aif chapter outlines 2015 spring (1)

TRANSCRIPT

You should…..

1) maximize the spreadsheet2) look for the tabs at the bottom of the spreadsheet (tabs, by chapter)3) click on a tab (at the bottom of the spreadsheet)4) print …

2

AIF - Chapter 11 - Time Value of Money - Making Decisions

1) Business decisions - Management Cycle

A) Planning Phase - 1) Conducting Long-Term Planning

2) What are the company's long-term goals?

B) Performing Phase -1) Developing the infrastructure for the company

2) Buying the equipment and resources necessary for the company

C) Control & Evaluation Phase 1) The business leaders are evaluating the past business decisions

2) Major parts of investing

1) Return of Investment vs. Return on Investment

a) Example

Start End

1,000 1,100

1000 100Return of Return on Investment Investment

Dollar Return = 1,100 (1,000) = 100

Rate of Return = Dollar Return = 100 = 10%Original Investment 1,000

A) Return - Measures the performance of an investment

3

B) Risk1) A chance of Loss

a) Receive a lower return than expectedb) Receive a return that eats into your initial investment

2) All individuals have different attitudes towards riska) Risk seekersb) Risk avoiders

3) Different Types of Risk

a) Risk-free rate - rate of return on a virtually riskless investment1) (Short-Term US Government bond)

b) Inflation Risk - a decline in purchasing power due to rising prices1) as prices increase - more money is needed to purchase the same item

c) Business Risk - Risk associated with a specific business1) Example - Walmart vs. Kmart- more business risk associated with Kmart

d) Liquidity Risk - Risk an investment cannot easily be converted into cash1) Example - Selling a house vs. selling 100 shares of IBM

a) selling a house can take months, selling IBM share (seconds)

4) Risk and Return are relateda) As the risk of an investment increases, the require return by the market place increase

1) contrast GAP stock with a short-term US treasury bond

3) Time value of Money

A) Basic concepts - Value of Money

1) Example

Today 1 Year

1

Today 1 Year

1 Which would you rather have????

Dollar todayDollar 1 year from now

4

B) Simple vs. compound Interest

Periods X Rate X principal

a) Simple Interest Example

Periods = 2 yearsRate = 10%principal 1,000

2 X .10 X 1,000 = 200 <=== Simple Interest

b) Simple Interest has NO Compounding

a) Define - Compounding has interest earned on interest

b) Compound Interest Example

Periods = 2 yearsRate = 10%principal 1,000

Year 1: 1,000 X .10 X 1 year = 100Year 2: 1,100 X .10 X 1 year = 110

Total 210 <== Interest Earned

1,000 + 100

3) Application / Decision Making:

a) Which would you rather have:

1) CD earning simple interest?2) CD earning compound interest? < = Answer

b) Which would you rather have:

1) loan with simple interest? < = Answer2) loan with compound interest?

1) Simple Interest -

2) Compound Interest

5

C) Major Time Value of Money Concepts

1) Future Value

a) Define - What will a deposit today be worth in the future?

b) Example - Real-Life Example - Place money in a bank - value after a few years??

c) Example - Use Packet

2) Example

Start 1 2 3

15,000.00 ????

2) Present Value

a) Define - What is the value of a future deposit worth today?

b) Example - Use Packet

2) Example

Start 1 2 3

???? 35,000

3) Future Value of an Ordinary Annuity

a) Annuity - A series of equal payments or deposits

b) Future value of an ordinary annuityStart 1 2 3

100 100 100

Deposits ????

c) Real-Life Example - 401K deposits, creating a "nest egg" for the future

d) Example - Use Packet

1) Spend time on the rate per period and the rate per year.

1) Spend time on the rate per period and the rate per year.

1) Spend time on the rate per period and the rate per year.

6

4) Present Value of an Ordinary Annuity

a) Present value of an ordinary annuityStart 1 2 3

100 100 100

Payment ????

b) Real-Life Examples - CAR LOAN, HOUSE LOAN

c) Example - Use Packet

Parts of this document are the exclusive property of Rodney Vogt.

1) Spend time on the rate per period and the rate per year.

5) Solving for Unknown Values - PACKET EXAMPLE

Those parts are protected by copyright laws (© Rodney Vogt, 2012).

7

AIF - Chapters 12 & 13AIF - Chapter 12 - Business Investment

1) General Chapter Direction

A) We are going to look at different ways to evaluate different investment alternatives.

B) ExampleYes

Invest in a new building No

2) Capital Budgeting

A) Define - Process of acquiring long-term investments

1) Example - Long-term investment - Shop Building

B) Decision Point / Life Application

1) A good business will require the investment to generate a minimum return

C) Uses of Capital Budgeting

1) Expand operations

2) Replace - unproductive and worn-out assets

3) Comply with government regulations

a) example => oil refineries => need to meet government regulations

3) Capital Budgeting Steps

A) Identify long-term investment alternatives

B) Select an Investment

C) Finance the investment

D) Evaluate the investment results

8

4) Select an Investment (Step 3 B - Capital Budgeting Steps)

A) Business investments should generate an acceptable rate of return (minimum return)

B)

1) Define - Cost of Capital - Weighted-average cost of debt and equity for a business

2) Simple Example - Cost of Capital

a) Company has 25,000 debt and 75,000 equityb) Debt rate = 12%c) Equity required rate = 15%d)

25,000 0.25 75,000 0.75 100,000

( .25 X .12) + ( .75 X .15 ) = 0.1425 <= Cost of Capital

Cost of Capital => A Rate / % Weighting => Based on => Total Assets

5) Estimate an investment's profitability => NPV

A) Investment tool = Net Present Value = NPV

B) Big Picture = NPV

1) Start 1 2 3

100 100 100PV - Net Investment CostNPV

What is the present value of the above cash inflows?Compare the cash inflows to the cost of the asset.

Businesses use - Cost of Capital as a minimum return rate

Compute the Cost of Capital

9

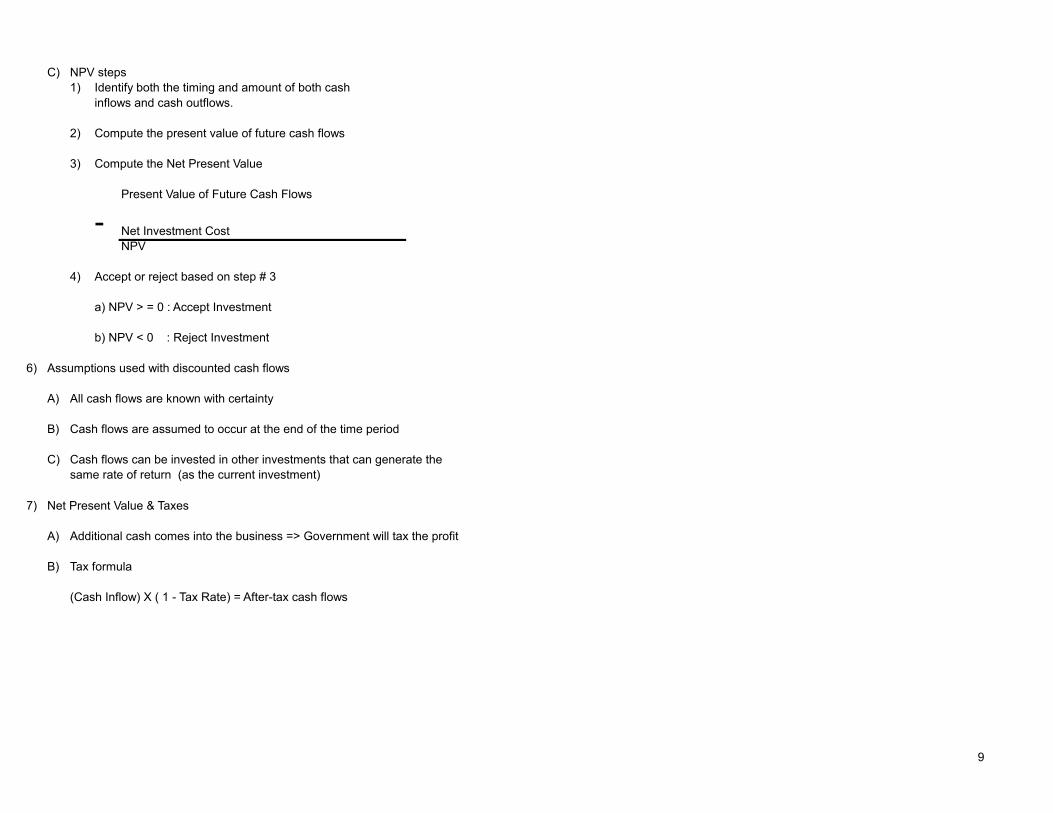

C) NPV steps1) Identify both the timing and amount of both cash

inflows and cash outflows.

2) Compute the present value of future cash flows

3) Compute the Net Present Value

Present Value of Future Cash Flows

- Net Investment CostNPV

4) Accept or reject based on step # 3

a) NPV > = 0 : Accept Investment

b) NPV < 0 : Reject Investment

6) Assumptions used with discounted cash flows

A) All cash flows are known with certainty

B) Cash flows are assumed to occur at the end of the time period

C) Cash flows can be invested in other investments that can generate thesame rate of return (as the current investment)

7) Net Present Value & Taxes

A) Additional cash comes into the business => Government will tax the profit

B) Tax formula

(Cash Inflow) X ( 1 - Tax Rate) = After-tax cash flows

10

C) Taxes & Depreciation Expense

1) Journal entry for Depreciation Expense

Depreciation Expense 100,000 Accumulated Depreciation 100,000

2) The above journal entry will reduce taxes:

a) Depreciation is a tax deduction

3) The above journal entry does not represent a cash outflow

a) NO CASH OUTFLOW

4)

5) Depreciation Expense Example

Corp. A Corp. BIncome before Depr. Expense 200,000 200,000 Depreciation Expense (100,000) (200,000)Taxable Income 100,000 - Taxes ( 30 % tax rate) 30% 30%Tax Expense 30,000 -

6) Summary => Depreciation expense reduces taxable income, shielding a business entity from paying taxes.

D) Taxes ==> Gains & Losses

1) Gains: ==> Selling a piece of equipment

Cost 300Accum. Depr. 200 Book Value = Bal. Sheet ValueBook Value 100Cash Received 110 110Gain 10 Gain: On the Inc. Statement, Adds to Net IncomeTax Rate ( 30 %) 30%Tax Expense 3 -3

After-Tax Cash Flows => 107

Depreciation creates a cash savings = Also called a Tax Shield

Depr. Expense shields the company from paying taxes

11

12

2) Losses: ==> Selling a piece of equipment

Cost 300Accum. Depr. 200 Book Value = Bal. Sheet ValueBook Value 100Cash Received 90 90Loss -10 Loss: On the Inc. Statement, decreases Net IncomeTax Rate ( 30 %) 30%Tax Savings -3 3

After-Tax Cash Flows => 93

a) The deduction will reduce taxes (create a tax savings), but no cashoutflow will be generated

E) Use Tax Packet Example

AIF - Chapter 13 - Planning for Equity Financing

1) Equity Financing & Debt Financing

A) Rewards of Equity Financing

1) Generate a return on your equity investment

2)

B) Risks of Equity Financing

1) Not receiving a good return

a) Expect a 15% return, only receive 5%

2) Receive a negative return

a) Receive a return that eats into your investment Receive less than your initial investment (end of investment)

C) Rewards of Debt Financing

1) Financial Leverage - Reward of Debt Financing

a) Define - Financial leverage occurs when the return from borrowed funds is greater than the

Psychological (ego) Reward - I own a business

13

cost of borrowed funds.

D) Risk of Debt Financing

1) Financial Risk - the chance a company might default on its debt obligations

2) Equity Financing => Sole Proprietorship & Partnerships

A) Disadvantage - Unlimited liability - liability extends beyond the business, personal wealth can be taken (beyond the business wealth)

B) Disadvantage - hard to raise large amounts of capital

C) Advantage - Easy to form

D) Advantage - Income is only taxed once - No double taxation(pass-through entity, no tax at the business entity level)The net income will be taxed (passed to) on the individual'stax return.

E) Sole Proprietorships & Partnerships - use an account called - Capital

1)

a)b)c)d)

1) withdrawals are like dividend payments of a corporation

Capital account represents the owner's equity placed into the business

Owner's Capital is increased by contributions <==assets placed into the businessOwner's Capital is increased by any net incomeOwner's Capital is decreased by any net lossOwner's Capital is decreased by any withdrawals

14

3) More on Partnerships

A) Division of Partnership Income (ways to divide net income & net loss)

1) Fixed Ratio2) Ratio of Capital Balances3) Salary & Interest Allowance4)

B) Division of Partnership Net Income or Net Loss

1) Net Income Examplea) Capital balances - Beginning Balances

Partner A 40,000 0.40 Partner B 60,000 0.60

100,000 ======> Partnership Agreement

b) Partner A => Receives a 10,000 salary

c) Each partner receives a 5% interest allowance based onthe beginning capital balance of each partner.

d) Any remainder should be split based on a 2:1 ratio (Partner A = 2)

e) Solve based on a Net Income = $25,000

Partner A Partner B Bal.Beg. Balance 25,000 Salary Allowance 10,000 15,000 5% Interest Allowance 2,000 3,000 10,000 Remainder 6,667 3,333 -

18,667 6,333 < ===Amount added to each partner's capital account BB 40,000

0.05 2,000

RemainderBB 60,000 Partner A 2 66.67%

0.05 Partner B 1 33.33% 10,000 3,333 3,000 3

Divide the Remainder

15

f) Solve based on a Net Loss = $ (12,000)

Partner A Partner B Bal.Beg. Balance (12,000)Salary Allowance 10,000 (22,000)5% Interest Allowance 2,000 3,000 (27,000)Remainder (18,000) (9,000) -

(6,000) (6,000) < ===Amount subtracted from each partner's capital account BB 40,000

0.05 2,000

RemainderBB 60,000 Partner A 2 66.67%

0.05 Partner B 1 33.33% (27,000) (9,000) 3,000 3

4) Equity Financing => C Corporations

A) Characteristics of Corporation Equity

1) Advantage (limited liability) - An investor can only loose his or her investment (not personal property)=> True for => minority shareholders=> Major stockholders can be liable for their decisions

2) Advantage - Corporations can raise large amounts of capital (easier than sole proprietorships & partnerships)

3) Advantage - Unlimited Life - Use IBM Example

a) exchange of share ownership does not end the life of a corporation

4)

a) Dividend Example

1) Corporation has earnings => taxed on the earnings => Corporation pays a dividend => Individual shareholder pays a tax on the dividend

2) The above example shows the disadvantage of double taxation

Disadvantage - Double taxation

16

5) Equity Financing => C Corporations => Types of Stock

A) Characteristics of Common Stock

1) Right to vote (major events & board of directors)2) Right to sell shares of stock3) Preemptive Right - Existing shareholders have first right to purchase the newly issued shares

Who Cares??? = If existing shareholders do not purchase the newly issued shares, the existing shareholders will have reduced voting power.

4) Right to share in any dividends5) Right to share in any liquidation

a) Common shareholders are usually last in line to receive assets of the corporation in the event ofa bankruptcy.

B) Characteristics of Preferred Stock

1) Preferred stock has special characteristics

a) P/S is paid first on any dividends declared (vs. common stock)b) P/S is paid first on any liquidation (paid before common shareholders (bankruptcy issue))c) P/S usually has no voting say in the company (no say in the management of the business)

2) Cumulative P/S

a) Cumulative P/S

2) Use ==> Dividend in Use ==> Dividend in Arrears Example ==> Packet

1) Unpaid P/S dividends are called ==> Unpaid P/S dividends are called ==> Dividends in Arrears

17

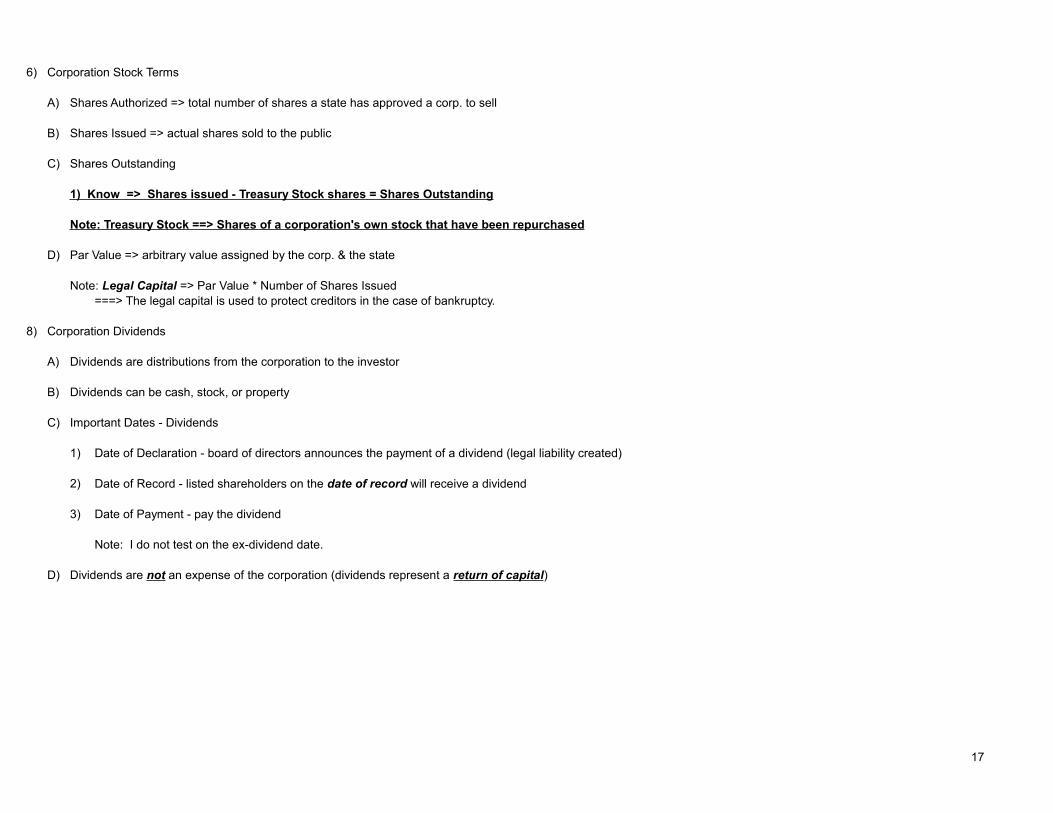

6) Corporation Stock Terms

A) Shares Authorized => total number of shares a state has approved a corp. to sell

B) Shares Issued => actual shares sold to the public

C) Shares Outstanding

1) Know => Shares issued - Treasury Stock shares = Shares Outstanding

Note: Treasury Stock ==> Shares of a corporation's own stock that have been repurchased

D) Par Value => arbitrary value assigned by the corp. & the state

===> The legal capital is used to protect creditors in the case of bankruptcy.

8) Corporation Dividends

A) Dividends are distributions from the corporation to the investor

B) Dividends can be cash, stock, or property

C) Important Dates - Dividends

1) Date of Declaration - board of directors announces the payment of a dividend (legal liability created)

2)

3) Date of Payment - pay the dividend

Note: I do not test on the ex-dividend date.

D)

Note: Legal Capital => Par Value * Number of Shares Issued

Date of Record - listed shareholders on the date of record will receive a dividend

Dividends are not an expense of the corporation (dividends represent a return of capital)

18

9) Stock Splits

A) General logic (Stock Splits)

1) Reduce the price of the stock (more people can purchase

===> Increasing the Liquidity (of the stock) => increase the ease of buying or of selling the stock

===> Berkshire Hathaway Example

B) Stock splits require no journal entries

1) A memorandum entry should be made to record the stock split

C) Stock splits and par value

1) Stock splits reduce the par value proportionately

D) Stock splits increase the # of shares outstanding

E) Stock Split Example

1) Before the stock splita) 2 for 1 stock splitb) 100,000 shares outstandingc) Par value = $ 10.00 per shared) Market Value = $100.00 per share

2) After the stock splita) 200,000 shares outstandingb) Par value = $ 5.00 per share ($10.00 /2)c) Market Value = $50.00 per share ($100.00/2)

the stock at a lower price (increase the liquidity of the stock))

19

10) S Corporation & Limited Liability Company (LLC)

A) Characteristics - S Corporation

1) Limited Liability - provides protection against personal weath attacts

2) Only 100 shareholders allowed

3) All shareholders must be United States citizens.

4) Class of Stock ==> only one class

5) Minutes must be taken each year (more paper work vs. LLC)==> formal meetings required

6) More liability protection across different states (doing business in many states)==> An S Corp. provides more liability protection across states vs. an LLC

7) S Corporation ==> is a pass-through entity==> Income taxed at individual taxpayer level (not business entity level)

B) Characteristics - Limited Liability Company (LLC)

1) Limited Liability (best limitations on liability within one state)==> Limited Liability - provides protection against personal weath attacts

2) Less paperwork vs. S Corporation / C Corporation

3) An LLC ==> is a pass-through entity==> Income taxed at individual taxpayer level (not business entity level)

Parts of this document are the exclusive property of Rodney Vogt. Those parts are protected by copyright laws (© Rodney Vogt, 2012).

20

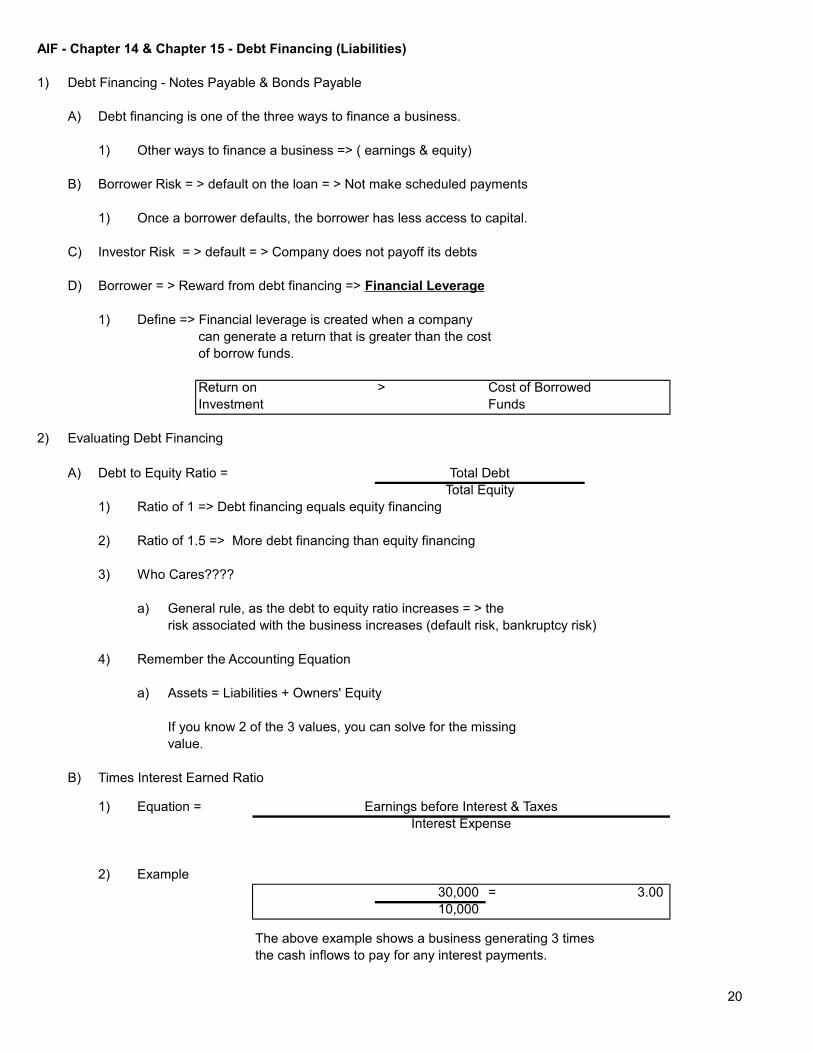

AIF - Chapter 14 & Chapter 15 - Debt Financing (Liabilities)

1) Debt Financing - Notes Payable & Bonds Payable

A) Debt financing is one of the three ways to finance a business.

1) Other ways to finance a business => ( earnings & equity)

B) Borrower Risk = > default on the loan = > Not make scheduled payments

1) Once a borrower defaults, the borrower has less access to capital.

C) Investor Risk = > default = > Company does not payoff its debts

D)

1) Define => Financial leverage is created when a company can generate a return that is greater than the cost of borrow funds.

Return on > Cost of BorrowedInvestment Funds

2) Evaluating Debt Financing

A) Debt to Equity Ratio = Total DebtTotal Equity

1) Ratio of 1 => Debt financing equals equity financing

2) Ratio of 1.5 => More debt financing than equity financing

3) Who Cares????

a) General rule, as the debt to equity ratio increases = > therisk associated with the business increases (default risk, bankruptcy risk)

4) Remember the Accounting Equation

a) Assets = Liabilities + Owners' Equity

If you know 2 of the 3 values, you can solve for the missing value.

B) Times Interest Earned Ratio

1) Equation = Earnings before Interest & TaxesInterest Expense

2) Example 30,000 = 3.00 10,000

The above example shows a business generating 3 times the cash inflows to pay for any interest payments.

Borrower = > Reward from debt financing => Financial Leverage

21

General Rule: As the times interest ratio goes up, the firm is in a better position to payoff creditors.

3) Debt Financing Terms

A) Note - Written promise to payoff a liability

1)

B) Covenants - Restrictions placed on the borrower

1) Why important???a) Example - A typical covenant might restrict the payment of dividends

of a borrower. Why??? A borrower might payout all the assets, then tell the debt investors there are no assets to payoff the debt investors (lenders).

C) Cash Proceeds - The amount of money received by the borrower.

D) Market Rate of Interest (also called yield, market, & effective rate)

1) The current market rate demanded by the market place (set by the market place)

E) Face Rate - Interest rate printed on the face of the note or bond.

4) Sources of debt financing

A) Nonpublic Sources - A business borrows from individuals or from institutions (like insurance companies)

B) Public Sources - A business borrows by issuing debt to the public (Example =>Chicago Board of Trade)

1) Corp. bonds then can be traded

5) Types of Notes & Bonds:

A)

1) Series of equal repayments

2) Each payment includes interest & principal

3) Examples - Real Life - Car Payments & House Payments

4) Installment Note # 1 in Packet

a) Interest Expense - Jan - June 20X4

10,000.00 0.05 <==== .10 / 2 500.00 Interest Expense

Note Maker - the person or business entity borrowing resources ( the Maker is borrowing resources)

Installment Note (only one interest rate used (market)):

22

b) Principal reduction after first payment

Cash Pmt - Interest Exp. = 2,820.08 (500.00) 2,320.08

c) Calculate the interest expense July - Dec. 20X4

7,679.92 < === 10,000.00 - 2,320.08 0.05 <==== .10 / 2 384.00 Interest Expense

5) Recording an Installment Note

a) Issuing the installment note

Cash 10,000.00 Notes Payable 10,000.00

b) Interest Payments - First Year ( 2 periods)

Interest Expense - Jan - June 20X4

Interest Expense 500.00 Notes Payable 2,320.08

Cash 2,820.08

Interest Expense July - Dec. 20X4

Interest Expense 384.00 Notes Payable 2,436.08

Cash 2,820.08

Interest Expense 500.00 384.00

Dec. 20X4 Bal. => 884.00

Notes Payable 10,000.00

2,320.08 2,436.08

Dec. 20X4 Bal. => 5,243.84 <== Carrying Value for the B/S

Reduction in Note Payable

Record the Cash Proceeds from an Installment Note

23

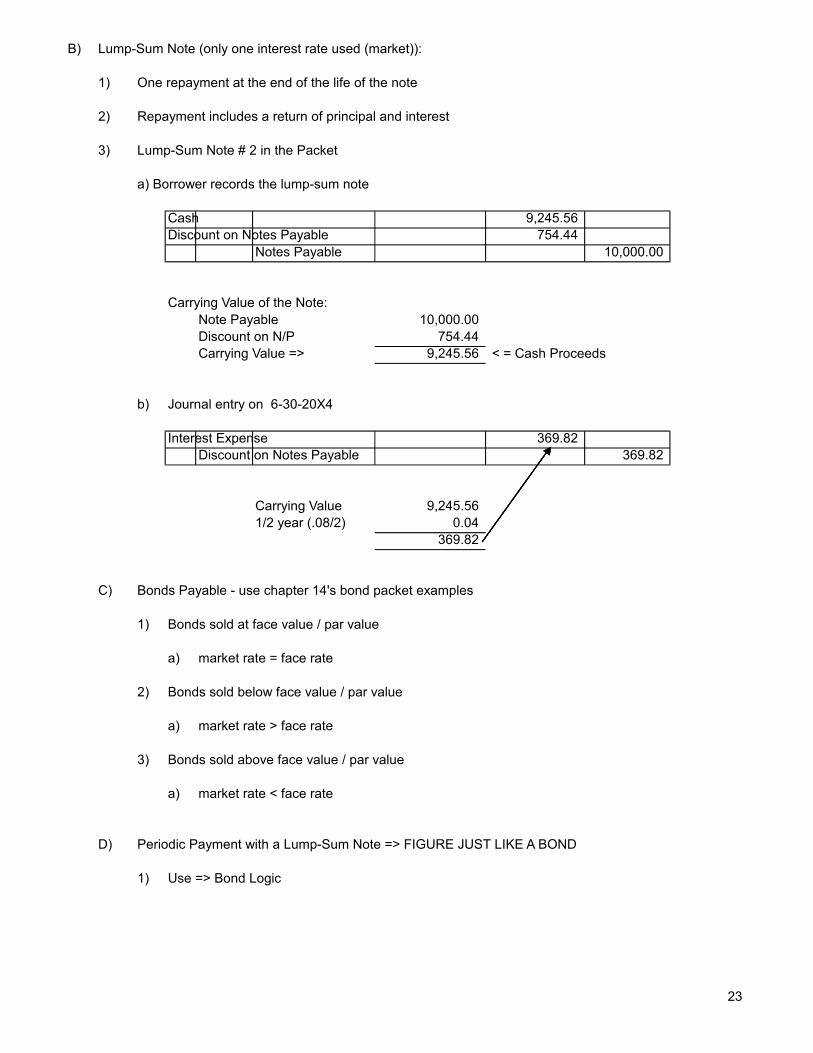

B) Lump-Sum Note (only one interest rate used (market)):

1) One repayment at the end of the life of the note

2) Repayment includes a return of principal and interest

3) Lump-Sum Note # 2 in the Packet

a) Borrower records the lump-sum note

Cash 9,245.56 Discount on Notes Payable 754.44

Notes Payable 10,000.00

Carrying Value of the Note:Note Payable 10,000.00 Discount on N/P 754.44 Carrying Value => 9,245.56 < = Cash Proceeds

b) Journal entry on 6-30-20X4

Interest Expense 369.82 Discount on Notes Payable 369.82

Carrying Value 9,245.56 1/2 year (.08/2) 0.04

369.82

C) Bonds Payable - use chapter 14's bond packet examples

1) Bonds sold at face value / par value

a) market rate = face rate

2) Bonds sold below face value / par value

a) market rate > face rate

3) Bonds sold above face value / par value

a) market rate < face rate

D) Periodic Payment with a Lump-Sum Note => FIGURE JUST LIKE A BOND

1) Use => Bond Logic

24

6) Leases

A) Define - An agreement to transfer use of property from one party to another party.

B) Lease Terms

1)

2)

C) Types of Leases

1)

a) Example - Rent a piece of equipment from True Value

b) Recording an operating lease

1) Lease Expense (rent) XXCash XX

Only pay for use, no ownership interest by lessee (like rent expense)

2)

Lessee - Buyer - Property transferred to ==> Lessee

Lessor - Seller - Property transferred from ==> Lessor

Operating Lease - Lessor / seller retains a substantial interest in the property

Capital Lease - Lessee / Buyer acquires a substantial interest in the leased property

25

7) More on discounts & premiums

A)0.15 0.10

1) Par value / Face value of Bond or Note = $1,000, then the company will receive less than $1,000

B)0.08 0.15

1) Par value / Face value of Bond or Note = $1,000, then the company will receive more than $1,000

C)0.05 0.05

1) Par value / Face value of Bond or Note = $1,000, then the company will receive $1,000.

D) Student Examples - Bonds

1) Borrower sets the face rate = 10% Sell to B

Try to sell bonds to public

2) Borrower sets the face rate = 17%Sell to A

Try to sell bonds to public

3) The above examples show that the borrower will always pay the market rate. The borrower should alwayspay the market rate (independent of the face rate).

8) Collateral => Assets used to secure a loan

9) Liabilities & Cash Flow Timing

A) A business needing a short-term loan to finance an inventory purchase might use a short-term installment note to finance the inventory.

B) A business needing to purchase a long-termasset (a building) might issue long-term bondsto finance the long-term asset purchase.

C) A business leader should evaluate the timing of benefits (cash received) against the cash paymentsrequired by the liability.

Market Rate > Face Rate ==> Bond or note sold at a discount

Market Rate < Face Rate ==> Bond or note sold at a premium

Market Rate = Face Rate ==> Bond or note sold at a face value (par value)

Investor A wants a 15% Return

Investor B wants a 13%

Return

CFO will sell to investor B => at a discount

Investor C wants a 13% Return

Investor D wants a 15%

Return

CFO will sell to investor A => at a premium

26

Parts of this document are the exclusive property of Rodney Vogt.

Those parts are protected by copyright laws (© Rodney Vogt, 2012).

27

AIF - Chapter 15 - Recording & Communicating Equity Financing Activities

1) Sole Proprietorship & Partnerships

A) Review

1)

2)

a)b)c)d)

1) withdrawals are like dividend payments of a corporation

B) Partnership Equity Transactions - Packet & See Web site

2) Corporate Equity Transactions

A) Par Value - Legal capital of the corporation

1) The par value is the minimum price a stock should be sold forat its initial public offering (IPO).

2) If a share of stock is sold below the par value during the IPO, then the shareholderbecomes liable for the difference between the par value and the market value.

3) Both Common & Preferred Stock can have par values

B) Additional paid-in capital, excess of par value

1) Add. PIC is used to record value received beyond the par value of the stock

C) No par stock, without a stated value (will not use the account Add. PIC )

An owner has a capital account

The Capital account represents the owner's equity placed into the business

Owner's capital is increased contributions (into the business)Owner's capital is increased by any net incomeOwner's capital is decreased by any net lossOwner's capital is decreased by any withdrawals

28

D) Par Value Stock Example

1) Common Stock, Par value per share = $ 1.00 2) 50,000 shares issued 50,000 3) Market Price per share = $ 10.00

Journal entry = issuer / seller of stock

Cash 500,000 Asset +Common Stock 50,000 OE +Add. PIC - C/S 450,000 OE +

50,000 shares X $10.00

50,000 shares X $1.00

500,000 (50,000) 450,000 Add. PIC - C/S

Total Increase in OE => 500,000

3) Corporate Earnings

A) Retained Earnings - A corporation's earnings flow into an account called retained earnings.

Retained EarningsNormal Bal. Beg. Bal.

Net Loss Net Income

normal credit bal.

B) Quick Review

1) Revenues & Gains - Expenses & Losses > 0 ===> Net Income

2) Revenues & Gains - Expenses & Losses < 0 ===> Net Loss

C) Chapter 15 packet information on closing entries

1) Go over the closing entries featured in the AIF packet

Dividends Declared

29

4) Treasury Stock

B) Example ==> Apple Corp. buys back Apple Corp. stock

C) More on treasury stock

1) Treasury stock is NOT an asset of the corp.

2) Treasury stock is found in the stockholders' equity section of the balance sheet.

3) Treasury stock reduces stockholders' equity

4) Treasury stock reduces the number of shares outstanding

D) Example - treasury stock

1) IBM buys its own stock back at $1002) # of shares purchased = 5,000

Make the journal entry to record the treasury stock transaction

Treasury Stock 500,000 Cash 500,000

5,000 share X $100

3) Treasury Stock 500,000

What is the normal balance in most stockholders' equity accounts? ===> Credit Balance, notice treasury stock has a debit balance

4) =========> Treasury Stock Beg. Bal.

5)6) Contra-equity account

A) Define => treasury stock => Company / corporation buys back its own stock

+ Purchases (at cost)

Sales (at cost)

Use the PACKET EXAMPLE for treasury stock

30

5) Stock Splits

A) General logic (Stock Splits)

1) Reduce the price of the stock, more people can purchase the stock at a lower price

===> Berkshire Hathaway Example

B) Stock splits require no journal entries

1) A memorandum entry should be made to record the stock split

C) Stock splits and par value

1) Stock splits reduce the par value proportionately

D) Stock splits increase the # of shares outstanding

E) Stock Split Example

1) Before the stock splita) 2 for 1 stock splitb) 100,000 shares outstandingc) Par value = $ 10.00 per shared) Market Value = $100.00 per share

2) After the stock splita) 200,000 shares outstandingb) Par value = $ 5.00 per share ($10.00 /2)c) Market Value = $50.00 per share ($100.00/2)

6) Recording Corp. Dividends - Corporation

A) Date of Declaration

Dividends Declared or Retained Earnings 1,000 Dividends Payable 1,000

B) Date of Record

NO ENTRY REQUIRED

C) Date of Payment

Dividends Payable 1,000 Cash 1,000

D) Dividends should be based on the number of shares outstanding.=> Shares Outstanding = Shares issued - Treasury Stock Shares

31

7) Stock Dividend (Small => Under 20%)

A) Stock Dividend => Purpose => Conserve Resources (assets)

B) Small Stock Dividend => Under 20% of the => shares outstanding

C) Small Stock Dividend => Example

InformationA) Shares Outstanding (Common Stock) => 100,000B) 2% Stock Dividend Declared (June 15, 20X7)C) Market Rate => Date of Declaration => $50 Per ShareD) Date Issued (the shares) => July 1, 20X7E) Par Value Per Share => $ 10

F) Solve

June 15, 20X7 => DeclarationDebit Credit

Retained Earnings 100,000 < =(100,000*.02)*50Stock Dividends Distributable - C/S 20,000 < =(100,000*.02)*10Add. PIC - C/S 80,000 <= Plug

July 1, 20X7 => Date Issued (Common Stock)Debit Credit

Stock Dividends Distributable - C/S 20,000 Common Stock 20,000

Stock Div. Dist. - C/SDate Issued ===> 20,000 20,000 <= Declaration

The below account is a permanent account (balance sheet account) thatwill hold the par value of the common stock shares until the common stockshares are issued.

Account => Stock Dividends Distributable - C/S

Parts of this document are the exclusive property of Rodney Vogt.

Those parts are protected by copyright laws (© Rodney Vogt, 2013).

32

AIF - Chapter 16 - Operational Assets

1) Accounting Equation Assets = Liabilities + Owners' Equity

PP & E Equipment / BuildingsXXX

Accumulated Depr. Depreciation ExpenseXXX XXX

LandXXX NO DEPRECIATION EXP

Patents Amortization ExpenseIntangible Assets XXX XXX

Natural Resources MinesXXX

Depletion creates Inventory Inventory Cost of Goods Sold

XXX XXX

Customer picks up the ore,then the inventory becomes anexpense (cost of goods sold).

2) Property, Plant, & Equipment

A) Balance Sheet Presentation

Equipment 10,000 Less: Accumulated Depr. 7,000

3,000

Value found on the balance sheet

Also called==>Book Value, Carrying Value, &Remaining Undepreciated Cost

33

B) Assets found in PP & E

1) Land - Not depreciated

2) Buildings

3) Equipment

C) PP & E assets are viewed as long-term assets (benefit more than one accounting period)

D) Acquiring PP & E

1)

2) Other items added to PP & E

a) Sales tax

b) Setup costs

c) Freight

d) Key - The capitalized asset should include all costs necessary to getthe asset ready for its intended use.

3)

a) Company buys a drill press for the shop = invoice price = $10,000

b) Sales tax for drill press = $800

c) Freight to get the drill press to the shop = $ 500

d) Necessary setup charges = $ 200

e) Solve for Capitalized Cost

Invoice Price 10,000 Sales Tax 800 Freight 500 Setup Charges 200

Capitalized Cost 11,500

Starting point for depreciationCost placed on the balance sheet, before any depreciation expense (taken)

4) Items that should NOT be capitalized (generally)

---> property taxes paid each year, insurance paid each year, & other recurring items ---> items not part of the asset acquisition should not be capitalized

PP & E assets are capitalized - placed on the balance sheet, not expensed all at once (used in the business, NOT FOR RESALE (not inventory))

Capitalized Cost example - PP & E ( Buildings & Equipment )

=> items that are recurring in nature are generally not capitalized

34

5)

a) Land is part of the PP & E balance sheet category (must be used in the operations of the business)

b) Land is NOT depreciated

c) Items included in the cost of land

1) Invoice / purchase price of the land

2) Costs to clear the land for its intended use

3) Real estate fees & closing cost fees

4) Key - The capitalized asset should include all costs necessary to getthe asset ready for its intended use.

6) Capital Expenditure Vs. Revenue Expenditure

a)

1) Examples - PP& E, Intangible Assets, and other Long-Term Assets

2) Capitalized Cost - Generally found on the balance sheet

b)

1) Example ==> Salary of an office worker

2) An expense is created

Office Salaries Expense 850Cash 850

Capitalized Cost example - PP & E ( Land)

Capital Expenditure - the expenditure's benefits extend beyond the current period

Revenue Expenditure - the expenditure's benefits do not extend beyond the current period

35

3) PP & E , Matching Principle & Depreciation Expense

A) Matching Principle - Accrual accounting tries to match the benefits (revenues generated) with the expenses that created the benefits.

1) Assets used ==> benefits receivedMatch => benefits with => expenses (use)

B) Recognize Depreciation Expense

Depreciation Expense 500Accumulated Depreciation 500

1) Depreciation Expense => Reduces Net Income

2)

3)

Accumulated Depr.XXX

Not closed - balance sheet account

C)

4) Depreciation Calculations

A) Factors impacting the depreciation calculation

1) Capitalized cost of the asset (not an estimate)

2) Estimated useful life

a) Useful life is impacted by:

1) Physical wear & tear

2) Obsolescence - (Example) - the obsolescence of computers (quickly worth nothing)

3) Estimated Salvage Value / Residual Value

4) Depreciable Cost

a)

Depreciation Expense => Is Not a cash outflow

A credit to Accumulated Depreciation reduces total assets

Contra Asset

The recording of depreciation is not an attempt to measure fairmarket value. Depreciation is just the systematic allocation ofthe cost of an asset over the life of the asset (book value not equal to FMV).

Depreciable cost = Capitalized Cost of the asset - Salvage Value of the asset

36

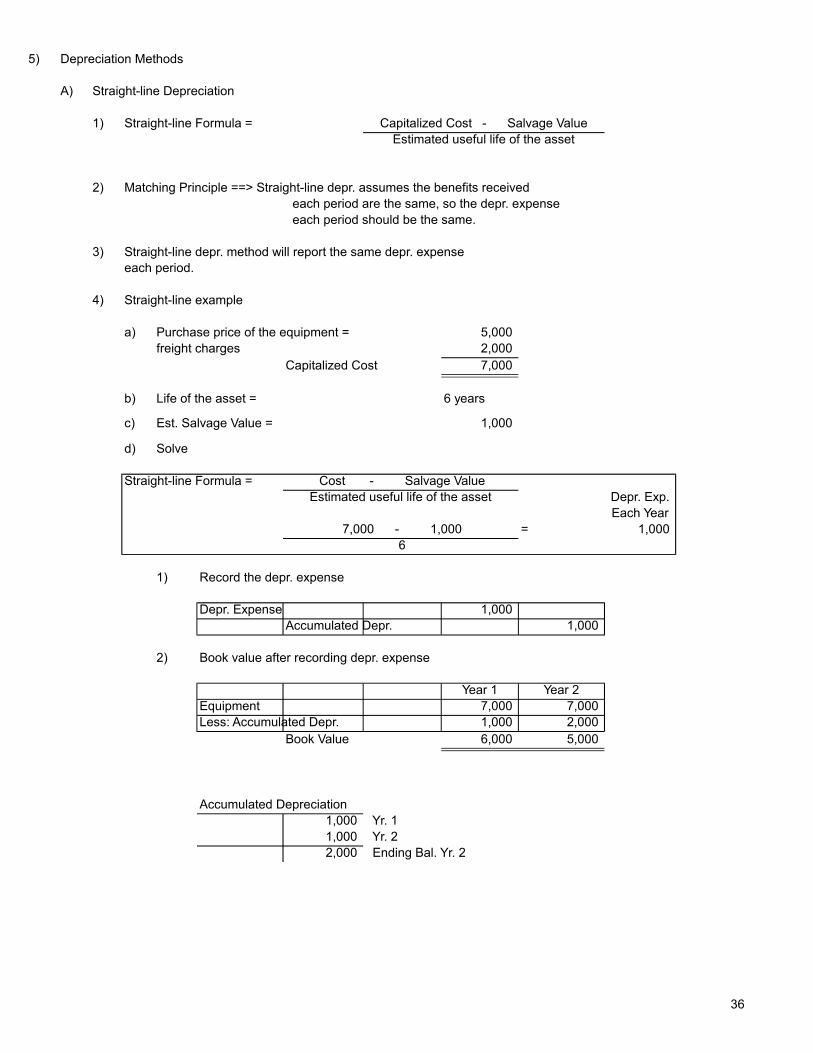

5) Depreciation Methods

A) Straight-line Depreciation

1) Straight-line Formula = Capitalized Cost - Salvage ValueEstimated useful life of the asset

2) Matching Principle ==> Straight-line depr. assumes the benefits received each period are the same, so the depr. expense each period should be the same.

3) Straight-line depr. method will report the same depr. expenseeach period.

4) Straight-line example

a) Purchase price of the equipment = 5,000 freight charges 2,000

Capitalized Cost 7,000

b) Life of the asset = 6 years

c) Est. Salvage Value = 1,000

d) Solve

Straight-line Formula = Cost - Salvage ValueEstimated useful life of the asset Depr. Exp.

Each Year7,000 - 1,000 = 1,000

6

1) Record the depr. expense

Depr. Expense 1,000 Accumulated Depr. 1,000

2) Book value after recording depr. expense

Year 1 Year 2Equipment 7,000 7,000 Less: Accumulated Depr. 1,000 2,000

Book Value 6,000 5,000

Accumulated Depreciation 1,000 Yr. 1 1,000 Yr. 2 2,000 Ending Bal. Yr. 2

37

B) Units-of-Production

1) Units-of-Production formula = Capitalized Cost - Salvage ValueEstimated output

can be hours, units produced, miles, and any other output measure

2) 2 steps for figuring ==> units-of-production

a) Step 1: Figure ==> Depr. expense per unit of output (see above formula)

b)

3) Units-of-Production example

a) Purchase price for equipment 8,000 Sale Tax for equipment 2,000

Capitalized Cost 10,000

b) Salvage Value = 1,000

c) Actual hours worked the first year = 8,000

d) Actual hours worked the second year = 10,000

e) Estimated hours of output from the machine 100,000

Units-of-Production = Cost - Salvage Value Per unit of output Estimated Output

Exp. Per HourStep 1: 10,000 - 1,000 = 0.090

100,000

Step 2: Figure ==> Depreciation Expense = Depr. expense per unit X Actual Output

Depr. Expense = .09 X 8,000 hours the first year = 720

1) Record the depr. expense

Depr. Expense 720 Accumulated Depr. 720

2) Book value after recording depr. expense

Year 1 Year 2Equipment 10,000 10,000 Less: Accumulated Depr. 720 1,620

Book Value 9,280 8,380

Accumulated Depr. 720 Year 1

900 year 2 10,000 X .09 1,620

3) Matching Principle ==> Units-of-production method assumes depr. expense is a function of use (benefits received from use). As a company uses the asset, the asset's value should decrease do to the use / wear and tear. (match benefits with expenses)

Step 2: Figure ==> Depreciation Expense = Depr. expense per unit X Actual Output

38

C) Double-Declining Balance (DDB)

1)

a) More depreciation is taken in the earlier years of the asset's life

b) Matching Principle ==> DDB assumes more benefits will be received in the earlier years of anasset's life. Since more benefits are produced in the earlieryears of an asset's life, more depreciation expense should be matched with the earlier years.

c) Real-life examples

1) Car ==> A car's value will decrease faster in the first few years of a car's life.

2) Computer => A computer's value will decrease faster in the first few years of a computer's life.

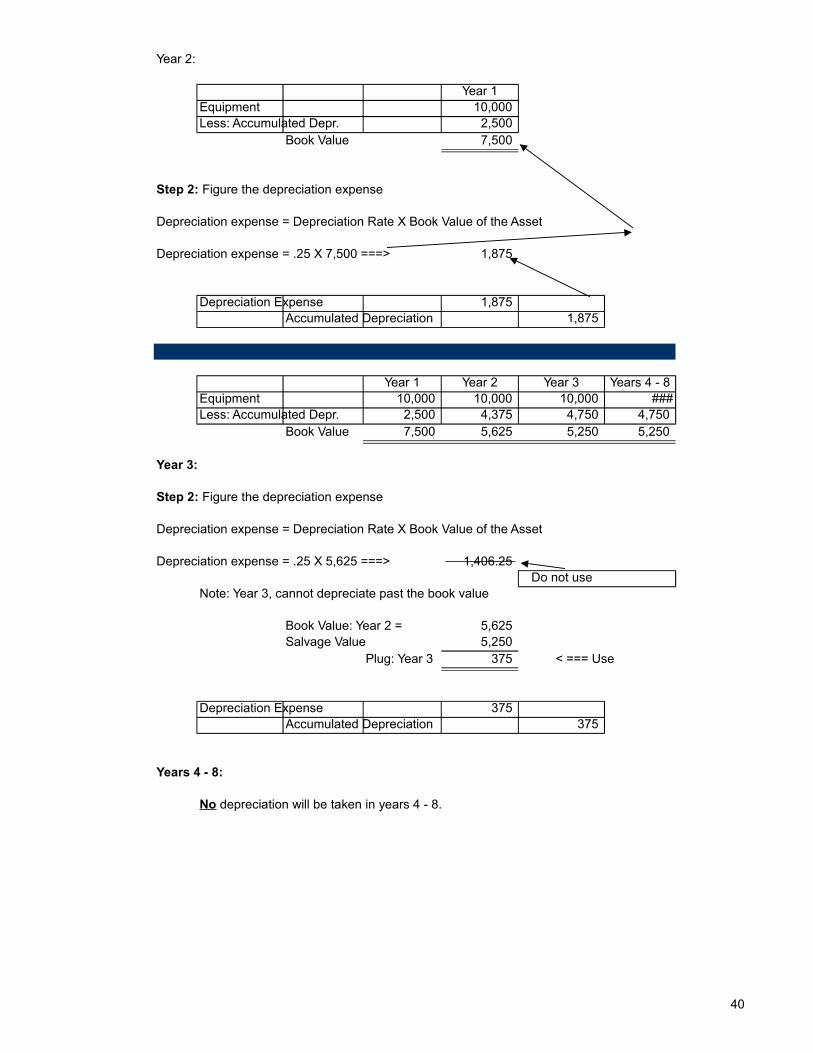

2) DDB Calculation

a)

Depreciation rate = ( 1 / estimated useful life of the asset ) X 2

b) Step 2: Figure the depreciation expense

Depreciation expense = Depreciation Rate X Book Value of the Asset

equals the capitalized cost of the asset (starting point).

c)equals the salvage value, stop the DDB depreciation expense process.

d) DDB Example

Asset Purchased, January 1, 20X5Asset's capitalized cost = 10,000 Salvage Value 5,250 Est. Life of the Asset 8 Year

Depreciation rate = ( 1 / estimated useful life of the asset ) X 2

Depreciation Rate = ( 1 / 8) * 2 =====> 0.25

Depreciation expense = Depreciation Rate X Book Value of the Asset

Depreciation expense = .25 X 10,000 ===> 2,500

Note: First year: Book Value equals cost

Depreciation Expense 2,500 Accumulated Depreciation 2,500

Double-Declining Balance is an accelerated depreciation method

Step 1: Figure the depreciation rate

Note: Look at the starting point for the first year. The book value

Do not depreciate more than the depreciable cost. Once the book value

Step 1: Figure the depreciation rate

Step 2: Figure the depreciation expense

39

40

Year 2:

Year 1Equipment 10,000 Less: Accumulated Depr. 2,500

Book Value 7,500

Depreciation expense = Depreciation Rate X Book Value of the Asset

Depreciation expense = .25 X 7,500 ===> 1,875

Depreciation Expense 1,875 Accumulated Depreciation 1,875

Year 1 Year 2 Year 3 Years 4 - 8Equipment 10,000 10,000 10,000 ###Less: Accumulated Depr. 2,500 4,375 4,750 4,750

Book Value 7,500 5,625 5,250 5,250

Year 3:

Depreciation expense = Depreciation Rate X Book Value of the Asset

Depreciation expense = .25 X 5,625 ===> 1,406.25 Do not use

Note: Year 3, cannot depreciate past the book value

Book Value: Year 2 = 5,625 Salvage Value 5,250

Plug: Year 3 375 < === Use

Depreciation Expense 375 Accumulated Depreciation 375

Years 4 - 8:

Step 2: Figure the depreciation expense

Step 2: Figure the depreciation expense

No depreciation will be taken in years 4 - 8.

41

3) Double-Declining Balance - Other

There is a quick way to figure the DDB method.=> formula (life = 8 years, capitalized cost = $10,000)

(1/8)*2 = .25 (the depreciation rate)

BB PPE item * ( 1 - Depr. Rate) = EB PPE item

The change in the net value of the PPE item will be the depreciation expense recorded for the period.

=> example (using the DDB example numbers)

Period # 1: $ 10,000 * ( 1 - .25) = $ 7,500

Period # 2: $ 7,500 * ( 1 - .25) = $ 5,625

Depr. Exp.Period # 1: BB PPE Item: $ 10,000 $ 2,500 Period # 1: EB PPE Item: $ 7,500

Depr. Exp.Period # 2: BB PPE Item: $ 7,500 $ 1,875 Period # 2: EB PPE Item: $ 5,625

42

6) Disposal of PP & E

A) Step 1: Make sure depr. expense has been updated to the point of sale

B) Step 2: Record the Sale

C) Disposal of PP & E - Example

1) Equipment is sold on June 30th, 20X12) Straight-line depreciation each year = $ 2,0003) Capitalized Cost of the Equipment = $ 20,0004) Asset was sold for ==> $ 9,0005) Accumulated Depreciation = $ 12,000

Equipment 20,000

Accumulated Depr. 12,000 Past depr. recorded 1,000 January 1, 20X1 - June 30, 20X1 13,000

Cost 20,000 Accumulated Depr. 13,000 Book Value 7,000 Cash Received 9,000 Gain on Sale of Equip. 2,000

Step 1: Update Depr.

Depreciation Expense 1,000 Accumulated Depreciation 1,000

2,000 X 1/2 a year

Step 2: Record the sale of the asset

Cash 9,000 Accumulated Depreciation 13,000

Equipment 20,000 Gain on Sale of Equip. 2,000

43

7) Natural Resources

A) Examples of Natural Resources

1) Coal

2) Gold Mine

3) Oil

B) Formula for Depletion = Cost - Salvage ValueEstimated units of Natural Resources

C) Depletion ==> Creates ==> Inventory

44

8) Intangible Assets & Amortization Expense

A) Intangible Assets ==> have no physical substance

B) Intangible Asset Examples

1) Goodwill

=> General Example

=> Total Stock Value => $25,000

=> FMV Assets - FMV Liabilities => $ 17,000 - $ 7,000 => $ 10,000=> Net Assets = FMV Assets - FMV Liabilities

=> Total Stock Value - (FMV of the Net Assets ( FMV Assets - FMV Liab.)) = Goodwill

=> $ 25,000 - $ 10,000 = Goodwill of => $ 15,000

2) Patents

3) Copyrights

C) Purchase a Patent (example)

Patent 57,000 Cash 57,000

D) Journal entry to amortize an intangible asset

Amortization Expense 1,200 Patent 1,200

The above entry will increase an expense and reduce an asset's value.

The above journal entry will reduce net income (income statement issue).

The above journal entry will not reduce the company's cash (st. of cash flows issue).

E) An intangible asset should be amortized over the shorter of an intangible asset's economic life or an intangible asset's legal life.

F) Remember ====> Matching Principle

The patent creates benefits. The benefits are matched with the cost of the intangible asset (over the useful life of the asset).

=> Internally generated goodwill will NOT be found on the balance sheet

45

9) Revision of Estimates

A) Periodically the initial estimates about an asset will be incorrect.(example => A corporation buys a piece of factory equipment. The initiallife is assumed to be 10 years. The corporation uses the equipment one yearand realizes the equipment will only last 4 years. The corporation will need to revise the asset's life (change from 10 to 4 years).

B)

C) Formula

Carrying Value - Revised Salvage Value ====> Depr. ExpenseRemaining Useful Life

D) An estimate change will impact the current period and future periods. Previous financials statement will not be revised.

10) Ordinary Repairs & Ordinary Maintenance

A) An ordinary repair should be expensed in the period the expense is incurred.

B) Example Journal Entry

Maintenance Expense 200 Cash 200

A revision of an estimate is not an error.

46

11) Exchange of Similar & Dissimilar Assets (New GAAP rules)

A) Exchange of Similar Assets => Car exchanged for a car

=> Loss always recognized=> Gain => Generally recognized (always for this class)

Record the exchange at the fair market value of the asset received.

=> Example

* FMV => New Car 12,000 Cost of Old Car 10,000 A/D Old Car 7,000

Journal Entry

FMV => Equipment (new car) 12,000 A/D - Old Car 7,000

Equipment (old car) 10,000 Gain on Exchange 9,000

B) Exchange of Dissimilar Assets => Car exchanged for a boat

=> Loss always recognized=> Gain will be recognized

Record the exchange at the fair market value of the asset received.

=> Example

* FMV => New Boat 15,000 Cost of Old Car 20,000 A/D Old Car 2,000

Journal Entry

FMV => Equipment (new boat) 15,000 A/D - Old Car 2,000 Loss on Exchange 3,000

Equipment (old car) 20,000

12) Extraordinary Repairs & Betterments

=> Repairs and betterments that extend the life of the asset or make the asset better should be capitalized.

13) Additions => should be capitalized

=> A company adds a new building to a shop. This addition should be capitalized.

47

14) Tax Laws

=> Depreciation is based on MACRS.=> MACRS => Modified Accelerated Cost Recovery System

=> The MACRS rules classify property based on the tax laws.

=> Half-year convention => A company can generally only depreciatean asset for half of the first year (based on the IRS rules).

=> The MACRS rules do not allow for any salvage value of the assetat the end of the life of the asset (under the IRS rules).

15) Land held for speculation / held as an investment (not part of the operating assets)

=> This type of land should be classified as an investment asset (not part of PP&E).

16) Research & Development (R&D)

=>General Rule => Expense

=> Reason => High degree of uncertainty with the success of R&D projects (conservative approach)

=> Exceptions to the general rule

=> Long-Term R&D assets that will benefit more than one R&D project should be capitalized. The long-term R&D asset will thenbe depreciated (example => R&D research building).

=> legal and filing fees should be capitalized (for an internally created patent)

17) Impairment Issues

=> General Idea => An impairment adjustment will need to be made to account for the decrease in the value of a long-term asset.

A) Limited-Life Intangibles (example=> a patent)

Recoverability test => then fair value test

B) PP & E => Recoverability test => then fair value test

Impairment LossAccumulated Impairment Loss (contra-asset account)

C) Indefinite-Life Intangibles (example => goodwill) => fair value tests

48

18) Reporting Investing Activities (assets of the business)

A) Trading Securities (purchasing stocks & debt securities as investments)=> Valued on the balance sheet at FMV (current asset)=> Assumed to be sold within the near future (intent of management)

=> Example (Trading Security)

November 1 => Purchased 1,000 shares of Adams Inc. @ $20.00 per share

Trading Security - Adams Inc. $ 20,000 Cash $ 20,000

Dec. 31, Year-End Value => 1,000 shares of Adams Inc., FMV @ $22.00 per share

Trading Security - Adams Inc. $ 2,000 Unrealized Gain - Trading Sec. $ 2,000

*****Unrealized Gain - Other Income Item - (on the income statement)

B) Available-for-Sale Securities (purchasing stocks & debt securities as investments)=> Valued on the balance sheet at FMV (generally classified as investment assets, not current assets)=> Securities assumed to not be sold in the near future (intent of management)

=> Unrealized gains & losses will be found in stockholders' equity (balance sheet, other comprehensive income)

C) Held-to-Maturity Securities (example => investing in another corporation's bonds)=> Intent of management => hold to maturity=> Valued on the balance sheet at amortized cost ---> (generally classified as an investment asset, not a current asset)

---> can move to a current assets based on maturity date

=> Unrealized gains & losses will impact net income (shown on the income statement)

=> Unrealized gains & losses will NOT impact net income

49

19) Ethical Case:

You start a small oil corporation. This corporation has a few assets. The assets' prices have increased in value.The reputation of your business has also grown over thepast few years. Your customers know and value yourtechnology.

Your accountant creates the below information.

Per GAAPCash 100,000 A/R 120,000 PP&E 650,000 Patents 20,000

Total 890,000

You believe the accountant's numbers do notreflect the true economic values.

Cash 100,000 A/R 120,000 PP&E 900,000 Patents 1,200,000 Goodwill 500,000

Total 2,820,000

Issues:The financial statements should be created in conformitywith GAAP rules. GAAP usually will not let long-term assetsbe increased in value. The internally generated goodwillwill NOT be found on the balance sheet.

20) IFRS - Long-Term Assets

International Financial Reporting Standards (IFRS) - Key Items

=> IFRS will allow impairments to be reversed (based on the IFRSconditions). GAAP rules will not allow impairmentsto be reversed.

=> IFRS will allow long-term assets to bevalued at FMV ( based on IFRS rules).

Parts of this document are the exclusive property of Rodney Vogt.

Est. Economic

Value

Those parts are protected by copyright laws (© Rodney Vogt, 2012).

50

Chapter 17

1) Comprehensive Income

A) Define - Measures all changes in owners' equity except

1) Except - Investments by owners & distributions to owners

2) Except - Errors made on past financial statements

2) Major Financial Statement=> Income Statement

A) Purpose => The income statement reflects the earnings generated by the company during the accounting period.

B) Types of Income Statement Formats

1) Single-step Format

a) Total Revenues - Total Expenses

2) Multi-Step Format

a) Under the multi-step format, income & expenses are divided by the activities that created the income or expense

51

3) More on the Multi-Step Format

A) Net Sales = Sales - Sales Returns & Allowances - Sales Discounts

B) Gross Profit = Net Sales - Cost of Goods Sold Expense!!!!

1) Gross Profit = Gross Margin (same number)

C)

D) Other Revenues & Other Expenses

1) Interest Revenue / Interest Income2) Gains3) Dividend Revenue / Dividend Income4) Interest Expense5) Losses6) Unrealized Gains & Losses on Trading Securities

E) Income From Continuing Operations (before taxes)

F) Income Taxes

G) Income From Continuing Operations

1)

H) DE items

1) D = Discontinued Operations (net of taxes)

2) E = Extraordinary Items (net of taxes)

I) Net Income

4) More on the DE Items (all net of taxes)

A) D = Discontinued Operations (net of taxes)

1) Discontinued operations are operations management of a company believeswill not contribute to the operations of the business in the future.

2) Reason for separation - Show financial statement readers the discontinued operations

a)

contribute to the future earnings of the business.

Income from Operations = Gross Profit - Selling & Administrative Expenses (Operating Exp.)

Income From Continuing Operations => AFTER-TAX NUMBER

will not contribute towards future earnings.

If the discontinued operations were mingled with the other central operations of thebusiness, a reader could not see the sections of the business that will not

52

3) Discontinued Operations (Gain) - Shown Net of Taxes

a) Discontinued Operations - Gain 1,000 (Before Taxes)

b) Tax Rate - 30%

c) Discontinued Operations ==> 700 <= Shown on the Income Statement

1) ( 1,000 X ( 1 - .3)) (net of taxes)

4) Discontinued Operations (Loss) - Shown Net of Taxes

a) Discontinued Operations - Loss (10,000) (Before Taxes)

b) Tax Rate - 30%

c) Discontinued Operations ==> (7,000) <= Shown on the Income Statement

1) ( -10,000 X ( 1 - .3)) (net of taxes)

B) E = Extraordinary Item (net of taxes)

1) Extraordinary Items => 2 requirements => Both must be met

a) Unusual => Unusual for the business (not a typical transaction)

b) Infrequent => Event does not happen very often (almost never again)

2) Extraordinary Example

a) Gas fire in Hutchinson --> Say a business was damaged by the gas fire,this type of event is very unusual and should never happen again.

3) Why Important to Separate Out

a)

be used to evaluate the future earning potential of the business (eventshould never happen again).

b) Without separating extraordinary events out, readers would believe theevents were part of the normal operations of the business.

4) Extraordinary Items => Shown => Net of Taxes

Show the financial statement readers the event is not part of the normal operations of the business. The event should not

53

5) Earnings Per Share ===> EPS

A) Earnings Per Share Formula = Net Income - Preferred Stock DividendsWeighted-Average # of Common Shares Outstanding

1) Remember => Shares Outstanding = (Shares Issued - Treasury Stock)

B) EPS Example:

1) Net Income = $ 600,0002) Preferred Stock (Shares Issued = 60,000, P/S Share in Treasury = 5,000

P/S rate = 6%, P/S par value = $100) , (60,000 -5,000) * 100 * .06 = $ 330,000

3) Common Stock Shares Outstanding ( Jan. 1 - March 31) = 30,000 Shares4) Common Stock Purchased (Treasury Stock), (April 1) 5,000 Shares5) Additional Shares Issued (September 1) 20,000 Shares

6) Solve - EPS

a) Weighted-Average # of Shares Outstanding

30,000 X 3 / 12 7,500 (30,000-5,000) 25,000 X 5 / 12 10,417 (25,000+20,000) 45,000 X 4 / 12 15,000

32,917

or (30,000-5,000+20,000)

b) EPS = $ 600,000 - $ 330,000 =====> $ 8.20 32,917 Shares

C) Diluted Earnings Per Share* Items => Stock Options & Convertible Debt

54

6) Financial Accounting Standards Board (FASB) - Statement 154

=> Accounting Changes & Error Corrections

A) Past History

=> The income statement would account for thetotal change from one accounting principle to another accounting principle. This catch-up number was called

The catch-up number would adjust net income in total for the past differences between the two accounting principles.

Example=> DDB deprecation => would be higher than straight-line depreciation

B) Current FASB rules - Statement 154

=> Changes in accounting principles from one period to the next period

financial statement should be restated to adjust for the application of the new accounting principle.

=> Exception to the General Rule

=> Past accounting rules required a change in a depreciation

=> Statement 154 treats a change in a depreciation methodas a change in an estimate. This change will only impactcurrent and future periods. Use the same logic for changesamortization and for changes in depletion.

C)

The new rules have replaced the cumulative accounting logicfound in the book.

a cumulative effect of a change in accounting principle.

should be handled retrospectively.

=> Retrospectively => Retrospective treatment means that past

method to be treated as a cumulative effect of a change in accounting principle.

The Book (old book issue)=> Cumulative Effect of a Change in Accounting Principle

55

7) Earnings Quality

A) Definition of Earnings Quality

Definition => High quality earnings should help a financial statement reader predict future earnings.

*Transitory Earnings => Transitory earnings are earnings that are not part of the normal earning process.

* (not what the company does), (not part of the normal earning process)

* Example => Gains & Losses on PP&E Item (selling PP&E assets)* Example => Impairment Item

* Permanent Earnings => The earnings generated from the central operations of the business.

* Permanent earnings are usually income statement accounts found before the "other items."

* Net Sales* Cost of Goods Sold (Gross Margin)* Selling & Administrative Expenses (Operating Exp.)

8) A new revenue recognition process will be used by the business world (rules for 2017). This revenue recognition process will replace the old GAAP rules.

A) Old GAAP Rules

Two Conditions

a. realized (cash now)b. realizable (receive something that can be converted into value (A/R))

B) New Rules (starting in 2017)

Logic of the Five-Step ProcessThe new rules will take an asset/liability approach. The new approach will lookat the changes in an entity's assets and the changes in an entity's liabilities.These changes in the assets and the liabilities will be used to develop the revenue that should be recognized.

The asset => the consideration to be received from the customer (value to be received)The liability => the obligation to the customer

Steps in the Five-Step Process

1) The business entity should identify the contract(s) with the customer.2) The business should identify the separate performance obligation(s) with the customer (liability or liabilities).3) The business entity should determine the transaction price (consideration/value/asset(s)).4) The business should then allocate the transaction price to the separate performance obligation(s).5) The business should recognize revenue after each performance obligation is satisfied.

1) Earned 2) Revenue must be realized or realizable

56

Parts of this document are the exclusive property of Rodney Vogt.

Those parts are protected by copyright laws (© Rodney Vogt, 2014).

AIF - Chapters 20 - Financial Statement Analysis

1) Financial statement analysis:

A) Leadership Position - Hopefully each student will be in a leadershipposition. Leaders generally must look at financial statements.

B) Personal Financial Responsibility - Our generation cannot rely on pension plans.

1) Our generation must take responsibility for our own personal investment.

C)

1) I believe everyone in this room will have some individual stock ownership.Any financial statement analysis knowledge should help you makebetter investment decisions.

2) Major users of financial analysis

A) Creditors - Banks & Bond Investors

1) Creditors want to make sure they get their investments back and receive a return.

2) Credit Rating Agencies ---> Watched closely by creditors ( Moody's & Standards & Poor)

B) Equity Investors - Individuals with a stock ownership in the company.

1) Equity investors want the stock to generate an acceptable return.

A) Returns from ---> Stock price increasing

B) Returns from ---> dividends (if an issue)

2) What happens when an investor does not feel he or she will receive an acceptable rateof return?

** Investor will ---> Sell the stock

Individual Stock Purchases - Life Application

3) Horizontal vs. Vertical Analysis

A) Horizontal analysis generally compares one period against another period

1) Horizontal analysis compares:

B) Vertical analysis compare a given period by a total for the period

1) Vertical analysis compares:

a) Balance sheet -----------> account / total assets

b) Income statement -----> account / total net sales

2) Common-Size Analysis - Every account in relation to some item…

4) Ratio Analysis

A) Activity Ratios

1) Why care about "activity ratios?"

a) Answer ---> Activity ratios help a financial statement reader assesswhether the company is experiencing any changes in the normal flow of business.

2) Major Activity Ratios

a) Accounts Receivable Turnover Ratio =

Net Credit SalesAvg. Net Accounts Receivable

converting accounts receivable into cash.

1)receivable turnover ratio.

a) Why ----> Higher ratio means cash is coming into thebusiness faster.

Importance: The ratio explains how fast the company is

General Rule: A company wants to increase the accounts

b) Inventory Turnover Ratio =

Cost of Goods SoldAvg. Inventory for the Period

converting inventory into sales.

1)turnover ratio.

a) Why ----> Higher ratio means inventory is not building.Companies want to keep inventory as low aspossible and satisfy customer needs.Also, inventory does not produce a return (comparedto a short-term investment).

B) Liquidity

1) Current Ratio =

Current AssetCurrent Liabilities

cover current liabilities.

* General Rule: A banker would be more likely to give a short-term loan to acompany with a high current ratio vs. a low current ratio.

* Why ----> A high current ratio means a banker has a higherlikelihood of receiving the bank's money back.

2) Working Capital = Current Assets - Current Liabilities

of a business. Could the current assets cover the currentliabilities?

Importance: The ratio explains how fast the company is

General Rule: A company wants to increase the inventory

Importance: The ratio shows the amount of current assets to

Importance: This calculation tries to measure the short-term liquidity

C) Major Profitability Ratios

1) Gross Margin Ratio =

Gross MarginNet Sales

each sale ( Gross Margin = Net Sales - Cost of Goods Sold)

* General Rule: A company wants to increase the gross margin on each sale. The additional gross margin can be used to cover expenses below the gross margin.

2) Earning Per Share (EPS)

Net Income - Preferred DividendsWeighted - Avg. # of Common Stock Outstanding

* General Rule: A company wants to increase its earnings per share.

3) Price-earnings Ratio

Current Stock Market PriceEarnings Per Share (EPS)

* General Rule: An investor wants to buy a stock before the P/E ratio increases.

Importance: The ratio shows the % of profit generated by

Importance: The EPS ratio is the most talked about financial ratio.

Importance: As the P/E ratio increases, the stock becomes a more expensive stock.

D) Evaluating Debt Financing

1) Debt to Equity Ratio = Total DebtTotal Equity

* Ratio of 1 => Debt financing equals equity financing

* Ratio of 1.5 => More debt financing than equity financing

* Who Cares????

a) General rule, as the debt to equity ratio increases = > therisk associated with the business increases (default risk)

* Remember the Accounting Equation

* Assets = Liabilities + Owners' Equity

If you know 2 of the 3 values, you can solve for the missing value.

2) Times Interest Earned Ratio

* Equation = Earnings before Interest & TaxesInterest Expense

* Example 30,000 = 3.00 10,000

The above example shows a business generating 3 times the cash inflows to pay for any interest payments.

General Rule: As the times interest ratio goes up, the firm is in a better position to payoff creditors.

Parts of this document are the exclusive property of Rodney Vogt. Those parts are protected by copyright laws (© Rodney Vogt, 2013).

AIF - Chapter 18 - Balance Sheet

1) Balance Sheet / Statement of Financial Position

A) General Formula

1) Assets = Liabilities + Owners' Equity

B) Reports => Assets ==> Resources having future economic benefits

1) Types of Assets

2) Amount of Assets

C) Reports => Liabilities ==> Liabilities represent future economic sacrifice of resources

1) Types of Liabilities

2) Amount of Liabilities

D) Reports => Owners' Equity ==> Residual interest in the corporation

1) Assets - Liabilities = Owners' Equity

Residual Interest

2) Classified Balance Sheet

A) Why Classify ==> The balance sheet is classified to help readers understand the different types of assets, liabilities, and owners' equity.

B) Major Classifications

Note: Assets are placed on the balance sheet according totheir liquidity (Liquidity = > How easily can the assetbe converted into cash).

1) Current Assets - These assets will be converted into cash or used up within one year.

a) Common Current Assets

1) Cash

2) Marketable Securities

==> Trading Securities (value at FMV)

3) A/R ====> A/R 10,000 Less: Allow. for D/A (600)

9,400 *** Net Realizable Value (expected cash to be received)

4) Inventory

5) Prepaids

2) Investments ==> Long-term investments made by a company

a) Best Example - A company purchases another company (makes an investment)b) Land held for speculation (non-operational asset)c) Available-for-Sale Securities (at FMV) & Held-to-Maturity Securities (amortized cost)

(not meeting the definition of a current asset)

3) Property, Plant, & Equipment ( PP & E)

a) Characteristics of PP & E

1) Tangible assets - can touch and feel ( have physical substance)

2) Used in the business

3) Long-Term Assets

b) PP & E assets are shown ( net of accumulated depreciation) => Balance Sheet

1) Exception ===> Land is not depreciated

c) Examples of PP & E

1) Land

2) Buildings

3) Equipment

4) Capital Leases

4) Intangible Assets

a) Intangible assets lack physical substance

b) Patents =>Shown on the balance sheet => Net of Amortization

c) Examples of Intangible Assets

1) Patents (net of amortization)

2) Goodwill - (reviewed annual for a decreased in the value )

5) Current Liabilities: (Liability order based on the timing of payment)

a) Remember LiabilitiesXXXXX

b) Define ==> Current Liabilities ==> economic sacrifice of resources within one year

c) Examples (Current Liabilities)

1) Accounts Payable

2) Salaries Payable

3) Taxes Payable

4)

5) Unearned Revenue

6) Accrued Liabilities

7) Customer Deposits (likely returned to the customer)

8) Bank overdrafts (general rule)

6) Long-Term Liabilities

a) Define ==> Long-Term Liabilities ==> future economic sacrifice of resources beyond the next year

b) Examples

1) Notes Payable ( Long-Term)

Notes Payable 10,000 Less: Discounts on Notes Payable 500 Carrying Value 9,500

2) Bonds Payable

Bonds Payable 30,000 Premium on Bonds Payable 1,000 Carrying Value 31,000

c) Long-Term Liabilities can become ==> Current liabilities

d) Banker Classification Example

Notes Payable (short-term)

7) Stockholders' Equity: Contributed Capital

a) Define - Value provided by the owners

b) Examples

1) Common Stock

2) Preferred Stock

3) Additional Paid-in Capital

8) Stockholders' Equity : Earnings Retained

a) Retained Earnings summarizes the earnings retained by the corporation

Retained EarningsNormal Bal.

Net Loss Net Income

Dividends Declared

9) Stockholders' Equity: Other

a) Treasury Stock ==> Contra-Equity Account

3) Go over a balance sheet example

4) Different Types of Audit Reports

A) Unqualified Opinion - Financial statements conform to GAAP

1) Clean, no material errors or misstatements

B) an item (an auditor might not agree with one application of a GAAP principle)

C) Adverse Opinion - Financial statements are not found to be in accordance with GAAP.

1) Material errors - mislead a financial statement reader

D) Disclaimer of Opinion - No opinion is given on the financial statements

1) Might be a scope restriction

1) Bob owns a CPA firm that audits a Manhattan client. Inventory represents a large asset for this client.The inventory is warehoused in Colorado.The Manhattan client will not let Bob & his staff investigate theinventory in Colorado.

Bob cannot give an opinion on the financial statements withoutinvestigating the inventory in Colorado.

5) Statement of Retained Earnings

A) This statement is a link between the income statement and the balance sheet.

B) General Flow => Statement of Retained Earnings

Beginning Balance, Retained Earnings XX+ or - Prior Period Adjustments XXAdjusted, Retained Earnings Balance XX+ or - Net Income XX

Ending Balance, Retained Earnings XX

C) Prior Period Adjustments=> Adjustments to => Beg. Balance Retained Earnings (net of taxes)=> Previously undiscovered error

Parts of this document are the exclusive property of Rodney Vogt.

Qualified Opinion - Financial statements are clean - except for

a) Example of a scope restriction

Those parts are protected by copyright laws (© Rodney Vogt, 2013).

68

AIF - Chapter 19 - Statement of Cash Flows

1) Statement of Cash Flows

A) Provides a link between the income statement & the balance sheet

B) Assesses the entity's ability to generate positive future cash flows

C) Assesses the entity's ability to meet obligations (pay debts) &pay dividends

D) Assesses the differences between net incomeand cash flows

E) Assess both cash & noncash investing and financing activities

1) Example - Cash Investing

Equipment 50,000 Cash 50,000

Cash Payment for equipment

2) Example - Noncash Investing & Financing

Equipment 50,000 Bonds Payable 50,000

Investment in equipment without any cash outflow

Cash will flow from the business as the bonds are paid off

69

2) Sections of the Statement of Cash Flows

A) Operating Section

1) Reports cash flows from ==> Normal operations of the business

a) The main business activities of the business

1) Examples => selling grain & selling lumber

b)

c)

d)

e)

B) Investing Section

1) Acquiring & Disposing of PP & E and other long-term investments

2) Example => Buy Equipment (PP & E) or Sell Equipment

3) Short-Term Marketable Securities => investments with a life greater than 90 days

4) Principal transactions (Lending money to other entities)=> Notes Receivable (principal only)

Cash paid for interest

Cash received from interest

Cash received from dividends

Cash paid for taxes

70

C) Financing Section

1) Groups transactions relating to the financing of the business

2) Examples

a) Issue Stock => Cash Inflow

b) Issue Bonds => Cash Inflow

c) Buy treasury stock => cash outflow

d)

e) Pay off Bonds Payable => Cash outflow

3) Short-Term Debt (general obligation debt)

a)

D)

1) Footnotes - report noncash investing & financing activities

a) Examples - Equipment purchased

Equipment 50,000 Bonds Payable 50,000

Equipment 75,000 Common Stock 75,000

2) Footnotes => Disclose

a) Cash paid for interest

b) Cash paid for income taxes

PAYMENT of dividends (cash outflow), not the declaration of dividends

Example => Short-term Note Payable

Minor Section - Statement of Cash Flows (Footnotes)

71

3) More examples of transactions found in each section - statement of cash flows

A) Operating Section

1) Cash Inflows

a) Cash received from customers

b)

2) Cash Outflows

a) Cash paid to suppliers

b) Cash paid for operating activities

c)

d) Cash paid for taxes

B) Investing Section

1) Cash Inflows

a) Selling equipment

b) Selling a building

c)

d) Short-Term Marketable Securities (cash received)=> investments with a life greater than 90 days

2) Cash Outflows

a) Buying equipment

b) Buying a building

c)

d) Short-Term Marketable Securities (cash paid)

Cash received from interest revenue and dividend revenue

Cash paid for interest expense

Principal returned (from a Note Receivable (asset))

Principal invested (from a Note Receivable (asset))

72

=> investments with a life greater than 90 days

C) Financing Activities

1) Cash Inflows

a) Borrowing / Issuing Debt => Short-Term Note Payable (general obligation debt)=> Long-Term Debt (example => Bonds)

b) Issuing / Selling Equity => Stocks

c) Selling / Reissuing Treasury Stock

2) Cash Outflows

a) Pay off long-term debt => Bonds Payable=> Short-Term Note Payable (general obligation debt)=> Long-Term Debt (example => Bonds)

b) Purchasing treasury stock

c)

1)

PAYING dividends

Does NOT include just declaring a dividend

73

4) Major Differences Between the Income Statement & the Statement of Cash Flows

A) Sales on Account

A/R 80,000 Sales 80,000

Increase Net IncomeNo cash Inflow

B) A/R customer - cash received

Cash 80,000 A/R 80,000

No impact on Net IncomeCash comes into the business ==> operating section

C) Accrue Salaries - Wages have been earned by the workers, but no cash has been paid

Salaries Expense 3,000 Salaries Payable 3,000

Reduce Net IncomeNo cash outflow

D) Depreciation Expense

Depreciation Expense 9,000 Accumulated Depreciation 9,000

Decrease Net IncomeNo Cash Outflow

5) Cash Equivalents => Short-term investments (maturity => within 90 days)=> Highly liquid (easy to covert into cash)

74

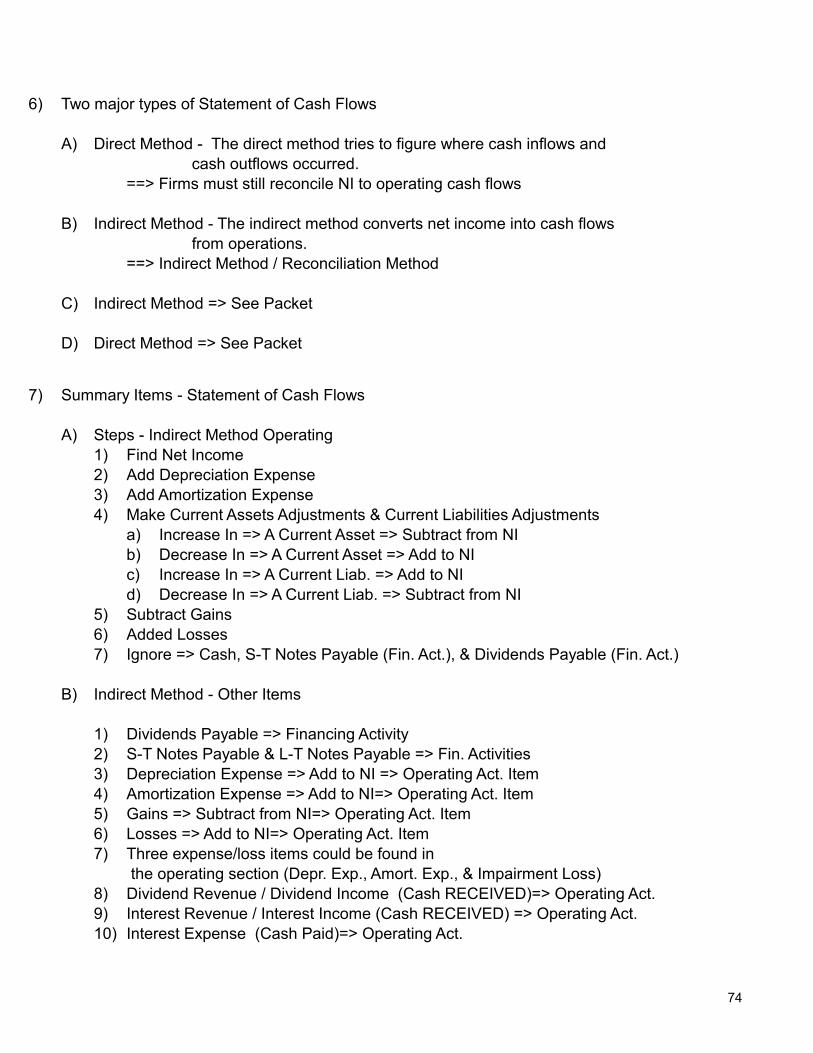

6) Two major types of Statement of Cash Flows

A) Direct Method - The direct method tries to figure where cash inflows and cash outflows occurred.

==> Firms must still reconcile NI to operating cash flows

B) Indirect Method - The indirect method converts net income into cash flows from operations.

==> Indirect Method / Reconciliation Method

C) Indirect Method => See Packet

D) Direct Method => See Packet

7) Summary Items - Statement of Cash Flows

A) Steps - Indirect Method Operating 1) Find Net Income2) Add Depreciation Expense3) Add Amortization Expense4) Make Current Assets Adjustments & Current Liabilities Adjustments

a) Increase In => A Current Asset => Subtract from NI b) Decrease In => A Current Asset => Add to NI c) Increase In => A Current Liab. => Add to NI d) Decrease In => A Current Liab. => Subtract from NI

5) Subtract Gains6) Added Losses7) Ignore => Cash, S-T Notes Payable (Fin. Act.), & Dividends Payable (Fin. Act.)

B) Indirect Method - Other Items

1) Dividends Payable => Financing Activity2) S-T Notes Payable & L-T Notes Payable => Fin. Activities3) Depreciation Expense => Add to NI => Operating Act. Item4) Amortization Expense => Add to NI=> Operating Act. Item5) Gains => Subtract from NI=> Operating Act. Item6) Losses => Add to NI=> Operating Act. Item7) Three expense/loss items could be found in

the operating section (Depr. Exp., Amort. Exp., & Impairment Loss)8) Dividend Revenue / Dividend Income (Cash RECEIVED)=> Operating Act.9) Interest Revenue / Interest Income (Cash RECEIVED) => Operating Act.10) Interest Expense (Cash Paid)=> Operating Act.

75

11) DIVIDENDS PAID => Financing Act.

76

8) Another Item (indirect statement of cash flows)

You should assume a corporation has only the below journal entry for a given year.

Operating Expense 50,000 Salaries Expense 20,000

Cash 70,000

Quick St. of Cash Flows

Net Loss (70,000) Adj. to the NL

None / Zero adj. 0

Cash Flows From Operating Act. (70,000)

Summary:Cash Outflows = ExpensesNo adjustments

You should assume a corporation has only the below journal entry for a given year.

Operating Expense 50,000 Salaries Expense 20,000

Utilities Payable 3,000 < = C. Liab. Salaries Payable 2,000 < = C. Liab. Cash 65,000

Quick St. of Cash Flows

Net Loss (70,000) Adj. to the NL

Utilities Payable 3,000 Salaries Payable 2,000

Cash Flows From Operating Act. (65,000)

Summary:Cash Outflows ≠ ExpensesAdj. must be made

77

78

9) IFRS - Statement of Cash Flows

International Financial Reporting Standards (IFRS)

A) IFRS will allow for more flexibility in theclassification of interest received, interest paid,and dividends paid. These items must be shownas separate items on the statement of cash flows.IFRS requires consistent classification of interest received, interest paid, and dividends paid (between two reporting periods).

B) GAAP - Review

1) Interest Received / Interest Income => Operating Item2) Interest Paid / Interest Expense => Operating Item3) Dividends Paid => Financing Item

Parts of this document are the exclusive property of Rodney Vogt.

Those parts are protected by copyright laws (© Rodney Vogt, 2013).