aercap holdings - iis windows serverlibrary.corporate-ir.net/.../271139/roadshow_q3_2007.pdfaercap...

TRANSCRIPT

AerCap HoldingsAerCap Holdings

November 2007November 2007

Klaus Heinemann, CEO

RoadshowRoadshow US and EuropeUS and Europe

2

Forward Looking Statements & Safe HarborForward Looking Statements & Safe Harbor

This presentation contains certain statements, estimates and forecasts with respect to future performance and events. These statements, estimates and forecasts are “forward-looking statements”. In some cases, forward-looking statements can be identified by the use of forward-looking terminology such as “may,” “might,” “will," “should,” “expect,” “plan,” “intend,” “estimate,” “anticipate,” “believe,”“predict,” “potential” or “continue” or the negatives thereof or variations thereon or similar terminology. All statements other than statements of historical fact included in this presentation are forward-looking statements and are based on various underlying assumptions and expectations and are subject to known and unknown risks, uncertainties and assumptions, may include projections of our future financial performance based on our growth strategies and anticipated trends in our business. These statements are only predictions based on our current expectations and projections about future events. There are important factors that could cause our actual results, level of activity performance or achievements to differ materially from the results, level of activity, performance or achievements expressed or implied in the forward-looking statements. As a result, there can be no assurance that the forward-looking statements included in this presentation will prove to be accurate or correct. In light of these risks, uncertainties and assumptions, the future performance or events described in the forward-looking statements in this presentation might not occur. Accordingly, you should not rely upon forward-looking statements as a prediction of actual results and we do not assume any responsibility for the accuracy or completeness of any of these forward-looking statements. We do not undertake any obligation to, and will not, update any forward-looking statements, whether as a result of new information, future events or otherwise.

3

AgendaAgenda

The Investment Story

Market Opportunities

AerCap Business Model and Strengths

Financial Overview

Reasons to Invest in AerCap

4

AerCap at a GlanceAerCap at a Glance

Global aviation company with proven track record and integrated business model providing aircraft, engines and parts to customers in every major region of the world

North America/Caribbean 20% of YTD Sept 2007

lease revenues

Latin America9% of YTD Sept 2007 lease revenues

Asia / Pacific33% of YTD Sept

2007 lease revenues

Total Assets $4.3Bnat September 30, 2007

Contracted Orders $4.9Bn_____

Total Assets $9.2Bn Including Purchase Commitments

325 Aircraft65 Engines

107 Customers in 46 CountriesAerCap Locations

Europe 38% of YTD Sept 2007

lease revenues

5

Investment HighlightsInvestment Highlights

Powerful, differentiated integrated business model, extracting value over entire asset life

+Attractive market with strong travel demand and tight aircraft supply

+Contracted orders of $4.9Bn creates strong pipeline of growth

+Experienced management team with proven track record and deep

industry and securitization experience

=Proven earnings and cash flow growth

6

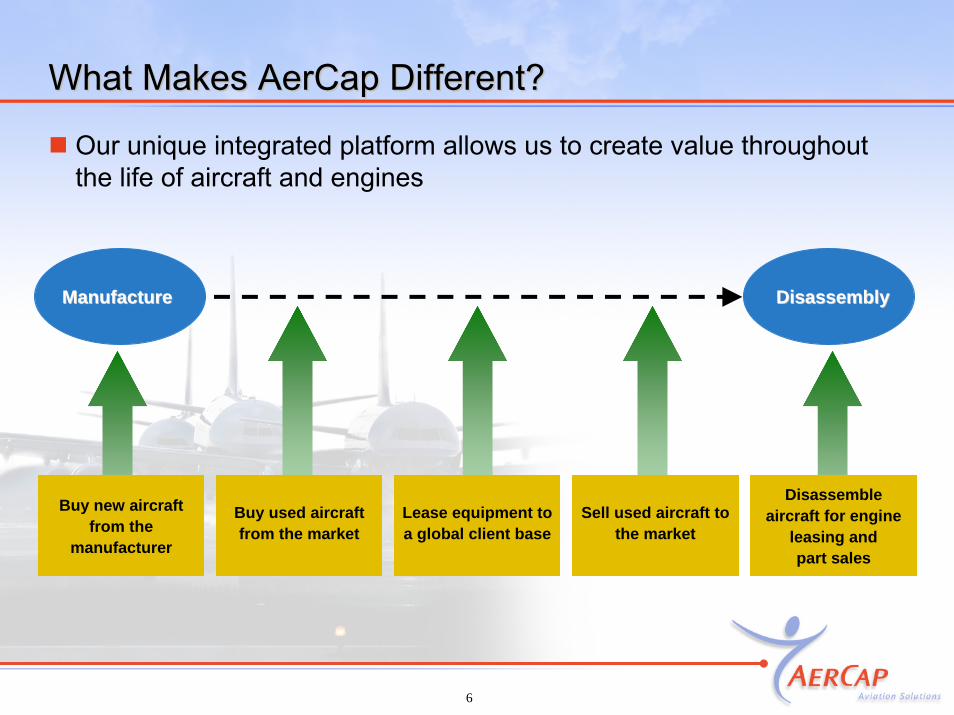

What Makes AerCap Different?What Makes AerCap Different?

Our unique integrated platform allows us to create value throughout the life of aircraft and engines

ManufactureManufacture DisassemblyDisassembly

Buy new aircraft from the

manufacturer

Buy used aircraft from the market

Lease equipment to a global client base

Sell used aircraft to the market

Disassemble aircraft for engine

leasing and part sales

7

Robust Demand and Tight SupplyRobust Demand and Tight Supply

Demand for new and used commercial aircraft is driven by:― Aging world aircraft fleet ― Ongoing restructuring of U.S. “legacy” carriers― Rapid emergence of high-growth “Low Cost Carriers”― Rapid airline passenger growth in emerging markets― Higher fuel prices― More stringent environmental regulations of noise and emissions

Used aircraft availability in March 2007 is at lowest point since 5 years (1)

Strong aircraft demand driving large increase in orders and production backlog

Manufacturers cannot increase supply sufficiently to meet near term demand

Significant shift among airlines to lease rather than own aircraft

(1) Source: Ascend MarketI

Market Opportunities:Market Opportunities:

8

Ageing World Aircraft FleetAgeing World Aircraft Fleet

Commercial Jets – Average Fleet Age 2007Passenger Jets

2,9562,270

685 496

2,077

1,132

309

2,082

476

429

762 613

4,366

333

1,908

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

North America Europe Asia and PacificRim

Africa and MiddleEast

South America

Avg:11.2 Years

Avg:18.4 Years

Avg:10.4 Years

Avg:14.2 Years

Avg:19.1 Years

Less Than 11 Years 11 to 20 Years Greater Than 21 Years

21% of World Fleet >21 years creates significant refleeting need

Source: SH&E Analysis Sept 2007

9

LCC Share of Order Backlog by RegionLCC Share of Order Backlog by Region

2

21

30

36

48

0

10

20

30

40

50

60

Europe North America South America Asia Pacific Africa and Middle East

LCC Share of March 2007 Order Backlog, by RegionLCC Share (%)

Source: ACAS March 2007, SH&E Analysis

10

Emerging Markets A Key FocusEmerging Markets A Key Focus

30.4

13.0

3.7 3.1 2.7 1.3 1.2 0.60.0

7.0

14.0

21.0

28.0

35.0

NorthAmerica

WesternEurope

Asia Pacific(excl.

China)

SouthAmerica

(excl.Brazil)

Brazil China Russia India

Current Fleet Backlog

Ratio of Current Fleet and Order Backlog to Population(1)

(Aircraft / Million of Population)Aircraft / Population Ratio

(1) Source: AvSoft U.K. Aircraft Analytical System (“ACAS”)(April 2006) and IMF World Economic Outlook, April 2006.

AerCap 2007 Sept YTD Lease Revenues by Region (%)

Asia / Pacific

Europe

North America/Caribbean

Latin America

33

38

20

9

11

Supply Remains TightSupply Remains Tight

Notes:(1) 2007 projected deliveries (Source: Boeing, Airbus)(2) Current “in production aircraft” available for sale / lease (Source: BACK JetMart)(3) Average annual demand estimated for next 20 years as projected by Boeing (Source: SH&E)

(3)

at Boeing and Airbus

(2)

(1)

1,430

69920

0

200

400

600

800

1,000

1,200

1,400

1,600

Annual AircraftProduction

Stored Aircraft Estimated AnnualDemand

Long-haul network 3%

Freight 3%

Low cost / short haul 37%

Global network carriers 54%

Charter 3%

12

XXXXXXXXXXXXXXX

XXXXXXXXXXXXXXX

XXX

XXXXX

XXXX

XX

XXXXXX

XXXXXX

ILFCPegasus AviationMacQuarieAviation CapitalCIT AerospaceBoeing CapitalRBS Aviation CapitalBabcock and BrownAWASPembroke GroupSingapore Aircraft LeasingORIXSumishoAircastleGenesis

AerCapGECAS

Integrated Business ModelIntegrated Business Model

MRO / Part-out

BusinessEngine Leasing

CapacityLarge Orders

in Place (in Excess of 50)

Experience in Securitization Market

Fleet Size in Excess of 100 Aircraft

Top Operating Lessors

Global Reach Capability and Risk Diversification: Financing: Growth:

Revenue Diversification:

13

High Quality and Well Diversified PortfolioHigh Quality and Well Diversified Portfolio

84% narrowbody – “Work Horses” of industry

High share of liquid / remarketable aircraft

Average age of owned aircraft fleet 7.3 years

65 engines in portfolio, as of September 30, 2007

― CFM56 engines, one of the most widely used engines in the commercial aviation industry, represented 80% of our portfolio

(1) Includes one A319 aircraft on order by us and 18 A319 aircraft on order by AerVenture.(2) Includes three A320 aircraft on order by us and 51 A320 aircraft on order by AerVenture.(3) Excludes the four aircraft which we intend to disassemble or sell when their leases expire, consisting of three DC-9

and one Boeing 767 aircraft.(4) Excluding 8 Aeroturbine aircraft and 2 aircraft under LOI / purchase contract.

Owned Portfolio

Managed Portfolio

Number of Aircraft

Owned (3)Number of

Aircraft

Airbus A300 Freighter 2 – – – 2

Total 133 79 103 0 315(4)

Airbus A319 11 – 19(1) – 30

Airbus A320 54 13 54(2) – 121

Airbus A321 21 1 _ – 22

Airbus A330 6 _ 30 – 36

Airbus A340 1 1 – – 2

Boeing 737 21 30 – _ 51

Boeing 767 1 2 – – 3

Boeing 757 2 3 – – 5

DHC Dash 8 1 – – – 1

Fokker 100 7 3 – – 10

Fokker 70 – 2 – – 2

MD 11 Freighter 1 1 – – 2

MD-83 1 7 – – 8

MD-82 4 6 – – 10

Fairchild Dornier 328 – 10 – – 10

Number of Aircraft

on Order

Number of Aircraft under

Purchase Contract

Total Owned, Managed

and Ordered Aircraft

Aircraft Portfolio as of September 30, 2007

14

Managing Our Aircraft PortfolioManaging Our Aircraft Portfolio

New Aircraft Leases Used Aircraft Leases

61.268.7

103.2 104.0

2004 2005 2006 3Q 2007

38.1

50.6

58.7

75.0

2004 2005 2006 3Q 2007

Lease Terms in Months Continue to Lengthen

(1) Based on 34 LOIs and 3 lease agreements signed in resspect of new aircraft for the 9 months ended Sept 2007

(1)

15

Funding StrategyFunding Strategy

Optimize Funding Costs

- Utilize Capital Markets, ECA Funding, Tax-Based Structures, etc.

- Overall Cost of Capital Competitive with Key Industry Leaders

Eliminate Liquidity Risk

- No Bullet Maturities

- Securitization Vehicles Allow Extension of Terms

- Available Lines of Credit in addition to Capital Markets

Minimize Risk to Equity (Recession Proofing)

- Key Investments and Funding Vehicles are “Ring-Fenced”

- Recourse to AER Significantly Reduced

16

Highlights Q3 2007Highlights Q3 2007

Net income was $58.1 million for third quarter 2007, exclusive of non-cash charges relating to mark-to-market of interest rate caps and share-based compensation

Earnings per share for third quarter 2007 was $0.68 excluding the above charges

Leasing revenue for third quarter 2007 was $137 million, up 23% from third quarter 2006 (Total revenues up 12% over 2006)

Total assets were $4.3 billion as of September 30, 2007, up 20% from September 30, 2006

Committed purchases for full year 2007 thus far, are $854 million

On October 10, 2007, a $182 million PDP funding facility was closed for eight new A330s under forward order

Contracted 2008 lease revenues already 108% of 2007 revenues

17

Strong Revenue and Earnings GrowthStrong Revenue and Earnings Growth(US$MM)

$28

$106

$177

$120

$177

2004 PF 2005 2006 YTD 3Q2006

YTD 3Q2007

Net Income

$892

$603

$814

$611

$391

2004 PF 2005 2006 YTD 3Q2006

YTD 3Q2007

Revenues

48%

Notes:(1) Excludes pre-tax impairment charges of $134.7MM in 2004.(2) Pro-forma for Cerberus Acquisition, AeroTurbine Acquisition and IPO (excludes share-based compensation; includes maintenance adjustment)(3) Excludes non-cash share-based compensation charge of $68.3MM after-tax.(4) Adjusted for : Mark to Market interest rate caps, share based compensation, and Q2 2007 refinancing charges

(2)(2)(1) (3)

* Before $ 24m after tax charge relating to debt refinancing

48%

(4)(4)

18

As of Sept 30, 2007

(US$ in millions)332.8

3,091.2

181.4

225.2

422.6

4,253.2

2,781.6

563.7

907.9

4,253.2

3.1

Cash and Cash Equivalents

Flight Equipment, Net

Notes Receivable, NetPrepayments onFlight EquipmentOther Assets

Total Assets

Term Debt

Other Liabilities

Shareholders’ EquityTotal Liabilities and Shareholders’ EquityDebt / Equity (x)

Strong Balance Sheet with Contracted GrowthStrong Balance Sheet with Contracted Growth

$3,604$3,061

$3,918$4,253

$4,926

2004 2005 2006 3Q 2007 2007 – 2012Estimated

CapEx

2012

Total Assets

Balance Sheet Positioned for Future Growth

$9,179

19

Reasons to invest in AerCapReasons to invest in AerCap

Powerful, differentiated integrated business model, extracting value over entire asset life

+Attractive market with strong travel demand and tight aircraft supply

+Contracted orders of $4.9Bn creates strong pipeline of growth

+Experienced management team with proven track record and deep

industry and securitization experience

=Proven earnings and cash flow growth