agenda county of oxford council meeting wednesday, august ... room... · county of oxford council...

TRANSCRIPT

AGENDA

COUNTY OF OXFORD

COUNCIL MEETING

WEDNESDAY, AUGUST 12, 2015 9:30 A.M.

COUNCIL CHAMBER, OXFORD COUNTY ADMINISTRATION BUILDING, WOODSTOCK

MEETING #20

County of Oxford ~ eAgenda Application Version 0.3.0 Agenda Version 1, Addition to Agenda►

1. CALL TO ORDER Time ______

2. APPROVAL OF AGENDA

3. DISCLOSURES OF PECUNIARY INTEREST AND THE GENERAL NATURE THEREOF

4. ADOPTION OF COUNCIL MINUTES OF PREVIOUS MEETING

July 8 2015

5. PUBLIC MEETINGS

6. DELEGATIONS AND PRESENTATIONS

7. CONSIDERATION OF DELEGATIONS AND PRESENTATIONS

8. CONSIDERATION OF CORRESPONDENCE

1. Township of ZorraJuly 21, 2015

Re: Membership - Community Schools AllianceTwp of Zorra - 072115

Resolution

That the correspondence from the Township of Zorra, dated July 21, 2015, advising of theTownship's 2015 Community Schools Alliance membership and 2016 new initiative forbudget consideration, be received as information.

2. Township of NorwichRe: Support of Application for Draft Plan of Condominium and Exemption from Draft Plan Approval - 487223 Ontario Limited (Gabriel Kirchberger), File No. CD 15-02-3

Twp of Norwich - 072115

PAGE 2COUNCIL AGENDAAUGUST 12, 2015

County of Oxford ~ eAgenda Application Version 0.3.0 Agenda Version 1, Addition to Agenda►

Resolution

That the correspondence from the Township of Norwich, supporting the application fordraft plan of condominium and exemption from draft plan approval - 487223 OntarioLimited (Gabriel Kirchberger), File No. CD 15-2-3, be received and referred forconsideration under CASPO Report No. 2015-160.

3. Randy Pettapiece, MPP, Perth-WellingtonJuly 21, 2015

Re: Requesting Support of Private Member's Resolution for Fairness in Provincial Infrastructure Funds

R Pettapiece- 072115

Resolution

Link to Resolution

9. REPORTS FROM DEPARTMENTS

PUBLIC WORKS

PW 2015-37Re: Oxford Road 12 Parking Report

Recommendation

That Schedule E within By-law No. 4897-2007 be amended to include, and staffauthorized to implement, a “No Parking” designation on Oxford Road 12 (Mill Street), asincluded within the approved Oxford Road 12 Class Environmental Assessment.

PW 2015-43Re: Trans Canada Trail

Recommendations

1. That County Council authorize staff to negotiate an agreement with the Township of Norwich and the Town of Tillsonburg for the construction and operation of the Trans Canada Trail (TCT) from the existing TCT in Tillsonburg easterly to Norfolk County and the proposed trail under the Canada 150 Community Infrastructure Program from Tillsonburg to Springford, including County financing of the project subject to final approval of County Council;

2. And further, that County staff work with Norwich and South-West Oxford Townships and the Town of Tillsonburg to undertake Public Consultation for the proposed trails on County owned lands including the TCT extension and those seeking partnership funding through the Canada 150 Community Infrastructure Program in Norwich and South-West Oxford Townships.

PW 2015-41Re: Drumbo Wide Area Network Tower Relocation and Replacement

Recommendation

1. That County Council authorize Public Works to proceed in 2015 with the unanticipated relocation and replacement of the Drumbo wide area network tower at a cost of $225,000, to be financed from the Facilities Reserve.

PAGE 3COUNCIL AGENDAAUGUST 12, 2015

County of Oxford ~ eAgenda Application Version 0.3.0 Agenda Version 1, Addition to Agenda►

COMMUNITY AND STRATEGIC PLANNING

CASPO 2015-159Re: Application for Draft Plan of Subdivision SB 15-01-2; 1187688 Ontario Limited

Recommendation

1. That Oxford County Council grant draft plan approval to a proposed plan of subdivision submitted by 1187688 Ontario Limited (File No. SB 15-01-2), prepared by Ricor Engineering Limited, dated April 22, 2015, as shown on Plate 3 of Schedule “A” of Report No. CASPO 2015-159, for lands described as Part of Lots 9 & 10, Concession 17 (East Zorra), in the Village of Innerkip, subject to the conditions attached as Schedule “A” to this Report being met prior to final approval.

CASPO 2015-160Re: Application for Draft Plan of Condominium and Exemption from Draft Plan Approval CD 15-02-3: 487223 Ontario Limited (Gabriel Kirchberger)

Recommendations

1. That Oxford County Council grant draft plan approval of a proposed plan of condominium submitted by 487223 Ontario Limited (Gabriel Kirchberger), (File No. CD 15-02-3); prepared by J.H. Cohoon Engineering Ltd. and dated June 3, 2015, for lands described as Part Lot 677, Plan 955, in the Village of Norwich.

2. And further, that Oxford County Council approve the application for exemption from the draft plan of condominium approval process submitted by 487223 Ontario Limited (Gabriel Kirchberger), (File No. CD 15-02-3) for lands described as Part Lot 677, Plan 955, in the Village of Norwich, as all matters relating to the development have been addressed through the Site Plan Approval process and a registered site plan agreement.

CORPORATE SERVICES

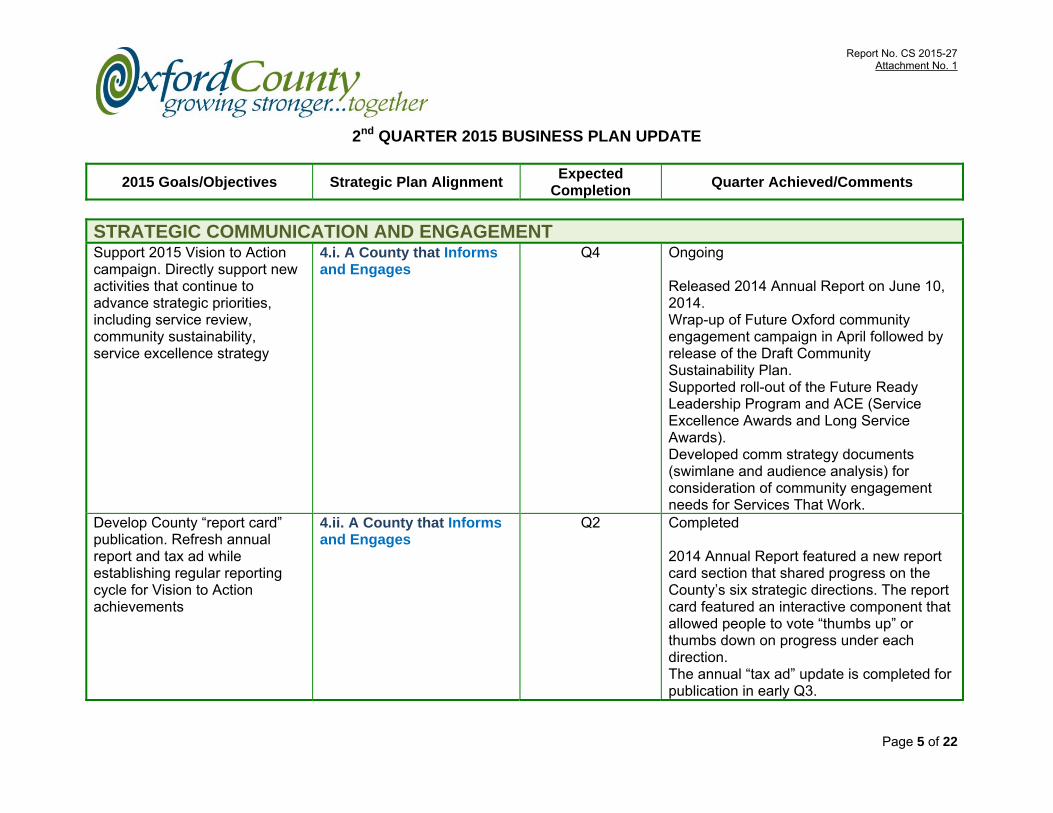

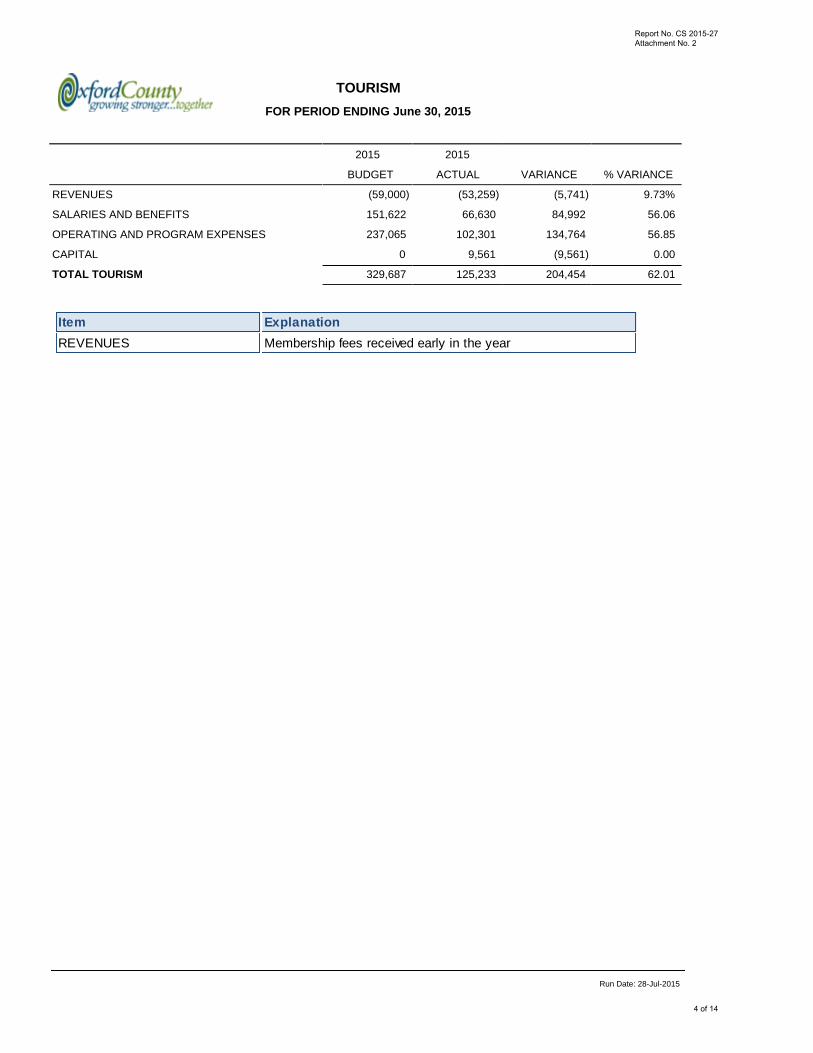

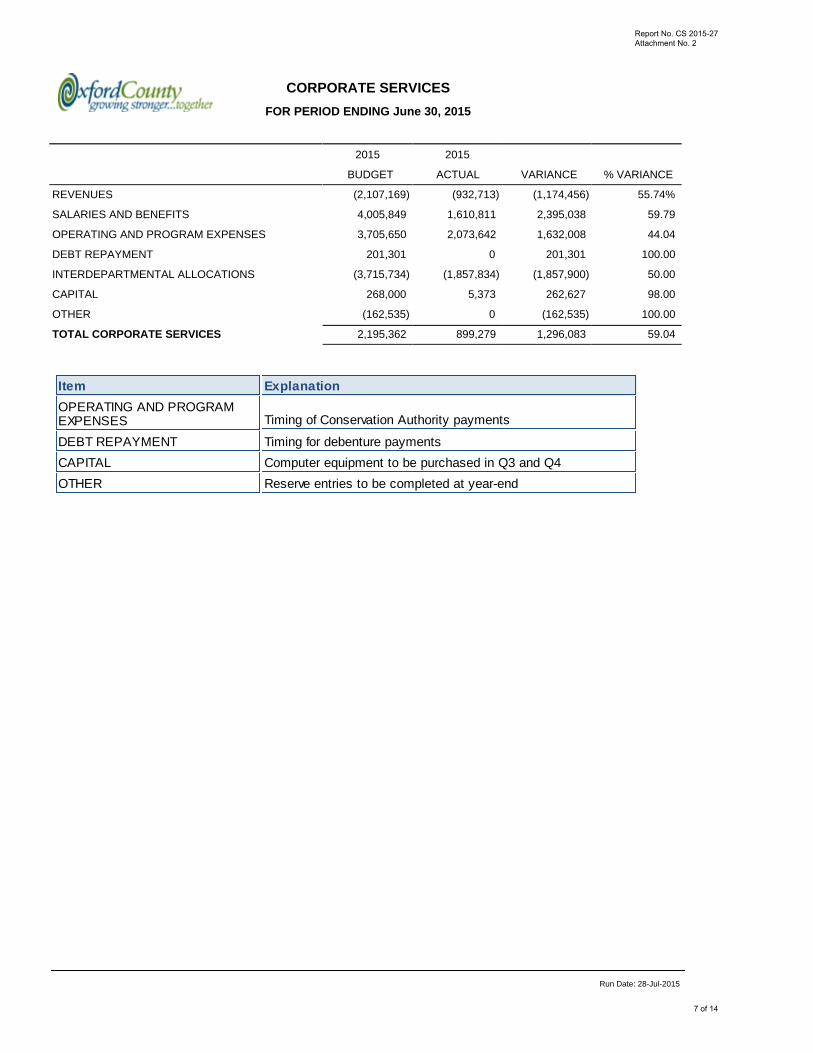

CS 2015-27Re: Business Plan and Budget Review – 2nd Quarter

Recommendation

1. That Report No. CS 2015-27 entitled “Business Plan and Budget Review – 2nd Quarter” be received for information.

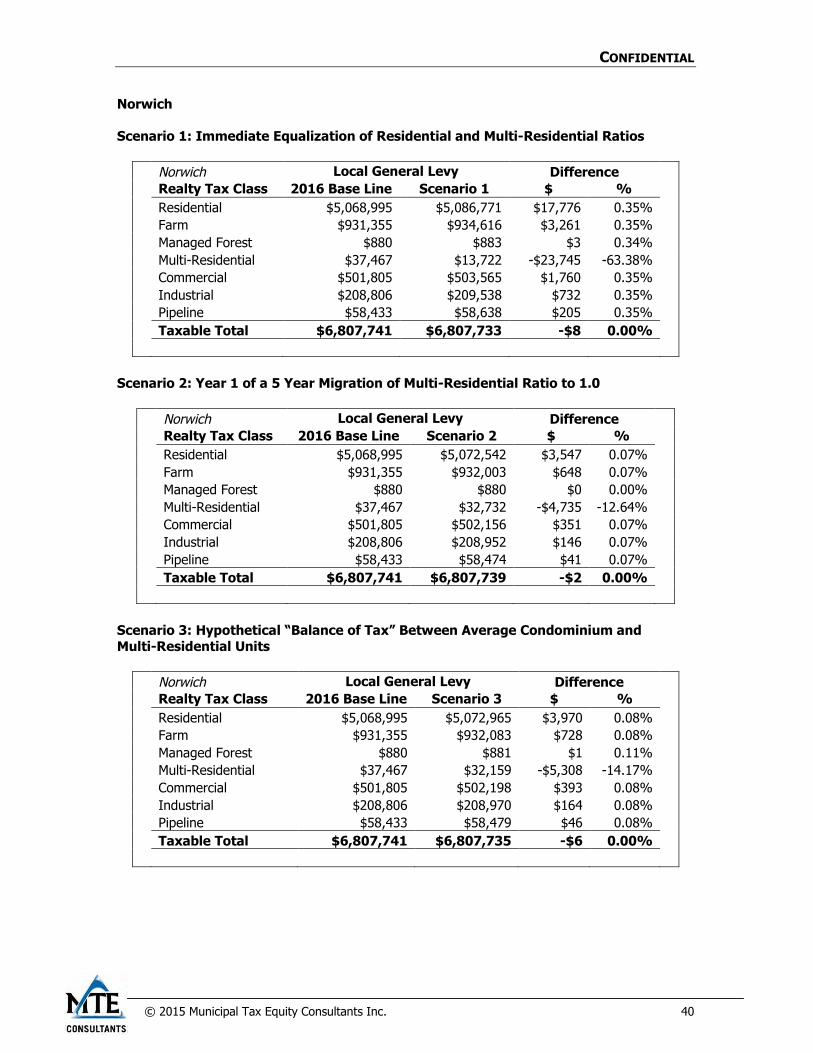

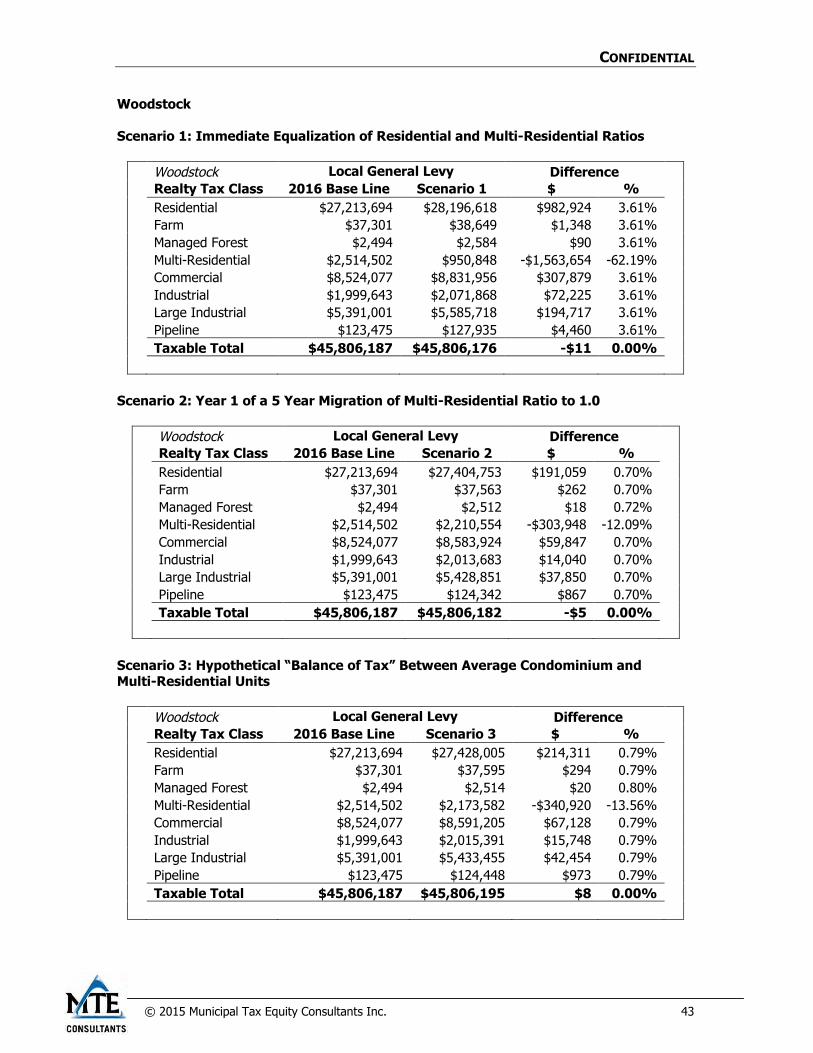

CS 2015-26Re: Multi-Residential Tax Ratio Review Consultant Presentation

Recommendations

1. That based on the results of the multi-residential ratio review as described in Report No. CS 2015-26 entitled “Multi-Residential Tax Ratio Review” no action is to be taken at this time;

2. And further, that a follow-up multi-residential tax ratio review be undertaken in 2019, unless new information arises in the interim that may significantly alter the findings or interpretations of the review contained in this report.

PAGE 4COUNCIL AGENDAAUGUST 12, 2015

County of Oxford ~ eAgenda Application Version 0.3.0 Agenda Version 1, Addition to Agenda►

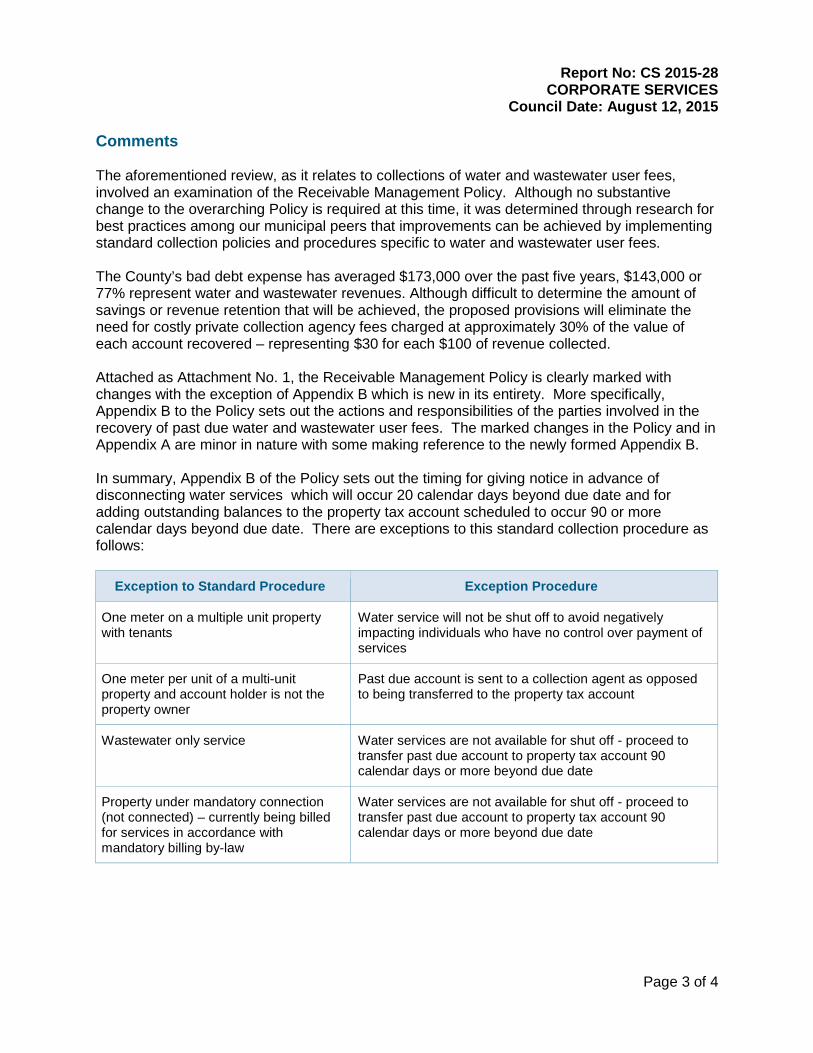

CS 2015-28Re: Receivables Management Policy Amendments

Recommendation

1. That the Receivables Management Policy be amended as set out in Attachment No. 1 to Report No. CS 2015-28, effective August 12, 2015.

10. UNFINISHED BUSINESS

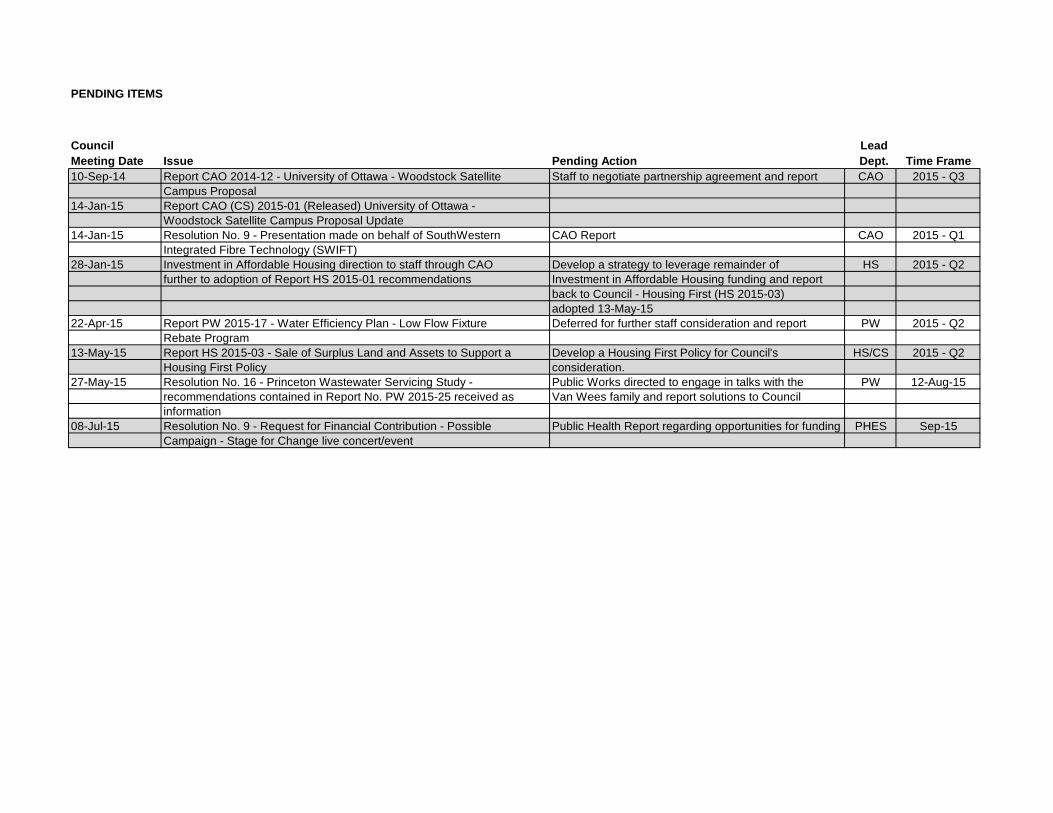

Pending Items

11. MOTIONS

12. NOTICE OF MOTIONS

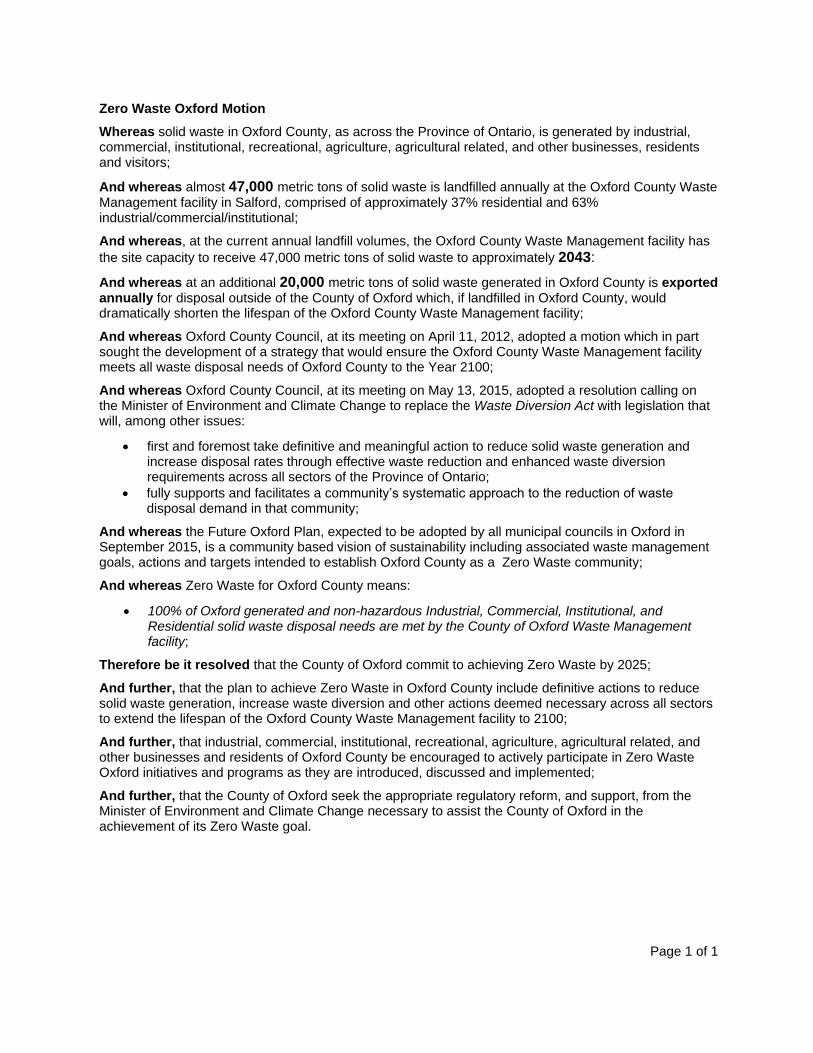

Deputy Warden Comiskey gives notice that at the September 9, 2015 meeting he willintroduce the following motion:

Link to Zero Waste Oxford Motion

13. NEW BUSINESS/ENQUIRIES/COMMENTS

14. CLOSED SESSION (Room 129)

Resolution Time ______

That Council rise and go into a Closed session for the purpose of consideringReports No. HR (CS) 2015-03, No. HR (CS) 2015-04, No. PW (CS) 2015-31,No. PW (CS) 2015-42 and a CASPO Verbal Report and associated correspondence fromGiffen Lawyers LLP, dated July 9, 2015, regarding matters that have not been madepublic concerning labour relations or employee negotiations, personal matters about anidentifiable individual, proposed or pending acquisition or disposition of land, litigation orpotential litigation and the receiving of advice that is subject to solicitor-client privilege,including communications necessary for that purpose.

Resolution Time ______

That Council rise and reconvene in Open session.

15. CONSIDERATION OF MATTERS ARISING FROM THE CLOSED SESSION

HUMAN RESOURCES

HR (CS) 2015-03

HR (CS) 2015-04

PUBLIC WORKS

PW (CS) 2015-31

PW (CS) 2015-42

PAGE 5COUNCIL AGENDAAUGUST 12, 2015

County of Oxford ~ eAgenda Application Version 0.3.0 Agenda Version 1, Addition to Agenda►

COMMUNITY AND STRATEGIC PLANNING

Verbal Report regarding matters that have not been made public concerning litigation orpotential litigation and the receiving of advice that is subject to solicitor-client privilege,including communications necessary for that purpose.

Associated Correspondence

1. Giffen Lawyers LLPJuly 9, 2015

Re: OMB Matter No.: PL130846[Closed Session Document]

16. BY-LAWS

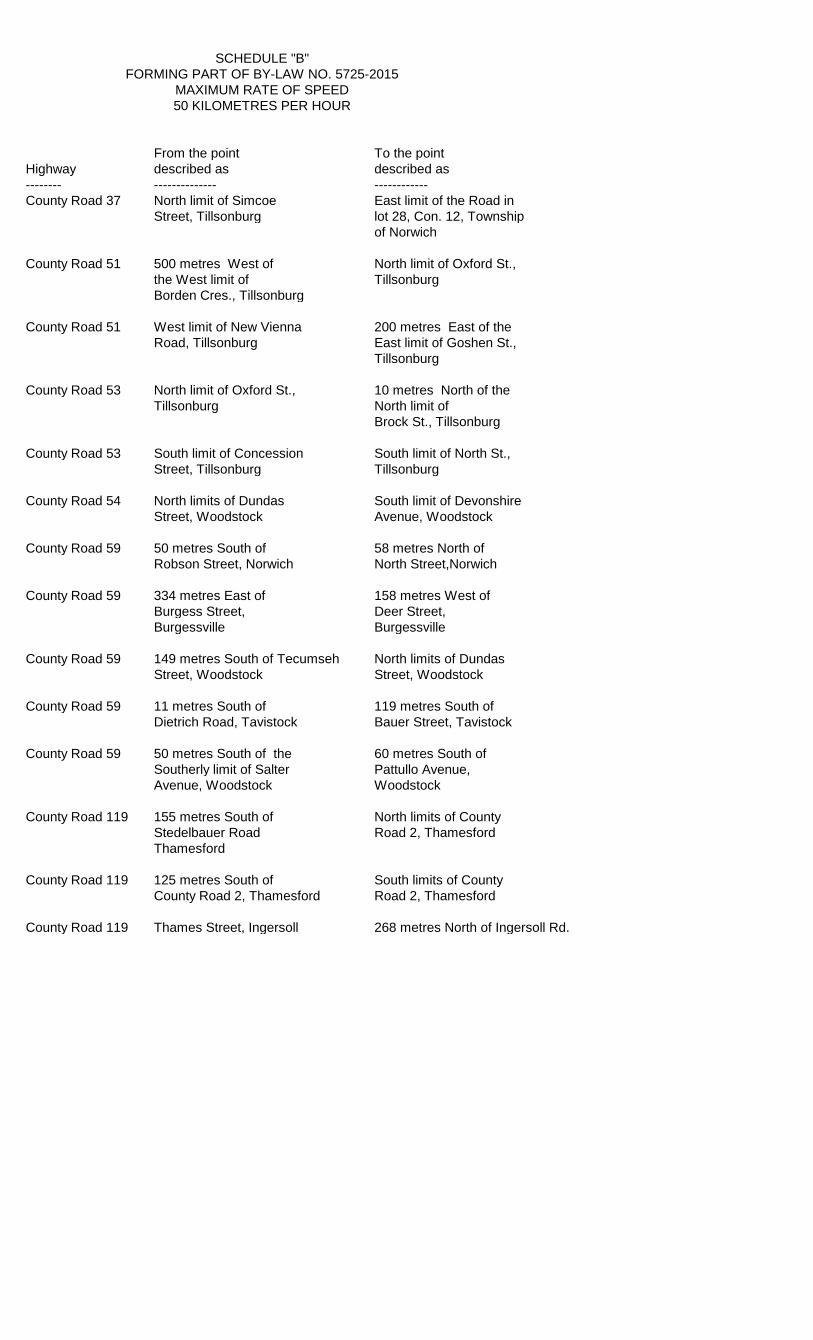

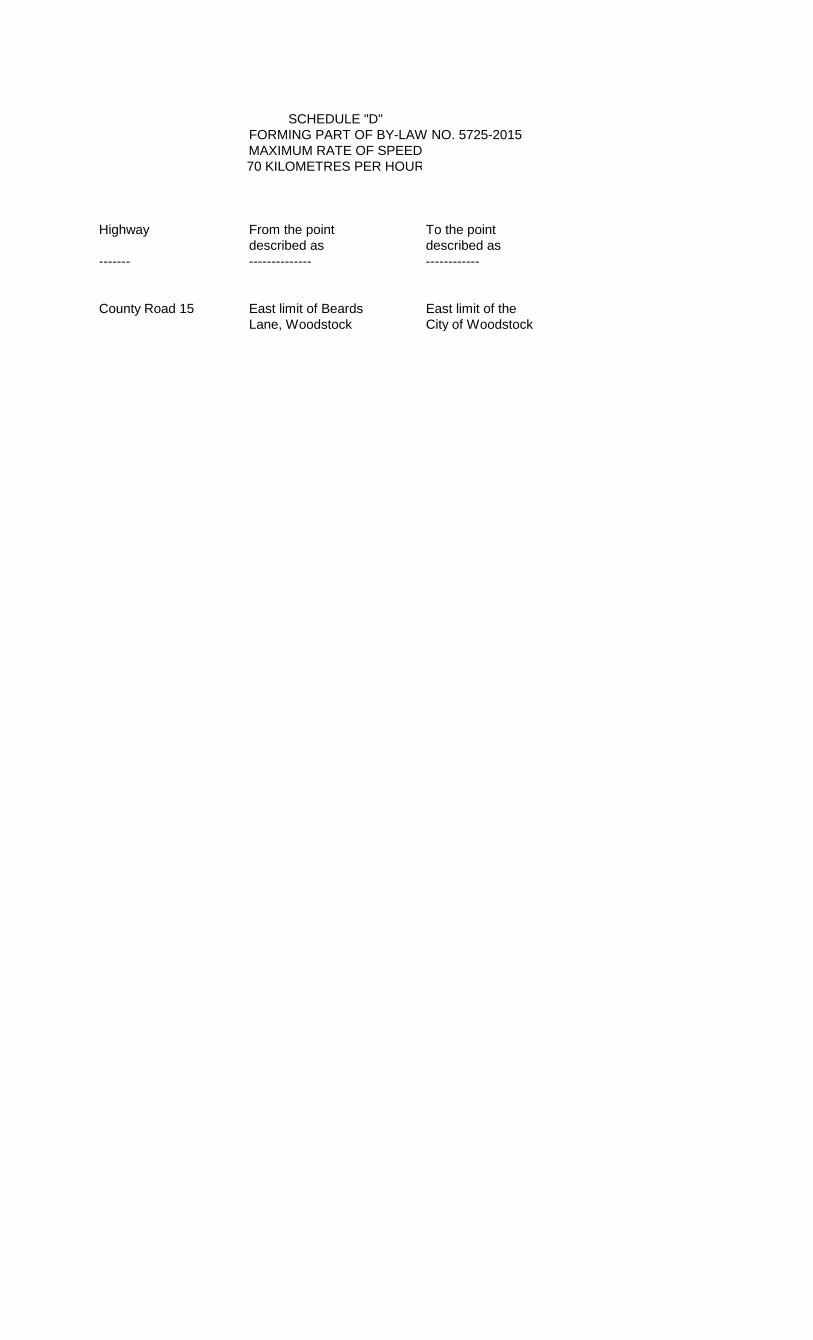

BY-LAW NO. 5725-2015Being a By-law to repeal By-law No. 3742-98 and to enact a new By-law to provide for speed limits on County Roads.

BY-LAW NO. 5726-2015Being a By-law to repeal By-law No. 3755-98.

BY-LAW NO. 5727-2015Being a By-law to amend By-law No. 5616-2014, being aBy-law to remove certain lands from Part Lot Control.

BY-LAW NO. 5728-2015Being a By-law to confirm all actions and proceedings of the Councilof the County of Oxford at the meeting at which thisBy-law is passed.

17. ADJOURNMENT Time ______

MINUTES

OF THE

COUNCIL OF THE

COUNTY OF OXFORD

County Council Chamber Woodstock July 8, 2015

MEETING #19 Oxford County Council meets in regular session this eighth day of July 2015, in the Council Chamber, County Administration Building, Woodstock. 1. CALL TO ORDER: 9:30 a.m., with Warden Mayberry in the chair. All members of Council present. Staff Present: P. M. Crockett, Chief Administrative Officer L. Beath, Director of Public Health and Emergency Services P. D. Beaton, Director of Human Services L. S. Buchner, Director of Corporate Services C. Fransen, Director of Woodingford Lodge G. K. Hough, Director of Community and Strategic Planning A. Smith, Director of Human Resources R. G. Walton, Director of Public Works B. J. Tabor, Clerk Warden Mayberry welcomes Dave MacKenzie, MP, Oxford, who is in the gallery today. D. MacKenzie brings greetings on behalf of the Federal Government. 2. APPROVAL OF AGENDA: RESOLUTION NO. 1: Moved by: Trevor Birtch Seconded by: Deborah Tait That the Agenda be approved. DISPOSITION: Motion Carried 3. DISCLOSURES OF PECUNIARY INTEREST AND THE GENERAL NATURE THEREOF: NIL 4. ADOPTION OF COUNCIL MINUTES OF PREVIOUS MEETING: Council Minutes of June 24, 2015

Page 2 July 8, 2015 RESOLUTION NO. 2: Moved by: Trevor Birtch Seconded by: Deborah Tait That the Council Minutes of June 24, 2015 be adopted. DISPOSITION: Motion Carried 5. PUBLIC MEETINGS: RESOLUTION NO. 3: Moved by: Deborah Tait Seconded by: Trevor Birtch That Council rise and go into a public meeting pursuant to Section 17(15) of the Planning Act, R.S.O. 1990, as amended, to consider an application for Official Plan Amendment for Application No. OP 15-03-8, and that the Warden chair the public meeting. DISPOSITION: Motion Carried (9:32 a.m.) 1. Application for Official Plan Amendment 751485 Ontario Inc. - OP 15-03-8

to redesignate subject lands from "Low Density Residential" to "High Density Residential" - subject lands are described as Block 117, Plan 41M-98, located on the southwest corner of Lansdowne Avenue and Nellis Street, municipally known as 1180 Nellis Street in the City of Woodstock

The Chair asks G. Hough, Director of Community and Strategic Planning, to come forward to present the application. G. Hough summarizes Official Plan Amendment Application OP 15-03-8 as is contained in Report No. CASPO 2015-138. The Chair opens the meeting to questions from members of Council. There are none. The Chair asks if anyone on behalf of the proponent wishes to speak. Steve Hunt, the owner of the property in question, states that he has nothing further to add. The Chair asks if there are any members of the public wishing to speak for or against the application. No one indicates such intent. RESOLUTION NO. 4: Moved by: Deborah Tait Seconded by: Trevor Birtch That Council adjourn the public meeting and reconvene as Oxford County Council with the Warden in the chair. DISPOSITION: Motion Carried (9:37 a.m.) CASPO 2015-138 Re: Application for Official Plan Amendment OP 15-03-8: 751485 Ontario Inc.

Page 3 July 8, 2015 RESOLUTION NO. 5: Moved by: Deborah Tait Seconded by: Trevor Birtch That the recommendations contained in Report No. CASPO 2015-138, titled “Application for Official Plan Amendment - OP 15-03-8: 751485 Ontario Inc.”, be adopted. DISPOSITION: Motion Carried Recommendations Contained in Report No. CASPO 2015-138: 1. That Oxford County Council approve the application submitted by 751485 Ontario Inc. to redesignate the subject lands from ‘Low Density Residential’ to ‘High Density Residential’ with a special development policy to facilitate the development of a 5-storey residential apartment building on lands described as Block 117, 41M-98, City of Woodstock; 2. And further, that Council approve the attached Amendment No. 190 to the County of Oxford Official Plan; 3. And further, that the necessary by-law to approve Amendment No. 190 be raised. RESOLUTION NO. 6: Moved by: Sandra Talbot Seconded by: Margaret Lupton That Council rise and go into a public meeting pursuant to Section 51(20) of the Planning Act, R.S.O. 1990, as amended, to consider an application for approval of a draft plan of subdivision, and that the Warden chair the public meeting. DISPOSITION: Motion Carried (9:39 a.m.) 2. Application for Draft Plan of Subdivision

1187688 Ontario Limited - SB 15-01-2 - subject lands are described as Part of Lots 9 & 10, Concession 17 (East Zorra), in the Township of East Zorra-Tavistock, located east of Blandford Street, bound by George Street to the south and Main Street to the north and municipally known as 77 Main Street in the Village of Innerkip

The Chair asks G. Hough, Director of Community and Strategic Planning, to come forward to present the application. G. Hough summarizes the application for Approval of Draft Plan of Subdivision as is contained in Report No. CASPO 2015-139. The Chair opens the meeting to questions from members of Council. There are none. The Chair asks if anyone on behalf of the proponent wishes to speak. Rick Dykstra, Ricor Engineering Ltd., states that they are in support of the recommendation before Council. The Chair asks if there are any members of the public wishing to speak for or against the application. No one indicates such intent. RESOLUTION NO. 7: Moved by: Sandra Talbot Seconded by: Margaret Lupton That Council adjourn the public meeting and reconvene as Oxford County Council with the Warden in the chair. DISPOSITION: Motion Carried (9:41 a.m.)

Page 4 July 8, 2015 CASPO 2015-139 Re: Application for Draft Plan of Subdivision SB 15-01-2 – 1187688 Ontario Limited RESOLUTION NO. 8: Moved by: Sandra Talbot Seconded by: Margaret Lupton That the recommendation contained in Report No. CASPO 2015-139, titled “Application for Draft Plan of Subdivision - SB 15-01-2 – 1187688 Ontario Limited”, be adopted. DISPOSITION: Motion Carried Recommendation Contained in Report No. CASPO 2015-139: 1. That Oxford County Council refer Application File No. SB 15-01-2 submitted by 1187688 Ontario Limited for draft approval of a residential plan of subdivision prepared by Ricor Engineering Limited, dated April 22, 2015, as shown on Plate 3 of Report No. CASPO 2015- 139, for lands described as Part of Lots 9 & 10, Concession 17 (East Zorra), in the Village of Innerkip to Council’s regular meeting of August 12, 2015 for final consideration. 6. DELEGATIONS AND PRESENTATIONS: 1. Oxford Drug Awareness Committee Stacey Smith, Chairperson, Oxford Stage for Change Event (Spokesperson) Re: Stage for Change Live Concert/Event to create Awareness about the Possible Campaign - proposed free event to be held in Woodstock on Friday, November 20th during Addiction Awareness Week Stacey Smith, Chairperson, Oxford Stage for Change Event, comes forward and informs Council regarding a proposed “Stage for Change” free event to be held at Woodstock Collegiate Institute (WCI) on the recently revised date of Friday, November 20th, during Addiction Awareness Week. She explains that it is a live concert/event to create awareness about the “Possible Campaign” as it relates to addiction awareness. She elaborates on information contained in correspondence from the Oxford Drug Awareness Committee which was provided as an attachment to Council’s electronic Agenda. During her presentation, S. Smith requests a financial contribution from the County in support of the event which focuses on a County problem. She stresses the importance of the community backing the event as it is possible to make changes by coming together. The Warden opens the meeting to questions from Council. S. Smith responds to questions and comments from Councillors Molnar and Talbot. 7. CONSIDERATION OF DELEGATIONS AND PRESENTATIONS: RESOLUTION NO. 9: Moved by: Ted Comiskey Seconded by: Sandra Talbot That the request for a financial contribution to the Possible Campaign, regarding a free Stage for Change live concert/event to create awareness about addiction and recovery, proposed to be held in Woodstock on Friday, November 20th during Addiction Awareness Week, be received with a Report back to Council from Public Health regarding opportunities for funding. DISPOSITION: Motion Carried

Page 5 July 8, 2015 8. CONSIDERATION OF CORRESPONDENCE: NIL 9. REPORTS FROM DEPARTMENTS: COMMUNITY AND STRATEGIC PLANNING CASPO 2015-138 Re: Application for Official Plan Amendment OP 15-03-8: 751485 Ontario Inc. Report dealt with under Public Meetings. CASPO 2015-139 Re: Application for Draft Plan of Subdivision SB 15-01-2 – 1187688 Report dealt with under Public Meetings. PUBLIC WORKS PW 2015-38 Re: Road Improvements – Part of Oxford Road 8 Construction Contract RESOLUTION NO. 10: Moved by: Ted Comiskey Seconded by: Sandra Talbot That the recommendations contained in Report No. PW 2015-38, titled “Road Improvements – Part of Oxford Road 8 Construction Contract”, be adopted. DISPOSITION: Motion Carried Recommendations Contained in Report No. PW 2015-38: 1. That County Council awards a contract to Steve Smith Construction, in the amount of $1,715,855 plus HST for road improvements on part of Oxford Road 8 (west limit of Hickson to the 10th Line); 2. And further, that a by-law be raised authorizing the Chief Administrative Officer to sign all documents related thereto. PW 2015-39 Re: Disposal of Oxford County Owned Lands at Balsam Street, Innerkip (Designated as Part 9 on Plan 41R-2592) RESOLUTION NO. 11: Moved by: Stephen Molnar Seconded by: Larry Martin That the recommendations contained in Report No. PW 2015-39, titled “Disposal of Oxford County Owned Lands at Balsam Street, Innerkip (Designated as Part 9 on Plan 41R-2592)”, be adopted. DISPOSITION: Motion Carried

Page 6 July 8, 2015 Recommendations Contained in Report No. PW 2015-39: 1. That Oxford County Council declare County owned land on Balsam Street, Innerkip (designated as Part 9 on Plan 41R-2592) as surplus and authorize the disposal of the land. 2. And further, that staff be authorized to enact a by-law to declare the lands surplus. PW 2015-36 Re: Oxford County Applications to Independent Electricity System Operator (IESO) Feed-in Tariff Program RESOLUTION NO. 12: Moved by: Stephen Molnar Seconded by: Larry Martin That the recommendations contained in Report No. PW 2015-36, titled “Oxford County Applications to Independent Electricity System Operator (IESO) Feed-in Tariff Program”, be adopted. DISPOSITION: Motion Carried Recommendations Contained in Report No. PW 2015-36: 1. That County Council authorize the Chief Administrative Officer to submit an application to the Independent Electricity System Operator (IESO) Feed-in-tariff program for the project as outlined in Report PW 2015-36; 2. And further, that the Township of South-West Oxford be requested to support by Council Resolution the proposed Oxford County SmallFIT project at the County of Oxford’s Landfill in Salford. PW 2015-40 Re: 75 Graham Street Limited License Agreement for the Victim Witness Assistance Program (VWAP) RESOLUTION NO. 13: Moved by: Larry Martin Seconded by: Stephen Molnar That the recommendation contained in Report No. PW 2015-40, titled “75 Graham Street Limited License Agreement for the Victim Witness Assistance Program (VWAP)”, be adopted. DISPOSITION: Motion Carried Recommendation Contained in Report No. PW 2015-40: 1. That a by-law be raised to authorize the Chief Administrative Officer to execute a short term license Agreement with Her Majesty the Queen in Right of Ontario as represented by the Minister of Economic Development, Employment and Infrastructure, for 8,586 square feet of space at 75 Graham Street, Woodstock Ontario for a term not to exceed September 30, 2015. PW 2015-35 Re: Ingersoll Sanitary Sewer and Watermain Extension Project

Page 7 July 8, 2015 RESOLUTION NO. 14: Moved by: Larry Martin Seconded by: Stephen Molnar That that the recommendation contained in Report No. PW 2015-35, titled “Ingersoll Sanitary Sewer and Watermain Extension Project”, be adopted. DISPOSITION: Motion Carried Recommendation Contained in Report No. PW 2015-35: 1. That By-law No. 5718-2015, being a by-law to authorize the funding sources and mandatory connection for the Ingersoll Sanitary Sewer and Watermain Extension be presented to Council for enactment. CORPORATE SERVICES CS 2015-23 Re: Tax Recoveries By-law - 2015 RESOLUTION NO. 15: Moved by: Marion Wearn Seconded by: Stephen Molnar That that the recommendations contained in Report No. CS 2015-23, titled “Tax Recoveries By-law - 2015”, be adopted. DISPOSITION: Motion Carried Recommendations Contained in Report No. CS 2015-23: 1. That Council approves funding of the Maximum Tax Protection Mechanism for the County’s portion of taxes for the Year 2015 to be recovered within the same tax class by clawing back from decreasing properties; 2. And further, that By-law No. 5719-2015, being a by-law to establish decrease limits for certain property classes for the Year 2015, be presented to Council for enactment. CS 2015-24 Re: 2016 Draft Budget Schedule RESOLUTION NO. 16: Moved by: Marion Wearn Seconded by: Stephen Molnar That that the recommendation contained in Report No. CS 2015-24, titled “2016 Draft Budget Schedule”, be adopted. DISPOSITION: Motion Carried Recommendation Contained in Report No. CS 2015-24: 1. That the 2016 draft budget schedule as set out in Report No. CS 2015-24 be approved. CS 2015-25 Re: OILC Financing Application – Woodstock

Page 8 July 8, 2015 RESOLUTION NO. 17: Moved by: Margaret Lupton Seconded by: Ted Comiskey That that the recommendation contained in Report No. CS 2015-25, titled “OILC Financing Application – Woodstock”, be adopted. DISPOSITION: Motion Carried Recommendation Contained in Report No. CS 2015-25: 1. That By-law No. 5722-2015, being a by-law to authorize the submission of an application to the Ontario Infrastructure Lands Corporation for temporary and long-term borrowing through the issue of debentures for the purposes of the City of Woodstock, be presented to Council for enactment. HUMAN SERVICES HS 2015-08 Re: 10 Year Shelter Plan Annual Progress Report RESOLUTION NO. 18: Moved by: Margaret Lupton Seconded by: Ted Comiskey That that the recommendation contained in Report No. HS 2015-08, titled “10 Year Shelter Plan Annual Progress Report”, be adopted. DISPOSITION: Motion Carried Recommendation Contained in Report No. HS 2015-08: 1. That County Council receive the 2014 Annual Progress Report of the Oxford County 10 Year Shelter Plan as attached to Report 2015-08. 10. UNFINISHED BUSINESS: Pending Items No discussion takes place regarding the Pending Items list. 11. MOTIONS: NIL 12. NOTICE OF MOTIONS: NIL 13. NEW BUSINESS/ENQUIRIES/COMMENTS: Deputy Warden Comiskey gives Council an update on the Canterbury Folk Festival to be held in Ingersoll this weekend. He thanks the many volunteers and extends an invitation to all to attend. 14. CLOSED SESSION: NIL

Page 9 July 8, 2015 15. CONSIDERATION OF MATTERS ARISING FROM THE CLOSED SESSION: Not Required. 16. BY-LAWS: BY-LAW NO. 5718-2015 Being a By-law to mandate connection to and impose the cost of the water and sanitary sewage system to the area designated and referred to as the South Ingersoll (Kirwin Dr., Pine St., Elm St. and Royland Cres.) Sewer and Watermain Extension Project. BY-LAW NO. 5719-2015 Being a By-law to Establish Decrease Limits for Certain Property Classes for the Year 2015. BY-LAW NO. 5720-2015 Being a By-law to authorize the Chief Administrative Officer to execute contract documents between the County of Oxford and Steve Smith Construction Corporation for road improvements on part of Oxford Road 8 (west limit of Hickson to the 10th Line). BY-LAW NO. 5721-2015 Being a By-law to authorize the Chief Administrative Officer to execute a License Agreement, No. L12253, with Her Majesty the Queen in Right of Ontario as represented by the Minister of Economic Development, Employment and Infrastructure, for space at 75 Graham Street, Woodstock. BY-LAW NO. 5722-2015 Being a By-law to authorize the submission of an application to Ontario Infrastructure and Lands Corporation ("OILC") for financing certain ongoing capital works of the Corporation of the City of Woodstock; and to authorize long term borrowing for such works through the issue of debentures by County of Oxford (The "Upper-tier Municipality") to OILC. BY-LAW NO. 5723-2015 Being a By-law to adopt Amendment Number 190 to the County of Oxford Official Plan. BY-LAW NO. 5724-2015 Being a By-law to confirm all actions and proceedings of the Council of the County of Oxford at the meeting at which this By-law is passed. RESOLUTION NO. 19: Moved by: Don McKay Seconded by: Margaret Lupton That the following By-laws be now read a first and second time: No. 5718-2015, No. 5719-2015, No. 5720-2015, No. 5721-2015, No. 5722-2015, No. 5723-2015 and No. 5724-2015. DISPOSITION: Motion Carried

Page 10 July 8, 2015 RESOLUTION NO. 20: Moved by: Don McKay Seconded by: Margaret Lupton That the following By-laws be now given third and final reading: No. 5718-2015, No. 5719-2015, No. 5720-2015, No. 5721-2015, No. 5722-2015, No. 5723-2015 and No. 5724-2015. DISPOSITION: Motion Carried 17. ADJOURNMENT: Council adjourns its proceedings until the next meeting scheduled for Wednesday, August 12, 2015 at 9:30 a.m. 10:15 a.m. Minutes adopted on by Resolution No.

WARDEN

CLERK

July 21, 2015

Ms. Brenda Tabor County Clerk County of Oxford 21 Reeve Street P.O. Box 1614 Woodstock, ON N4S 7Y3

Dear Ms. Tabor

TOWNSHIP OF ZORRA 274620 271h Line, PO Box 306 Ingersoll , ON, N5C 3K5

Ph. (519) 485-2490 • 1-888-699-3868 •Fax (519) 485-2520

Re: Township of Zorra Resolutions

Please be advised the Township of Zorra passed the following resolution at the July 14, 2015 Council meeting :

"WHEREAS the Community Schools Alliance continues to advocate for a closer working relationship between school boards and municipal councils; AND WHEREAS both municipalities and school boards represent the same residents, both should regard our schools as critically important components of our public infrastructure and both should work together to ensure our communities are well served by those schools; AND WHEREAS the Community Schools Alliance advocates for changes that are needed to protect our schools and to protest changes that threaten them; AND WHEREAS in order to be effective with its advocacy, it requires needed research, resources and municipal support; NOW THEREFORE BE IT RESOLVED THAT Zorra Township become a member of the Community Schools Alliance for 2015 at a rate of $250 supported from the Township general funds budget and this membership be brought forward to the 2016 Township budget as a new initiative for further consideration and forwarded to Oxford County Council and all Oxford County Municipalities for consideration." Disposition: Carried

Please let me know if you have any questions.

Yours truly.

~~~ ~artin Clerk

Internet: www.zorra.on .ca Email: zorra@zorra .on.ca

THE CORPORATION OF THE TOWNSHIP OF NORWICH

February 6, 2014

County of Oxford PO Box 1614 Woodstock, ON N4S 7Y3

Dear Warden McKay and County Councillors

COUNTY OF OXFORD CAO/CLERK'S OFFICE

RECEIVED

JUL 2 1 2015

REFER TO _,_ft.,_,,,.11""Al,..d=<>=' ~---File/EDMS: ______ _

Please be advised that at their meeting held July 14, 2015, the Council of the Township of Norwich adopted the following resolution:

"That the Council of the Township of Norwich advise County Council that the Township supports the application for draft approval of a proposed condominium submitted by 487223 Ontario Limited (Garbriel Kirchberger), File No. CD 15-02-3; prepared by J.H. Cohoon Engineering Limited, and dated June 3, 2015, for lands described as Part Lot 677, Plan 955, in the Village of Norwich.

And further, that the Council of the Township of Norwich advise County Council that the Township supports the application for exemption from draft plan of condominium approval process submitted by 487223 Ontario Limited, (Gabriel Kirchberger), File No. CD15-02-3; prepared by J.H. Cohoon Engineering Limited, and dated June 3, 2015, for lands described as Part Lot 677, Plan 955, in the Village of Norwich, as all matters relating to the development have been addressed through the Site Plan Approval process and a registered site plan agreement."

Should ·you require any further information, please do not hesitate to contact the undersigned.

Yours truly

'1)~'\1J~4\, ~· Kimberley Armstrong 0 Deputy Clerk

cc. Community & Strategic Planning Department

The Corporation of The Township of Norwich 285767 Airport Road, Norwich, ON, NOJ 1 PO

Phone (519) 468-2410 Fax:(519) 468-2414 www.norwich.ca

. .Randy Pettapiece, MPP

COUNTY OF OXFORD CAO/CLERK'S OFFICE

RECEIVED

JUL 2 4 2015 Perth-Wellington Constituency Office Perth-Wellington • ;J

Stratford, Ontario REFERT0.1.fC.1.J2JLIALld<:&JJ"""-' -----

July 21, 2015 File/EDMS: ______ _

Brenda). Tabor Clerk County of Oxford 21 Reeve St PO Box 1614 Woodstock, ON N4S 7Y3

Dear Ms. Tabor:

Re: Resolution for Fairness in Provincial Infrastructure Funds

I am writing to inform you of my upcoming private member's resolution in the Ontario legislature and to formally request your support. It reads as follows:

That, in the opinion of this House, the government should guarantee thatgovernmentheld ridings and opposition-held ridings be given equal and transparent consideration on infrastructure funding, and that when funding decisions are made, should guarantee that all MPPs, whether in government or opposition, be given fair and equal advance notice of the official announcement.

The basis for my resolution is simple: When municipalities apply for provincial infrastructure funding, you should expect that your application would be evaluated based on merit. You should expect that it would be evaluated promptly, based on well-defined and transparent criteria. Finally, you should expect that the decision to approve your application would never depend on your MPP's political stripe.

There is, after all, no such thing as Liberal, PC or NDP infrastructure money; there is only public money. That money comes from taxes that we all pay; everyone in the province should expect a similar quality of infrastructure and services, regardless of where they live.

Because municipalities rely on provincial partnerships to fund critical infrastructure projects, the consequences of provincial funding decisions can be far-reaching. The provincial government must respect this partnership and ensure that government and opposition-held ridings are given equal consideration when it comes to infrastructure investment decisions. Too often, however, there is at least a persistent perception that public infrastructure dollars have, in at least some cases, been directed according to politics and not according to need.

. .. /2

Constituency Office • 55 Lorne Avenue East • Stratford, Ontario N5A 6S4 •Tel. (519) 272-0660 •Toll-free: 1-800-461-9701 • Fax (519) 272-1064 E-mail: [email protected]

Having served as a municipal councillor, I know that the process to apply for infrastructure funding is a major-and sometimes frustrating-undertaking. It often entails significant red tape and investments of staff time and resources. Before making those investments, municipalities need some assurance that, based on clear criteria, your application has a reasonable chance of success. You also need to know that your MPP will advocate on your behalf and, most importantly, decision-makers will be receptive to that advocacy no matter if the MPP serves in government or opposition.

The final section of my resolution deals with infrastructure announcements themselves. These announcements must, I believe, be depoliticized irt order to address the perception that opposition-held ridings are disadvantaged-or worse yet, being punished-for voting against the government.

If your municipality supports the intent of my resolution, I would encourage you to consider passing a formal resolution to support it. If your Council decides to proceed in this way, I would appreciate receiving a copy of your resolution as soon as possible. Debate on this resolution is scheduled for October 8, 2015.

I would appreciate your views on this matter, and your own experience in your municipality concerning access to provincial infrastructure funds. If you have any feedback on this issue, or if you require any additional information, please don't hesitate to contact me at 519-272-0660 or by email: [email protected].

Thank you very much for your consideration.

Sincerely, {/)

1::v,,?/7wl! £/;;:7 '···.") j[/;l () £,<'t>"~~~.,-c

Randy Pettapiece, MPP Perth-Wellington

That the July 21, 2015 letter from Randy Pettapiece, MPP Perth-Wellington regarding his request for support of a proposed Resolution for Fairness in Provincial Infrastructure Funds be received as information; And further, that the County of Oxford envisions the proposed Moving Ontario Forward program for infrastructure investment outside of the Greater Toronto and Hamilton Area (GTHA) as an opportunity for strategic infrastructure investment and that, in partnership with the Federal Government, could stimulate and strengthen the provincial and national economy while addressing significant deficits and needs in key infrastructure outside of the GTHA; And further, that the County of Oxford expects Southwestern Ontario to receive its fair and non-partisan share of the Moving Ontario Forward infrastructure investment in a manner which:

advances Southwestern Ontario’s key infrastructure needs and priorities;

optimizes the strategic and transformational potential of the investment program; and

strengthens strategic federal, provincial, and municipal partnerships; And further, that significant attention be given to the strategic and transformational value of investment in Southwestern Ontario’s mobility, connectivity, vitality, and inclusivity through strategic investments in:

the proposed SWIFT ultra high-speed fibre network;

the provincial network of highways, interchanges, and bridges;

the major municipal road and bridge network;

Network Southwest and ongoing enhancements to the VIA passenger rail system and a fully integrated bus feeder (motor coach) network connecting communities across Southwestern Ontario to the rail corridor and each other;

municipal (urban) transit systems;

current Go Transit service areas;

municipal community infrastructure; and

quality of life investments in social housing And further that the Warden write Mr. Pettapiece, the Honourable Kathleen Wynne, the Honourable Deb Matthews and the Honourable Brad Duguid regarding this resolution.

Report No: PW 2015-37 PUBLIC WORKS

Council Date: August 12, 2015

Page 1 of 3

To: Warden and Members of County Council

From: Director of Public Works

Oxford Road 12 Parking Report

RECOMMENDATION

1. That Schedule E within By-law No. 4897-2007 be amended to include, and staffauthorized to implement a “No Parking” designation on Oxford Road 12 (MillStreet), as included within the approved Oxford Road 12 Class EnvironmentalAssessment.

REPORT HIGHLIGHT

Seeking Council approval for the implementation of a “No Parking” designation on the east side of Oxford Road 12 between Park Row and Spencer Street and the west side between Fifth Avenue and Spencer Street. The Oxford Road 12 roadway is outlined in Attachment 1.

Implementation Points

Implementation of the recommended removal of on-street parking will allow cycling lanes to be constructed and improve roadway safety.

Signage would be placed in the ”No Parking” designated area in accordance with the Ontario Traffic Manual and roadway paint markings revised accordingly.

Financial Impact

The cost to install signs is estimated to be $300. The cost of line painting is estimated to be $3,000. Funding is available within the approved 2015 Roads Operations Budget.

The Treasurer has reviewed this report and agrees with the financial impact information.

Risks/Implications

Risks and implications of the removal of paving on Mill Street was considered during the Class EA conducted in 2014.

Report No: PW 2015-37 PUBLIC WORKS

Council Date: August 12, 2015

Page 2 of 3

Strategic Plan (2015-2018)

County Council adopted the County of Oxford Strategic Plan (2015-2018) at its regular meeting held May 27, 2015. The initiative contained within this report supports the Values and Strategic Directions as set out in the Strategic Plan as it pertains to the following Strategic Directions:

1. ii. A County that Works Together – Enhance the quality of life for all of our citizens by:

- Maintaining and strengthening core infrastructure, including affordable housing and fibre optic systems infrastructure

5. ii. A County that Performs and Delivers Results - Deliver exceptional services by:

- Regularly reviewing service level standards to assess potential for improved access to services / amenities

DISCUSSION

Background

The Municipal Class Environmental Assessment for Oxford Road 12 (Mill Street), Report PW 2014-63, outlines the requirement to eliminate on-street parking. The removal of on-street parking provides the physical space to safely accommodate bike lanes.

Comments

Existing on-street parking on the east side of Oxford Road 12 from Park Row to Spencer Street and on the west side from Fifth Avenue to Spencer Street are the only on-street parking currently permitted along Oxford Road 12.

On-street parking in both areas along Oxford Road 12 is not required for residential properties, as all homes in these areas have adequate driveways to facilitate parking. On-street parking is a sensitive issue and could cause concern with adjacent residents. Through the Class EA process for Oxford Road 12, directly affected property owners and the City of Woodstock were engaged during the study.

Elimination of the on-street parking improves the overall safety for the travelling motorists, cyclists and pedestrians.

Funding for the installation of the “No Parking” signs and paint markings would be funded through the approved 2015 Roads Operations budget.

Staff have been in discussion with City of Woodstock Engineering regarding the removal of on-street parking and they are in agreement. City staff will be reporting on changes to the City parking by-law to accommodate this change at the August 13, 2015 City Council Meeting.

Report No: PW 2015-37 PUBLIC WORKS

Council Date: August 12, 2015

Page 3 of 3

Conclusions

Staff are of the opinion that the proposed amendments to By-law 4897-2007, are required to implement the measures outlined in the Mill Street Class EA and to implement the cycling lanes on Mill Street and Parkinson Road as per the County Transportation Master Plan and the City of Woodstock Cycling Master Plan.

SIGNATURES

Report Author:

Original signed by:

Melissa Abercrombie, P.Eng. Manager of Roads and Facilities

Departmental Approval:

Original signed by:

Robert Walton, P.Eng. Director of Public Works

Approved for submission:

Original signed by:

Peter M. Crockett, P.Eng. Chief Administrative Officer

ATTACHMENT

Attachment 1 Oxford Road 12 Woodstock, June 22, 2015 (MA/DA)

0 50 100 150 20025Meters

KEY PLAN

SITE

Woodstock

Attachment 1 to PW 2015-37August 12, 2015

Report No: PW 2015-43

PUBLIC WORKS Council Date: August 12, 2015

Page 1 of 4

To: Warden and Members of County Council

From: Director of Public Works

Trans Canada Trail

RECOMMENDATIONS 1. That County Council authorize staff to negotiate an agreement with the Township

of Norwich and the Town of Tillsonburg for the construction and operation of the Trans Canada Trail (TCT) from the existing TCT in Tillsonburg easterly to Norfolk County and the proposed trail under the Canada 150 Community Infrastructure Program from Tillsonburg to Springford, including County financing of the project subject to final approval of County Council;

2. And further, that County staff work with Norwich and South-West Oxford

Townships and the Town of Tillsonburg to undertake Public Consultation for the proposed trails on County owned lands including the TCT extension and those seeking partnership funding through the Canada 150 Community Infrastructure Program in Norwich and South-West Oxford Townships.

REPORT HIGHLIGHTS Total cost of the trail is estimated at $870,000, and $510,000 in funding has been secured

from the TCT and the Pan Am Games Legacy Funding.

Tillsonburg and Norwich Councils are considering the proposed partnerships at their August 10 and 11, 2015 meetings respectively.

It is important that Public Consultation start as soon as practical such that funding deadlines set out in the grant programs can be achieved.

Implementation Points This section of the TCT is identified in the County of Oxford Trails Mater Plan. The proposed project follows the trails development model in the Master Plan including partnerships in this case with two area municipalities, with the County assisting to facilitate the inter-municipal project on County owned lands. Public Consultation will be essential to identify public needs and concerns with respect to the trail design, construction and operations.

Report No: PW 2015-43

PUBLIC WORKS Council Date: August 12, 2015

Page 2 of 4

Financial Impact The 2015 County Budget anticipated the staff time and bridge improvements required for the TCT project. The money required to fund the area municipal portion of this project, estimated at $360,000, will be financed through the County. The agreements with the area municipalities will detail the repayment program. The Treasurer has reviewed this report and agrees with the financial impact information.

Risks/Implications This project has numerous risks and implications. Many of these will be identified and dealt with through the Public Consultation and through the agreements with the area municipalities. One major risk is in losing the grant funding if the project does not proceed soon.

Strategic Plan (2015-2018) County Council adopted the County of Oxford Strategic Plan (2015-2018) at its regular meeting held May 27, 2015. The initiative contained within this report supports the Values and Strategic Directions as set out in the Strategic Plan as it pertains to the following Strategic Directions:

1. i. A County that Works Together – Strengthen, diversify and broaden the economic/prosperity base through:

- Strategies to retain and support existing businesses and grow our green economy

2. i. A County that is Well Connected – Improve travel options beyond the personal vehicle by:

- Creating, enhancing and promoting the use of an integrated trail and bike path system - Promoting active transportation

4. i. A County that Informs and Engages - Harness the power of the community through conversation and dialogue by:

- Understanding and addressing public aspirations for a more livable community

DISCUSSION

Background Attachment 1 is a map showing the proposed TCT and the proposed trails applied for under the Canada 150 Community Infrastructure Program. Reports PW 2014-67 of December 10, 2014 and PW 2013-75 of December 11, 2013 and the Oxford County Trails Master Plan (adopted by County Council September 10, 2014) provide much of the background information for this report.

Report No: PW 2015-43

PUBLIC WORKS Council Date: August 12, 2015

Page 3 of 4

Since December 2014 the following actions or issues have arisen: 1. Grants in the amount of $310,000 from the TCT and $200,000 from the Pan Am/Para Pan

Am Games Legacy Funding have been approved. The funding deadlines are March 2016 for the Pan Am Funding and 2017 for TCT funding.

2. On May 27, 2015 County Council approved Resolution No. 10 to apply for funding under the Canada 150 Community Infrastructure Program for expansion of the trail system. The expansion as shown on Attachment 1 includes trails in the Townships of South-West Oxford and Norwich and the Town of Tillsonburg. The funding for these projects is to be from long term financing through the County paid over time by the area municipalities involved.

3. At their respective Council Meetings on August 10 and 11, 2015 the Town of Tillsonburg and the Township of Norwich will be considering staff reports for a partnership agreement on the TCT and the Canada 150 Community Infrastructure Program extension from Tillsonburg to Norwich (subject to funding approval). Attachment 2 is a letter from Tillsonburg confirming this.

4. The Township of South-West Oxford has agreed to complete the Canada 150 Community Infrastructure Program extension from Tillsonburg to Brownsville subject to funding approval.

5. Approval of the Canada 150 Community Infrastructure Program Fund timing is not yet known.

Comments The previous reports outlined all the tremendous benefits of these projects including exercise, tourism, active transportation and healthy living. At this time, the trail extensions proposed by the Canada 150 Community Infrastructure Program have not received funding approval but planning and Public Consultation towards eventual implementation could commence along with the TCT Public Consultation. The proposed agreement between the Town of Tillsonburg and Township of Norwich for construction of the TCT (to be ratified by each Council meeting August 10 and 11, 2015 respectfully) and Public Consultation are the remaining items to be completed to allow this project to proceed. Time is of the essence to proceed with the Public Consultation to meet the project funding deadlines.

Report No: PW 2015-43

PUBLIC WORKS Council Date: August 12, 2015

Page 4 of 4

Conclusion The project to construct the TCT and the planned extensions considered by the Canada 150 Community Infrastructure Program are important projects identified in the County of Oxford Trails Master Plan. The partnerships established to execute these projects are exactly as envisioned in the Trails Master Plan. It is hoped that the next steps to move forward with this project are realized so that Public Consultation and construction follow very soon.

SIGNATURES

Report Author: Original signed by: Robert Walton, P.Eng. Director of Public Works

Approved for submission: Original signed by:

Peter M. Crockett, P.Eng. Chief Administrative Officer

ATTACHMENTS Attachment 1 Proposed TCT and proposed trails Attachment 2 Correspondence from Tillsonburg regarding upcoming Council Meeting

KEY PLAN

Attachment 1 for PW 2015-43August 12, 2015

0 5.5 112.75Kilometers

OXFORD COUNTY

Proposed Trails for Canada 150Community Infrastructure

Proposed Trans-Canada Trail

Existing Trans-Canada Trail

TOWNSHIP OFSOUTH-WEST

OXFORD

TOWNSHIP OFNORWICH

Attachment 2 for PW 2015-43August 12, 2015

Report No: PW 2015-41 PUBLIC WORKS

Council Date: August 12, 2015

To: Warden and Members of County Council

From: Director of Public Works

Drumbo Wide Area Network Tower Relocation and Replacement

RECOMMENDATION

1. That County Council authorize Public Works to proceed in 2015 with the unanticipated relocation and replacement of the Drumbo wide area network tower at a cost of $225,000, to be financed from the Facilities Reserve.

REPORT HIGHLIGHTS

To obtain County Council approval to undertake construction of the new tower that was notanticipated during preparation of the 2015 Capital Budget.

Implementation Points

If Council approves this report, staff will proceed to undertake this work.

Financial Impact

The cost for this work was not included in the 2015 Budget and is estimated to be $225,000. If approved the construction would be funded from the Facilities Reserve. The Facilities Reserve is estimated to have a 2015 ending balance of $3,261,637.

The Treasurer has reviewed this report and agrees with the financial impact information.

Risks/Implications

If this report is not approved the County would be in a position of liability exposure as the tower’s structural integrity has diminished. There is also the issue of diminished connectivity due to the growing canopy which presents operational difficulty to clients/staff that require network access.

Page 1 of 3

Report No: PW 2015-41 PUBLIC WORKS

Council Date: August 12, 2015

Strategic Plan (2015-2018)

County Council adopted the County of Oxford Strategic Plan (2015-2018) at its regular meeting held May 27, 2015. The initiative contained within this report supports the Values and Strategic Directions as set out in the Strategic Plan as it pertains to the following Strategic Directions:

1. ii. A County that Works Together – Enhance the quality of life for all of our citizens by:

- Adapting programs, services and facilities to reflect evolving community needs - Working with community partners and organizations to maintain / strengthen public safety

2. iii. A County that is Well Connected – Strengthen community access and Internet connectivity

3. iii. A County that Thinks Ahead and Wisely Shapes the Future - Demonstrated commitment to sustainability by:

- Ensuring that all significant decisions are informed by assessing all options with regard to the community, economic and environmental implications including:

o Life cycle costs and benefit/costs, including debt, tax and reserve levels andimplications

DISCUSSION

Background

The County has and continues to partner with area municipalities, sharing communications infrastructure to better the programs in helping the citizens of Oxford County. The County’s shared municipal wide area network towers are a crucial and valuable, point to point infrastructure for communications. These towers provide a desirable location for our municipal and community partners to mount important communication strategies such as the Township Fire Communications Network.

Comments

The five Townships are currently upgrading their Public Safety Emergency Radio Communication System. Part of the upgrade will require a microwave dish on the Drumbo wide area network tower located at the Drumbo County Works Yard. A structural assessment and subsequent report was completed as per County procedures when reviewing requests to add devices to County owned communications towers. The report summary stated the condition of the Drumbo tower foundation is not acceptable creating an overload condition. Consequentially, the tower cannot support any additional load from communication devices such as requested by the Townships until this structural issue is corrected.

The recommended repair will require the antennas/devices currently fixed on the tower removed, the tower relocated, on site, a new engineered footing and structural base installed with the antennas remounted to the tower, please refer to Attachment 1.

Page 2 of 3

Report No: PW 2015-41 PUBLIC WORKS

Council Date: August 12, 2015

Further, the Drumbo tower has been experiencing connectivity issues due to the ongoing growing canopy. Staff is recommending installing a new 185’ tower to replace the existing 150’ tower which will correct any connectivity issues stemming from the current canopy growth and for years to come.

Repairs to correct the towers current condition falls under the County purview and should be followed through to ensure the structural integrity of the tower is sound are keeps the County out of a position of liability. Addressing the connectivity issues with the installation of a new taller tower will eliminate the need to revisit this tower for remediation in the future to compensate for the uncontrolled growth of canopy avoiding anticipated escalated construction costs. Once a new tower has been erected and structural needs corrected the additional devices requested for installation by the Townships would be allowed.

Conclusions

If approved by Council, staff will proceed with the design and construction of a new Drumbo shared municipal wide area network tower in 2015.

SIGNATURES

Report Author:

Original signed by:

Sam Pennisi Supervisor of Facilities

Departmental Approval:

Original signed by:

Robert Walton P.Eng. Director of Public Works

Approved for submission:

Original signed by:

Peter M. Crockett, P.Eng. Chief Administrative Officer

ATTACHMENT

Attachment #1: Existing and New Location of Drumbo Network Tower

Page 3 of 3

EXISTING NETWORK TOWER

7.62m+/-

NEW NETWORK TOWERLOCATION PERIMETER

EMS

OXFORD ROAD 3

895939

DrumboPatrolYard

Attachment 1 to PW 2015-41 August 12, 2015

Oxford Road 29

Oxford Road 3

KEY PLAN

InnerkipDrumbo

Tower

Report No: CASPO 2015-159 COMMUNITY AND STRATEGIC PLANNING

Council Date: August 12, 2015

Page 1 of 2

To: Warden and Members of County Council

From: Director of Community and Strategic Planning

Application for Draft Plan of Subdivision SB 15-01-2; 1187688 Ontario Limited

RECOMMENDATION 1. That Oxford County Council grant draft plan approval to a proposed plan of

subdivision submitted by 1187688 Ontario Limited (File No. SB 15-01-2), prepared by Ricor Engineering Limited, dated April 22, 2015, as shown on Plate 3 of Schedule “A” of Report No. CASPO 2015-159, for lands described as Part of Lots 9 & 10, Concession 17 (East Zorra), in the Village if Innerkip, subject to the conditions attached as Schedule “A” to this Report being met prior to final approval.

REPORT HIGHLIGHTS The purpose of this report is to consider draft plan approval of a residential plan of

subdivision within the Township of East Zorra-Tavistock.

Implementation Points This application will be implemented in accordance with the relevant policies contained in the Official Plan.

Financial Impact The approval of this application will have no financial impact beyond what has been approved in the current year’s budget. The Treasurer agrees with this financial impact statement.

Risks/Implications There are no risks or other implications anticipated as a result of this application beyond those that can reasonably be expected for any such proposal with respect to potential appeals to the Ontario Municipal Board.

Strategic Plan County Council adopted the County of Oxford Strategic Plan (2015-2018) at its regular meeting of May 27, 2015. The initiatives contained in this report support the Values and Strategic Directions set out in the Strategic Plan as they pertain to the following:

Report No: CASPO 2015-159 COMMUNITY AND STRATEGIC PLANNING

Council Date: August 12, 2015

Page 2 of 2

3. ii. A County that Thinks Ahead and Wisely Shapes the Future – Implement development policies, land uses and community planning guidelines that:

- Strategically grow our economy and our community - Actively promote the responsible use of land and natural resources by focusing on higher

density options before considering settlement boundary expansions - Provides a policy framework which supports community sustainability, health and well-being - Supports healthy communities within the built environment - Supports and protects a vibrant and diversified agricultural industry

DISCUSSION

Background County Council held a public meeting pursuant to Section 51(20) of the Planning Act, R.S.O. 1990, as amended, on July 8, 2015 to consider an application for draft approval of a residential plan of subdivision. No concerns were raised at the public meeting.

Comments Township of East Zorra-Tavistock Council, at their regular meeting of June 17, 2015, passed a resolution recommending that draft plan approval be given by the County. County Council is now in a position to give draft plan approval to subdivision File No. SB 15-01-2.

Conclusions It is the opinion of the Community and Strategic Planning Office that draft approval of the residential plan of subdivision, SB 15-01-2, is appropriate from a planning perspective, subject to the draft plan conditions attached as Schedule “A”.

SIGNATURES original signed by Gordon K. Hough, MCIP, RPP Director

Approved for submission: original signed by Peter M. Crockett, P.Eng. Chief Administrative Officer

ATTACHMENTS Schedule “A” – Conditions of Draft Approval (SB 15-01-2: 1187688 Ontario Limited)

Schedule “A” To Report No. CASPO 2015-159

Page 1 of 5

CONDITIONS OF DRAFT APPROVAL – 1187688 ONTARIO LIMITED 1. This approval applies to the draft plan of subdivision submitted by 1187688 Ontario

Limited (File No. SB 15-01-2) and prepared by Ricor Engineering Limited, dated April 13, 2015, shown on Plate 3 of Report No. 2015-139 and comprising Part Lots 9 & 10, Concession 17 (East Zorra) in the Township of East Zorra-Tavistock, showing 92 lots for single detached dwellings, a 1.96 ha (4.84 ac) townhouse block, a 1.14 ha (2.82 ac) stormwater management block and 5 internal streets.

2. The owner agrees in writing to satisfy all requirements, financial and otherwise, of the Township of East Zorra-Tavistock regarding the construction of roads, installation of services, including the water, sewer and electrical distribution systems, sidewalks and drainage facilities, and other matters pertaining to the development of the subdivision, in accordance with the standards of the Township of East Zorra-Tavistock.

3. The subdivision agreement shall make provision for phasing of the subdivision, to the

satisfaction of the Township of East Zorra-Tavistock and that 0.3 m (1 ft) reserves shall be included at the road stubs corresponding to the phasing.

4. The subdivision agreement shall be registered by the Township of East Zorra-Tavistock against the land to which it applies at the developer’s expense.

5. The subdivision agreement shall contain a condition whereby the developer shall be responsible for the preparation of new assessment schedules for municipal drains affected by subdivision lands, to the satisfaction of the Township of East Zorra-Tavistock.

6. The subdivision agreement shall make provision for the dedication of 5% cash-in lieu of parkland to the Township of East Zorra-Tavistock in accordance with the relevant provisions of the Planning Act.

7. The subdivision agreement shall contain the following items specific to this development,

to the satisfaction of the Township of East Zorra-Tavistock:

i. that the noise provisions providing a maximum of 59 dBA for Outdoor Living Areas and all other noise provisions contained within the Noise and Vibration Feasibility Study that are in accordance with the Ministry of Environment guidelines, prepared by HGC Engineering, dated December 18, 2008, shall be incorporated into the agreement;

ii. that the acoustic barriers required by the Noise and Vibration Feasibility Study shall be

located and installed to satisfaction of the Township of East Zorra-Tavistock; iii. that once floor plan is available for Lot 71, a Professional Engineer qualified to perform

acoustical engineering services in the Province of Ontario should determine and/or refine the glazing construction to meet the minimum requirements specified in the Noise & Vibration Study;

iv. prior to the issuance of building permits, a Professional Engineer qualified to perform

acoustical engineer services in the Province of Ontario shall review the grading plans to certify that the noise control measures as recommended in the Noise & Vibration Study have been incorporated;

Schedule “A” To Report No. CASPO 2015-159

Page 2 of 5

v. prior to the issuance of occupancy permits, a Professional Engineer qualified to perform acoustical engineer services in the Province of Ontario should certify that the noise control measures have been properly installed and constructed.

8. The subdivision agreement shall contain a provision for the fencing of the rear lot lines of

Lots 1 – 10 inclusive and the northerly interior side yard of Lot 10 at the developer’s expense, to the satisfaction of the Township of East Zorra-Tavistock.

9. The subdivision agreement shall contain a cost sharing agreement between the developer

and the Township of East Zorra-Tavistock for the reconstruction of Main Street and George Street to an urban cross-section as per the Township of East Zorra-Tavistock’s design standards, as follows:

i. Main Street: from Queen Street to existing intersection with George Street to the east; ii. George Street: from the proposed Queen Street extension to future Jonker Street to

the satisfaction of the Township of East Zorra-Tavistock. 10. The subdivision agreement shall contain provisions for landscaping the street-fronting side

of the acoustic barrier located on Lot 71 to the satisfaction of the Township of East Zorra-Tavistock.

11. The subdivision agreement shall contain a provision directing the owner and all future

owners of properties within the draft plan to include the following warning in all offers to purchase, agreements of purchase and sale or lease and in the title deed or lease of each dwelling within 300 m (984 ft) of the railway right-of-way:

“Purchasers are advised of the existence of a Railway right-of-way within 300 m (984 ft) and there is a possibility of alterations including that the Railway may expand its operations, which may affect the living environment of the residents notwithstanding the inclusion of noise and vibration attenuating measures in the design of the subdivision and individual units, and that the Railway will not be responsible for complaints or claims arising from the use of its facilities or operations.”

12. The subdivision agreement shall contain a provision directing the owner and all future owners of properties within the draft plan to include the following warning in all offers to purchase and sale or lease, and be registered on title, or included in the lease for each dwelling affected by any noise and vibration attenuation measures:

“Any berm, fencing or vibration isolation features implemented are not to be tampered with, or altered, and further that the owner shall have the sole responsibility for and shall maintain these features.”

13. The subdivision agreement shall contain a provision directing the owner and all future owners of properties within the draft plan to include the following warning clauses in all purchase and sale agreements and be registered on title:

“Purchasers are advised that dust, odour and other emissions from agricultural activities conducted in the periphery of the Township of East Zorra-Tavistock may be of concern and may interfere with residential activities.” “Purchasers are advised that the municipal water system is not designed or capable of providing fire flow service.”

Schedule “A” To Report No. CASPO 2015-159

Page 3 of 5

14. The subdivision agreement shall contain a provision directing the owner and all future owners of Lot 10 within the draft plan to include the following warning clause in all purchase and sale agreements and be registered on title:

“Purchasers are advised that dust, noise, odour and other emissions from industrial activities conducted in the immediate vicinity may be of concern and may interfere with residential activities.”

15. The subdivision agreement shall contain a provision directing the owner and all future owners of Lots 1-10 inclusive within the draft plan to include the following warning clause in all purchase and sale agreements and be registered on title:

“Purchasers are advised that noise, odour and other emissions from commercial activities conducted in the immediate vicinity may be of concern and may interfere with residential activities.”

16. The subdivision agreement shall contain a provision directing the owner and all future owners of Lots 1, 2, 72 – 82 inclusive and 91 and 92 inclusive within the draft plan to include the following warning clause in all purchase and sale agreements and be registered on title:

“This dwelling unit has been fitted with a forced air heating system and the ducting was sized to accommodate central air conditioning. Installation of central air conditioning will allow windows and exterior doors to remain closed, thereby ensuring that the indoor sound levels are within the criteria of the Municipality and the Ministry of the Environment.”

17. The subdivision agreement shall contain a provision directing the owner and all future owners of Lot 71 within the draft plan to include the following warning clause in all purchase and sale agreements and be registered on title:

“This dwelling has been supplied with a central air conditioning system which allows windows and exterior doors to remain closed, thereby ensuring that the indoor sound levels are within the noise criteria of the Municipality and Ministry of the Environment.”

18. Prior to final approval of the plan, the subdivision agreement shall contain provisions indicating that prior to grading and issuance of building permits, that a storm water management report, grading plan and an erosion and siltation control plan be reviewed and approved by the Township of East Zorra-Tavistock, the Upper Thames River Conservation Authority and the Canadian Pacific Railway, and further, the subdivision agreement shall include provisions for the implementation, monitoring and maintenance of stormwater management works in accordance with the approved plans and reports.

19. The road allowances included in the draft plan of subdivision shall be dedicated as public

highways. 20. The streets included in the draft plan of subdivision shall be named to the satisfaction of

the Township of East Zorra-Tavistock. 21. All 0.3 m (1 ft) reserves as indicated on the revised draft plan of subdivision shall be

conveyed to the Township of East Zorra-Tavistock free of all costs and encumbrances.

Schedule “A” To Report No. CASPO 2015-159

Page 4 of 5

22. Prior to the final approval of the plan, the owner shall submit to the Township of East Zorra-Tavistock detailed road alignment design for the following street alignments:

i. Existing Queen Street with the proposed Queen Street extension; ii. Proposed Queen Street extension with existing Thompson Place; iii. Existing James Street with the recent James Street extension to the satisfaction of the

Township of East Zorra-Tavistock. 23. Prior to the final approval of the plan, the owner shall provide to the Township of East

Zorra-Tavistock road widenings along Main Street and George Street where they abut the subdivision, to bring the road allowance to the standard 20 m (66 ft) road width, which are to be conveyed to the Township of East Zorra-Tavistock.

24. Prior to the final approval of the plan, all lots and blocks shall conform to the zoning

requirements of the Township of East Zorra-Tavistock Zoning By-Law. Certification of lot areas, lot frontages and lot depths shall be obtained from an Ontario Land Surveyor retained by the developer.

25. Prior to final approval of the plan, all existing buildings and structures on the lands, except

for the dwelling located in Block 93, shall be removed prior to the registration of the first phase of the subdivision, to the satisfaction of the Township of East Zorra-Tavistock. The existing dwelling located in Block 93 shall be removed prior to the registration of the phase which includes Block 93, to the satisfaction of the Township of East Zorra-Tavistock.

26. Prior to final approval of the plan, the owner shall obtain permission from the Township of

East Zorra-Tavistock to maintain one existing access to the existing dwelling located on Block 93 until such time that the dwelling is removed.

27. The owner agrees in writing that, prior to final registration of the plan, Block 94 shall be

conveyed to the Township of East Zorra-Tavistock for storm water management purposes free of all encumbrances, financial or otherwise, and this block shall be landscaped, graded, seeded with grass and fenced to the satisfaction of the Township of East Zorra-Tavistock.

28. The owner agrees in writing to satisfy all the requirements, financial and otherwise,

including payment of applicable development charges, of the County of Oxford Department of Public Works regarding the installation of the water distribution system, the installation of the sanitary sewer system, and other matters pertaining to the development of the subdivision.

29. The subdivision agreement shall make provision for the assumption by the County of

Oxford of the water system and sewage system within the draft plan subject to the approval of the County of Oxford Public Works Department.

30. Prior to final approval of the plan, the owner shall receive confirmation from the County of

Oxford Public Works that there is sufficient capacity in the sanitary and water services to service the plan of subdivision.

31. Prior to final approval of the plan, such easements as may be required for utility or

drainage purposes shall be granted to the appropriate authority.

Schedule “A” To Report No. CASPO 2015-159

Page 5 of 5

32. Prior to final approval of the plan, any proposed utilities under or over railway property to serve the development must be approved prior to their installation and be covered by the Canadian Pacific Railway’s standard agreement.

33. Prior to final approval of the plan, detailed stormwater management design plans as well

as grading and sediment and erosion plans be submitted to the satisfaction of the Upper Thames River Conservation Authority.

34. Prior to the signing of the final plan, the County of Oxford shall be advised by the County

of Oxford Department of Public Works that Conditions 28 – 31 inclusive have been met to the satisfaction of the Public Works Department. The clearance letter shall include a brief statement for each condition detailing how each has been satisfied.

35. Prior to the signing of the final plan, the County of Oxford shall be advised by the Upper

Thames River Conservation Authority that Conditions 18 and 34 have been met to the satisfaction of the Conservation Authority. The clearance letter shall include a brief statement for this condition detailing how it has been satisfied.

36. Prior to the signing of the final plan, the County of Oxford shall be advised by the

Canadian Pacific Railway that Conditions 18 and 32 have been met to the satisfaction of the Railway. The clearance letter shall include a brief statement for each condition detailing how each has been satisfied.

37. Prior to the signing of the final plan, the County of Oxford shall be advised by the

Township of East Zorra-Tavistock that Conditions 1 - 27 inclusive, 29 and 31 have been met to the satisfaction of the Township of East Zorra-Tavistock. The clearance letter shall include a brief statement for each condition detailing how each has been satisfied.

38. This plan of subdivision shall be registered by August 12, 2018, after which time this draft

plan approval shall lapse unless an extension is authorized by the County of Oxford.

Plate 3: Proposed Draft Plan of SubdivisionSB 15-01-2 - 1187688 Ontario Inc. - 77 Main Street, Innerkip

Page 1 of 5

Report No: CASPO 2015-160 COMMUNITY AND STRATEGIC PLANNING

Council Date: August 12, 2015

To: Warden and Members of County Council From: Director, Community and Strategic Planning

Application for Draft Plan of Condominium and Exemption from Draft Plan Approval CD 15-02-3: 487223 Ontario Limited (Gabriel Kirchberger)

RECOMMENDATIONS 1. That Oxford County Council grant draft plan approval of a proposed plan of

condominium submitted by 487223 Ontario Limited (Gabriel Kirchberger), (File No. CD 15-02-3); prepared by J.H. Cohoon Engineering Ltd. and dated June 3, 2015, for lands described as Part Lot 677, Plan 955, in the Village of Norwich.

2. And further, that Oxford County Council approve the application for exemption from the draft plan of condominium approval process submitted by 487223 Ontario Limited (Gabriel Kirchberger), (File No. CD 15-02-3) for lands described as Part Lot 677, Plan 955, in the Village of Norwich, as all matters relating to the development have been addressed through the Site Plan Approval process and a registered site plan agreement.

REPORT HIGHLIGHTS The purpose of this report is to consider the approval of a draft plan of condominium and

exemption from the draft approval process to facilitate the development of a 20-unit condominium on the subject property.

The proposal is consistent with the relevant policies of the 2014 Provincial Policy Statement, the County’s Official Plan and the provisions of the Township of Norwich Zoning By-law.

The Council of the Township of Norwich supported the request for approval of the draft plan

of condominium and the exemption from the draft approval process at its regular meeting on July 14, 2015.

Implementation Points This application will be implemented in accordance with the relevant policies contained in the Official Plan.

Report No: CASPO 2015-160 COMMUNITY AND STRATEGIC PLANNING

Council Date: August 12, 2015

Page 2 of 5

Financial Impact The approval of this application will have no financial impact beyond what has been approved in the current year’s budget. The Treasurer agrees with this financial impact statement.

Risks/Implications There are no risks or other implications anticipated as a result of this application beyond those that can reasonably be expected for any such proposal.

Strategic Plan County Council adopted the County of Oxford Strategic Plan (2015-2018) at its regular meeting held May 27, 2015. The initiative contained within this report supports the Values and Strategic Directions as set out in the Strategic Plan as it pertains to the following:

3. ii. A County that Thinks Ahead and Wisely Shapes the Future – Implement development policies, land uses and community planning guidelines that:

- Strategically grow our economy and our community - Actively promote the responsible use of land and natural resources by focusing on higher

density options before considering settlement boundary expansions - Provides a policy framework which supports community sustainability, health and well-

being - Supports healthy communities within the built environment - Supports and protects a vibrant and diversified agricultural industry

DISCUSSION

Background Owner: Gabriel Kirchberger 487223 Ontario Limited P.O. Box 4647 Brantford, ON N3T 6J7 Applicant: Bob Phillips J.H. Cohoon Engineering Ltd. 440 Hardy Road, Unit 1 Brantford, ON N3T 5L8 Location: The subject lands are described as Part Lot 677, Plan 955, West Side of Dufferin Street, Village of Norwich. The lands are located on west side of Dufferin Street, south of Carman Street, and are municipally known as 10 Dufferin Street in Norwich.

Report No: CASPO 2015-160 COMMUNITY AND STRATEGIC PLANNING

Council Date: August 12, 2015

Page 3 of 5

County of Oxford Official Plan:

Schedule “C-3” County of Oxford Settlement Strategy Plan Serviced Village Schedule “N-2” Village of Norwich Land Use Plan Medium Density Residential Township of Norwich Zoning By-law No. 07-2003-Z:

Existing Zoning: Special Residential Type 3 Zone (R3-1) Application Review (a) Proposal and Background An application has been received for approval of a plan of condominium and exemption from the draft approval process to facilitate the development of 16 townhouse dwelling units, and 4 street fronting townhouse dwelling units.

A condominium development differs from a plan of subdivision in that the roads and other ‘common’ features within the plan are typically owned privately by the condominium corporation. Further, services such as water and sanitary sewers are often held in private ownership by the corporation. The consideration of these matters, along with others (including, but not limited to parking design, site grading and drainage, building layout and landscaping) were considered through the Site Plan Approval process, which was undertaken by the Township in May of 2014, and a final Site Plan agreement was established in August of 2014 between the Township and the property owner.

Comments (a) 2014 Provincial Policy Statement

The 2014 Provincial Policy Statement (PPS) provides policy direction on matters of provincial interest related to land use planning and development. Under Section 3 of the Planning Act, where a municipality is exercising its authority affecting a planning matter, such decisions “shall be consistent with” all policy statements issued under the Act. Policies within the PPS direct municipalities to provide for a range of housing types and densities to meet the needs of current and future residents as well as promoting compact built forms of development. The policies also advise municipalities to permit and facilitate all forms of housing to meet the social, health and wellbeing of current and future residents and to promote residential intensification where it can be accommodated taking into account existing building stock, efficient use of infrastructure and public service facilities, providing there are no negative impacts on natural environmental features. (b) Official Plan The subject property is located within the Medium Density Residential designation, according to the Village of Norwich Land Use Plan, as contained in the County Official Plan. Medium Density Residential areas are those lands within the Serviced Village designation that are primarily