aggressive investment, financing policy of working …universalrg.org/fulltext/201419724.pdf ·...

TRANSCRIPT

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

170

The 2014 third Conference on Modern Management Sciences (CMMS 2014)

Aggressive Investment, Financing Policy of working capital with

profitability

Esmaeil amiri Master Student of Accounting , Shahid Bahonar University of Kerman, Kerman.

Abstract- In this study, Investigate the relationship between Aggressive Investment Policy and

Aggressive Financing Policy of working capital with profitability of Tehran’s stock market were

analyzed. For this purpose statistical society includes 93 firms and also, 1 period of 5 years (2005-

2009).with systematic elimination method were selected. The results indicate that there is no

relationship between(AFB) and (AIP). Also, there is no significant relationship between AIP

with ROA and ROE . Further analysis showed that is no significant relationship between AFP

with ROA and is no significant relationship AFP with ROE.

Keywords; Aggressive, Conservative, working capital, profitability.

1.Introduction

The definition of working capital in accounting literature is current assets minus current debts

and indicates the amount company's investment in cash, marketable securities, Commercial

receivable accounts, Inventories minus current debts. Some author, define working capital as the

sum of the current assets and current debts and expressed their differences as the net working

capital. In other words, net working capital represents that part of the current assets which is

more than the current debts and is protected through long-term loan and equities. Shabahang,

2008).

Today, working capital management which is the resource and current expenditures management

are significant for maximizing shareholders wealth as part of the financial management

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

171

responsibility. Now, the financial management focuses at topics, such as the relationship

between risk and return and maximizing the return against risk. Since the financial management

has the significant impact on organizations improvement and performance and on function

enhancement and their profitability, investment and Financing decisions is the most important

financial decision of a company which is considered as the sub-category of working capital

management.(Nikoomaram et al, 2006)

There are various strategies for working capital which are obtained by modulating current assets

and current debts strategies. In working capital management, according to different conditions,

some appropriate strategies should be selected in order to handle effectively the current assets

and debts of a commercial unit, and the financial needs of the commercial unit provide

properly.As a result, the company shareholder return and the shareholders wealth would be

increased. The total strategies of working capital management would be categorized into three

categories: 1) conservative strategies 2) Aggressive strategies 3) moderate strategies. (Jhankhany

and Parsaeian, (2001), RaymondP(1986)).

2.Theoretical Foundations & Background

The growing importance of working capital in continuation of business unit has led to several

strategies considered for working capital management. Profit units are able to impact the

company liquidity by means of using different strategies with regard to working capital

management. Each of the various strategies has different risk and efficiency. Financial managers

of the companies with regard to conditions prevailing in the company as well as their personality

and individuality would select “daring” or risk strategy and/or “conservative” or risk aversion

strategy.

The liquidity of the company can be influenced by using different strategies in regard to working

capital management. The working capital managers are divided into two categories: conservative

and Aggressive. Conservative strategy in working capital management causes the increase of

liquidity strength excessively. In implementing conservative policies, the risk of the inability of

maturity debts refund has been tried to reach to the lowest level. In this strategy, the manager try

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

172

to keep the large amount of the current assets (whose return rate is low). Hence, companies with

this kind of strategy have risk liquidity and less refund. . Aggressive strategy manager, with the

lowest current asset, try to take maximum advantage from current debts through daring strategy

and manage the company in this way. In implementing this strategy, the liquidity risk would

increase and the company which carries out this strategy often encounters such situation that

cannot pay the debt maturities. On the other hand, because the amount of current asset is at its

lowest level, the rate of the investment refund would be increased (of course, if the company is

not bankrupted). Companies that use risk strategy actually accept a high risk and their refund rate

is so high. Companies can apply various strategies in managing the current assets and debts.By

combining different strategies, a policy can be applied in order to optimize the working capital.

Current Assets Strategy

Having a strategy in managing the working capital requires determining and maintaining a

certain level of each of the current asset andtotal current assets.

Conservative Strategy (in current assets management)

In this kind of strategy, the company tries to keep the liquidity by maintaining the cash and

marketable securities.This is a very low risk strategy. Because having a relatively high liquidity

allows the company to provide the goods inventory sufficiently and sell on credit.

Risk Strategy (in working capital management)

The manager who uses risk strategy always tries to lessen the cash and marketable securities. If

the manager acts daringly, he will attempt to reduce the funds which are invested in products

inventory. A company which has the courage to decrease the cash and securities should accept

the risk of lack of timely payment of debt maturities. Such company may not be able to meet the

customers’ needs and it will run at a loss. For compensating this loss, the company tries to use

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

173

financial resources in order to provide the fixed assets. This strategy means that, the rate of fixed

assets refund is much higher than the rate of cash and marketable securities efficiencies.

The conservative manager tries to lessen the rate of short-term loan in company’s capital

structure. He tries to use long-term loans with floating interest in order to provide current assets.

The manager who is so conservative attempts to use other financial resources (shareholders

capital) instead of taking out such loans. The structure of the company in which this policy is

applied almost consists of two types: debts and equity.

If a manager use risk policy, he tries to maximize the level of short-term loans and supplies the

current assets from these loans. This policy does not mean that the company never uses the long-

term loan. Because the fixed assets can be used from long-term loans. (Jhankhany and Parsaeian,

(2001), RaymondP(1986)).

Working capital is a vital part of business investment which is essential for continuous business

operations. It is required by a firm to maintain its liquidity, solvency and profitability

(Pirashanthini et al,2013).

Working capital management is an essential part of the short-term finance of a firm. With an

efficient working capital management, a firm can release capital for more strategic objectives,

reduce the financial costs, and improve profitability. (Taghizadeh et al,2012) studies the

relationship of working capital management on performance of firms Listed in Tehran Stock

Exchange (TSE). Average Collection Period, Inventory Turnover in days, Average Payment

Period, Cash Conversion Cycle, and Net Trading Cycle were used to assess working capital

management, and Net Operating Profitability was used to assess firms' performance.. The results

showed that the increase in Collection Period, Payment Period, and Net Trading will lead

towards the reduction of profitability in the firm. In other words, managers can increase the

profitability of their firms reasonably, by reducing Collection Period, Inventory Turnover, and

Payment Period.

Mohamadi (2009), In study examines the the effect of working capital management on

profitability. The variable used as the profitability measure of companies was the ratio of gross

profit on total assets. Variables used for the measures of capital investment, were Receivables

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

174

Collection Period, inventories turnover, creditors deposit period, and convert cycle of cash fund.

Variables, which were used as control variables, were company size, sale growth, ratio of

financial assets on total assets and financial liabilities to total assets. The result of this research

stated that there is negative relation between companies’ profitability and, and convert cycle of

cash fund. In the other words, managers can increase their companies’ profitability by logical

decreasing Receivables Collection Period, and inventories turnover. The results of this research

relating to creditors deposit period states that he more profitable is the company the less is the

creditor’s cycle.

Malekiniya,(2012). the reviews onthe relationship between working capital policy and

profitability of companies in automobile, pharmaceutical and mineral industries in Tehran Stock

Exchange. The results of this study indicate that there is no direct and significant relationship

between working capital management strategies with earning per share and return on equity, but

there is a direct and significant relation between working capital management strategies and

return on investment but not very strong correlation, and only 6% of the variation in the return on

investment can be justified by the variation in the working capital management strategies.

Zohdi(2011),The reason that most bankruptcy corporations’ does not succeed is the unfavorable

status and improper management of working capital. These corporations have good financial

status in the long run, but because of incompetent working capital, are not able to compete with

other corporations’ and they expelled. Profit units are able to affect corporations’ rate of cash by

applying various policies in relation to working capital management. These strategies can affect

rate of risk and their return. Studied the affect of policies of corporations’ working capital over

the rare of Companies risk. The results of this research reveal that, there is a significant and

positive relationship between the policies of working capital and corporations’ risk. Other

findings of the research show that there is a significant and positive relationship between

corporations’ size and risk.

(Ding et al,2013), with use a panel of over 116,000 Chinese firms over the period 2000–2007 to

analyze the extent to which firms owned by differentagents are able to use working capital to

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

175

mitigate the effects of financing constraints on their fixed capital investment. These findings

indicate that, in the presence of fluctuations in cash flow, firms tend to adjust both their fixed

and working capital investment. Yet, when we differentiate firms into those with a relatively

high and a relatively low working capital to fixed capital ratio, and in the presence of cash flow

shocks, it is only those firms with a high ratio that are able to adjust their working capital

investment. Furthermore, for all but foreign firms, the sensitivity of fixed capital investment to

cash flow is much lower for those firms with high working capital: these may therefore use their

working capital to alleviate the effects of cash flow shocks on their fixed capital investment.To

fully take into account the.

Bei & Wijewardana (2012) to investigates working capital policy (WCP) practices in Sri Lankan

context. For this aim Sample of this investigation consist 155 companies listed in Colombo Stock

Exchange (CSC) from 2002 -2006. The study finding explore the impact of different types of

working capital policy practises are differently affect the firm liquidity, efficiency, profitability

and capacity usage

Nazir & Afza (2007), ) to investigates the traditional relationship between working capital

management policies and a firm’sprofitability. Using the panel data set for the period 1998-2005,

the impact of aggressive working capital investment and financing policies has been evaluated

using return on assets as well as Tobin’s q. The study finds a negative relationship between the

profitability measures of firms and degree of aggressiveness of working capital investment and

financing policies. Theseresults were further validated by examining the impact of aggressive

working capital policieson market measures of profitability, which was not tested before. The

results of Tobin’s q werein line of the accounting measures of profitability and produced almost

similar results for working capital investment policy.

Liquid assets management decisions are very complex. On the one hand, when too much money

is tied up in working capital, the business face higher costs of managing liquid assets with

additional high alternative costs. On the other hand, the higher liquidity assets policy could help

enlarge income from sales. (Michalski 2008).

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

176

ALShubiri (2011), to investigates the Effect of Working Capital Practices on Risk Management

The sample includes 59 industrial firms and 14 banks listed on the Amman Stock Exchange for

the period of 2004-2008. The results indicate a negative relationship between profitability

measures and working capital aggressiveness, investment and financing policy. Firms have

negative returns if they follow an aggressive working capital policy. In general, there is no

statistically significant relationship between the level of current assets and current liabilities on

operating and financial risk in industrial firms. There is some statistically significant evidence to

indicate a relationship between standard deviation of return on investments and working capital

practices in banks.

Pirashanthini et al,(2013), to investigates the relationship between the aggressive working capital

policies and profitability and to identify the impact of working capital policies on profitability

with the samples of twenty Manufacturing companies listed under Colombo stock exchange

(CSE) in Sri Lanka The study found that there is no relationship between the profitability

measures of firms and working capital investment and financing policies. Further, the working

capital aggressive investment and financing policies have no impact on profitability measures of

ROA and ROE.

3.Research Hypotheses:

H1: There is a significant relationship between the Aggressive Investment Policy (of working

capital and profitability.

H2: There is a significant relationship between the Aggressive Financing Policy of working

capital and profitability

H3: There is a significant relationship between Aggressive investment Policy and aggressive

Financing Policy.

4.Measuring the research variables

in this study Variables consists of three sections:

Dependent variable= to calculate the Profitability ratios measure Has been used (ROA) and

(ROE).

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

177

Independent variables=in this research and based on the researches by Afza and Sajid Nazir

(2008) To calculate Aggressive Investment Policy and Aggressive Investment Policy As have

been considered independent variables.

Controlling variables: Variables of firm size, sales growth, asset growth is considered as a control

variable.

Table 1: Calculation of dependent and independent variables

Variable

Symbol Explanation

Aggressive Investment Policy AIP

(Total Current Assets)/(Total Assets)

Aggressive Investment Policy AFP (Total Current Liabilities)/(Total Assets)

Return on Assets ROA Net Income / Assets

Return on Equity ROE Net Income/ Equity

Size Size ln sale

Sales growth SG (current year sales -last year sales)

/ last year sales

5.Methodology:

This study is of applied type as far as goal is concerned and the research method is experimental.

The literature about the research was collected from the theoretical topics of library resources,

scientific databases and local and international papers. In order to assess and analyze the data,

regression method was used. In order to analyze data, EViews software was applied.

6.Sample & Data

The statistical society of this study was selected among the admitted companies to Tehran Stock

Exchange following systematic elimination of banks and insurance companies and financial

mediation and eventually about 93 companies were selected in the cycle of 2005-2009. They had

to possess the following characteristics:

1) The fiscal year of the company had to end on 20 March.

2) The companies should not have had financial changes from 2005 -2009.

3) The companies should have been admitted to Tehran Stock Exchange by the end of fiscal year

2009.

4) The desired data of the research should be available to calculate the test of hypotheses.

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

178

5) They should not have had a stop of transactions for more than 6 months during the study

cycle.

7.Methodology

To test hypotheses 1 and 2, the relationship between profitability and Aggressive Investment

Policy, Aggressive Financing Policy, is used following pattern.

ROA=α+β1 AIP+ β2 Size+β3 SG +ε Model(1)

ROE =α+β1 AIP+ β2 Size+β3 SG +ε Model(2)

ROA=α+β1 AFP+ β2 Size+β3 SG +ε Model(3)

ROE =α+β1 AFP+ β2 Size+β3 SG +ε Model(4)

The following model is estimated to test hypotheses 3

H0:β1=β2 …….y=α+β1x Model(5)

H1:β1≠β2

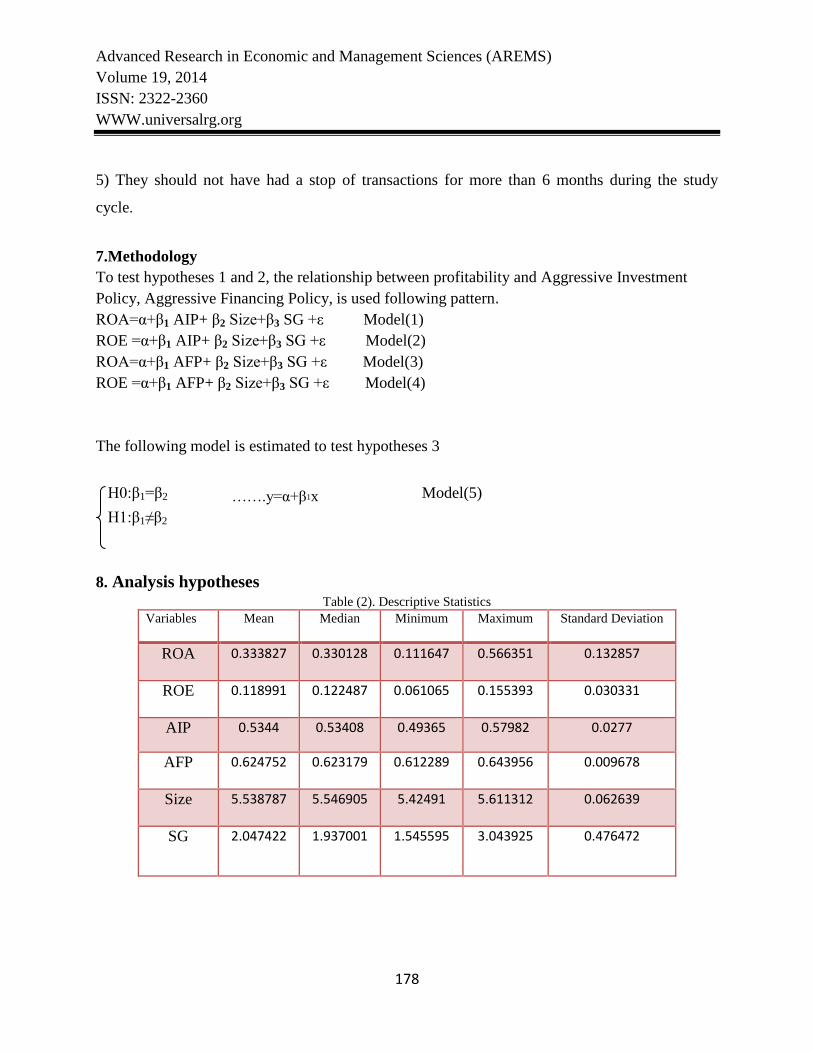

8. Analysis hypotheses

Table (2). Descriptive Statistics

Variables Mean

Median

Minimum

Maximum

Standard Deviation

ROA 0.333827 0.330128 0.111647 0.566351 0.132857

ROE 0.118991 0.122487 0.061065 0.155393 0.030331

AIP 0.5344

0.53408

0.49365

0.57982 0.0277

AFP 0.624752 0.623179 0.612289 0.643956 0.009678

Size 5.538787 5.546905

5.42491

5.611312

0.062639

SG 2.047422

1.937001

1.545595

3.043925 0.476472

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

179

Table (3). Model(1)

Variables Coefficient t-Statistic Prob.

β0 16.767 1.101816 0.0092

AIP -0.96446 -0.29299 0.8186 SIZE 2.69775 1.28273 0.0000 SG 33.437 0.42257 0.0055 D.W 2.28

Table (4). Model(2)

Variables Coefficient t-Statistic Prob.

β0 3.321776 1.134603 0.0099

AIP -0.489465 -0.772869 0.5811

SIZE 0.51963 1.284233 .0000

SG 2.16378 0.142135 .0000

D.W 2.28

Table (5). Model(3)

Variables Coefficient t-Statistic Prob.

β0 14.8559 22.88813 0.0278 AFP -11.1647 -13.5753 0.0468 SIZE -1.17901 -9.42109 0.0073 SG -34.8457 -8.78221 0.0022 (F) 0.039286

Adj.R 0.99

D.W 1.72

Table (6). Model(4)

Variables Coefficient t-Statistic Prob.

β0 1.833145 3.014359 0.2039

AFP -2.49603 -3.23919 0.1906

SIZE -0.04238 -0.36144 .0000

SG 2.741551 0.73746 .0000

D.W 1.72

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

180

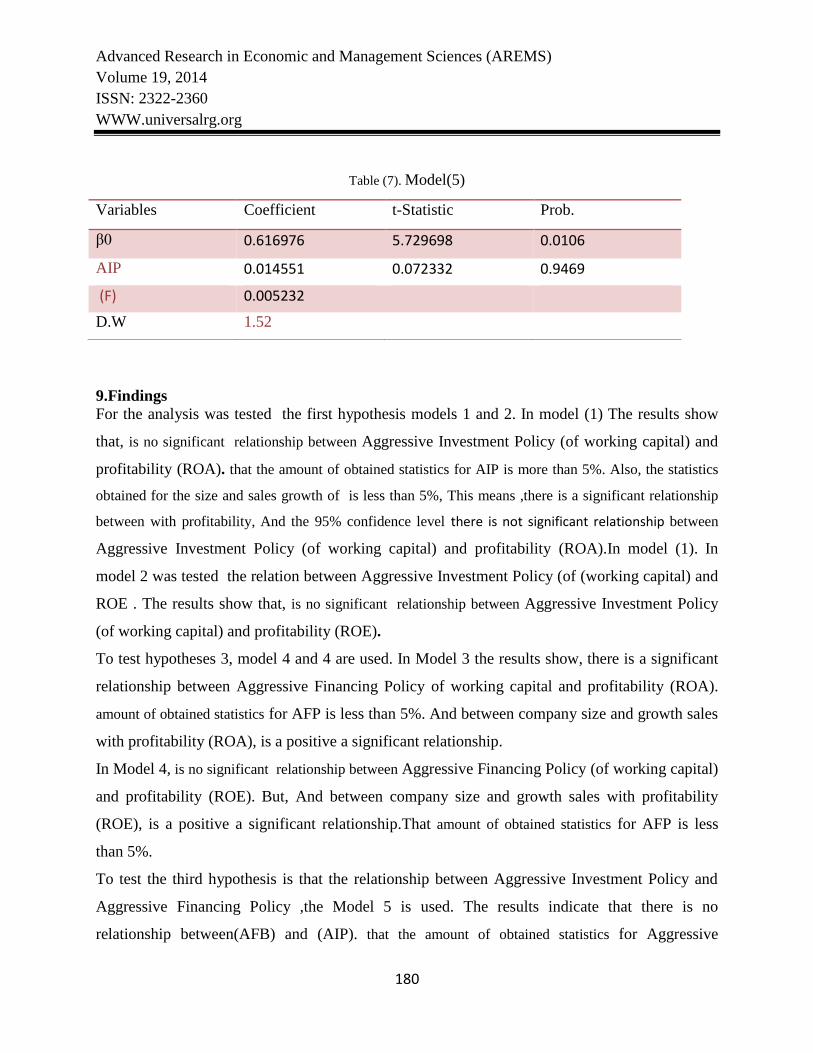

Table (7). Model(5)

9.Findings

For the analysis was tested the first hypothesis models 1 and 2. In model (1) The results show

that, is no significant relationship between Aggressive Investment Policy (of working capital) and

profitability (ROA). that the amount of obtained statistics for AIP is more than 5%. Also, the statistics

obtained for the size and sales growth of is less than 5%, This means ,there is a significant relationship

between with profitability, And the 95% confidence level there is not significant relationship between

Aggressive Investment Policy (of working capital) and profitability (ROA).In model (1). In

model 2 was tested the relation between Aggressive Investment Policy (of (working capital) and

ROE . The results show that, is no significant relationship between Aggressive Investment Policy

(of working capital) and profitability (ROE).

To test hypotheses 3, model 4 and 4 are used. In Model 3 the results show, there is a significant

relationship between Aggressive Financing Policy of working capital and profitability (ROA).

amount of obtained statistics for AFP is less than 5%. And between company size and growth sales

with profitability (ROA), is a positive a significant relationship.

In Model 4, is no significant relationship between Aggressive Financing Policy (of working capital)

and profitability (ROE). But, And between company size and growth sales with profitability

(ROE), is a positive a significant relationship.That amount of obtained statistics for AFP is less

than 5%.

To test the third hypothesis is that the relationship between Aggressive Investment Policy and

Aggressive Financing Policy ,the Model 5 is used. The results indicate that there is no

relationship between(AFB) and (AIP). that the amount of obtained statistics for Aggressive

Variables Coefficient t-Statistic Prob.

β0 0.616976 5.729698 0.0106

AIP 0.014551 0.072332 0.9469

(F) 0.005232

D.W 1.52

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

181

Investment Policy of more than 5%. and obtained amount for Durbin-Watson statistic 1.52, is

between 2.5 to 1.5, which indicate that there is no auto-correlation between each of the

hypotheses.

10.Conclusions

The working capital managers are divided into two categories: conservative and Aggressive.

Conservative strategy in working capital management causes the increase of liquidity strength

excessively. In implementing conservative policies, the risk of the inability of maturity debts

refund has been tried to reach to the lowest level. Aggressive strategy manager, with the lowest

current asset, try to take maximum advantage from current debts through daring strategy and

manage the company in this way. In this study, Investigate the relationship between Aggressive

Investment Policy , Aggressive Financing Policy and profitability of Tehran’s stock market were

analyzed. For this purpose statistical society includes 93 firms and also, 1 period of 6 years (2004-

2008).with systematic elimination method were selected. The results indicate that there is no

relationship between(AFB) and (AIP). Also, there is no significant relationship between AIP

with ROA and ROE . Further analysis showed that is no significant relationship between AFP

with ROA and no significant relationship AFP with ROE.

References

1-Mohamadi ,Mohamad,(2009), effect of working capital management on profitability of

accepted companies in tse, Pajouheshgar (journal of management) , 6(14):91-80.

2-Malekiniya,Nahid,Asgari Alouj Hossein,Ghezelbash Azam,(2012), Study of reaationship

between working capital strategy and profitabilitt measures the companies in automobile,

pharmaceutical and mineral industries in tehran stock exchange ,journal of monetary &

financial economics , 18(2):160-139.

3-Zohdi,Mohhamad, Valipour, Hadi, , Alireza Hashem,Shahabi, ,(2011), Working capital and

corporations’risk policies, The financial accounting and auditing research ; 2(8):210-186.

4-Ding, Sai, Guariglia, Alessandra, Knight, John,(2013), Investment and financing constraints in

China: Does working capital management make a difference?, Journal of Banking &

Finance 37 (2013) 1490–1507.

Advanced Research in Economic and Management Sciences (AREMS)

Volume 19, 2014

ISSN: 2322-2360

WWW.universalrg.org

182

5-Bei , Zhao, W. P Wijewardana,(2012), Working capital policy practice: Evidence from Sri

Lankan companies, Procedia - Social and Behavioral Sciences 40 ( 2012 ) 695 – 700

6-Taghizadeh .V.,Akbari .khsroshahi M.,Ebrati M.R.(2012), An investigation of the association

between working capital management and corporate performance, International journal of

management and business research, 2(3):218-203

7-Nazir , Mian Sajid, Afza, Talat,(2009), Impact of Aggressive Working Capital Management

Policy on Firms’ Profitability, Journal of Applied Finance, Vol. 15, No. 8, pp. 19-30,

8-Michalski ,Grzegorz Marek, (2008), Liquidity or Profitability: Financial Effectivness of

Investments in Working Capita, l, International financial systems, http://ssrn.com/

abstract=1299586

9-Shabahang R,(2008), Financial Management, Audit Organization Publications, Volume I & II,

10 Rahnamay rood poshti ,Nikoomaram H.,. Rahnamay rood poshti.F, Heibati,F,(2010),

Foundations Financial Management, Volume I & II, Termeh Publications,.

11-RaymondP.Neneu,(1986),Fundamentals of managerial finance,3rd ed,Cincinnati ohio:South-

Western Publishing Co.

12- Jhankhany, Ali, Parsaeian, A., (2001), Financial Management, Volume II, issued position