african auto industry & market outlook q1 2017

TRANSCRIPT

Profiling African Auto

Industry and Market

Perspective on

Current State and

Growth Potential

Eugene Nizeyimana

Director for Engineering and Management Consulting

Automotive and Industrial Sector

Content

SSCG at a Glance

African Auto Industry Economic Outlook

Auto Industry and Motorization Road Map

Vehicle Production Rate, Sales & Usage

Global OEMs Production and Assembly Footprint in Sub-Saharan Africa

Evolution of Domestic African Auto Industry and Vehicles

Mega Trends Reshaping African Auto Industry: Revenue, Cost, Production, Import, Competition and Market Share

Vehicles Designed and Manufactured in Africa

Major Forces Driving Auto Industry Market Share and Growth

Factors affecting location of Assembly Plant - Key success factors for considerations

Unlocking New Potential in Africa

Recent Growth Trends Transforming the Industry

Economic forces and key drivers reshaping the auto industry and the location of assembly facilities

Our Engineering Solutions for Automotive & Industrial Sector

Customized Automotive and Industrial Landscape

Market intelligence & insights

Delivery approach

Contact us

CO

MP

AN

Y N

AM

E

SSCG at a Glance

SSCG is global management consulting and professional firm. We

provide engineering and management advisory across business

services, automotive, industrial manufacturing and emerging markets

sectors.

We provide informed perspective on the issues faced by our clients.

The insights and quality solutions delivered to support our clients to

build trust and confidence in the markets and in economies.

We combines our multi-disciplinary approach with deep, practical

industry knowledge to support our clients meet market dynamic

challenges and respond to opportunities.

In response to market shift and new challenges faced by our clients .

We do not just to react , but also aspire and strive to develop innovative

approaches and transformative solutions on our promises to help

them outperform in their territories.

We have developed a new value proposition for our clients and

provides a range of solutions that can be integrated across businesses

and/or to specific sector domains. In so doing, we are playing a critical

role in building stronger and competitive enterprises, for our clients, in

the economies and consulting space.

CO

MP

AN

Y N

AM

E

African cities are becoming congested with

traffic comprising mainly of second hand

vehicles. There are several manufacturers

in the continent assembling new vehicles

however, faces market challenges,

complexity and poor operational climate

which inhibit growth and competitiveness.

Despite rising growth over the past decade,

governments all over Africa have failed to

frame industrial policies and build robust

infrastructures capable of boosting home-

grown industry. The lack of such projects is

a handicap for the future.

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

CO

MP

AN

Y N

AM

E

African Auto Industry Economic Outlook

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

• Africa currently produces less than 1% of the world's manufactured goods.

• Approx 42 Million registered passenger vehicles operate in Africa today

• Motorisation rate of 44 vehicles per 1 000 inhabitants. Far below global average of 180 vehicles per 1 000

inhabitants,

• 2 million Cars Projected Sales in 2017. Sales projected to reach up to 10 million units per annum within the

• next 15 years based on current trends.

• 1.2 Billion population

• South Africa, Egypt, Algeria and Morocco are the established and rapidly developing automotive industries.

Collectively, accounted for more than 80% of total new vehicle sales in 2015

• Apart from South Africa, Morocco, Algeria and Mauritius, Sub-Saharan African economies and Auto industry sectors

lacks capabilities and capacity to compete in the global market.

CO

MP

AN

Y N

AM

E

Automobiles are a liberating technology for people and goods to move

around the world. This allows commuting in ways that were

unimaginable a century ago. Automobiles improve quality of life, provide

access to markets, amenities , jobs, transport of goods and services to

customers. The auto industry remains a fundamental engine of

economic growth.

The global auto industry is a key sector of the every economy. The

industry continues to grow, registering increase in sales over the past

decade and cover over 5 % of the world’s total manufacturing

employment. The industry has created opportunities within the supply

chain , boosting sales and usage.

Today, motor-vehicle application in Africa have led to far-reaching and

complex economic transformations creating mobility opportunities.

African motoring is stepping up its game in the competition to challenge

the incumbent leaders in the region such as the Germans, French,

Indians, Japanese, Korean and Chinese . The industry is also creating

wholly locally sourced vehicles but yet to achieve the capability to

compete in the global market.

Auto Industry and Motorization Road Map

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

CO

MP

AN

Y N

AM

E

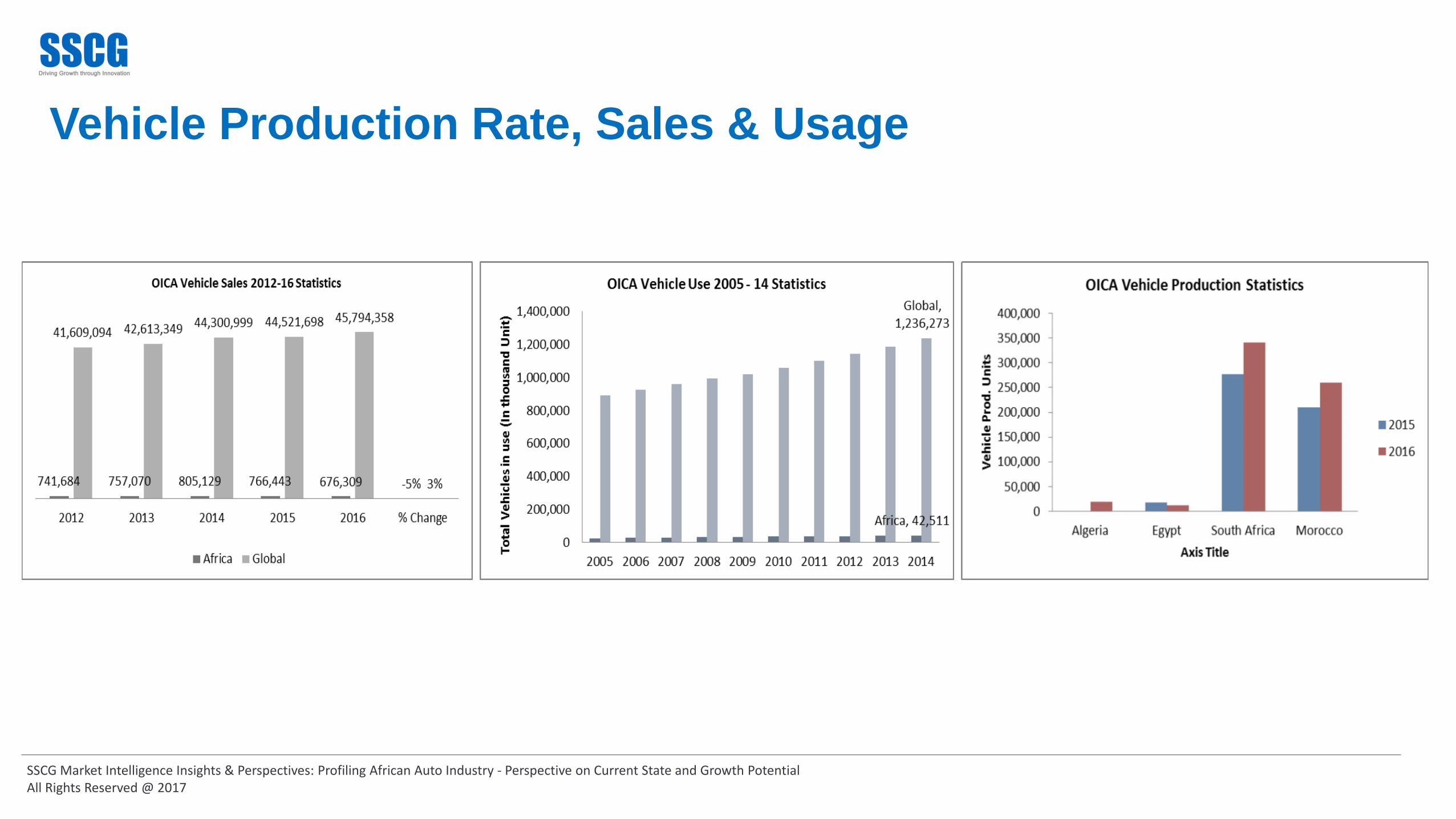

Vehicle Production Rate, Sales & Usage

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

CO

MP

AN

Y N

AM

E

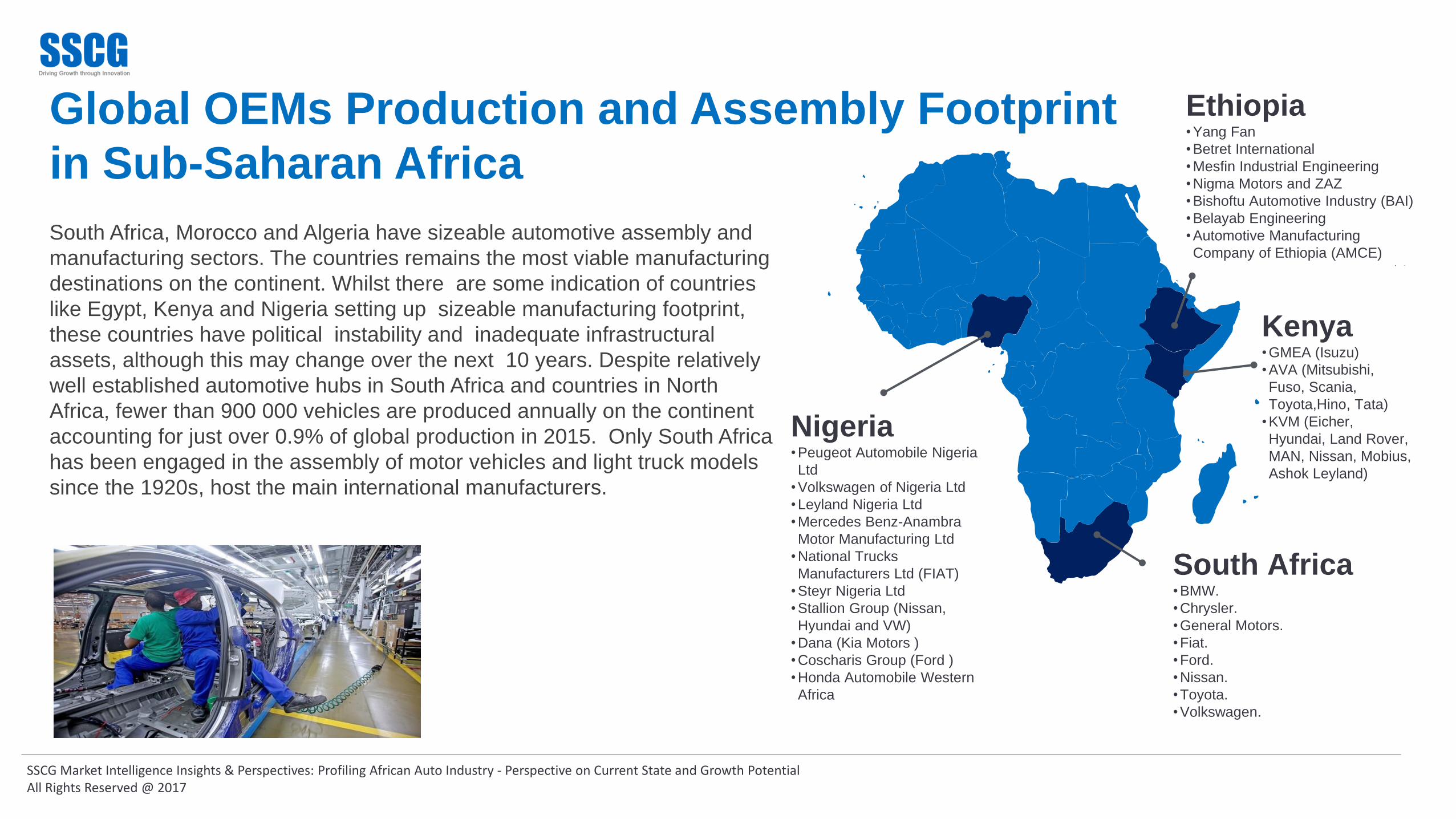

Kenya •GMEA (Isuzu)

•AVA (Mitsubishi,

Fuso, Scania,

Toyota,Hino, Tata)

•KVM (Eicher,

Hyundai, Land Rover,

MAN, Nissan, Mobius,

Ashok Leyland)

Ethiopia •Yang Fan

•Betret International

•Mesfin Industrial Engineering

•Nigma Motors and ZAZ

•Bishoftu Automotive Industry (BAI)

•Belayab Engineering

•Automotive Manufacturing

Company of Ethiopia (AMCE)

Global OEMs Production and Assembly Footprint

in Sub-Saharan Africa

South Africa, Morocco and Algeria have sizeable automotive assembly and

manufacturing sectors. The countries remains the most viable manufacturing

destinations on the continent. Whilst there are some indication of countries

like Egypt, Kenya and Nigeria setting up sizeable manufacturing footprint,

these countries have political instability and inadequate infrastructural

assets, although this may change over the next 10 years. Despite relatively

well established automotive hubs in South Africa and countries in North

Africa, fewer than 900 000 vehicles are produced annually on the continent

accounting for just over 0.9% of global production in 2015. Only South Africa

has been engaged in the assembly of motor vehicles and light truck models

since the 1920s, host the main international manufacturers.

South Africa •BMW.

•Chrysler.

•General Motors.

•Fiat.

•Ford.

•Nissan.

•Toyota.

•Volkswagen.

Nigeria •Peugeot Automobile Nigeria

Ltd

•Volkswagen of Nigeria Ltd

•Leyland Nigeria Ltd

•Mercedes Benz-Anambra

Motor Manufacturing Ltd

•National Trucks

Manufacturers Ltd (FIAT)

•Steyr Nigeria Ltd

•Stallion Group (Nissan,

Hyundai and VW)

•Dana (Kia Motors )

•Coscharis Group (Ford )

•Honda Automobile Western

Africa

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

Sub-Saharan Africa is projected to remain one of the

fastest growing regions in the world. While Africa’s

economy is soaring past most regions with an annual

growth rate of about 5% due mainly to increased

agriculture production, infrastructure investment

including transportation, ports and energy as well as

buoyant services led by tourism, telecommunications

and financial services, the continent’s middle class is

expected to swell to approximately 300 million people.

Additionally, Its projected that private consumption in

the region to remain strong in 2017; particularly with

the continent’s burgeoning middle class looking to

splurge on new passenger vehicles and for most, their

first such purchase.

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

KIIRA EV, Uganda's first electric car

Evolution of Domestic African Auto Industry and Vehicles

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

Africa is projected to see sales of new 2 million cars in 2017, with major auto players

such as Toyota, Tata Motors and General Motors GM -0.78% looking at the continent for

growth opportunities.

There are approximately 21.6 million passenger vehicles operating in Africa today;

making the continent’s nearly 1.2 billion population a very attractive prospect for global

automobile manufacturers to penetrate.

Not to be left out of the lucrative market, African entrepreneurs are now entering the

automobile industry; designing and developing vehicles specifically geared for the local

market and consumers but with global aspirations.

Investment/capital

Manufacturing technology

Design

Raw materials and sub

assembly parts

Labour Certification

and homologation

Engineering skills and

competencies

Robust supply chain

Operating environment

Scalability

Factors influencing vehicle manufacturing

CO

MP

AN

Y N

AM

E

Mega Trends Reshaping African Auto Industry: Revenue,

Cost, Production, Import, Competition and Market Share

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

Key Trends

Operating environment – Operating hard and soft economic infrastructures

Drivers preferences

Competition

Increase in supply chain distribution channels

Urbanisation, rapid middle class growth and rise in income

Regulation and government policies – Restrictions of second hand imported vehicles

Improvement of road infrastructure

Supplier supply chain development, production localization and collaboration

Capacity development

Global OEMs redefining manufacturing landscape building wider R&D competence and cost optimisation through outsourcing and modularisation

Local industry capacity

evaluation factors

Demand and supply

Products adaptation

Business and operating

model models

alignment

Market dynamics

Supply chains/value

chains

Capitalisation and

investment

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

Nyumbu - Tanzania

Automotive technology

center (TANZANIA)

Innoson Vehicle

Manufacturing (IVM) Co,

LTD. (Nigeria)

Saroukh el-Jamahiriya

(Libya)

Kiira Motors (Uganda) Kantanka Automobile

Company, Ghana

Wallyscar (Tunisia) Optimal Energy Joule

(South Africa)

Advanced Automotive

Design (South Africa)

Bailey Edwards Cars

(South Africa)

Birkin Cars (South

Africa) Perana

Performance

Group (South

Africa)

Laraki (Morocco)

Mobius Motors (Kenya) The African Bull Dog

( KENYA)

KIIRA EV, Uganda's

Vehicles Designed and Manufactured in Africa

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

Innoson Vehicle Manufacturing (IVM) Company, Nigeria

CO

MP

AN

Y N

AM

E

African Automotive Industry continues to

adjust to market forces. Although,

manufacturing level is being impacted by

the increasing number of imported vehicles

and the after affects of the global economic

crisis.

Lack of adequate operating

environment, infrastructure, labor

market and auxiliary industries

Business Climate Policies Lack of conducive policies to provide targeted support

to the industry and to unlock the new market

opportunities.

Product Appreciation Indigenous manufacturers are

stifled by the lack of appreciation

of their products.

Second-Hand Vehicle imports Consolidating a highly fragmented aftersales market and

overcoming the over-reliance on second-hand vehicle

imports.

Taxes & Competitive

Pricing High tax rates on vehicles reduce the

affordability, especially given the low

income of the population, and restrains

the vehicle retail market.

Quality, Homologation &

Standardization Lack of robust quality assurance and

competitive pricing

1 2 3

8

6

4

Challenges

Digital disruption is a reality that affects car

manufacturers, marketers, and dealerships.

Consumers are demanding more interactive and

connected vehicles. Different markets and diverse

brands respond differently to this disruption and

there is no one-size-fits all strategy.

5 Greener Road &

Electrification African consumers are less concerned with

greener emissions than they are with

affordability or even just access to mobility in

any form. The exception may be in the small

premium segment, and even, the greener

route would only be adopted if it also

represented more convenience.

Labour Dispute 9 Car manufacturing industry has

continued to buckle under the

pressure of large-scale strikes and

labour disputes especially in South

Africa

Technology & Digital Disruption 7

Major Forces Driving Auto Industry Market Share and

Growth

Factors affecting the location of

Plant • The quality and availability of raw materials and adequate

infrastructure.

• Low cost and competent labor with right of skill mix

• Population density

• Government policies and regulations

• Availability of associated industries “knowledge networks”

• Security and political stability

Key success factors in

manufacturing

• Low cost production efficiency (achieve scale economies, capture experience curve effects)

• Manufacturing quality (fewer defects, less repair)

• High utilisation of fix assets.

• Access to adequate supply of skilled labour

• Low cost locations.

• High labour productivity.

• Low cost product design and engineering

• Ability to manufacture or assemble products that are customised to buyers specifications.

• Optimised supply chain.

• Effective and efficient suppliers

• Industry 4.0 – Production technology

• Low cost raw materials.

Factors affecting location of Assembly Plant - Key

success factors for considerations

Africa’s auto market is regarded as the final frontier for the global automotive industry, is

relatively very small however presents huge consumption opportunities. Consumer buying

power is on the rise as the continent’s middle class increases exponentially.

Global automotive companies are looking at Africa as the last frontier for growth, scrambling

for market share. German brands such as BMW and Volkswagen; Ford, Chrysler and General

Motors from the US; and Japanese manufacturers Nissan and Toyota already have

established plants in South Africa which hey hope to use as a launch pad for expansion in Sub

Saharan Africa. While most cars are sold locally, many are exported, mostly to Europe and the

US.

Unlocking New Potential in Africa

Factors affecting supply

Vehicle price

Import duties and taxes

Supply chain

Brand

Vehicle time in services

Demand dynamics

Factors affecting sales/demand

Financing options

Advertising and marketing

Vehicle pricing

Affordability – Growing middle class

Vehicle design specification

Imports of second hand cars

OEM Brand

Durability

Running cost

Usage/Application

Urbanisation

C O M P A N Y N A M E

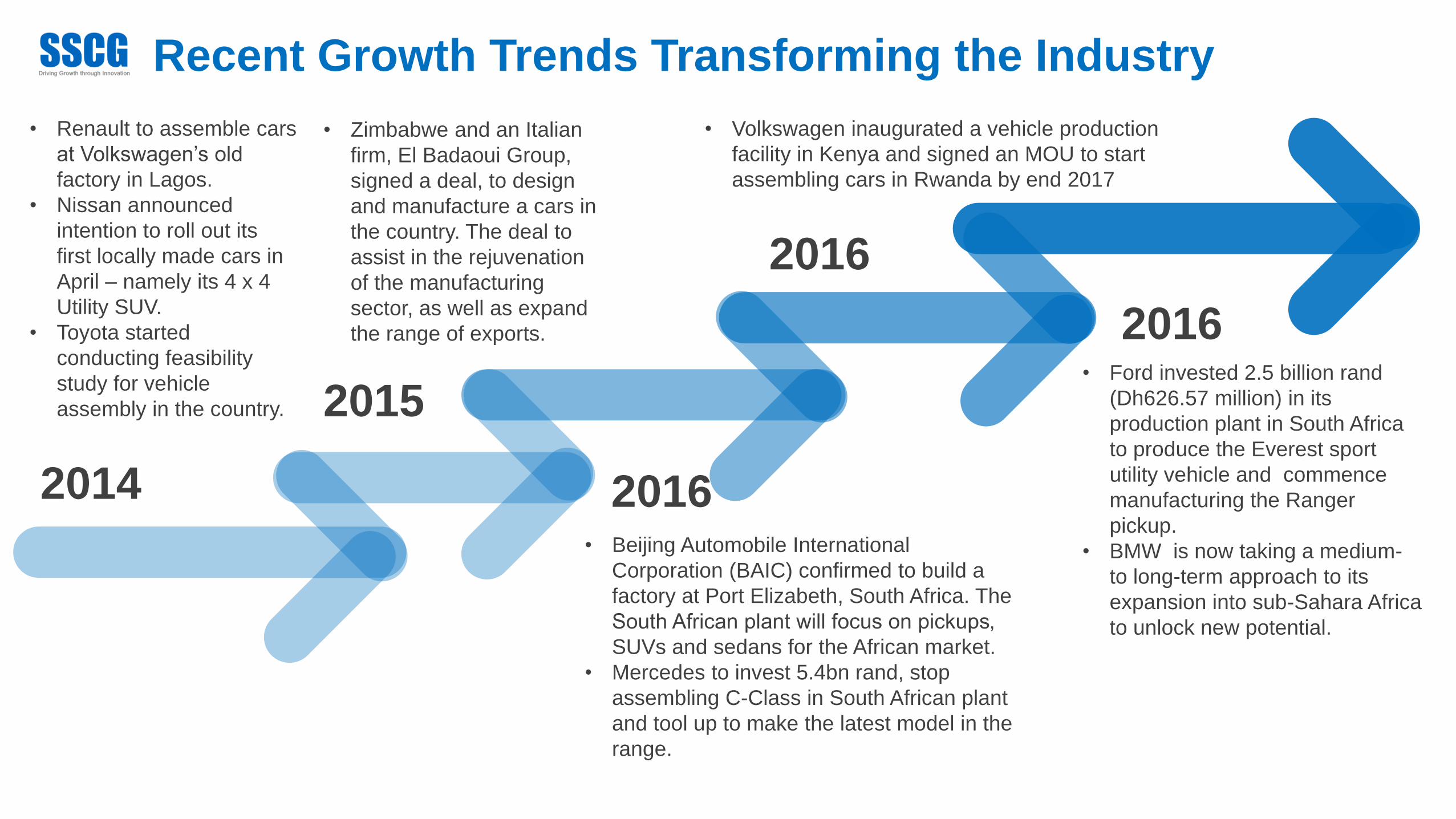

• Volkswagen inaugurated a vehicle production

facility in Kenya and signed an MOU to start

assembling cars in Rwanda by end 2017

• Beijing Automobile International

Corporation (BAIC) confirmed to build a

factory at Port Elizabeth, South Africa. The

South African plant will focus on pickups‚

SUVs and sedans for the African market.

• Mercedes to invest 5.4bn rand, stop

assembling C-Class in South African plant

and tool up to make the latest model in the

range.

• Ford invested 2.5 billion rand

(Dh626.57 million) in its

production plant in South Africa

to produce the Everest sport

utility vehicle and commence

manufacturing the Ranger

pickup.

• BMW is now taking a medium-

to long-term approach to its

expansion into sub-Sahara Africa

to unlock new potential.

• Zimbabwe and an Italian

firm, El Badaoui Group,

signed a deal, to design

and manufacture a cars in

the country. The deal to

assist in the rejuvenation

of the manufacturing

sector, as well as expand

the range of exports.

• Renault to assemble cars

at Volkswagen’s old

factory in Lagos.

• Nissan announced

intention to roll out its

first locally made cars in

April – namely its 4 x 4

Utility SUV.

• Toyota started

conducting feasibility

study for vehicle

assembly in the country.

Recent Growth Trends Transforming the Industry

2014

2015

2016

2016

2016

Economic forces and key drivers reshaping the auto

industry and the location of assembly facilities

1 Decreasing the age of cars

allowed for import in many

countries while simultaneously

decreasing the affordability by

increasing the taxes levied will

drive sales of more affordable,

newer and locally-assembled cars.

2 Localisation incentives to

assemble locally, such as tax

breaks or waiving of import duties

for parts, will make it more

affordable to assemble vehicles in

frontier economies in the short to

medium term, and could

encourage production in the long

term.

3

4

Definitions of local content have

been developed and aligned to the

other EAC members’ automotive

and manufacturing policies..

The creation of a controlled

operating environment iinstituted

for assemblers to ensure that

investors compete on a level

playing field, which in turn would

encourage international

automotive companies and

suppliers to invest in the region.

5

6

Governments have commissioned

programmes to increase

electricity accessibility and

enhance infrastructure. Investment

in infrastructure development has

increased, highways, railways ,

Airports and ports being enlarged

to improve regional linkage and

capacity..

Nigeria’s federal government

introduced National Automotive Policy,

to revive the country’s auto

manufacturing base and creation of

automotive hubs..

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

7 Effort being made to develop and

promote auxiliary industries

including steel, rubber, leather and

glass.

8 Ethiopia instituted programmes to transform assemblers that

bolt together imported kits into a network of factories. Industrial

zones around Addis Ababa and the northern city of Mekelle,

where Ethiopian firms and Chinese partners assemble the

vehicle kits. The government is supporting industrialisation and

development of auxiliary industries coupled with a large cost

competitive labour pool, and sizeable investments in

infrastructure, have positioned the country favourably for

automotive manufacturing.

9 Zimbabwe and El Badaoui Group signed a deal

to design and manufacture a cars in the country.

The deal is to rejuvenation of the manufacturing

sector, as well as to expand the range of

exports.

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

Economic forces and key drivers reshaping the auto

industry and the location of assembly facilities

CO

MP

AN

Y N

AM

E

How we can support your

business Delivering integrated strategies &

Transformative Solutions

.

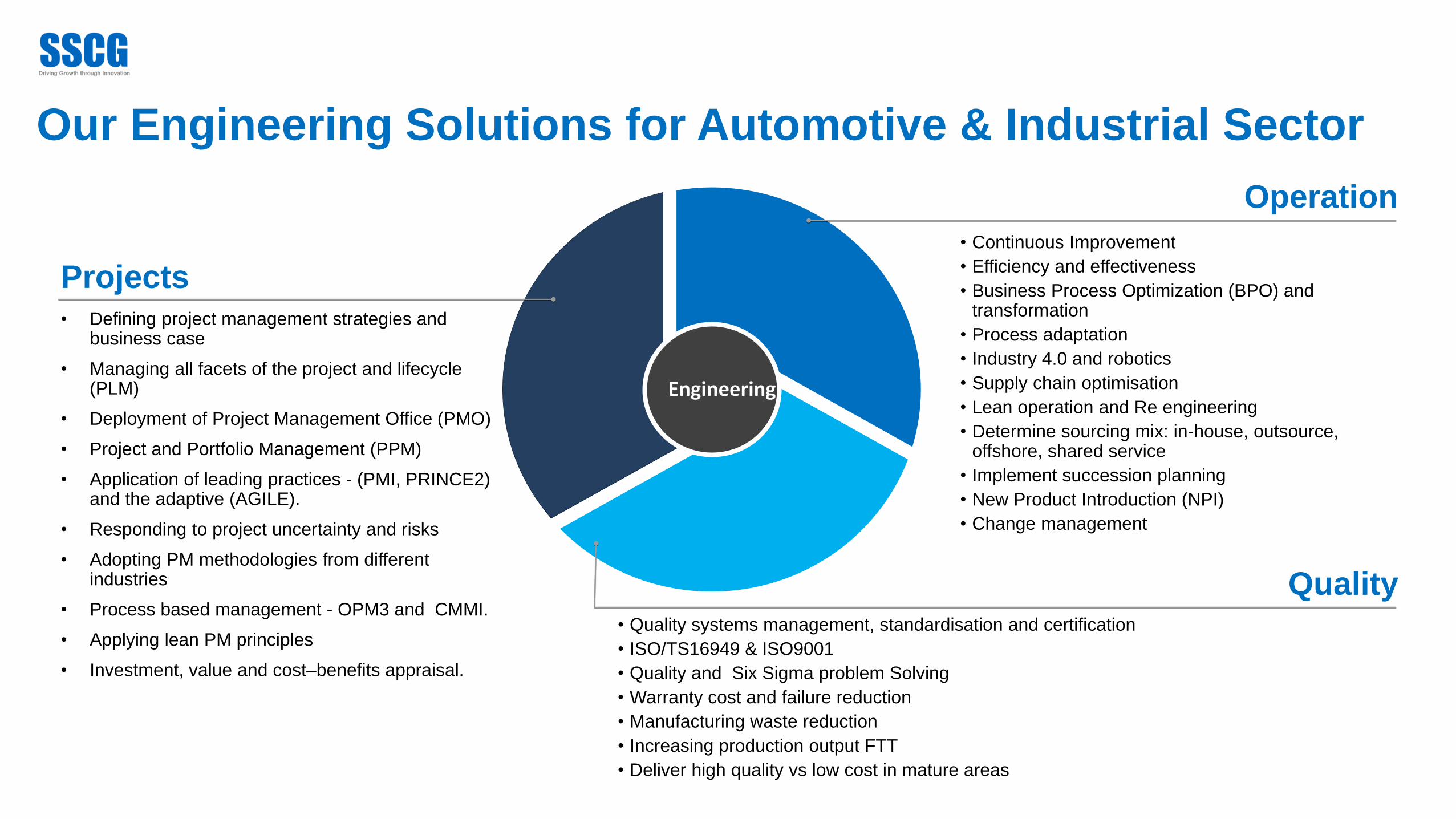

Engineering

Quality

Operation

Projects

• Continuous Improvement

• Efficiency and effectiveness

• Business Process Optimization (BPO) and transformation

• Process adaptation

• Industry 4.0 and robotics

• Supply chain optimisation

• Lean operation and Re engineering

• Determine sourcing mix: in-house, outsource, offshore, shared service

• Implement succession planning

• New Product Introduction (NPI)

• Change management

• Quality systems management, standardisation and certification

• ISO/TS16949 & ISO9001

• Quality and Six Sigma problem Solving

• Warranty cost and failure reduction

• Manufacturing waste reduction

• Increasing production output FTT

• Deliver high quality vs low cost in mature areas

• Defining project management strategies and business case

• Managing all facets of the project and lifecycle (PLM)

• Deployment of Project Management Office (PMO)

• Project and Portfolio Management (PPM)

• Application of leading practices - (PMI, PRINCE2) and the adaptive (AGILE).

• Responding to project uncertainty and risks

• Adopting PM methodologies from different industries

• Process based management - OPM3 and CMMI.

• Applying lean PM principles

• Investment, value and cost–benefits appraisal.

Our Engineering Solutions for Automotive & Industrial Sector

2 4

Customized Automotive and Industrial Landscape S

SC

G A

uto

mo

tive &

In

du

str

ial

Vehicle

Control & Driving

Technologies

Certification & Homologation

Powertrain

Manufacturing & Assembly

Quality

Platforms

Processes

Operations

Supply Chain

Technologies

Mobility

Connected Cars

Autonomous Driving

Economy, Design & Performance Technologies

Drivelines

Engines

Electrification & Hybridisation

Competitiveness Benchmarking

Market Intelligence Insights & Perspectives

O.E.M

Established Market Incumbent Leaders New Innovative and Disruptive Entrants

Mercedes

VW Audi

BMW

GM

Ford

Toyota

Nissan

Honda

Peugeot Citreon

Mitsubishi

Kia Hyundai

Jaguar Landrover

Volvo

Subaru

Tesla

Lucid

SSCG’s dedicated Automotive and industrial sector work with major OEMs and focuses on global auto industry trends to offer leading-edge solutions, insights and

perspectives. To help our clients navigate changes, improve operational performance capabilities, streamline processes and deploy latest technologies to enhance growth,

competitiveness and reduce risks.

Market Intelligence Insights & Perspectives

Market Intelligence

& Insights

Economic and Market

Opportunities

Risks

Future

Structure Key Areas

Economic landscape and financial performance

Market development, growth and technologies

Disruption, issues, threats and challenges

Growth strategies, solutions and best practices

Industry landscape, shift, disruptions, revolution, risks and regulations.

Global Auto Industry Market Outlook

Market outlook, industry development, key growth opportunities and risks

African Auto Industry Market Outlook

Control technologies, IC engines development, EV & FCV cars and market

Powertrain Technologies & Revolution

Market development, competition, analytics, process and technologies

Supply Chain Evolution & Dynamics

Technology evolution, cyber security and market development

Connected & Autonomous Cars

Lean, quality, technologies smart manufacturing, industries 4.0 and robotics

Automotive Manufacturing & Assembly

Strategy, product design, projects, contracts, quality & six sigma solutioning

Engineering Management & Transformation

Consumers, competitors, markets, and business models are driving change

Global Mobility Evolution & Shift

Cli

en

t S

olu

tio

ns

SSCG

Market perspectives and insights on emerging trends and developments in the Automotive sector to help you understand key issues, development dynamics, evolution,

growth trends, technological advancement , innovation and changing regulations.

CO

MP

AN

Y N

AM

E

How we can help your business

optimise processes, capabilities and

reduce risks

1 - Define – Work with you to understand strategic and

operation issues you are experiencing, scope, requirements

and expectations. Complete organisation environment and

process analysis to understand current business context.

2 - Solutions Architecture - Work with you to

device transformation solutions, improvements or to identify

growth opportunities. Consult with you throughout to ensure

our solutions address your needs. Device deployment

framework and timeframe to suit your needs, budget and

delivery time.

3 - Deploy and transform - Work with you to

deploy solutions or change effectively and efficiently.

4 - Continuous Improvement - Performance assessment of impact and realignment where

necessary. Support you to device continuous improvement

actions.

5 - Monitoring and Control – Work with you

to prepare handover and transfer ownership. Develop risk

management plan

How we can help your business optimise processes, capabilities and reduce risks

SSCG Market Intelligence Insights & Perspectives: Profiling African Auto Industry - Perspective on Current State and Growth Potential All Rights Reserved @ 2017

Advisory | Consulting | Engineering

About SSCG SSCG is global management consulting and professional firm. We provide engineering and management

advisory across business services, automotive, industrial manufacturing and emerging markets sectors.

We provide informed perspective on the issues faced by our clients. The insights and quality solutions

delivered to support our clients to build trust and confidence in the markets and in economies. We combines

our multi-disciplinary approach with deep, practical industry knowledge to support our clients meet market

dynamic challenges and respond to opportunities.

W: www.s-scg.com

@ SSCG Copyright 2017, All Rights Reserved