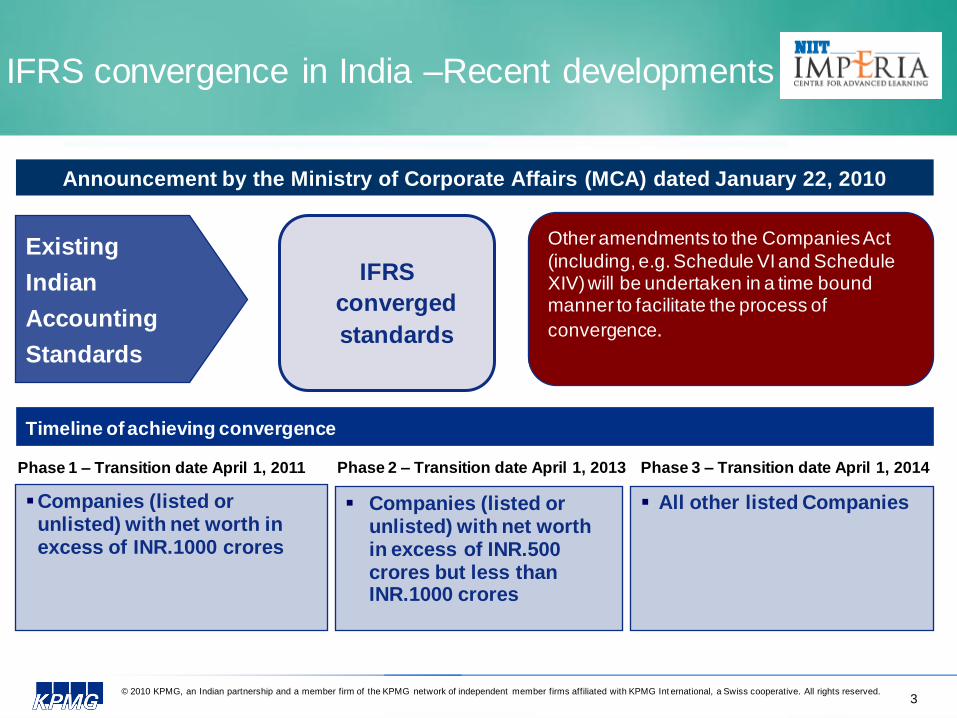

IFRS convergence in India –Recent developments

Announcement by the Ministry of Corporate Affairs (MCA) dated January 22, 2010

Other amendments to the Companies Act

(including, e.g. Schedule VI and Schedule XIV) will be undertaken in a time bound manner to facilitate the process of

convergence.

Timeline of achieving convergence

Phase 1 – Transition date April 1, 2011

Companies (listed or unlisted) with net worth in excess of INR.1000 crores

Phase 2 – Transition date April 1, 2013

Companies (listed or unlisted) with net worth in excess of INR.500 crores but less than INR.1000 crores

Phase 3 – Transition date April 1, 2014

All other listed Companies

Existing

Indian

Accounting

Standards

IFRS

converged

standards

© 2009 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

About the

program

4

5© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

About the program

Professional from KPMG in India with significant IFRS conversion

experience

Trainers of International Repute

Focused toward challenges to be faced by each stakeholder in

IFRS conversion

Practical inputs on carrying out a conversion exercise

Mix of Experience Sharing Real Life Case Discussion

Use of Illustrative Financial Statements Industry Disclosure

Requirements, etc.

Certification of completion on successful assessment clearance from

KPMG in India and NIIT Imperia

Faculty

Program Design

Pedagogy

Certification

In the first nine batches, organizations like Wipro Technologies, ICICI Prudential Life Insurance, Capgemini,

Oriental bank of Commerce, Hindustan Motors, NHPC, Reliance Power, Tata Motors, Bank of Maharashtra, Yahoo, etc. have nominated their employees for the program

6© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

About the program

Program Director: Sandip Khetan

Listen to Sandip Khetan talking about the program

Duration – Batch 10 : 11 weeks

Duration – Batch 11 : 6 weeks

Eligibility: Graduate min 2yrs. Work experience are eligible to join the

program [Experience requirement are waived off for CA, CS, CWA’s, MBA

(Finance) and corporate nomination]

Tentative Class Schedule:

Batch 10 – Sat 5.30PM – 9.30 PM Oct 9, 23, 30 Nov 13, 20, 27 Dec 4, 11, 18

Jan 8, Sun 1.30PM – 5.30PM Jan 9,16

Batch 11 – Wed 9.00 AM – 5.30PM Oct 6, 13, 20, 27 Nov 3, 10

Fees:

Batch 10 - Program Fee – Rs. 47,100/- + 10.3% Service Tax – Rs. 51,951/-

Batch 11 - Program Fee – Rs. 38,500/- + 10.3% Service Tax – Rs. 42,466/-

7© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Who should attend?

This program should be of value to you if you are:

CFO & Finance Director

Analysts, Accountant

Investment Banker

Corporate Banker

Strategic Planner

Auditor

Private Equity & Merger & Acquisition specialist

Tax Director

Consultant

Practicing CA, CS, CWA, and professionals from Indian companies

with a global presence

© 2009 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Program

Modules

8

9© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

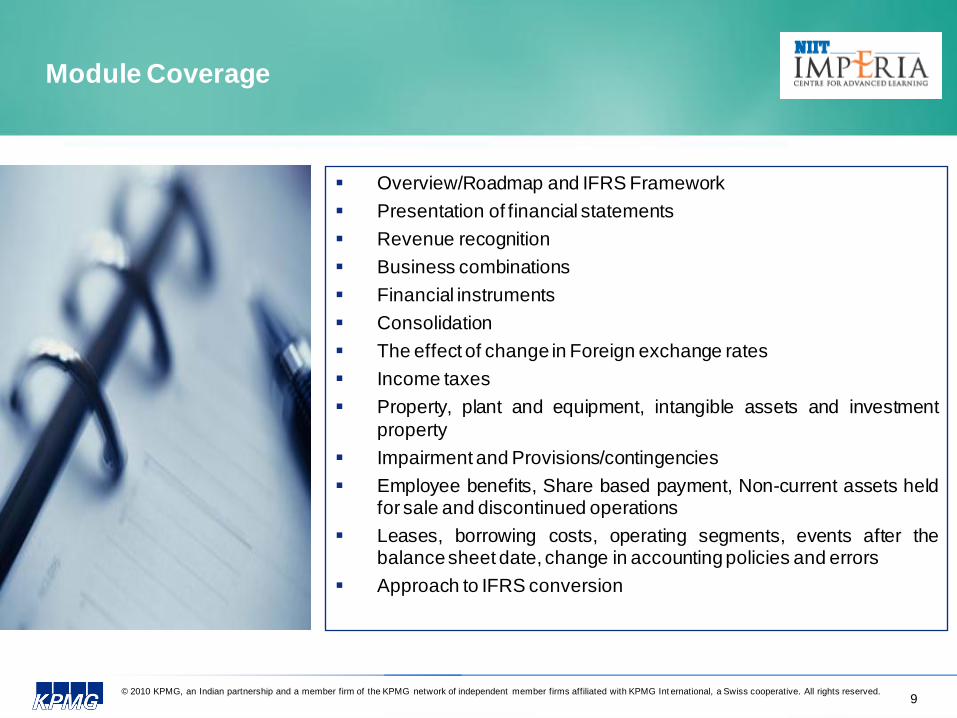

Overview/Roadmap and IFRS Framework

Presentation of financial statements

Revenue recognition

Business combinations

Financial instruments

Consolidation

The effect of change in Foreign exchange rates

Income taxes

Property, plant and equipment, intangible assets and investment

property

Impairment and Provisions/contingencies

Employee benefits, Share based payment, Non-current assets heldfor sale and discontinued operations

Leases, borrowing costs, operating segments, events after thebalancesheet date, change in accountingpolicies and errors

Approach to IFRS conversion

Module Coverage

10© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Upon completion you should understand

– The purpose, status and scope of the Framework

– The fundamental concepts and definitions upon which IFRS’s are

based

– The history and objectives of IASB

– IASB as an organisation

– IFRS’s around the world

– IASB’s work programme

– The concept paper of ICAI and current environment on transition

to IFRS

Topics covered in the module

– IFRS’s issued by the IASB including IFRS 1

– IAS’s issued by the IASC or revisions thereof issued by the IASB

– Interpretations issued by the IFRIC and approved by IASB

– SIC interpretations approved by the IASB or the IASC

Overview/Roadmap and IFRS Framework

11© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Upon completion you should understand

– The required components of financial statements

– How to apply overall financial statement concepts

and assumptions

– The structure of financial statements

Topics covered in the module

– Statement of financial position

– Statement of comprehensive income

– Statement of changes in equity

– Statement of cash flows

– Notes

Presentation of financial statements

12© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Revenue recognition

Upon completion you should understand

– The types of income that exist and what the applicable

standards and interpretations are (e.g., IAS 18, IAS 11 or other)

– When revenue should be recognised

– How revenue is measured

–The steps that should be followed for revenue recognition

– When to separate components of a contract

– The presentation and disclosure requirements

Topics covered in the module

– IAS 18- Revenue recognition

– IAS 11- Construction contracts

– IFRIC 13 –Customer royalty programme

13© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Business Combination

Upon completion you should understand

– Business combination and identify transactions qualifying as

business combination– How to identify the effective date, transactions that meet the

definition of business and control

– How to identify the acquirer in a business combination– How to determine the date of business combination/acquisition

and the date on which the acquirer obtains control of theacquiree

– How to recognise all assets acquired, all liabilities, and any

non- controlling interest in the acquiree at their acquisition datefair values

– How to determine the consideration transferred and goodwill or bargain purchase in a business combination

– How to determine the amount of contingent consideration to be

accounted as part of consideration transferred– The presentation and disclosure requirements related to

business combinations and non-controlling interest

Topics covered in the module

– IFRS 3

– IFRIC 17 Distributions of Non-cash Assets to Owners

14© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Financial instruments

Upon completion you should understand

– The definition of financial instruments and different categories

of financial instruments

– The accounting for each of the categories of financial

instruments

– The definition of derivatives and an introduction to plain vanilla

derivative products (options, swaps etc.) and the overall

accounting framework for derivatives

– The concept of embedded derivatives (hybrid instruments)

– The concept of ‘Hedging’ by learning the three different

types of hedging relationships and the key accounting

differences in those three different hedging relationships

– The classification and disclosure of financial instruments

Topics covered in the module

– IAS 39- Financial instruments: recognition and measurement

– IAS 32- Financial instruments: disclosure and presentation

– IFRS 7- Financial instruments: disclosure

15© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Consolidation

Upon completion you should understand

– How to distinguish different kinds of entities (subsidiaries,

associates and joint ventures)

– How to account for them

– The principles of consolidation, equity accounting and proportionate consolidation

– The consolidation disclosure requirements

Topics covered in the module

– IAS 27- Consolidation and separate financial statements

– IAS 28- Investment in associates

– IAS 31- Interest in joint ventures

– SIC 12- Consolidation – Special purpose entities

16© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

The effect of change in foreign exchange rates

Upon completion you should understand

– How to determine a company’s functional currency

– How foreign currency transactions and balances are translated

into a company’s functional currency

– How foreign currency financial statements are translated for consolidation purposes

– The presentation and disclosure requirements

– The indicators of a hyperinflationary economy

Topics covered in the module

– IAS 21- The effect of change in foreign exchange rates

– IAS 29- Financial reporting in hyperinflationary economies

17© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Income taxes

Upon completion you should understand

– The concepts of current and deferred income taxes

– How income taxes are accounted for by the asset / liability

method

– The concept of ‘temporary differences’ and ascertain how these differences arise and how they need to be accounted for

– How to evaluate the appropriateness of recording valuation allowance against deferred tax assets

– The presentation and disclosure requirements relating to current

and deferred income taxes

Topics covered in the module

– IAS 12- Income taxes

18© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

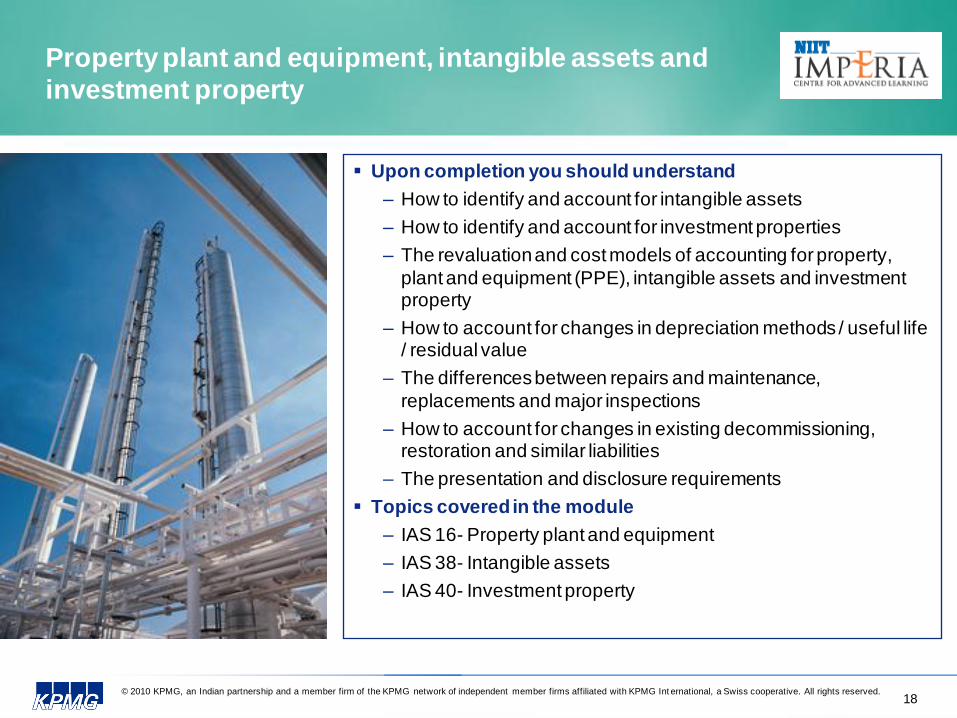

Property plant and equipment, intangible assets and

investment property

Upon completion you should understand

– How to identify and account for intangible assets

– How to identify and account for investment properties

– The revaluation and cost models of accounting for property,

plant and equipment (PPE), intangible assets and investment property

– How to account for changes in depreciation methods / useful life / residual value

– The differences between repairs and maintenance,

replacements and major inspections

– How to account for changes in existing decommissioning, restoration and similar liabilities

– The presentation and disclosure requirements

Topics covered in the module

– IAS 16- Property plant and equipment

– IAS 38- Intangible assets

– IAS 40- Investment property

19© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Impairment and provisions/contingencies

Upon completion you should understand

– The procedures that an entity applies to help ensure that its

assets are carried at no more than their recoverable amount

– The practical difficulties in applying this standard

– The definition of a provision, contingent liability and contingent asset

– The recognition and measurement criteria for provisions, contingent liabilities and contingent assets

– The application of IAS 37 to specific circumstances

– The presentation disclosure requirements

– About the current developments – IASB & IFRIC – regarding

IAS 37

Topics covered in the module

– IAS 36- Impairment of assets

– IAS 37- Provision contingent liabilities and contingent assets

20© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Employee benefits, Share based payment, Non-current

assets held for sale and discontinued operations

Upon completion you should understand

– The key application issues on employee benefits

– The key application issues on share based payments

– The key application issues on non current assets held for sale

– The key application issues on discontinued operations

– The key differences on the above topics with reference to Indian

GAAP

Topics covered in the module

– IAS 19- Employee benefits

– IFRS 2- Share based payments

– IFRS 5- Non current assets held for sale and discontinued operations

21© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Leases, borrowing costs, operating segments, events

after the balance sheet date, change in accounting

policies and errors

Upon completion you should understand

– The key application issues on leasing including right to use

– The key application issues on borrowing costs

– The key application issues on operating segments

– The key application issues on event occurring after the balance sheet date

– The key application issues on change in accounting policies and errors

– The key differences on the above topics with reference to Indian GAAP

Topics covered in the module

– IAS 17 and IFRIC 4- Leases and Determining whether an arrangement contains a lease

– IAS 23- Borrowing costs

– IFRS 8- Operating Segments

– IAS 8 – Accounting policies, change in accounting estimates and errors

– IAS 10 – Events after the reporting period

22© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Approach to IFRS Conversion

Upon completion you should understand

– How and when to start IFRS conversion

– The different steps involved in IFRS conversion

– The role of different stakeholders in the IFRS conversion

– How to assess the impact of IFRS conversion on company

existing financial reporting and practices

– IFRS 1 – First time adoption of IFRS

Topics covered in the module

– IFRS 1 – First time adoption of IFRS

– KPMG approach to IFRS conversion

© 2009 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Know your

Program Director

23

24© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Sandip Khetan

Name Sandip Khetan

Position Director, Accounting Advisory Services

Qualifications Member of the Institute of Chartered Accountants of India (14th Rank

Holder all India)

Experience Sandip Khetan is a director in the Accounting Advisory Services of

KPMG and is based out of Delhi. He has more than 10 year of auditing and accounting experience. Sandip is a member of the Institute of Chartered Accountants of India as well as an alumnus of IIM Ahmedabad

Sandip has extensive audit experience spanning across a sector of industries including IT/ITES, Media, Auto and Telecom dealing with US

GAAP/GAAS and IFRS. He has worked with both large Indian business houses and multinationals. He is the engagement manager on a largest BPO company in India which is only domestic SEC registrant from India.

Sandip has gained significant experience of US GAAP and US Capital market while managing the US IPO process of a large global company

as based out of India.

Sandip is an active participant in training initiatives and have conducted many training session on US GAAP/ IFRS for clients and for different

member firms (Dubai, Moscow, Egypt) in the past.

© 2009 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

About KPMG

IFRS practice

25

26© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

KPMG IFRS practice in India

Established IFRS practice in India with more than 100

engagements and more than 200 resources. Integrated teams to

address technology and process issues related to IFRS adoption.

Committed to providing thought leadership in IFRS.

Significant experience of carrying out large IFRS conversion

projects.

Professional staff having international experience implementing

IFRS and are extremely well networked within core IFRS

practices in Europe, Canada and Australia.

Dedicated centralized IFRS technical group which works closely

with KPMG's International Financial Reporting Group in London.

© 2009 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Synchronous

Learning – NIIT

Imperia

27

28© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

NIIT Imperia - Technology Edge

18 Classrooms in 17 cities

Direct one-to-one interaction is fostered through individual

ICT systems for each student:

– High-performance PCs

– Webcam

– Audio system and microphone at each workstation,

connected directly to faculty at institutes

Classroom interactions & ambience are facilitated by

clusters of student-stations and camera & projection

systems that can span the full classroom.

6 Synchronous Learning Centers created within corporate

premises

Learning Management System (LMS):

– supplementary e-learning

– program-specific notices

– online submission of assignments

– reminder services

– online testing

– student recordsCLASSROOM

VIEW

STUDIO VIEW

29© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Synchronous Learning

REPLICATION OF LIVE CLASSROOM

Full features of face-to-face teaching

Raised-hand-seeking-teacher's-attention

Link- Virtual Tour of Synchronous Learning

Tabulation of responses

Quizzes randomly created by the teacher

30© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

© 2009 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International, a Swiss cooperative. All rights reserved.

Other Details

31© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Course & Reference Material

Name of the book - Insights to IFRS - KPMG's practical

guide to International Financial Reporting Standards 5th

Edition 2008/09

MRP: €155

KPMG Publications - Common

– IFRS: An Overview

– Disclosure Checklist

– Illustrative Financial Statements - The purpose of this

publication is to assist you in preparing financial statements

in accordance with International Financial Reporting

Standards (IFRSs).

– IFRS Developing Roadmap to Convergence

32© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Industry Specific Reference Material

Industry Reference Material

Mining Mining Executive Summary

Airline Accounting for Leases of Aircraft Fleet Assets in the Global Airline Industry

Components of Aircraft Acquisition Cost Associated Depreciation and Impairment Testing in

the Global Air

Consumer

Goods The Application of IFRS on Consumer Good Sector

Pharma IFRS - KPMG's Pharmaceutical and Life Sciences IFRS Conversion Guide

IFRS and Pharmaceuticals Companies

Telecom IFRS Accounting in the Telecoms Industry

Banks IFRS Convergence for the Indian banking sector

IFRS-Illustrative-financial-statements_Banks

Media IFRS Practical Issues Accounting Strategies for the Media and Publishing Industries

Technology The Application of IFRS for Technology Companies

Oil & Gas IFRS-application on oil-gas

Power IFRS-application-power-utilities

Infrastructure Impact of IFRS on Infrastructure companies

Retail Impact of IFRS on Retail Sector

33© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

What our earlier batch participants had to say

about the program?

"The program has helped me in getting a detailed knowledge about the application of IFRS

Standards its application and treatment of accounting records."

- Ajay Mukherjee, Divisional Controller F&A, Tata Steel Processing & Distribution Ltd.

"Well organized, effective learning, all the speakers were good, Specially Mr Iyer, Mr Khetan

& Mr Mankani were very good."

- Ms. Yogini Medadkar, Manager ,Finance & Accounts, Soham Surface Coatings Pvt. Ltd.

"The content is adequate and very informative. The faculty is experienced and teachers give

lot of practical examples, thereby the program is not monotonous."

- Anil Lamba, Head ,Finance & Accounting, Max Buba Health Insurance Company Limited

"A well-structured program to give a holistic view of the IFRS on a macro level and some

relevant aspects of the workings of IFRS in the Indian context."

- Apurv Relan, Partner, Apurv Relan & Co., Chartered Accountant

34© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Sample Certificate

35© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Application period

– Application for the Batch will commence from Aug 11, 2010. Limited

Seats Availability.

Application forms

– Application forms can be obtained from www.niitimperia.com or at

local NIIT Imperia Centers

Documents Required for Application

– 1 Passport size photo affixed [Latest photo with light backdrop]

Information Session

– To attend information session about the program Register Here

How to Apply

36© 2010 KPMG, an Indian partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG Int ernational, a Swiss cooperative. All rights reserved.

Call Us At 1800-266-0304

(Or)

Write to [email protected]

The information contained herein is of a general nature and is not intended to address the circumstances of any particular in dividual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the da te it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

KPMG and the KPMG logo are registered trademarks of KPMG International, a Swiss cooperative.

Contact us

For any Queries Or Doubts,