aig sample illustrations for critical, chronic & terminal illness benefits iv

TRANSCRIPT

®

QoLGuarantee Plus IIA Flexible Premium Adjustable Life Insurance PolicyLife Insurance Policy Quotation

Designed forMrs. VCClient State: Idaho

Presented byLee Rogers WA

Date PreparedJune 17, 2016

Issued by:

American General Life InsuranceCompany2727-A Allen ParkwayHouston, TX 77019

Please read your quotation carefully. It is designed to aid your understanding of the policy bydemonstrating how policy benefits and premiums are affected under different assumptions. Thisquotation is not a contract and is not intended to predict actual performance.

This information may be subject to change, and does not constitute legal, tax or accounting advicefrom American General Life Insurance Company (AGL), its employees, financial professionals orother representatives. Applicable laws and regulations are complex and subject to change. Any taxstatements in this material are not intended to suggest the avoidance of U.S. federal, state or localtax penalties. For advice concerning your individual circumstances, consult your attorney, tax advisoror accountant.

Issuing insurance company AGL is a member of American International Group, Inc. (AIG). Guaranteesare backed by the claims-paying ability of the issuing insurance company.

(Form ICC15-15442)

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 1 of 24

YOUR POLICY SUMMARY

Initial Death Benefit (Specified Amount) .............................................. $500,000Death Benefit Option ........................................................................... LevelInitial Planned Premium ...................................................................... $4,959.85Annual Premium Outlay ...................................................................... $4,959.85Premium Mode .................................................................................... AnnualDeath Benefit Guaranteed to (Guaranteed Period) ............................. To Age 100Premium Paid To................................ ................................................. To Age 36IRC 7702 Life Insurance Test .............................................................. Guideline Premium TestInitial Guideline Single Premium .......................................................... $199,710.80Initial Guideline Level Premium ........................................................... $15,758.42Seven Pay Premium ............................................................................ $23,855.88

Rider(s) Initial Premium Initial Benefit

QoL® SelectChoice II Accelerated Death Benefit Riders(Critical, Chronic, and Terminal)*........................................................... Automatically Included See Qol ABRs Section

Enhanced Surrender Value Rider* ........................................................ Automatically Included See ROP Section

CustomChoice Lifestyle Income Solution®(CCLIS) - Income Rider ....................................................................... $887.57 in Year 1 See CCLIS Rider Section

*Automatically included in policy

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 2 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

YOUR QUOTATION DESCRIPTIONYour QoL Guarantee Plus II policy is an individual universal life insurance policy that features flexible premiums and guaranteed death benefitprotection. With QoL Guarantee Plus II, you may select your guarantee period, or how long you want your death benefit protection to beguaranteed1. With your premium funding period, you can decide how long you want to pay.

Your QoL Guarantee Plus II policy also includes an automatically included Enhanced Surrender Value Rider2, or guaranteed return of premium(ROP) feature. In addition, besides receiving death benefit protection your QoL Guarantee Plus II policy includes, for no additional premium,QoL® SelectChoice II Accelerated Benefit Riders3 for Chronic, Critical and Terminal Illness that allow you to access your death benefit whileyou are alive if you have a qualifying illness or condition. The riders can help to pay for the costs of treatment for qualifying illnesses or conditions- or any other expenses, by paying your death benefit prior to death at a discount.

You have also elected CustomChoice Lifestyle Income Solution (CCLIS)5 that pays your death benefit dollar-for-dollar as guaranteed incomeonce exercised.

IMPORTANT NOTICE ABOUT YOUR QUOTATIONYour quotation is not a contract and is not intended to predict actual performance. No current values have been used in your quotation. Allvalues shown are guaranteed. It is not complete and valid unless presented with all pages. American General Life Insurance Company, itsemployees, agents and representatives do not render legal or tax advice and your quotation should not be construed as such. You shouldcontact your own tax or legal advisor regarding the tax and other consequences which may result from alternatives shown in this quotation.

1Guarantees are subject to the claims-paying ability of the issuing insurance company.2Enhanced Surrender Value Rider see p.3QoL® SelectChoice II Accelerated Benefit Riders see p.5Guaranteed Withdrawal Benefit Rider (CustomChoice Lifestyle Income Solution “CCLIS”) see p.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 3 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

74

11

YOUR QoL SELECTCHOICE II ACCELERATED DEATH BENEFIT RIDERS SUMMARYThe QoL SelectChoice II Accelerated Death Benefit Riders for Critical, Chronic and Terminal Illness are three valuable riders automaticallyincluded in your policy at no additional premium cost that allow you to access all or a portion of your QoL Guarantee Plus II policy death benefitif you have a qualifying critical, chronic or terminal illness condition.

Each accelerated death benefit rider may be subject to requirements and limitations not specifically described in this quotation. See each riderfor additional terms, conditions, and limitations.

The QoL SelectChoice II Accelerated Death Benefit Riders allow you to receive a portion of the death benefit under the policy, during yourlifetime, upon submission of required documentation regarding a qualifying event. The death benefit that you elect to accelerate will be paid ata discounted amount because it is being paid prior to the actual time of death. However, the accelerated benefit you receive will not be lessthan the guaranteed minimum benefit based on different categories of illnesses, subject to the terms and conditions of the rider.

The following are hypothetical examples of benefits that you may receive from the QoL SelectChoice II Accelerated Death Benefit Riders fordifferent types of illnesses if you file a claim to accelerate the full death benefit of your policy for a qualifying illness or event. The hypotheticalamounts shown assume that no policy premiums are unpaid and that there is no loan balance. Amounts do not reflect any applicable administrativecharge. Also, if you choose to elect less than your policy’s full death benefit, the actual payment will be lower than the examples provided below,but your policy’s remaining death benefit will be higher.

Please see the rider description section of this quotation for the definitions of these qualifying illnesses or conditions and for additional ImportantConsiderations and Disclosures.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 4 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

QoL SELECTCHOICE II CRITICAL ILLNESS ACCELERATED DEATH BENEFITThe values below represent the guaranteed minimum benefit and the potential benefit payout for a hypothetical example* when a claim is filedat the estimated age below to accelerate the full initial death benefit of the policy as a lump sum payment for a qualifying critical illness (MajorHeart Attack, Coronary Artery Bypass, Stroke, Invasive Cancer, Major Organ Transplant, End Stage Renal Failure, Paralysis, Coma, SevereBurn). For a qualifying critical illness, the actual benefit paid will never be less than the guaranteed minimum benefit (Minimum AcceleratedBenefit Amount) calculated using the applicable percentages on the Minimum Accelerated Benefit Percentage page of the Rider Schedule.

*The hypothetical example shown assumes that the policy is issued with a life insurance benefit of $500,000 on a female, age 45, StandardNon-Tobacco. Hypothetical amounts shown assume that no policy premiums are unpaid and that there is no loan balance. The potential benefitpayouts were calculated using assumptions that are not guaranteed and may be changed at any time. Actual payouts may be more or lessfavorable.

QoL SELECTCHOICE II CHRONIC ILLNESS ACCELERATED DEATH BENEFITThe values below represent the guaranteed minimum benefit and the potential benefit payout for a hypothetical example* when a claim is filedat the estimated age below to accelerate the full initial death benefit of the policy as a lump sum payment for a qualifying chronic illness. Youcan also choose to receive your benefit on an annual or monthly basis. For a qualifying chronic illness, the actual benefit paid will never be lessthan the values shown in the guaranteed minimum benefit.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 5 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

*The hypothetical example shown assumes that the policy is issued with a life insurance benefit of $500,000 on a female, age 45, StandardNon-Tobacco. Hypothetical amounts shown assume that no policy premiums are unpaid and that there is no loan balance. The potential benefitpayouts were calculated using assumptions that are not guaranteed and may be changed at any time. Actual payouts may be more or lessfavorable.

QoL SELECTCHOICE II TERMINAL ILLNESS ACCELERATED DEATH BENEFIT

The values below represent the guaranteed minimum benefit and the potential benefit payment for a hypothetical example* when a claim isfiled at the estimated age below to accelerate the full initial death benefit of the policy as a lump sum payment for a qualifying terminal illness.

*The hypothetical example shown assumes that the policy is issued with a life insurance benefit of $500,000 on a female, age 45, StandardNon-Tobacco. Hypothetical amounts shown assume that no policy premiums are unpaid and that there is no loan balance. The potential benefitpayouts were calculated using assumptions that are not guaranteed and may be changed at any time. Actual payouts may be more or lessfavorable.

GUARANTEED MINIMUM CASH VALUES

With your QoL Guarantee Plus II policy, you have access to guaranteed minimum Cash Values which often exceed the Cash Values that wouldbe generated by your policy without this feature. You may access this free, additional provision through Full or Partial Surrenders.The Cash Value of your policy will vary by sex, age, duration, and smoking classification.Please note:• Increases in the Specified Amount or any changes to underwriting class will terminate the guaranteed Cash Value provision.• The guaranteed Cash Values will not be reinstated once terminated.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 6 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

YOUR GUARANTEED RETURN OF PREMIUM (ROP)Enhanced Surrender Value Rider(Form # ICC15-15990)

Your QoL Guarantee Plus II policy offers a guaranteed Enhanced Surrender Value Rider that is offered at no additionalcost and is automatically attached to your policy. The rider provides you, in most cases, with two opportunities to fullysurrender your policy and receive enhanced cash surrender value:

• At the end of Policy Year 20, you may fully surrender the policy and receive 50% of premiums paid1; or, alternatively,• At the end of Policy Year 25, you may fully surrender the policy and receive 100% of premiums paid1

1.See the rider for additional terms and conditions

Example:

Face Amount: $500,000Annual Premium: $4,960

Year 20 Cumulative Premiums: $99,197 Year 25 Cumulative Premiums: $123,996Enhanced Surrender Value Year 20: $49,599 Enhanced Surrender Value Year 25: $123,996

The Enhanced Surrender Value Rider will terminate on the earliest of the date the policy terminates or the date of insufficient funds.

- The Enhanced Surrender Value (“ROP”) is capped at 40% of specified face amount; for example, the benefit under a policy with a $1,000,000specified amount could never be greater than $400,000.

- The option to surrender the policy for its Enhanced Surrender Value must be exercised, if at all, during one of the 60-day periods followingPolicy Year 20 or Policy Year 25.

- Payment of the Enhanced Surrender Value assumes that all premiums are paid. The Enhanced Surrender Value is less any partial surrendersand outstanding loans.

- The Enhanced Surrender Value will not be paid in addition to the policy's Cash Surrender Value.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 7 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

ADDITIONAL INFORMATION REGARDING YOUR QoL SELECTCHOICE II ACCELERATED DEATH BENEFITRIDERS (ABRs)

The QoL SelectChoice II Accelerated Benefit Riders for Critical, Chronical and Terminal Illness are three valuable ridersautomatically included in your policy at no additional cost that allow you to access all or part of your QoL Guarantee PlusII policy death benefit if you have a qualifying critical, chronic or terminal illness or condition. You can use the benefit tohelp pay for the costs of treatment for qualifying illnesses or conditions - or any other expenses.

QoL SelectChoice II Accelerated Benefit Riders will pay the death benefit you elect to accelerate at a discounted amount because it is beingpaid prior to the actual time of death. However, the accelerated death benefit you receive is guaranteed to be no less than the guaranteedminimum benefit payout, which is a percentage of the death benefit accelerated. Actual payment will always be no less than the guaranteedminimum payout which takes into account outstanding loan amounts and premiums. The actual accelerated death benefit payment that we willoffer for acceleration will be based on our determination of the expected future mortality of a qualifying insured at the time an accelerated deathbenefit claim is made, and will be subject to an administrative charge, and payment of any unpaid but due policy premiums, and payment of apro rata amount of any policy loans if applicable. You can accelerate up to 100% of the death benefit, subject to a limit of the lesser of $2,000,000or any lesser amount set forth in your policy.

QoL SELECTCHOICE II CRITICAL ILLNESS ACCELERATED DEATH BENEFIT RIDER(Form # ICC15-15604)

The QoL SelectChoice II Critical Illness Accelerated Death Benefit Rider provides you access to your policy’s death benefit if you have one ofthe qualifying critical illnesses or conditions as specified below. There is a 30-day waiting period (90-day for Invasive Cancer) during which yourpolicy must be in-force before the benefit from this rider is available.

Qualifying Critical Illness• Major Heart Attack •Stroke •Major Organ Transplant •Paralysis •Severe Burn• Coronary Artery Bypass •Invasive Cancer •End Stage Renal Failure •Coma

Please see rider for the definitions of these qualifying illnesses or conditions.

Critical Illness BenefitIf you have a qualifying critical illness, you can file a claim and accelerate all or a portion of your policy’s death benefit. Your benefit will be paidin the form of a lump sum payment.

There is a guaranteed minimum benefit for the death benefit you choose to accelerate for a qualifying critical illness, depending on whether itis invasive cancer or other qualifying illness that is not invasive cancer. The actual critical illness accelerated death benefit amount available tobe paid as an accelerated death benefit will be based on our determination of the expected future mortality of a qualifying insured at the timean accelerated death benefit claim is made and will be at least as great as the guaranteed minimum benefit payout percentage multiplied bythe death benefit you choose to accelerate and less certain deductions.

If a benefit under the Critical Illness Accelerated Death Benefit Rider is payable, we will provide you with one (1) opportunity to elect a CriticalIllness Accelerated Death Benefit Amount as to the occurrence of the Qualifying Critical Illness in question. To make such an election, the Ownermust complete an election form and return it to AGL within 60 days of the owner’s receipt of the election form. For example, if you have aqualifying major heart attack, you will be provided an opportunity to elect a Critical Illness Accelerated Death Benefit Amount if you file a claim.If you elect not to receive an Accelerated Death Benefit, you will not be able to elect another Critical Illness Accelerated Death Benefit Amountfor the same major heart attack. However, if you have another qualifying illness event later, you can still choose to accelerate your remainingdeath benefit.

If, as to the occurrence of a Qualifying Critical Illness, You decide not to elect a Critical Illness Accelerated Death Benefit or if You decide toelect to receive less than the maximum Accelerated Death Benefit available for such Qualifying Critical Illness, You cannot thereafter elect aCritical Illness Accelerated Death Benefit and receive an Accelerated Death Benefit for the same occurrence of such Qualifying Critical Illness.

QoL SELECTCHOICE II CHRONIC ILLNESS ACCELERATED DEATH BENEFIT RIDER(Form # ICC15-15603)

The QoL SelectChoice II Chronic Illness Accelerated Death Benefit Rider provides you access to your policy’s death benefit if you have aqualifying chronic illness. There is a 30-day waiting period during which your policy must be in-force before the benefit from this rider is available.There is also an Elimination Period following the waiting period. The Elimination Period is a 90-day period in which you must be chronically illbefore you become eligible for an accelerated death benefit.This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 8 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Qualifying Chronic IllnessTo qualify as chronically ill, you must be certified by a Licensed Health Care Practitioner within the preceding 12-month period as:

• unable to perform, without Substantial Assistance from another person, at least two Activities of Daily Living (ADLs) for a period of at least90 consecutive days due to a loss of functional capacity; or

• Requires Substantial Supervision to protect such Insured Person from threats to health and safety due to Severe Cognitive Impairment;

ADLs: Bathing, Dressing, Toileting, Transferring, Continence, Eating.

Severe Cognitive impairment is a loss or deterioration in intellectual capacity that is comparable to (and includes) Alzheimer’s disease andsimilar forms of irreversible dementia. Proof of the determination is required prior to receiving any accelerated death benefit.

Chronic Illness BenefitIf you have a qualifying chronic illness, you can file a claim to accelerate your death benefit. You can choose to receive your chronic illnessbenefit in one lump-sum payment or in periodic payments. We will divide the Chronic Illness Accelerated Death Benefit Amount you elect intoequal periodic payments over the requested period. If you request to receive the Chronic Illness Benefit in periodic payments beyond the 12-month period from the initial certification submitted in support of your claim, a new certification must be provided as described by the rider foreach benefit period.

For a qualifying chronic illness, the actual benefit paid will never be less than the Minimum Accelerated Death Benefit Amount calculated usingthe applicable percentages on the Minimum Accelerated Benefit Percentage page of the Rider Schedule. Under certain circumstances wherean insured’s mortality (i.e., our expectation of the insured’s life expectancy) is not significantly changed by a Qualifying Chronic Illness and,notwithstanding the Minimum Accelerated Benefit Amount provision, the accelerated death benefit may be zero. See the rider for details.

Payments received under this chronic illness accelerated death benefit rider are not part of a health, long-term care, or nursing home insurancepolicy and may not be sufficient to cover medical, nursing home or other bills.

Coordination of QoL SelectChoice II Chronic Illness Benefit Rider with Accelerated Access Solution RiderWhen you file a claim and are determined to be eligible to receive an Accelerated Access Solution benefit for a qualified chronic illness, anybenefit will be paid under the Accelerated Access Solution rider first. Once the benefit under this rider is exhausted, you may be paid under theQoL SelectChoice II Chronic Illness Benefit Rider if there is any benefit remaining available.

QoL SELECTCHOICE II TERMINAL ILLNESS ACCELERATED DEATH BENEFIT RIDER(Form # ICC15-15602)

QoL SelectChoice II Terminal Illness Accelerated Death Benefit Rider provides you access to your policy’s death benefit if you are terminally ill.

Qualifying Terminal IllnessA Qualifying Terminal Illness is an illness or physical condition that is diagnosed by a physician to be reasonably expected to result in the insured’sdeath within 24 months from the date of diagnosis.

Terminal Illness BenefitIf you have a qualifying terminal illness, you can file a claim and request a one-time full acceleration or partial acceleration of the policy’s deathbenefit. Your benefit will be paid in the form of a lump sum payment.

There is a Guaranteed Minimum Benefit for the death benefit you choose to accelerate for a qualifying terminal illness. The actual accelerateddeath benefit payment that we will offer for acceleration will be based on our determination of the expected future mortality of a qualifying insuredat the time an accelerated death benefit claim is made and will be at least as great as the Minimum Accelerated Benefit Amount, which is thegreater of (1) the guaranteed payout percentage multiplied by the death benefit you choose to accelerate, less any loan amount and premiumdue, or (2) the pro rata portion of the Cash Surrender Value corresponding to the accelerated death benefit.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 9 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Important ConsiderationsThe QoL SelectChoice II Accelerated Death Benefit Riders will impact the policy. The specified amount, policy values and outstanding loanbalances will be reduced if an accelerated death benefit is paid. You should contact your personal tax advisor for specific advice before exercisingthese benefits.

All provisions of the policy that do not conflict with this rider apply to this rider. Where there is any conflict between the rider provisions and thepolicy provisions, the rider provisions prevail.

You should consider that receiving or having the contractual right to receive any Accelerated Death Benefit payment may affect your eligibilityfor Medicaid, Social Security Income (SSI), or other government benefits or entitlements. You are advised to contact the Medicaid Unit of yourlocal Department of Public Welfare and the Social Security Administration for more information.

Benefits may be subject to taxation and may impact eligibility for Medicaid or other public assistance programs. Consult your legal and taxadvisor for more information and refer to the rider for qualifications, limitations and fees.

The owner should consult a competent tax advisor to determine the current tax consequences before requesting any accelerated death benefits.This rider is not intended to be a health contract, qualified long term care insurance contract under section 7702B(b) of the Internal RevenueCode or a non-qualified long term care insurance contract.

Disclosures Applicable to Critical Illness Accelerated Death Benefit Rider, Chronic Illness Accelerated Death Benefit Rider, and TerminalIllness Accelerated Death Benefit Rider

(1) When filing a claim for Qualifying Critical Illness under a Critical Illness Accelerated Death Benefit Rider, for Qualifying Chronic Illness undera Chronic Illness Accelerated Death Benefit Rider or for Qualifying Terminal Illness under a Terminal Illness Accelerated Death Benefit Rider, theclaimant must provide to the Company a completed claim form and then-current Certification which must be received at its Administrative Center.

(2) If a benefit under the Critical Illness Accelerated Death Benefit Rider is payable, the Company will provide the Owner with one (1) opportunityto elect a Critical Illness Accelerated Benefit Amount as to the occurrence of the Qualifying Critical Illness in question. To make such an election,the Owner must complete an election form and return it to AGL within the Election Period set forth in the rider (i.e., within 60 days of the owner’sreceipt of the election form). The Company will not provide a later opportunity to elect a Critical Illness Accelerated Benefit Amount under a Policyas to the same occurrence of a Qualifying Critical Illness.

(3) If a benefit under the Chronic Illness Accelerated Death Benefit Rider or under the Terminal Illness Accelerated Death Benefit Rider is payable,the Company will provide the Owner with an opportunity to elect a Chronic Illness Accelerated Benefit Amount as to the Qualifying Chronic Illnessin question or to elect a Terminal Illness Accelerated Death Benefit Amount as to the Qualifying Terminal Illness in question, as applicable. Tomake an election, the Owner must complete an election form and return it to AGL within 60 days of the Owner’s receipt of the election form.

(4) Under certain circumstances where an insured’s mortality (i.e., our expectation of the insured’s life expectancy) is not significantly changedby a Qualifying Critical Illness or a Qualifying Chronic Illness and, notwithstanding the Minimum Accelerated Benefit Amount provision, theaccelerated benefit may be zero.

(5) The failure to provide a required election form (with the requested attachments) within the Election Period provided by the applicable rider (i.e., within 60 days of the owner’s receipt of the election form) may preclude payment of a benefit.

(6) Benefits payable under an accelerated death benefit rider may be taxable. Neither American General Life Insurance Company nor any agentrepresenting it is authorized to give legal or tax advice. Please consult a qualified legal or tax advisor regarding questions concerning the informationand concepts contained in this material.

(7) Generally, we will send you an IRS Form 1099-LTC if you receive an accelerated death benefit on account of a Chronic Illness or a TerminalIllness. We will send you an IRS Form 1099-R if you receive an accelerated death benefit on account of a Critical Illness. The sum that will beincluded in Box 2 (Accelerated death benefits paid) of IRS Form 1099-LTC or in Box 1 (Gross distribution) of IRS Form 1099-R will be the actualsum you received by check or otherwise minus any refund of premium and/or loan interest included with our benefit payment plus any unpaidbut due policy premium, if applicable, and/or pro rata amount of any loan balance.

(8) The maximum amount of life insurance death benefits that may be accelerated as to an Insured Person under all accelerated benefit ridersis the lesser of the existing amount of such death benefits or a lifetime maximum of $2,000,000.

(9) See your policy for details.This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 10 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Supplemental Benefit Riders limit or expand the policy’s terms of coverage and may increase your premium. Each rider may be subject torequirements and limitations not contained within these explanations. Refer to the policy and riders for a full description of your available riders.

YOUR GUARANTEED WITHDRAWAL BENEFIT RIDER(Form # 15972)

Lifestyle Income Solution (LIS)The Lifestyle Income Solution is an optional rider that helps to protect you against outliving your retirement income. LISprovides you with access to your death benefit in monthly payments when the following requirements are met:

• Your policy and rider have been in effect for at least 15 years, and• The amount of policy premiums paid prior to the initial election date are sufficient to guarantee death benefits until

you reach age 100 (without regard to any waiver benefit under the policy)

Other requirements include:• Death benefit option is level• Policy is not a Modified Endowment Contract (MEC)• Policy has no outstanding loans• Payment of benefit beginning on the initial election date does not cause the policy to fail to meet the definition of life insurance under

Internal Revenue Code (IRC) Section 7702• The policy is not within seven years of a material change as defined by Section 7702A of the IRC on the initial election date• No claim is pending as to any accelerated death benefit under the policy

LIS provides guaranteed withdrawal benefits beginning on the election date for withdrawal benefits and on each month thereafter as long asthe Withdrawal Benefit Balance under the rider is greater than zero and benefit conditions under the rider are being met.

The initial Withdrawal Benefit Balance is calculated on the Initial Election Date and depends on:• the Withdrawal Benefit Basis specified at the time of application multiplied by• an adjustment factor depending on risk class, gender, and the duration since the effective date of rider coverage

YOUR WITHDRAWAL BENEFIT BASISInitial Specified Amount: $500,000% of Initial Specified Amount 100.00%Guaranteed Monthly Withdrawal Benefit Percentage 0.83%

(Equal to 10% Annual)Guaranteed Monthly Withdrawal Benefit Amount $4,166.67(Benefit Payments Begin at Age 85)Minimum # of Monthly Withdrawal Benefit Payments 120

Your Guaranteed Monthly Withdrawal Benefit Amount is determined on the Initial Election date and is equal to your Initial Benefit Balance timesthe Guaranteed Monthly Withdrawal Benefit Percentage.

LIS includes a provision which will waive the amount necessary to prevent the policy from going into grace beginning on the initial election datefor withdrawal benefits and while eligibility requirements under the rider continue to be met.

You may request to receive withdrawal benefit payments of less than the Guaranteed Withdrawal Benefit Amount, subject to Company rulesthen in effect for such payments. You may request a suspension of Guaranteed Withdrawal Benefit Amount payments by notifying the Companyin writing.

Payment of the Guaranteed Withdrawal Benefits Amount may be resumed if the Benefit Eligibility Test is met and the then-current WithdrawalBenefit Balance is greater than zero.

You may not request payment of a withdrawal benefit that exceeds the lesser of the Guaranteed Withdrawal Benefit Amount or the WithdrawalBenefit Balance under this rider.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 11 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Each withdrawal benefit payment will reduce the Withdrawal Benefit Balance by the amount of such withdrawal benefit payment. The WithdrawalBenefit Basis will be reduced in the same proportion as the reduction in the Withdrawal Benefit Balance. Each withdrawal benefit paid will resultin a reduction in the Specified Amount, the Cash Surrender Value, Cash Value, and Continuation Guarantee Account Value of the policy.

The Accumulation Value, Cash Surrender Value, Cash Value and Continuation Guarantee Account value of the policy will be reduced in thesame proportion as the reduction in the Specified Amount of the policy. See the Continuation Guarantee Account section beginning on page .

Note: The cost for this rider will vary by issue age, gender, and underwriting class. Benefits paid under this rider may be taxable. Any withdrawalsthat are not withdrawals of basis may be taxable to the policy owner. If so, you may incur a tax obligation. You should consult your tax advisorfor further information.

Important Information Regarding the Lifestyle Income Solution: If our underwriters determine that you are in overall good health and/or are anon-user of tobacco and/or otherwise have a reasonable expectation of longer life, your premium for the Lifestyle Income Solution may be higherthan the premium for someone whose overall health condition is not as good and/or who uses tobacco, because of the greater potential thatyou may receive benefits under the rider.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 12 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

18

IMPORTANT INFORMATION ABOUT YOUR QUOTATION

Life InsuranceQuote

Your guaranteed Policy Quotation concept shows guaranteed values only.The net annual premium outlay column includes total quoted annual premium for the base policy and any riders lessany loans, dividends and/or surrenders of other policy values, plus any tax consequences that might result from situationssuch as the policy becoming a Modified Endowment Contract.Please refer to the Guaranteed Values section and to the Key Terms section for a complete description of guaranteedvalues including definitions of cash value and death benefit columns.

GuaranteedValues

This quotation is based on guaranteed values provided you make timely payments of the scheduled premiums due asquoted; you do not elect to take policy loans or withdrawals of cash values not otherwise quoted; and you make nomaterial policy changes (e.g., increase of death benefit, add/terminate any riders). This is a quotation only and doesnot constitute an offer or contract. The death benefit is subject to certain policy exclusions such as the suicide orcontestability provisions. Any deviations from the outlined conditions may cause the stated values to no longer be ineffect. The death benefit is subject to certain policy exclusions such as the suicide or contestability provisions. Anydeviations from the outlined conditions may cause the stated values to no longer be in effect.

Periodic Review An in-force quotation may be produced at any time after the policy has been in-force for one year. You should alwaysconsider a periodic review of your insurance coverage with your insurance producer.

Assumptionsand Changes in

Assumptions

This quotation assumes the Company receives all premiums in time to be processed on the first day of each modalperiod, starting with the Date of Issue. This is not likely to occur. Policy values and benefits may also be affected byyour decisions to change elements, such as but not limited to: amount of premium paid, timing of premium payments,lapse and reinstatement, loans, full surrenders, addition/termination of riders, and/or any other Owner-initiated contractualchanges such as increasing or decreasing the death benefit. Actual policy results will be more or less favorable. Youmay request quotations with different assumptions to better understand how the changes affect policyvalues and benefits.Changes to your policy could result in distributions that are subject to tax penalties or limit the amount of future premiumsthat can be paid into the policy.

UnderwritingClass

The underwriting class used in this quotation has a significant impact on the resulting values. Your actual underwritingclass will be determined prior to issue.

KEY TERMS

Cash SurrenderValue

The Cash Surrender Value is the amount available to you when the policy is terminated for a reason other than death.This is equal to the Cash Value less policy loans and accumulated loan interest. This quotation shows the Cash SurrenderValue at the end of each policy year.

Death Benefit The Death Benefit is the amount of money payable to the beneficiary if you die while the policy is in force. The InitialSpecified Amount is specified in the policy at issue and the Specified Amount may be changed subject to the policy’sprovisions. Fees and/or charges may apply when changing the Specified Amount and it may have adverse taxconsequences. Refer to the Tax and Compliance section of this quotation and consult your legal and tax advisor formore information.

Lapse Policy Lapse refers to termination of the policy. When a policy lapses, it has no cash value and no death benefit ispayable. Zeros in the Death Benefit, Accumulation Value, and Cash Surrender Value columns indicate the policy haslapsed under that scenario.

Premium Outlay Premium outlay is the amount you plan to pay. It is equal to planned premium payments plus loan repayments.

ROP (EnhancedSurrender Value)

Your Enhanced Surrender Value Rider is the guaranteed return of premium available. Refer to the Enhanced SurrenderValue section for details.

Withdrawals This represents the amount withdrawn from the policy.

Year and Age Year is the policy year; Age is the Insured's age at the Date of Issue plus the number of years the policy is assumed tohave been in force.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 13 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Your Policy QuotationInitial Annual Premium: $4,959.85Premium Mode: Annual

Guaranteed at 2.00%

Year Age Premium Outlay* Withdrawals ROP (EnhancedSurrender Value) Death Benefit Cash Surrender Value

1 50 4,960 0 500,000 0

2 51 4,960 0 500,000 0

3 52 4,960 0 500,000 0

4 53 4,960 0 500,000 0

5 54 4,960 0 500,000 0

6 55 4,960 0 500,000 0

7 56 4,960 0 500,000 0

8 57 4,960 0 500,000 0

9 58 4,960 0 500,000 0

10 59 4,960 0 500,000 2,790

Subtotal 49,599

11 60 4,960 0 500,000 2,843

12 61 4,960 0 500,000 2,927

13 62 4,960 0 500,000 3,011

14 63 4,960 0 500,000 3,095

15 64 4,960 0 500,000 3,179

16 65 4,960 0 500,000 3,226

17 66 4,960 0 500,000 3,309

18 67 4,960 0 500,000 3,392

19 68 4,960 0 500,000 3,475

20 69 4,960 0 49,599 500,000 4,520

Subtotal 99,197

21 70 4,960 0 500,000 6,451

22 71 4,960 0 500,000 8,545

23 72 4,960 0 500,000 10,675

24 73 4,960 0 500,000 13,065

25 74 4,960 0 123,996 500,000 15,432

26 75 4,960 0 500,000 18,571

27 76 4,960 0 500,000 21,903

28 77 4,960 0 500,000 25,127

29 78 4,960 0 500,000 28,803

30 79 4,960 0 500,000 32,277

Subtotal 148,796

31 80 4,960 0 500,000 36,018

32 81 4,960 0 500,000 39,445

33 82 4,960 0 500,000 42,943

34 83 4,960 0 500,000 47,097

35 84 4,960 0 500,000 50,776

36 85 4,960 0 500,000 56,046This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 14 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Your Policy QuotationInitial Annual Premium: $4,959.85Premium Mode: Annual

Guaranteed at 2.00%

Year Age Premium Outlay* Withdrawals ROP (EnhancedSurrender Value) Death Benefit Cash Surrender Value

37 86 0 0 500,000 59,815

38 87 0 0 500,000 63,340

39 88 0 0 500,000 65,627

40 89 0 0 500,000 66,381

Subtotal 178,555

41 90 0 0 500,000 64,833

42 91 0 0 500,000 62,742

43 92 0 0 500,000 61,331

44 93 0 0 500,000 58,138

45 94 0 0 500,000 52,928

46 95 0 0 500,000 47,253

47 96 0 0 500,000 39,726

48 97 0 0 500,000 30,222

49 98 0 0 500,000 21,718

50 99 0 0 500,000 11,142

Subtotal 178,555

51 100 0 0 500,000 0

52 101 0 0 0 0

53 102 0 0 0 0

54 103 0 0 0 0

55 104 0 0 0 0

56 105 0 0 0 0

57 106 0 0 0 0

58 107 0 0 0 0

59 108 0 0 0 0

60 109 0 0 0 0

Subtotal 178,555

61 110 0 0 0 0

62 111 0 0 0 0

63 112 0 0 0 0

64 113 0 0 0 0

65 114 0 0 0 0

66 115 0 0 0 0

67 116 0 0 0 0

68 117 0 0 0 0

69 118 0 0 0 0

70 119 0 0 0 0

Subtotal 178,555

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 15 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Your Policy QuotationInitial Annual Premium: $4,959.85Premium Mode: Annual

Guaranteed at 2.00%

Year Age Premium Outlay* Withdrawals ROP (EnhancedSurrender Value) Death Benefit Cash Surrender Value

71 120 0 0 0 0

72 121** 0 0 0 0

73 122 0 0 0 0

74 123 0 0 0 0

75 124 0 0 0 0

76 125 0 0 0 0

77 126 0 0 0 0

78 127 0 0 0 0

79 128 0 0 0 0

80 129 0 0 0 0

Subtotal 178,555

81 130 0 0 0 0

82 131 0 0 0 0

Total 178,555*Based on the planned Premium Outlay and other assumptions used in preparing this quotation, the proposed policy, if issued as quoted, willremain in force through policy year 51, Insured's Age 100. The Owner may need to continue or increase premium payments due to certainevents, such as skipping a premium or paying a premium late.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 16 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

YOUR SIGNATURE CONFIRMATION

BY SIGNING THIS FORM, YOU ACKNOWLEDGE THAT YOU HAVE READ, UNDERSTAND, AND AGREE TO THE FOLLOWING STATEMENTS:

I have received a copy of this quotation and understand it is not a contract. I have been advised to consult my own tax or legal advisors regarding the taxeffects of the proposed Coverage. I understand that proper maintenance of the policy is essential, and it is recommended that I regularly review my policy.Annual reviews of my policy include review of the annual statement, review of my in-force quotation, review to determine whether any adjustments arenecessary to my planned premium payments, and review of distributions. I further understand the guarantees are directly affected by the amount or timing ofpremiums paid.

Owner's Signature Date

Joint Owner's Signature Date

I certify that this quotation has been presented to the applicant and that I have explained that the Owner should consult with his or her legal or tax advisor. Ihave made no statements that are inconsistent with the quotation.

WAInsurance Producer's Signature Date Agent's Address

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 17 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

YOUR POLICY FEATURES AND OPTIONSCash Access

PartialWithdrawals

You have the option to access cash from your QoL Guarantee Plus II policy through partial withdrawals. You may takepartial withdrawals from your policy any time after the fifth policy year without losing guarantees, allowing you to maintainyour policy with proportionately reduced premiums, Cash Value accumulation, and Death Benefit. The amount availablefor a partial withdrawal will be the Accumulation Value less surrender charges and any outstanding loans. See yourpolicy for details.

Loans Standard Loans You have the option to access cash from your QoL Guarantee Plus II policy through variable loans. The loan interestdue on variable loans accrues daily at a variable rate. The maximum interest rate charged shall not exceed the greaterof:1. The Moody's Corporate Bond Yield Average - Monthly Average Corporates (hereafter referred to as “Moody's Bond

Yield Average”) for the month of October preceding the calendar year for which the loan interest rate is determined;or

2. The interest rate used to calculate Cash Values under this policy during the period for which the interest rate is beingdetermined, plus 1%.

Preferred Loans You have access to Preferred Loans after ten policy years. The amount that may be taken for a Preferred Loan isrestricted to policy earnings, which is the excess of the Accumulation Value less Surrender Charge, less outstandingloans at the beginning of the year, less the sum of premiums paid over Partial Withdrawals. The amount of PreferredLoan has a guaranteed interest credited rate of 3.00%. The charge rate will equal the interest credited rate and will bea net zero cost.

Other Features

ContinuationGuarantee

Account

Your QoL Guarantee Plus II policy includes a Continuation Guarantee Account (CGA). The CGA can prevent the policyfrom lapsing when the Cash Surrender Value falls to zero. This is shown on the quotation in years where the CashSurrender Value shown is zero, but the Death Benefit continues and is not zero. This quotation assumes that theCompany receives all premiums by the beginning of each modal period, starting with the Date of Issue. Any premiumreceived prior to the next Monthly Deduction Day following its due date will be applied to the CGA as if the premium hadbeen received on the Monthly Deduction Day. Any deviations from the amount, frequency, or timing of premium paymentsor policy elements shown in the quotation may cause the policy not to continue as quoted. The quotation will show azero for the Death Benefit if the Cash Surrender Value is zero and the criteria outlined in the Continuation Guaranteeprovisions and other policy provisions are not met. The Continuation Guarantee does not add value to the Death BenefitProceeds. Refer to the policy for more information about the initial premium.

Effect ofPremium

Payments onYour CGA Value

andAccumulation

Value

a) Your Initial Premium - If Paid on a Timely Basis. This quotation assumes the initial premium is received by theCompany prior to the next Monthly Deduction Day following the Date of Issue. If it is, the policy's CGA will becredited as if the premium had been paid on the Date of Issue. This means that the CGA will be assessed allpolicy charges and credited with interest from the Date of Issue, and the policy's guarantee will remain intact.

b) Your Initial Premium - If Paid Later than the Next Monthly Deduction Day Following the Date of Issue. If the initialpremium is received later than the next Monthly Deduction Day following the Date of Issue, both the AccumulationValue and the CGA will be assessed all policy charges from the Date of Issue, but will be credited with interestonly from the date the initial premium is paid and all other delivery requirements are completed. Because of thepotentially significant impact of late payment (the policy's cash values and guarantees will be impacted), a newquotation will be provided to you upon payment of your initial premium to demonstrate the effect of that timing ofpremium payments has on the policy's Accumulation Value and CGA in future policy years.

c) The new quotation will display the effect upon the policy's CGA and Accumulatoin Value of: (i) assessing all policycharges from the Date of Issue; and (ii) crediting interest only from the Monthly Deduction Day that immediatelyfollows the date you paid the initial premium and all other delivery requirements were completed. Death Benefitcoverage will begin only upon payment of the initial premium to the Company and all other delivery requirementare completed, as is outlined in your application for insurance and if issued, the policy documents.

d) Subsequent Premiums and Continuation Guarantee Account. For purposes of the policy's CGA only, eachsubsequent modal premium you pay prior to the next Monthly Deduction Day following its due date will be creditedas if the premium had been paid on its due date. This means that the CGA will be assessed all policy chargesand credited with interest from the application due date, and the policy's guarantees will remain intact.

e) Subsequent Premiums and Accumulation Value. Your policy's Accumulation Value will also be assessed allcharges as of the due date and interest will be credited only from the date you paid the modal premium.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 18 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

ExternalRollovers

This quotation assumes your External Rollover premium, if any, is received on the Date of Issue. An External Rolloveris Cash Surrender Value from a policy issued by another company that qualifies under Internal Revenue Code section1035. If the entire External Rollover premium is not received by the time this policy is issued, your cash value will beaffected and the policy will not continue as quoted.

Refer to IRC section 1035 for more information about 1035 exchanges. You should also obtain your own legal and taxadvice.

Lump Sum/1035Premium

A 1035 Exchange is an exchange of contracts, generally upon which no gain or loss is recognized under section 1035of the Internal Revenue Code of 1986, as amended. 1035 Premium is premium received from the issuer of one or morelife insurance contracts exchanged for the quoted policy in a 1035 Exchange. A Lump Sum is additional out of-pocketmoney paid in the first policy year above the initial planned premium outlay. A 1035 Exchange may result in non-recognition of gain on the exchange.

Option to ResetDate of Issue

Within twenty calendar days of the date the initial premium is paid, you may elect to have the policy’s Date of Issue resetto the first designated issue date after the initial premium was paid. Such an election must be made in writing. In theevent you elect to have the Date of Issue reset and the date of the initial premium payment was either the 29th, 30th or31st calendar day of the month, the Date of Issue will be reset to the 1st designated issue date of the month followingthe month in which the initial premium was paid.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 19 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

TAX AND COMPLIANCE

GuidelinePremium Test

Under current federal tax law, the policy will qualify as life insurance only if: (a) the sum of premiums paid, less partialsurrenders, at any time does not exceed the greater of the guideline single premium or the sum of the guideline levelannual premiums at such time and (b) the death benefit under the policy at any time is not less than the minimum requiredso that the policy falls within the cash value corridor as prescribed in section 7702(d) of the Internal Revenue Code.

Initial Guideline $15,758.42 Initial Guideline $199,710.80 Seven Pay $23,855.88Level Premium Single Premium Premium

ModifiedEndowment

Contract

The Technical and Miscellaneous Revenue Act of 1988 (“TAMRA”), which is effective for policies issued after June 21,1988, classifies certain policies as Modified Endowment Contracts (“MEC”). A life insurance policy becomes a MEC, asdefined in section 7702A of the Internal Revenue Code, if at any time during the first seven policy years, the actualpremiums paid exceeds the sum of an annually paid "7-Pay Premium". If a policy violates the 7-Pay Premium test, itmay be classified as a MEC retroactively to the time that it was issued. The 7-Pay Premium is the level annual premiumthat could fund all future benefits without regard to loads and expenses under the policy in seven years. All distributions,including loans, from a MEC may be taxable to the extent there is a gain in the policy. In addition, such distributionsprior to age 59 1/2 may be subject to an additional 10.00% penalty. Changes made at any time to a policy will affectthe TAMRA 7-Pay Premium. If appropriate, the owner should discuss the transaction with his insurance, legal, and/ortax advisors.

MEC Status Based on our understanding of the Internal Revenue Code, a policy issued and maintained consistent with theassumptions in this quotation would not be a MEC at issue or become one thereafter. The Owner should ask theCompany to recalculate the 7-Pay Premium before making any change to the policy, including changes that are shownin this quotation. The TAMRA 7-Pay Premium indicated in the Policy Summary section is based upon the lowest specifiedamount in the first seven years.Whether and when your policy might actually become a MEC depends on the timing and amounts of premium paymentsand withdrawals, the policy's non-guaranteed elements, your actual use of the policy's options, and any policy changesmade pursuant to your request. The federal income tax consequences of a MEC can be significant. Consult your taxadvisor for further details.

Replacement ofExisting

Insurance

If the Owner is purchasing a new life insurance policy that will replace an existing policy or if the Owner is using thefunds from one policy to pay all or part of the premiums on a new policy, make sure that these actions are in the Owner’sbest interest. Many times it will be in the Owner’s best interest to keep or modify an existing policy. Depending uponthe type of policies involved, the Owner should gather information to compare such things as: premiums, guaranteedinterest rates, surrender charges, policy fees and expenses, cash surrender values, contract provisions, companyfinancial strength, and tax consequences. Ultimately, it is the Owner’s decision whether to proceed with the transaction.

Policy Loans,Surrenders and

SpecifiedAmount

Reductions

Generally, surrenders from a policy that is not a MEC are not taxable until the amount surrendered exceeds the total ofthe premiums paid, which represents the Owner’s basis in the policy. However, when there is a reduction in the SpecifiedAmount as a result of a partial surrender or at the Owner’s request, there may be a taxable event. A portion of the amountwithdrawn may be taxable under the “Recapture Ceiling Test” described under section 7702(f)(7) of the Internal RevenueCode even if the surrender does not exceed the Owner’s basis in the policy. Reductions in the Specified Amount mayforce a distribution of cash from the policy, a portion of which may be taxable. The Owner should verify whether a taxis incurred before taking surrenders or requesting a reduction in the Specified Amount during the first 15 policy years.Loans are not taxable as long as the policy is not a MEC and remains in force. If a policy lapses or is surrendered, anyoutstanding loans will be treated as if they were distributions and will be subject to income tax to the extent they exceedthe Owner’s basis in the policy.

Company notProviding Legal

or Tax Advice

This material is not intended or written by the Company to be used, and it cannot be used by any taxpayer, for thepurpose of avoiding penalties imposed on the taxpayer. This material is written to support the promotion or marketingof the transaction(s) or matter(s) addressed by this material. Any taxpayer should seek advice based on the taxpayer’sparticular circumstances from an independent tax advisor.

Although the information contained in this quotation is based on our understanding of the Internal Revenue Code andon certain tax and legal assumptions, it is not intended to be tax or legal advice. Such advice should be obtained fromyour own counsel or other tax advisor. Tax laws or interpretations of tax laws can change. This may cause the performanceand underlying tax assumptions of this policy, including any riders, to be different than quoted. For example, tax lawchanges may result in distributions that are more or less than quoted. In some cases, these changes could result in adecrease in policy values or lapse. After the first policy year, you should periodically request an in-force quotation fromyour insurance producer to monitor your policy’s performance in light of any tax law changes. Your actual taxes may bedifferent from what is quoted.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 20 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Policy Changesand Extending

Coverage

The Company will not permit a change to the policy that would result in the policy not meeting the definition of lifeinsurance under section 7702 of the Internal Revenue Code. The 2001 CSO Mortality Tables provide a stated terminationdate of age 121. The Option to Extend Coverage allows the policy to continue beyond age 121. The tax consequencesof extending the Maturity Date beyond the age 121 termination date of the 2001 CSO Mortality Tables are unclear. TheOwner should consult with a personal tax adviser about the effect of any changes to the policy as it relates to section7702 and the termination date of the Mortality Tables since, after the insured reaches the attained age 121, this policymay not qualify as life insurance under the federal income tax definition of life insurance and may be subject to adversetax consequences.

AcceleratedDeath Benefit

Rider

Benefits payable under an accelerated death benefit rider may be taxable. If so, you may incur a tax obligation. NeitherAmerican General Life Insurance Company nor any agent representing it is authorized to give legal or tax advice. Pleaseconsult a qualified legal or tax advisor regarding questions concerning the information and concepts contained in thismaterial.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 21 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

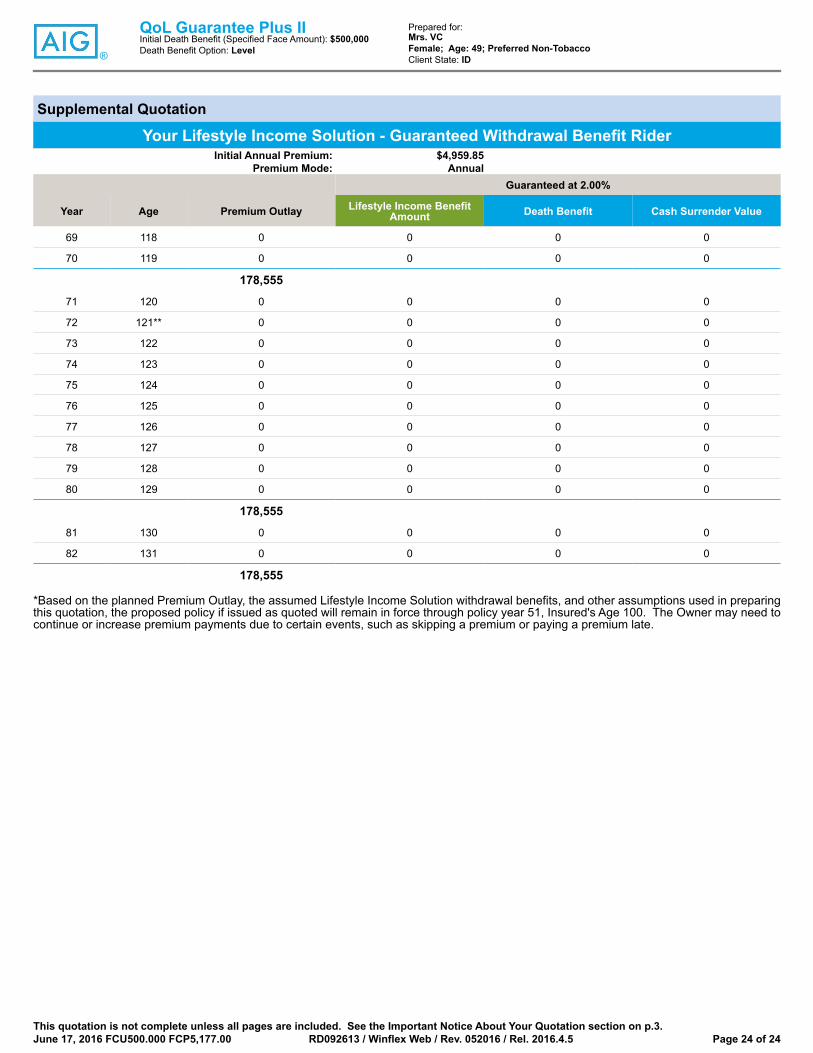

Supplemental Quotation

Your Lifestyle Income Solution - Guaranteed Withdrawal Benefit RiderInitial Annual Premium: $4,959.85

Premium Mode: AnnualGuaranteed at 2.00%

Year Age Premium Outlay Lifestyle Income BenefitAmount Death Benefit Cash Surrender Value

1 50 4,960 0 500,000 0

2 51 4,960 0 500,000 0

3 52 4,960 0 500,000 0

4 53 4,960 0 500,000 0

5 54 4,960 0 500,000 0

6 55 4,960 0 500,000 0

7 56 4,960 0 500,000 0

8 57 4,960 0 500,000 0

9 58 4,960 0 500,000 0

10 59 4,960 0 500,000 2,790

49,599

11 60 4,960 0 500,000 2,843

12 61 4,960 0 500,000 2,927

13 62 4,960 0 500,000 3,011

14 63 4,960 0 500,000 3,095

15 64 4,960 0 500,000 3,179

16 65 4,960 0 500,000 3,226

17 66 4,960 0 500,000 3,309

18 67 4,960 0 500,000 3,392

19 68 4,960 0 500,000 3,475

20 69 4,960 0 500,000 4,520

99,197

21 70 4,960 0 500,000 6,451

22 71 4,960 0 500,000 8,545

23 72 4,960 0 500,000 10,675

24 73 4,960 0 500,000 13,065

25 74 4,960 0 500,000 15,432

26 75 4,960 0 500,000 18,571

27 76 4,960 0 500,000 21,903

28 77 4,960 0 500,000 25,127

29 78 4,960 0 500,000 28,803

30 79 4,960 0 500,000 32,277

148,796

31 80 4,960 0 500,000 36,018

32 81 4,960 0 500,000 39,445

33 82 4,960 0 500,000 42,943

34 83 4,960 0 500,000 47,097

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 22 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Supplemental Quotation

Your Lifestyle Income Solution - Guaranteed Withdrawal Benefit RiderInitial Annual Premium: $4,959.85

Premium Mode: AnnualGuaranteed at 2.00%

Year Age Premium Outlay Lifestyle Income BenefitAmount Death Benefit Cash Surrender Value

35 84 4,960 0 500,000 50,776

36 85 4,960 0 500,000 56,046

37 86 0 50,000 450,000 48,091

38 87 0 50,000 400,000 40,115

39 88 0 50,000 350,000 31,076

40 89 0 50,000 300,000 22,759

178,555

41 90 0 50,000 250,000 15,091

42 91 0 50,000 200,000 8,997

43 92 0 50,000 150,000 4,506

44 93 0 50,000 100,000 0

45 94 0 50,000 50,000 0

46 95 0 50,000 0 0

47 96 0 0 0 0

48 97 0 0 0 0

49 98 0 0 0 0

50 99 0 0 0 0

178,555

51 100 0 0 0 0

52 101 0 0 0 0

53 102 0 0 0 0

54 103 0 0 0 0

55 104 0 0 0 0

56 105 0 0 0 0

57 106 0 0 0 0

58 107 0 0 0 0

59 108 0 0 0 0

60 109 0 0 0 0

178,555

61 110 0 0 0 0

62 111 0 0 0 0

63 112 0 0 0 0

64 113 0 0 0 0

65 114 0 0 0 0

66 115 0 0 0 0

67 116 0 0 0 0

68 117 0 0 0 0

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 23 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Supplemental Quotation

Your Lifestyle Income Solution - Guaranteed Withdrawal Benefit RiderInitial Annual Premium: $4,959.85

Premium Mode: AnnualGuaranteed at 2.00%

Year Age Premium Outlay Lifestyle Income BenefitAmount Death Benefit Cash Surrender Value

69 118 0 0 0 0

70 119 0 0 0 0

178,555

71 120 0 0 0 0

72 121** 0 0 0 0

73 122 0 0 0 0

74 123 0 0 0 0

75 124 0 0 0 0

76 125 0 0 0 0

77 126 0 0 0 0

78 127 0 0 0 0

79 128 0 0 0 0

80 129 0 0 0 0

178,555

81 130 0 0 0 0

82 131 0 0 0 0

178,555

*Based on the planned Premium Outlay, the assumed Lifestyle Income Solution withdrawal benefits, and other assumptions used in preparingthis quotation, the proposed policy if issued as quoted will remain in force through policy year 51, Insured's Age 100. The Owner may need tocontinue or increase premium payments due to certain events, such as skipping a premium or paying a premium late.

This quotation is not complete unless all pages are included. See the Important Notice About Your Quotation section on p.3.June 17, 2016 FCU500.000 FCP5,177.00 RD092613 / Winflex Web / Rev. 052016 / Rel. 2016.4.5 Page 24 of 24

®

QoL Guarantee Plus IIInitial Death Benefit (Specified Face Amount): $500,000Death Benefit Option: Level

Prepared for:Mrs. VCFemale; Age: 49; Preferred Non-TobaccoClient State: ID

Client Input Summary

Company:

Product:

American General Life Insurance Company

QoL Guarantee Plus II

June 17, 2016

2.51.00, 7.31.04

Insured

Client Name Mrs. VC

Sex Female

Date of Birth

Age 49

Save Age?

Class Preferred Non-Tobacco

Table Rating

Temporary Flat Extra

Permanent Flat Extra

State of Issue Idaho

Solve For

Solve For Premium

Premium Solve Option Guarantee Premium

Guarantee Age @100

Face Amount 01 to 99 - 500,000

Years to Pay Premium

Living Benefit Option Yes

Accelerated Access Solution - AAS

Lifestyle Income Solution - LIS Yes

Asset Protector Living Benefits Bundle - AAS & LIS

Years/Age to Pay Premium @85

LIS Monthly Benefit Amount

LIS Start Age 85

LIS Benefit Percentage 100

AAS Death Benefit Percentage

Monthly Benefit Payout Amount

Disbursements

Disbursements No

Policy Options

Death Benefit Option Level

Premium Payment Mode Annually

Death Benefit Compliance Test Guideline

External 1035 Amount

Internal 1035 Amount

Policy Is A Mec

External Lump Sum Amount 01 to 121 - 0

Internal Lump Sum Amount 01 to 121 - 0

Page 1 of 3

Client Input Summary

Company:

Product:

American General Life Insurance Company

QoL Guarantee Plus II

June 17, 2016

2.51.00, 7.31.04

Policy Options - Cont'd

Revised Quote? No

Financial Institution? No

Discounts

Are you applying for QoL Flex Term at the same time as base UL Policy? No

Will you be the same owner as the Associated UL Policy?

Will you use the same ABC billing as the Associated UL Policy?

Class

Table Rating

Permanent Flat

Temporary Flat

For Years

1 - Face Amount

Level Premium Period

2 - Face Amount

Level Premium Period

3 - Face Amount

Level Premium Period

4 - Face Amount

Level Premium Period

5 - Face Amount

Level Premium Period

Total Coverage

Riders

QoL Accelerated Benefit Riders - Critical, Chronic, Terminal Yes

Waiver of Monthly Deduction No

Waiver Rating

Enhanced Surrender Value Rider [ROP]

Maturity Extension Rider

Accidental DB No

Accidental DB Amount

Child Insurance Benefit No

Number of CIB Units

Age to End CIB Rider

Spouse/Other Insured Term Rider No

Spouse/OI Term Units

Spouse/OI Term Age to End

Spouse/OI Sex

Spouse/OI Age

Spouse/OI Smoker

Page 2 of 3

Client Input Summary

Company:

Product:

American General Life Insurance Company

QoL Guarantee Plus II

June 17, 2016

2.51.00, 7.31.04

Riders - Cont'd

Spouse/OI Table Rating

Reports

Quote? Yes

IRR Report? No

Preliminary Information Statement

Policy Summary?

Disclosure of Policy Charges? No

Quote IRA Strategy

IRA Concept?

Prior Year End IRA Value

Hypothetical Annual Growth Rate %

Beneficiary Hypothetical Tax Rate %

IRA Owner's Hypothetical Tax Rate %

Withdraw Excess Premium from IRA?

Agent Info

Agent Name Lee Rogers

Agent Company

Agent Address1

Agent Address2

Agent Address3

Agent City

Agent State Washington

Agent Zip Code

Agent Phone

Agent Fax

Agent Email

Agent License #

Access

Access Code

Access Code

Access Code

Access Code

Access Code

Page 3 of 3