agriculture - india brand equity foundation, ibef, business

TRANSCRIPT

AGRICULTURENovember 2010

2

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

AGRICULTURE November 2010

3

Advantage India

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 3 December 2010; ―Agriculture and Food Management,‖ Economic Survey 2009-10,

Government of India: Union Budget and Economic Survey website, http://indiabudget.nic.in/es2009-10/esmain.htm, accessed 08 March 2010;

―India’s Macroeconomic Indicators,‖ ―Third Advance Estimates of Crop Production Released,‖ PIB press release website,

http://pib.nic.in/release/release.asp?relid=61781, accessed 14 July 2010.

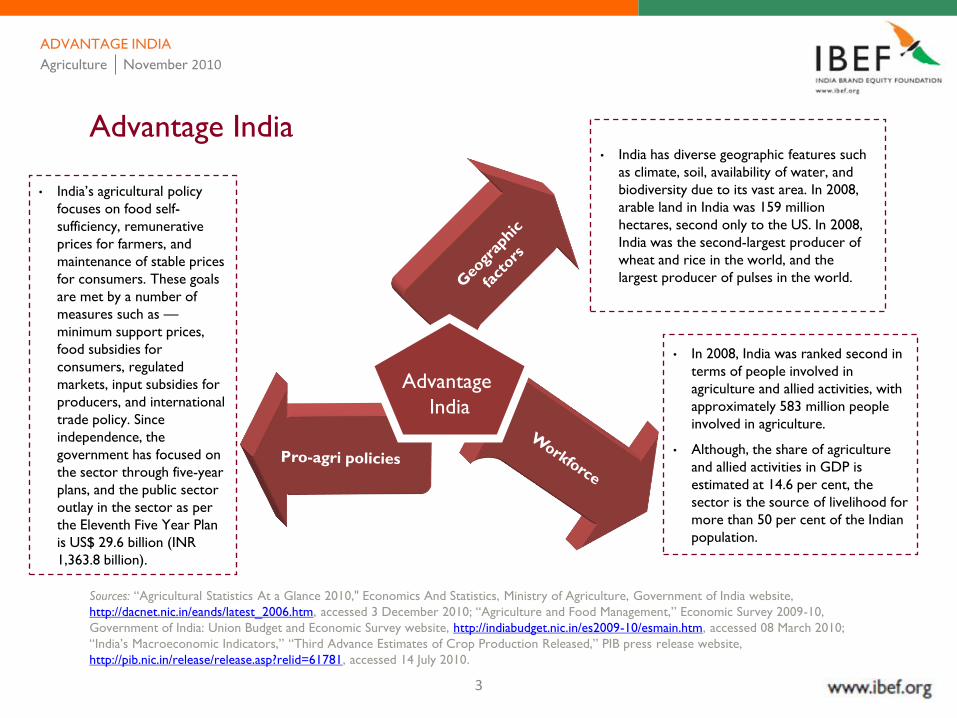

• India’s agricultural policy

focuses on food self-

sufficiency, remunerative

prices for farmers, and

maintenance of stable prices

for consumers. These goals

are met by a number of

measures such as —

minimum support prices,

food subsidies for

consumers, regulated

markets, input subsidies for

producers, and international

trade policy. Since

independence, the

government has focused on

the sector through five-year

plans, and the public sector

outlay in the sector as per

the Eleventh Five Year Plan

is US$ 29.6 billion (INR

1,363.8 billion).

• In 2008, India was ranked second in

terms of people involved in

agriculture and allied activities, with

approximately 583 million people

involved in agriculture.

• Although, the share of agriculture

and allied activities in GDP is

estimated at 14.6 per cent, the

sector is the source of livelihood for

more than 50 per cent of the Indian

population.

• India has diverse geographic features such

as climate, soil, availability of water, and

biodiversity due to its vast area. In 2008,

arable land in India was 159 million

hectares, second only to the US. In 2008,

India was the second-largest producer of

wheat and rice in the world, and the

largest producer of pulses in the world.

Advantage

India

Agriculture November 2010

ADVANTAGE INDIA

4

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

AGRICULTURE November 2010

5

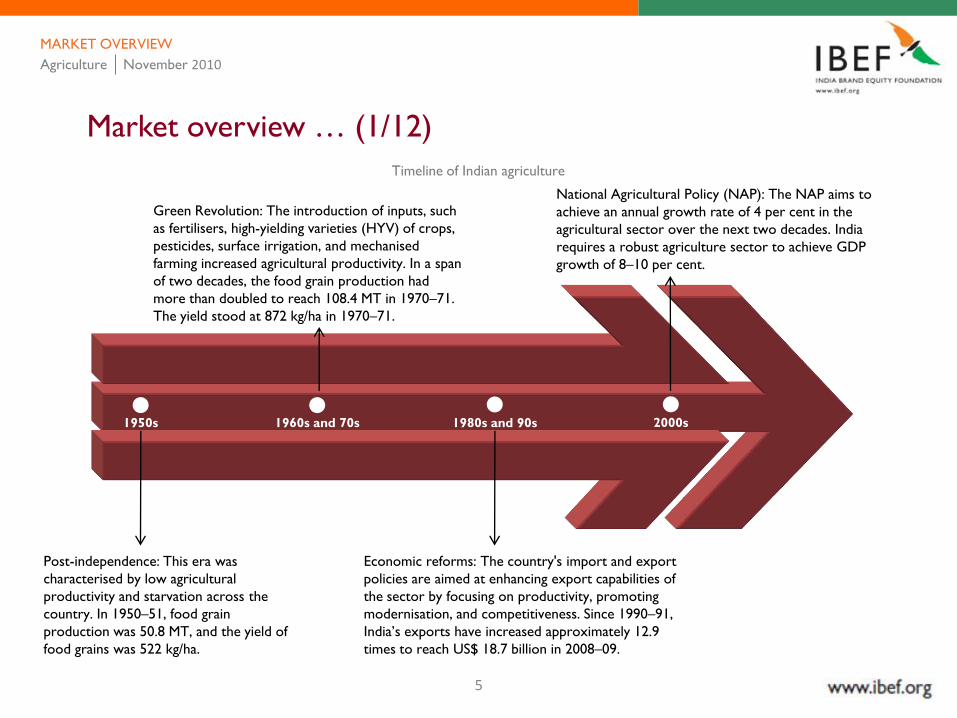

1950s 1960s and 70s

Post-independence: This era was

characterised by low agricultural

productivity and starvation across the

country. In 1950–51, food grain

production was 50.8 MT, and the yield of

food grains was 522 kg/ha.

Green Revolution: The introduction of inputs, such

as fertilisers, high-yielding varieties (HYV) of crops,

pesticides, surface irrigation, and mechanised

farming increased agricultural productivity. In a span

of two decades, the food grain production had

more than doubled to reach 108.4 MT in 1970–71.

The yield stood at 872 kg/ha in 1970–71.

Economic reforms: The country's import and export

policies are aimed at enhancing export capabilities of

the sector by focusing on productivity, promoting

modernisation, and competitiveness. Since 1990–91,

India’s exports have increased approximately 12.9

times to reach US$ 18.7 billion in 2008–09.

1980s and 90s 2000s

National Agricultural Policy (NAP): The NAP aims to

achieve an annual growth rate of 4 per cent in the

agricultural sector over the next two decades. India

requires a robust agriculture sector to achieve GDP

growth of 8–10 per cent.

MARKET OVERVIEW

Market overview … (1/12)

Timeline of Indian agriculture

Agriculture November 2010

6

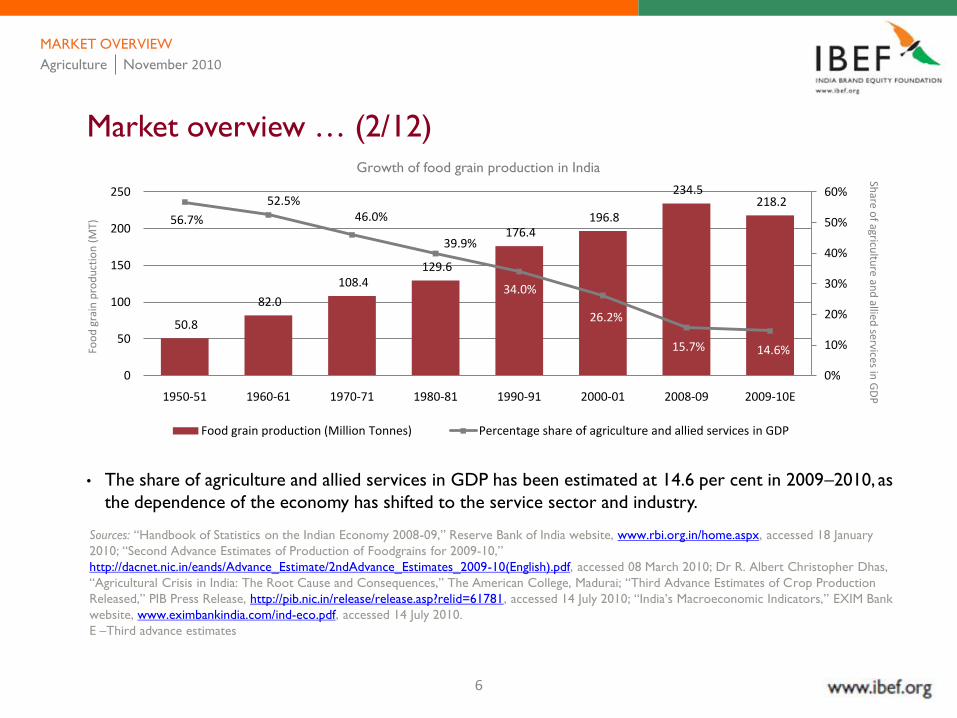

• The share of agriculture and allied services in GDP has been estimated at 14.6 per cent in 2009–2010, as

the dependence of the economy has shifted to the service sector and industry.

Market overview … (2/12)

MARKET OVERVIEW

Growth of food grain production in India

Sources: ―Handbook of Statistics on the Indian Economy 2008-09,‖ Reserve Bank of India website, www.rbi.org.in/home.aspx, accessed 18 January

2010; ―Second Advance Estimates of Production of Foodgrains for 2009-10,‖

http://dacnet.nic.in/eands/Advance_Estimate/2ndAdvance_Estimates_2009-10(English).pdf, accessed 08 March 2010; Dr R. Albert Christopher Dhas,

―Agricultural Crisis in India: The Root Cause and Consequences,‖ The American College, Madurai; ―Third Advance Estimates of Crop Production

Released,‖ PIB Press Release, http://pib.nic.in/release/release.asp?relid=61781, accessed 14 July 2010; ―India’s Macroeconomic Indicators,‖ EXIM Bank

website, www.eximbankindia.com/ind-eco.pdf, accessed 14 July 2010.

E –Third advance estimates

50.8

82.0

108.4 129.6

176.4 196.8

234.5 218.2

56.7%

52.5%46.0%

39.9%

34.0%

26.2%

15.7% 14.6%

0%

10%

20%

30%

40%

50%

60%

0

50

100

150

200

250

1950-51 1960-61 1970-71 1980-81 1990-91 2000-01 2008-09 2009-10E

Food grain production (Million Tonnes) Percentage share of agriculture and allied services in GDP

Foo

d g

rain

pro

du

ctio

n (

MT)

Share o

f agricultu

re and

allied services in

GD

P

Agriculture November 2010

7

• Over the 50-year period, i.e. , from 1950–51 to 2000–01, food grain production in India has increased at

a compound annual growth rate (CAGR) of approximately 2.7 per cent, to reach 196.8 million tonnes

(MT) in 2000–01. The increase in food grain production is largely attributed to the Green Revolution,

which took place in the 1960s and 1970s. Agri-inputs, such as fertilisers, high-yielding varieties (HYV) of

crops, pesticides, surface irrigation, and mechanised farming were primarily responsible for the increase

in agricultural productivity.

Market overview … (3/12)

Sources: ―Handbook of Statistics on the Indian Economy 2008-09,‖ Reserve Bank of India website, www.rbi.org.in/home.aspx, accessed 18

January 2010; ―Second Advance Estimates of Production of Foodgrains for 2009-10,‖

http://dacnet.nic.in/eands/Advance_Estimate/2ndAdvance_Estimates_2009-10(English).pdf, accessed 08 March 2010; Dr R. Albert Christopher

Dhas, ―Agricultural Crisis in India: The Root Cause and Consequences,‖ The American College, Madurai; ―Third Advance Estimates of Crop

Production Released,‖ PIB Press Release, http://pib.nic.in/release/release.asp?relid=61781, accessed 14 July 2010; ―India’s Macroeconomic

Indicators,‖ EXIM Bank website, www.eximbankindia.com/ind-eco.pdf, accessed 14 July 2010.

E –Third advance estimates

MARKET OVERVIEW

Agriculture November 2010

8

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Second Advance Estimates of Production of Foodgrains for 2009-10,‖

http://dacnet.nic.in/eands/Advance_Estimate/2ndAdvance_Estimates_2009-10(English).pdf, accessed 08 March 2010.

*Fourth Advance Estimates as released on 19 July 2010

Kharif and Rabi seasons

India has two crop seasons, Kharif and Rabi, based on the dependence of crop productivity on the monsoons. The Kharif season is during the summer and monsoon months, lasting from April to September, and rice is the main crop grown during the season. The Rabi season is during the winter months of October to March, and wheat is the main crop of this sesason.

Market overview … (4/12)

India — Kharif and Rabi (production in million tonnes)

51.9% 52.7% 49.9% 54.9% 52.1% 52.7% 50.9% 52.4% 50.4% 46.0%

48.1% 47.3% 50.1% 45.1% 47.9% 47.3% 49.1% 47.6% 49.6% 54.0%

2000-01 2001-02 2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09 2009-10*

Kharif Rabi

100%= 196.8 212.9 174.8 213.2 198.4 208.6 217.3 230.8 234.5 218.2

MARKET OVERVIEW

Agriculture November 2010

9

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Second Advance Estimates of Production of Foodgrains for 2009-

10,‖ http://dacnet.nic.in/eands/Advance_Estimate/2ndAdvance_Estimates_2009-10(English).pdf, accessed 08 March 2010.

*Fourth Advance Estimates as released on 19 July 2010

• According to estimates by the Department of Agriculture and Cooperation, production of food grains

in 2009–2010 is estimated to be 218.2 million tonnes, with the Rabi crops accounting for 117.83

million tonnes and Kharif crops accounting for 100.37 million tonnes. According to first advance

estimates by the Department of Agriculture and Cooperation, production of food grains in 2010–11 is

estimated to be 114.63 million tonnes.

Market overview … (5/12)

MARKET OVERVIEW

Agriculture November 2010

1010

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Second Advance Estimates of Production of Foodgrains for 2009-10,‖

http://dacnet.nic.in/eands/Advance_Estimate/2ndAdvance_Estimates_2009-10(English).pdf, accessed 08 March 2010; ―Handbook of Statistics on

the Indian Economy 2008-09,‖ Reserve Bank of India website, www.rbi.org.in, accessed 18 January 2010.

*Fourth Advance Estimates as released on 19 July 2010; Note: For cotton production is in million bales of 170 kg each

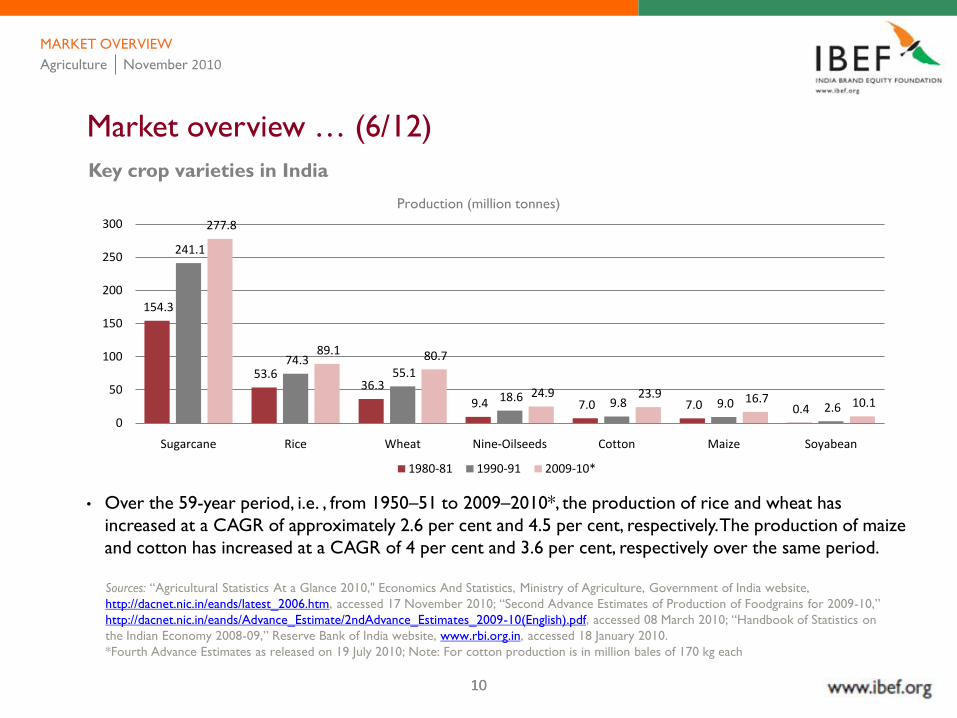

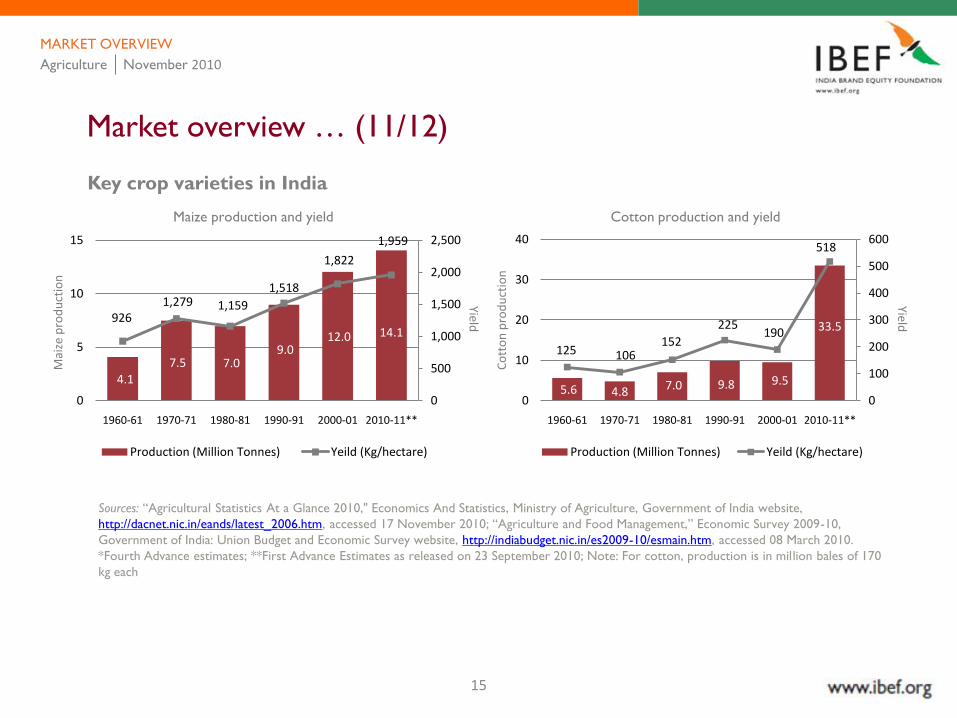

• Over the 59-year period, i.e. , from 1950–51 to 2009–2010*, the production of rice and wheat has

increased at a CAGR of approximately 2.6 per cent and 4.5 per cent, respectively. The production of maize

and cotton has increased at a CAGR of 4 per cent and 3.6 per cent, respectively over the same period.

Market overview … (6/12)

Key crop varieties in India

Production (million tonnes)

154.3

53.6 36.3

9.4 7.0 7.0 0.4

241.1

74.3 55.1

18.6 9.8 9.0 2.6

277.8

89.1 80.7

24.9 23.9 16.7 10.1

0

50

100

150

200

250

300

Sugarcane Rice Wheat Nine-Oilseeds Cotton Maize Soyabean

1980-81 1990-91 2009-10*

MARKET OVERVIEW

Agriculture November 2010

1111

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Second Advance Estimates of Production of Foodgrains for 2009-10,‖

http://dacnet.nic.in/eands/Advance_Estimate/2ndAdvance_Estimates_2009-10(English).pdf, accessed 08 March 2010; ―Handbook of Statistics on

the Indian Economy 2008-09,‖ Reserve Bank of India website, www.rbi.org.in, accessed 18 January 2010.

*Fourth Advance Estimates as released on 19 July 2010; ** First Advance Estimates as released on 23.09.2010.

Note: For cotton production is in million bales of 170 kg each

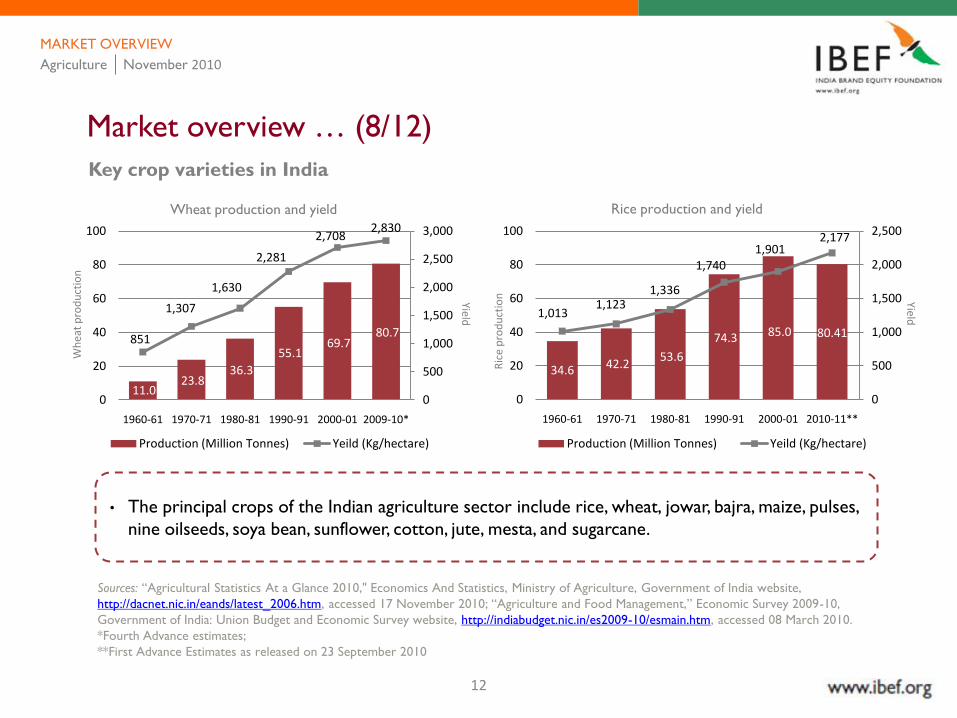

• The yield of crops has witnessed an increase since the Green Revolution. Between 1950–51 and 2009–

2010*, the yield of rice and wheat has increased by 3.3 and 4.4 times, to reach 2,130 kg/ha and 2,830

kg/ha, respectively. The yield of sugarcane has doubled since 1950–51 to reach around 66,922 kg/ha in

2010–11**.

Market overview … (7/12)

Key crop varieties in India

MARKET OVERVIEW

Agriculture November 2010

12

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Agriculture and Food Management,‖ Economic Survey 2009-10,

Government of India: Union Budget and Economic Survey website, http://indiabudget.nic.in/es2009-10/esmain.htm, accessed 08 March 2010.

*Fourth Advance estimates;

**First Advance Estimates as released on 23 September 2010

• The principal crops of the Indian agriculture sector include rice, wheat, jowar, bajra, maize, pulses,

nine oilseeds, soya bean, sunflower, cotton, jute, mesta, and sugarcane.

Market overview … (8/12)

Key crop varieties in India

Wheat production and yield Rice production and yield

11.0 23.8

36.3

55.1 69.7

80.7 851

1,307

1,630

2,281

2,7082,830

0

500

1,000

1,500

2,000

2,500

3,000

0

20

40

60

80

100

1960-61 1970-71 1980-81 1990-91 2000-01 2009-10*

Production (Million Tonnes) Yeild (Kg/hectare)

34.6 42.2 53.6

74.3 85.0 80.41

1,0131,123

1,336

1,7401,901

2,177

0

500

1,000

1,500

2,000

2,500

0

20

40

60

80

100

1960-61 1970-71 1980-81 1990-91 2000-01 2010-11**

Production (Million Tonnes) Yeild (Kg/hectare)

MARKET OVERVIEW

Wh

eat

pro

du

ctio

n

YieldR

ice

pro

du

ctio

n Yield

Agriculture November 2010

13

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Agriculture and Food Management,‖ Economic Survey 2009-10,

Government of India: Union Budget and Economic Survey website, http://indiabudget.nic.in/es2009-10/esmain.htm, accessed 08 March 2010.

*Fourth Advance estimates

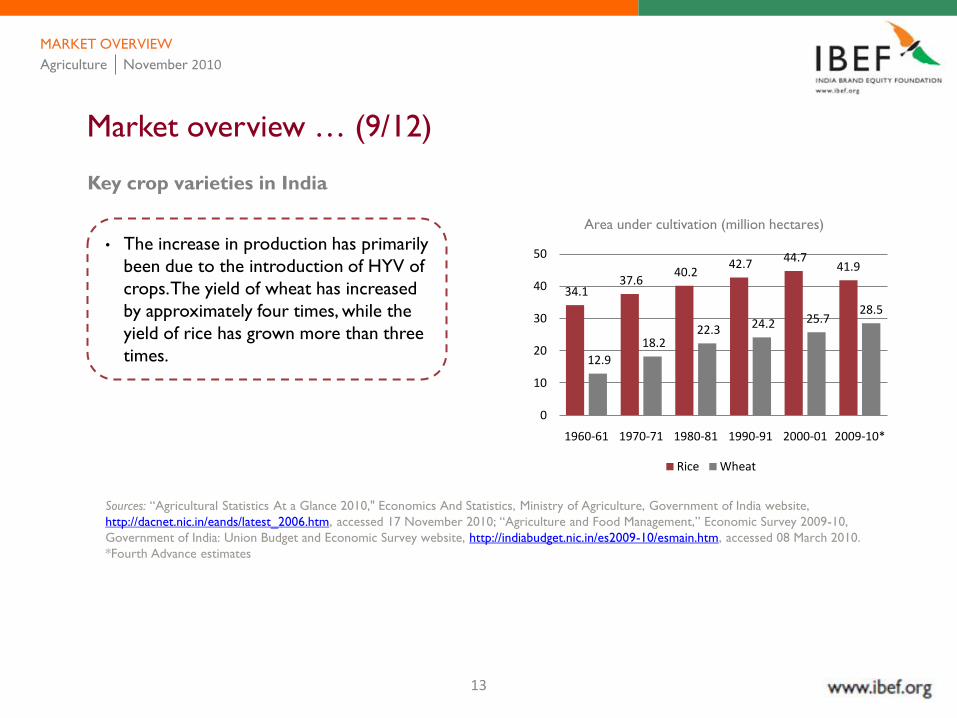

• The increase in production has primarily

been due to the introduction of HYV of

crops. The yield of wheat has increased

by approximately four times, while the

yield of rice has grown more than three

times.

Market overview … (9/12)

Area under cultivation (million hectares)

Key crop varieties in India

34.1 37.6

40.2 42.7 44.7

41.9

12.9

18.2 22.3 24.2 25.7

28.5

0

10

20

30

40

50

1960-61 1970-71 1980-81 1990-91 2000-01 2009-10*

Rice Wheat

MARKET OVERVIEW

Agriculture November 2010

14

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Agriculture and Food Management,‖ Economic Survey 2009-10,

Government of India: Union Budget and Economic Survey website, http://indiabudget.nic.in/es2009-10/esmain.htm, accessed 08 March 2010.

*Fourth Advance estimates;

**First Advance Estimates as released on 23 September 2010

Market overview … (10/12)

Key crop varieties in India

Nine oilseeds production and yieldSugarcane production and yield

110.0 126.4154.3

241.1296.0 324.9

45,549

48,322

57,844 65,395

68,577 66,922

0

20,000

40,000

60,000

80,000

0

100

200

300

400

1960-61 1970-71 1980-81 1990-91 2000-01 2010-11**

Production (Million Tonnes) Yeild (Kg/hectare)

7.0 9.6 9.4

18.6 18.4 24.9

507 579

532

771 810

955

0

200

400

600

800

1,000

1,200

0

5

10

15

20

25

30

1960-61 1970-71 1980-81 1990-91 2000-01 2009-10*

Production (Million Tonnes) Yeild (Kg/hectare)

MARKET OVERVIEWSu

garc

ane

pro

du

ctio

n

Yield

Nin

e-O

ilsee

ds

YieldAgriculture November 2010

15

Sources: ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November 2010; ―Agriculture and Food Management,‖ Economic Survey 2009-10,

Government of India: Union Budget and Economic Survey website, http://indiabudget.nic.in/es2009-10/esmain.htm, accessed 08 March 2010.

*Fourth Advance estimates; **First Advance Estimates as released on 23 September 2010; Note: For cotton, production is in million bales of 170

kg each

Market overview … (11/12)

Key crop varieties in India

Maize production and yield Cotton production and yield

4.1 7.5 7.0

9.0 12.0 14.1

926 1,279 1,159

1,518

1,822

1,959

0

500

1,000

1,500

2,000

2,500

0

5

10

15

1960-61 1970-71 1980-81 1990-91 2000-01 2010-11**

Production (Million Tonnes) Yeild (Kg/hectare)

5.6 4.8 7.0 9.8 9.5

33.5

125 106 152

225 190

518

0

100

200

300

400

500

600

0

10

20

30

40

1960-61 1970-71 1980-81 1990-91 2000-01 2010-11**

Production (Million Tonnes) Yeild (Kg/hectare)

MARKET OVERVIEWM

aize

pro

du

ctio

n

Yield

Co

tto

n p

rod

uct

ion

YieldAgriculture November 2010

16

Source: ―Handbook of Statistics on the Indian Economy 2008-09,‖ Reserve Bank of India website, www.rbi.org.in/home.aspx, accessed 18 January

2010; ―Agricultural Statistics At a Glance 2010," Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 3 December 2010.

Note: Total production does not include Union Territories

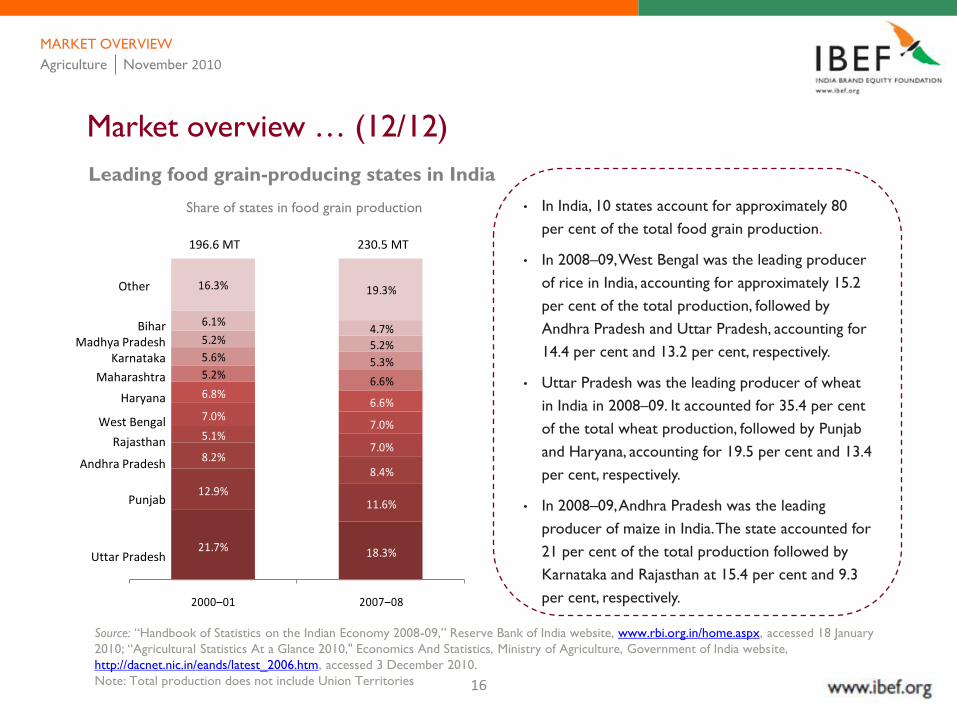

• In India, 10 states account for approximately 80

per cent of the total food grain production.

• In 2008–09, West Bengal was the leading producer

of rice in India, accounting for approximately 15.2

per cent of the total production, followed by

Andhra Pradesh and Uttar Pradesh, accounting for

14.4 per cent and 13.2 per cent, respectively.

• Uttar Pradesh was the leading producer of wheat

in India in 2008–09. It accounted for 35.4 per cent

of the total wheat production, followed by Punjab

and Haryana, accounting for 19.5 per cent and 13.4

per cent, respectively.

• In 2008–09, Andhra Pradesh was the leading

producer of maize in India. The state accounted for

21 per cent of the total production followed by

Karnataka and Rajasthan at 15.4 per cent and 9.3

per cent, respectively.

Market overview … (12/12)

Leading food grain-producing states in India

MARKET OVERVIEW

21.7% 18.3%

12.9%11.6%

8.2%8.4%

5.1%7.0%

7.0%7.0%

6.8%6.6%

5.2%6.6%

5.6% 5.3%

5.2% 5.2%

6.1%4.7%

16.3% 19.3%

2000–01 2007–08

196.6 MT 230.5 MT

Uttar Pradesh

Punjab

Andhra Pradesh

Rajasthan

West Bengal

Haryana

Maharashtra

KarnatakaMadhya Pradesh

Bihar

Other

Share of states in food grain production

Agriculture November 2010

17

Source: ―Agricultural Statistics At a Glance 2010," Economics

And Statistics, Ministry of Agriculture, Government of India

website, http://dacnet.nic.in/eands/latest_2006.htm, accessed

17 November 2010.

P – Provisional

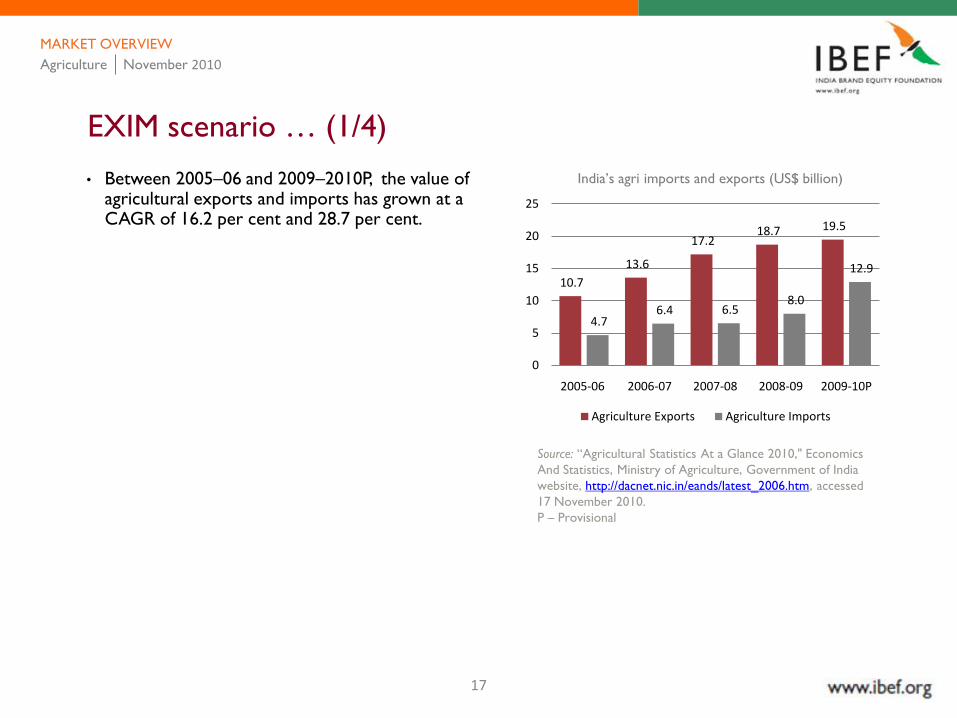

EXIM scenario … (1/4)

• Between 2005–06 and 2009–2010P, the value of agricultural exports and imports has grown at a CAGR of 16.2 per cent and 28.7 per cent.

India’s agri imports and exports (US$ billion)

10.7

13.6

17.2 18.7 19.5

4.7 6.4 6.5

8.0

12.9

0

5

10

15

20

25

2005-06 2006-07 2007-08 2008-09 2009-10P

Agriculture Exports Agriculture Imports

MARKET OVERVIEW

Agriculture November 2010

18

Source: ―Agricultural Statistics At a Glance 2010," Economics And

Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17

November 2010.

P – Provisional

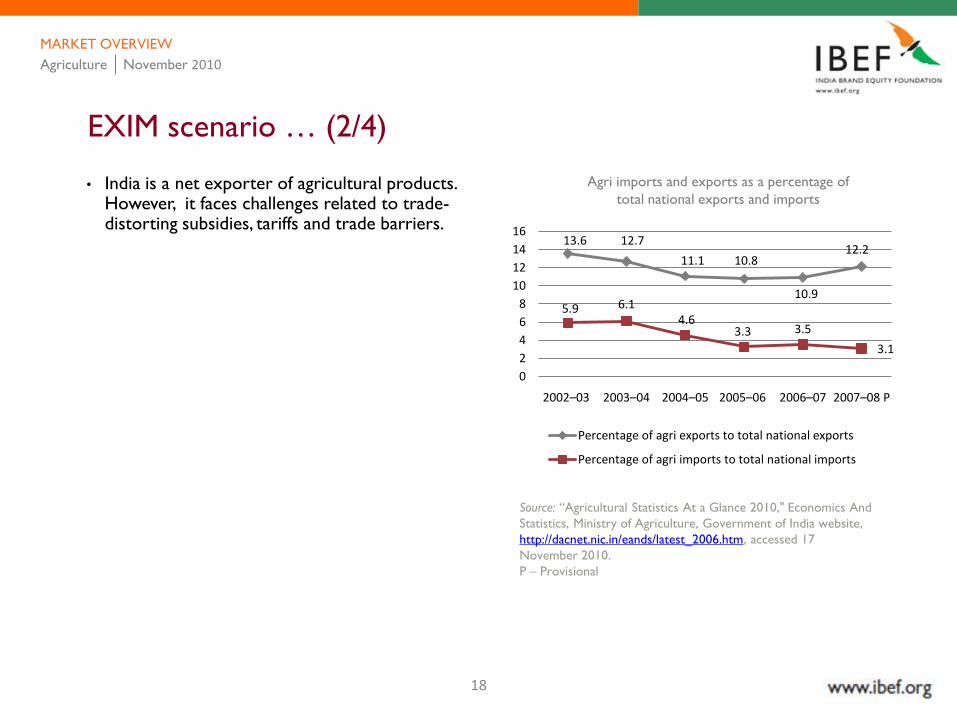

EXIM scenario … (2/4)

• India is a net exporter of agricultural products. However, it faces challenges related to trade-distorting subsidies, tariffs and trade barriers.

Agri imports and exports as a percentage of

total national exports and imports

MARKET OVERVIEW

Agriculture November 2010

13.6 12.7

11.1 10.8

10.9

12.2

5.9 6.1 4.6

3.3 3.5

3.1

0

2

4

6

8

10

12

14

16

2002–03 2003–04 2004–05 2005–06 2006–07 2007–08 P

Percentage of agri exports to total national exports

Percentage of agri imports to total national imports

19

Source: ―Agricultural Statistics At a Glance 2010," Economics And

Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November

2010.

*Provisional

EXIM scenario … (3/4)

• In 2008–09, India’s export of cereals amounted to US$ 3.29 million, with Saudi Arabia, the UAE and Malaysia being the leading export destinations. Rice (basmati and non-basmati) and other cereals were the leading cereals exported from the country.

100%= US$ 19.5 billion

Key agri products exported by India, 2009–2010*

(US$ billion)

8.8%

12.1%

11.0%

6.9%

6.3%7.0%

0.1%

47.8%

Oil Meals

Rice Basmati

Marine Products

Spices

Paper/Wood products

Meat & Preparations

Sugar

Other

MARKET OVERVIEW

Agriculture November 2010

20

Source: ―Agricultural Statistics At a Glance 2010," Economics And

Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/latest_2006.htm, accessed 17 November

2010.

*Provisional

EXIM scenario … (4/4)

• Vegetable oil is a leading agricultural product imported by India from developing countries such as Malaysia and Indonesia. 100%= US$ 12.9 billion

Key agri products imported by India, 2009–2010*

(US$ billion)

44.6%

12.6%

16.3%

0.4%

26.1%

Vegetable Oils Fixed (Edible)

Wood & Wood Products

Pulses

Wheat

Other

MARKET OVERVIEW

Agriculture November 2010

21

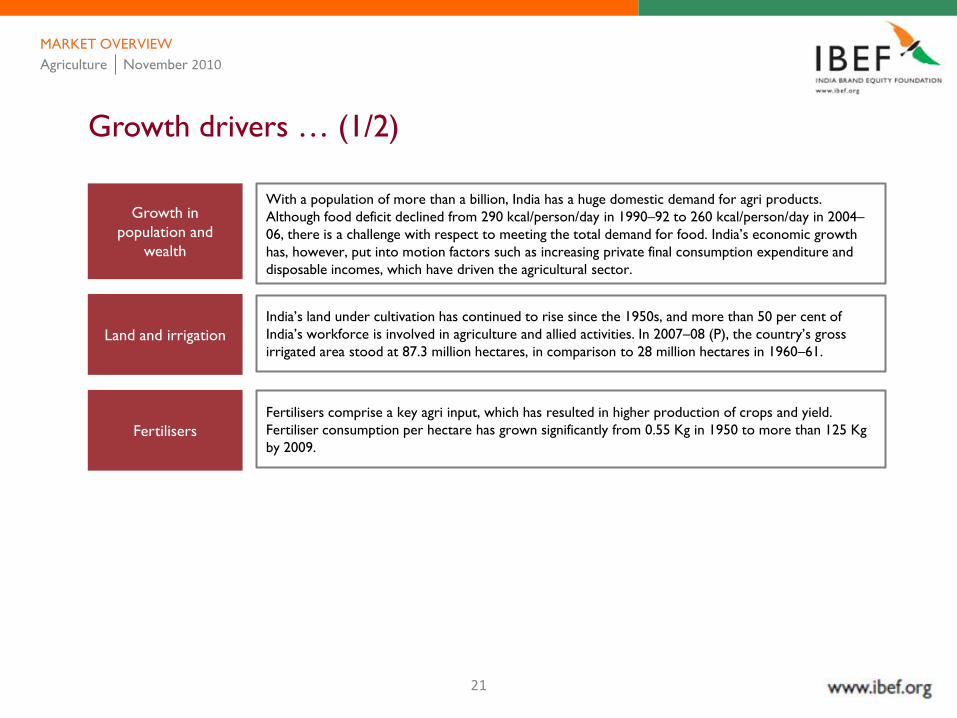

Growth drivers … (1/2)

Growth in

population and

wealth

Land and irrigation

Fertilisers

With a population of more than a billion, India has a huge domestic demand for agri products.

Although food deficit declined from 290 kcal/person/day in 1990–92 to 260 kcal/person/day in 2004–

06, there is a challenge with respect to meeting the total demand for food. India’s economic growth

has, however, put into motion factors such as increasing private final consumption expenditure and

disposable incomes, which have driven the agricultural sector.

India’s land under cultivation has continued to rise since the 1950s, and more than 50 per cent of

India’s workforce is involved in agriculture and allied activities. In 2007–08 (P), the country’s gross

irrigated area stood at 87.3 million hectares, in comparison to 28 million hectares in 1960–61.

Fertilisers comprise a key agri input, which has resulted in higher production of crops and yield.

Fertiliser consumption per hectare has grown significantly from 0.55 Kg in 1950 to more than 125 Kg

by 2009.

MARKET OVERVIEW

Agriculture November 2010

22

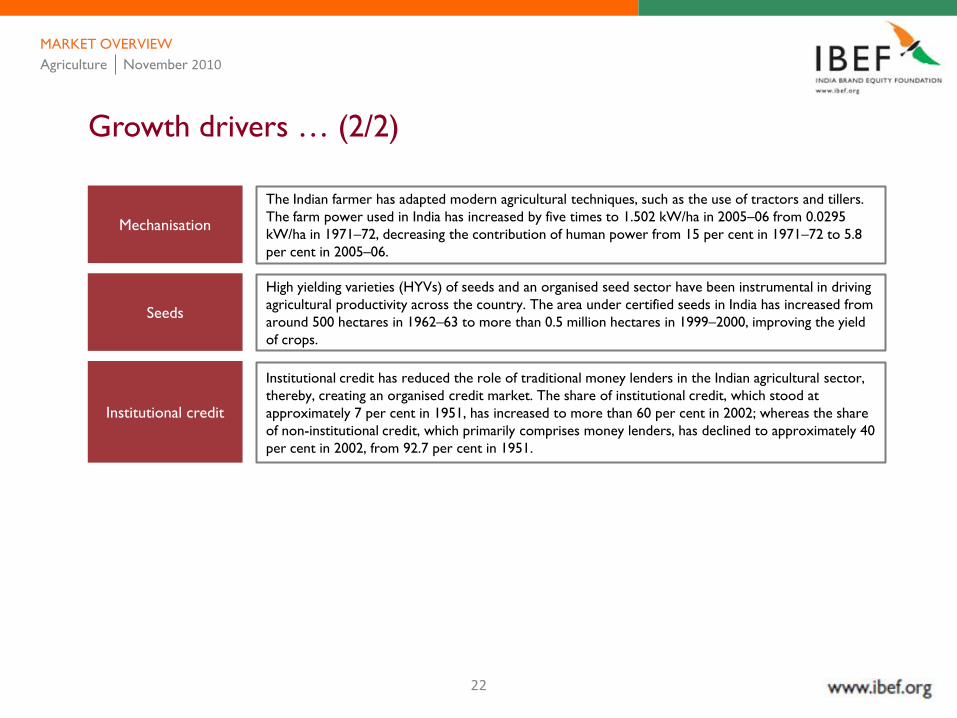

Growth drivers … (2/2)

Mechanisation

Institutional credit

Seeds

The Indian farmer has adapted modern agricultural techniques, such as the use of tractors and tillers.

The farm power used in India has increased by five times to 1.502 kW/ha in 2005–06 from 0.0295

kW/ha in 1971–72, decreasing the contribution of human power from 15 per cent in 1971–72 to 5.8

per cent in 2005–06.

High yielding varieties (HYVs) of seeds and an organised seed sector have been instrumental in driving

agricultural productivity across the country. The area under certified seeds in India has increased from

around 500 hectares in 1962–63 to more than 0.5 million hectares in 1999–2000, improving the yield

of crops.

Institutional credit has reduced the role of traditional money lenders in the Indian agricultural sector,

thereby, creating an organised credit market. The share of institutional credit, which stood at

approximately 7 per cent in 1951, has increased to more than 60 per cent in 2002; whereas the share

of non-institutional credit, which primarily comprises money lenders, has declined to approximately 40

per cent in 2002, from 92.7 per cent in 1951.

MARKET OVERVIEW

Agriculture November 2010

23

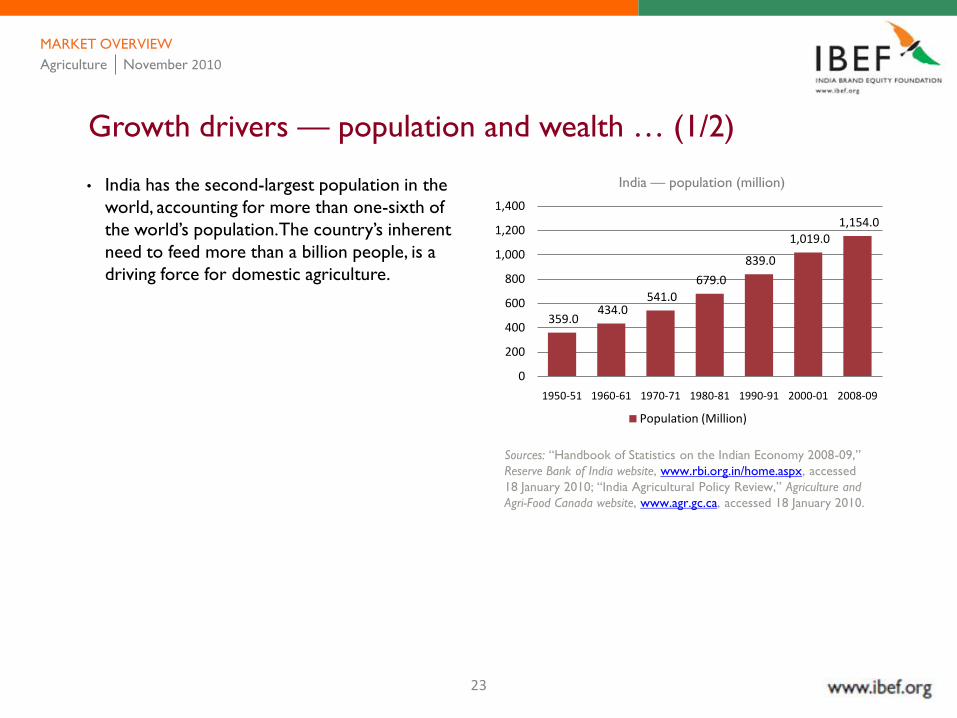

• India has the second-largest population in the

world, accounting for more than one-sixth of

the world’s population. The country’s inherent

need to feed more than a billion people, is a

driving force for domestic agriculture.

Growth drivers — population and wealth … (1/2)

Sources: ―Handbook of Statistics on the Indian Economy 2008-09,‖

Reserve Bank of India website, www.rbi.org.in/home.aspx, accessed

18 January 2010; ―India Agricultural Policy Review,‖ Agriculture and

Agri-Food Canada website, www.agr.gc.ca, accessed 18 January 2010.

India — population (million)

359.0 434.0

541.0

679.0

839.0

1,019.0 1,154.0

0

200

400

600

800

1,000

1,200

1,400

1950-51 1960-61 1970-71 1980-81 1990-91 2000-01 2008-09

Population (Million)

MARKET OVERVIEW

Agriculture November 2010

24

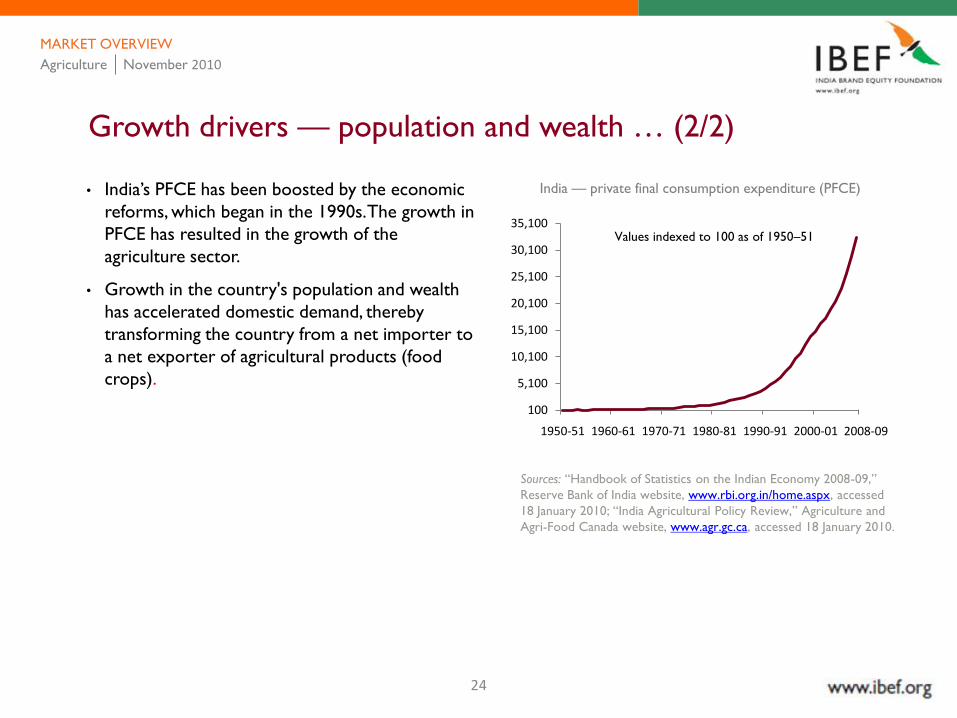

• India’s PFCE has been boosted by the economic

reforms, which began in the 1990s. The growth in

PFCE has resulted in the growth of the

agriculture sector.

• Growth in the country's population and wealth

has accelerated domestic demand, thereby

transforming the country from a net importer to

a net exporter of agricultural products (food

crops).

Growth drivers — population and wealth … (2/2)

Sources: ―Handbook of Statistics on the Indian Economy 2008-09,‖

Reserve Bank of India website, www.rbi.org.in/home.aspx, accessed

18 January 2010; ―India Agricultural Policy Review,‖ Agriculture and

Agri-Food Canada website, www.agr.gc.ca, accessed 18 January 2010.

India — private final consumption expenditure (PFCE)

100

5,100

10,100

15,100

20,100

25,100

30,100

35,100

1950-51 1960-61 1970-71 1980-81 1990-91 2000-01

Values indexed to 100 as of 1950–51

2008-09

MARKET OVERVIEW

Agriculture November 2010

25

Sources: ―Agricultural Statistics At a Glance 2010," Economics

And Statistics, Ministry of Agriculture, Government of India

website, http://dacnet.nic.in/eands/latest_2006.htm, accessed 17

November 2010

P – Provisional

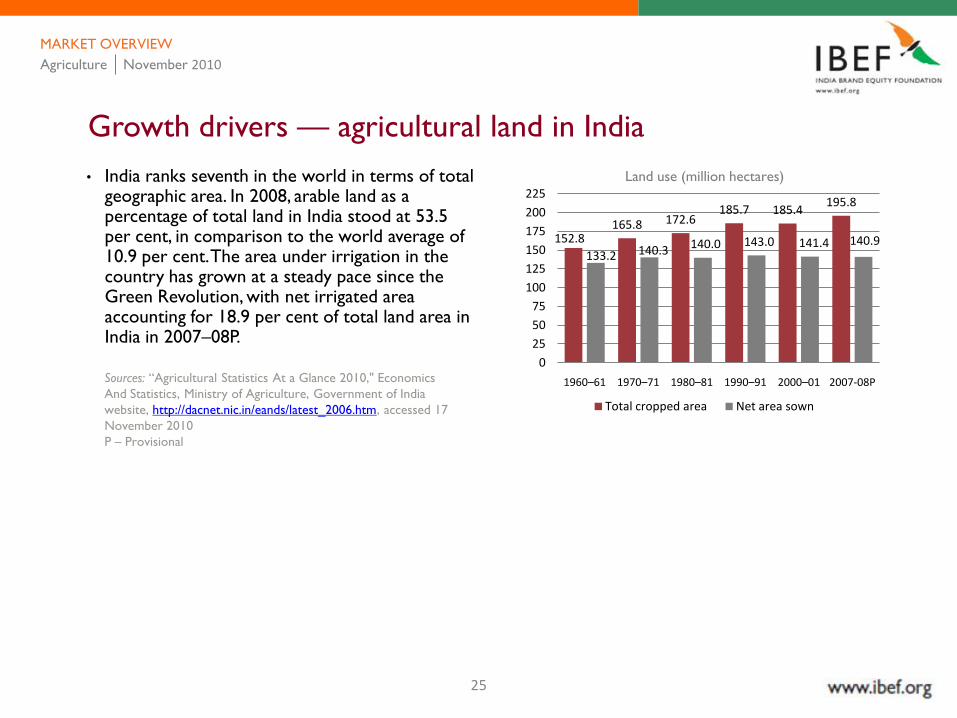

Growth drivers — agricultural land in India

• India ranks seventh in the world in terms of total geographic area. In 2008, arable land as a percentage of total land in India stood at 53.5 per cent, in comparison to the world average of 10.9 per cent. The area under irrigation in the country has grown at a steady pace since the Green Revolution, with net irrigated area accounting for 18.9 per cent of total land area in India in 2007–08P.

Land use (million hectares)

MARKET OVERVIEW

152.8165.8 172.6

185.7 185.4195.8

133.2 140.3 140.0 143.0 141.4 140.9

0

25

50

75

100

125

150

175

200

225

1960–61 1970–71 1980–81 1990–91 2000–01 2007-08P

Total cropped area Net area sown

Agriculture November 2010

26

Sources: "Agricultural Statistics At a Glance 2008,‖ Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/At_Glance_2008.htm, accessed 18 January 2010; "Agricultural Statistics At a Glance 2009," Economics And Statistics,

Ministry of Agriculture, Government of India website, http://dacnet.nic.in/eands/pdf%20files/tb14.5U.pdf, accessed 14 July 2010; P Kataria and

AS Joshi, ―Energy Use in Indian Agriculture,‖ Department of Economics, Punjab Agricultural University, Ludhiana, India; ―Agriculture and Food

Management,‖ Economic Survey 2009-10, Government of India: Union Budget and Economic Survey website, http://indiabudget.nic.in/es2009-

10/esmain.htm, accessed 08 March 2010.

P – Provisional

Growth drivers — improved irrigation facilities in India

Irrigated area (million hectares)

28.0 38.2

49.8

63.2

76.6

87.3

24.7 31.1

38.7 48.0

55.1 62.3

0102030405060708090

100

1960-61 1970-71 1980-81 1990-91 2000-01 2007-08P

Gross Irrigated Area Net Irrigated Area

• The government has taken several initiatives

through five-year plans to improve irrigation

facilities in India. The Working Group on Water

Resources for the Eleventh Five Year Plan (2007–

2012) has proposed creation of irrigation

potential of 16 million hectare during the

Eleventh Five Year Plan period. The total

irrigation potential in the country has increased

from 81.1 million ha in 1991–92 to 102.77

million ha by March 2007.

MARKET OVERVIEW

Agriculture November 2010

27

• In 1950, per hectare use of fertilisers in India was 0.55 Kg. However, backed by government policies and

initiatives, the consumption increased to more than 125 Kg per hectare by 2009.

• The government has taken various policy initiatives for the fertiliser sector, such as pricing policy for

indigenous urea, new investments in the urea sector, nutrient-based pricing, production and availability

of fortified and coated fertilisers, uniform freight subsidy on all fertilisers under the fertiliser subsidy

regime, concession scheme for decontrolled phosphatic and potassic fertilisers, etc.

Source: ―Agriculture and Food Management,‖ Economic Survey 2009-10, Government of India: Union Budget and Economic Survey website,

http://indiabudget.nic.in/es2009-10/esmain.htm, accessed 08 March 2010.

Growth drivers — increasing role of fertilisers

Fertilisers — production and consumption Fertiliser consumption per hectare

0.2 1.1 3.0

9.0

14.8 14.3

0.3 2.2

5.5

12.5

19.7

24.9

0

5

10

15

20

25

30

1960-61 1970-71 1980-81 1990-91 2000-01 2008-09

Production (Million Tonnes) Consumption (Million Tonnes)

88.9

105.5 111.8 116.8

128.6

0

20

40

60

80

100

120

140

2000-01 2005-06 2006-07 2007-08 2008-09

Consumption (Kg/ha)

MARKET OVERVIEW

Agriculture November 2010

28

Sources: ―Annual Report 2009–10,‖ Department of Agriculture &

Cooperation, Ministry of Agriculture, Government of India website,

http://agricoop.nic.in/AnnualRepor2009-10/AR.pdf, accessed 14 July

2010; P Kataria and AS Joshi, ―Energy Use in Indian Agriculture,‖

Department of Economics, Punjab Agricultural University, Ludhiana,

India.

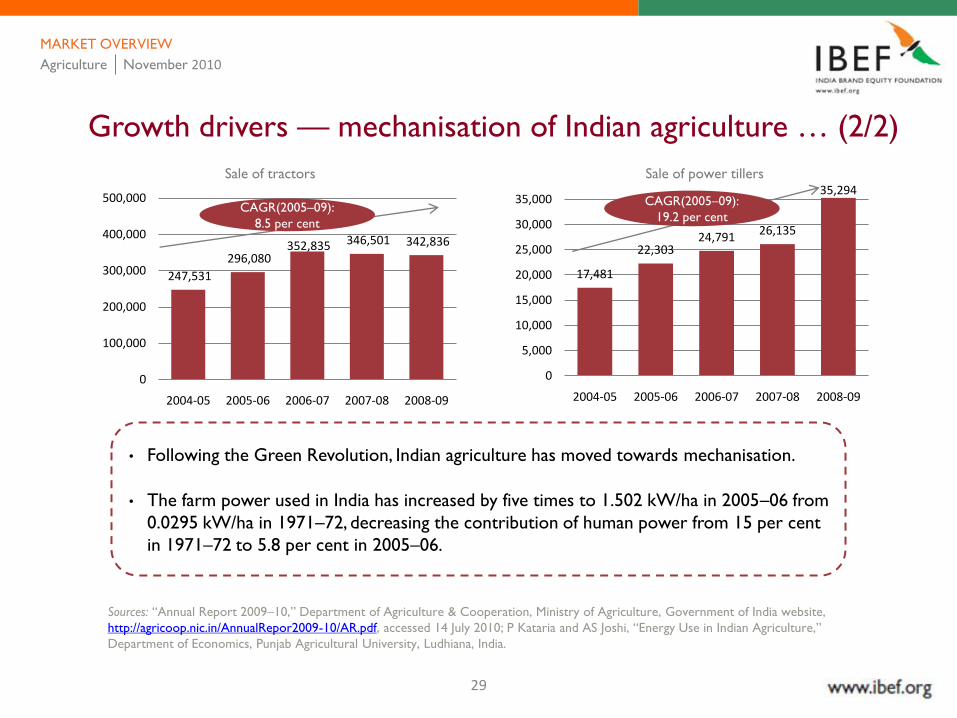

Growth drivers — mechanisation of Indian agriculture … (1/2)

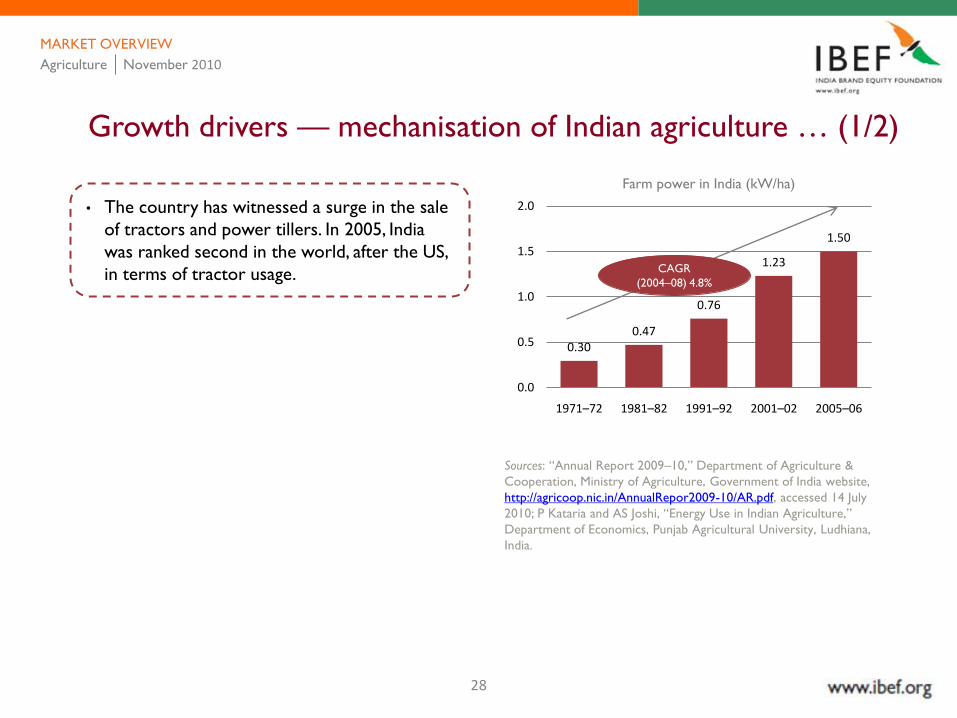

• The country has witnessed a surge in the sale

of tractors and power tillers. In 2005, India

was ranked second in the world, after the US,

in terms of tractor usage.

Farm power in India (kW/ha)

MARKET OVERVIEW

0.300.47

0.76

1.23

1.50

0.0

0.5

1.0

1.5

2.0

1971–72 1981–82 1991–92 2001–02 2005–06

CAGR

(2004–08) 4.8%

Agriculture November 2010

29

Sources: ―Annual Report 2009–10,‖ Department of Agriculture & Cooperation, Ministry of Agriculture, Government of India website,

http://agricoop.nic.in/AnnualRepor2009-10/AR.pdf, accessed 14 July 2010; P Kataria and AS Joshi, ―Energy Use in Indian Agriculture,‖

Department of Economics, Punjab Agricultural University, Ludhiana, India.

Growth drivers — mechanisation of Indian agriculture … (2/2)

• Following the Green Revolution, Indian agriculture has moved towards mechanisation.

• The farm power used in India has increased by five times to 1.502 kW/ha in 2005–06 from

0.0295 kW/ha in 1971–72, decreasing the contribution of human power from 15 per cent

in 1971–72 to 5.8 per cent in 2005–06.

Sale of tractors Sale of power tillers

MARKET OVERVIEW

247,531

296,080 352,835 346,501 342,836

0

100,000

200,000

300,000

400,000

500,000

2004-05 2005-06 2006-07 2007-08 2008-09

CAGR(2005–09):

8.5 per cent

17,481

22,30324,791

26,135

35,294

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

2004-05 2005-06 2006-07 2007-08 2008-09

CAGR(2005–09):

19.2 per cent

Agriculture November 2010

30

Source: ―Annual Report 2009–10,‖ Department of Agriculture & Cooperation, Ministry of Agriculture, Government of India website,

http://agricoop.nic.in/AnnualRepor2009-10/AR.pdf, accessed 14 July 2010.

A – Anticipated

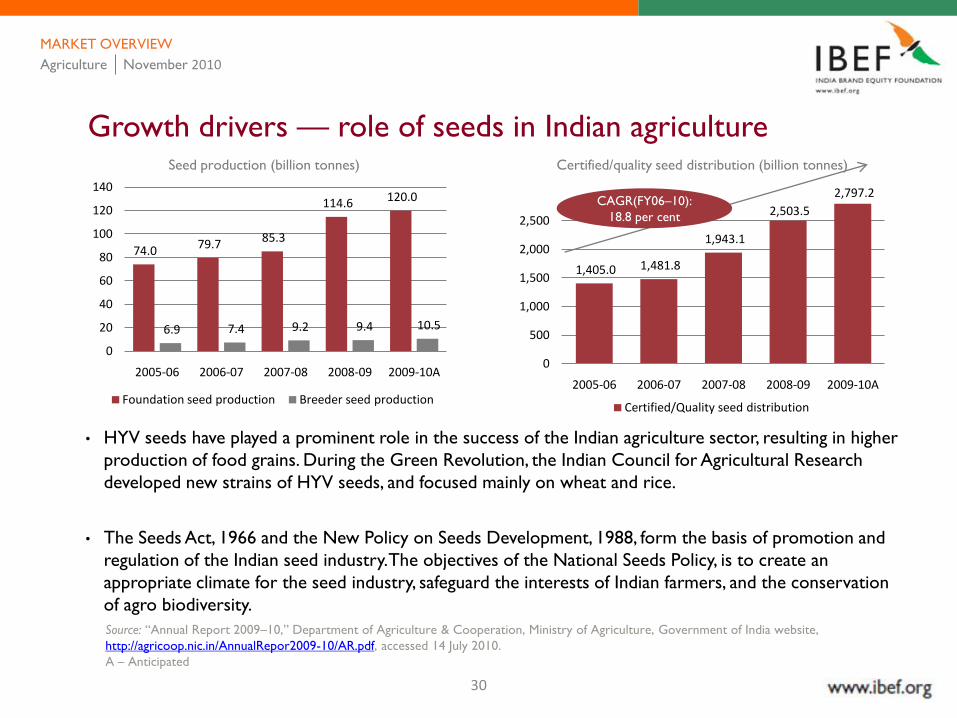

Growth drivers — role of seeds in Indian agriculture

• HYV seeds have played a prominent role in the success of the Indian agriculture sector, resulting in higher

production of food grains. During the Green Revolution, the Indian Council for Agricultural Research

developed new strains of HYV seeds, and focused mainly on wheat and rice.

• The Seeds Act, 1966 and the New Policy on Seeds Development, 1988, form the basis of promotion and

regulation of the Indian seed industry. The objectives of the National Seeds Policy, is to create an

appropriate climate for the seed industry, safeguard the interests of Indian farmers, and the conservation

of agro biodiversity.

Seed production (billion tonnes) Certified/quality seed distribution (billion tonnes)

MARKET OVERVIEW

74.0 79.7 85.3

114.6 120.0

6.9 7.4 9.2 9.4 10.5

0

20

40

60

80

100

120

140

2005-06 2006-07 2007-08 2008-09 2009-10A

Foundation seed production Breeder seed production

1,405.0 1,481.8

1,943.1

2,503.5

2,797.2

0

500

1,000

1,500

2,000

2,500

2005-06 2006-07 2007-08 2008-09 2009-10A

Certified/Quality seed distribution

CAGR(FY06–10):

18.8 per cent

Agriculture November 2010

31

Sources: ―Annual Report 2009–10,‖ Department of Agriculture & Cooperation, Ministry of Agriculture, Government of India website,

http://agricoop.nic.in/AnnualRepor2009-10/AR.pdf, accessed 14 July 2010; ―Flow of institutional credit to agriculture and allied activities,‖ Economic

Survey 2008–09; Ramesh Golait, ―Current Issues in Agriculture Credit in India: An Assessment,‖ Summer 2007, Reserve Bank of India Occasional

Papers, RBI website, http://rbidocs.rbi.org.in/rdocs/Publications/PDFs/82933.pdf, accessed 18 January 2010.

P – Provisional

Growth drivers — improved agricultural credit

• Institutional credit, which comprises loans from commercial banks, cooperatives societies and banks as

well as regional rural banks (RRBs), has grown at a CAGR of about 25 per cent between 2002–03 and

2008–09.

• In 2008–09, the amount disbursed by all banks (including cooperative banks and RRBs) to agriculture

and allied activities stood at US$ 57.5 billion (INR 2,644.6 billion), with commercial banks accounting

for more than three-fourth of the amount disbursed.

Flow of institutional credit to agriculture and allied activities (US$ billion)

MARKET OVERVIEW

57.2% 60.3% 65.0% 69.5% 72.6% 71.1% 76.7%

34.1% 31.0% 25.1% 22.0% 18.5% 19.0% 13.5%

8.7% 8.7% 9.9% 8.4% 8.9% 9.9% 9.8%

2002-03 2003-04 2004-05 2005-06 2006-07 2007-08 2008-09P

Commercial banks Cooperative banks RRBs

100%=

US$ billion15.1 18.9 27.2 39.2 49.9 55.4 57.5

Agriculture November 2010

32

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

AGRICULTURE November 2010

33

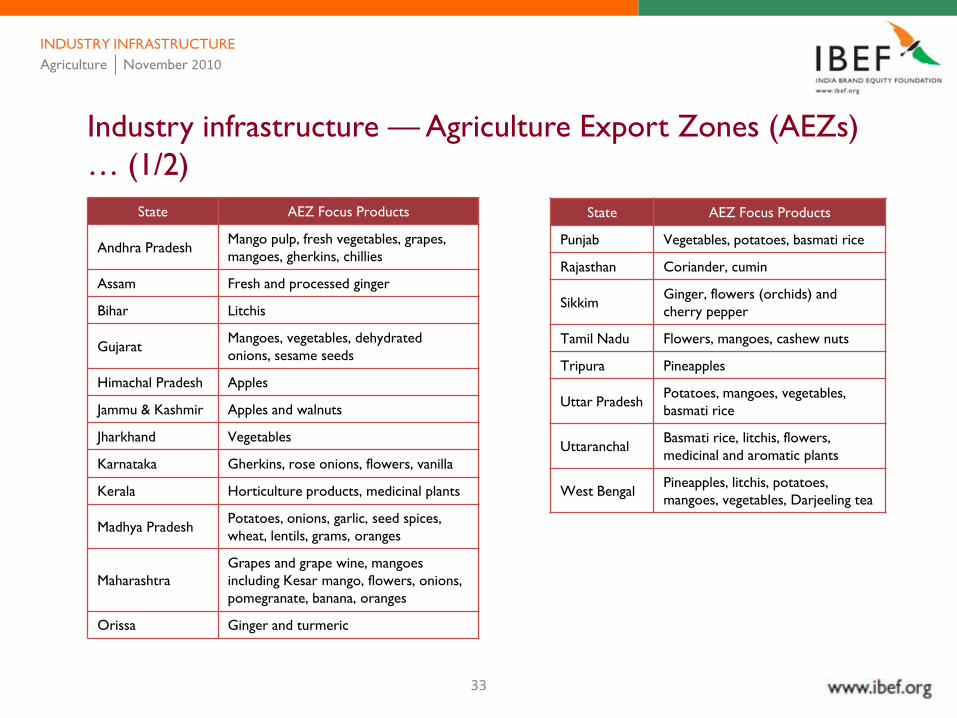

Industry infrastructure — Agriculture Export Zones (AEZs)

… (1/2)

State AEZ Focus Products

Andhra PradeshMango pulp, fresh vegetables, grapes,

mangoes, gherkins, chillies

Assam Fresh and processed ginger

Bihar Litchis

GujaratMangoes, vegetables, dehydrated

onions, sesame seeds

Himachal Pradesh Apples

Jammu & Kashmir Apples and walnuts

Jharkhand Vegetables

Karnataka Gherkins, rose onions, flowers, vanilla

Kerala Horticulture products, medicinal plants

Madhya PradeshPotatoes, onions, garlic, seed spices,

wheat, lentils, grams, oranges

Maharashtra

Grapes and grape wine, mangoes

including Kesar mango, flowers, onions,

pomegranate, banana, oranges

Orissa Ginger and turmeric

State AEZ Focus Products

Punjab Vegetables, potatoes, basmati rice

Rajasthan Coriander, cumin

SikkimGinger, flowers (orchids) and

cherry pepper

Tamil Nadu Flowers, mangoes, cashew nuts

Tripura Pineapples

Uttar PradeshPotatoes, mangoes, vegetables,

basmati rice

UttaranchalBasmati rice, litchis, flowers,

medicinal and aromatic plants

West BengalPineapples, litchis, potatoes,

mangoes, vegetables, Darjeeling tea

INDUSTRY INFRASTRUCTURE

Agriculture November 2010

34

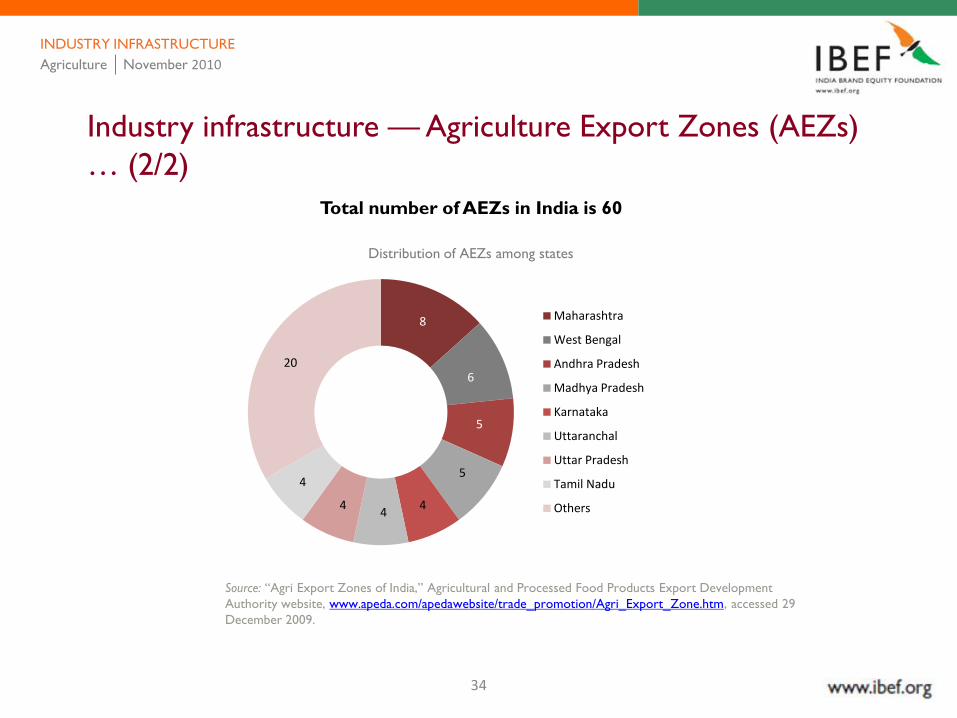

Industry infrastructure — Agriculture Export Zones (AEZs)

… (2/2)

Source: ―Agri Export Zones of India,‖ Agricultural and Processed Food Products Export Development

Authority website, www.apeda.com/apedawebsite/trade_promotion/Agri_Export_Zone.htm, accessed 29

December 2009.

Distribution of AEZs among states

Total number of AEZs in India is 60

8

6

5

5

44

4

4

20

Maharashtra

West Bengal

Andhra Pradesh

Madhya Pradesh

Karnataka

Uttaranchal

Uttar Pradesh

Tamil Nadu

Others

Distribution of AEZs among states

INDUSTRY INFRASTRUCTURE

Agriculture November 2010

35

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

AGRICULTURE November 2010

36

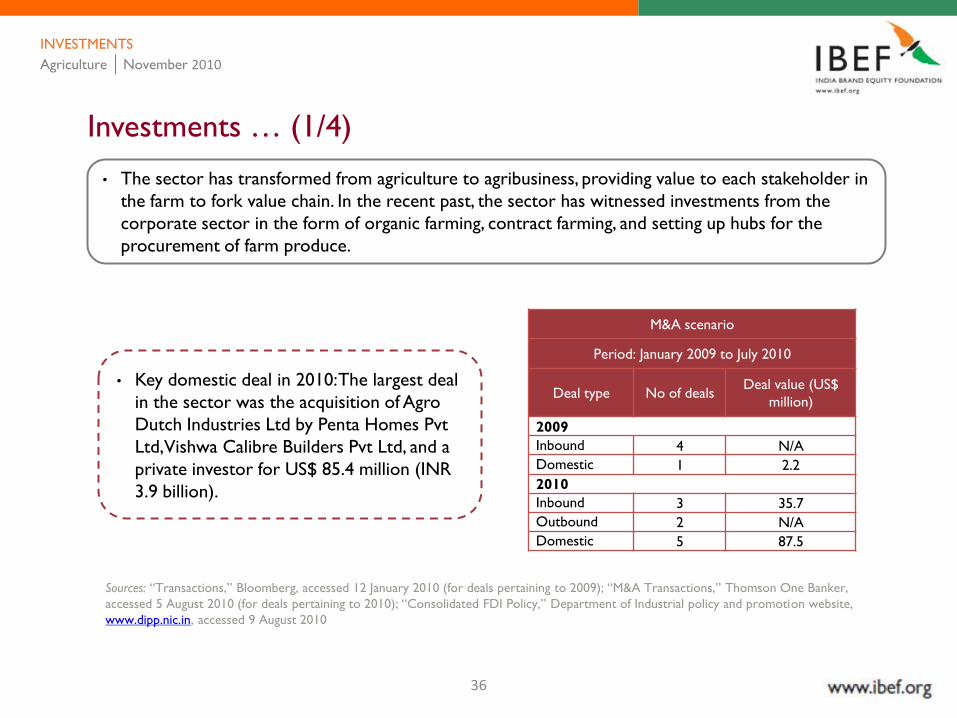

Investments … (1/4)

• The sector has transformed from agriculture to agribusiness, providing value to each stakeholder in

the farm to fork value chain. In the recent past, the sector has witnessed investments from the

corporate sector in the form of organic farming, contract farming, and setting up hubs for the

procurement of farm produce.

INVESTMENTS

Sources: ―Transactions,‖ Bloomberg, accessed 12 January 2010 (for deals pertaining to 2009); ―M&A Transactions,‖ Thomson One Banker,

accessed 5 August 2010 (for deals pertaining to 2010); ―Consolidated FDI Policy,‖ Department of Industrial policy and promotion website,

www.dipp.nic.in, accessed 9 August 2010

M&A scenario

Period: January 2009 to July 2010

Deal type No of dealsDeal value (US$

million)

2009

Inbound 4 N/A

Domestic 1 2.2

2010

Inbound 3 35.7

Outbound 2 N/A

Domestic 5 87.5

• Key domestic deal in 2010: The largest deal

in the sector was the acquisition of Agro

Dutch Industries Ltd by Penta Homes Pvt

Ltd, Vishwa Calibre Builders Pvt Ltd, and a

private investor for US$ 85.4 million (INR

3.9 billion).

Agriculture November 2010

37

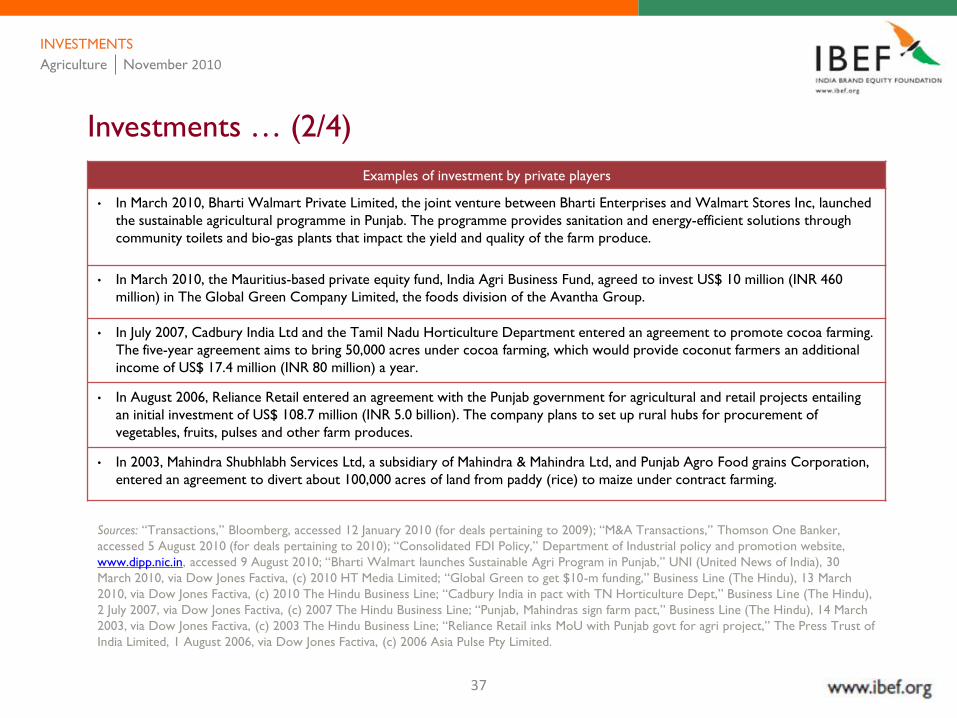

Investments … (2/4)

INVESTMENTS

Examples of investment by private players

• In March 2010, Bharti Walmart Private Limited, the joint venture between Bharti Enterprises and Walmart Stores Inc, launched

the sustainable agricultural programme in Punjab. The programme provides sanitation and energy-efficient solutions through

community toilets and bio-gas plants that impact the yield and quality of the farm produce.

• In March 2010, the Mauritius-based private equity fund, India Agri Business Fund, agreed to invest US$ 10 million (INR 460

million) in The Global Green Company Limited, the foods division of the Avantha Group.

• In July 2007, Cadbury India Ltd and the Tamil Nadu Horticulture Department entered an agreement to promote cocoa farming.

The five-year agreement aims to bring 50,000 acres under cocoa farming, which would provide coconut farmers an additional

income of US$ 17.4 million (INR 80 million) a year.

• In August 2006, Reliance Retail entered an agreement with the Punjab government for agricultural and retail projects entailing

an initial investment of US$ 108.7 million (INR 5.0 billion). The company plans to set up rural hubs for procurement of

vegetables, fruits, pulses and other farm produces.

• In 2003, Mahindra Shubhlabh Services Ltd, a subsidiary of Mahindra & Mahindra Ltd, and Punjab Agro Food grains Corporation,

entered an agreement to divert about 100,000 acres of land from paddy (rice) to maize under contract farming.

Sources: ―Transactions,‖ Bloomberg, accessed 12 January 2010 (for deals pertaining to 2009); ―M&A Transactions,‖ Thomson One Banker,

accessed 5 August 2010 (for deals pertaining to 2010); ―Consolidated FDI Policy,‖ Department of Industrial policy and promotion website,

www.dipp.nic.in, accessed 9 August 2010; ―Bharti Walmart launches Sustainable Agri Program in Punjab,‖ UNI (United News of India), 30

March 2010, via Dow Jones Factiva, (c) 2010 HT Media Limited; ―Global Green to get $10-m funding,‖ Business Line (The Hindu), 13 March

2010, via Dow Jones Factiva, (c) 2010 The Hindu Business Line; ―Cadbury India in pact with TN Horticulture Dept,‖ Business Line (The Hindu),

2 July 2007, via Dow Jones Factiva, (c) 2007 The Hindu Business Line; ―Punjab, Mahindras sign farm pact,‖ Business Line (The Hindu), 14 March

2003, via Dow Jones Factiva, (c) 2003 The Hindu Business Line; ―Reliance Retail inks MoU with Punjab govt for agri project,‖ The Press Trust of

India Limited, 1 August 2006, via Dow Jones Factiva, (c) 2006 Asia Pulse Pty Limited.

Agriculture November 2010

38

Investments … (3/4)

Sources: ―Agriculture and Food Management,‖ Economic Survey 2009-10, Government of India: Union Budget and Economic Survey

website, http://indiabudget.nic.in/es2009-10/esmain.htm ,accessed 08 March 2010.

INVESTMENTS

Key state-wise contract farming initiatives by private sector

State Crop Company/Corporate Area (Hectares)

Maharashtra Soyabean Tinna Oils and Chemicals 134,800

Madhya Pradesh Wheat Hindustan Lever Ltd (HLL) 15,000

Punjab Rice (Basmati)

Satnam Overseas, DD Intenational Inc,

Amira Foods India Ltd (Escorts Ltd & Grain

Tech)

14,700

PunjabRice (Basmati), Groundnut & Potato,

tomato, chilliPepsiCo India Ltd ~6,000

Karnataka Marigold & Caprica Chili AVT Natural Products Ltd 4,000

Punjab Rice (Basmati), Maize Satnam Overseas 4,000

Punjab Barley United Breweries Ltd 2,270

Agriculture November 2010

39

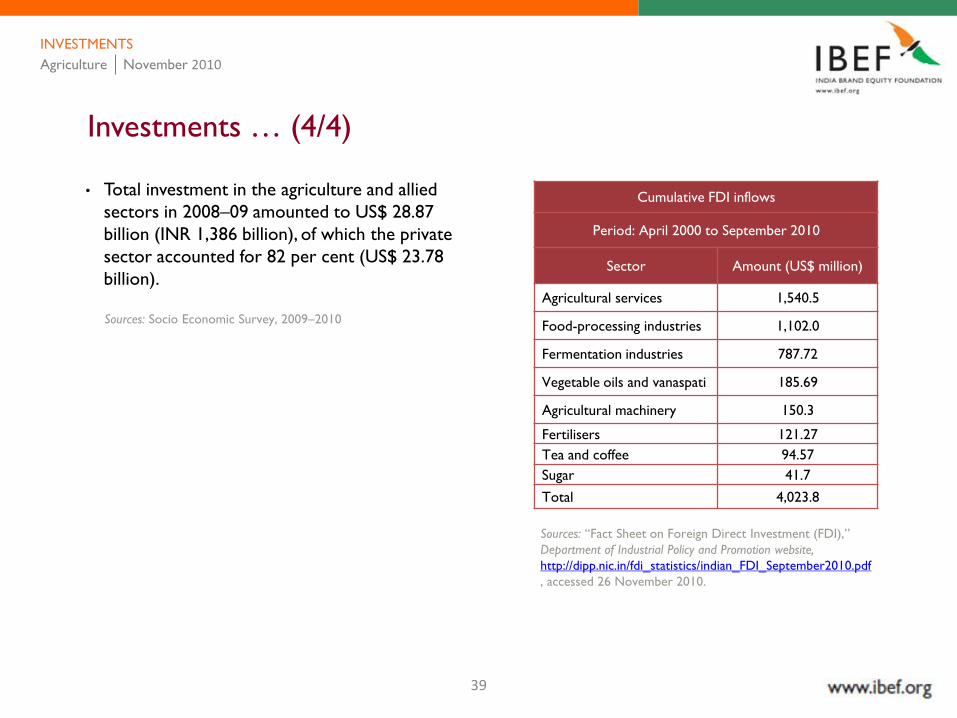

Investments … (4/4)

INVESTMENTS

Cumulative FDI inflows

Period: April 2000 to September 2010

Sector Amount (US$ million)

Agricultural services 1,540.5

Food-processing industries 1,102.0

Fermentation industries 787.72

Vegetable oils and vanaspati 185.69

Agricultural machinery 150.3

Fertilisers 121.27

Tea and coffee 94.57

Sugar 41.7

Total 4,023.8

• Total investment in the agriculture and allied

sectors in 2008–09 amounted to US$ 28.87

billion (INR 1,386 billion), of which the private

sector accounted for 82 per cent (US$ 23.78

billion).

Sources: Socio Economic Survey, 2009–2010

Sources: ―Fact Sheet on Foreign Direct Investment (FDI),‖

Department of Industrial Policy and Promotion website,

http://dipp.nic.in/fdi_statistics/indian_FDI_September2010.pdf

, accessed 26 November 2010.

Agriculture November 2010

40

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

AGRICULTURE November 2010

41

Policy and regulatory framework … (1/8)

The various ministries within the Government of India and other agencies responsible

for the development of the agricultural sector include

• Ministry of Food Processing Industries

• Department of Agriculture & Cooperation (National Horticulture Board)

• Department of Animal Husbandry, Dairying and Fisheries

• Ministry of Commerce and Industry (commodity boards for rubber, coffee, tea and spices)

• National Dairy Development Board (NDDB)

POLICY AND REGULATORY FRAMEWORK

Agriculture November 2010

42

Policy and regulatory framework … (2/8)

The major acts and rules pertaining to the agro industry:

• Agriculture Produce (Grading & Marking) Act, 1937

• Fruit Products Order, 1955

• Coconut Development Board Act, 1979

• National Cooperative Development Corporation (NCDC Act), 1962

• Seed Act, 1966

• Seeds Control Order, 1983

POLICY AND REGULATORY FRAMEWORK

Agriculture November 2010

43

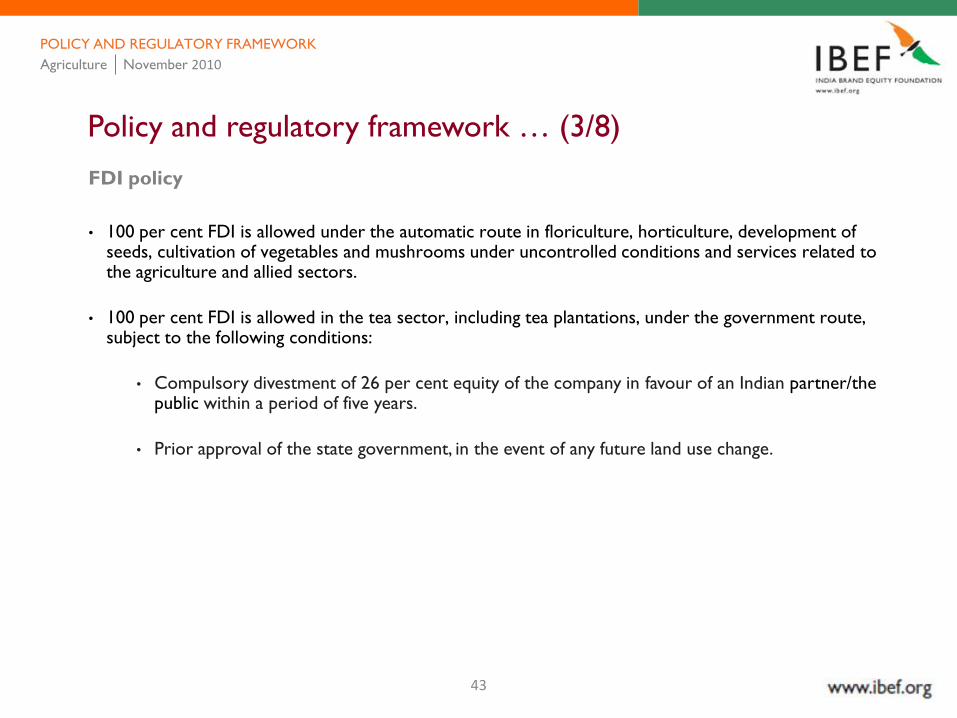

Policy and regulatory framework … (3/8)

FDI policy

• 100 per cent FDI is allowed under the automatic route in floriculture, horticulture, development of seeds, cultivation of vegetables and mushrooms under uncontrolled conditions and services related to the agriculture and allied sectors.

• 100 per cent FDI is allowed in the tea sector, including tea plantations, under the government route, subject to the following conditions:

• Compulsory divestment of 26 per cent equity of the company in favour of an Indian partner/the public within a period of five years.

• Prior approval of the state government, in the event of any future land use change.

POLICY AND REGULATORY FRAMEWORK

Agriculture November 2010

44

Policy and regulatory framework … (4/8)

Government initiatives

1. Vishesh Krishi Gram UdyogYojana (VKGUY) — special agriculture and village industry scheme

The objective of this scheme is to promote exports in the following areas

• Agricultural produce and its value-added products

• Minor forest produce and its value-added variants

• Gram udyog products

• Forest-based products

• Other products

POLICY AND REGULATORY FRAMEWORK

Agriculture November 2010

45

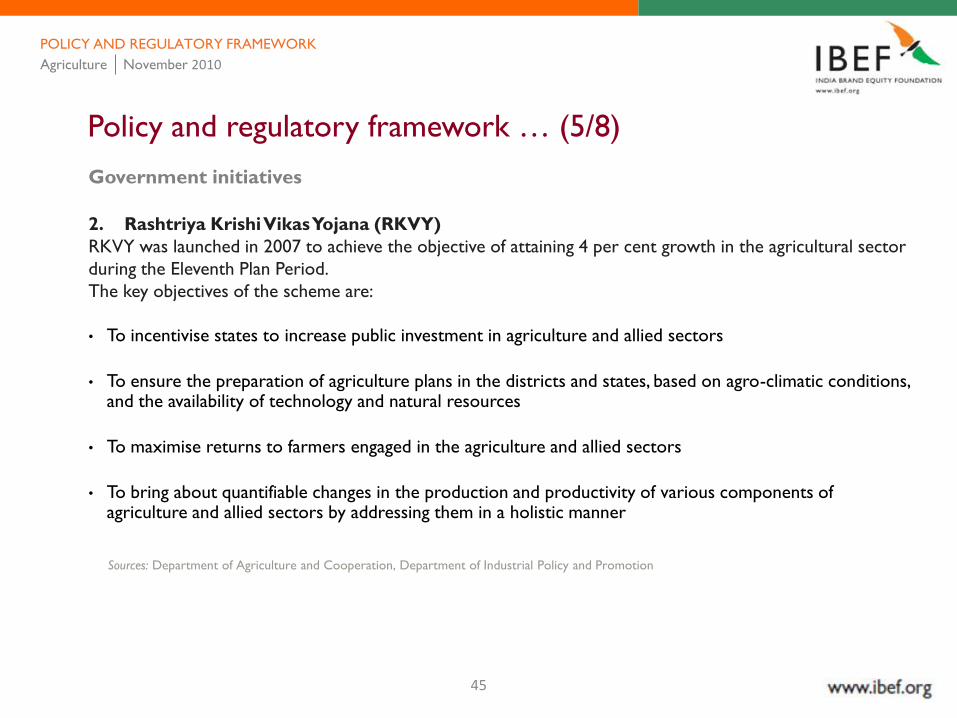

Policy and regulatory framework … (5/8)

Government initiatives

2. Rashtriya KrishiVikasYojana (RKVY)

RKVY was launched in 2007 to achieve the objective of attaining 4 per cent growth in the agricultural sector

during the Eleventh Plan Period.

The key objectives of the scheme are:

• To incentivise states to increase public investment in agriculture and allied sectors

• To ensure the preparation of agriculture plans in the districts and states, based on agro-climatic conditions, and the availability of technology and natural resources

• To maximise returns to farmers engaged in the agriculture and allied sectors

• To bring about quantifiable changes in the production and productivity of various components of agriculture and allied sectors by addressing them in a holistic manner

Sources: Department of Agriculture and Cooperation, Department of Industrial Policy and Promotion

POLICY AND REGULATORY FRAMEWORK

Agriculture November 2010

46

Sources: ―Share of Public Sector Outlays and Expenditure under Agriculture and Allied Activities during Ninth Plan, Tenth Plan, and Eleventh Plan,‖

Department of Agriculture & Cooperation, Ministry of Agriculture, Government of India,

http://dacnet.nic.in/eands/At_Glance_2008/Agriculture_new.html accessed 18 January 2010; Source: "Agricultural Statistics At a Glance 2008,‖

Economics And Statistics, Ministry of Agriculture, Government of India website, http://dacnet.nic.in/eands/At_Glance_2008.htm, accessed 18

January 2010.

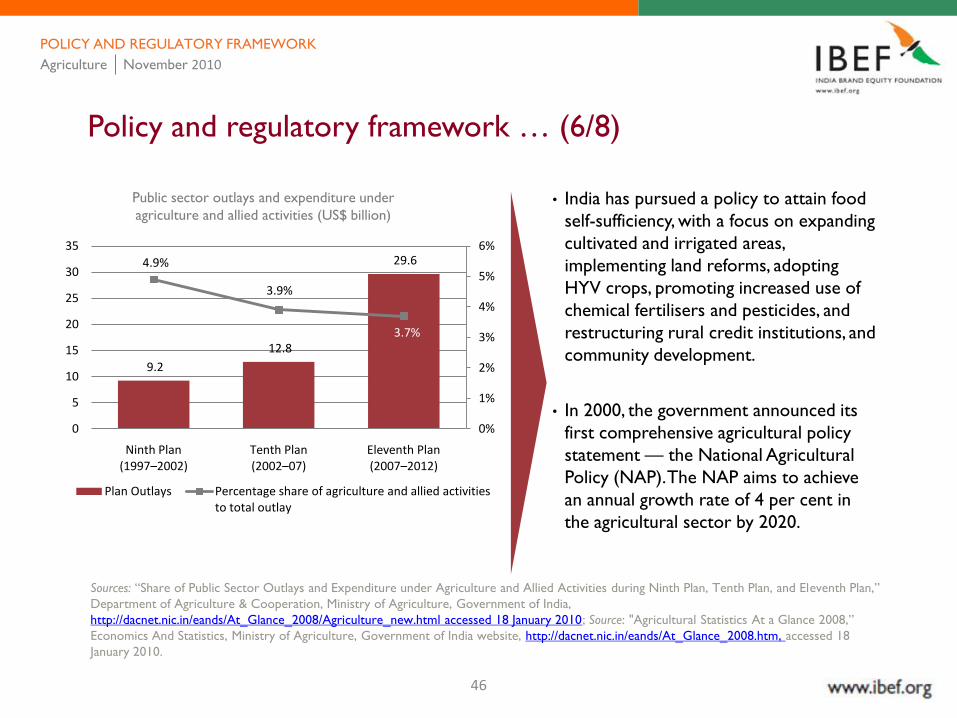

Policy and regulatory framework … (6/8)

Public sector outlays and expenditure under

agriculture and allied activities (US$ billion)

POLICY AND REGULATORY FRAMEWORK

• India has pursued a policy to attain food

self-sufficiency, with a focus on expanding

cultivated and irrigated areas,

implementing land reforms, adopting

HYV crops, promoting increased use of

chemical fertilisers and pesticides, and

restructuring rural credit institutions, and

community development.

• In 2000, the government announced its

first comprehensive agricultural policy

statement — the National Agricultural

Policy (NAP). The NAP aims to achieve

an annual growth rate of 4 per cent in

the agricultural sector by 2020.

9.2

12.8

29.6 4.9%

3.9%

3.7%

0%

1%

2%

3%

4%

5%

6%

0

5

10

15

20

25

30

35

Ninth Plan (1997–2002)

Tenth Plan (2002–07)

Eleventh Plan (2007–2012)

Plan Outlays Percentage share of agriculture and allied activities to total outlay

Agriculture November 2010

47

Policy and regulatory framework … (7/8)

• Currently, India’s agricultural policy focuses on food self-sufficiency, remunerative prices for farmers, and

maintaining stable prices for consumers. These goals are met by a number of instruments such as —

minimum support prices (MSP), food subsidies for consumers, regulated markets, input subsidies for

producers, and international trade policy.

• Since independence, the country has focused on the agricultural sector, through five year plans. The

government’s Eleventh Five Year Plan (2007–2012), focuses on inclusive growth, and rests upon substantial

increase in public sector outlay. In the Eleventh Plan, the public sector outlay towards agriculture and

allied activities stands at US$ 29.6 billion (INR 1,363.8 billion).

POLICY AND REGULATORY FRAMEWORK

Sources: ―Share of Public Sector Outlays and Expenditure under Agriculture and Allied Activities during Ninth Plan, Tenth Plan, and Eleventh Plan,‖

Department of Agriculture & Cooperation, Ministry of Agriculture, Government of India,

http://dacnet.nic.in/eands/At_Glance_2008/Agriculture_new.html accessed 18 January 2010;

Source: "Agricultural Statistics At a Glance 2008,‖ Economics And Statistics, Ministry of Agriculture, Government of India website,

http://dacnet.nic.in/eands/At_Glance_2008.htm, accessed 18 January 2010.

Agriculture November 2010

48

Policy and regulatory framework … (8/8)

The Union Budget 2010–11 focused on the following:

• Provision of US$ 86.9 million (INR 4 billion) to extend the Green Revolution to the eastern region of the country, comprising Bihar, Chhattisgarh, Jharkhand, Eastern Uttar Pradesh, West Bengal and Orissa.

• Provision of US$ 65.2 million (INR 3 billion) to organise 60,000 pulses and oil-seed villages in rain-fed areas in 2010–11 and to provide an integrated intervention for water harvesting, watershed management and soil health to improve productivity of the dry land farming areas.

• Provision of US$ 43.4 million (INR 2 billion) to sustain the gains already made in the green revolution areas through conservation farming, which involves concurrent attention to soil health, water conservation and preservation of biodiversity.

• Banks have been consistently meeting the targets set for agricultural credit flow in the past few years. For the year 2010–11, the agricultural credit flow target has been set at US$ 81.5 billion (INR 3.7 billion).

• In addition to the 10 mega food park projects already being set up, the government has decided to establish five more similar parks.

• External commercial borrowings are to be available for cold storage or cold room facility, including those for farm level pre-cooling, for preservation or storage of agricultural and allied products, marine products and meat.

POLICY AND REGULATORY FRAMEWORK

Source: ―India Agricultural Policy Review,‖ Agriculture and Agri-Food Canada website, www4.agr.gc.ca/AAFC-AAC/display-

afficher.do?id=1201538787839&lang=eng, accessed 18 January 2010.

Agriculture November 2010

49

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

AGRICULTURE November 2010

50

Opportunities … (1/3)

Sources: ―Surabhi Mittal, ―Working Paper No 209: Demand-Supply Trends and Projections of Food in India,‖ Indian Council For Research On

International Economic Relations (ICRIER) website, www.icrier.org, accessed 22 January 2010; ―India needs a pulses revolution,‖ The Economic

Times website, http://economictimes.indiatimes.com/opinion/perspectives/India-needs-a-pulses-revolution/articleshow/5035613.cms, accessed 21

September 2009.

OPPORTUNITIES

Demand–supply gap of cereals in India (MT)

188.5

245.1

277.2

209.7242.2

260.2

0

50

100

150

200

250

300

350

2011P 2021P 2026P

Demand Supply

• The demand-supply gap

for food in India shows

that in the short to

medium term, supply will

meet demand

requirements; from 2021

demand will outstrip

supply for cereals, pulses,

edible oil and sugar. Food

commodity prices are

likely to be high and

volatile for the next 10–

15 years. India needs a

pulses revolution in order

to meet the increasing

demand.

Agriculture November 2010

51

Opportunities … (2/3)

Sources: ―Surabhi Mittal, ―Working Paper No 209: Demand-Supply Trends and Projections of Food in India,‖ Indian Council For Research On

International Economic Relations (ICRIER) website, www.icrier.org, accessed 22 January 2010; ―India Agricultural Policy Review,‖ Agriculture and

Agri-Food Canada website, www4.agr.gc.ca/AAFC-AAC/display-afficher.do?id=1201538787839&lang=eng, accessed 18 January 2010.

OPPORTUNITIES

Demand-side

growth along

with

government

initiatives

expected to

help India

become a

leading agro

country

• India ranks among the fastest-growing global economies and is the world’s converging point of focus

amidst narrowing boundaries and well-connected international regions. The massive agrarian

employment base in India’s rural population is directly responsible for driving such unsurpassed growth

dynamics.

• The Indian population is projected to reach approximately 1.6 billion in 2050, thereby creating a huge

domestic demand for agricultural products.

• The various policies and growth initiatives of the Government of India are expected to further boost

growth in this sector. According to the Organisation for Economic Co-operation and Development -

Food and Agriculture Organization, India is estimated to account for 12.1 per cent and 21.8 per cent of

the world’s wheat and rice production, respectively by 2015.

Agriculture November 2010

52

Opportunities … (3/3)

Sources: ―Surabhi Mittal, ―Working Paper No 209: Demand-Supply Trends and Projections of Food in India,‖ Indian Council For Research On

International Economic Relations (ICRIER) website, www.icrier.org, accessed 22 January 2010; ―India Inc urged to invest more in agriculture,‖

Business Line (The Hindu), 23 September 2010, via Dow Jones Factiva, © 2010 The Hindu Business Line; ―PE funds invest $300 mn in food processing,

agri-based companies,‖ Business Standard, 21 July 2010, via Dow Jones Factiva, © 2010 Business Standard Ltd.

OPPORTUNITIES

Agricultural inputs

expected to grow

due to increased

production levels

Private sector

involvement

expected to boost

Indian agriculture

further

• With the production levels expected to grow, agricultural input such as fertilisers, farm equipment

and machinery, irrigation facilities, institutional credit, and research and development are expected to

be driven towards a higher target. These inputs are an essential part of the agribusiness, and provide

opportunities across different levels in the agriculture value chain.

• Agriculture is expected to be a point of focus for the private sector in India, as a number of private

players are expected to venture into organic farming, contract farming, and setting up hubs for the

procurement of farm produce.

• Increased corporate investment in this sector is expected to offer a new frontier of growth across

many areas such as economies of scale through advanced models of farming, effective distribution

systems and food security.

• Increased private equity (PE) investment in the food processing and agri-based companies is also

expected to boost further employment in this sector. PE players have invested US$ 300 million in

these companies during January–June 2010.

Agriculture November 2010

53

Contents

Advantage India

Market overview

Industry Infrastructure

Investments

Policy and regulatory framework

Opportunities

Industry associations

AGRICULTURE November 2010

54

Industry associations … (1/3)

Autonomous Bodies

• National Institute of Agricultural Extension Management (MANAGE)

Rajendranagar, Hyderabad–500 030, Andhra Pradesh

Phone: 040-24016702 to 706

Fax: 040-24015388

• National Institute of Agricultural Marketing (NIAM)

Bambala, Kota RoadJaipur–302033, RajasthanPhone: 0141-2770027Fax: 0141-2771938, 2770027

INDUSTRY ASSOCIATIONS

Agriculture November 2010

55

Industry associations … (2/3)

Boards

• Central Insecticides Board and Registration Committee

Machinary Store Building,

N.H.IV Faridabad

Phone: 0129 -2413002

• Coconut Development Board

Kera Bhavan, SRVHS Road, Kochi

Kerala–682011Phone: 0484-2376265, 2377267, 2376553Fax: 0484-2377902

• National Dairy Development Board (NDDB)

PB No 40, Anand–388 001

Phone: 02692-260148/260149/260160

Fax: 02692-260157

INDUSTRY ASSOCIATIONS

Agriculture November 2010

56

Industry associations … (3/3)

Boards

• National Horticulture Board (NHB)

Ministry of Agriculture, Government of India85, Institutional Area, Sector-18Gurgaon–122015, Haryana

• National Oilseeds and Vegetable Oils Development Board (NOVOD)

86, Institutional Area, Sector-18

Gurgaon–122015, Haryana

Councils

• Indian Council of Agricultural Research (ICAR)

Krishi Bhavan, New Delhi 110 114

INDUSTRY ASSOCIATIONS

Agriculture November 2010

57

Wherever applicable, numbers in the report have been rounded off to the nearest whole number.

Conversion rate used: US$ 1= INR 48 and INR 46

Note

NOTE

Agriculture November 2010

58

AGRICULTURE November 2010

DISCLAIMER

India Brand Equity Foundation (IBEF) engaged Ernst &

Young Pvt Ltd to prepare this presentation and the same

has been prepared by Ernst & Young in consultation with

IBEF.

All rights reserved. All copyright in this presentation and

related works is solely and exclusively owned by IBEF. The

same may not be reproduced, wholly or in part in any

material form (including photocopying or storing it in any

medium by electronic means and whether or not

transiently or incidentally to some other use of this

presentation), modified or in any manner communicated

to any third party except with the written approval of

IBEF.

This presentation is for information purposes only. While

due care has been taken during the compilation of this

presentation to ensure that the information is accurate to

the best of Ernst & Young and IBEF’s knowledge and belief,

the content is not to be construed in any manner

whatsoever as a substitute for professional advice.

Ernst & Young and IBEF neither recommend nor endorse

any specific products or services that may have been

mentioned in this presentation and nor do they assume

any liability or responsibility for the outcome of decisions

taken as a result of any reliance placed on this

presentation.

Neither Ernst & Young nor IBEF shall be liable for any

direct or indirect damages that may arise due to any act

or omission on the part of the user due to any reliance

placed or guidance taken from any portion of this

presentation.