agrochemical intermediates & actives a losing battle? · mcdougall, the global agrochemicals...

TRANSCRIPT

The European fine chemicals industry is upbeat about agro, but the experts are sounding warning bells. AndrewWarmington reports from Chemspec Europe 2014

As the world’s largest trade exhibition inthe agrochemicals space, ChemspecEurope always has a strong

agrochemical element in its related content.That was never more the case than this year inBudapest, when almost all of the leadingconsultants in the field were among thespeakers at the European Fine Chemicals Group(EFCG) Crop Protection & Fine Chemicals forumand Agrow magazine’s AgrochemicalsConference.

Chemspec Europe itself has rebounded since2008, helped in no small measure by therecovery of the agrochemicals sector itself inthat time frame. Suppliers to the sector wereunanimously upbeat about the state of themarket when interviewed on the show floor andoptimistic going forward. Yet this was in manyways widely at odds with the gloomy prognosisfrom some consultants.

“The current business model is failing tosustain the European fine chemicals industryand it’s failing to make the contribution to theglobal environment that it should be making,”said Dr Rob Bryant of Brychem. Hispresentation was ultimately about showing howthe industry can regain lost ground andpersuade customers to let it resume doing“what it has done superbly in the recent past” –basically to make all their chemicals for them.

Many of the fundamental facts affecting theindustry appeared in multiple presentations andare beyond dispute. As the world populationgrows and demands more – perhaps 70% moreby 2050 - and more intensively grown foodfrom a decreasing area of farmland, a massiveincrease in productivity will be needed. Foodprices will continue to increase for theforeseeable future.

Meanwhile, the prospect that GM technologywould remove or even reduce the need for cropprotection has vanished, ironically giving atemporary boost to the market in Europe, the

world’s most conspicuously non-GM region.Keeping up with the constantly evolvingchallenge of pests is a vital part of the effort tofeed the world and will drive a continuingincrease in the volume and value ofagrochemicals used.

According to Dr Matthew Phillips of PhillipsMcDougall, the global agrochemicals market– including non-crop applications - at ex-manufacturer level stood at $60.7 billion in2013, an 8.5% increase on 2012. Seeds, justover half of which are now GM, were worth$39.4 billion, an increase of 5.0%. This cameafter years of pretty much continuous growthfrom a low of around $37 billion in 2006. Realgrowth of 2.6%/year is forecast to 2018.

Others cited basically similar figures, allowingfor the fact that definitions vary from oneanalyst to another. Europe accounts for about26% of the global agrochemicals market,though it was overtaken in size by Asia in 2012.Figures cited by Sanjiv Rana of Agrow itselffrom an ECPA report that was also compiled by

Phillips McDougall put the European market at$13.3 billion in 2012, with 9.9% growth since2007 (Figure 1). The EU 28 had enjoyed 8.9%growth, while those outside the EU – mostobviously Russia and Ukraine - had seen 14.5%growth.

In both volume and value terms, Ukraine wasthe fastest growing agrochemicals market(though one imagines, sadly, that this will notbe the case in 2014). Some crops, notablycereals, maize and sugar beet, saw double-digitgrowth in agrochemical demand; only potatoesdid not show growth and one might infer thatregulatory causes lay behind that.

Citing figures from Sumitomo ChemicalEurope, Bryant showed that for every majorcereal crop, biotic losses - those caused by thepests controlled by crop protection products -are a minor issue for farmers (Figure 2). Abioticlosses from drought, salinity, flood, chilling orclimate stress account for 65-81% of the gapbetween average and maximum attainableyields for corn, wheat, soybeans, sorghum, oatsand barley.

“It puts our industry’s role in perspective,”Bryant said. Crop protection chemicals, headded later, only account for 10% of allfarming input costs, while the $20-30 billionfine chemicals industry, excluding captiveproduction, is less than 1% of the totalchemicals industry, which, from CEFIC figures,were just over $3.1 trillion in 2013.

Meanwhile, shocking though it may sound,the proportion of the US crop lost to weeds,diseases and insects actually increased from30% in 1942-50 to nearer 35%. This was partlythe result of farm subsidies, the loss of activeingredients (AIs) deemed to be unsafe or toospecialised to support registrations and the big

A losing battle?� Agrochemical intermediates & actives

12 � Speciality Chemicals Magazine September 2014 www.specchemonline.com

Herbicides 46.7% ($6.2 billion; +9.1%)

Fungicides 36.2%($4.8 billion; +10.7%)

Insecticides 13.8% ($1.8 billion; +10.6%)

Others 3.3%($430 million; +11.2%)

a bHerbicides 42.5%

Fungicides 41.8%

Insecticides 4.9%Others 10.8%

0 5 10 15 20 25

Barley

Oats

Sorghum

Soybean

Wheat

Corn -65.8%

-82.1%

-69.3%

-80.6%

-75.1%

-75.4%

Yield (103 kg/ha)

Record yield

Abiotic losses

Biotic losses

Average yield

Source - Sumitomo Chemical

Figure 1 – European agrochemicals market by type 2013: Value (a) & volume (b)

Figure 2 – Losses to US crop yield by crop

The R&D-based companies, Uttley and Phillipsnoted, are spending an ever-increasingproportion of their budget on post-launchdevelopment, which mainly equates to cleverstrategies to prolong the lives of their productsbeyond patent expiry. This is just one of thepossible defence strategies against the declinein new AIs that Uttley discussed at length, but,one might argue, the process is tending toreinforce the decline in innovation.

Meanwhile, Bryant continued, the burden ofdiscovery has moved East. Japan and China nowaccount for a disproportionate number of newleads, 19 and 12 respectively in 2009-10, asagainst 13 in the US and ten in Europe. Oneconsequence of this is that insecticides, whichare more important in East Asian climates, havebecome the dominant R&D focus, reaching 28of the 45 new leads in 2009-10.

Meanwhile, the US-based majors have veryfew compounds in development because oftheir emphasis on GM research. (As Phillipsshowed, total R&D on seeds and traits matchedthat on traditional agrochemicals in 2009 andthe gap is growing still, albeit that total researchon both is still climbing.) “However, over-dependence on a limited range of tolerantherbicides has its dangers, as illustrated by theemergence of glyphosate resistance, particularlyin the US,” Bryant said.

Looking at the manufacture of AIs, heobserved, most are still made by majoragrochemicals groups in their own facilities,with only those for older, less importantproducts outsourced. Raw materials andintermediates are usually sourced fromspecialists, the former overwhelmingly fromChina – even India mainly depends on China inthat respect.

“Chemical process innovation is generallylimited to captive groups, which produce‘patent swamps’ to protect technology. Thetrend over the past ten to 15 years has been tofavour toll manufacture over custom synthesis inorder to retain tighter control of the technology.This has led to the dumbing down of the finechemicals industry,” noted Bryant.

Conversely, major agrochemicals companieshave still exposed their key technologies toAsian competition by starting to transfer even

their newest AIs straight to Asia. Bryant citedone new DuPont insecticide.

The company is making 2,000 tonnes of thisin 2014-15, a proportion of which is by twoChinese sub-contractors. Independent Chinesefirms are expected to make a further 750 andthere is also the threat of ‘clone’ factoriesspringing up to compete, as has happenedmany times before. “We’ve just sat back and letit happen,” he said.

Chemical process innovation remains inJapan, where early intermediates and pilotquantities of AI are sourced. Production scale-up mainly takes place in China; indeed, theCCPIA recently claimed that the sales of China’stop 100 agrochemicals companies nearlydoubled from $8 billion in the 2007-8 financialyear to $15.9 billion in 2013-4, with about80% being exported to the US, Europe andJapan.

Uttley separately showed that, through amixture of government sponsorship and the freemarket, the number of Chinese agrochemicalsmakers has boomed to over 2,600 in the pastten years. This has, however, led to oversupply,poor profitability and environmental problems.The Five-Year Plan that runs to the end of 2015envisages big changes to address this.

The numbers of pesticide and AS companiesare both to be reduced by about 30%, with thetop 20 accounting for 50% of sales by 2015and 70% by 2020. The government envisagescreating 20 companies with revenues of >$300million/year and two or three leaders with >$1.5billion/year – hence, in part ChemChina’sacquisition of Makhteshim Agan.

This, it is hoped, will alleviate some of theenvironmental problems that have arisen andlead to development being market-led ratherthan technology-driven, while also giving theworld greater transparency and security ofsupply from China. The big question, in Uttley’sview, is whether China will be able to continueto supply the growing demand for off-patentAIs.

All in all, Bryant said, the European finechemicals industry has been the loser throughall the trends. But is there a better way to makeagrochemicals? Yes, he thought, and preciselybecause of the problems caused by the fine

chemicals industry becoming a cost centre to bemanaged as investor power drove the chemicalsand biosciences industries to consolidate aroundkey products.

“The current problems are clear: too muchcapacity for any given technology, low averageprocess efficiencies, not enough goodengineering solutions being adopted,insufficient ingenuity and too much copying,regulatory ‘locking in’ and not enough timebeing devoted to generating the best processeconomics.”

The European fine chemicals industry is wellpositioned to recover some of what has beenlost, Bryant continued. Convincing customerswill not be easy and change will take a longtime to come but now is as good a time as anyto start. An independent fine chemicals industrycould bring a lot to agrochemicalmanufacturing:� An industry dominated by organic chemists

will continuously develop new and improvedprocesses, because that is what they careabout

� The fruits of cutting costs could be sharedequitably between the industry and itscustomers

� Investors could continue to reap returns atthe finished product stage, reconciling theirshort-term interests with the long-term needsof a capital- and technology-intensiveindustry

� European producers can be relied on torespect IP, because there is real legal redressin Europe against any who do not“As the relative cost advantages enjoyed by

Asian suppliers decrease, European finechemicals companies can emphasise theadvantages of an independent fine chemicalsindustry to their customers,” Bryant said. Theseadvantages are: reliable, local production thatconforms to increasingly stringent regulatorydemands; more efficient and better engineeredprocesses; a reduced environmental load; and,consolidation to avoid unnecessary capitalinvestments.

“The fine chemicals industry is uniquelypositioned to take on the challenge. China andIndia use established technology and have noincentive to change – yet. This is ouropportunity. We still have an education systemthat makes people think. The trouble has beenthat innovation doesn’t pay, nor does being achemist. That has made fine chemicals a mug’sgame.”

However, the European fine chemicalsindustry retains the scale and power to be itsown master again. It should persuade itscustomers to let them manufacture the AIswherever possible, and should also bothconsolidate and reduce its scale to recover itsnecessary dynamism.

The ingenuity of the chemists and engineersshould once again become the determinant ofsuccess. And after all that, “our customersmight again develop a respect for what ourprofession can offer and pay the industryaccordingly”.

� Agrochemical intermediates & actives

14 � Speciality Chemicals Magazine September 2014 www.specchemonline.com

0

50

100

150

200

250

300

2005-820001995

Chemistry

Biology

Toxicology/environmental chemistry

Chemistry

Field trials

Toxicology

Environmental chemistry

Registration

152

184

256

$ m

illio

ns

Development

67

Development

79

Research72

Research94

Development

146Research

85

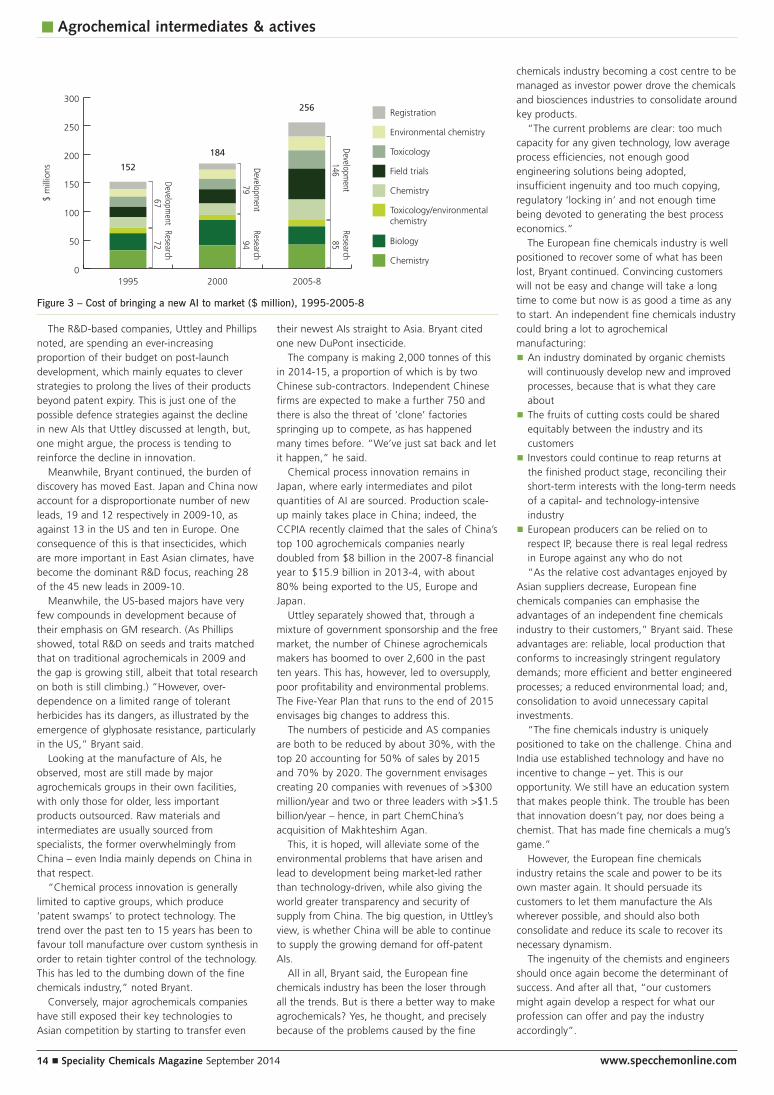

Figure 3 – Cost of bringing a new AI to market ($ million), 1995-2005-8