agenda - tegma 1 the transformation of the mexican railroad system scosttdale, az. january 2016...

TRANSCRIPT

01/02/2016

1

The Transformation of the Mexican Railroad System

Scosttdale, Az. January 2016

Agenda

1. The Past: Ferrocarriles Nacionales de Mexico.

2. The Transformation: Private Railroads performance

3. Grupo Mexico and Ferromex

4. Grain: Key to Ferromex´s results

5. Reform to Railroad Law

01/02/2016

2

How bad can a Railroad be?

Ferrocarriles Nacionales de México

Francisco J. Gorostiza, Renacimiento de los ferrocarriles de carga en México

FNM

01/02/2016

3

Francisco J. Gorostiza, Renacimiento de los ferrocarriles de carga en México

FNM

Francisco J. Gorostiza, Renacimiento de los ferrocarriles de carga en México

FNM

01/02/2016

4

Government owned FNM splits for future

bidding in 5 units

Grupo México creates GFM later owner of

Ferromex

KCS acquires TFM. New KCSM

Ferromexacquires Ferrosur

Ferromex wins dispute with Antitrust Commission

SEP´95

NOV´96

DEC´98 APR´05

NOV´05 MAR´11FEB´98

Ferromex starts operations

Ferrosur starts operations

New Railroad law

JAN´15

TFM starts operations

JUN´97

Time Line

*MTON-KM (Millions)

Mexico: Rail System

Private FNM INDICATOR 2014 1995 % VAR CARG

MTKM Millions 80,683 37,613 115% 4.3%EMPLOYEES 15,260 46,283 -67% -6.0%PRODUCTIVITY (TKM / EMPLOYEE) 5.29 0.81 551% 11.0%AVERAGE HP PER LOCOMOTIVE 3,035 2,696 13% 0.7%CARLOADS / TRAIN 75 37 103% 4.0%

Key Performance Indicators

01/02/2016

5

Mexico: Rail System

Key Performance Indicators

0.52 0.57

0.44

0.81

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

1980 1985 1990 1995 ‐

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

Empl

oyee

s

MTK

N /

Empl

oyee

MTKN/EMPLOYEE EMPLOYEE

3.18

5.33 5.45 5.29

0.81 -

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

2000 2005 2010 2014 1995 ‐

1.00

2.00

3.00

4.00

5.00

6.00

Empl

oyee

s

MTK

N /

Empl

oyee

MTKN/EMPLOYEE EMPLOYEE

FNM PRIVATE

65% FXE+FSRRMarket Share

% Railroad share MMTKM

Railroads Market Share

FXE, 41%FXE, 47% FXE, 52% FXE, 49%

FSRR, 9%FSRR, 8%

FSRR, 8% FSRR, 16%

KCSM, 35%KCSM, 33%

KCSM, 28%

KCSM, 31%

OTHERS, 14% OTHERS, 12% OTHERS, 12%OTHERS, 5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2000 2005 2010 2014

OTHERS KCSM FSRR FXE

Rail traffic share from land transportation increase from 19% to 26%, FXE+FSRR supports most of it

01/02/2016

6

USD

Cents P

erTo

n-Ki

lom

eter

Competitiveness

Source: Inter-American Development Bank, 2013OECD: Organization for Economic Cooperation and Development

Productivity per LocomotiveMillions tons - Km per Locomotive

Source: Inter-American Development Bank, 2013OECD: Organization for Economic Cooperation and Development

Productivity

01/02/2016

7

Mining

100%

Americas MiningCorporation (AMC)

85.2%

ASARCO

100%SouthernCopper

Corporation

MexicoDivision

100%

PeruDivision

100%

Transportation

75%

FMRail Holdings (FMRH)

FERROMEX

100%

26%

FERROSUR

100%

IMEX

100%

TEXAS PACIFICO

100%

Grupo FerrioviarioMexicano

74%

Infraestructura y Transportes Ferroviarios

100%

Infrastructure

100%

México Proyectos y Desarrollo

Perforadora México

100%

MéxicoGeneradora de Energía

100%100%

25%

MéxicoCompañía

Constructora e Ingeniería

Grupo Mexico: Structure

Grupo México Statistics

$9,3ANNUAL REVENUE (BILLION USD)

30,018EMPLOYEES

3 COUNTRIES

556 FORBES LIST 2015

LARGEST COPPER RESERVESWORLDWIDE1°4thCOPPER PRODUCER WORLDWIDE

COPPER PRODUCER WORLDWIDELARGEST RAILROAD IN MEXICO 1°

Grupo Mexico at a Glance

01/02/2016

8

Ferromex

The largest Railroad in Mexico

Ferromex at a Glance

6,719MILES

798LOCOMOTIVES 6 US BORDERS SERVED

9 PORTS SERVED

NTKM MOVED 201554 MM

27,485RAIL CARS

10,021EMPLOYEES 1.4MM CARLOADS MOVED 2015

Ferromex Statistics

01/02/2016

9

Ferromex Network

Ferromex: Customer Base

Grain 28.2%

Automotive 12.0%

Industrial 10.6%

Minerals 9.7%

Chemicals 8.5%

Energy 7.8%

Intermodal, 7.4%

Metals 6.2%

Cement 4.4%Others, 5.2%

01/02/2016

10

*MTON-KM (Millions)

Ferromex: Performance by Segment

Segment 2015 2000 %Part %VAR CARG

Total 54,220 27,292 99% 5%

Grain 19,545 7,607 36% 157% 7%Minerals 7,825 6,177 14% 27% 2%

Chemicals 4,757 3,186 9% 49% 3%Metals 4,733 776 9% 510% 14%

Intermodal 4,029 1,388 7% 190% 8%Energy 4,028 1,200 7% 236% 9%

Industrial 3,594 4,117 7% -13% -1%Cement 2,967 3,600 5% -18% -1%

Automotive 2,743 421 5% 552% 14%

Ferromex: Cross border volume

Cross border traffic key to our growth

33% 37%

49% 50% 51% 49% 48%50%

51%

0%

10%

20%

30%

40%

50%

60%

‐

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2,011 2012 2013 2014 2015

% SH

ARE

ofRA

ILRO

AD IN

TERN

ATIO

NALL

TRA

FFIC

CAR

LOAD

S (0

00's)

Expo Impo Market Share

01/02/2016

11

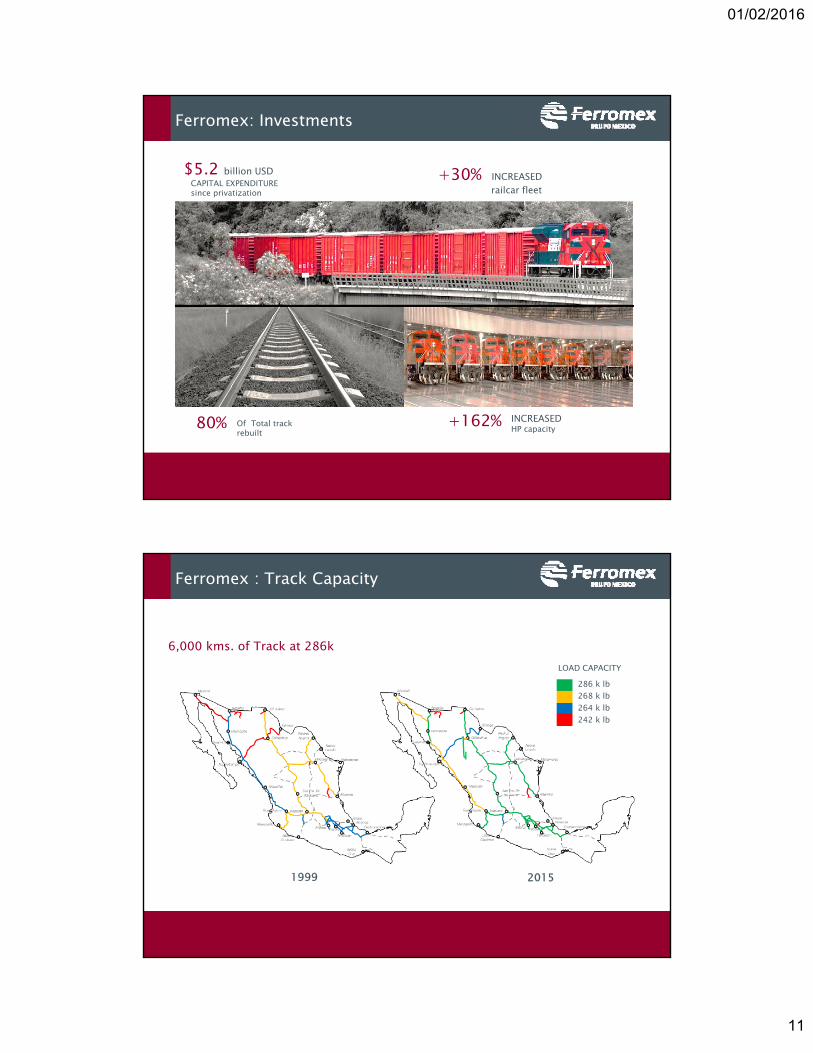

Ferromex: Investments

80%

CAPITAL EXPENDITUREsince privatization

$5.2 billion USD +30% INCREASED railcar fleet

+162%Of Total track rebuilt

INCREASED HP capacity

1999 2015

6,000 kms. of Track at 286k

Ferromex : Track Capacity

286 k lb268 k lb264 k lb242 k lb

LOAD CAPACITY

01/02/2016

12

Source: U.S. Census Bureau (2002 – 2011) and Association of American Railroad

Ferromex has invested 27.5 % of the total revenues, significantly above class 1’s and most industries.

Ferromex: Investments

GROSS TON-KM +186%

FUEL PRODUCTIVITY +33%

GROSS TONS PER TRAIN +52%

ACCIDENTS RATE -97%

Ferromex: Efficiency

01/02/2016

13

321

540

84

125

30

159

101

263

-

200

400

600

800

1,000

1,200

1999 2015

Grain

Auto

Consumer

Others

159% Cummulativegrowth

CARG 7%

*Does not include containers

Carloads (000,s)

Grain Products the biggest segment in FXE with high growth

Grain our key segment

Major Crop Areas (Million MT)

CornWheat

Sorghum

5.5

2.6

6.7

1.8

2.4

Corn

Wheat

Sorghum

Source: GCMA based on SIAP November and GCMA estimated for December

01/02/2016

14

SOYBEAN

CORN SORGHUM

WHEATPRODUCTION

3.8CONSUMPTION

8.2

DEFICIT -4,454%

PRODUCTION6.5

CONSUMPTION7.3

DEFICIT - 0.811%

PRODUCTION25.8

CONSUMPTION37.4

PRODUCTION0.5

CONSUMPTION6.2

DEFICIT -5.692 %

DEFICIT -11.431 %

Source: GCMA based on SIAP November and GCMA estimated for December

2015 Mexico Production/Consumption

Opportunities FXE

CORN: -1.2 SORGHUM: -0.5

WHEAT: -0.3 SOYBEAN: -0.8

-2,3

CORN: -6,5SORGHUM: -1,5

WHEAT: -3.2SOYBEAN: -1.0

-12,0

CORN: -2,.6SORGHUM: -0.6

WHEAT: -0.9SOYBEAN: -0.5

-3.4

Grain Deficit (Million MTons)

Source: GCMA based on SIAP November and GCMA estimated for December

01/02/2016

15

34 Shuttle Terminals in 2016

2000 2005 2010NEW

PROJECTS2015

4 6716 Source: GCMA based on SIAP November and GCMA estimated for December

Ferromex: Shuttle Trains

28

299

379

2000 2009 2015

+ 23 Terminals

CAGR30%

CAGR5%

+ 6 Terminals

01/02/2016

16

Grain: Our key segment

1. Track investments for longer and heavier trains

2. Equipment to capitalize on Northwest Crop

3. Continue development of grain terminals´ network

4. Continue development of unit an shuttle trains

5. Power increase and crews development

Our Strategy:

Grain: Our Key Segment

1. Add 550 new hoppers. Total fleet 5,552

2. Hopper car exchange with UP and BNSF during peak

seasons.

3. Reduce unload time to 15Hrs in shuttle train terminals

4. Rate incentives to increase unit and shuttle train use.

Our Plans:

01/02/2016

17

Reform to the Railroad Law

Mexico New Railroad Law

1. Open access for licensee carriers without concession

2. All rates, including contracts, to be published3. Concessionaries responsible for construction and

maintenance of railway crossings

4. Change to the exclusivity periods

Negative issues with the original proposal

01/02/2016

18

Mexico New Railroad Law

Negative Issues Original IniciativeFinal changes to the Law: Positive

Main changes:

Competition and Interchange More interchange points and guaranteed competition

Regulatory AgencyCreation of Regulatory AgencyRate regulation only with lack of effective competition

Rule 11 Customers can negotiate rates with each carrier

No licensee carriers Eliminated

Otherchanges:

Safety RailcrossingFund Creation of National Fund

Unused Track SCT to offer for bid

ConcessionRevocation More aggressive sanctions to revoke concessions

01/02/2016

19

01/02/2016

20

Transformation

01/02/2016

21