agence internationale de l’energieinternational energy agency h2 policy analysis using the etp...

TRANSCRIPT

AGENCE INTERNATIONALE DE L’ENERGIEINTERNATIONAL ENERGY AGENCY

H2 Policy Analysis using the ETP model

Dolf Gielen Giorgio Simbolotti

IPHE Task Force on Socio-Economics, Paris, 30 June 2005

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Key pointsHydrogen may play a significant role by 2050This will require R&D successes and cost

reductionFCV cost constitute a key issue for a

hydrogen transitionTotal incremental investment cost till 2050

1.7-3.5 trillion USDThe environmental & supply security benefits

could be substantial, but require policies and technology advance

Competing options may also play a key role

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Presentation Overview

Technology input data Investment analysis Baseline scenarios Sensitivity analysis Observations

AGENCE INTERNATIONALE DE L’ENERGIEINTERNATIONAL ENERGY AGENCY

Part 1: Technology input data

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Technology typesProduction

CentralizedDecentralized

DistributionRefueling stationsVehicles

Fuel cellOn-board storage

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

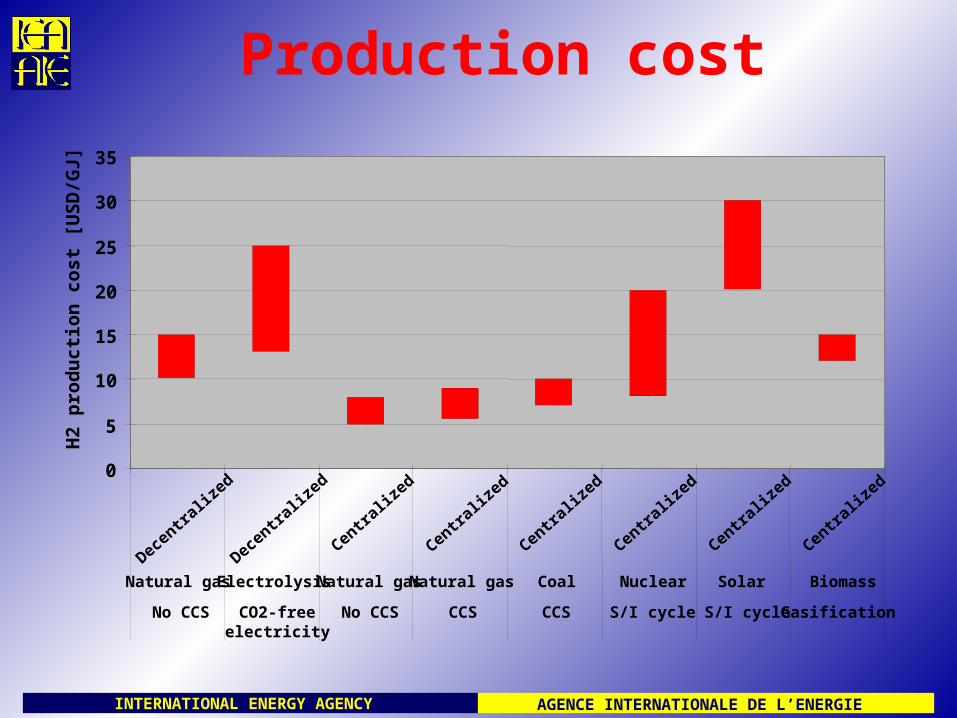

Production cost

0

5

10

15

20

25

30

35

Decentraliz

ed

Decentraliz

ed

Centraliz

ed

Centraliz

ed

Centraliz

ed

Centraliz

ed

Centraliz

ed

Centraliz

ed

Natural gas Electrolysis Natural gas Natural gas Coal Nuclear Solar Biomass

No CCS CO2-freeelectricity

No CCS CCS CCS S/I cycle S/I cycle Gasification

H2

pro

du

cti

on

co

st [

US

D/G

J]

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

H2 transportation cost

Pipelines constitute the only viable transportation mode

Some hydrogen (up to 9% e/e) can be mixed into natural gas in existing pipelines

New pipelines will be needed

Transportation cost six times those for natural gas

0.5-1 trillion USD for refuelling station supply, 5 trillion for all stationary gas users

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Distribution and refueling cost

Distribution (pipeline/LH2) adds 2 USD/GJ delivered

Liquefaction: 7-10 USD/GJ H2 delivered

Refuelling station cost 3-6 USD/GJ H2 delivered (incl. pressurization, excl. decentralized production cost)

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Hydrogen vehicles

EnginesHydrogen hybridsHydrogen FCVs

On-board storageGaseous 700 barGaseous 350 barLiquidMetal hydridesOther

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Fuel cellsPresent cost 2000 USD/kW<50 USD/kW neededProton Exchange Membrane Fuel Cells (PEMFC)Current technology: Nafion membrane, Pt/C

catalystSignificant cost reduction possible (mass

production), but less than 100 USD/kW seems not likely with current materials

New catalyst alloys needed, or HT-membranes New materials may offer cost reduction potential

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Future Cost Structure (2020)50% higher power density, 10 times cheaper

membranes, more than 50,000 cars/y (engines)

Cost Cost Share

[USD/m2] [USD/kW] [%]

Membrane 50 17 16

Electrode 150 50 49

Bipolar plates 91 30 29

Platinum catalyst 8 3 3

Peripherals 4 1 1

Assembly 2 2

Total 103 100

This is still too costly !!!

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Further cost reductione.g. through higher power density

Factor 2 gain100 → 50 USD/kW

Present0

0.02

0.04

0.06

0.08

0.1

0.12

0.14

0.16

0.18

0 2 4 6 8

Power [kW/m2]

Sta

ck

po

wer

del

iver

y co

st [

US

D/k

Wh

]

Stack 66 USD/kW

Stack 50 USD/kW due tobetter membrane

- Higher power density gives lower efficiency- Higher power density gives lower stack cost- Therefore a balancing of fuel & stack cost needed

Long termShort term

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

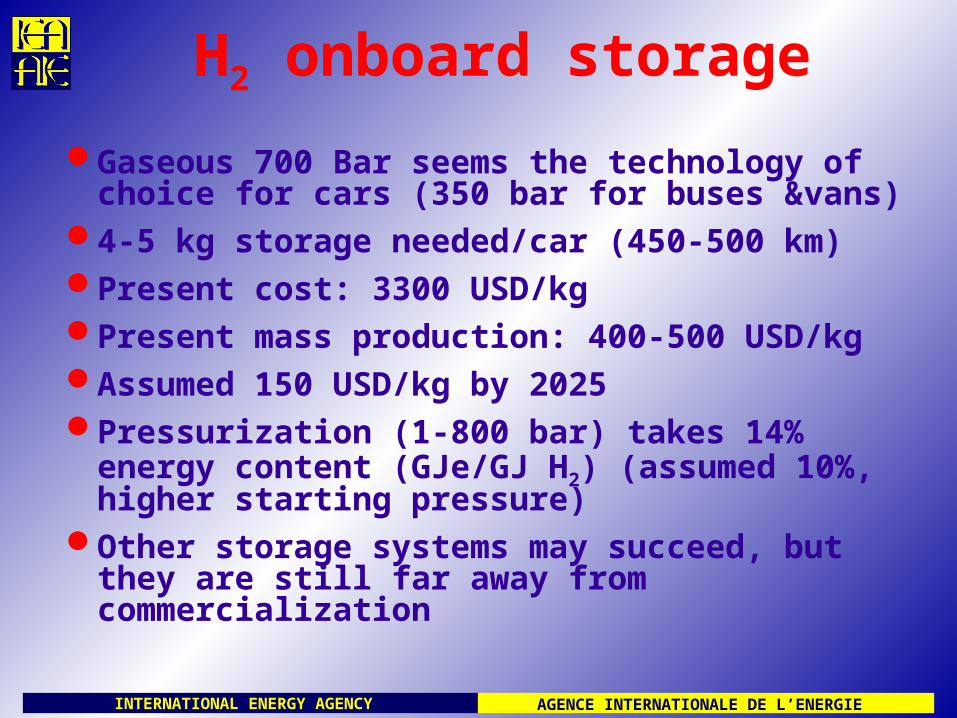

H2 onboard storage

Gaseous 700 Bar seems the technology of choice for cars (350 bar for buses &vans)

4-5 kg storage needed/car (450-500 km)Present cost: 3300 USD/kgPresent mass production: 400-500 USD/kgAssumed 150 USD/kg by 2025Pressurization (1-800 bar) takes 14% energy

content (GJe/GJ H2) (assumed 10%, higher starting pressure)

Other storage systems may succeed, but they are still far away from commercialization

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

H2 production

Comparison on GJ-basis is deceptive, as FCV efficiency is 2.5 times current ICE efficiency

H2 can be supplied at 15-20 USD/GJ (2020-2030)

Fuel cost (ex tax)/km about the same as current gasoline vehicles

AGENCE INTERNATIONALE DE L’ENERGIEINTERNATIONAL ENERGY AGENCY

Part 2: Investment analysis

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Assumed FC stack cost reduction35 USD/kW stack; 10 USD/kW storage; 15

USD/kW drive system

10

100

1000

10000

2000 2010 2020 2030 2040 2050

[US

D/k

W] GLO50

SensitivityAnalysis

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

FCVs: USD 1- 2.3 tr. incremental cost

2010 2015 2020 2030 2040 2050

Assumptions Used in Both Cases

Cumulative FCV Production, OECD (millions) 0.00 0.04 0.21 8.4 133.3 502.4

Cumulative FCV Production, World (millions) 0.00 0.04 0.22 8.6 143.7 727.5

FCV Share of Sales, OECD 0.0% 0.1% 0.2% 5.0% 50.0% 100.0%

FCV Share of total vehicle stock, OECD 0.0% 0.0% 0.1% 2.2% 13.1% 31.0%

Optimistic Case Results

FCV drive system cost, optimistic case (0.78 progress ratio) [USD/kW] 545 207 134 69 54 50

Total incremental cost of FCV, cumulative (bln USD) 0.1 0.6 2.1 27 244 965

Pessimistic Case Results

FCV cost drive system, pessimistic case (0.85 progress ratio) 545 284 207 114 81 69

Total incremental cost of FCV, cumulative (bln USD) 0.1 0.9 3.4 60 585 2,264

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Incremental investment needsExcludes centralized production processes

FCVs: 1-2.3 trillion USD

Distribution: 0- 1 trillion USD

Refueling infrastructure: 0.2-0.7 tr. USD

Total: 1.7-3.5 trillion USD

Total GDP 2000-2050: 4,500 trillion USD

Therefore 0.03-0.1% of GDP

AGENCE INTERNATIONALE DE L’ENERGIEINTERNATIONAL ENERGY AGENCY

Part 3: Baseline scenarios

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Why model analysis?

Account for competing options (e.g. biofuels)

Account for competing use of resources (e.g. electricity from renewables)

Account for regional differences (resource endowment, capital availability, car use etc.)

Quantify the relevance of H2 & FC on a global/regional level

Map uncertainties

Quantify the cost and specify additional policy requirements

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Hydrogen model structure

Electrolysis at fuel station

(3 types)

Natural gas pipeline

Pyrolysis/Gasifier/

Reformer plantFuture Gen

Heating/cooking

Coke Ovens

ICE mobile applications

Refinery/NH3 etc.H2 storage

Natural gas

Fuel oilCoal

Biological/Direct solar

Liquef. + H2 truck

Natural gas

Biomass

Fuel cell mobile applications

ICE mobile applications

Industry MCFC/SOFC

10%

Ren. ele

Fossil+CCS

Res/Com MCFC/PEM FC/

SOFC

Reformer at fuel station

Renewables

LH2 storage

H2 distrib.

Solar SI cycleNuclear

CO2 removal

H2 pipeline

H2 gas storage 350 bar

H2 gas storage 700 bar

MeH2 storageNuclear

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Structure of the analysis, so far

BASE scenario: no CO2 policies

GLO50 scenario: CO2 policies plus reasonable assumptions for H2/FC

GLO50 w/o H2/FC: what are the benefits on a systems level

Sensitivity analysis: individual parameter variations for GLO50

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

GLO50(reference)

21 model runs

ESTEC+++++

ESTEC-----

ESTEC++---

ESTEC+--+-

GLO50 w/o H2 & FC

BASEw&w/o

H2 & FC

GLO25w&w/o

H2 & FC

GLO50w&w/o

H2 & FC

BASE

Fuel Market Analysis

H2&FC Benefits Analysis

Scenario Analysis + Regional Results

H2&FC Potentials Analysis

Sensitivity Analysis

GLO50

how robust are H2 & FC results

H2 & FC supply security benefits

H2 & FC CO2&monetarybenefits

DRAFTREPORT

what are the key assumptions

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

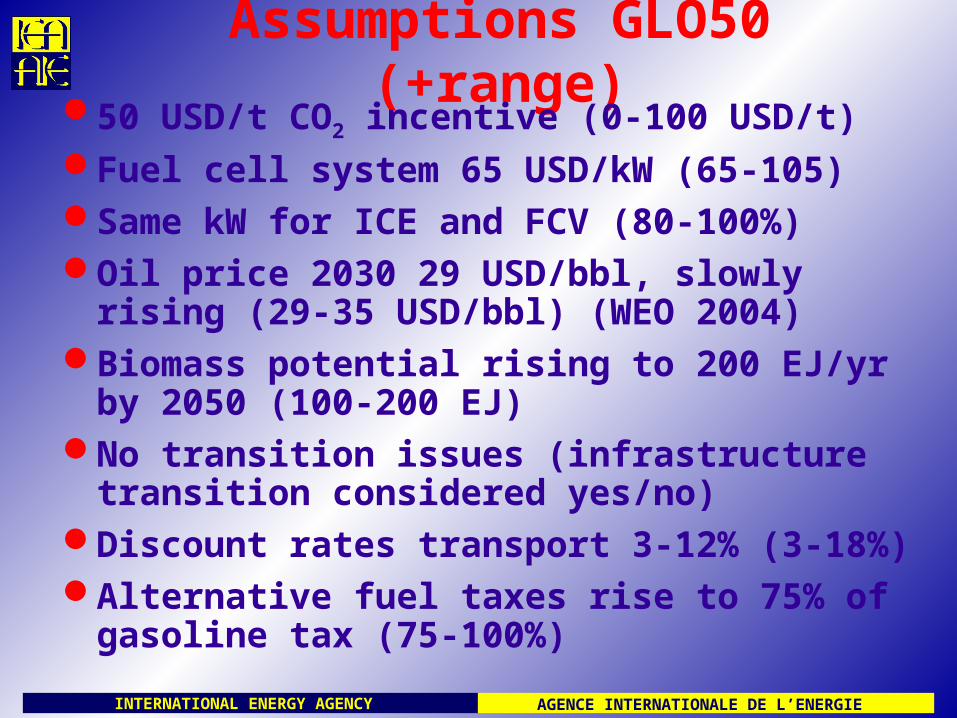

Assumptions GLO50 (+range)50 USD/t CO2 incentive (0-100 USD/t)Fuel cell system 65 USD/kW (65-105)Same kW for ICE and FCV (80-100%)Oil price 2030 29 USD/bbl, slowly rising (29-35

USD/bbl) (WEO 2004)Biomass potential rising to 200 EJ/yr by 2050

(100-200 EJ)No transition issues (infrastructure transition

considered yes/no)Discount rates transport 3-12% (3-18%)Alternative fuel taxes rise to 75% of gasoline

tax (75-100%)

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

CO2 price A gradual rise to 50 USD/t

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

CO2 emissions: 50 USD/t CO2 = Emissions Stabilization

0

10

20

30

40

50

60

70

1970 1980 1990 2000 2010 2020 2030 2040 2050

[Gt

CO

2/y

r]

Base

GLO50

Statistics

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Transport fuels

Total oil products

Hydrogen

CNG

Methanol/DME

FT fuels coal

FT fuels natural gas

Other biofuels

Ethanol

FT fuels biomass

Refinery products non-conventional oil

Refinery products conventional oil

ETP results

0

20

40

60

80

100

120

140

160

180

200

2002

WEO R

S 203

0

WBCSD 2

050

BASE, 205

0 (H

DR)

GLO50, 2

050

(HDR)

GLO50, 2

050

[EJ/

yr]

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Key insights

No CO2 policy: more than a doubling in fuel use; 2/3 oil products; 1/3 alternative fuels

CO2 policy: 1/3 oil products, 1/3 biofuels, 1/10 H2; 30% efficiency gains

1/10 hydrogen replaces 2 times as much oil products (27% H2 FCV by 2050)

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Transport CO2 emissions(WTW) -50% in 2050 but still rising

0

5

10

15

20

2000 2010 2020 2030 2040 2050

[Gt

CO

2/y

r]

BASE

GLO50

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Key emission reductions

Globally 32 Gt CO2 reduction in 2050

Transport (WTW) 8.5 Gt CO2 reduction in 2050:Biofuels: 1.5 GtCCS: 2 Gt (alternative fuels production) (+1.9 Gt

H2 production)

Substitution effect H2 use: 1 Gt due to H2 use

Efficiency: 4 Gt (including 1 Gt due to H2 use)

Total 2 Gt due to H2 use

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

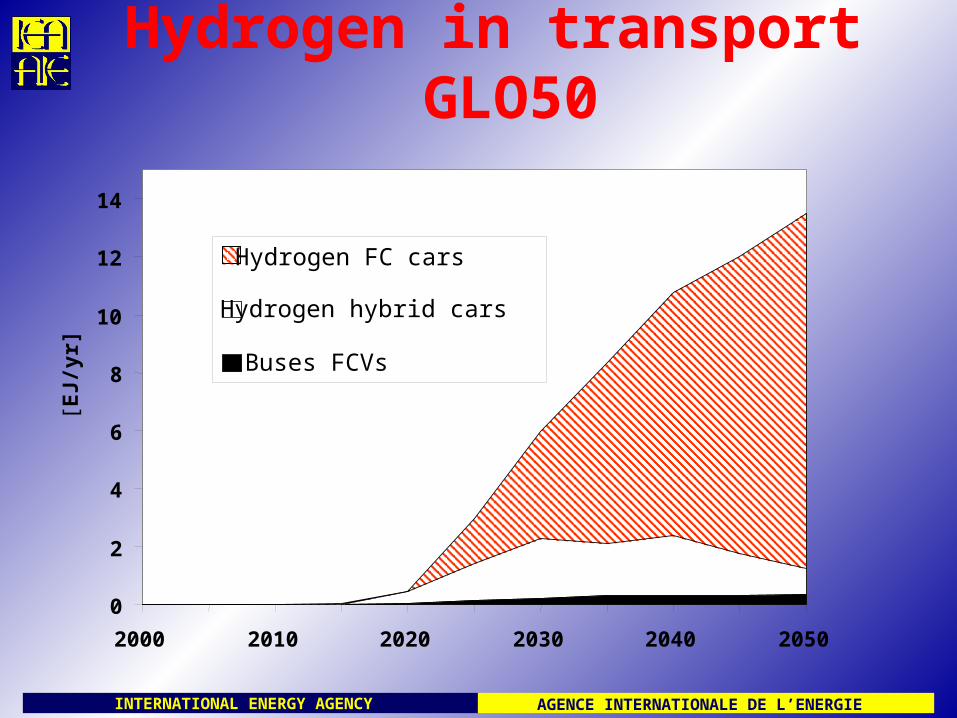

Hydrogen in transport GLO50

0

2

4

6

8

10

12

14

2000 2010 2020 2030 2040 2050

[EJ/

yr]

Hydrogen FC cars

Hydrogen hybrid cars

Buses FCVs

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Stationary fuel cells

MCFC/SOFC

At present 10,000-15,000 USD/kW (50% stack)

1,600 USD/kW target (50% stack)

This is an order of magnitude higher than for mobile applications

Electric efficiency decentralized 40-45%

Efficiency centralized integrated 45-70% (wide range of estimates)

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Stationary fuel cell useby sector

0

100

200

300

400

500

2000 2010 2020 2030 2040 2050

[GW

]

Power sector

Residential & Services

Industry

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Stationary fuel cell useby fuel

0

100

200

300

400

500

2000 2010 2020 2030 2040 2050

[GW

]

Oil

Coal

Natural gas

Hydrogen

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Comparison GLO50 to GLO50 w/o H2&FC

Systems effect: 1.3 Gt higher emissions in 2050 (+4%)

Systems effect: 7% higher crude oil use in 2050

This suggests significant benefits

AGENCE INTERNATIONALE DE L’ENERGIEINTERNATIONAL ENERGY AGENCY

Part 4: Sensitivity analysis

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

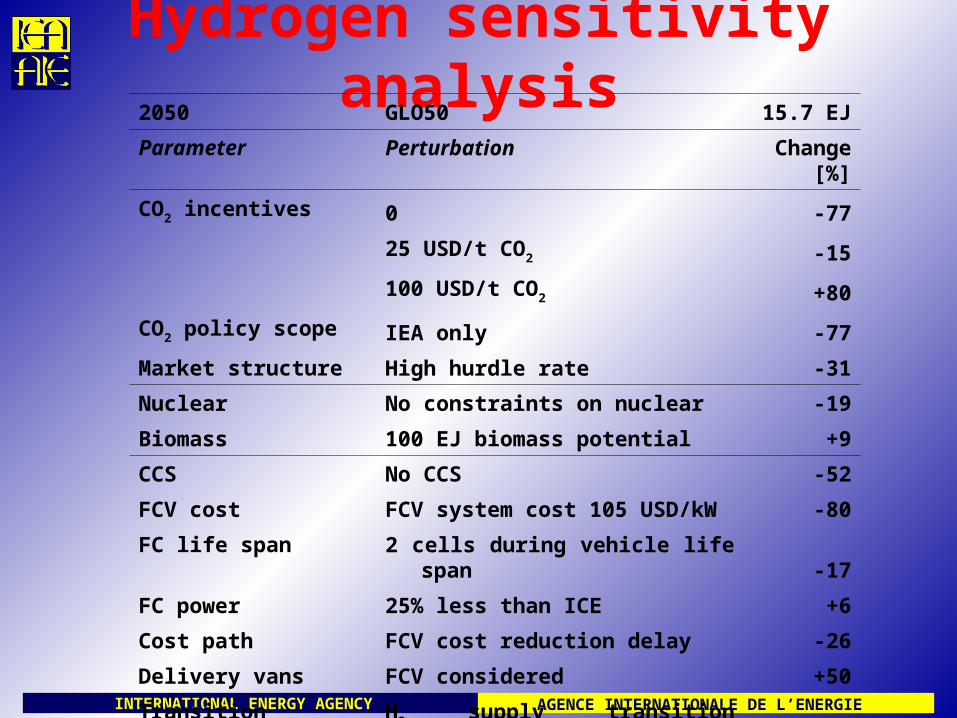

Hydrogen sensitivity analysis2050 GLO50 15.7 EJ

Parameter Perturbation Change[%]

CO2 incentives 0 -77

25 USD/t CO2 -15

100 USD/t CO2 +80

CO2 policy scope IEA only -77

Market structure High hurdle rate -31

Nuclear No constraints on nuclear -19

Biomass 100 EJ biomass potential +9

CCS No CCS -52

FCV cost FCV system cost 105 USD/kW -80

FC life span 2 cells during vehicle life span -17

FC power 25% less than ICE +6

Cost path FCV cost reduction delay -26

Delivery vans FCV considered +50

Transition H2 supply transition considered -42

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

H2 Production with & w/o transitionThe technology path is a key issue

0

2

4

6

8

10

12

14

16

18

2030 2030 2050 2050

GLO50 GLO50CHE GLO50 GLO50CHE

[EJ/

yr]

Other

Decentralized natural gas

Centralized natural gas + CCS

FutureGen

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Prospects for electrolysis

Electricity becomes virtually CO2-free at relatively low CO2 price levels

A trade-off between diurnal electricity prices and H2 storage cost

So far diurnal H2 storage not considered

May reduce production cost by 3 USD/GJ H2

So far no reliable data for efficiency & cost of advanced electrolysis

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

CO2-emissions of electricity production

0

2

4

6

8

10

12

14

16

18

2000 2005 2010 2015 2020 2025 2030 2035 2040 2045 2050

[Gto

n C

O2]

0$

10$

25$

25$ No CCS

50$

50$ No CCS

AGENCE INTERNATIONALE DE L’ENERGIEINTERNATIONAL ENERGY AGENCY

Part 5: Observations

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Need for secure, alternative transportation fuels beyond 2030 (supply argument)

CO2 policies (reduction/stabilization) also imply oil substitution (environmental argument)

Non-conventional oil, FT-synfuels, CNG have limited transition problems, but no substantial CO2 benefits

Efficiency, biofuels have limited transition problems, offer substantial CO2 benefits but limited potential

The H2 option requires R&D breakthroughs and cost reduction, transition will take decades; but holds potential for substantial benefits

The main challenge is the affordable FCV

Buses, delivery vans, H2 hybrids as a transition strategy

Overall benefits of having H2/FC: 4% lower GHG emissions, 7% less oil use

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Workshop SummaryRelevant other studies

WBCSD SMP Concawe/EUCAR/JRC WTW study H2A CUTE Hyways ETSAP

4 working groups Production, transportation&distribution FCVs Stationary&portable FCs Technology scenarios

INTERNATIONAL ENERGY AGENCY AGENCE INTERNATIONALE DE L’ENERGIE

Workshop conclusionsData are uncertain (present and future)Challenge to get “true” FC dataDemand for more sensitivity analysisOptimisation vs. policy simulation

scenariosMore emphasis on regional

differences/detailsFocus more on R&D policies & transition

instead of long-term economics