agricultural and food policy information workshop food & agribusiness research i trade disputes...

TRANSCRIPT

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Trade Disputes in an Unsettled Industry:

Mexican Sugar

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Sugar cane production is concentrated in the warmer

areas of Central Mexico2,000,000 to 19,200,000 (5)1,700,000 to 2,000,000 (2)1,200,000 to 1,700,000 (5)

300,000 to 1,200,000 (3)Less than 300,000 MT (5)

Source: Rabobank from SAGARPA data

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Consumption of sugar by major use

categories:2000

Soft Drink Bottlers

26%

Households49%

Bakery Products &

Cereal17%

Chocolate & Candies

2%

Others6%

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

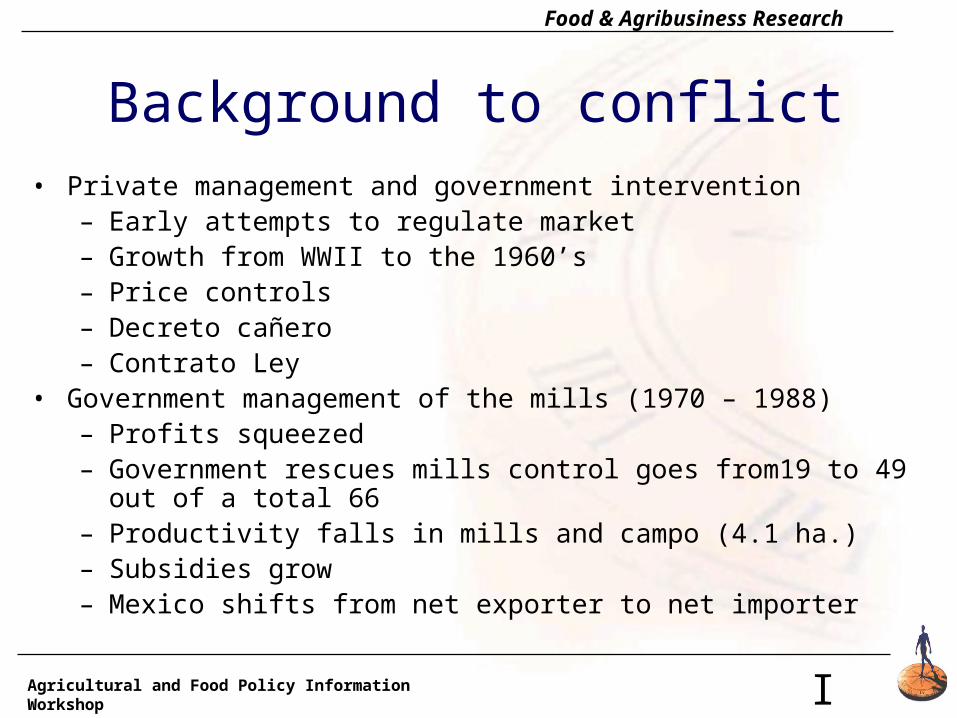

Background to conflict• Private management and government intervention

– Early attempts to regulate market– Growth from WWII to the 1960’s– Price controls– Decreto cañero– Contrato Ley

• Government management of the mills (1970 – 1988)– Profits squeezed – Government rescues mills control goes from19 to 49 out of

a total 66– Productivity falls in mills and campo (4.1 ha.)– Subsidies grow– Mexico shifts from net exporter to net importer

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

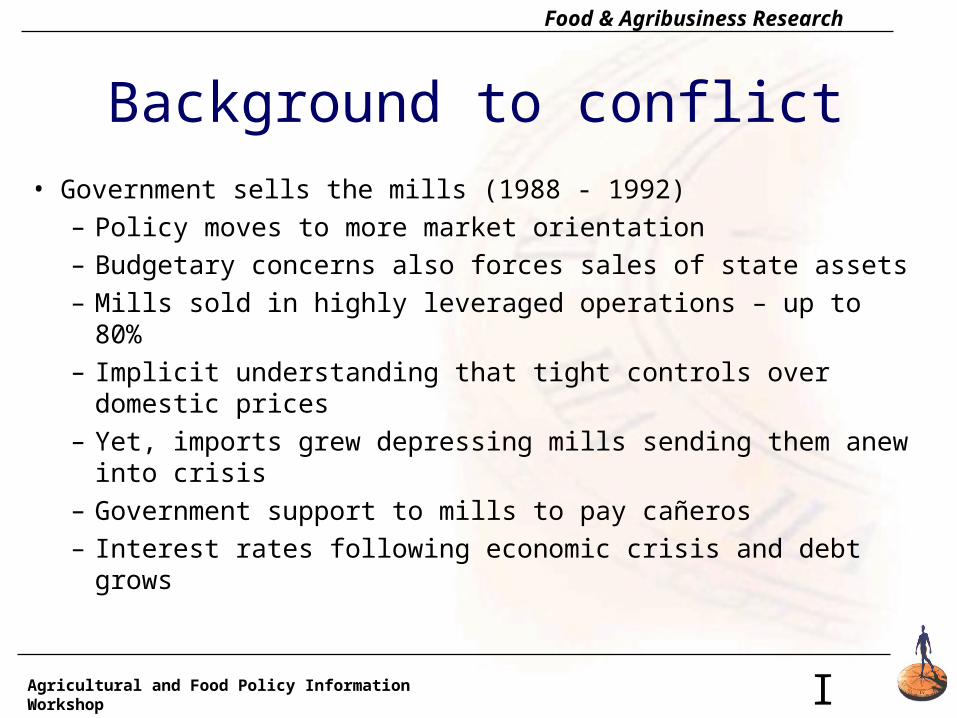

Background to conflict• Government sells the mills (1988 - 1992)

– Policy moves to more market orientation– Budgetary concerns also forces sales of state assets – Mills sold in highly leveraged operations – up to 80%– Implicit understanding that tight controls over

domestic prices– Yet, imports grew depressing mills sending them

anew into crisis– Government support to mills to pay cañeros– Interest rates following economic crisis and debt

grows

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

NAFTA• Mexico negotiates structural change• U.S. and Canada negotiate trade agreement• Mexico negotiations sugar sector• U.S. Negotiates sweetner sector• Mexico net importer of sugar• U.S.net importer of sugar• Mexico and U.S. protect domestic markets• Low level of HFCS trade

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Mexico’s foreign trade in sugar(million dollars)

0

50

100

150

200

250

300

1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001

ImportsExports

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

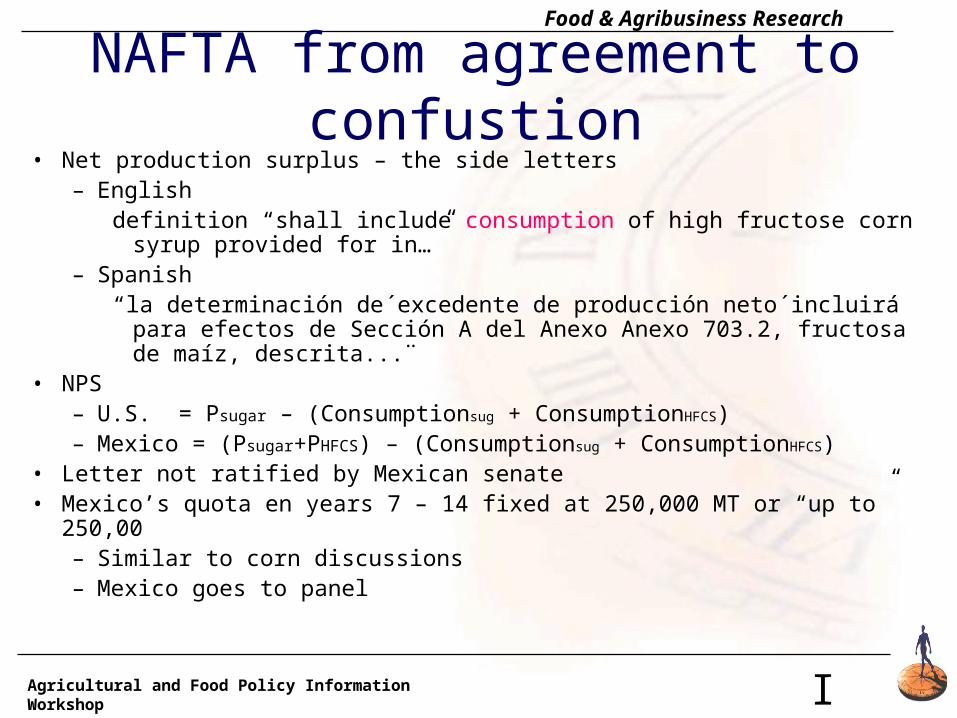

NAFTA from agreement to confustion

• Net production surplus – the side letters– English

definition “shall include consumption of high fructose corn syrup provided for in…”

– Spanish“la determinación de´excedente de producción neto´incluirá para

efectos de Sección A del Anexo Anexo 703.2, fructosa de maíz, descrita...¨

• NPS– U.S. = Psugar – (Consumptionsug + ConsumptionHFCS)– Mexico = (Psugar+PHFCS) – (Consumptionsug + ConsumptionHFCS)

• Letter not ratified by Mexican senate• Mexico’s quota en years 7 – 14 fixed at 250,000 MT or “up to” 250,00

– Similar to corn discussions– Mexico goes to panel

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

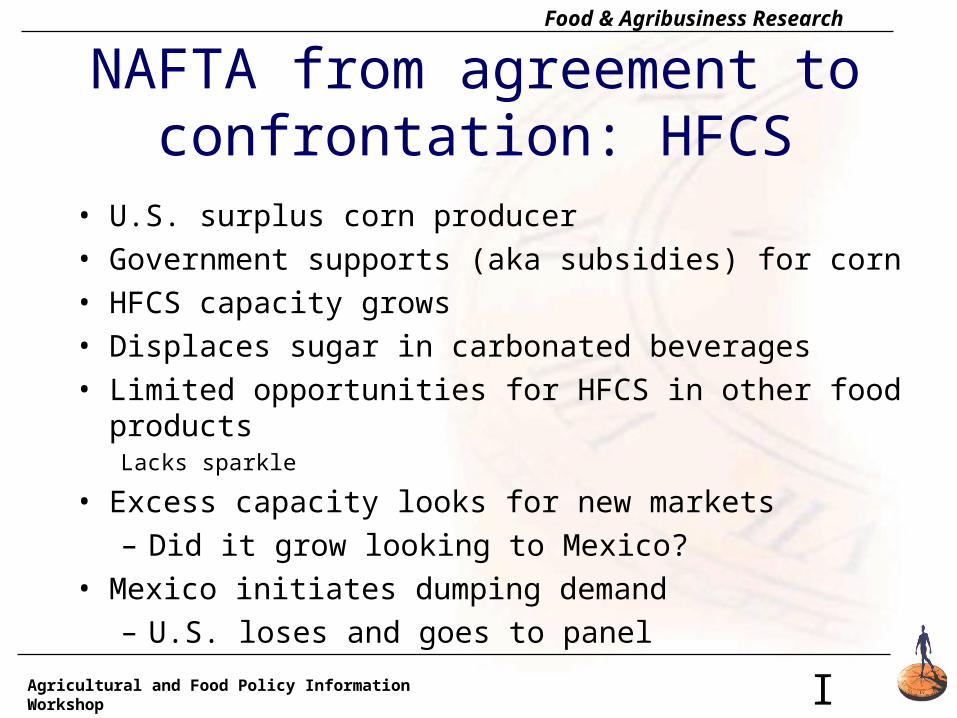

NAFTA from agreement to confrontation: HFCS

• U.S. surplus corn producer• Government supports (aka subsidies) for corn• HFCS capacity grows• Displaces sugar in carbonated beverages• Limited opportunities for HFCS in other food products

Lacks sparkle

• Excess capacity looks for new markets– Did it grow looking to Mexico?

• Mexico initiates dumping demand– U.S. loses and goes to panel

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Mexico’s imports of HFCS

0

50

100

150

200

250

300

350

1994 1995 1996 1997 1998 1999 2000 2001*

United States Other countries TOTAL1994 74,092 26 74,118 1995 57,758 1 57,759 1996 198,918 91 199,009 1997 347,799 3 347,802 1998 295,923 5 295,928 1999 344,910 1 344,911 2000 295,016 15,243 310,259

TOTAL FRUCTOSE MEXICAN IMPORTS

Imports of HFCS (55)(‘000 mt)

Source: Rabobank with data from the Secretaria de Economia

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

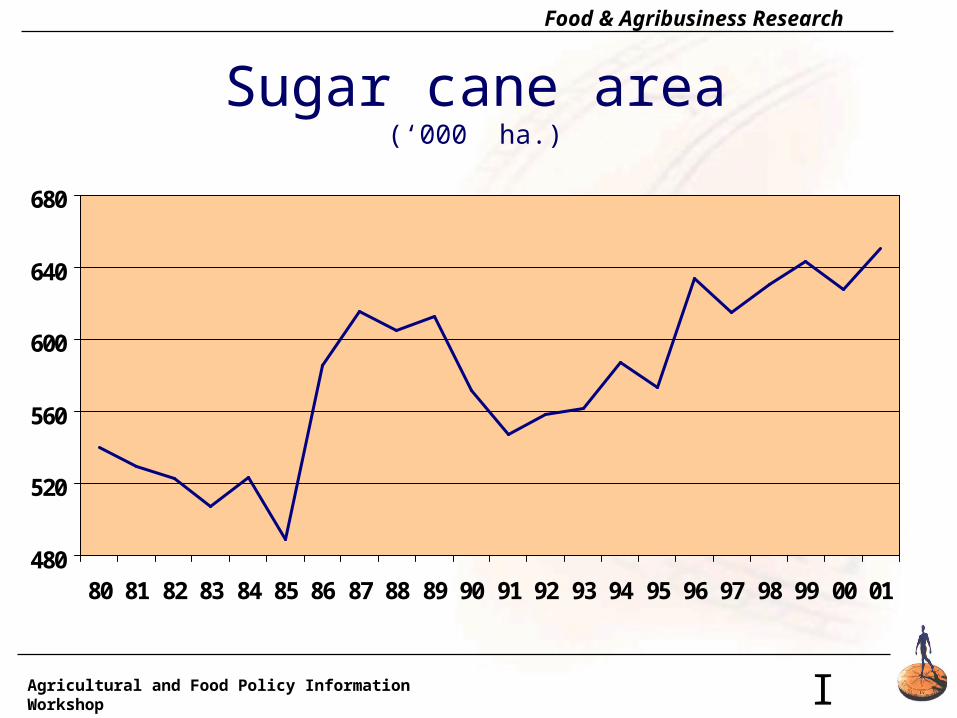

Sugar cane area(‘000 ha.)

480

520

560

600

640

680

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

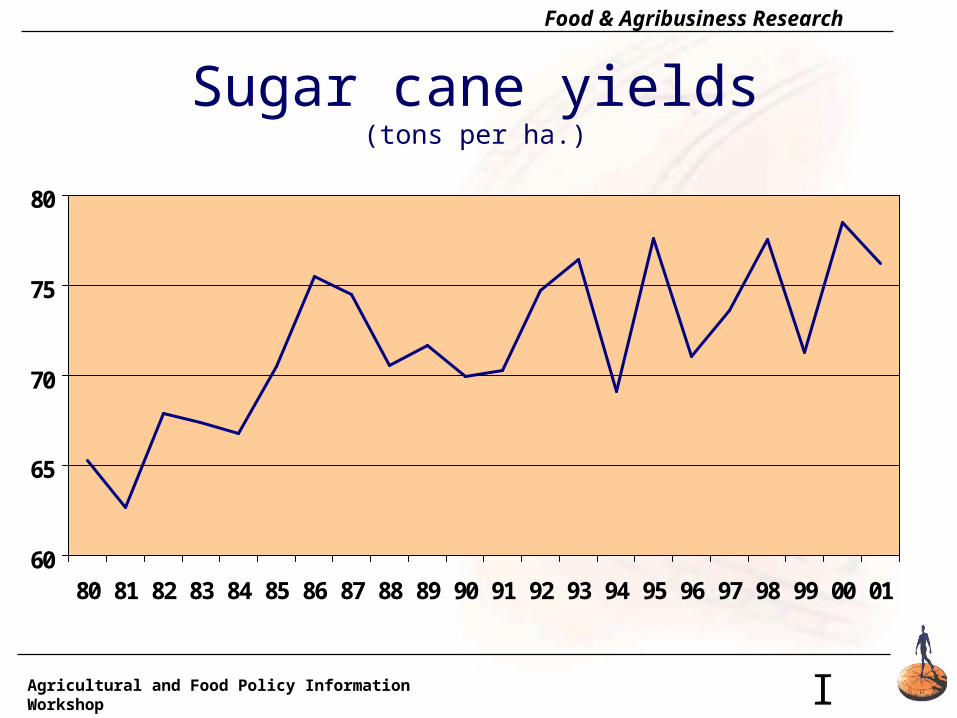

Sugar cane yields(tons per ha.)

60

65

70

75

80

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Sugar cane production(Million mt)

30

35

40

45

50

55

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Sugar production(Million mt)

2.0

2.4

2.8

3.2

3.6

4.0

4.4

4.8

5.2

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Sugar production per hectare(Million mt)

4.4

4.8

5.2

5.6

6.0

6.4

6.8

7.2

7.6

8.0

8.4

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

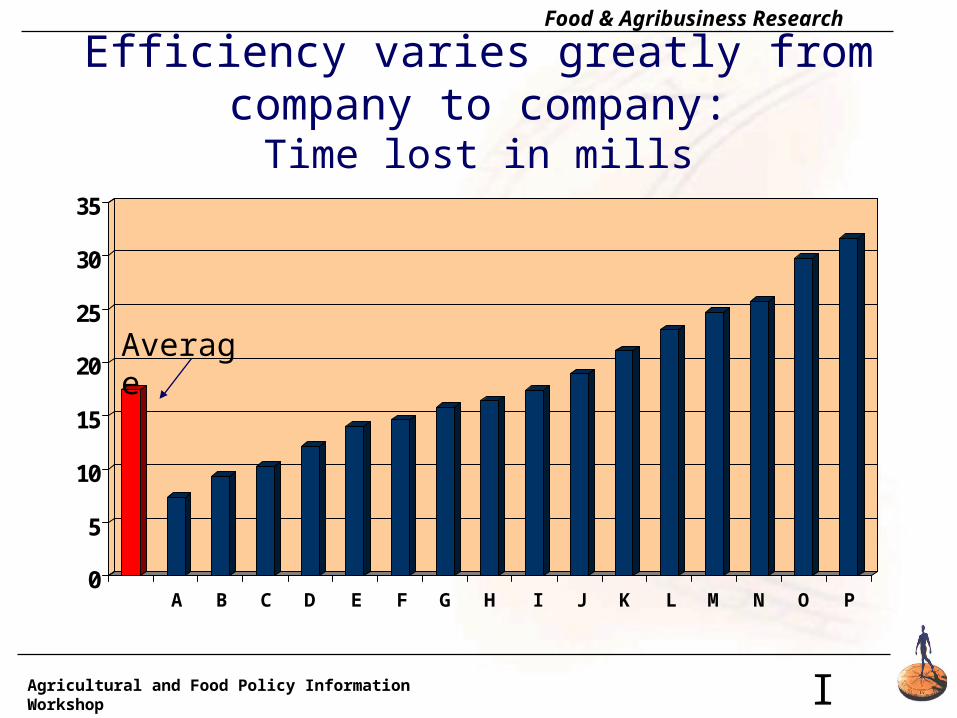

Efficiency varies greatly from company to company:

Time lost in mills

0

5

10

15

20

25

30

35

A B C D E F G H I J K L M N O P

Average

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Recent events• Consolidation of the milling sector of the industry• GAM goes into default• 2001 found the domestic market in disarray

– Low domestic prices– “Dumping of sugar on domestic market”– SAGARPA under state of siege by cane growers

and threats by mill workers• Mills of four companies expropriated• Government sets up agency to run mills and to

eventually privatize them

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

2001 Mexican sugar prices

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Seasonal nature of Mexico’s sugar harvest(mt per week)

0

50,000

100,000

150,000

200,000

250,000

2000/2001 crop

2001/2002 crop

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Recent events (cont.)• Congress enacts excise tax on HFCS used in soda pop

– Congress flexing muscle– Frustrated with slow pace is resolving dispute– Upset with SE decision to negotiate– Cañeros strength in Congress

• National Sugar Policy (Feb. 2002)– Bring order to the market– Mixed capital export company– Inventory financing – Modernize market

• Contrato Ley• Decreto cañero

• Temporary suspension of HFCS tax– Steel for HFCS?– Until Sep. 30– Criticized by industry and Congress

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

The future: 2and tier tariffs

• Allows for free imports of sugar paying declining tariffs

• U.S. WTO sugar quota– Trade policy, foreign policy or subsidies for

holders of quotas• Imports of sugar paying tariffs will displace quota

sugar• USDA baseline projection document raises question

of dumping of Mexican sugar

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

Over quota tariffs for imports of Mexican sugar into the U.S.

(cents per pound)

0

2

4

6

8

10

12

14

96 97 98 99 00 01 02 03 04 05 08

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

NAFTA high-tier Mexican sugar exports to the U.S.

0

250

500

750

1,000

1,250

1,500

02 03 04 05 06 07 08 09 10 11 12Source: Rabobank from USDA baseline projections

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

NAFTA high-tier Mexican sugar exports to the U.S.

0

250

500

750

1,000

1,250

1,500

02 03 04 05 06 07 08 09 10 11 12Source: Rabobank from USDA baseline projections

U.S. WTO import commitment

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

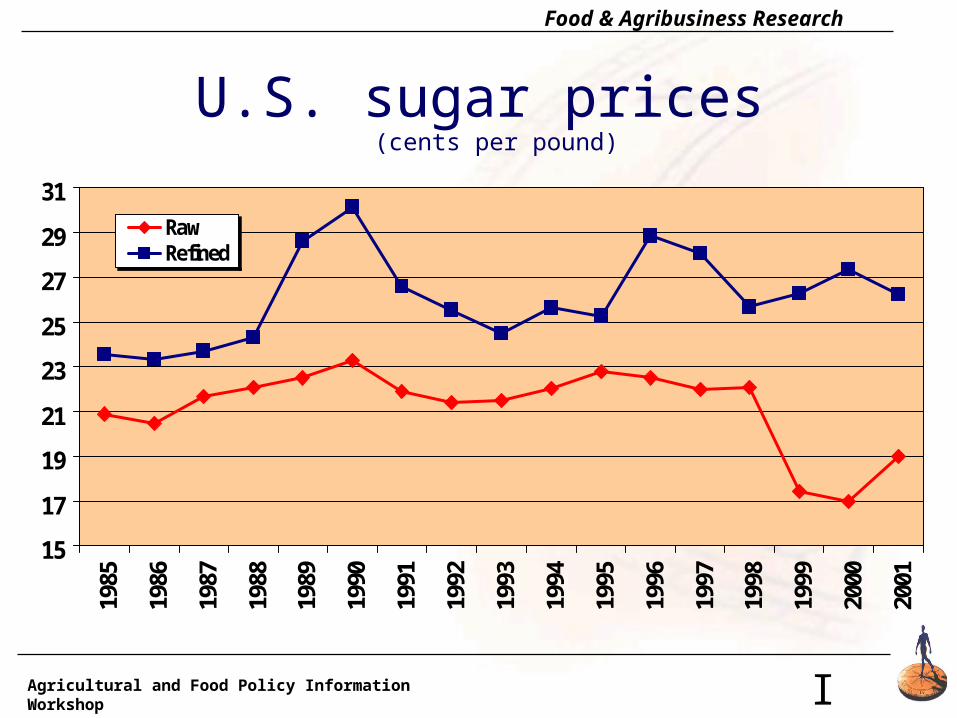

U.S. sugar prices (cents per pound)

15

17

19

21

23

25

27

29

31

1985

1986

1987

1988

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

Raw Refined

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

The future: 3 scenarios

• U.S.opens market to sugar imports– As Mexican imports grows U.S. recognizes that they can’t compete– Abandons all supports rather than support Mexican industry– 3rd party countries displace Mexican producers

• Creation of NAFTA sugar market– Mexico sugar displaces quota sugar– U.S. holders, and others, invest in Mexican mills– Minimal domestic pain– HCFS south and sugar north – happy corn growers and share

holders

• U.S. refuses to open border

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

The future: Spoilers

• Cuba– Life after Castro

• FTAA– Brazil takes over the market (4 cents lbs. break even)

Agricultural and Food Policy Information Workshop

Food & Agribusiness Research

I

U.S. and Mexican refined sugar prices

(cents per pound)

17

19

21

23

25

27

29

31

1995 1996 1997 1998 1999 2000 2001

MX RefinedUS Refined