agricultual rent survey to april 2013

DESCRIPTION

Rents rise by 30% - the fastest rate we have recordedTRANSCRIPT

smithsgore.co.uk

Market Intelligence Report

Agricultural Rent SurveyYear to 30 April 2013

Rents rise by 30% - the fastest rate we have recorded

Cover image - passing storm near Shap, Cumbria, England, UK

Rents rise by an average of 30%

Rents for all tenancy types have risen at the fastest rate we have seen since 2007, when this period of rent reviews started. It demonstrates the strong demand and resilience in farming, despite significant economic challenges in other sectors.

As a firm, we agreed more rents in this 12 month period than in any other ‘year’ since 2007.

Given the volume of settlements we agree, we can now use our database to break the market down further, and look at rent reviews of existing and new tenancies.

Rents for existing tenancies rose by 25%, up from 23% for the year ending 30 April 2012.

Rents for new Farm Business Tenancies, with ‘new’ tenants and new tenancies with existing tenants, rose by 59% compared with the previous rent; it was 74% for the year ending 30 April 2012.

This illustrates the competitiveness of the market; rents have soared because of strong demand from farmers due to underlying profitability and relatively few rental opportunities.

The average FBT rents in this report are well below some of the rents that grab the headlines. This reflects the diversity of holdings and land, and that many landlords consider other factors than the highest rent when selecting tenants, such as supporting existing tenants.

Rupert ClarkHead of Rural Practice Petworth officet 01798 345999e rupert.clark @smithsgore.co.uk

Simon Blandford Head of Farm ManagementWinchester officet 01962 857405e simon.blandford @smithsgore.co.uk

Average percentage change in year to 30 April (all farm and tenancy types)

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Overall averageScottish TenanciesFBTAHA

2010-2013201320122011

Key points

• Arable FBT rents are the highest and are increasing fastest

• Rents for higher quality soil continue to increase most

• Scottish rents continue to rise more slowly than elsewhere in Great Britain

Growth by Farm Type2013 High rises in all sectors

Rents for all types of existing tenancies increased by an average of 25% in the year to 30 April 2013, up from 23% in 2012 and the 22% average for 2009 to 2012.

Arable and livestock rents continued to increase the most. Arable rents rose by 34%, up from 26% in 2012, and livestock rents by 26%, the same as in 2012.

These figures are averages and, as stated before, there is considerable variation around the averages, as illustrated by the graph at the end of the existing tenancies section.

Rent review results by farm type in year to April 2013

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Arable £99 £73 34% 149 40,414

Dairy £81 £69 17% 73 18,554

Livestock £53 £44 26% 179 64,578

Mixed £77 £64 21% 173 38,905

Overall average

£76 £61 25% 574 162,451

2010 - 20131 24% increase on average

Rents have risen by 24% on average in the three years to 30 April 2013.

For the average sized farm in the database, this has meant an increase in rent of £3,800 a year – so £11,400 over a three-year rent review cycle.

All sectors have experienced increases, with the largest being in the arable sector, and the lowest for mixed and dairy farms.

Rent review results by farm type 2010 – 2013

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Arable £91 £70 30% 367 90,230

Dairy £81 £69 17% 146 32,854

Livestock £52 £43 25% 444 183,354

Mixed £74 £63 19% 383 86,405

Overall average

£72 £59 24% 1,340 392,843

1 “2010 – 2013” and “last three years” relates to the period between 1 May 2010 and 30 April 2013.

Rents for existing tenancies

Growth by Tenancy Type

2013 FBTs continue to show greatest rises

FBT2 rents rose by 35% compared with 22% for AHA and 13% for Scottish tenancies. This is as rent review clauses in FBTs allow rents to be revised to current open market levels while AHA and Scottish rent tenancies have a less open market nature, although this should change following the Moonzie case, which will apply across Great Britain.

Rent review results by tenancy type in year to April 2013

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

AH

A

Arable £77 £64 20% 80 26,835

Dairy £80 £70 16% 47 11,240

Livestock £48 £40 34% 70 30,702

Mixed £75 £64 18% 101 23,218

AHA average £70 £59 22% 298 91,996

FBT

Arable £134 £89 55% 60 11,183

Dairy £105 £82 28% 16 4,308

Livestock £76 £62 25% 62 9,159

Mixed £90 £72 28% 53 10,731

FBT average £101 £75 35% 191 35,381

Scot

tish

te

na

nci

es

Arable £59 £51 15% 8 2,353

Dairy £49 £46 5% 10 3,006

Livestock £27 £24 14% 43 24,417

Mixed £48 £42 16% 19 4,956

Scottish average £38 £34 13% 80 34,733

Overall average £76 £61 25% 569 162,109

Rent review results by tenancy type in year to April 2013

£0

£20

£40

£60

£80

£100

£120

£140

£160

New rent (£/acre)Old rent (£/acre)

Ove

rall

Scot

tish

Ave

rage

Mix

ed

Live

stoc

k

Dai

ry

Ara

ble

FBT

Ave

rage

Mix

ed

Live

stoc

k

Dai

ry

Ara

ble

AH

A A

vera

ge

Mix

ed

Live

stoc

k

Dai

ry

Ara

ble

AHA FBT Scottish Tenancies All

Rents for existing tenancies

2 NB This data excludes ‘new’ FBTs, which are covered in the rents for new Farm Business Tenancies section.

2010 - 2013 Growth lowest in dairy sector

In these three years, FBT rents have increased by 31%, compared with 22% for AHAs and 14% for Scottish tenancies.

For both FBTs and AHAs, livestock rents have increased particularly strongly in percentage terms.

Dairy rents have risen less than other farm types, which is expected given the tight margins and long-term economic challenges faced by the sector. Industry figures show that only the top 25-33% of dairy farmers are making sustainable profit margins.

Rent review results by tenancy type 2010 - 2013

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

AH

A

Arable £80 £66 22% 233 66,435

Dairy £81 £70 18% 90 20,017

Livestock £52 £43 29% 175 78,734

Mixed £72 £62 18% 250 58,142

AHA average £71 £60 22% 748 223,328

FBT

Arable £117 £80 47% 117 20,378

Dairy £93 £79 18% 40 8,111

Livestock £75 £61 27% 139 25,690

Mixed £92 £76 24% 95 17,213

FBT average £94 £72 31% 391 71,392

Scot

tish

Te

na

nci

es

Arable £67 £59 14% 16 3,374

Dairy £45 £43 6% 16 4,727

Livestock3 £24 £21 15% 115 77,183

Mixed £44 £38 15% 38 11,050

Scottish average £34 £30 14% 185 96,334

Overall average £72 £59 24% 1,324 391,054

3 One reason Scottish livestock rents per acre are lower than in England is as the average farm size is much larger in Scotland.

Rent review results by tenancy type 2010 - 2013

£0

£20

£40

£60

£80

£100

£120

£140

£160

New rent (£/acre)Old rent (£/acre)

Ove

rall

Scot

tish

Ave

rage

Mix

ed

Live

stoc

k

Dai

ry

Ara

ble

FBT

Ave

rage

Mix

ed

Live

stoc

k

Dai

ry

Ara

ble

AH

A A

vera

ge

Mix

ed

Live

stoc

k

Dai

ry

Ara

ble

AHA FBT Scottish Tenancies All

Rents for existing tenancies

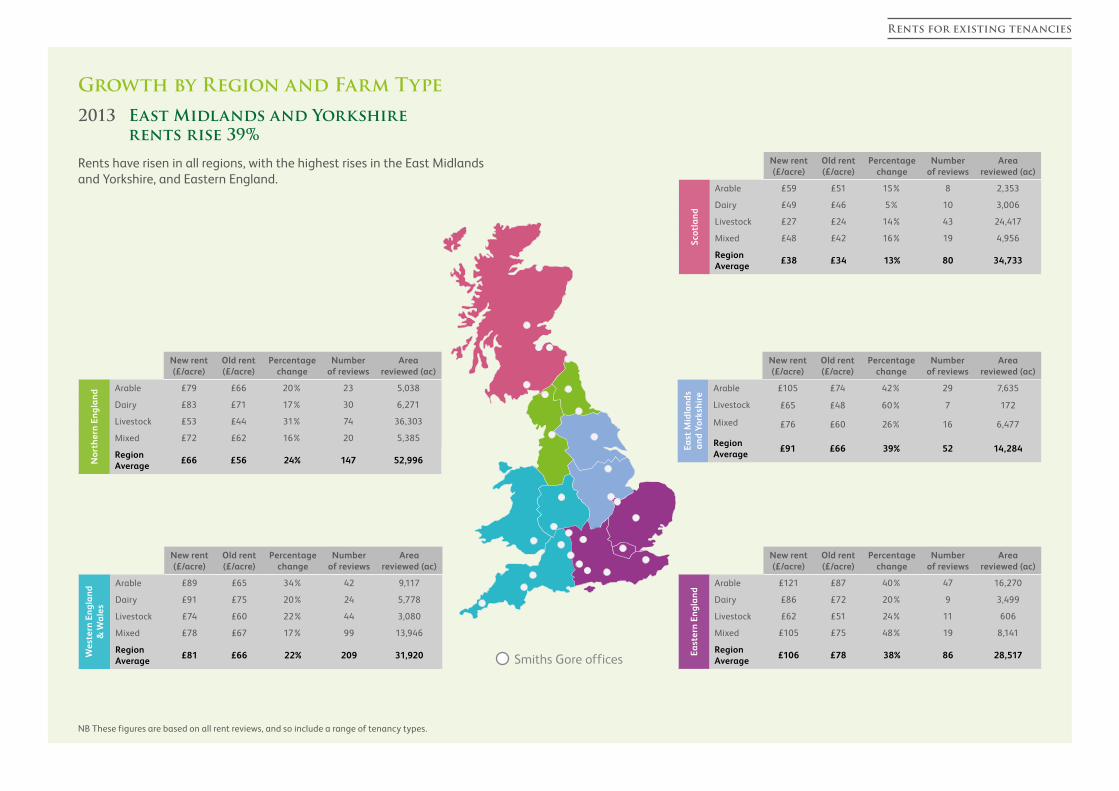

Growth by Region and Farm Type

2013 East Midlands and Yorkshire rents rise 39%

Rents have risen in all regions, with the highest rises in the East Midlands and Yorkshire, and Eastern England.

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Scot

lan

d

Arable £59 £51 15% 8 2,353

Dairy £49 £46 5% 10 3,006

Livestock £27 £24 14% 43 24,417

Mixed £48 £42 16% 19 4,956

Region Average

£38 £34 13% 80 34,733

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

East

Mid

lan

ds

an

d Yo

rksh

ire

Arable £105 £74 42% 29 7,635

Livestock £65 £48 60% 7 172

Mixed £76 £60 26% 16 6,477

Region Average

£91 £66 39% 52 14,284

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

East

ern

Eng

lan

d

Arable £121 £87 40% 47 16,270

Dairy £86 £72 20% 9 3,499

Livestock £62 £51 24% 11 606

Mixed £105 £75 48% 19 8,141

Region Average

£106 £78 38% 86 28,517

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Nor

ther

n En

gla

nd Arable £79 £66 20% 23 5,038

Dairy £83 £71 17% 30 6,271

Livestock £53 £44 31% 74 36,303

Mixed £72 £62 16% 20 5,385

Region Average

£66 £56 24% 147 52,996

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Wes

tern

En

gla

nd

&

Wa

les

Arable £89 £65 34% 42 9,117

Dairy £91 £75 20% 24 5,778

Livestock £74 £60 22% 44 3,080

Mixed £78 £67 17% 99 13,946

Region Average

£81 £66 22% 209 31,920

NB These figures are based on all rent reviews, and so include a range of tenancy types.

Smiths Gore offices

Rents for existing tenancies

Smiths Gore offices

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Scot

lan

d

Arable £67 £59 14% 16 3,374

Dairy £45 £43 6% 16 4,727

Livestock £24 £21 15% 115 77,183

Mixed £44 £38 15% 38 11,050

Region Average

£34 £30 14% 185 96,334

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

East

Mid

lan

ds

an

d Yo

rksh

ire

Arable £84 £65 30% 104 23,219

Dairy £85 £74 16% 8 1,737

Livestock £57 £42 58% 23 4,625

Mixed £79 £67 19% 56 15,363

Region Average

£79 £63 29% 191 44,944

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

East

ern

Eng

lan

d

Arable £108 £81 35% 131 38,586

Dairy £86 £72 20% 9 3,499

Livestock £59 £47 31% 25 3,526

Mixed £87 £66 36% 52 23,547

Region Average

£97 £73 34% 217 69,158

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Nor

ther

n En

gla

nd

Arable £81 £66 22% 35 7,495

Dairy £80 £69 17% 60 11,208

Livestock £54 £45 26% 166 88,331

Mixed £75 £65 16% 31 8,385

Region Average £65 £55 23% 292 115,418

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Wes

tern

En

gla

nd

&

Wa

les

Arable £82 £63 28% 81 17,556

Dairy £90 £77 19% 53 11,683

Livestock £74 £60 25% 115 9,689

Mixed £75 £66 15% 206 28,061

Region Average

£78 £65 21% 455 66,989

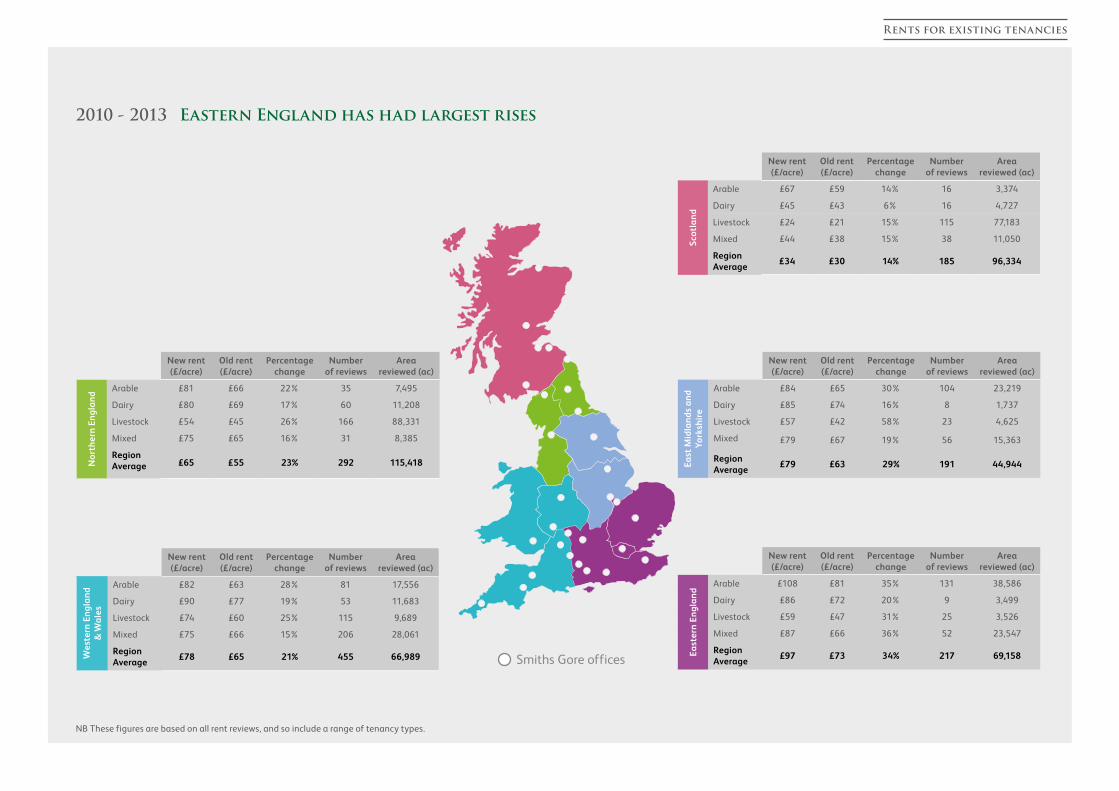

2010 - 2013 Eastern England has had largest rises

NB These figures are based on all rent reviews, and so include a range of tenancy types.

Rents for existing tenancies

The effect of land quality – premium rents for premium land

Not only is the rental value of better quality land higher, rents for Grade 1 and 2 land have risen by the greatest percentage over the last three years. Average Grade 1 rents are now 62% higher than Grade 3, compared with 47% before these reviews were undertaken.

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Grade 1 £131 £96 39% 25 10,992

Grade 2 £94 £72 30% 155 43,638

Grade 3 £78 £65 23% 904 174,828

Grade 4 £45 £37 20% 186 75,090

Grade 5 £12 £10 20% 79 90,733

Overall average £72 £59 23% 1,349 395,280

2010 - 2013 The effect of houses and farm buildings

Equipped AHA holdings with houses and buildings continue to have higher rents than bare land lettings4.

There is very little difference in FBT rents being paid for bare or equipped land. We think this is because the buildings and equipment being offered frequently do not suit the tenants’ needs.

Rents for equipped holdings are affected by the quality and quantity of buildings available. Tenants will pay more for better buildings and equipment.

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of reviews

Area reviewed (ac)

Well equipped £71 £60 21% 197 89,671

Averagely equipped £73 £61 20% 435 183,331

Poorly equipped £59 £48 21% 174 67,222

Overall average £69 £58 20% 806 340,224

4 There is one exception to this which is livestock farms, where extensive equipped holdings mean the average equipped rent is lower.

£0

£20

£40

£60

£80

£100

£120

£140

Overall averageMixedLivestockDairyArable

Equipped FBTBare FBTEquipped AHABare AHA

Rent review results by tenancy type and equipped 2010 - 2013

Rents for existing tenancies

Each point on this graph shows an actual rent agreed. If you look at ‘25%’, this is the point at which 25% of rents are lower and 75% are higher; for arable farms this is £65 per acre. Variation is greatest amongst livestock rents as both very low and high quality land can be used for livestock farming.

Distribution of AHA rent review results

£0

£20

£40

£60

£80

£100

£120

0% 25% 50% 75% 100%

Arable Dairy Livestock Mixed

New

rent

(£/a

cre)

Lowest to highest rent (excluding the top and bottom 5%)Arable Dairy Livestock Mixed

Lowest to highest rent (excluding the top and bottom 5%)

New

rent

(£/a

cre)

0% 25% 50% 75% 100%£0

£20

£40

£60

£80

£100

£120

Top 25% of rents

Rent review results for AHA tenancies by farm type in year to April 2013

Rents for existing tenancies

2013

2013 Strong rental uplift for all farm types

We let just under 12,000 acres on new FBTs in the year to 30 April 2013, which is an average size of 115 acres. The arable lettings averaged 122 acres, whilst livestock lettings averaged 55 acres; mixed lettings at an average of 174 acres were largest. 18% of the lettings were over 200 acres, and there were 13 equipped farms let.

Rents for new FBTs are 57% higher on average than they were under the previous letting of the holding.

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of lettings

Area let (ac)

Arable £135 £90 48% 60 7,305

Livestock £83 £50 74% 24 1,329

Mixed £103 £65 67% 18 3,129

Overall average £117 £76 57% 102 11,763

New tenancies – FBT rents agreed by farm type in year to April 2013

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of lettings

Area let (ac)

Arable £123 £84 42% 115 14,266

Livestock £89 £53 77% 69 6,741

Mixed £98 £69 66% 33 5,408

Overall average £108 £73 56% 217 26,416

New tenancies – FBT rents agreed by farm type 2010 – 2013

5 Scottish tenancies have been excluded as there were not enough new tenancies to produce robust data.

2010-2013

Rents have risen by 56% on average in the three years to 30 April 2013.

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of lettings

Area let (ac)

East Midlands and Yorkshire

£129 £82 78% 26 1,520

Eastern England £125 £89 39% 35 5,349

Northern England £110 £64 77% 21 3,078

Western England & Wales

£99 £69 35% 21 2,131

Overall average £118 £76 59% 103 12,078

New rent (£/acre)

Old rent (£/acre)

Percentage change

Number of lettings

Area let (ac)

East Midlands and Yorkshire

£112 £74 55% 65 5,339

Eastern England £123 £83 48% 61 10,300

Northern England £99 £69 60% 48 7,147

Western England & Wales

£100 £64 60% 50 5,110

Overall average £110 £73 56% 224 27,896

New tenancies – FBT rents agreed by region in year to April 2013 New tenancies – FBT rents agreed by region 2010 – 2013

Rents for new Farm Business Tenancies5

English & Welsh viewPositive outlook for rents

We have continued to settle rents, for both AHAs and FBTs, in 2013 with no evidence of tenants or their agents seriously holding out for standstills or reductions, despite some clouds on the horizon.

The difficulties of last year’s weather may be tempering landlords’ ambitions in some cases, where cropping has been affected, but parties are generally aware that the rent being agreed applies for three years and so needs to reflect more than just one bad (or good) year.

Given the above, and the generally positive outlook for farming, there is little down-side risk for landlords serving notice for reviews in 2014.

However, both landlords and tenants should take care with holdings where the rent is heavily reliant on an agri-environment scheme which is due to expire in 2014 or 2015. There is potentially a 1-2 year period with no grant income and no guarantee of future agri-environment income thereafter.

Toby Metcalfe PartnerEdinburgh officet 0131 344 0885e toby.metcalfe @smithsgore.co.uk

Scottish viewThirst unquenched

It will not come as a surprise to anyone that the weather last summer had a significant impact on agriculture in Scotland. At the time the impact was felt most immediately by the arable sector but there was also a big impact on the livestock sector which has spilled over into this year. In our experience the challenges created by the weather were fully understood by all of our clients and there was a realism about any rent review discussions scheduled for this year. Increases have come about as a result of constructive negotiations and in the main simply reflect the inflationary increase experienced over the preceding three years.

It is interesting to reflect on whether the slight slow down in the pace of rental increases in Scotland is driven only by the weather or if other factors are at play. It is I think fair to report that the mood of farming tenants generally remains buoyant. There is an expectation that the historically long and almost uninterrupted increase in farming incomes will continue on the back of a growing population. This mood is reflected by the rental offers received as a result of open market reletting exercises we have undertaken for clients this year. There is no doubt that the thirst for more land to rent is a very long way from being quenched and this will undoubtedly continue until there is a game changer either in terms of the supply of land to rent or the underlying economics. Neither show any sign of changing in the near future. In broadest summary the drivers continue to be the desire of tenant farmers to grow and spread fixed costs and landowners wish to rationalise the asset. Behind all the headlines there are plenty of constructive examples of the two parties working together to agree rent reviews, consider ways of improving performance and delivering their objectives to mutual advantage.

Stephen Spencer PartnerLichfield officet 01543 266403 e stephen.spencer @smithsgore.co.uk

Our experience over the past year

About the agricultural rent survey

This report provides details of average rents agreed at rent reviews,re-lettings and new lettings in:

(i) 2013: the 12 months to 30 April 2013 (691 rent settlements covering 176,000 acres)

(ii) 2010 - 2013: the 36 months to 30 April 2013 (1,610 rent settlements covering 428,000 acres)

The complete database now contains details of over 2,700 rent settlements, covering over 750,000 acres of land in England, Scotland and Wales with a rent roll in excess of £39 million per annum. It is one of the most comprehensive databases available in Great Britain.

Average rents

Please note that the rents shown are averages and that there can be considerable variation in rent either side of the average depending on the location and quality of the holding and its fixed equipment. Some rents have dropped, usually when properties are taken out of the tenancy agreement, and others increased by well over 100%. This analysis focuses on what might therefore be described as trends.

How we use the database

Our surveyors use the database as a source of information when they are conducting reviews, and we carry out performance reviews for estates and portfolios against the database.

Demand for farmland for rent remains very strong, due to competition between farmers seeking to expand and spread fixed costs.

If you are a landowner, landlord, tenant or are looking to contract or share farm land, please contact our local team to discuss the options available to you. They can advise you on the best course of action to suit your circumstances. They will also have details of land in your area that is available to rent. Their contact details are at the end of this report.

The Outlook for 2014 and 2015Should I serve a rent review notice?

Our view on the main sectors is positive but we recommend, as we have said before, careful assessment of the current rent, what level a new rent might be and your attitude to risk.

Arable 2013 has been a better autumn and input costs have eased. Although there are some challenges in terms of commodity prices, we think there is a positive outlook. Strong rents at reviews and for new tenancies are likely to continue.

Beef and sheep

After a tough start to the year, a good summer and better forage stocks have given the sector a boost. We expect UK supply of beef and sheep to remain tight, which will support prices. The upwards pressure on feed costs has eased. Key to profitability is control of fixed costs. There is a more positive outlook than there was last year and there is still scope for rent increases but pick the unit!

Dairy

There has been downward pressure on prices but this is now changing and lower feed costs and better quality forage has made the outlook more positive. We expect consolidation of the industry to continue as only the top slice of producers are making sustainable margins. The amount of capital investment needed on a unit is a key factor in determining rental levels but for good units we continue to expect strong rent settlements.

Simon Blandford Head of Farm ManagementWinchester officet 01962 857405e simon.blandford @smithsgore.co.uk

Giles WordsworthNational Head of Farm Agencyt 01865 733302e [email protected]

To discuss the sale or purchase of agricultural land, please contact:

Contacts

If you would like to discuss rent reviews or options for letting land, please contact:

ScotlandToby Metcalfe t 0131 344 0885e [email protected]

NorthPhilip Colest 01325 370511e [email protected]

East Midlands and Yorkshire & HumberDavid Goodsont 01733 559306 e [email protected]

Western England and WalesStephen Spencert 01543 251221e [email protected]

South East and East of EnglandRupert Clarkt 01798 345999e [email protected]

South WestCharles Dixont 01392 294892 e [email protected]

Smiths Gore offices

smithsgore.co.uk