ageas - full year 2016 results

TRANSCRIPT

Periodical Financial Information

FY 2016RESULTS

Table of contents Slides used during analyst call 2

Segment information 18

Equity / Solvency 49

Investment portfolio 58

Legal Settlement 63

General Information 68

Main messagesGood operating performance across most segments - negative exceptionals in UK

3Periodic financial Information I FY 16 results I 15 February 2017

*Consolidated entities only

Insurance

performance

Group result

Balance sheet

Gross dividend

Fortis settlement

Insurance net profit of EUR 821 mio (+9%) – Q4 at EUR 18 mio

Inflow @ 100% of EUR 31.7 bn (+6%) – Q4 at EUR 7.0 bn

Life Guaranteed margin at 93 bps* (vs.90 bps) – Q4 at 80 bps

Group combined ratio at 98.7%* (vs.96.9%) – Q4 at EUR 103.7%

Life Technical Liabilities at EUR 74.5 bn* (+1% vs. YE 2015)

Group net profit of EUR 127 mio – Q4 profit of EUR 9 mio

General Account net loss of EUR 694 mio as result of provision for

Fortis settlement – Q4 loss of EUR 8 mio

Shareholders’ equity at EUR 9.7 bn or EUR 47.03 per share

UG/L at EUR 2.5 bn or EUR 12.03 per share

Insurance Solvency IIageas at 182%, Group ratio at 195%

Total Liquid Assets General Account at EUR 1.9 bn (vs.EUR 1.6 bn)

Proposal of 2.10 EUR/share – incl. 0.40 EUR related to cap gain HK

Hearing Amsterdam Court on 24 March 2017

Judgment on binding character expected by mid 2017

199

573

505

182

118755

821

FY 15 FY 16

cap gain AICA Life Non-Life

In EUR mio In EUR bn

Non-Life combined ratio incl. 4.9 pp terrorism, weather & UK one-offs

Inflows*: strong Life growth in Asia & BelgiumIn EUR bn

Total Insurance: HeadlinesGood operating performance across most segments – UK result including one-off items

4Periodic financial Information I FY 16 results I 15 February 2017

Operating margin Guaranteed up on cap gains on Real Estate in BE

Operating margin Unit-Linked down on divestment HK

In bps avg technical liabilities In bps avg technical liabilities

* incl. non-consolidated partnerships @ 100%

In % NEP

Net result: Q4 including EUR 137 mioexceptionals in UK & Asia

Life Technical liabilities up – impact sale Hong Kong EUR 3.2 bn

147

81

(5)(63)

142

18

Q4 15 Q4 16

23.5 25.4

6.36.3

29.831.7

FY 15 FY 16

Life Non-Life

5.6 5.5

1.5 1.5

7.0 7.0

Q4 15 Q4 16

96.9 98.7

FY 15 FY 16

102.1 103.7

Q4 15 Q4 16

90 93

FY 15 FY 16

119

80

Q4 15 Q4 16

3625

FY 15 FY 16

35 36

Q4 15 Q4 16

74.1 75.3 74.5

61.166.4 69.5

135.2141.6 144.0

FY 15 9M 16 FY 16

conso non-conso

10/03/2010 I page 5

Overview of net realised capital gains* on investmentsSupport of cap gains substantially lower in Asia

5Periodic financial Information I FY 16 results I 15 February 2017

* Net capital gains include capital gains, impairment & related changes in profit sharing, net of tax & @ ageas’s part –

CEU JV’s not included

EUR mio FY 15 FY 16 Q4 15 Q4 16

Life 75 76 41 (4) Comparable impact on FY basis

Non-Life (1) 9 (4) (3) cap gains on RE in H1 2016

Total Belgium 75 85 37 (7) impairments in Q4 2016

Non-Life 9 10 2 0

Total UK 9 10 2 0

Life (7) (4) (4) 1

Non-Life 1 1 0 0 Downward equity movements

Total CEU (6) (4) (4) 2

Life 107 (8) 37 (19) Exceptionally high level of

Non-Life (1) 3 0 cap gains in 2015

Total Asia 107 (5) 37 (19) Equity impairments in Q4 2016

Life 175 64 73 (22)

Non-Life 9 22 (2) (2)

Total Ageas 183 86 71 (24)

456

188

391

197

(313)

188

624

270

654

309

737

329

755

338

821

423

2010 2011 2012 2013 2014 2015 2016 2017

6Periodic financial Information I FY 16 results I 15 February 2017

Proposed gross cash dividend of EUR 2.10 / share EUR 0.4/share related to sale Hong Kong – total 3.7 bn returned to shareholders since 2009

* calculation based on day before dividend declaration

** 45% pay-out ratio on insurance net result excluding UK exceptionals

Dividend distributed duringbased on

Net result of the year before

**

since '09

gross dividend / share 0.80 0.80 0.80 1.20 1.40 1.55 1.65 1.70 9.90

additional dividend / share 0.40 0.40

pay-out ratio 41% 50% - 43% 47% 45% 45% 52%

dividend yield* 2.9% 3.7% 4.7% 4.6% 4.4% 5.0% 4.9% 5.3%

Paid dividend 188 197 188 270 309 329 338 423 2,242

Share buy-back executed 230 160 144 209 250 244 40 1,277

Capital reduction 223 223

Total returned to shareholders 188 427 348 637 518 579 582 463 3,743

Belgium268

Belgium168

Belgium294

Belgium333

UK 23

UK 82

UK 64

UK 50

UK 47

CEU 7

CEU 36

CEU150

CEU 53 CEU 19

Asia 12

Asia 52

Asia106 Asia 43

Asia89

42

438

488

440

487

2012 2013 2014 2015 2016

7

Disciplined cash upstream from operating companiesConsistent average upstream of ≈ EUR 450 mio per annum since Vision 2015

Belgium main contributor of cash

Upstream covering dividend & holding costs on FY basis

On top of these amounts ≈ EUR 430 mio upstream linked

to capital optimization in 2013 & 2014

In EUR mio

Biggest part

of upstream

done in H1

Italy 10

9

Malaysia17

Thailand11

China61

Upstream duringbased on net result of the year before

Periodic financial Information I FY 16 results I 15 February 2017

Luxembourg

* internal loan granted

*

*

3.8 4.2

1.91.9

5.76.1

FY 15 FY 16

Life Non-Life

9955

21

26

120

82

Q4 15 Q4 16

In bps avg technical liabilities In bps avg technical liabilitiesIn % NEP

8Periodic financial Information I FY 16 results I 15 February 2017

In EUR mio In EUR bn In EUR bn

281 288

103 102

384 391

FY 15 FY 16

Life Non-Life

1.1 1.0

0.4 0.4

1.5 1.5

Q4 15 Q4 16

56.3 59.8 59.0

FY 15 9M 16 FY 16

86 86

FY 15 FY 16

94.7 96.0

FY 15 FY 16

96.2 92.8

Q4 15 Q4 16

27

64

Q4 15 Q4 16

32 31

FY 15 FY 16

131

70

Q4 15 Q4 16

Belgium : HeadlinesNet profit up despite adverse impact terrorism & weather events

Net result slightly up - Q4 lower on less realised capital gains

Inflows: growth driven by Life short term investment products - levelled off in Q4

Life Technical liabilities up 5%

Non-Life combined ratio 93.9% when excluding terrorism - excellent in Q4

Operating margin Guaranteed: cap gains spread differently over quarters

Operating margin Unit-Linked almost stable

102.1 106.0

FY 15 FY 16

In EUR mio

9Periodic financial Information I FY 16 results I 15 February 2017

In % of NEPIn EUR bn

* incl. non-consolidated partnerships @ 100%

30

(56)

FY 15 FY 16

(35)

(110)

Q4 15 Q4 16

112.9

126.3

Q4 15 Q4 16

2.5 2.2

FY 15 FY 16

0.60.5

Q4 15 Q4 16

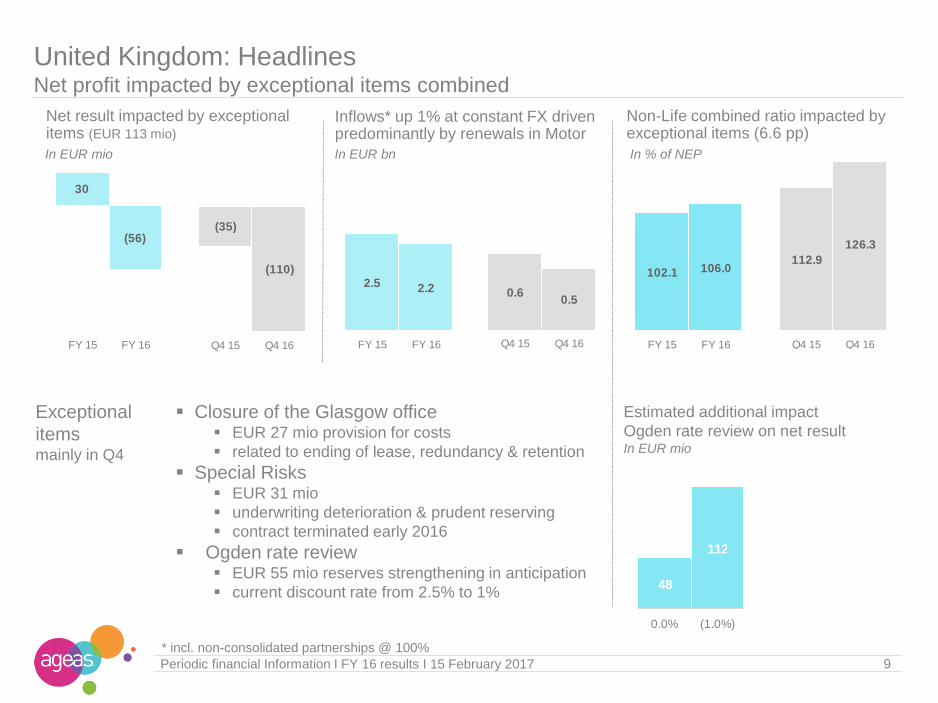

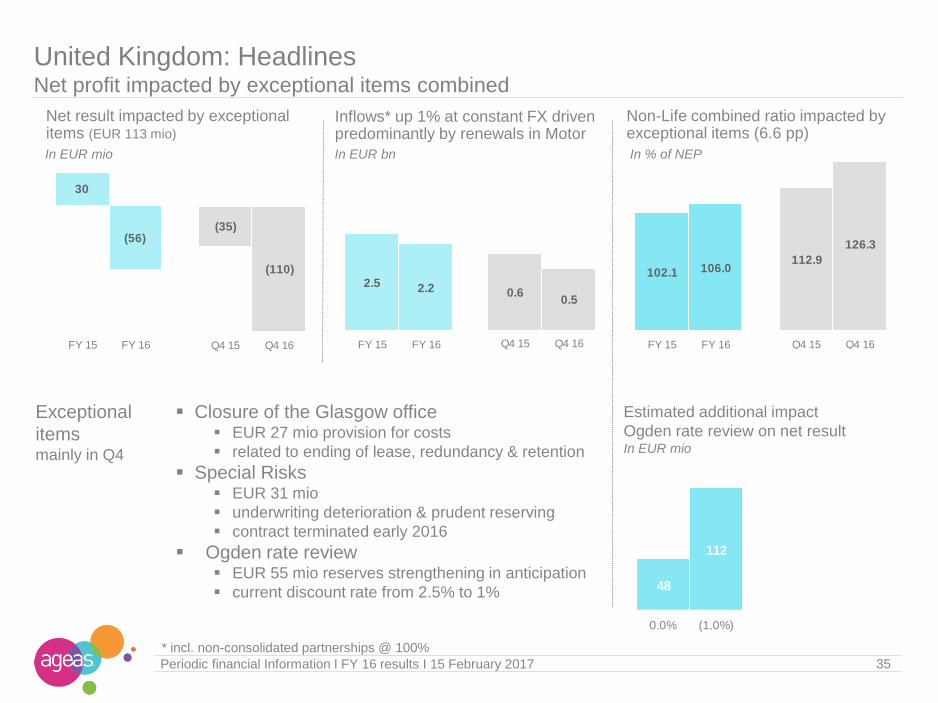

United Kingdom: HeadlinesNet profit impacted by exceptional items combined

Net result impacted by exceptional items (EUR 113 mio)

Inflows* up 1% at constant FX driven predominantly by renewals in Motor

Non-Life combined ratio impacted byexceptional items (6.6 pp)

Estimated additional impact

Ogden rate review on net resultIn EUR mio

Closure of the Glasgow office EUR 27 mio provision for costs

related to ending of lease, redundancy & retention

Special Risks EUR 31 mio

underwriting deterioration & prudent reserving

contract terminated early 2016

Ogden rate review EUR 55 mio reserves strengthening in anticipation

current discount rate from 2.5% to 1%

Exceptional

itemsmainly in Q4

48

112

0.0% (1.0%)

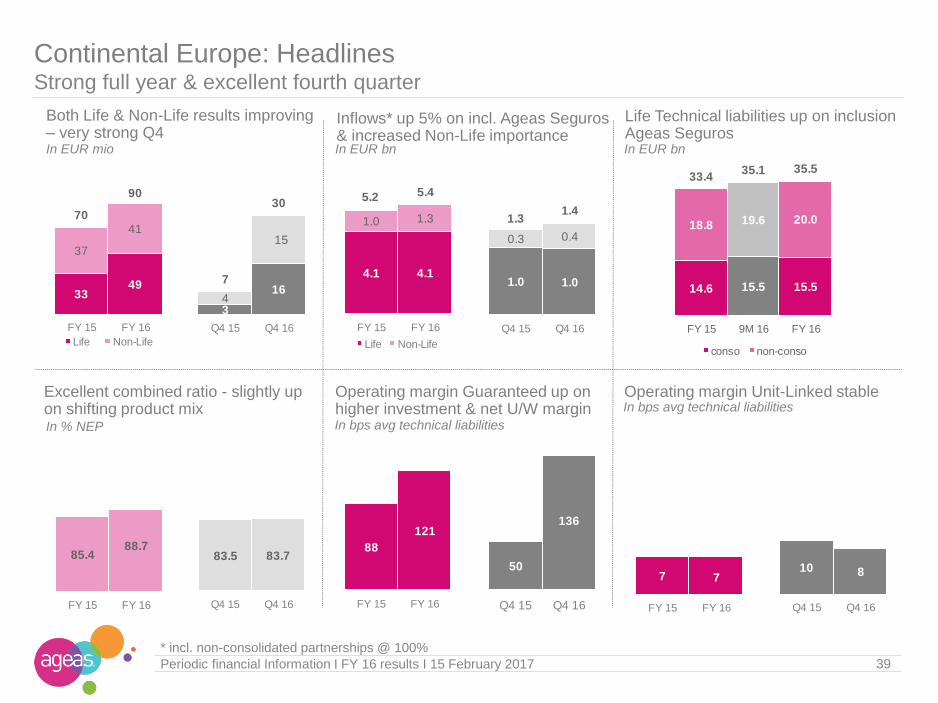

Both Life & Non-Life results improving – very strong Q4In EUR mio In EUR bn

Excellent combined ratio - slightly up on shifting product mix

Inflows* up 5% on incl. Ageas Seguros& increased Non-Life importance

In EUR bn

Continental Europe: Headlines Strong full year & excellent fourth quarter

Operating margin Guaranteed up on higher investment & net U/W margin

10Periodic financial Information I FY 16 results I 15 February 2017

Life Technical liabilities up on inclusion Ageas Seguros

Operating margin Unit-Linked stable

In % NEP

* incl. non-consolidated partnerships @ 100%

3349

37

4170

90

FY 15 FY 16

Life Non-Life

3

164

15

7

30

Q4 15 Q4 16

4.1 4.1

1.0 1.3

5.2 5.4

FY 15 FY 16

Life Non-Life

1.0 1.0

0.3 0.4

1.31.4

Q4 15 Q4 16

14.6 15.5 15.5

18.8 19.6 20.0

33.435.1 35.5

FY 15 9M 16 FY 16

conso non-conso

85.488.7

FY 15 FY 16

83.5 83.7

Q4 15 Q4 16

88

121

FY 15 FY 16

50

136

Q4 15 Q4 16

7 7

FY 15 FY 16

10 8

Q4 15 Q4 16

In bps avg technical liabilities

In bps avg technical liabilities

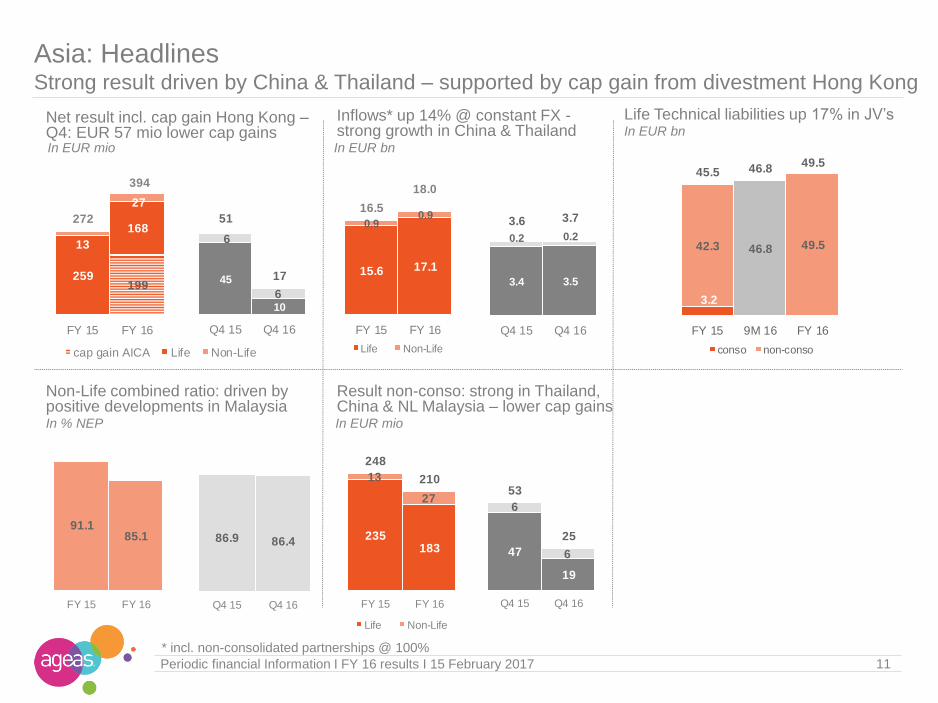

Net result incl. cap gain Hong Kong –Q4: EUR 57 mio lower cap gainsIn EUR mio In EUR bn

Non-Life combined ratio: driven by positive developments in Malaysia

Inflows* up 14% @ constant FX -strong growth in China & Thailand

Life Technical liabilities up 17% in JV’sIn EUR bn

Asia: Headlines Strong result driven by China & Thailand – supported by cap gain from divestment Hong Kong

11Periodic financial Information I FY 16 results I 15 February 2017

In EUR mio

Result non-conso: strong in Thailand, China & NL Malaysia – lower cap gains

In % NEP

* incl. non-consolidated partnerships @ 100%

199259

168

13

27

272

394

FY 15 FY 16

cap gain AICA Life Non-Life

15.6 17.1

0.90.9

16.5

18.0

FY 15 FY 16

Life Non-Life

3.4 3.5

0.2 0.2

3.6 3.7

Q4 15 Q4 16

45

10

6

6

51

17

Q4 15 Q4 16

3.2

42.3 46.8 49.5

45.5 46.849.5

FY 15 9M 16 FY 16

conso non-conso

235183

13

27

248

210

FY 15 FY 16

Life Non-Life

86.9 86.4

Q4 15 Q4 16

91.185.1

FY 15 FY 16

47

19

6

6

53

25

Q4 15 Q4 16

In EUR mio

12Periodic financial Information I FY 16 results I 15 February 2017

In % NEPIn EUR mio

Intreas: HeadlinesInternal Non-Life reinsurance company established in July 2015

Net result Inflows Combined ratio

0 0

3

FY 15 FY 16

0 (1)

Q4 15 Q4 16

41

FY 15 FY 16

9

Q4 15 Q4 16

86.1

FY 15 FY 16

334.4

Q4 15 Q4 16

0 0 0

Result Q4 lower on revaluation RPN(i)In EUR mio

Accounting value of remaining legacies

General Account: Headlines Impacted by cap gain on sale of Hong Kong, Fortis settlement & revaluation RPN(i) liability

13Periodic financial Information I FY 16 results I 15 February 2017

Total liquid assets up on sale HK –EUR 0.8 bn ring-fenced for settlement

In EUR mioImpact on P&L from RPN(i) Staff & Operating expenses up on one-

offs (legal settlement & HR related)

In EUR mio In EUR bn

In EUR mio

In EUR mio

Accounting value on AG Insurance put option: up driven by higher multiples

15

(694)

FY 15 FY 16

29

(8)

Q4 15 Q4 16

1.3

1.8 1.8

0.3

0.2 0.21.6

2.0 1.9

FY 15 9M 16 FY 16

net cash liquid assets

(402)(295) (275)

41 41 42

(133)

(1,019) (1,024)

FY 15 9M 16 FY 16

RPN(i) RPI Settlement

(1,064) (1,083)(1,266)

FY 15 9M 16 FY 16

1732

53

63

70

95

FY 15 FY 16

Staff & Intercompany Operating

4 9

15 14

1923

Q4 15 Q4 16

65 83

FY 15 FY 16

43

20

Q4 15 Q4 16

14Periodic financial Information I FY 16 results I 15 February 2017

Shareholders’ equity at EUR 9.7 bn - UG/L of EUR 12.03/shareDown on legal settlement, financial market, put option & return to shareholders

In EUR mio

7,0956,554

2,952

2,498

1,330

604

821

(694)(484)

(338) (244)(289)

(430)(57) (4)

EUR 53.59 EUR 47.03

11,376

9,656

FY 15 ResultInsurance

ResultGen Acc

ChangeUG/L

Dividend TreasuryShares

Reval AGput option

Forex IAS 19 Other FY 16

InsuranceUCG/L Insurance

UCG/L

Shareholders’

equity per

segment

Shareholders’

equity per share

FY 15 FY 16 FY 15 FY 16

Belgium 4,932 ► 4,683 Asia 3,009 ► 2,004

UK 1,129 ► 911 Reinsurance 104

Continental Europe 977 ► 1,350 Insurance 10,047 ► 9,052

General Account 1,330 ► 604

2.9 2.8

0.8 0.7 0.7 0.90.3 0.0

(0.3) (0.3)

4.4 4.2

0.0 0.1

4.4 4.2

0.71.6

6.9 6.9

1.10.8 0.9 1.2

0.60.1 (1.5)(1.5)

8.07.6

1.4

0.7

9.4

8.3

1.8

4.3

FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16

15Periodic financial Information I FY 16 results I 15 February 2017

Solvency IIageasImpact from exceptional items in UK compensated by Belgium & CEU

Solvency IIageas

in %

In EUR bn

Own Funds

SCR

Non EU

Non-controlled

participations*

Insurance ratio remains stable

Group ratio influenced by legal settlement & increasing put option liability

Expected dividend deducted

242% 244% 130% 120% 131% 127% 179% - - 278% 182% 182% 212% 195% 253% 264%

Belgium UK CEU Asia Reins. Diversification Insurance GA Group

Non-transferable

* Based on local solvency requirements

1. 2016 was remarkable & good year for Ageas &

last week’s news on UK did not change that

2. Settlement agreement big milestone

3. Further structural improvement of earnings in most segments

4. Proposed gross dividend as a sign of comfort with respect to

the financial health of Ageas

Table of contents Slides used during analyst call 2

Segment information 18

Equity / Solvency 49

Investment portfolio 58

Legal Settlement 63

General Information 68

Non-Life combined ratio – 4.9 pp exceptional items

Solvency II ageas – comfortably above 175%

Ambition 2018 targetsReaching 4 targets out of 6

19Periodic financial Information I FY 16 results I 15 February 2017

Operating margin Guaranteed above target range

Operating margin Unit-Linked far below target range

* Calculated on insurance net result excluding UK exceptionals – 52% pay-out ratio on total Insurance result

ROE – ROE excl Hong Kong @ 9.6% Proposed gross dividend in line with promised pay-out ratio*

11% 12%

11% - 13%

2015 2016 target

96.9 98.7

97 %

2015 2016 target

90 93

85 - 90 bps

2015 2016 target

45% 45%

40% - 50%

2015 2016 target

3625

40 - 45 bps

2015 2016 target

182% 181%

175%

2015 2016 target

Periodic financial Information I FY 16 results I 15 February 2017 20

Key financials

In EUR mio FY 15 FY 16 Q4 15 Q4 16

Gross inflows 29,792 31,654 6% 7,023 6,962 (1%)

Net result Insurance 755 821 9% 142 18 (87%)

By segment: - Belgium 384 391 2% 120 82 (32%)

- UK 30 (56) (290%) (35) (110) 213%

- Continental Europe 70 90 28% 7 30 330%

- Asia 272 394 45% 50 17 (67%)

- Reinsurance 0 3 0 (1)By type: - Life 573 704 23% 147 81 (45%)

- Non-Life 182 118 (36%) (5) (63) 1164%

Net result General Account 15 (694) 29 (8) (129%)

Net result Ageas 770 127 171 9 (95%)

Earnings per share (in EUR) 3.57 0.61

Life Operating Margin Guaranteed (in bps) 90 93 119 80

Life Operating Margin Unit-Linked (in bps) 36 25 35 36

Combined ratio (in %) 96.9 98.7 102.1 103.7

FY 15 FY 16

Shareholders' equity 11,376 9,656 (15%)

Net equity per share (in EUR) 53.59 47.03

Insurance ROE excl.UG/L 11.0% 12.0%

Insurance Solvency IIageas ratio 182% 182%

For a definition see Lexicon in annex to the press release

199

573

505

182

118755

821

FY 15 FY 16

cap gain AICA Life Non-Life

In EUR mio In EUR bn

Non-Life combined ratio incl. 4.9 pp terrorism, weather & UK one-offs

Inflows*: strong Life growth in Asia & BelgiumIn EUR bn

Total Insurance: HeadlinesGood operating performance across most segments – UK result including one-off items

21Periodic financial Information I FY 16 results I 15 February 2017

Operating margin Guaranteed up on cap gains on Real Estate in BE

Operating margin Unit-Linked down on divestment HK

In bps avg technical liabilities In bps avg technical liabilities

* incl. non-consolidated partnerships @ 100%

In % NEP

Net result: Q4 including EUR 137 mioexceptionals in UK & Asia

Life Technical liabilities up – impact sale Hong Kong EUR 3.2 bn

147

81

(5)(63)

142

18

Q4 15 Q4 16

23.5 25.4

6.36.3

29.831.7

FY 15 FY 16

Life Non-Life

5.6 5.5

1.5 1.5

7.0 7.0

Q4 15 Q4 16

96.9 98.7

FY 15 FY 16

102.1 103.7

Q4 15 Q4 16

90 93

FY 15 FY 16

119

80

Q4 15 Q4 16

3625

FY 15 FY 16

35 36

Q4 15 Q4 16

74.1 75.3 74.5

61.166.4 69.5

135.2141.6 144.0

FY 15 9M 16 FY 16

conso non-conso

Inflows @ 100% Growth driven by Asian & Belgian Life & inclusion Ageas Seguros – 4% negative FX

22Periodic financial Information I FY 16 results I 15 February 2017

EUR mio FY 15 FY 16 FY 15 FY 16 FY 15 FY 16

Belgium 75% 3,799 4,182 10% 1,881 1,883 0% 5,679 6,065 7%

United Kingdom - 2,457 2,203 (10%) 2,457 2,203 (10%)

Consolidated entities 100% - 1,905 1,720 (10%) 1,905 1,720 (10%)

Non-consolidated JV's 552 483 (12%) 552 483 (12%)0 0

Continental Europe 4,109 4,122 0% 1,048 1,307 25% 5,157 5,429 5%

Consolidated entities 2,013 1,903 (5%) 512 740 44% 2,526 2,643 5%

Portugal 51% - 100% 1,533 1,497 (2%) 293 513 75% 1,826 2,010 10%

France 100% 480 406 (15%) 480 406 (15%)

Italy 50% 219 227 3% 219 227 3%

Non-consolidated JV's 2,096 2,219 6% 536 567 6% 2,632 2,786 6%

Turkey 36% 536 567 6% 536 567 6%

Luxembourg 33% 2,096 2,219 6% 2,096 2,219 6%

Asia 15,585 17,064 9% 913 893 (2%) 16,498 17,957 9%

Consolidated entities 100% 557 183 (67%) 557 183 (67%)

Non-consolidated JV's 15,028 16,881 12% 913 893 (2%) 15,941 17,774 11%

Malaysia 31% 571 587 3% 615 575 (7%) 1,186 1,162 (2%)

Thailand 31%-15% 2,311 2,485 8% 298 318 7% 2,609 2,803 7%

China 25% 11,966 13,611 14% 11,966 13,611 14%

Philippines 50% 0 5 0 5 Vietnam 32% 0 0 0 0 India 26% 180 193 7% 180 193 7%

Insurance Ageas 23,493 25,368 8% 6,299 6,286 (0%) 29,792 31,654 6%#DIV/0! ###### ######

Consolidated entities 6,369 6,269 (2%) 4,298 4,342 1% 10,667 10,611 (1%)

Non-consolidated JV's 17,124 19,100 12% 2,001 1,943 (3%) 19,125 21,043 10%

Reinsurance 0 41 0 41

Life Non-Life Total

Inflows @ Ageas’s partStrong growth in Asian JV’s & Guaranteed Life in Belgium

In EUR mio

23Periodic financial Information I FY 16 results I 15 February 2017

2,849 3,137 1,961 1,953

4,474 4,574

9,283 9,663

0

1,410 1,412

2,181 1,962

596 831

235 225

4,422 4,430

7%

(10%)

9%

2%

3%

4,259 4,549

2,556 2,783

4,708 4,799

13,705 14,093

0 41

FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16

Up 7% @ constant FX

UK up 2% @ constant FX - Asia: up 7% @ constant FX

Belgium: sales Savings products up in H1 – growth stopped in Q4

CEU: Ageas Seguros contributing

EUR 89 mio in Life / EUR 191 mio in Non-Life

Non-Life

Life

Belgium UK CEU Asia Insurance Reins.

Insurance net resultHit by one-off charges in UK

24Periodic financial Information I FY 16 results I 15 February 2017

BE: Solid Life & Non-Life performance - net cap gains up EUR 10 mio, mainly RE – EUR 47 mio negative from terrorism & weather

UK: EUR 113 mio one-off charges for restructuring & reserves strengthening

CEU: Good operating performance - transformation plan Seguros on track

Asia: Improved performance mainly in China & Thailand - Hong Kong& equity impairments vs. exceptional investment result in 2015

Non-Life

Life

Belgium UK CEU Asia Reins. Insurance

In EUR mio

281 288

33 49

259

367

573

704 103 102

3741

13

27

182

118

384 391

30 (56)

70 90

272

394

0 3

755

821

FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16

25Periodic financial Information I FY 16 results I 15 February 2017

Insurance Combined ratio Combined ratio hit by terrorism, weather & reserves strengthening in UK

Combined ratio

Brussels terrorism events impacting for 0.9 pp -

mainly in Other lines and Accident & Health

Weather events in Belgium & UK increasing COR

with 1.7 pp (vs. 1.8 pp in 2015)

Provision strengthening for Special Risks & Ogden

in UK impacting for 2.3 pp

Q4 Combined ratio

Increase on one-off charges in UK (8.2 pp)

somewhat mitigated by excellent combined ratio in

BE (92.8%) & CEU (83.7%)

Claims ratio

CY claims ratio at 69.4% (vs. 68.1%) – 3.9 pp

impact from exceptional items

PY claims ratio flattening out over the year – 1 pp

impact Ogden

Expense ratio

Down on commissions in UK

Net earned premium (In EUR mio)

In % Net earned premium

73.2 69.0 68.1 64.3 64.4 62.2 64.6 68.2 69.4

32.831.1 31.0 34.0 35.2

34.7 34.133.9 34.3

106.0100.1 99.1 98.3 99.6

96.9 98.7102.1 103.7

(3.7) (3.5) (3.1) (3.8) (4.0) (5.9) (4.8) (3.5)(0.8)

2010 2011 2012 2013 2014 2015 2016 Q4 15 Q4 16

claims ratio expense ratio PY claims ratio

2,858 3,507 4,178 3,749 3,843 4,038 4,112 1,027 1,034

42.9

67.2 66.5 62.471.2

57.9 60.4

41.2

44.8 44.9 45.5

50.6

46.4 44.4

84.1

112.0 111.4 107.9

121.8

104.3 104.8

2010 2011 2012 2013 2014 2015 2016

75.061.9 55.6 51.5 51.5 50.4 50.5

43.2

41.541.6 44.0 44.6 41.6 42.7

118.2

103.497.2 95.5 96.1 92.0 93.2

2010 2011 2012 2013 2014 2015 2016

74.3 71.9 70.5 70.0 67.3 65.4 67.5

24.8 25.0 25.5 25.6 27.0 28.3 27.2

99.1 96.9 96.0 95.6 94.3 93.7 94.7

2010 2011 2012 2013 2014 2015 2016

78.4 72.0 73.6 69.8 69.6 69.1 72.6

29.025.3 25.4 29.3 29.7 30.5 29.8

107.497.3 99.0 99.1 99.3 99.6 102.4

2010 2011 2012 2013 2014 2015 2016

Insurance Combined ratio per product lineExceptional items impacting COR

26Periodic financial Information I FY 16 results I 15 February 2017

NEP 714 736 763 813 813 811 838 NEP 1,134 1,571 2,058 1,557 1,616 1,724 1,790

NEP 750 892 1,007 986 1,029 1,078 1,067 NEP 261 308 349 394 385 424 418

Motor: improvement in CEU – 3.0 pp Ogden in UKAccident & Health: 2.0 pp terrorism (Worker’s Comp.)

Other: 4.0 pp terrorism BE & 9.4 pp impact UKHousehold: 6.8 pp impact weather events in BE & UK

In bps Avg techn. liabilities

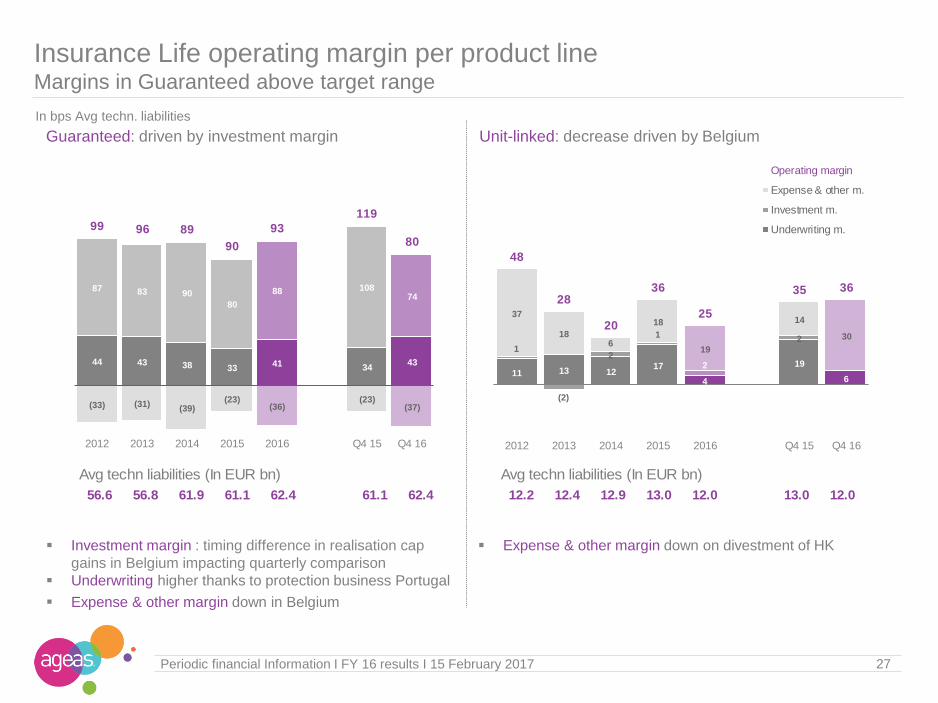

Insurance Life operating margin per product lineMargins in Guaranteed above target range

Guaranteed: driven by investment margin Unit-linked: decrease driven by Belgium

Expense & other margin down on divestment of HK Investment margin : timing difference in realisation cap

gains in Belgium impacting quarterly comparison

Underwriting higher thanks to protection business Portugal

Expense & other margin down in Belgium

27Periodic financial Information I FY 16 results I 15 February 2017

Avg techn liabilities (In EUR bn)

56.6 56.8 61.9 61.1 62.4 61.1 62.4

Avg techn liabilities (In EUR bn)

12.2 12.4 12.9 13.0 12.0 13.0 12.0

44 43 38 3341 34

43

87 83 90

80

88 10874

(33) (31)(39)

(23)(36)

(23)(37)

99 96 89

90

93

119

80

2012 2013 2014 2015 2016 Q4 15 Q4 16

11 13 1217

4

19

6

1

(2)

2

1

2

2

37

186

18

19

14

30

48

28

20

36

25

35 36

2012 2013 2014 2015 2016 Q4 15 Q4 16

Operating margin

Expense & other m.

Investment m.

Underwriting m.

3.8 4.2

1.91.9

5.76.1

FY 15 FY 16

Life Non-Life

9955

21

26

120

82

Q4 15 Q4 16

In bps avg technical liabilities In bps avg technical liabilitiesIn % NEP

28Periodic financial Information I FY 16 results I 15 February 2017

In EUR mio In EUR bn In EUR bn

281 288

103 102

384 391

FY 15 FY 16

Life Non-Life

1.1 1.0

0.4 0.4

1.5 1.5

Q4 15 Q4 16

56.3 59.8 59.0

FY 15 9M 16 FY 16

86 86

FY 15 FY 16

94.7 96.0

FY 15 FY 16

96.2 92.8

Q4 15 Q4 16

27

64

Q4 15 Q4 16

32 31

FY 15 FY 16

131

70

Q4 15 Q4 16

Belgium : HeadlinesNet profit up despite adverse impact terrorism & weather events

Net result slightly up - Q4 lower on less realised capital gains

Inflows: growth driven by Life short term investment products - levelled off in Q4

Life Technical liabilities up 5%

Non-Life combined ratio 93.9% when excluding terrorism - excellent in Q4

Operating margin Guaranteed: cap gains spread differently over quarters

Operating margin Unit-Linked almost stable

491 479

576 578

625 633

189 194

1,881 1,883

FY 15 FY 16

3,3083,779

491

404

+10%

3,7994,182

FY 15 FY 16

Life In EUR mio

Non-Life In EUR mio

29Periodic financial Information I FY 16 results I 15 February 2017

Unit-Linked

Guaranteed

Other

Household

Accident & Health

Motor

Belgium: Inflows@ 100%Guaranteed Individual Life: Strong growth driven by Life investment products

Guaranteed

Strong growth (+14%) attributable to short term investment products

thanks to attractive guarantee in comparison with alternative savings

products available in the market & despite three consecutive lowering

of guaranteed rate (1% 0.75% 0.50% 0.25 – last lowering as

from 1 November 2017))

Growth slowed down in Q4

Group Life Inflows remained stable at EUR 1.1 billion

Unit-linked

Further decrease in Individual Unit-linked (-18%) due to a lower

appetite for open funds

Technical liabilities

Up 5% vs. FY 15 to EUR 59.0 bn mainly as a consequence of lower

interest rates compared to last year

Up 2.4% when excluding shadow accounting

Household, Motor, Other stable

Accident & Health

Pruning actions in Workers’ Compensation drive inflows slightly lower

30Periodic financial Information I FY 16 results I 15 February 2017

Net earned premium (in EUR mio)

In % Net earned premium

Belgium: Combined ratio Solid operating performance with excellent Q4 combined ratio at 92.8%

Combined ratio

Impacted by

terrorism events of 22 March 2016 (2.1 pp)

adverse weather events (3.2 pp)

Q4 Combined ratio

Excellent ratio driven by solid performance of several

product lines

Claims ratio

CY ratio (66.5% vs. 64.1%) - strongly impacted by

terrorism & adverse weather events. Barring this

impact, CY claims ratio would be lower than last year

@ 61.2%.

PY ratio: in line with last year after several years of

improving reserving adequacy– high level of H1 PY

flattened over the year

Expense ratio flat

68.7 64.3 62.7 63.2 63.556.9 58.3 58.0 56.2

36.436.8 36.8 36.7 37.7

37.8 37.7 38.236.6

105.1101.1 99.5 99.9 101.2

94.7 96.0 96.292.8

(6.6) (7.3) (4.5) (3.6) (3.4)(7.2) (8.2)

(2.8)(5.7)

2010 2011 2012 2013 2014 2015 2016 Q4 15 Q4 16

claims ratio expense ratio PY claims ratio

1,541 1,601 1,698 1,785 1,815 1,832 1,836 459 462

31Periodic financial Information I FY 16 results I 15 February 2017

Belgium: Combined ratio per product lineStrong impact of the terrorism & adverse weather events

Accident & Health: strong result, despite impact terrorism

(3.5 pp - mostly in Workers’ Comp.)

Motor: somewhat higher frequency & average claims cost

Household: 9.9 pp impact terrorism & weather – good Q4 Other: 8.8 pp terrorism impact - mostly on TPL

75.8 73.8 73.0 73.7 70.1 70.4 70.0

21.9 23.8 24.0 23.8 25.4 27.6 27.6

97.7 97.6 97.0 97.5 95.5 98.0 97.6

2010 2011 2012 2013 2014 2015 2016

NEP 451 451 480 507 504 484 472 NEP 498 525 540 552 562 568 570

71.058.9 64.7 64.7 62.6 56.2 59.7

35.7

35.335.8 36.3 37.2

36.4 36.4

106.7

94.2100.5 101.0 99.8

92.6 96.1

2010 2011 2012 2013 2014 2015 2016

NEP 463 484 530 564 579 595 605

75.663.0

50.5 51.4 51.7 43.9 47.8

47.1

46.9

46.2 45.6 45.745.2 44.8

122.7

109.9

96.7 97.0 97.489.1 92.6

2010 2011 2012 2013 2014 2015 2016

10.4

58.2 65.9 66.187.5

65.8 58.350.9

49.548.1 47.2

47.6

45.044.6

61.3

107.7114.0 113.3

135.1

110.8102.9

2010 2011 2012 2013 2014 2015 2016

NEP 129 142 149 162 170 185 190

32Periodic financial Information I FY 16 results I 15 February 2017

Belgium Life operating margin per product line

Guaranteed: operating margin reaching target

Operating result at EUR 418 mio, up from EUR 413 mio

Investment margin higher cap gains in RE, especially in H1

Sum of underwriting and expense & other margin relatively

stable

Unit-linked: stable

Operating result down from EUR 20 mio to EUR 19 mio –

Q4 driven by improving risk & expense result

In bps Avg techn. liabilities

4 4

(2)

1 0 0 17

4438

32 31 3124

47

4741

30 32 31

27

64

2012 2013 2014 2015 2016 Q4 15 Q4 16

Operating margin

Investment m.

Expense & other m.

Underwriting m.

32 32 30 25 29

3

30

93 88 9588

91127 72

(29) (31) (38)(27) (34)

(21)(32)

96 89 8786

86131

70

2012 2013 2014 2015 2016 Q4 15 Q4 16

Avg techn liabilities (In EUR bn)

5.3 5.5 5.8 6.0 6.1 6.0 6.1

Avg techn liabilities (In EUR bn)

47.4 47.6 51.8 50.3 52.9 50.3 52.9

33

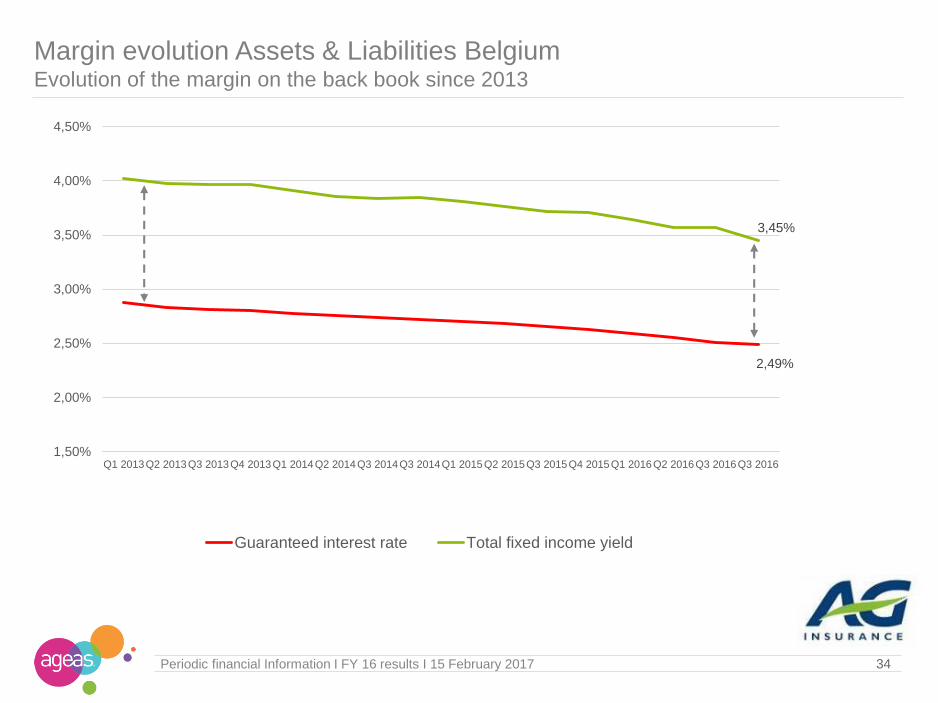

Margin evolution Assets & Liabilities BelgiumYield & guaranteed rate on back book down at the same pace

Life

Back book

FY 13 FY 14 FY 15 FY 16

Guaranteed interest rate 2.80% 2.71% 2.63% 2.49%

Fixed income yield 3.97% 3.84% 3.71% 3.45%*

Liabilities Guaranteed(EUR bn) 47.6 51.8 50.3 52.9

FY 14 FY 15 FY 16

Fixed income yield 2.89% 2.11% 1.71%

Reinvested amount (EUR bn) 4.6 4.2 4.5

New money

Life & Non-Life

Periodic financial Information I FY 16 results I 15 February 2017

* Total fixed income yield figure are as at end of August 2016

Newly invested money mostly corporate bonds, government related loans, mortgages &

infrastructure loans

>95% investment grade quality

Guaranteed retail Life:

Yield lowered from 1% to 0.75% as from 1 April 2016

Yield lowered to 0.5% as from 1 August 2016

Yield further lowered to 0.25% as from 1 November 2016

34

Margin evolution Assets & Liabilities BelgiumEvolution of the margin on the back book since 2013

Periodic financial Information I FY 16 results I 15 February 2017

2,49%

3,45%

1,50%

2,00%

2,50%

3,00%

3,50%

4,00%

4,50%

Q1 2013Q2 2013Q3 2013Q4 2013Q1 2014Q2 2014Q3 2014Q3 2014Q1 2015Q2 2015Q3 2015Q4 2015Q1 2016Q2 2016Q3 2016Q3 2016

Guaranteed interest rate Total fixed income yield

102.1 106.0

FY 15 FY 16

In EUR mio

35Periodic financial Information I FY 16 results I 15 February 2017

In % of NEPIn EUR bn

* incl. non-consolidated partnerships @ 100%

30

(56)

FY 15 FY 16

(35)

(110)

Q4 15 Q4 16

112.9

126.3

Q4 15 Q4 16

2.5 2.2

FY 15 FY 16

0.60.5

Q4 15 Q4 16

United Kingdom: HeadlinesNet profit impacted by exceptional items combined

Net result impacted by exceptional items (EUR 113 mio)

Inflows* up 1% at constant FX driven predominantly by renewals in Motor

Non-Life combined ratio impacted byexceptional items (6.6 pp)

Estimated additional impact

Ogden rate review on net resultIn EUR mio

Closure of the Glasgow office EUR 27 mio provision for costs

related to ending of lease, redundancy & retention

Special Risks EUR 31 mio

underwriting deterioration & prudent reserving

contract terminated early 2016

Ogden rate review EUR 55 mio reserves strengthening in anticipation

current discount rate from 2.5% to 1%

Exceptional

itemsmainly in Q4

48

112

0.0% (1.0%)

36Periodic financial Information I FY 16 results I 15 February 2017

* incl. non-consolidated partnerships @ 100%

Non-LifeIn EUR mio

Other

Household

Accident & Health

Motor

United Kingdom: Inflows@ 100%Inflows down 10%, impacted by adverse FX - up 1.2% at constant FX

Non-Life

Up 1.2% @ constant FX, with growth in all products except

Accident & Health

Motor up 4% @ constant FX driven by volume growth and

strong retention in H2’16 in a hardening market

Household up 4% @ constant FX as a result of the positive

impact of new deals announced earlier in the year

Other lines up 3% @ constant FX reflecting the contribution

of new commercial insurance schemes achieved this year

Accident & Health down 42% @ constant FX due to the loss

of 2 schemes71 37

1,6451,493

499

452

242

221

-10%2,457

2,203

FY 15 FY 16

37Periodic financial Information I FY 16 results I 15 February 2017

Net earned premium (In EUR mio)

Restatement for deconsolidation of Tesco Underwriting since 2013. 2015 figures restated for consolidation Non-Life & Other

In % Net earned premium

United Kingdom: Combined ratio COR impacted by reserves strengthening

Combined ratio

Impact adverse evolution Other lines (Special risks -

2.5 pp), Ogden impact (3.4 pp) & June weather (0.8

pp) vs. flood impact in 2015 (4.2 pp)

Combined ratio Tesco Underwriting 104.2% (vs.

104.4%) including 6 pp Ogden

Q4 Combined ratio

Q4’16 impacted by Special risks (8.2 pp), Ogden

reserving (14.1 pp) & higher average costs of large

Motor claims vs. Q4 ’15 hit by floods (16.6 pp) &

benefiting from very low quarterly expense ratio

Claims ratio

CY ratio (74.8% vs. 73.7%) – 4.0 pp impact

exceptional items

PY ratio: lower releases Other lines & Ogden in Motor

(2.6 pp)

Expense ratio

Expense ratio lower driven by efficiencies, reduced

marketing spend & 2016 bonus provision release

81.574.6 73.3

65.6 66.3 69.374.5

83.494.3

28.0

25.3 26.532.2 33.5

32.831.5

29.5

32.0109.5

99.9 99.8 97.8 99.8 102.1106.0

112.9

126.3

(1.1)0.1

(2.1) (4.0) (4.6) (4.4)(0.3)

(2.1)

11.0

2010 2011 2012 2013 2014 2015 2016 Q4 15 Q4 16

claims ratio expense ratio PY claims ratio

948 1,524 2,083 1,562 1,613 1,751 1,598 450 382

38Periodic financial Information I FY 16 results I 15 February 2017

Restatement for deconsolidation of Tesco Underwriting since 2013. 2015 figures restated for consolidation Non-Life & Other

United Kingdom: Combined ratio per product line

Accident & Health driven by lower volumes & higher CY Motor: Ogden provisioning 5.3 pp

Other: Special Risks deterioration & provisioning 21.1 pp

97.987.7

78.1 76.266.0

55.8 58.4

24.0

23.228.2 34.3

38.743.3 40.9

121.9110.9

106.3 110.5104.7

99.1 99.3

2010 2011 2012 2013 2014 2015 2016

82.9 79.2 77.2 71.9 74.6 75.8 81.2

23.319.5 21.3 25.0 25.1 27.2

25.6

106.298.7 98.5 96.9 99.7 103.0 106.8

2010 2011 2012 2013 2014 2015 2016

77.461.4 62.3

51.4 51.062.2 57.6

38.2

35.3 36.742.4 43.3

37.3 40.6

115.6

96.7 99.093.8 94.3

99.5 98.2

2010 2011 2012 2013 2014 2015 2016

75.1 71.6 67.7 59.8 56.0 55.373.7

30.4 39.3 42.144.4 54.3 48.6

44.9

105.5110.9 109.8

104.2110.3

103.9

118.6

2010 2011 2012 2013 2014 2015 2016

NEP 58 65 57 79 71 72 39 NEP 532 949 1,420 907 958 1,062 1,014

NEP 248 366 434 374 399 413 361 NEP 110 143 173 202 185 204 185

Household: Favourable weather vs. 2015, offset by escape of water & fire

Both Life & Non-Life results improving – very strong Q4In EUR mio In EUR bn

Excellent combined ratio - slightly up on shifting product mix

Inflows* up 5% on incl. Ageas Seguros& increased Non-Life importance

In EUR bn

Continental Europe: Headlines Strong full year & excellent fourth quarter

Operating margin Guaranteed up on higher investment & net U/W margin

39Periodic financial Information I FY 16 results I 15 February 2017

Life Technical liabilities up on inclusion Ageas Seguros

Operating margin Unit-Linked stable

In % NEP

* incl. non-consolidated partnerships @ 100%

3349

37

4170

90

FY 15 FY 16

Life Non-Life

3

164

15

7

30

Q4 15 Q4 16

4.1 4.1

1.0 1.3

5.2 5.4

FY 15 FY 16

Life Non-Life

1.0 1.0

0.3 0.4

1.31.4

Q4 15 Q4 16

14.6 15.5 15.5

18.8 19.6 20.0

33.435.1 35.5

FY 15 9M 16 FY 16

conso non-conso

85.488.7

FY 15 FY 16

83.5 83.7

Q4 15 Q4 16

88

121

FY 15 FY 16

50

136

Q4 15 Q4 16

7 7

FY 15 FY 16

10 8

Q4 15 Q4 16

In bps avg technical liabilities

In bps avg technical liabilities

2,085 2,282

2,024 1,840

+0%

4,109 4,122

FY 15 FY 16

348 417

289

473221

276191

141

+25%

1,048

1,307

FY 15 FY 16

Life In EUR mio

Non-Life In EUR mio

Continental Europe: Inflows @ 100%Higher sales in Non-Life & stable in Life

40Periodic financial Information I FY 16 results I 15 February 2017

Unit-Linked

Guaranteed

Other

Household

Accident & Health

Motor

* incl. non-consolidated partnerships @ 100%

Life

Inflows, including non-controlling interests @ 100% & Ageas Seguros,

remained stable

Consolidated inflows down 5%

Portugal: down 2% in a market decreasing by more than 25%. As

anticipated lower guaranteed sales due to continued low interest rate

environment, partially offset by a boost in Unit-Linked & inclusion of

Ageas Seguros (EUR 89 mio)

France: down 15% due to decision to sell less guaranteed business

& last year’s level of single premium being exceptionally high

Luxembourg: up 6% benefiting from strong sales to High-Net-Worth

customers

Technical liabilities

Consolidated at EUR 15.5 bn, up 6% - increase mainly related to

inclusion of Ageas Seguros

Including non-consolidated JVs @ 100%: at EUR 35.5 bn, up 6%

Non-Life

Inflows consolidated entities up 44% driven by an excellent performance

in Portugal strongly outperforming the market & inclusion of Ageas

Seguros (EUR 191 mio)

Turkey up 17% @ constant FX – strong growth in Motor (both Own

Damage & Third Partly Liability)

41Periodic financial Information I FY 16 results I 15 February 2017

Continental Europe: Combined ratio Excellent combined ratio well below group target

Net earned premium (In EUR mio)

* Scope: only consolidated companies

In % Net earned premium*

71.0 66.4 63.6 63.7 61.355.9 58.6

49.8 51.0

30.330.3

29.8 30.0 30.8

29.530.1

33.7 32.7

101.396.7

93.4 93.7 92.185.4

88.783.5 83.7

1.9(2.0) (2.5) (4.0) (4.3) (6.5) (6.5)

(12.1) (13.0)2010 2011 2012 2013 2014 2015 2016 Q4 15 Q4 16

claims ratio expense ratio PY claims ratio

Combined ratio

Reflecting continued excellent operating

performance with steady improvement in combined

ratio since 2010

Slight increase vs. 2015 due to inclusion Ageas

Seguros that is already showing an encouraging

improvement although still in the middle of a

transformation plan

Combined ratio Turkey at 98.1% (vs. 109.7%) with

results improving in all major product lines

Q4 combined ratio

Slight increase in claims ratio fully compensated by

lower expenses

Claims ratio

CY ratio at 65.1% (vs 62.4%) increase related to

Ageas Seguros

PY ratio stable

Expense ratio

Expense ratio increase in Italy related to business

development & inclusion of Ageas Seguros

369 382 397 403 415 454 664 118 189

Continental Europe: Combined ratio per product lineContinued good claims experience in all product lines

Motor: driven by positive run-off in ItalyAccident & Health: increase related to Workers’ Comp

Household: very strong ratio despite events in Portugal

(fire & storms)

Other: very good claims ratio partly thanks to higher run-off

42Periodic financial Information I FY 16 results I 15 February 2017

64.2 63.5 63.3 59.7 61.9 58.8 64.9

31.6 27.8 28.226.6 26.7 25.2

25.1

95.891.3 91.5

86.3 88.684.0

90.0

2010 2011 2012 2013 2014 2015 2016

90.571.8 69.8

79.360.1

71.5 65.5

27.0

29.2 28.129.2

31.6

32.332.5

117.5

101.0 97.9108.5

91.7

103.898.0

2010 2011 2012 2013 2014 2015 2016

53.5 53.7 51.8 53.5 54.036.1 42.3

27.7 34.2 33.538.8 40.3

35.938.0

81.287.9 85.3

92.3 94.3

72.080.3

2010 2011 2012 2013 2014 2015 2016

73.394.5

62.8 59.672.3

31.712.1

39.0

50.0

43.3 43.7

45.1

40.8

41.3

112.3

144.5

106.1

103.3117.4

72.5

53.4

2010 2011 2012 2013 2014 2015 2016

NEP 205 220 226 227 238 255 328 NEP 104 97 99 99 96 94 202

NEP 39 42 44 48 51 70 91 NEP 21 23 28 29 30 35 43

Continental Europe Life operating margin per product lineHigher in Guaranteed & stable in Unit-Linked

Guaranteed: increased due to higher investment & U/W

margin

Unit-linked: stable

43Periodic financial Information I FY 16 results I 15 February 2017

Expense & other margin remained stable compared to LY Investment margin increasing in both France & Portugal

Underwriting margin higher thanks to overall strong claims

performance in Portugal & inclusion of Ageas Seguros

Expenses & other margin improved due to higher technical

liabilities

In bps Avg techn. liabilities

118 106 95 100 110

10

118

6968 77 59

76

25

89

(85) (83)(102)

(71) (65) (77) (71)

10291 70

88

121

50

136

2012 2013 2014 2015 2016 Q4 15 Q4 16

2 11 2

3(5)

4151

94 5

5 12

1

(5)

1 22

1

44

47

107 7

108

2012 2013 2014 2015 2016 Q4 15 Q4 16

Operating margin

Investment m.

Expense & other m.

Underwriting m.

Avg techn liabilities (In EUR bn)

7.8 7.7 8.3 8.5 9.6 8.5 9.6

Avg techn liabilities (In EUR bn)

6.4 6.3 6.2 6.1 5.9 6.1 5.9

Net result incl. cap gain Hong Kong –Q4: EUR 52 mio lower cap gainsIn EUR mio In EUR bn

Non-Life combined ratio: driven by positive developments in Malaysia

Inflows* up 14% @ constant FX -strong growth in China & Thailand

Life Technical liabilities up 17% in JV’sIn EUR bn

Asia: Headlines Strong result driven by China & Thailand – supported by cap gain from divestment Hong Kong

44Periodic financial Information I FY 16 results I 15 February 2017

In EUR mio

Result non-conso: strong in Thailand, China & NL Malaysia – lower cap gains

In % NEP

* incl. non-consolidated partnerships @ 100%

199259

168

13

27

272

394

FY 15 FY 16

cap gain AICA Life Non-Life

15.6 17.1

0.90.9

16.5

18.0

FY 15 FY 16

Life Non-Life

3.4 3.5

0.2 0.2

3.6 3.7

Q4 15 Q4 16

45

10

6

6

51

17

Q4 15 Q4 16

3.2

42.3 46.8 49.5

45.5 46.849.5

FY 15 9M 16 FY 16

conso non-conso

235183

13

27

248

210

FY 15 FY 16

Life Non-Life

86.9 86.4

Q4 15 Q4 16

91.185.1

FY 15 FY 16

47

19

6

6

53

25

Q4 15 Q4 16

Life

Non-Life

Asia: Inflow @ 100%Strong growth in new business & renewals especially in China & Thailand

45Periodic financial Information I FY 16 results I 15 February 2017

15,26716,896

318

168

+9%

15,58517,064

FY 15 FY 16

420 410

108 108

96 106

289 269

-2%

913 893

FY 15 FY 16

Unit-Linked

Guaranteed

Other

Household

Accident & Health

Motor

In EUR mio

In EUR mio

Life

New business premiums up 16% @ constant FX with EUR 3.8 bn single

premium (+7%) & EUR 3.9 bn regular premium (+25%)

Renewal premiums up to EUR 9.5 bn (+15% @ constant FX) benefiting from

prior year strong sales & continued good persistency

China +20% @ constant FX - new business premium up 23% with successful

sales campaigns & increased number of agents (254K). Persistency ratio

remains strong.

Malaysia +9% @ constant FX – change in product mix towards regular premium

& good persistency has increased renewal – high sales of endowment products

Thailand +10% @ constant FX - good persistency resulted in higher renewal

India +12% @ constant FX - good performance in Banca regular premium –

positive impact of demonetization cannot be excluded

Philippines reported good progress in Mortgage Reducing Term Assurance

(MRTA) products

Hong Kong inflow until May 12th (closing of sale) amounted to EUR 183 mio

Vietnam: license obtained

Non-Life

Malaysia -1% @ constant FX - mainly impacted by slowdown economy

Thailand +10% @ constant FX - mainly driven by Motor & Personal Accident

Result Q4 lower on revaluation RPN(i)In EUR mio

Accounting value of remaining legacies

General Account: Headlines Impacted by cap gain on sale of Hong Kong, Fortis settlement & revaluation RPN(i) liability

46Periodic financial Information I FY 16 results I 15 February 2017

Total liquid assets up on sale HK –EUR 0.8 bn ring-fenced for settlement

In EUR mioImpact on P&L from RPN(i) Staff & Operating expenses up on one-

offs (legal settlement & HR related)

In EUR mio In EUR bn

In EUR mio

In EUR mio

Accounting value on AG Insurance put option: up driven by higher multiples

15

(694)

FY 15 FY 16

29

(8)

Q4 15 Q4 16

1.3

1.8 1.8

0.3

0.2 0.21.6

2.0 1.9

FY 15 9M 16 FY 16

net cash liquid assets

(402)(295) (275)

41 41 42

(133)

(1,019) (1,024)

FY 15 9M 16 FY 16

RPN(i) RPI Settlement

(1,064) (1,083)(1,266)

FY 15 9M 16 FY 16

1732

53

63

70

95

FY 15 FY 16

Staff & Intercompany Operating

4 9

15 14

1923

Q4 15 Q4 16

65 83

FY 15 FY 16

43

20

Q4 15 Q4 16

47Periodic financial Information I FY 16 results I 15 February 2017

Total liquid assets General AccountProceeds sale Hong Kong, SBB, legal settlement & investments in Europe & Asia

In EUR mio

Proceeds of sale Hong Kong activities received on 12/05/16

Upstream from operating companies compensate for dividend & holding costs

2015 Share buy-back completed dd. 05/08/16 – Another EUR 40 mio cash-out

related to 2016 SBB dd. 12/02/17

Cash-out in Asia & Europe related to various investments in developing business

EUR 0.8 bn ring-fenced for legal settlement

1,604 1,943

(339)

(244)

(250)(84)

(379)

(44) (110)

1,221

513

20

35

FY 15 sale HK Upstream Dividend Sharebuy-back

Legalsettlement

Asia Europe CASHES Regional& HQ

expenses

Other FY 16

EUR 0.8 bn ring-fenced

for legal settlement

48Periodic financial Information I FY 16 results I 15 February 2017

Main characteristics Hybrids Leverage optimized at holding level & at AG Insurance

In EUR mio Ageas

AgeasfinluxFresh

Ageas HybridFinancingHybrone

Fixed-to-Floating Rate

Callable

Fixed Rate Reset Perpetual

Subordinated Loans

Fixed Rate Reset Dated

Subordinated Notes

CASHES

% 3m EUR + 135 bps 5.125% 5.25% 6.75% 3.5% 3m EUR +200 bps

Amountoutstanding

1,250 95 450 550 USD 400 948

ISIN XS0147484074 XS0257650019 BE6261254013 BE6251340780 BE6277215545 BE0933899800

Call dateUndated,

strike 315.0 mandatory 472.5

Jun 16Step up to 3M

Euribor +200 bps

Jun 24Step up to 3M

Euribor +413 bps

Mar 19 Step up to 6yr USD

swap + 533 bps

June 2027Step up after 12 years of 100bps

Undated, strike 239.4,

mandatory 359.1

OtherOn lent to AG

Insurance

Subscribed byAgeas & BNP Paribas Fortis

Public issue Public issue

Coupon served by FBB, trigger ACSM

linked to Ageas dividend

Market Price (31/12/16)

48.58 114.73 106.00 96.92 66.40

Fortis Bank (now BNP PF)

AG Insurance (Belgium)

Called

20/06/16

Table of contents Slides used during analyst call 2

Segment information 18

Equity / Solvency 49

Investment portfolio 58

Legal Settlement 63

General Information 68

50Periodic financial Information I FY 16 results I 15 February 2017

Shareholders’ equity at EUR 9.7 bn - UG/L of EUR 12.03/shareDown on legal settlement, financial market, put option & return to shareholders

In EUR mio

7,0956,554

2,952

2,498

1,330

604

821

(694)(484)

(338) (244)(289)

(430)(57) (4)

EUR 53.59 EUR 47.03

11,376

9,656

FY 15 ResultInsurance

ResultGen Acc

ChangeUG/L

Dividend TreasuryShares

Reval AGput option

Forex IAS 19 Other FY 16

InsuranceUCG/L Insurance

UCG/L

Shareholders’

equity per

segment

Shareholders’

equity per share

FY 15 FY 16 FY 15 FY 16

Belgium 4,932 ► 4,683 Asia 3,009 ► 2,004

UK 1,129 ► 911 Reinsurance 104

Continental Europe 977 ► 1,350 Insurance 10,047 ► 9,052

General Account 1,330 ► 604

51

Tangible net equityHigh quality capital structure

10/03/2010 I page 51

EUR bn FY 15 FY 16

IFRS Shareholders' Equity 11.4 9.7

Unrealised gains real estate 0.5 0.5

Goodwill (0.8) (0.7)

VOBA (Value of Business Acquired) (0.3) (0.1)

DAC (Deferred Acquisition Cost) (0.9) (0.5)

Other (0.4) (0.4)

Goodwill, DAC, VOBA related to N-C interests 0.4 0.4

25% tax adjustment DAC, VOBA & Other 0.3 0.2

IFRS Tangible net equity 10.2 9.0

IFRS Tangible net equity/ IFRS Shareholder's Equity 90% 93%

Periodic financial Information I FY 16 results I 15 February 2017

2.9 2.8

0.8 0.7 0.7 0.90.3 0.0

(0.3) (0.3)

4.4 4.2

0.0 0.1

4.4 4.2

0.71.6

6.9 6.9

1.10.8 0.9 1.2

0.60.1 (1.5)(1.5)

8.07.6

1.4

0.7

9.4

8.3

1.8

4.3

FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16

Periodic financial Information I FY 16 results I 15 February 2017

Solvency IIageasImpact from exceptional items in UK compensated by Belgium & CEU

Solvency IIageas

in %

In EUR bn

Own Funds

SCR

Non EU

Non-controlled

participations*

52

Insurance ratio remains stable

Group ratio influenced by legal settlement & increasing put option liability

Expected dividend deducted

242% 244% 130% 120% 131% 127% 179% - - 278% 182% 182% 212% 195% 253% 264%

Belgium UK CEU Asia Reins. Diversification Insurance GA Group

Non-transferable

* Based on local solvency requirements

53

Ageas Group Solvency IIageasMain elements driving movement in Solvency ratio

Periodic financial Information I FY 16 results I 15 February 2017

Impact on

Solvency IIageas*

FY ’15 FY ’16

212% 195%

9M ’16 FY ’16

199% 195%

Model refinements

Mainly implementation internal model Real

Estate +13 pp +0 pp

Capital movements

Hong Kong , Portugal, investments in Asia,

SBB & Hybrone +9 pp -1 pp

UK exceptionals -3 pp -3 pp

Legal settlement -20 pp +0 pp

Expected dividend -10 pp -1 pp

Reval put option -5 pp -4 pp

Market movements & other -1 pp +5 pp

* Estimated impact of the movement, including secondary impact, diversification & non-transferable

54

Ageas Insurance Solvency sensitivitiesProviding more granularity on spread sensitivity to allow more accurate assessment

Periodic financial Information I FY 16 results I 15 February 2017

As per 31/12/’15Based on Solvency IIageas

SCR OF Solvency

Base caseBefore stress – excl. Hong Kong

4,132 7,494 181%

Yield curveDown 1% (floor 0%, UFR 4.2%)

4,539 7,337 162%

UFRDown to 3.7%

4,148 7,440 179%

EquityDown 30%

3,938 6,961 177%

PropertyDown 20%

3,946 7,013 178%

SpreadSpreads on corporate & government bonds up 50 bps

4,256 6,971 164%

Corporate spread*Spreads on corporate bonds up 50 bps

4,002 7,533 188%

Sovereign spread*Spread on government bonds up 50 bps

4,423 6,959 157%

* Corporate & Sovereign spread sensitivities based on detailed calculation of 100 bps movement impact – linear approach

leading to conservative estimation of impact

Periodic financial Information I FY 16 results I 15 February 2017

Insurance SCRageas per risk typeMarket risk main factor in SCR – Decrease of SCR related to Belgium & Hong Kong

Market risk down on implementation

internal model RE in pillar II – look

through on own funds & SCR

55

In EUR bn

( 1.6 ) ( 1.5 )

( 0.6 ) ( 0.5 )

( 1.1 ) ( 1.0 )

4.7 4.3

0.3 0.3

0.8 0.6

0.4 0.4

0.8 0.8

0.7 0.7

4.4 4.2

2015 2016

Non Diversifiable

Non-life UW

Health UW

Life UW

Counterparty Default

Market

Loss-Absorption Deferred Taxes

Loss-Absorption Techn. Liab.

Diversification

Diversification

Loss-Absorption Deferred Taxes

Life UW down on sale HK

Periodic financial Information I FY 16 results I 15 February 2017

Solvency PIM – as reported to the regulatorInsurance ratio down on market movements

Solvency II PIM

in %

In EUR bn

Own Funds

SCR

Non EU

Non-controlled

participations*

56

3.03.4

0.9 0.7 0.6 0.80.4 0.0 (0.3) (0.3)

4.5 4.6

0.0 0.1

4.6 4.6

0.71.6

6.9 6.8

1.10.8 0.9

1.7

0.60.1 (1.5)

(1.6)

8.17.7

1.4

0.5

9.4

8.2

1.8

4.3

FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16 FY 15 FY 16

234% 201% 124% 114% 148% 211% 158% - - 259% 178% 169% 206% 177% 253% 264%

Belgium UK CEU Asia Reins. Diversification Insurance GA Group

Non-transferable

BE: mainly yield impact increasing SCR – internal model RE not implemented in PIM UK: impact from Q4 negative exceptionals CEU: approval transitional measures in Portugal (Q3) & France (Q4)

* Based on local solvency requirements

Periodic financial Information I FY 16 results I 15 February 2017

Tiering of Group PIM own funds High quality of own funds

57

Tier 1:

Equity down on legal settlement,

return to shareholders & financial

markets

In EUR bn

6.9

5.8

1.8

1.4

0.5

0.9

0.2

0.1

9.4

8.2

FY 15 FY 16

Tier 3

Tier 2

Tier 1 restricted

Tier 1

Tier 1 restricted:

Hybrone repaid & limit to 20% of

total Tier 1

Tier 2 : up on overflow from Tier 1

Table of contents Slides used during analyst call 2

Segment information 18

Equity / Solvency 49

Investment portfolio 58

Legal Settlement 63

General Information 68

59Periodic financial Information I FY 16 results I 15 February 2017

In EUR bn

* All assets at fair value except the ‘Held to Maturity’ assets & loans which are valued at amortized costs

Asset mix

Changed scope with divestment Hong Kong (-EUR 2.4 bn) &

acquisition Ageas Seguros (+EUR 1.4 bn) in H1 16

Combined negative impact of scope change compensated by

increased market value bonds because of lower interest rates

Loans & equities increased at the expense of corporate bonds

Gross unrealized gains/losses on Available for Sale

Total portfolio: up to EUR 8.3 bn (vs. EUR 7.6 bn); up in fixed

income

Fixed income: at EUR 7.7 bn (vs. EUR 7.1 bn FY 15)

Sovereigns at EUR 5.8 bn (vs. EUR 5.5 bn)

Corporates at EUR 1.8 bn (vs. EUR 1.6 bn)

Equities: stable at EUR 0.6 bn

Gross UG/L on Real Estate: stable at EUR 1.5 bn - not

reflected in shareholders’ equity

EUR 2.4 bn unrealized gains/losses on Held to Maturity (vs. EUR 2 bn) - not reflected in shareholders’ equity

Investment portfolio Investment portfolio up on unrealized gains on bonds & investment in loans and equities

Sovereign bonds 36.4

Sovereign bonds 37.9

Corporate bonds 25.9

Corporate bonds 24.1

Structured0.2

Structured0.1

Loans7.3

Loans8.7

Equities 3.9Equities 4.4

Real Estate5.4

Real Estate5.3

Cash 2.4Cash 2.2

81.5 82.7

FY 15 FY 16

Increase driven by lower i-rates

Gross UG/L at EUR 5.8 bn (vs. EUR 5.5 bn)

94% investment grade; 86% rated A or higher

Belgium Duration gap close to zero – matched portfolio

Belgium18.2

Belgium19.0

France 6.0France 6.3

Austria 2.8Austria 2.9

Portugal 2.1Portugal 2.4Italy 1.6

Italy 1.5Spain, 0.8Spain, 1.5

Germany 1.3

Germany 1.2Ireland 0.7

Ireland 0.7Other 3.0Other 2.4

36.437.8

FY 15 FY 16

In EUR bn

Sovereign bond portfolio*

Sovereign & Corporate bond portfolioValue fixed income portfolio driven by evolution unrealized gains & divestment Hong Kong

60Periodic financial Information I FY 16 results I 15 February 2017

Gross UG/L at EUR 1.8 bn (vs. EUR 1.6 bn)

Decrease mainly due to divestment of Hong Kong with

investments predominantly in corporate bonds

Credit quality remains very good with 93% investment

grade; 58% rated A or higher

Corporate bond portfolio*

Banking 4.6 Banking 3.8

Other financials 1.7

Other financials 1.9

Non Financials

13.6

Non Financials

13.5

Government related 6.0

Government related 4.9

25.924.1

FY 15 FY 16

* All assets at fair value except the ‘Held to Maturity’ assets & loans which are valued at amortized costs

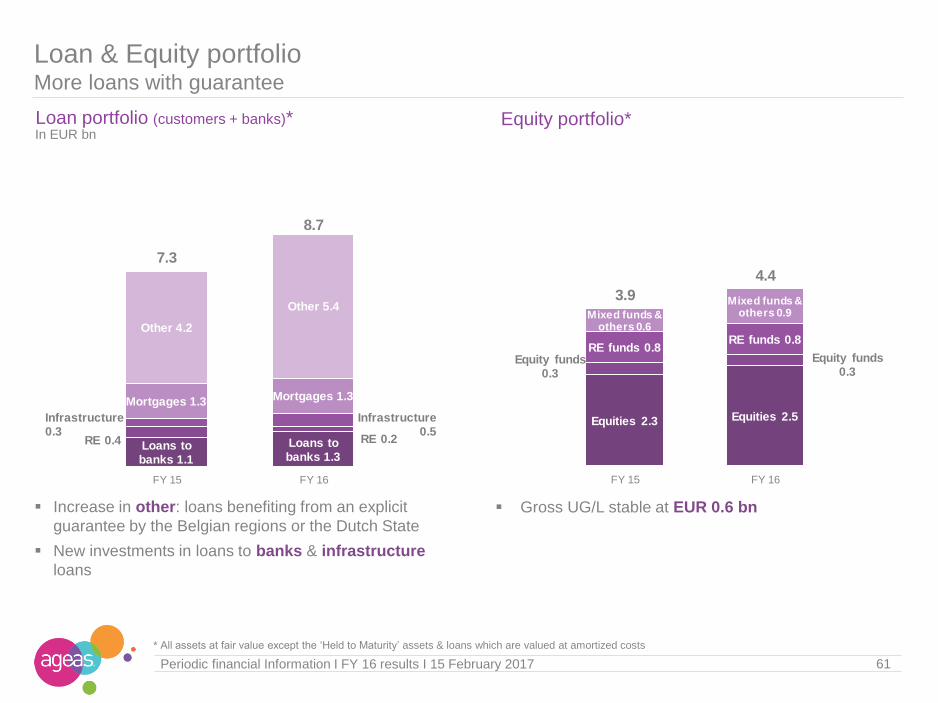

Loan portfolio (customers + banks)*

Loan & Equity portfolioMore loans with guarantee

Loans to banks 1.1

Loans to banks 1.3

RE 0.4 RE 0.2

Infrastructure0.3

Infrastructure0.5

Mortgages 1.3 Mortgages 1.3

Other 4.2

Other 5.4

7.3

8.7

FY 15 FY 16

Increase in other: loans benefiting from an explicit

guarantee by the Belgian regions or the Dutch State

New investments in loans to banks & infrastructure

loans

61Periodic financial Information I FY 16 results I 15 February 2017

Equity portfolio*

Gross UG/L stable at EUR 0.6 bn

Equities 2.3 Equities 2.5

Equity funds0.3

Equity funds0.3

RE funds 0.8RE funds 0.8

Mixed funds & others 0.6

Mixed funds & others 0.9

3.9

4.4

FY 15 FY 16

* All assets at fair value except the ‘Held to Maturity’ assets & loans which are valued at amortized costs

In EUR bn

62Periodic financial Information I FY 16 results I 15 February 2017

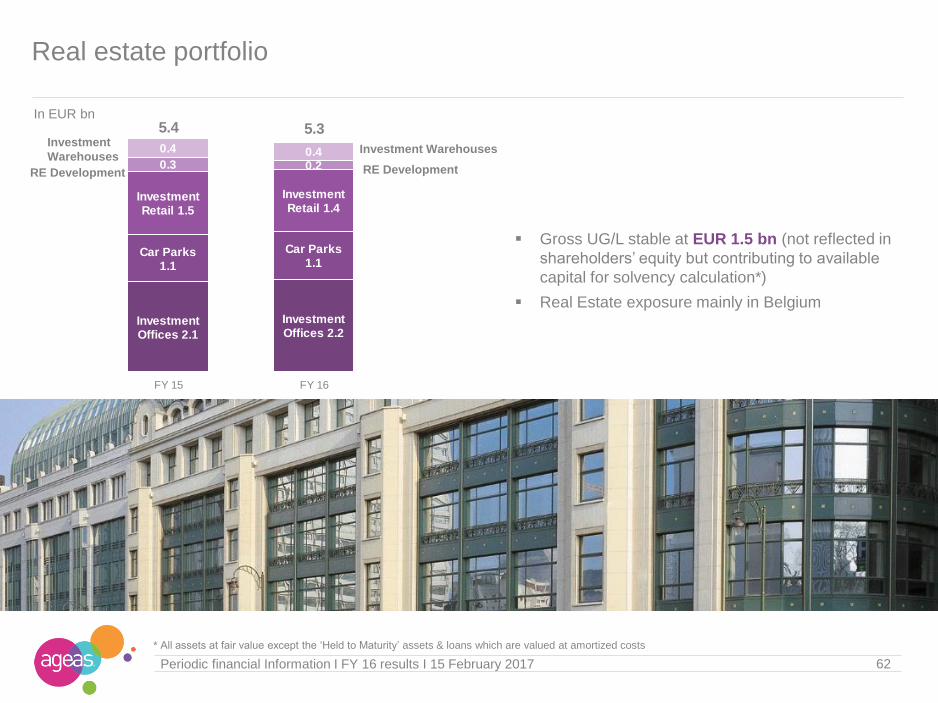

Real estate portfolio

10/03/2010

Gross UG/L stable at EUR 1.5 bn (not reflected in

shareholders’ equity but contributing to available

capital for solvency calculation*)

Real Estate exposure mainly in BelgiumInvestment Offices 2.1

Investment Offices 2.2

Car Parks1.1

Car Parks1.1

Investment Retail 1.5

Investment Retail 1.4

0.3 0.2

0.4 0.4

5.4 5.3

FY 15 FY 16

Investment Warehouses

RE Development

Investment

Warehouses

RE Development

In EUR bn

* All assets at fair value except the ‘Held to Maturity’ assets & loans which are valued at amortized costs

Table of contents Slides used during analyst call 2

Segment information 18

Equity / Solvency 49

Investment portfolio 58

Legal Settlement 63

General Information 68

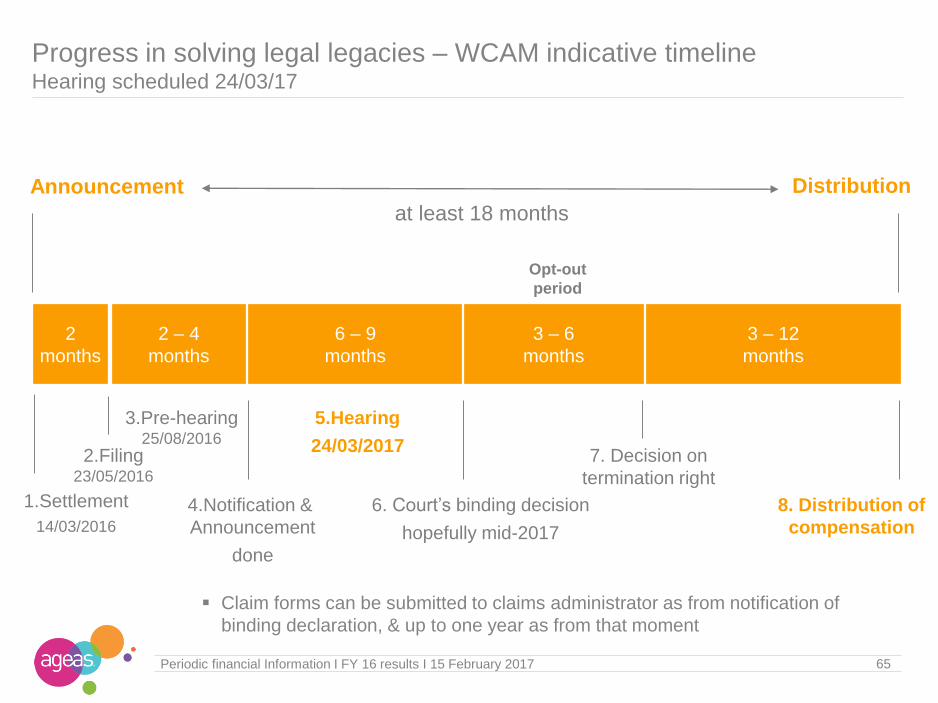

64Periodic financial Information I FY 16 results I 15 February 2017

Progress in solving legal legaciesSettlement between Ageas & claimants organisations

Ageas pays EUR 1,204 mio compensation - Cash impact of EUR 1,021 mio

P&L impact of EUR 889 mio in Q1 2016

No recognition of any wrongdoing by Ageas

Commitment by eligible shareholders to abandon any ongoing civil proceeding &

not to start any legal proceeding related to the events

Intervention of Amsterdam Court declaring settlement binding

First distribution of compensation not before 18 months after announcement

Filing done 23/05/2016

Additional support received since announcement

Hearing scheduled on 24/03/2017

First cash-out of EUR 250 mio over 2016

Judgment on binding character expected by mid 2017

More details on compensation per share & calculation aid available on

www.Forsettlement

Announcement

14/03/2016

Based on WCAM

Current status

2 – 4

months

6 – 9

months

3 – 6

months

3 – 12

months

2.Filing 23/05/2016

4.Notification &

Announcement

done

3.Pre-hearing25/08/2016

5.Hearing

24/03/2017

6. Court’s binding decision

hopefully mid-2017

Opt-out

period

2

months

1.Settlement

14/03/2016

8. Distribution of

compensation

Announcement Distribution

65Periodic financial Information I FY 16 results I 15 February 2017

at least 18 months

7. Decision on

termination right

Progress in solving legal legacies – WCAM indicative timelineHearing scheduled 24/03/17

Claim forms can be submitted to claims administrator as from notification of

binding declaration, & up to one year as from that moment

66Periodic financial Information I FY 16 results I 15 February 2017

21 September 2007 7 November 2007 cob Communication on subprime exposure, organisation of capital increase for ABN AMRO

acquisition - period linked to AFM II fine

13 May 2008 25 June 2008 cob Communication on solvency after full integration of ABN AMRO – period linked to AFM I fine

29 September 2008 3 October 2008 cob Communication on the deal with the Benelux governments – period linked to FortisEffect case

The various litigation procedures

Main allegations

Judgments rendered so far

Open of

business

Close of

business

(cob) 28/02/07 14/10/08

21/09/07 07/11/07 13/05/08 25/06/08 29/09/08 03/10/081 2

3

4

5

6

7

8

Eligible period

3 reference

periods

Reference

periods

based on

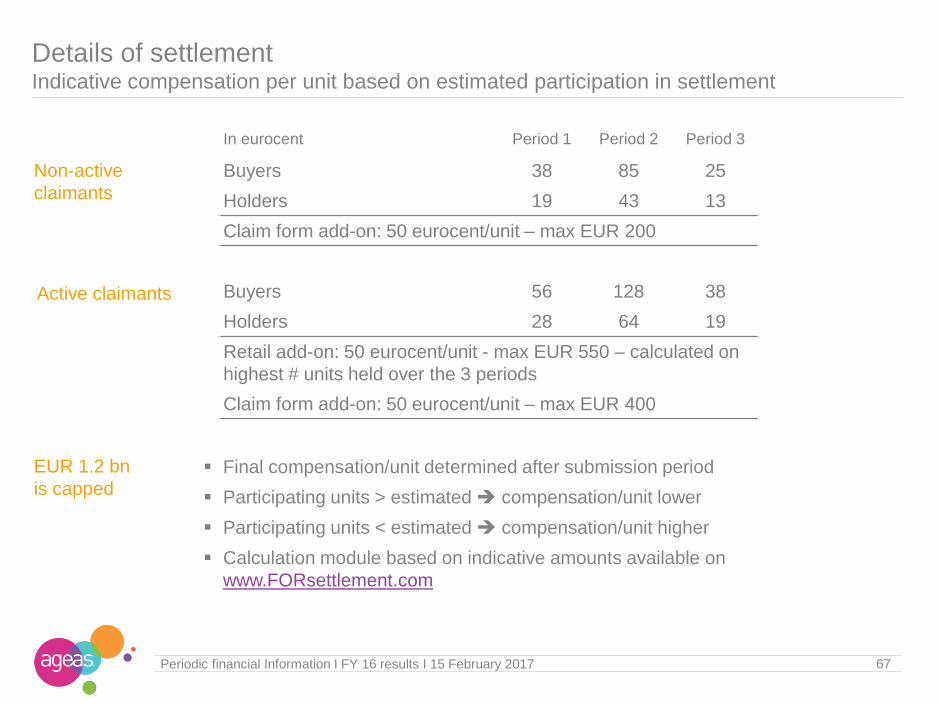

Progress in solving legal legaciesPeriods involved

Final compensation/unit determined after submission period

Participating units > estimated compensation/unit lower

Participating units < estimated compensation/unit higher

Calculation module based on indicative amounts available on

www.FORsettlement.com

67Periodic financial Information I FY 16 results I 15 February 2017

Details of settlementIndicative compensation per unit based on estimated participation in settlement

In eurocent Period 1 Period 2 Period 3

Buyers 38 85 25

Holders 19 43 13

Claim form add-on: 50 eurocent/unit – max EUR 200

Buyers 56 128 38

Holders 28 64 19

Retail add-on: 50 eurocent/unit - max EUR 550 – calculated on

highest # units held over the 3 periods

Claim form add-on: 50 eurocent/unit – max EUR 400

Active claimants

Non-active

claimants

EUR 1.2 bn

is capped

Table of contents Slides used during analyst call 2

Segment information 18

Equity / Solvency 49

Investment portfolio 58

Legal Settlement 63

General Information 68

situation 31/12/2015 situation 31/12/2016 situation 11/02/2017

223,778,433 216,570,471 216,570,471

16,086,350 15,143,439 16,138,953

7,207,962 7,170,522 8,166,036

3,968,254 3,968,254 3,968,254

266,230 45,804 45,804

4,643,904 3,958,859 3,958,859

207,692,083 201,427,032 200,431,518

69Periodic financial Information I FY 16 results I 15 February 2017

Total number of outstanding shares7.2 mio shares cancelled in April – 8.1 mio shares bought back since

Total Issued Shares

Shares not entitled to dividend nore voting rights

1. TREASURY SHARES Share buy-back

FRESH

Other treasury shares

2. CASHES

Shares entitled to dividend & voting rights

CASHES deal

with BNP

SBB &

cancellation

cancellation

70Periodic financial Information I FY 16 results I 15 February 2017

Shareholders structureAgeas above 5% threshold following SBB

Based on number of shares as at 10 February 2016

Ageas5.6%

Ping An

BlackRock, Inc.

Schroders

Franklin Mutual Advisers Identified retail

investors19%

Identified institutional investors

47%Other

investors9%

Based upon press release 14 November 2016

Based upon the number of shares mentioned in the notification received 6 May 2013

Based upon the number of shares mentioned in the notification received 17 March 2014

Based upon the number of shares mentioned in the notification received 14 December 2015

Based upon the number of shares mentioned in the notification received 14 July 2015

Estimate by

Estimate by

Ageas

Ping An

BlackRock, Inc.

Schroders

Franklin Mutual Advisers

Identified retail investors

Identified institutional investors

71Periodic financial Information I FY 16 results I 15 February 2017

Financial calendar 2016 - 2017

15 February

FY 2016 results

10 May

3M 2017 results

17 May

Ordinary & Extraordinary

shareholders’ meeting Brussels

29 May

Ex-dividend date

7 April

Annual report 2016

31 May

Payment 2016 dividend

9 August

6M 2017 results

8 November

9M 2017 results

10 August

6M 2016 results

16 November

9M 2016 results

26 September

Investor Dinner

6 June

Investor Day

72Periodic financial Information I FY 16 results I 15 February 2017

RatingImproved rating for operating entities & holding

S&P MOODY'S FITCH

Operating AG Insurance (Belgium) A / stable A2 / stable* A+ / stable

entities Last change 06/11/15 17/03/16 09/12/16

unsollicited

Ageas Insurance Limited A / stable A+ / stable

Last change 06/11/15 23/11/16

Muang Thai Life BBB+ / stable A- / stable

Last change 29/12/10 27/07/16

Etiqa Insurance Berhad (Malaysia) BBB+ / stable

Last change 27/07/16

Intreas A / stable

Last change 11/11/16

Holding ageas SA/NV BBB / stable Baa3 / positive* A / stable

Last change 15/03/16 30/11/16 09/12/16

unsollicited

* Ageas has requested in early 2009 that this rating should be withdrawn. Ageas no longer participates in Moody's credit rating process.

Ageas does not provide, for purposes of Moody's rating, access to the books, records and other relevant internal documents of these rated entities.

73Periodic financial Information I FY 16 results I 15 February 2017

Certain of the statements contained herein are statements of

future expectations and other forward-looking statements that are based on management's current views and assumptions and involve

known and unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those expressed

or implied in such statements. Future actual results, performance or events may differ materially from those in such statements due to,

without limitation, (i) general economic conditions, including in particular economic conditions in Ageas’s core markets, (ii) performance of

financial markets, (iii) the frequency and severity of insured loss events, (iv) mortality and morbidity levels and trends, (v) persistency levels,

(vi) interest rate levels, (vii) currency exchange rates, (viii) increasing levels of competition, (ix) changes in laws and regulations, including

monetary convergence and the Economic and Monetary Union, (x) changes in the policies of central banks and/or foreign governments and

(xi) general competitive factors, in each case on a global, regional and/or national basis. In addition, the financial information contained in

this presentation, including the pro forma information contained herein, is unaudited and is provided for illustrative purposes only. It does not

purport to be indicative of what the actual results of operations or financial condition of Ageas and its subsidiaries would have been had

these events occurred or transactions been consummated on or as of the dates indicated, nor does it purport to be indicative of the results of

operations or financial condition that may be achieved in the future.

Investor Relations

Tel:

E-mail:

Website:

+ 32 2 557 57 34

www.ageas.com