agent-based models: understanding the economy from the ... · topical articles agent-based models:...

TRANSCRIPT

Topical articles Agent-based models: understanding the economy 173

Agent-based models: understanding the economy from the bottom upBy Arthur Turrell of the Bank’s Advanced Analytics Division.(1)

• Agent-basedmodellinghaslongenjoyedsuccessinthenaturalsciences,providinginsightsintoeverythingfromcancertotheeventualfateoftheUniverse.

• Itissuitedtomodellingcomplexsystemssuchastheeconomy,particularlythoseinwhichdifferentagents’interactionscombinetoproduceunexpectedoutcomes.

• Ineconomics,agent-basedmodelshaveshownhowbusinesscyclesoccur,howthestatisticsobservedinfinancialmarkets(suchas‘fattails’)arise,andhowtheycanbeausefultoolinformulatingpolicy.

Overview

Agent-basedmodelsexplainthebehaviourofasystembysimulatingthebehaviourofeachindividual‘agent’withinit.Theseagentsandthesystemstheyinhabitcouldbetheconsumersinaneconomy,fishwithinashoal,particlesinagas,orevengalaxiesintheUniverse.

Thestrengthofthesemodelsisthattheyshowhowevenverysimplebehaviourscancombinefromthe‘bottomup’torecreatethemorecomplexbehavioursobservedintherealworld.Anexamplewouldbehowthedecisionsofeachindividualfishcreatetheseeminglyorganisedandunpredictablemovementsoftheshoal.

This‘bottom-up’approachisincontrasttomodelswhichare‘topdown’,andwhichpresumehowagents’behaviourswillcombinetogether,sometimesbyassumingthatallagentsareidentical.Thedifferentapproacheshavedifferentstrengths.

Theagent-basedapproachtoproblem-solvingbeganinthephysicalsciencesbuthasnowspreadtomanyotherdisciplinesincludingbiology,ecology,computerscienceandepidemiology.Inrecentyears,agent-basedmodelshavebecomemorecommonineconomics,includingattheBankofEngland.

Therearechallengestotheiruse,includingtheneedforadvancedprogrammingskills,theneedtocarefullyinterprettheirresults,andhowtobestselecttheappropriatebehavioursfortheagents.Inparticular,therearenotalwaysobviouscriteriaforchoosingwhichbehavioursarethemost

realistic.Theseissueshavebeenabarriertotheirmorewidespreadadoptionineconomics.

Despitebeinglesswidelyused,agent-basedmodelshaveproducedmanyimportantinsightsineconomics,includinghowthestatisticsobservedinfinancialmarketsarise,andhowbusinesscyclesoccur.

Recently,theBankofEnglandhasdevelopedagent-basedmodelsoftwomarkets:corporatebondsandhousing.Theincreasedavailabilityofdataandcomputationalpowermeanthatagent-basedmodellinglookssettogainimportanceasatoolforbothunderstandingtheeconomy,andforexploringtheconsequencesofpolicyactions.

(1) TheauthorwouldliketothankDavidBholatandChrisCaifortheirhelpinproducingthisarticle.

ENVIRONMENT

Agents Agent-agent interactions Agent-environment interactions

Summary figure Schematic of the typical elements of an agent-based model

174 Quarterly Bulletin 2016 Q4

Introduction

Thisarticleconsidersthestrengthsofagent-basedmodellingandthewaysthatitcanbeusedtohelpcentralbanksunderstandtheeconomy.ThesemodelsprovideacomplementtomoretraditionaleconomicmodellingwhichwascriticisedfollowingtheGreatRecession.(1)

Agent-basedmodelshavedifferentstrengthsandweaknessestootherapproachesineconomics.Theyhaveadvantagesindescribinghowthedifferentactionsandpropertiesofindividualagentscombinetodrivetheoverallbehaviourofsystems.

Thisarticleexplainsthemotivationbehinddevelopingmodelsandhowtheycanbeusedtobetterunderstandtheworld,beforediscussingmoredetailsofwhatmakesagent-basedmodelsdifferent.Itthendescribeshowthesemodelswerefirstdevelopedandusedindisciplinesoutsideofeconomics.

Thegeneralstrengthsandweaknessesofagent-basedmodelsarediscussed,withexamplesofhowtheiradvantageshavebeenusedtoimprovetheunderstandingofcertainmarkets.

Thepenultimatesectionisanoverviewofhowagent-basedmodelsarebeingappliedineconomicsingeneralandattheBankofEnglandspecifically.Finally,somethoughtisgiventohowthislineofmodellingmightbeusedinthefuture.

Agent-basedmodelsarecalledbydifferentnamesindifferentdisciplines,includingMonteCarlosimulations(inthephysicalsciences),individual-basedmodels(inbiologyandecology),agent-basedcomputationaleconomicsmodels(ineconomics)andmulti-agentsystems(incomputerscienceandlogistics).Thisarticleuses‘agent-basedmodel’torefertoanymodelinwhichtheinteractionsandbehavioursofalargenumberofheterogeneousagentsaresimulated,manuallyorbyacomputer.

ModellingModellingisubiquitousacrossacademicdisciplines,governmentsandtheprivatesector.Mostmodelsattempttoisolatetheunderlyingcausesofthebehaviourofsystems,removingextraneousdetailandfocusingonwhatmatterstothehypothesis,questionorpolicyunderconsideration.Modelsmaybeassimpleasthoughtexperimentsbut,inquantitativesubjects,ofteninvolvemathematicsandsimulation.

Usinganartificialandsimplifiedversionoftheworldallowsresearchersandpolicymakerstoexplorewhatmighthappenincertainscenarios.Inmacroeconomics,datamaybescarceandexperimentscanrarely,ifever,beperformedintherealworld,andthismakesmodelsespeciallyuseful.Differentmodelsare

goodforansweringdifferentquestionsandsoawiderangeofthemarerequired.

Allmodelsshouldbeabletoreproduce,asmuchaspossible,therealworldobservablestheyseektoexplain.Italsohelpsiftheyareeasytouseandinterpret,andiftheycanexplainthephenomenaassimplyaspossible.Overtime,modelswhichexplainrealitymoreadequatelyandmoreconciselyarefavoured,replacingthosewhichexplainitlesswell.

Agent-basedmodelsaresuitedtostudyingproblemsinwhichthecombinationoftheinteractionsofmanyagentsdrivestheoverallbehaviourofthesystem.Theysolveproblemsfromthe‘bottomup’ratherthanthroughrulesimposedfromthe‘topdown’.Typically,creatinganagent-basedmodelrequiresknowledgeofmathematics,statistics,andcomputerscience,aswellasthedisciplineinwhichitisbeingapplied.

Thesemodelsgettheirnamebecausetheyinvolvesimulatingalargenumberof‘agents’.Eachagentisaself-containedunitwhichfollowsitsownbehaviouralrules.Mostoften,thisisachievedwithinacomputersimulationbutitneednotbe.

Agentscouldrepresenttheconsumersinaneconomy,fishwithinashoal,particlesinagas,orevengalaxiesintheUniverse.Thebehavioursorrulesthatagentsfollowdependonthequestionofinterest.Somemodelshavemanydifferenttypesofagent,forinstancefirms,workersandgovernments.Thesemaythemselvesdiffer;forinstance,eachworkermighthaveadifferentproductivity,eachfirmadifferentsize.Agent-basedmodelshaveilluminatedasurprisinglywiderangeofsubjectsincludingmilitaryplanningandbattlefieldanalysis,operationalresearch,computerscience,biology,ecology,epidemiology,economics,socialsciencesandthephysicalsciences.

Withthem,suchvariedproblemsastheseparationofBrazilnutsfromothermixednuts,thebehaviouroftradersinthestockmarket,theflockingofbirds,thefallofancientcivilisations,thespreadofdisease,andtheeventualfateoftheUniversehavebeenexamined.

Inafewcases,resultswhichcouldonlyhavebeenobtainedthroughagent-basedmodellinghavesignificantlychangedthecourseofhistory:calculationsofthewaythatparticlesaretransportedthroughapileoffissilematerialinanuclearreactororweaponwouldbeprohibitivelydifficulttodoinanyotherway.

Theiruseineconomicscomeswithsomeparticularnuanceswhichareexploredinthisarticle.Inthenaturalsciences,agentbehavioursaretypicallymuchmoreconstrainedthanin

(1) SeeHaldane(2016).

Topical articles Agent-based models: understanding the economy 175

economics.Becauseofthis,agent-basedmodelsineconomicstypicallyproduceinsightsratherthanquantitativeforecasts.Theyaretypicallyqualitativeratherthanquantitative,andtheyaregoodfordeterminingwhatscenariosmightoccurratherthanexactlywhatwilloccur.

Anagent-basedmodelineconomicswouldnotnormallybeappropriateforforecastingthepriceofaparticularasset,forexample.Butitcangiveanideaofwhatactionsbytradersmightmovethepricesofassets,orwhythesupplyofanassetismuchmorevolatilethanthedemandforit.Otherphenomenawhichtheyhaveexplainedindifferentcontextsincludecycles,bubbles,clusteredvolatility,firesalesofassets,andtheonsetof‘bear’and‘bull’markets.(1)Despitebeingmoresuitedtoinsightsthanquantitativeprediction,therehavebeensomesuccessfulexamplesofforecastingwithagent-basedmodelsineconomics;forexample,forthedemandforelectricityortherepaymentrateofmortgages.(2)

TheGreatRecessionprofoundlychallengedtheeconomicsprofession,particularlyeconomicmodelling.Itdemonstratedthattheeconomyiscomplex,andnotalwaysatastableequilibrium.Theafter-effectsofthecrisisarestillbeingfelt.Establishedtools,suchas‘dynamicstochasticgeneralequilibrium’models(3)havebeencriticised(4)fornothavingenoughtosayaboutthedynamicsofcrises.Agent-basedmodelsareoneresponsetothechallengeandthisarticleexplorestheirpotentialinaidingourunderstandingoftheeconomy.

Theremainderofthissectionillustrateshowthesemodelshavedevelopedandwhatusestheyhavepreviouslybeenputto.Then,thearticleturnstoaspecificexampleofagent-basedmodellingineconomicswhichdemonstratessomeoftheirgeneralfeatures.

Theoriginsofagent-basedmodellingTheinitialspurfordevelopingagent-basedmodelscameinthe1930swhenphysicistEnricoFermiwastryingtosolveproblemsinvolvingthetransportofneutrons,asub-atomicparticle,throughmatter.Neutrontransportwasdifficulttomodelaseachstepinaneutron’sjourneyisprobabilistic:thereisachancetheparticlewilldirectlyinteractwith,scatteroff,orpass-byotherparticles.Previousmethodshadtriedtocapturetheaggregatebehaviourofalltheneutronsatonce,buttheimmensenumberofdifferentpossibilitiesforneutronpathsthroughmattermadetheproblemverychallenging.

Fermidevelopedanewmethodtosolvetheseproblemsinwhichhetreatedtheneutronsindividually,usingamechanicaladdingmachinetoperformthecomputationsforeachindividualneutroninturn.Thetechniqueinvolvedgeneratingrandomnumbersandcomparingthemtotheprobabilitiesderivedfromtheory.Iftheprobabilityofaneutroncollidingwere0.8,andhegeneratedarandomnumbersmallerthan0.8,

healloweda‘simulated’neutrontocollide.Similartechniqueswereusedtofindtheoutgoingdirectionoftheneutronafterthecollision.Bydoingthisrepeatedly,andforalargenumberofsimulatedneutrons,Fermicouldbuildupapictureoftherealwaythatneutronswouldpassthroughmatter.Fermitookgreatdelightinastonishinghiscolleagueswiththeaccuracyofhispredictionswithout,initially,revealinghistrickoftreatingtheneutronslikeagents.(5)

Theagent-basedtechniquesFermiandcolleaguesdevelopedwentontoplayanimportantroleinthedevelopmentofnuclearweaponsandnuclearpower.AtaroundthesametimethatFermiwasdevelopinghistechnique,thefirstelectroniccomputerswerebecomingavailableattheworld’sleadingscientificinstitutions.Computingpowerremainskeytoagent-basedmodellingtoday,withsomeoftheworld’ssupercomputersbeingharnessedforevermoredetailedsimulations.(6)

By1947scientistshaddevelopedanameforthistechniquewhichreflecteditsprobabilisticnature:theMonteCarlomethod.ThestorygoesthatthenamewasinspiredbyStanislawUlam’suncle,whowouldoftenasktoborrowmoneybysayinghe‘justhadtogotoMonteCarlo’.In1949,MetropolisandUlampublishedapapertogetherentitledThe Monte Carlo Method(7)whichexplainedthemanyusesofthenewtechniqueofusingrandomnumberstotackleproblems.Notallofthesewereagent-basedmodelsbutallreliedonusingartificiallygeneratedrandomnumberstosolveproblems.ThismoregeneralMonteCarlotechniquehasbeenappliedverywidely,forinstancetocalculatingsolutionstoequationswithmanyparameters,tothemanagementofriskandcatastrophes,andtoinvestmentsinfinance.

ThemoregeneralMonteCarlomethodhasthestrengththatitcanveryefficientlyexplorealargenumberofpossibilities.Forinstance,theusualwayforFermi’sneutronproblemtohavebeentreatedwouldhavebeentocreateagridofeverysinglepossibilityandthenfillinwhathappensforeachofthem.Thismeansthatevenimplausiblyunlikelyscenariosarecomputed.MonteCarloinsteadfocusesonthemostlikelyoutcomes.Thispropertycanmakethedifferencetowhetheraparticularproblemissolvableornot.TheMonteCarlomethodcanalsodealwithdistributions,forinstanceacrossincome,whicharenotdescribedbyanormaldistribution.(8)

(1) SeeZeeman(1974).(2) SeeGeanakoploset al(2012).(3) Aclassofmodelsinwhichmarketsareassumedtosimultaneouslyclear;see

Burgesset al(2013).(4) SeeMankiw(2006);Haldane(2016);Ascari,FagioloandRoventini(2015).(5) SeeMetropolis(1987).(6) LawrenceLivermoreNationalLaboratory(2013),‘Recordsimulationsconductedon

LawrenceLivermoresupercomputer’,availableathttps://www.llnl.gov/news/record-simulations-conducted-lawrence-livermore-supercomputer.

(7) SeeMetropolisandUlam(1949).(8)Normaldistributionsarewhatphysicalproperties,suchasheight,tendtofollowand

theyhaveawell-knownmathematicaldescription.TheyarealsoknownasGaussiandistributionsor‘bell-curves’.Manypropertiessuchaswealth,income,orfirmsizedonotfollowanormaldistribution.

176 Quarterly Bulletin 2016 Q4

Thesearestrengthswhichagent-basedmodelsinheritfromthemoregeneraltechnique.However,thisarticlefocusessolelyonMonteCarlosimulation,alsoknownasagent-basedmodelling.Thisseekstodescribeasystemofinteractingagentsandtheevolutionofthatsystem,ratherthancalculatethesolutiontoasingleequation.Inthisarticle,MonteCarlosimulationandagent-basedmodellingareusedsynonymously.

Agent-basedmodellinghasbeenusedacrossawiderangeofdisciplines,asdiscussedintheboxonpage177.Beforeembarkingonthestrengthsandweaknessesofagent-basedmodels,asimpleexampleispresentedwhichillustratessomeoftheirgeneralfeatures.ThisexampleisanearlyandinfluentialmodelbyeconomicsNobelMemorialprizelaureateThomasSchelling.

An early agent-based model in economicsInthelate1960sandearly70s,ThomasSchelling(1)developedamodelthatseekstounderstandtheeffectsofagents’preferencesaboutwheretheylive.ThedescriptionbelowdoesnotexactlyfollowSchelling’soriginalexample,butretainsitsmostsalientfeatures.

ImaginetherearetwospeciesnamedEconsandHumanswhoco-exist.Econsarealwaysrational.Humansareemotionalandsometimesmakemistakes.AlthoughEconsandHumanspeacefullyco-existandliveinthesamecity,theyeachhaveaslightpreferenceforlivingclosertothesamespecies.

Thispropensitytowanttobenearothersoftheirtypecanbecharacterisedbyanumberf,whichcanbethoughtofastheirstrengthofpreference.Itrepresentsthefractionofneighboursthattheyideallywishtobeofthesamespecies,withanfof1meaningthattheywillonlybehappyifalloftheirneighboursareofthesamespecies.

Ifagentsofeithertypeareunhappy,theycanchoosetomovehouseand,atrandom,aregivenanewproperty.Overtime,moreandmoreagentswillbehappywithwheretheyliveandstopmoving.Usingsimulations,Figure 1showsaninitialneighbourhoodofHumansandEconswhichismixed.

WhathappensiftheHumansandEconsarenowallowedtomovearounduntilalmostallofthemare‘happy’accordingtothevalueoff?Figure 2showsoneexamplesimulationwithf=25%;theagentsremaingenerallyinter-mixed.WhatissurprisingishowquicklythemixofHumansandEconsbecomessegregatedasfincreases.Figure 3showsanexampleofafinaldistributionwithf=26%.

Theagentsarenowclearlysegregated,eventhoughthechangeintheirpreferenceswasverysmallfromFigure 2.Thisisanexampleofa‘tippingpoint’,alsoknowninthephysicalsciencesasa‘phasetransition’.Itisasudden,emergentchangeintheoverallsystem.Tippingpointslikethiscanoccur

insystemswhicharecoupledtogetherbytheiragents;here,asmallchangeinfcanmeanthatalmosteveryonehastomoveinordertosatisfytheirnewpreferences.Asaresult,theneighbourhoodcanlookverydifferentafterthechangeinf.

Humans Econs

Figure 1 The initial distribution of Humans and Econs

Humans Econs

Figure 2 The final distribution of Humans and Econs with f=25%

Humans Econs

Figure 3 The final distribution of Humans and Econs with f=26%

(1) SeeSchelling(1969,1971);foranexampleseewww.jeromecukier.net/projects/models/segregate.html.

Topical articles Agent-based models: understanding the economy 177

Agent-based modelling across disciplines

Agent-basedmodellingsoonbecameaverypopulartechniqueinthephysicalsciences;(1)anearlypaperhasreceivedover30,000citationsbyotherresearchers.(2)Deepinsightshaveemerged,forinstancethatthestructureoftheUniversemaybeflatratherthancurved,(3)meaningthattheUniverseisunlikelytoendina‘BigCrunch’withallmatterconcentratedatasinglepointinspace.

Therangeofapplicationsinthephysicalsciencestodayisbroadindeedandincludesplasmaphysics,(4)particle-basedcancertherapies,materialsscience,crystallisation,magnetismandnuclearfusion.(5)Oneunexpectedapplication,publishedwiththetitleWhy the Brazil Nuts Are on Top,(6)simulatedhowmixednutssegregateovertimeinabag,researchwhichhashadimportantimplicationsforindustriesdealingwithparticulatemattersuchaspharmaceuticalsandmanufacturing.

Computersciencehasalsoseenheavyuseofthetechnique.ThepolymathJohnvonNeumannisbestknownineconomicsforhisworkongametheorybuthewasalsoaformidablecomputerscientist.Ina1948lecturehedescribeshisideafor‘cellularautomata’.Theseareartificialmodelsof‘cells’,whichlooklikefilledsquaresonaboard(similartotheSchellingmodeldiscussedinthisarticle).(7)VonNeumannfoundthat,contrarytointuition,verysimplerulesforthecellagentsgaverisetopuzzlinglycomplexbehaviourwhichlookslife-like.Thisisaso-calledemergentbehaviourbecauseitisalmostimpossibletopredictbasedontheruleswhichtheindividualagentsfollow.

Themilitarywereearlyadoptersofagent-basedmodelling.Wargameshadbeenplayedwithboardanddiceformanyyears,buttherewasaswitchtocomputationalagentsinthe1960s.Aswellasbeingusedtounderstandthedynamicsofpastbattles,suchashowoptimalthesearchingoperationsoftheBritishArmywereindetectingGermanU-boatsintheBayofBiscay,(8)theyaretodayusedbytheworld’slargestarmiestoformulatemilitarystrategy.Inrecenttimes,theautomatedbehaviourofagentsinwarmodelshasspilledoverintorealitywiththedevelopmentofautonomousweaponsandvehicles.

Thistrendisalsoreflectedincivilapplicationsofautonomousrobots.Mostrecently,therehasbeenmuchworkonmultipleautonomousroboticssystemsinwhichtheagentsarerobotsthatneedtodecidehowtomoveaboutintherealworld,forinstanceindriverlesscars.Itisextremelyusefultobeablemodelthebehaviourofautonomousrobotsbeforetryingthemoutinthefield.Forsometasks,centralisedcontrolofallrobotsisnotfeasiblesodesigningindividualbehaviourswhichproducetheoveralldesiredoutcomeisimportant.

Biologistsandecologistbegansimulatingthebehaviouroforganismswithinanenvironmentusingagent-basedmodelsinthe1980s.Thesemodelswereextendedtoincludemorecomplexphenomena,suchasagent-environmentinteractions.Anexampleistheresearchonmarineorganismswhichincludesbehaviourssuchasswimming,feeding,beingpreyedupon,andorganisms’interactionswithoceancurrents.Oneofthemanyapplicationsofthissortofmodelcouldbeexamininghoworganismsfairwithhigheroceantemperatures,orhigherconcentrationsofCO2.

(9)

Successesofthesemodelsincludepredictingthespawninglocationsoffish,explaininghowthetroutinLakeMichigan,USA,becamecontaminated,anddescribinghowsociallylearnedbehavioursleadtodistinctculturalgroupsamongmammals.Inthesecasestheadvantageofanagent-basedmodelwastobeabletoincludemanydifferentagentsandagentbehavioursinasinglemodelwhichcouldberunmillionsoftimestodeterminethemostprobableoutcomes.

Recentapplicationshavefocusedonconservationandmigration,includingthemanagementofforests,thetimingofanimalmigrations,andthepopulationpressuresonendangeredspecies.Forinstance,onemodelisoftheendangeredtigerpopulationinNepal;itusestheobservedbehaviourofindividualtigerstoexplorefutureconservationscenarios.(10)

Animportanthealth-relatedapplicationofagent-basedmodelsisinepidemiology—thestudyofthespreadofdiseases.Agoodunderstandingofthecomplexdynamicsofepidemicscouldsavemillionsoflives.Agent-basedmodelshaveallowedcountry-specificinformationsuchasgeographicaldata,commutingpatterns,agedistributionsandothercensusinformationtobetakenintoaccount.(11)

Inbiology,agent-basedmodelsarenowbeingusedtosimulateentireanimalcells,cancers,bacteriaandeventheeffectsofnewdrugsonpatients.Otherapplicationsincludeairtrafficcontrol(inwhichagentsrepresentaircraftandco-ordinatetominimisefueluse),transportationsystems(matchingagentstodestinations),crowdcontrolinemergencysituations,shoppingpatterns,predictinglandusepatterns(12)andnon-playeragentsincomputergames.

(1) SeeHaldane(2016)formore.(2) SeeMetropoliset al(1953).(3) SeeDaviset al (1985).(4) SeeTurrell,SherlockandRose(2015).(5) SeeTurrell(2013).(6) SeeRosatoet al(1987).(7) SeevonNeumann(1951);anexamplemaybefoundat

www.jeromecukier.net/projects/models/ca.html.(8) SeeCarl(2015);ChampagneandHill(2009).(9) SeeWerneret al(2001).(10)SeeCarteret al(2015).(11) SeeDegliAttiet al (2008).(12)SeeHeppenstallet al(2011).

178 Quarterly Bulletin 2016 Q4

Figure 4showswhatcanhappenwhenallagentshaveverystrongpreferences.

Schelling’smodelisverysimplebutitshowshowevenmildchangesinpreferencescanleadtosignificantchangesatthemacro-level.

Figure 5 showsthatstrikinglysimilarpatternsmaybeseenintheUSCensusdataforChicago.However,therearemanydifferencesbetweenthesimplemodelpresentedandtherealworld;preferencesmaynotbesymmetricacrossgroupsasisassumedinthebasicSchellingmodel,therearemanypracticalbarrierstomoving(suchasbudgetconstraints)andwhatwaslabelledas‘preference’islikelytobemuchricherinreality,reflectingthecomplicatedsocio-economichistoricalrelationshipsbetweengroups.

What is agent-based modelling good (and bad) for?

Theprevioussectiongaveaspecificexampleofthekindsofinsightswhichcomeoutofagent-basedmodels.Acrossmanyoftheirapplications,thereareasetofrecurringstrengthsandweaknesseswhichareexploredinthissection.Particularreferenceismadetotheapplicationsofthesemodelstoproblemsineconomicsandthesocialsciences.

StrengthsEmergentbehaviourThesinglemostpowerfulfeatureofagent-basedmodellingisthattheindividualactionsoftheagentscombinetoproducemacroscopic(1)behaviour.

Agoodexampleofthisistheherdingofsheeportheflockingofbirds.(2)Individualbehaviourscombinetoproduceaneffectwhichlooksorganisedevenwhentherulesforeachagentareincrediblysimple.(3)Trafficjamsareanotherfamiliarandunwelcomeexample;modelsandexperimentshaveshownthatjamscanresultevenwhenthereisnoimpedimenttotraffic.(4)Peoplecanherdintheireconomicactionsandexpectationstoo,forinstanceintheirexpectationsaboutinflation.Thishasdirectconsequencesfortheeconomy.

ThemostimportantexampleofemergentbehaviourineconomicsisAdamSmith’smetaphoroftheinvisiblehand:howtheself-interestedactionsofrealagentsintheeconomycombinetoproducesociallyoptimaloutcomes.Oneofthestrengthsofagent-basedmodellingisthatthisinvisiblehandismadevisibleanditsworkingsmaybeexamined.Thisisincontrasttosomeothermodelapproachesinwhichtheactionsofmanyindividualsareassumedtoleadtoaparticularoutcome,oftenusingasinglerepresentativeagent.Thissimplificationisvalidinsomecasesbutnotallcombinationsofbehaviourscanberepresentedbytheactionsofasingleagent.(5)

HeterogeneityAsindividualagentsaremodelled,itispossibletoexploretheconsequencesofagentsbeingheterogeneous;thatisagentsbeingdifferentinsomeway,perhapsbyincome,preferences,educationorproductivity.

Incorporatingheterogeneityallowsforthemodellingofmuchricherbehaviour.Inequalityisagoodexample—aggregatewealthcanincreasebutifitisonlyasmallfractionofthepopulationdrivingthisphenomenonitwouldsuggestvery

Humans Econs

Figure 4 The final distribution of Humans and Econs with f=70%

Figure 5 US Census data for Chicago showing segregation(a)

Source:http://demographics.coopercenter.org/DotMap/.

(a) NateSilver,538.com;seehttp://fivethirtyeight.com/features/the-most-diverse-cities-are-often-the-most-segregated/.

(1) Atthelargescale,inthiscasethesizeofthesystemwhichtheagentsinhabit.(2) SeeMacyandWiller(2002).(3) Anexamplemaybefoundatwww.tjansson.dk/2012/11/yabi-yet-another-boids-

implementation-simulation-of-flocking-animals/.(4)Anexampleofanagent-basedmodeloftrafficjamscanberuninyourinternet

browseratwww.traffic-simulation.de/.(5) Thisisanexampleofthe‘fallacyofcomposition’.

Topical articles Agent-based models: understanding the economy 179

differentunderlyingeconomicreasonsthaniftheentirepopulationwerebecomingwealthier.

StylisedfactsPerhapsthegreatestsuccessofagent-basedmodelsineconomicshasbeenexplainingthestylisedfactsobservedinassetmarkets.(1)(2)Thereareanumberofphenomenaobservedempiricallyinthemarketsforassetssuchasbondsorequitieswhicharenotexplainedbytraditionaleconomictheory.Someofthetwomostwidelyseenacrossmarketsare:

• Clusteredvolatility,inwhichthestandarddeviationofreturnsonanassetexhibitstrendswhichare‘clustered’intime.(3)

• ‘Fattails’,inwhichextremeeventssuchaslargepricechangesoccurmorefrequentlythanwouldbeexpectedifanormal(orGaussian)distributionwasassumedandfarbeyondwhatwouldbeexpectediftraderswerebehavingrationally.AnexampleisshowninChart 1.

TheSanta Fe Artificial Stock Market(4)isagoodexampleofhowtradingactivitiescanaffectaggregatemarketstatistics.Thismodelissimilarinmanyrespectstoatraditionaleconomicmodelbutwiththeimportantdistinctionthatagentshaveheterogeneousexpectationsofreturns.Thismakesitimpossibleforoneagenttoknowwhatotheragents’expectationsare,andthusimpossibletoformanunambiguousandrationalexpectationofprice.Instead,agentsadaptivelylearnusingarangeofexpectationmodels.Anevolutionaryprocessoccursonagents’strategies;theyareconstantlyupdatedinlightoftheactualpathofthemarket.Interestingly,themodelproducestworegimes—onewhichlookslikestherationalexpectationsworldwithamarketpriceatthefundamentalpriceofthefinancialproduct,andoneinwhichclusteredvolatilityand‘fattails’occur.Rapidevolution

ofstrategiescausesthenon-rationalmarketswhicharemorelikethoseobservedinreality.

Manyagent-basedmodelshaveshownthatchartistortrend-basedtrading(inwhichtradersfollowthetrenddirectionofprices),andalsoleverage,(5)cancontributetopriceovershoots,andthatthiscandriveclusteredvolatility,hightradingvolumesandfattails.(6)

RealisticbehavioursThegenerationofrealisticbehaviour,basedonobservedbehaviour,canbeastrengthofagent-basedmodels.Researchinbehaviouraleconomicshasshownthatpeopleoftenuseheuristics(7)whenmakingdecisionsandthattheyarenotfullyrational.Thesebehaviourscanbecollectivelydescribedas‘boundedrationality’.Anexampleisthatpeoplereactmorenegativelytolossthantheydopositivelytogain,aphenomenonknownaslossaversion.Thereareseveralmodelswhichexplorewhathappenswhenpurelyrationaloptionsarenotavailableoraretoocostly,orwhenagents’environmentschangeovertime.(8)

ExploringthepossibilitiesOneoftheadvantagesofagent-basedmodellingisthatitcanveryefficientlyexplorealargenumberofpossibilities.Probabilisticrulesappliedtoeachindividualagentinturncanbeasimplerwayofexploringscenariosthanworkingouthowtheentirepopulationofagentsshouldbehavetogether.Anexampleisinthetransportofparticles,andwasthepromptforFermitooriginallydeveloptheMonteCarlomethod.Anotherisinepidemiology,whichcansimilarlybemodelledeitherwithsetsofequationswhichtrytosummariseallbehaviouratonce,oranagent-basedmodel.Theequationapproachquicklybecomescomplicatedasmoreandmoreagentpropertiesthatarerelevanttodisease(suchashealth,age,andevencommutingpattern)areintroduced.Oragent-basedmodelscanbeappliedtoconflictinwhicharelativelyinflexiblesetofequationsmodellingtherateofchangeofsizeofarmiescanbereplacedwithagent-basedmodelswhichcancapturethefullheterogeneityofcombatantsinmodernwarfare.

(1) SeeHongandStein(1999).(2) SeeCutler,PoterbaandSummers(1989);LuxandMarchesi(1999,2000).(3) SeeCont(2007).(4) SeeLeBaron,ArthurandPalmer(1999).(5) SeeThurner,FarmerandGeanakoplos(2012).(6) SeeTesfatsion(2002).(7) Heuristicsare‘rulesofthumb’formakingdecisionswhichsimplifytheprocessbut

maynotalwaysgivetheoptimaldecisioninallcircumstances.(8) SeeGodeandSunder(1993);Farmer,PatelliandZovko(2005);Challetand

Zhang(1997);Hommes(2006);Axelrod(2006).

Equity prices

Best Gaussian fit

40 20 0 20 40– +

10-0

10-1

10-2

10-3

10-4

Probability density

Month-on-month change, per cent

Chart 1 Not normal: changes in the price of equities have a fat-tailed distribution (1709–2016)

Sources:Hills,ThomasandDimsdale(2016)andBankcalculations.

180 Quarterly Bulletin 2016 Q4

Complexity,non-linearityandmultipleequilibriaAnotherstrengthofagent-basedmodelsisthattheycandescribecomplexsystems.Complexsystemsarecharacterisedbyhavingmanyinterconnectedparts,havingvariableswhichcanchangedramaticallyandwhichcandemonstrateself-organisation.Additionally,complexsystemsundergosudden,dramatictransitions,sometimescalledphasetransitions.Recentworkonagent-basedmodelsofthemacroeconomyhasdescribedphasetransitionsbetweenlowandhighunemployment.(1)Theeconomydisplaysmanyofthecharacteristicsassociatedwithcomplexsystems.

WeaknessesToomuchfreedom?Whileitistruethatagent-basedmodellinghasmanystrengths,italsopresentschallenges.

Inmanyways,thegreateststrength—theflexibilitytomodelsuchavastrangeofscenarios—isalsothegreatestweakness.Thesheerextentofchoiceinconstructingagent-basedmodelsascomparedtomoretraditionaleconomicmodelsmeansthatmodellersfacetheproblemofselectingtherightcomponentsfortheproblemathand.Simulationresultscanvarydramaticallydependingonwhichassumptionsareused,somodellersmusttakegreatcareinchoosingthem.Furtherworkisneededtodevelopobjectivemeansforchoosingthemostappropriateassumptions.

TheLucascritiqueThehugerangeofbehavioursavailableforagentsmeansthatagent-basedmodelscanbevulnerabletotheLucascritique.Thiscritiquecentresaroundthefactthatagents’choicesmaynotfollowhistoricallyobservedrelationshipswhenpolicyinterventionsaremadewhicharepremisedonthoserelationships.Inprinciple,agentbehaviourscanbedesignedtorespondtochangingcircumstancesbutthereisatrade-offbetweencreatingagentsthatwillalwaysfollowtheiroptimalcourseofactionandbuildingsimple,understandablemodels.Thisiswhyfullyrationalbehaviourisusefulasanapproximation:itgivesanunambiguousandrelativelysimplesetofrulesforhowagentscanalwaysactintheirownbestinterests.

Eachagent-basedmodelshouldbeasLucas-critiqueproofaspossiblebutoftenthemostinterestingbehaviours—suchasboundedrationality—aretheoneswhicharethemostdifficulttomakerobusttothecritique.

DifficulttogeneraliseTheproliferationofchoicesinconstructingagent-basedmodelsleadstoanotherweakness,whichisthattheytendtobebespoke.Forinstance,theagent-basedmodelwhichtellsushowbondsaretradedisunlikelytobeveryhelpfulforansweringquestionsaboutthehousingmarket.

CalibrationandinterpretationCalibrationinvolvesadjustingthemodeltofitwiththeknownfacts,forinstanceinitialisingitwithempiricaldata.Validationischeckingthattheoutputofthemodelisreasonablegivenwhatisknown,andperhapscross-checkingitwithothermodelsorvariationsintheassumptions.Ifamodelcontainsmanydifferentoptionsinhowitisconstructed,itcanspuriouslyreproducedatathatlooksimilartoempiricaldata.Thisisknownasoverfitting,anditisaproblemforallmodels.Calibrationisevenmoredifficultinagent-basedmodels,however,becausetheytypicallyproducestylisedfactsratherthanquantitativeforecastsandtherearevariouswaystheagreementwithempiricallyobservedstylisedfactscouldbeassessed.

Theresultsofagent-basedmodelscanalsobedifficulttocommunicatebecausetheymustbepresentedalongsidetheassumptionsusedtocreatethem.Althoughtrueofallmodelstosomeextent,thisproblemislessacutewithmodelsbasedonhistoricaldataaloneastheyusecommonstatisticaltechniques.Norisitthecasewithmodelsbasedonrationalexpectations;ifagentscanonlyactperfectlyrationallythenthereisastrongconstraintwhichiseasilyunderstoodacrossallsimilarmodels.Whenusingagent-basedmodellingtoinformthechoicesofpolicymakers,thisweaknesscanbeabarrier.

Finally,itcanbedifficulttounderstandhowchangingmodelinputsaffectthemodeloutput.Thisisanunavoidablefeatureofcomplexsystems,andoftherealworlditself.Itisincontrasttomoreanalyticallytractablemodelsinwhichtheeffectsofchangingaparametermayhaveamuchclearereconomicinterpretation.Althougheveryagent-basedmodeldoeshaveauniquemathematicalrepresentation,theequationswouldbedifficulttotranscribefromacomputerprogramme.

Despitethesechallenges,agent-basedmodelsprovideanimportanttoolforunderstandingtheworld,andonewhichhasdeliveredinanastonishingrangeofscenarios.

Wenowturntohowthesemodelscanimproveourunderstandingoftheeconomyasawhole,atopicwhichisespeciallyrelevanttocentralbanks.

Macroeconomic agent-based modelling

Themacroeconomyischaracterisedbyhavingbusinesscycles:fluctuationsinthegrowthofGDParounditslong-termtrend.Instandardmacroeconomicmodelling,thesefluctuationsaretheresultofunexplained(‘exogenous’)shocks.(2)Forinstance,inflationwouldbeforcedtosuddenlychangebutnotasa

(1) SeeGualdiet al(2015).(2) Ashockcouldbedescribedasanunexpectedanddiscontinuouschangeinavariable.

Topical articles Agent-based models: understanding the economy 181

consequenceofanyemergentphenomenawithinthemodel.Thesearecalledexogenousshocks.

Intherealworld,thefluctuationsinGDParelikelytobeendogenous—thatis,generatedbytheeconomyitself.Agent-basedmodelsprovideawayofmakingthesefluctuationsendogenous,andthereforealsoprovidearoutetounderstandingtheircausesandwhatpoliciesmightaffectthem.TheGreatRecessionisacompellingexampleofareasonwhypolicymakersneedtounderstandwhatdrivesthesefluctuations.

Severalagent-basedmodelshavebeenputtingtogetherthedifferentelementsandagentswhicharerequiredtorealisticallyreproducethestylisedfactsoftheeconomyofanentirecountry,orevenseveralcountriesinterlinkedbytrade.Theseelementsincludetheentryandexitoffirms,(1)endogenousinnovation,monetarypolicyandfiscalpolicy.

Oneofthesemacroeconomicmodelsespeciallyaddressesmonetarypolicy.(2)Init,therearefirms,consumers,andpriceswhicharechangedaccordingtosimpleexpectations.Businesscyclessimilartothoseobservedinrealityaregenerated.Asimulatedexperimentshowsthatanactivemonetarypolicy,formulatedaccordingtoasimplerule,(3)reducesthesizeofthefluctuationsinGDPrelativetohavingastaticpolicyrule.Thisoccursbecausefirms’demandforcreditfallswhenthecentralbankraisesinterestratesaccordingtotherule.

Anothermodel(4)featuresaneconomycomposedofheterogeneouscapitalandconsumption-goodfirms,alabourforce,banks,agovernmentandacentralbank.Capital-goodfirmsperformresearchandproduceheterogeneousmachinetools.Consumption-goodfirmsinvestinnewmachinesandproduceahomogeneousconsumptiongood.Consumption-goodfirmsfinancetheirproductionandinvestmentsprimarilywiththeirliquidassetsand,ifrequired,bankcredit.Capital-goodfirmsproduceusingcashadvancedbytheirconsumers,ratherthanusingbanks.

Byincorporatingthefinancialsector,thismodelisabletoreproducemanyfeaturesseeninempiricalmacroeconomics,includingthecyclesinGDP,investmentandconsumption,aswellasthevolatilityofthesethreevariablesrelativetoeachother.Bankingcrisesarealsoanemergentphenomenaofthemodel;ashighproductionandinvestmentlevelsraisefirms’debt,thefirms’networthdecreases,increasingtheircreditrisk.Banksthenrationcreditandforcefirmstocurbproductionandinvestment,withthepotentialtotriggerarecession.Bankfailuresemergefromtheaccumulationofloanlossesonbanks’balancesheets.Themodelallowsforabetterunderstandingofthechainofeventswhichleadtobankingcrises.Confidencethattheseeventsdoreflecttherealworldsituationcanbegainedfromthereproductionof

stylisedfactssuchasthedistributionofbankingcrisisdurationsbeingveryclosetotheempiricalone.

ExperimentsonmonetarypolicywiththismodelsuggestthatadualmandatetotargetbothinflationandunemploymentresultinahigheraveragegrowthinGDPwithlowervolatilitythantargetinginflationaloneachieves.

Othermacroeconomicagent-basedmodels(5)havelookedathowinterestratesareset,(6)(7)athowliquiditytrapscanbeendogenously(8)generated(9)andattheeffectsofunconventionalmonetarypolicy.(10)

Thecostincomplexityofthesemacromodelsisbalancedbytheinsightswhicharegenerated.Theycanreproduceanimpressivelistofmacroeconomicstylisedfacts:businesscycles;theprocyclicalityofproductivity,nominalwages,firms’debt,bankprofitsandinflation;thecountercyclicalityofunemployment,(11)prices,mark-ups,andloanlosses;andtheappearanceoffattailsinthedistributionofoutputgrowth.Alternativeandcomplementarymodels,suchasdynamicstochasticgeneralequilibriummodels,havenotbeenabletogenerateallofthesephenomenaendogenously.(12)Thesemodelstherebyaidtheunderstandingofhowcomplexmacro-levelphenomenaemergefromunderlyingmicro-levelphenomena.

Thesestrongempiricalcredentialslendconfidencetotheconclusionsofpolicyexperimentsundertakenwithagent-basedmodels.Theflexibilityofthemodelsmeansthatextremelyfine-tunedregulationcanbe‘tested’usingthem.Examplesmightincludetheeffectofregulationonliquidityandprofitability,theinteractionofmicroandmacroprudentialpolicies,orhowcreditnetworkscangiverisetobusinesscyclesandfinancialcrises.(13)Asanexample,theNASDAQstockexchangehasusedanagent-basedmodeltodesignregulationwhicheliminatesloopholesthatcouldbeabusedbyitsusers.(14)

Thenextsectiondiscussestwoagent-basedmodelswhichhavebeendevelopedintheBankandwhichattempttoreplicatethestylisedfactsobservedintwodifferentmarkets:corporatebondsandhousing.

(1) SeeEliasson(1991).(2) SeeGattiandDesiderio(2015).(3) TheTaylorrule;seeTaylor(1993).(4) SeeDosiet al (2015);thismodelincorporatesaspectsofKeynesian,Schumpeterian

andMinskianeconomics.(5) SeeDilaver,JumpandLevine(2016).(6) SeeDelliGattiet al(2005).(7) SeeRaberto,TeglioandCincotti(2008).(8) Havinganinternalcauseratherthanbeingtheresultofanexternalshock.(9) SeeOeffner(2008).(10)SeeCincotti,RabertoandTeglio(2010).(11) SeeGualdiet al(2015).(12)SeeAscari,FagioloandRoventini(2015).(13)SeeGatti,GaffeoandGallegati(2010).(14)SeeBonabeau(2002).

182 Quarterly Bulletin 2016 Q4

Agent-based modelling in the Bank of England

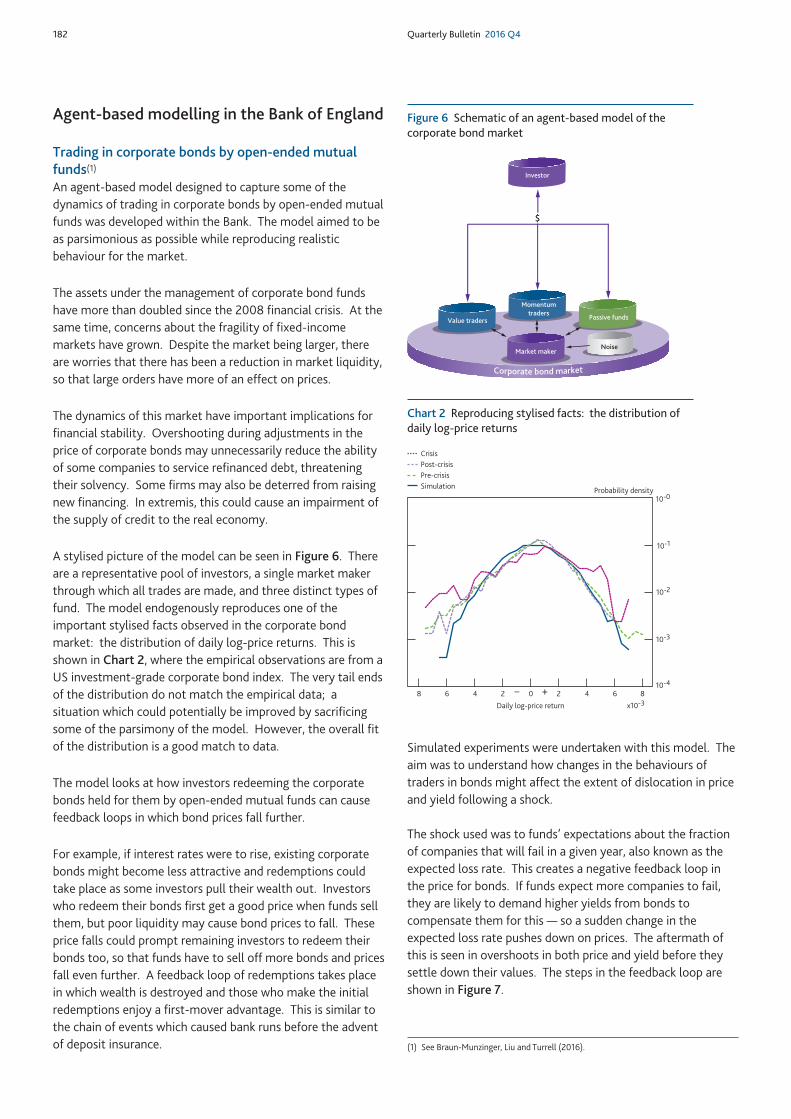

Trading in corporate bonds by open-ended mutual funds(1)

Anagent-basedmodeldesignedtocapturesomeofthedynamicsoftradingincorporatebondsbyopen-endedmutualfundswasdevelopedwithintheBank.Themodelaimedtobeasparsimoniousaspossiblewhilereproducingrealisticbehaviourforthemarket.

Theassetsunderthemanagementofcorporatebondfundshavemorethandoubledsincethe2008financialcrisis.Atthesametime,concernsaboutthefragilityoffixed-incomemarketshavegrown.Despitethemarketbeinglarger,thereareworriesthattherehasbeenareductioninmarketliquidity,sothatlargeordershavemoreofaneffectonprices.

Thedynamicsofthismarkethaveimportantimplicationsforfinancialstability.Overshootingduringadjustmentsinthepriceofcorporatebondsmayunnecessarilyreducetheabilityofsomecompaniestoservicerefinanceddebt,threateningtheirsolvency.Somefirmsmayalsobedeterredfromraisingnewfinancing.Inextremis,thiscouldcauseanimpairmentofthesupplyofcredittotherealeconomy.

AstylisedpictureofthemodelcanbeseeninFigure 6.Therearearepresentativepoolofinvestors,asinglemarketmakerthroughwhichalltradesaremade,andthreedistincttypesoffund.Themodelendogenouslyreproducesoneoftheimportantstylisedfactsobservedinthecorporatebondmarket:thedistributionofdailylog-pricereturns.ThisisshowninChart 2,wheretheempiricalobservationsarefromaUSinvestment-gradecorporatebondindex.Theverytailendsofthedistributiondonotmatchtheempiricaldata;asituationwhichcouldpotentiallybeimprovedbysacrificingsomeoftheparsimonyofthemodel.However,theoverallfitofthedistributionisagoodmatchtodata.

Themodellooksathowinvestorsredeemingthecorporatebondsheldforthembyopen-endedmutualfundscancausefeedbackloopsinwhichbondpricesfallfurther.

Forexample,ifinterestratesweretorise,existingcorporatebondsmightbecomelessattractiveandredemptionscouldtakeplaceassomeinvestorspulltheirwealthout.Investorswhoredeemtheirbondsfirstgetagoodpricewhenfundssellthem,butpoorliquiditymaycausebondpricestofall.Thesepricefallscouldpromptremaininginvestorstoredeemtheirbondstoo,sothatfundshavetoselloffmorebondsandpricesfallevenfurther.Afeedbackloopofredemptionstakesplaceinwhichwealthisdestroyedandthosewhomaketheinitialredemptionsenjoyafirst-moveradvantage.Thisissimilartothechainofeventswhichcausedbankrunsbeforetheadventofdepositinsurance.

Simulatedexperimentswereundertakenwiththismodel.Theaimwastounderstandhowchangesinthebehavioursoftradersinbondsmightaffecttheextentofdislocationinpriceandyieldfollowingashock.

Theshockusedwastofunds’expectationsaboutthefractionofcompaniesthatwillfailinagivenyear,alsoknownastheexpectedlossrate.Thiscreatesanegativefeedbackloopinthepriceforbonds.Iffundsexpectmorecompaniestofail,theyarelikelytodemandhigheryieldsfrombondstocompensatethemforthis—soasuddenchangeintheexpectedlossratepushesdownonprices.Theaftermathofthisisseeninovershootsinbothpriceandyieldbeforetheysettledowntheirvalues.ThestepsinthefeedbackloopareshowninFigure 7.

(1) SeeBraun-Munzinger,LiuandTurrell(2016).

Corporate bond market

$

Value traders

Momentumtraders Passive funds

Investor

Market makerNoise

Figure 6 Schematic of an agent-based model of the corporate bond market

Daily log-price return

8 6 4 2 0 2 4 6 8

10-0Probability densitySimulation

Pre-crisis

– +

10-1

10-2

10-3

10-4

x10-3

CrisisPost-crisis

Chart 2 Reproducing stylised facts: the distribution of daily log-price returns

Topical articles Agent-based models: understanding the economy 183

Giventheshock,anditsknowneffectsin‘normal’times,scenariosinwhichthetradingbehaviourwasdifferentcouldbeexplored.

Inoneofthesescenarios,theeffectofanincreaseinthefractionoffundswithpassivetradingstrategieswasexplored.Thisledtoasurprisingresult;thereisatailriskofsevereovershootswhenthepresenceofpassiveinvestmentfundsincreases.Anotherfindingisthatifallfundsweretoincreasethetimewindowoverwhichredemptionsweremadebyinvestors,theextentofpricedislocationwouldbesignificantlyreducedintimesofcrisis.ThisisbecausethefeedbackloopshowninFigure 7isstrongerwheninvestorswithdrawanamountofwealthonasingledayasopposedtowithdrawingitoveralongertimeperiod.

An agent-based model of the UK housing market(1)

Thehousingmarkethasoftenbeenasourceoffinancialstressandcrisis,lookingacrossawiderangeofcountriesandawidespanoftime.Themarketexhibitsclearandsignificantcyclicality.Capturingthesecyclicaldynamicsisnotstraightforwardandonepotentialreasonisthatthehousingmarketcomprisesmanytypesofparticipant—forinstancerenters,first-timebuyers,andbuy-to-letlandlords.Theseagentsareheterogeneousbyincome,gearingandlocation,sotheyhavedifferentincentives.Thecombinationoftheiractionsgivesrisetothecyclicaldynamics.

Inadditiontoabankingsector(mortgagelender)andacentralbank,themodelcompriseshouseholdsofthreetypes:

• renterswhodecidewhethertoattempttobuyahousewhentheirrentalcontractendsand,ifso,howmuchtobid;

• owner-occupierswhodecidewhethertoselltheirhouseandbuyanewoneand,ifso,howmuchtobid/askfortheproperty;and

• buy-to-letinvestorswhodecidewhethertoselltheirrentalpropertyand/orbuyanewoneand,ifso,howmuchtobid/askfortheproperty.Theyalsodecidewhethertorentoutapropertyand,ifso,howmuchrenttocharge.

Thebehaviouralrulesofthumbthathouseholdsfollowwhenmakingthesedecisionsarebasedonfactorssuchastheirexpectedrentalpayments,housepriceappreciationandmortgagecost.Thesehouseholdsdiffernotonlybytype,butalsobyage,income,bankbalances,rentalpaymentandotherproperties.

Animportantfeatureofthemodelisthatitincludesanexplicitbankingsector,whichprovidesmortgagecredittohouseholdsandwhichsetsthetermsandconditionsavailabletoborrowersinthemortgagemarket.Thebankingsector’slendingdecisionsarethemselvessubjecttoregulationbyacentralbank,whichsetsloantoincome(LTI),loantovalue(LTV),andinterestcoverratiopolicies(ICR).Thevariousdifferentagents,andtheirinterlinkages,areshowninFigure 8.

ThismodelwascalibratedusinghousingmarketdatasourcesandhouseholdsurveyssothattheagentsinthemodelhavecharacteristicswhichmatchthoseintheUKpopulationoveraparticularperiodoftime.Itincludesbehaviouralcharacteristicssuchashowoftenandbyhowmuchthepriceofahouseisreducedifitremainsunsold.

Funds’ demand forbonds is reduced

Price falls as market makersees reduced demand

Returns to investors fall as aconsequence of price drop

Investors reduce allocationof cash to funds

Shock toexpectedloss rate

Funds’ wealth is reduced

Figure 7 Capturing non-linear relationships: the feedback loop following a shock to funds’ expected loss rate

(1) SeeBaptistaet al(2016).

Central bank

sets caps on LTV, LTIand ICR ratios, andaffordability tests

Ownershipmarket

Rental market

Buy-to-letinvestors

Renters

Households

SocialhousingOwner-occupiers

Bank

givesmortgages

Figure 8 Agents and interactions in the housing market model

184 Quarterly Bulletin 2016 Q4

Oneofthekeyfeaturesofthemodelisthatitisabletoendogenouslygeneratereal-worldhousepricecyclesgeneratedbythemodelinChart 3.ItalsoreproduceskeyaspectsoftheUKhousingmarket,suchastheempiricaldistributionoftheshareofloansbyloantoincomebandbasedontheProductSalesDatabase(PSD)ofUKmortgages.ThisisshowninChart 4.

Themodelwasusedtolookatseveralscenariosforthehousingmarket.Inone,alargerbuy-to-letmarketwasfoundtocausemuchlargerswingsinhousepricesduringcycles.Inanother,theeffectofamacroprudentialpolicythatlimitslenderstomakingamaximumof15%ofitsmortgagesatloantoincomeratiosgreaterthan3.5wasexplored(thepre-existingBankpolicyisaratioof4.5).Withthislimitinplace,theendogenouscyclesinhousepricegeneratedbythemodelaredampened.

The future for agent-based modelling in economics

Agent-basedmodelsineconomicsthriveondata.Moredatameansfewerassumptionsneedtobemade,andmoreofthestructureofthemodelcanbebasedonwhatisobserved.Fortunatelyformodellers,theamountofmicroeconomicdatawhichisavailableisincreasingconsiderablyandopportunitiestorefinemodelsarelikelytobeinreadysupply.

Therelentlessimprovementsincomputerprocessingpoweralsoprovidenewopportunitiestomodeltheeconomyonevermoregranularscales,andwithmorecomplexbehaviours.

Inthefuture,theabilitytoincorporaterealisticbehaviourscouldbeexploitedfurtherasartificialintelligencematures.Thetechniqueknownasmachinelearningiswidelyusedbytechcompaniesto,forinstance,suggestthefilmsthataconsumermightliketowatch.(1)Inthefuture,thesetechniquescouldbeusedto‘train’anartificialagenttobehavelikearealconsumerorfirm.Advancedartificialintelligencecouldmakeagent-basedmodelsmoreLucas-critiqueproofbyhavingagentsrespondrealisticallytonewcircumstances.Aglimpseintowhatispossibleinthisrespectwasgivenrecentlywhenanartificialintelligencerepeatedlybeatatrainedfighterpilotinanair-to-aircombatsimulation(2)—anextremelydemandingscenarioforacomputer.Recentprogressbycomputersatvariousgames,includingGoandJeopardy!addweighttothisargument.

Therearelessexoticwaysinwhichprogressmightbeachieved,forinstancewiththedevelopmentofastandardsetoftoolsforcalibratingandvalidatingagent-basedmodels.Anotherwaytomeetsomeofthecriticismlevelledatthesemodelsisforresearcherstoinvestigatethemostparsimoniousmodelspossiblewhichstillreproduceobservedstylisedfacts.

Withrespecttocentralbanks,therearethreeparticularlypromisingareasofdevelopmentforagent-basedmodelling.Thefirstistheongoingapplicationofmacroeconomicagent-basedmodelstomonetarypolicy.Severalmodelswhichexplicitlyincludecentralbankshavenowbeenestablishedandareonhandtoexaminepolicyquestions.Thesecondisinmodellingthebankingandfinancialsector,todeterminehowfinancialstressistransmittedthroughthesystemasawhole.Third,researchingthepotentialimpactoftheintroductionofacentralbankdigitalcurrencycouldbeexploredusinganagent-basedmodel.Asrecentlydescribed,(3)somespecificationsforacentralbankissueddigitalcurrencycouldhaveconsequencesforfinancialstability.Anagent-basedmodelmaybesuitedforanalysingtheeffectsof

Simulation time (years)0 5 10 15 20 25 30 35 40

House price index

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

Chart 3 A benchmark run of the model showing boom and bust cycles in the house price index

0

5

10

15

20

25

0.0 0.5 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 5.5 More

Share of total loans, per cent

Loan to income band

Model simulation

PSD data

Chart 4 The model can reproduce the loan to income distribution for the United Kingdom

(1) SeeFriedman,HastieandTibshirani(2001).(2) SeeErnestet al(2016).(3) SeetheBankofEngland’sresearchquestionsoncentralbankdigitalcurrencies,

availableatwww.bankofengland.co.uk/research/Documents/onebank/cbdc.pdf.

Topical articles Agent-based models: understanding the economy 185

thedifferentpossiblespecificationsofacentralbankdigitalcurrency.

Conclusion

Sincetheirinception,agent-basedmodelshavebroughtawealthofinsightstothoseproblemstowhichtheyaresuited.Theyhavefounduseinanastonishinglydiverserangeofsubjects;fromtigerstotraders,fromparticlestopeople.

Thisincludescomplexsystemsgenerally,butparticularlythoseinwhichoutcomesemergefromindividuals’choicesoragentsareheterogeneous.Thishasobvious,usefulapplicationstomodellingtheeconomyandmanyexampleshavedemonstratedhowagent-basedmodelsineconomicscanaidtheunderstandingofempiricallyobservedphenomena.

A‘bottom-up’perspectiveontheeconomyisacompellingcomplement(1)tothe‘top-down’approacheswhicharealreadywidelyused.

Theagent-basedapproachcomeswithdifficultiesofitsown,especiallyaroundtheassumptionsandvalidity,butthefutureholdspromiseintheserespects,partlyduetoeverimprovingtechniquesbutalsobecauseoftheavailabilityofrichdatasetstocalibratethemodelsagainst.

Agent-basedmodelshaveanimportantplaceinunderstanding,andevendesigning,markets,andprovideauniqueplatformforaugmentingpolicymakers’judgementsabouttheeconomy.

(1) SeeFagioloandRoventini(2012).

186 Quarterly Bulletin 2016 Q4

References

Ascari, G, Fagiolo, G and Roventini, A (2015),‘Fat-taildistributionsandbusiness-cyclemodels’,Macroeconomic Dynamics, Vol.19(2),page465.

Axelrod, R M (2006),The evolution of co-operation,BasicBooks.

Baptista, R, Farmer, J D, Hinterschweiger, M, Low, K, Tang, D and Uluc, A (2016),‘Macroprudentialpolicyinanagent-basedmodeloftheUKhousingmarket’,Bank of England Staff Working Paper No. 619,availableatwww.bankofengland.co.uk/research/Documents/workingpapers/2016/swp619.pdf.

Braun-Munzinger, K, Liu, Z and Turrell, A (2016),‘Anagent-basedmodelofdynamicsincorporatebondtrading’,Bank of England Staff Working Paper No. 592,availableatwww.bankofengland.co.uk/research/Documents/workingpapers/2016/swp592.pdf.

Bonabeau, E (2002),‘Agent-basedmodeling:methodsandtechniquesforsimulatinghumansystems’,Proceedings of the National Academy of Sciences, Vol.99(3),pages7,280–287.

Burgess, S, Fernandez-Corugedo, E, Groth, C, Harrison, R, Monti, F, Theodoridis, K and Waldron, M (2013),‘TheBankofEngland’sforecastingplatform:COMPASS,MAPS,EASEandthesuiteofmodels’,Bank of England Working Paper No. 471,availableatwww.bankofengland.co.uk/research/Documents/workingpapers/2013/wp471.pdf.

Carl, C R G (2015),Search theory and U-boats in the Bay of Biscay,PicklePartnersPublishing.

Carter, N, Levin, S, Barlow, A and Grimm, V (2015),‘Modelingtigerpopulationandterritorydynamicsusinganagent-basedapproach’,Ecological Modelling,Vol.312,pages347–62.

Challet, D and Zhang, Y C (1997),‘Emergenceofcooperationandorganizationinanevolutionarygame’,Physica A: Statistical Mechanics and its Applications, Vol. 246(3),pages407–18.

Champagne, L E and Hill, R R (2009),‘Asimulationvalidationmethodbasedonbootstrappingappliedtoanagent-basedsimulationoftheBayofBiscayhistoricalscenario’,The Journal of Defense Modeling and Simulation: applications, methodology, technology, Vol.6(4),pages201–12.

Cincotti, S, Raberto, M and Teglio, A (2010),‘Creditmoneyandmacroeconomicinstabilityintheagent-basedmodelandsimulatorEurace’,Economics: the Open-Access, Open-Assessment E-Journal, Vol.4.

Cont, R (2007),‘Volatilityclusteringinfinancialmarkets:empiricalfactsandagent-basedmodels’,Long memory in economics,SpringerBerlinHeidelberg,pages289–309.

Cutler, D M, Poterba, J M and Summers, L H (1989),‘Whatmovesstockprices?’,Journal of Portfolio Management,Vol.15(3),pages4–12.

Davis, M, Efstathiou, G, Frenk, C S and White, S D (1985),‘Theevolutionoflarge-scalestructureinauniversedominatedbycolddarkmatter’,The Astrophysical Journal,Vol.292,pages371–94.

Degli Atti, M L C, Merler, S, Rizzo, C, Ajelli, M, Massari, M, Manfredi, P, Furlanello, C, Tomba, G S and Iannelli, M (2008),‘MitigationmeasuresforpandemicinfluenzainItaly:anindividualbasedmodelconsideringdifferentscenarios’,PLoSONE,3(3),e1790.

Delli Gatti, D, Di Guilmi, C, Gaffeo, E, Giulioni, G, Gallegati, M and Palestrini, A (2005),‘Anewapproachtobusinessfluctuations:heterogeneousinteractingagents,scalinglawsandfinancialfragility’,Journal of Economic Behavior and Organization,Vol.56(4),pages489–512.

Dilaver, O, Jump, R and Levine, P (2016),‘Agent-basedmacroeconomicsanddynamicstochasticgeneralequilibriummodels:wheredowegofromhere?’,Discussion Papers in Economics,DP01/16.

Dosi, G, Fagiolo, G, Napoletano, M, Roventini, A and Treibich, T (2015),‘Fiscalandmonetarypoliciesincomplexevolvingeconomies’,Journal of Economic Dynamics and Control,Vol.52,pages166–89.

Eliasson, G (1991),‘Modelingtheexperimentallyorganizedeconomy:complexdynamicsinanempiricalmicro-macromodelofendogenouseconomicgrowth’,Journal of Economic Behavior and Organization,Vol.16(1–2),pages153–82.

Epstein, J M and Axtell, R (1996),Growing artificial societies: social science from the bottom up,BrookingsInstitutionPress.

Topical articles Agent-based models: understanding the economy 187

Ernest, N, Carroll, D, Schumacher, C, Clark, M and Cohen, K (2016),‘Geneticfuzzybasedartificialintelligenceforunmannedcombataerialvehiclecontrolinsimulatedaircombatmissions,JDefManag,6(144).

Fagiolo, G and Roventini, A (2012),‘MacroeconomicpolicyinDSGEandagent-basedmodels’,Revue de l’OFCE,Vol.5,pages67–116.

Farmer, J D, Patelli, P and Zovko, I I (2005),‘Thepredictivepowerofzerointelligenceinfinancialmarkets’,Proceedings of the National Academy of Sciences of the United States of America,Vol.102(6),pages2,254–259.

Friedman, J, Hastie, T and Tibshirani, R (2001),The elements of statistical learning,Springer,Berlin:SpringerSeriesinStatistics,Vol.1.

Gatti, D D and Desiderio, S (2015),‘Monetarypolicyexperimentsinanagent-basedmodelwithfinancialfrictions’,Journal of Economic Interaction and Coordination,Vol.10(2),pages265–86.

Gatti, D D, Gaffeo, E and Gallegati, M (2010),‘Complexagent-basedmacroeconomics:amanifestoforanewparadigm’,Journal of Economic Interaction and Coordination,Vol.5(2),pages111–35.

Geanakoplos, J, Axtell, R, Farmer, D J, Howitt, P, Conlee, B, Goldstein, J, Hendrey, M, Palmer, N M and Yang, C Y (2012),‘Gettingatsystemicriskviaanagent-basedmodelofthehousingmarket’,The American Economic Review,Vol.102(3),pages53–58.

Gode, D K and Sunder, S (1993),‘Allocativeefficiencyofmarketswithzero-intelligencetraders:marketasapartialsubstituteforindividualrationality’,Journal of Political Economy,pages119–37.

Gualdi, S, Tarzia, M, Zamponi, F and Bouchaud, J P (2015),‘Tippingpointsinmacroeconomicagent-basedmodels’,Journal of Economic Dynamics and Control,Vol.50,pages29–61.

Haldane, A G (2016),‘Thedappledworld’,availableatwww.bankofengland.co.uk/publications/Documents/speeches/2016/speech937.pdf.

Heppenstall, A J, Crooks, A T, See, L M and Batty, M (eds)(2011),Agent-based models of geographical systems,SpringerScienceandBusinessMedia.

Hills, S, Thomas, R and Dimsdale, N (2016),‘Threecenturiesofdata—version23’,availableatwww.bankofengland.co.uk/research/Pages/onebank/threecenturies.aspx.

Hommes, C H (2006),‘Heterogeneousagentmodelsineconomicsandfinance’,Handbook of Computational Economics,Vol.2,pages1,109–86.

Hong, H and Stein, J C (1999),‘Aunifiedtheoryofunderreaction,momentumtrading,andoverreactioninassetmarkets’,The Journal of Finance,Vol.54(6),pages2,143–84.

LeBaron, B, Arthur, W B and Palmer, R (1999),‘Timeseriespropertiesofanartificialstockmarket’,Journal of Economic Dynamics and Control,Vol.23(9),pages1,487–516.

Lux, T and Marchesi, M (1999),‘Scalingandcriticalityinastochasticmulti-agentmodelofafinancialmarket’,Nature,Vol.397(6719),pages498–500.

Lux, T and Marchesi, M (2000),‘Volatilityclusteringinfinancialmarkets:amicrosimulationofinteractingagents’,International Journal of Theoretical and Applied Finance,Vol.3(4),pages675–702.

Macy, M W and Willer, R (2002),‘Fromfactorstoactors:computationalsociologyandagent-basedmodeling’,Annual Review of Sociology,pages143–66.

Mankiw, N G (2006),‘Themacroeconomistasscientistandengineer’,The Journal of Economic Perspectives,Vol.20(4),pages29–46.

Metropolis, N (1987),‘ThebeginningoftheMonteCarlomethod’,Los Alamos Science,Vol.15(584),pages125–30.

Metropolis, N, Rosenbluth, A W, Rosenbluth, M N, Teller, A H and Teller, E (1953),‘Equationofstatecalculationsbyfastcomputingmachines’,The Journal of Chemical Physics,Vol.21(6),pages1,087–92.

Metropolis, N and Ulam, S (1949),‘TheMonteCarlomethod’,Journal of the American Statistical Association,Vol.44(247),pages335–41.

188 Quarterly Bulletin 2016 Q4

Oeffner, M (2008),‘Agent–basedKeynesianmacroeconomics—anevolutionarymodelembeddedinanagent–basedcomputersimulation’,MPRA Paper 18199.

Raberto, M, Teglio, A and Cincotti, S (2008),‘Integratingrealandfinancialmarketsinanagent-basedeconomicmodel:anapplicationtomonetarypolicydesign’,Computational Economics,Vol.32(1-2),pages147–62.

Rosato, A, Strandburg, K J, Prinz, F and Swendsen, R H (1987),‘WhytheBrazilnutsareontop:sizesegregationofparticulatematterbyshaking’,Physical Review Letters,Vol.58(10),page1,038.

Schelling, T C (1969),‘Modelsofsegregation’,The American Economic Review,Vol.59(2),pages488–93.

Schelling, T C (1971),‘Dynamicmodelsofsegregation’,Journal of Mathematical Sociology,Vol.1(2),pages143–86.

Taylor, J B (1993),‘Discretionversuspolicyrulesinpractice’,Carnegie-Rochester Conference Series on Public Policy,North-Holland,Vol.39,pages195–214.

Tesfatsion, L (2002),‘Agent-basedcomputationaleconomics:growingeconomiesfromthebottomup,Artificial Life,Vol.8(1),pages55–82.

Thurner, S, Farmer, J D and Geanakoplos, J (2012),‘Leveragecausesfattailsandclusteredvolatility’,Quantitative Finance,Vol.12(5),pages695–707.

Turrell, A E (2013),‘Processesdrivingnon-Maxwelliandistributionsinhighenergydensityplasmas’,Doctoralthesis,ImperialCollegeLondon.

Turrell, A E, Sherlock, M and Rose, S J (2015),‘Ultrafastcollisionalionheatingbyelectrostaticshocks’,Nature Communications,Vol.6.

von Neumann, J (1951),‘Thegeneralandlogicaltheoryofautomata’,Cerebral Mechanisms in Behavior,Vol.1(41),pages1–2.

Werner, F E, Quinlan, J A, Lough, R G and Lynch, D R (2001),‘Spatially-explicitindividualbasedmodelingofmarinepopulations:areviewoftheadvancesinthe1990s’,Sarsia,Vol.86(6),pages411–21.

Zeeman, E C (1974),‘Ontheunstablebehaviourofstockexchanges’,Journal of Mathematical Economics,Vol.1(1),pages39–49.