aim seminar 1/20/15

TRANSCRIPT

Welcome to the Seminar

Denver, 2015

Accessing the Global Markets Through LondonDenver Seminar

20th January 2015

3

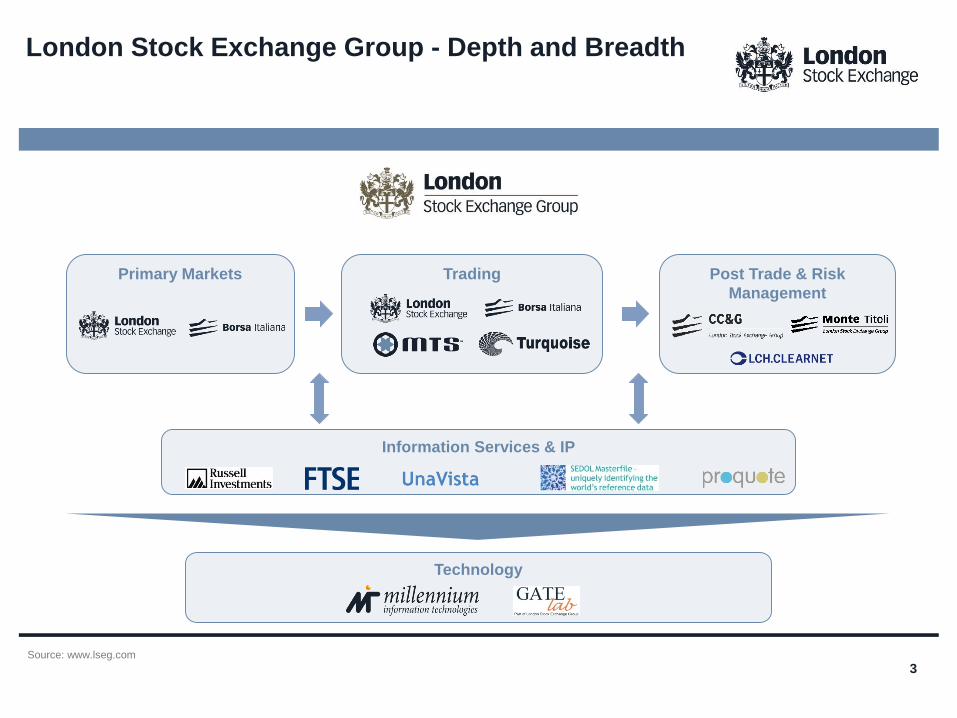

London Stock Exchange Group - Depth and Breadth

Source: www.lseg.com

Primary Markets Trading Post Trade & Risk

Management

Information Services & IP

Technology

4

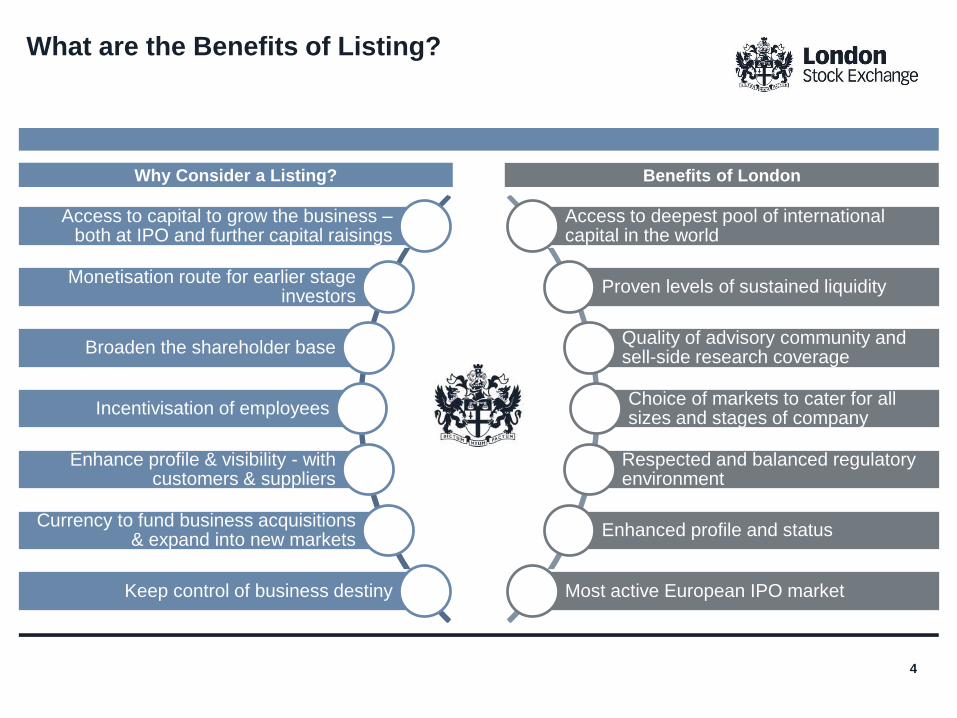

Access to capital to grow the business –both at IPO and further capital raisings

Monetisation route for earlier stage investors

Broaden the shareholder base

Incentivisation of employees

Enhance profile & visibility - with customers & suppliers

Currency to fund business acquisitions & expand into new markets

Keep control of business destiny

What are the Benefits of Listing?

Access to deepest pool of international capital in the world

Proven levels of sustained liquidity

Quality of advisory community and sell-side research coverage

Choice of markets to cater for all sizes and stages of company

Respected and balanced regulatory environment

Enhanced profile and status

Most active European IPO market

Why Consider a Listing? Benefits of London

5

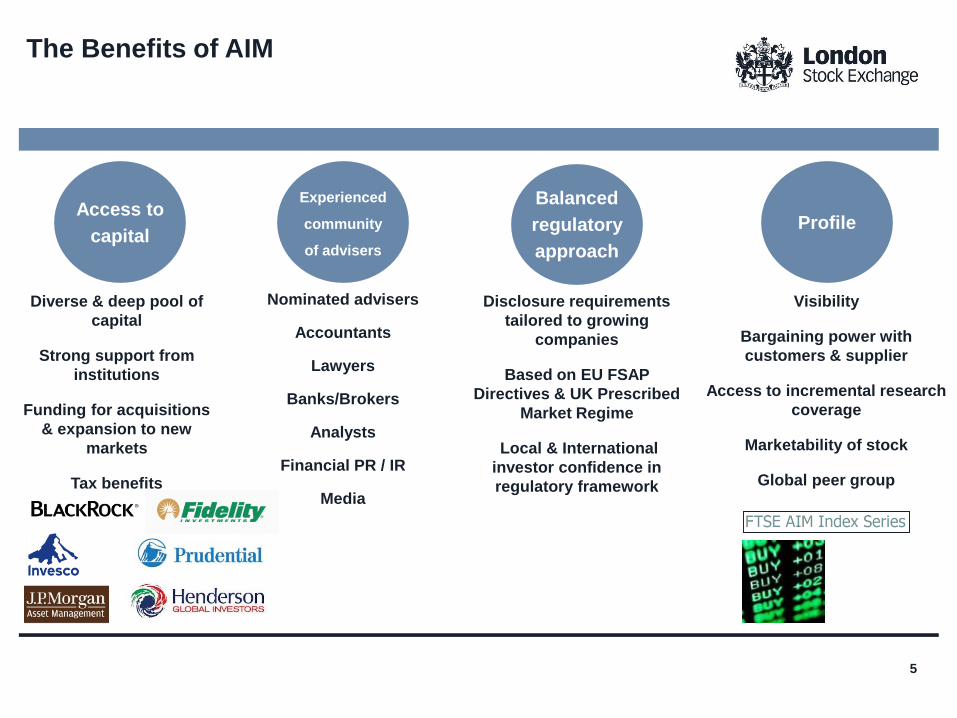

Diverse & deep pool of

capital

Strong support from

institutions

Funding for acquisitions

& expansion to new

markets

Tax benefits

The Benefits of AIM

Access to

capital

Experienced

community

of advisers

Profile

Nominated advisers

Accountants

Lawyers

Banks/Brokers

Analysts

Financial PR / IR

Media

Visibility

Bargaining power with

customers & supplier

Access to incremental research

coverage

Marketability of stock

Global peer group

Balanced

regulatory

approach

Disclosure requirements

tailored to growing

companies

Based on EU FSAP

Directives & UK Prescribed

Market Regime

Local & International

investor confidence in

regulatory framework

6

0

1

2

3

4

5

6

7

8

2009 2010 2011 2012 2013 2014

Mo

ney r

ais

ed

(£b

n)

Further

New

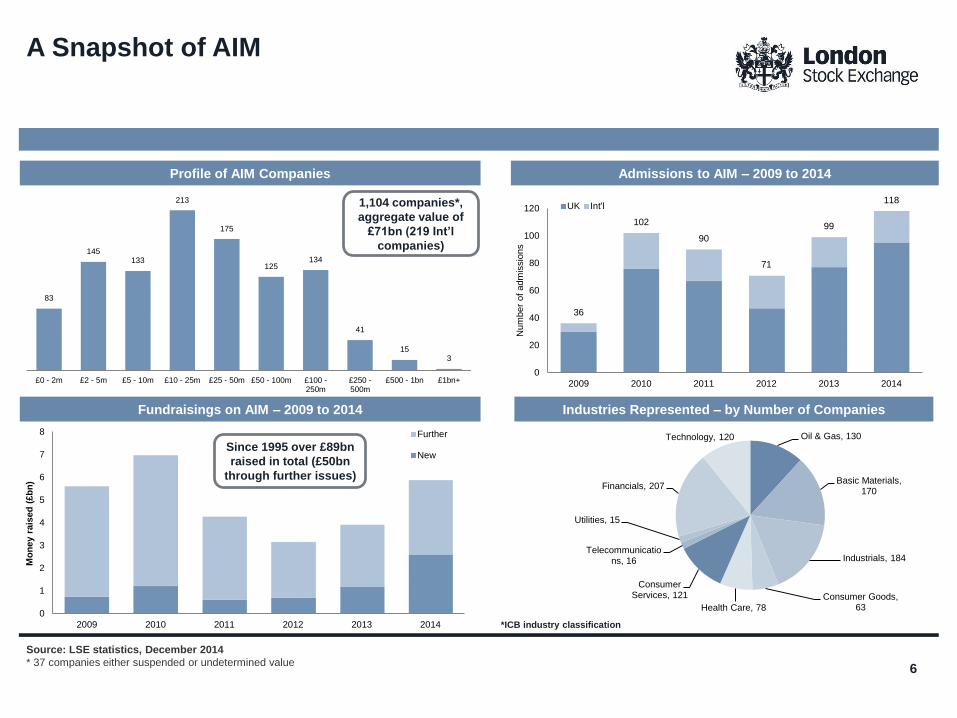

1,104 companies*,

aggregate value of

£71bn (219 Int’l

companies)

A Snapshot of AIM

Source: LSE statistics, December 2014

* 37 companies either suspended or undetermined value

*ICB industry classification

Since 1995 over £89bn

raised in total (£50bn

through further issues)

Profile of AIM Companies Admissions to AIM – 2009 to 2014

Industries Represented – by Number of CompaniesFundraisings on AIM – 2009 to 2014

315

41

134125

175

213

133145

83

£1bn+£500 - 1bn£250 -500m

£100 -250m

£50 - 100m£25 - 50m£10 - 25m£5 - 10m£2 - 5m£0 - 2m

36

102

90

71

99

118

0

20

40

60

80

100

120

2009 2010 2011 2012 2013 2014

Num

ber

of

adm

issio

ns

UK Int'l

Oil & Gas, 130

Basic Materials, 170

Industrials, 184

Consumer Goods, 63Health Care, 78

Consumer Services, 121

Telecommunications, 16

Utilities, 15

Financials, 207

Technology, 120

7

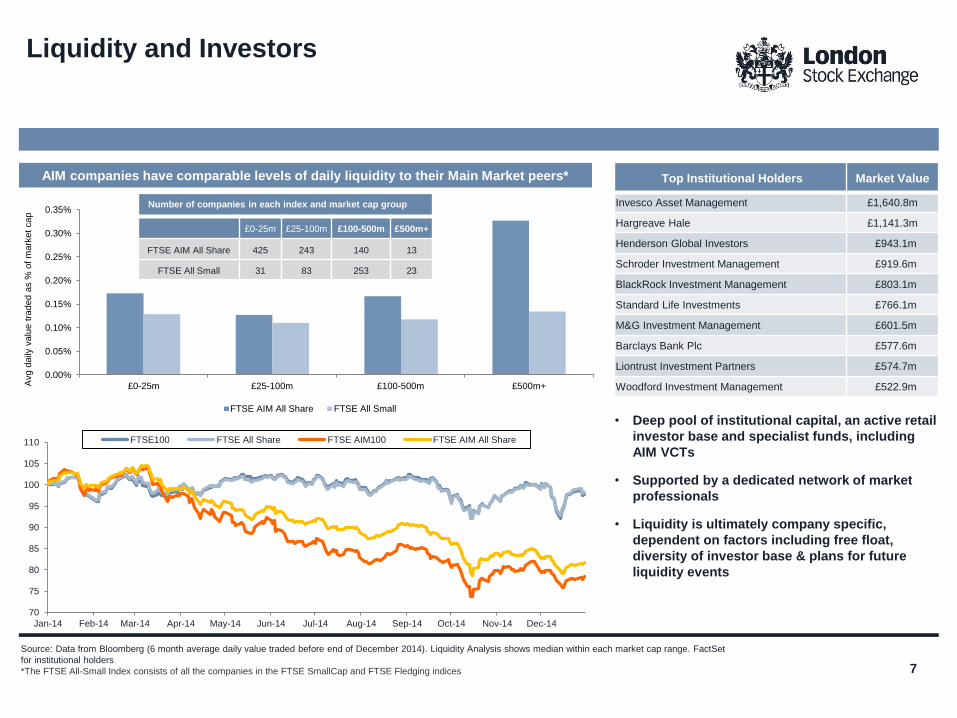

0.00%

0.05%

0.10%

0.15%

0.20%

0.25%

0.30%

0.35%

£0-25m £25-100m £100-500m £500m+Avg d

aily

valu

e t

raded a

s %

of

mark

et

cap

FTSE AIM All Share FTSE All Small

Liquidity and Investors

Source: Data from Bloomberg (6 month average daily value traded before end of December 2014). Liquidity Analysis shows median within each market cap range. FactSet

for institutional holders

*The FTSE All-Small Index consists of all the companies in the FTSE SmallCap and FTSE Fledging indices

• Deep pool of institutional capital, an active retail

investor base and specialist funds, including

AIM VCTs

• Supported by a dedicated network of market

professionals

• Liquidity is ultimately company specific,

dependent on factors including free float,

diversity of investor base & plans for future

liquidity events

Top Institutional Holders Market Value

Invesco Asset Management £1,640.8m

Hargreave Hale £1,141.3m

Henderson Global Investors £943.1m

Schroder Investment Management £919.6m

BlackRock Investment Management £803.1m

Standard Life Investments £766.1m

M&G Investment Management £601.5m

Barclays Bank Plc £577.6m

Liontrust Investment Partners £574.7m

Woodford Investment Management £522.9m

Number of companies in each index and market cap group

£0-25m £25-100m £100-500m £500m+

FTSE AIM All Share 425 243 140 13

FTSE All Small 31 83 253 23

AIM companies have comparable levels of daily liquidity to their Main Market peers*

70

75

80

85

90

95

100

105

110

Jan-14 Feb-14 Mar-14 Apr-14 May-14 Jun-14 Jul-14 Aug-14 Sep-14 Oct-14 Nov-14 Dec-14

FTSE100 FTSE All Share FTSE AIM100 FTSE AIM All Share

8

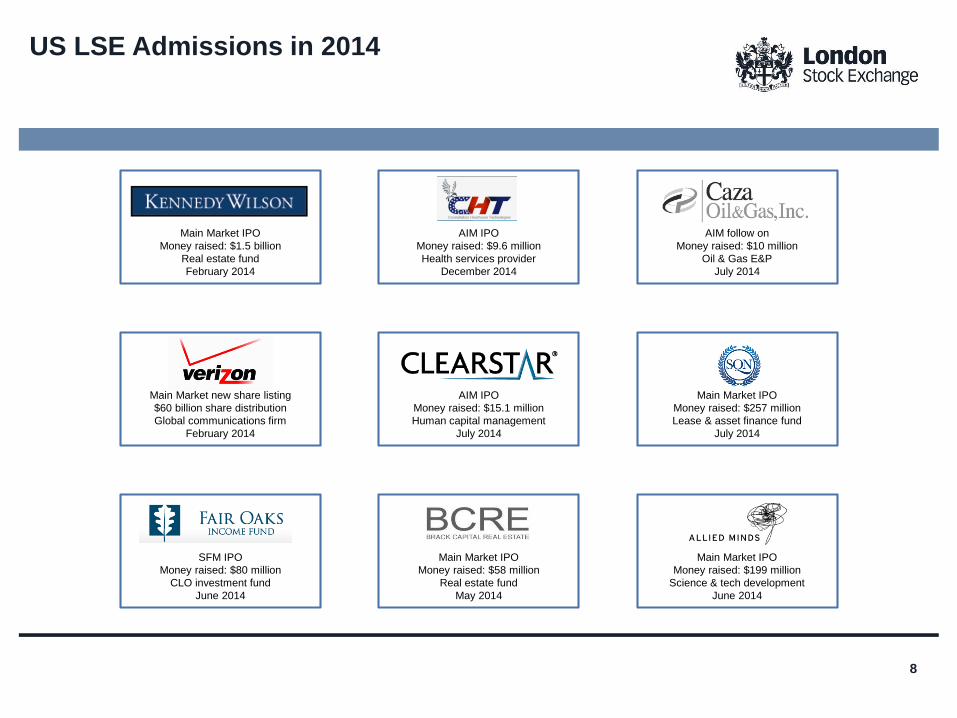

US LSE Admissions in 2014

Main Market IPO

Money raised: $1.5 billion

Real estate fund

February 2014

AIM IPO

Money raised: $9.6 million

Health services provider

December 2014

Main Market IPO

Money raised: $257 million

Lease & asset finance fund

July 2014

AIM IPO

Money raised: $15.1 million

Human capital management

July 2014

Main Market IPO

Money raised: $199 million

Science & tech development

June 2014

SFM IPO

Money raised: $80 million

CLO investment fund

June 2014

Main Market IPO

Money raised: $58 million

Real estate fund

May 2014

Main Market new share listing

$60 billion share distribution

Global communications firm

February 2014

AIM follow on

Money raised: $10 million

Oil & Gas E&P

July 2014

9

This document has been compiled by the London Stock Exchange plc (the “Exchange”). The Exchange has attempted to ensure that the information in thisdocument is accurate, however the information is provided “AS IS” and on an “AS AVAILABLE” basis and may not be accurate or up to date.

The Exchange does not guarantee the accuracy, timeliness, completeness, performance or fitness for a particular purpose of the document or any of theinformation in it. The Exchange is not responsible for any third party content which is set out in this document. No responsibility is accepted by or on behalf ofthe Exchange for any errors, omissions, or inaccurate information in the document.

No action should be taken or omitted to be taken in reliance upon information in this document. The Exchange accepts no liability for the results of any actiontaken on the basis of the information in this document.

All implied warranties, including but not limited to the implied warranties of satisfactory quality, fitness for a particular purpose, non-infringement, compatibility,security and accuracy are excluded by the Exchange to the extent that they may be excluded as a matter of law. Further, the Exchange does not warrant thatthe document is error free or that any defects will be corrected.

To the extent permitted by applicable law, the Exchange expressly disclaims all liability howsoever arising whether in contract, tort (or deceit) or otherwise(including, but not limited to, liability for any negligent act or omissions) to any person in respect of any claims or losses of any nature, arising directly orindirectly from: (i) anything done or the consequences of anything done or omitted to be done wholly or partly in reliance upon the whole or any part of thecontents of this document, and (ii) the use of any data or materials in this document.

Information in this document is not offered as advice on any particular matter and must not be treated as a substitute for specific advice. In particularinformation in the document does not constitute professional, financial or investment advice and must not be used as a basis for making investment decisionsand is in no way intended, directly or indirectly, as an attempt to market or sell any type of financial instrument. Advice from a suitably qualified professionalshould always be sought in relation to any particular matter or circumstances.

The contents of this document do not constitute an invitation to invest in shares of the Exchange, or constitute or form a part of any offer for the sale orsubscription of, or any invitation to offer to buy or subscribe for, any securities or other financial instruments, nor should it or any part of it form the basis of, orbe relied upon in any connection with any contract or commitment whatsoever.

London Stock Exchange and the London Stock Exchange coat of arms device are registered trade marks of London Stock Exchange plc. Other logos,organisations and company names referred to may be the trade marks of their respective owners.

© January 2015

London Stock Exchange plc10 Paternoster Square

London EC4M 7LSTelephone +44 (0)20 7797 1000

www.lseg.com

Legal Disclaimer

10

Other Details

Dorsey & Whitney (Europe) LLP

199 Bishopsgate

London EC2M 3UT

Phone: +44 (0)20 7031 3700

Fax: +44 (0)20 7031 3799

Aim Seminar

January 20, 2015

What is Capital 33?

1/20/2015 www.Capital33.net 12

Companies that May Qualify for AIM

• High-growth

• Revenue-producing (generally)

• Have an international component

• Can produce a healthy return

1/20/2015 www.Capital33.net 13

Why AIM Over US Public Markets?

• Less Complexity

• Lower Cost

• No Share limits

• No Min. Market Cap

• Lower Ongoing costs

• For growth stage companies

• Liquidity

• A different league to OTC, NYSE MKT

1/20/2015 www.Capital33.net 14

AIM Business Verticals

• Finance

• Consumer Services

• Energy

• Healthcare

• Technology

• Industrial

1/20/2015 www.Capital33.net 15

The Capital 33 Process

1. Exploration

2. Due Diligence

3. Document & Roadshow Preparation

4. Choosing Professional Service Providers

1/20/2015 www.Capital33.net 16

5. Pre-IPO Process

6. IPO

7. Ongoing PR, IR, Content Support

Other Reasons to Choose AIM

• Designed for Growth

• Secondary Market

• International Focus

• Potential Tax Advantages

1/20/2015 www.Capital33.net 17

Thank You!

James WallPrincipal, Capital 33303-894-3130 ext. [email protected]

Vincent DipasPrincipal, Capital [email protected]

1/20/2015 www.Capital33.net 18

Dorsey & Whitney – Preparing for an AIM IPO

4835-6552-6817

20Dorsey – A Global Business Law Firm

Dorsey is an international firm with over 550 lawyers in North America, Europe and Asia. Some of the world’s most successful

companies count on Dorsey to help them meet legal and business challenges. From technology, life sciences, health and pharma, to

energy, media, financial services and manufacturing, companies turn to us for assistance with legal issues that impact their business.

21Firm – Awards & Recognition

• Dorsey ranked No. 27 among the top 100 largestsecurities practices in the U.S. by Law360.

• 105 Dorsey lawyers representing 57 practice areaswere recognized in the 2014 edition of U.S. News’listing of Best Lawyers.

• Five Dorsey partners are members of the AmericanCollege of Trial Lawyers (ACTL). Membership in theACTL is by invitation only and is limited to only 1% oftotal lawyers per state or Canadian province.

• In 2013, World Trademark Review recognizedDorsey and six of its Trademark lawyers in its annualWorld Trademark Review 1000 - The World’sLeading Trademark Professionals.

• According to Thomson Reuters, Dorsey ranked No. 5for the number of announced Mid-Market M&A dealsin the U.S. in 2013 (#6 for Small-Cap deals). Dorseyranked #6 for the number of completed U.S. deals(any size) and #15 for the number of completed dealsworldwide in 2013.

• M&A Law Firm of the Year in China by Global LawExperts in 2014.

• Dorsey has twice been named “U.S. Mining Law Firmof the Year” by ACQ Magazine in its ACQ FinanceMagazine Country Law Awards. Dorsey was named2011 “Mining Law Firm of the Year” by LawyersWorld Law Awards and 2011 “Law Firm of the Year –Mining” by InterContinental Finance Magazine.

21

• Dorsey consistently ranks in the “BTI Client Service A-

Team” (including in 2014).

• Dorsey is recognized as a “Leading Firm" by Chambers

USA. Chambers USA also recognized 52 attorneys in 21

practices in its 2013 edition.

• Dorsey is an AMLAW 100 firm, according to American

Lawyer Magazine and a Top 100 Most Prestigious Firm

according to Vault.

• Dorsey was ranked in U.S. News 2015 Best Law Firms in

26 national categories and 102 local categories for various

metropolitan areas. 97 Dorsey lawyers were honored as

U.S. News 2015 Best Lawyers.

• Dorsey is the only firm ranked Top 10 by volume for US

M&A for each of the past 20 years (Thomson Reuters)

• Dorsey represents many well known Fortune 1000

companies throughout the US, including:

• UnitedHealth Group

• SUPERVALU

• U.S. Bank

• Hormel Foods

• St. Jude Medical

• Apple

• Procter & Gamble

• Medtronic

• Honeywell

• Delta Air Lines

• ConocoPhillips

• Micron Technology

• Wells Fargo

• The Mosaic Company

• Land O’Lakes

• Ameriprise Financial

• Target

• C.H. Robinson

22London – Overview

Services

Dorsey & Whitney’s London office serves as the backbone

of our European capabilities, providing excellent service to

clients globally.

Opened in 1986, it has grown to more than 30 partners,

associates and counsel. Our lawyers in the London office

have special expertise in the following areas:

• Anti-Corruption

• Construction and Engineering Projects

• Commercial Litigation

• Corporate and M&A

• Corporate Tax

• Emerging Companies and Venture Capital

• Employment

• Fraud and Regulatory Investigations

• International Arbitration

• International Banking and Finance

• International Capital Markets

• Intellectual Property

• Real Estate

Approach

• Our multi-jurisdictional and multi-lingual lawyers offer both

UK and US law capability in order to provide clients with the

most appropriate legal advice and services for their specific

needs.

• Lawyers in London regularly work in conjunction with

lawyers in the firm’s US and Asia offices on international

matters of finance, trade and commerce.

• The firm has developed a specialty in advising Norwegian,

Danish and Swedish companies on their entry into the

international capital markets and in working with global

companies accessing Scandinavian finance.

• The London office’s fraud and regulatory specialists

combine with US counterparts to provide an internal fraud

investigations service for clients with trans-Atlantic

interests.

• Dorsey’s London office prides itself on operating as a

stand-alone mid-market City practice with a cost-effective

offering.

23London – Awards & Recognition 23

• Firm and individuals ranked across multiple core practice areas by Legal 500 and by Chambers UK

• Corporate INTLMagazine Global Award named Dorsey’s London office:

o 2014 - Cross-Border M&A Law Firm of the Year (England) and Securities & Capital Markets Law Firm of

the Year (UK)

o 2013 and 2014 - Litigation Law Firm of the Year in England

o 2013 - Anti-Corruption Law Firm of the Year in England

o 2012 - UK Litigation Firm of the Year

• No. 1 underwriter counsel and No. 2 issuer counsel for AIM IPOs by deal volume in 2011 by Bloomberg.

• UK Capital Markets Law Firm of the Year for 2011 and 2012 by Lawyer Monthly.

• M&A Law Firm of the Year (UK) for 2014 by Finance Monthly.

• India Deal of the Year award in 2010, 2009 and 2007 by India Business Law Journal

24

Liberty Global plc

$422m private placement and resale

shelf registration

Keywords Studios plc

£49m AIM IPO and £6m secondary

fundraise – advised Numis

Securities Limited as nominated

adviser and broker

Oxford BioMedica plc

£21.6m firm placing, subscription

and open offer – advised Charles

Stanley & Co. Limited and WG

Partners LLP

Velocys Group plc

£52m secondary fundraise –

advised Numis Securities Limited

as nominated adviser and broker

London – Capital Markets Transactions

Rightster Group plc

£70m AIM IPO and £42m secondary

fundraise – advised Cenkos

Securities plc as nominated adviser

and broker

Primary Health Properties plc

£82.5m convertible bond issue –

advised ISM Capital as lead

manager

Heritage Bank Ltd

$100m convertible bond issue –

advised 46 Parallel Ltd as

cornerstone investor

AudioBoom Group plc

Reverse takeover and AIM

readmission – advised Arden

Partners plc as nominated adviser

Monitise plc

£100m placing – advised

Canaccord Genuity Limited as

nominated adviser and broker

Quindell plc

£200m institutional placing

JKX Oil & Gas plc

$48m convertible bond issue:

placing and open offer

Digital Barriers plc

£25m AIM IPO and £30m follow-on

placing – advised Investec as

nominated adviser and broker

Bio City Development Company

$200m convertible bond issue –

advised ISM Capital as lead

manager

ClearStar Inc.

£20m AIM IPO and placing –

advised Cenkos Securites plc as

nominated adviser and broker

SKIL Ports & Logistics Ltd

£110m AIM IPO and Rule 144A

offering

Corero Network Security Plc

Strategic investment into AIM-listed

Corero Plc – and subsequent

placing and acquisition / reverse

takeover of Top Layer Networks Inc

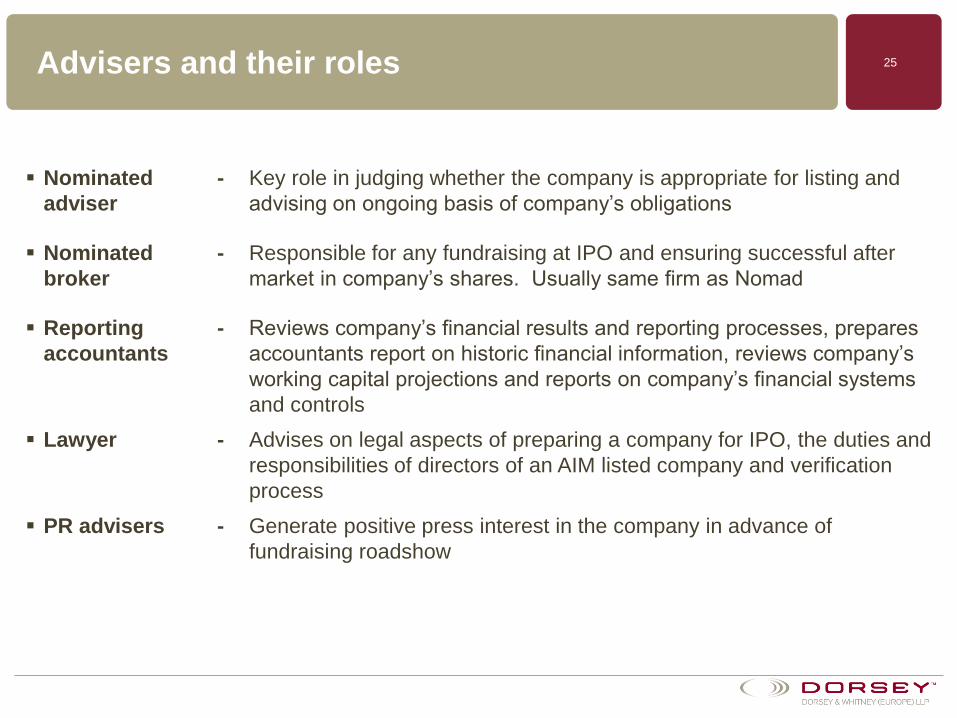

25Advisers and their roles

Nominated

adviser

- Key role in judging whether the company is appropriate for listing and

advising on ongoing basis of company’s obligations

Nominated

broker

- Responsible for any fundraising at IPO and ensuring successful after

market in company’s shares. Usually same firm as Nomad

Reporting

accountants

- Reviews company’s financial results and reporting processes, prepares

accountants report on historic financial information, reviews company’s

working capital projections and reports on company’s financial systems

and controls

Lawyer - Advises on legal aspects of preparing a company for IPO, the duties and

responsibilities of directors of an AIM listed company and verification

process

PR advisers - Generate positive press interest in the company in advance of

fundraising roadshow

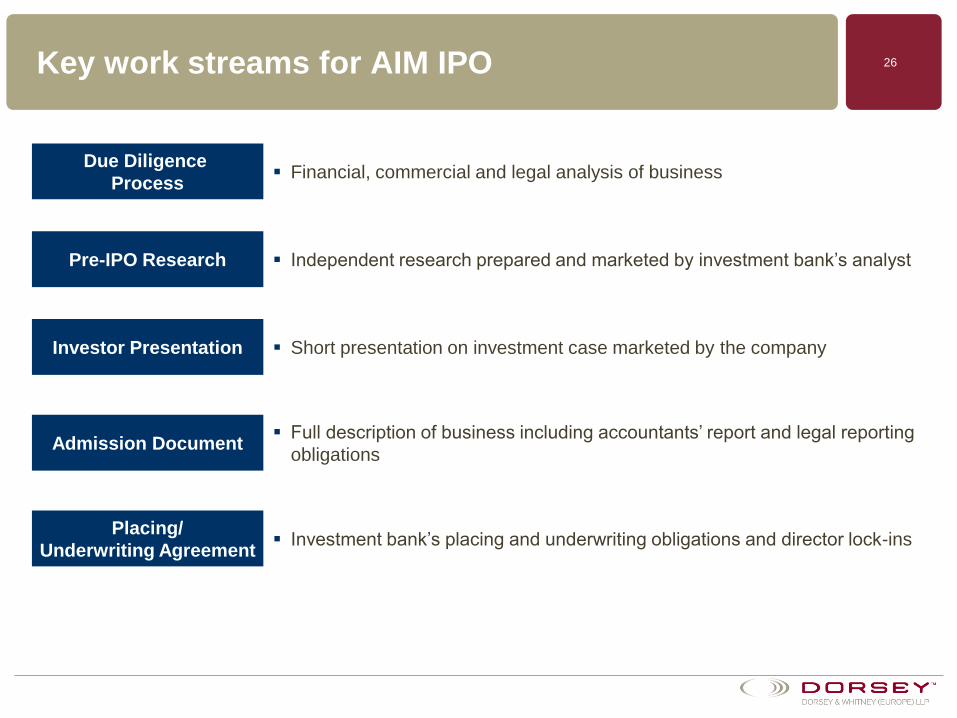

26Key work streams for AIM IPO

Financial, commercial and legal analysis of businessDue Diligence

Process

Independent research prepared and marketed by investment bank’s analystPre-IPO Research

Short presentation on investment case marketed by the companyInvestor Presentation

Full description of business including accountants’ report and legal reporting

obligationsAdmission Document

Investment bank’s placing and underwriting obligations and director lock-insPlacing/

Underwriting Agreement

27Potential issues to consider

Planned re-financings or disposals

Pre-IPO reorganisation

Corporate governance and other UK investor requirements

Directors service agreements/board composition

Any existing shareholders to remain significant shareholders on IPO

Management and major shareholders likely to be locked-in

Share option schemes/stock plans

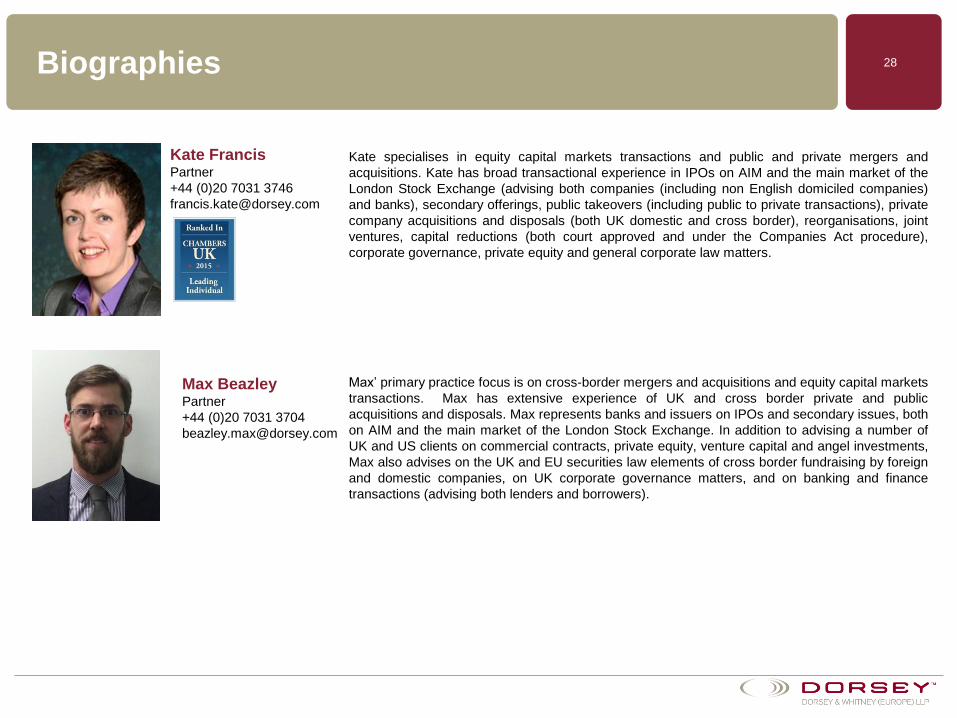

28Biographies

Kate FrancisPartner

+44 (0)20 7031 3746

Kate specialises in equity capital markets transactions and public and private mergers and

acquisitions. Kate has broad transactional experience in IPOs on AIM and the main market of the

London Stock Exchange (advising both companies (including non English domiciled companies)

and banks), secondary offerings, public takeovers (including public to private transactions), private

company acquisitions and disposals (both UK domestic and cross border), reorganisations, joint

ventures, capital reductions (both court approved and under the Companies Act procedure),

corporate governance, private equity and general corporate law matters.

Max BeazleyPartner

+44 (0)20 7031 3704

Max’ primary practice focus is on cross-border mergers and acquisitions and equity capital markets

transactions. Max has extensive experience of UK and cross border private and public

acquisitions and disposals. Max represents banks and issuers on IPOs and secondary issues, both

on AIM and the main market of the London Stock Exchange. In addition to advising a number of

UK and US clients on commercial contracts, private equity, venture capital and angel investments,

Max also advises on the UK and EU securities law elements of cross border fundraising by foreign

and domestic companies, on UK corporate governance matters, and on banking and finance

transactions (advising both lenders and borrowers).

29Other Details

Dorsey & Whitney (Europe) LLP

199 Bishopsgate

London EC2M 3UT

Phone: +44 (0)20 7031 3700

Fax: +44 (0)20 7031 3799

Copyright © 2015 Moye White LLP. All rights reserved.30

AIMLegal Brief

John W. KelloggMoye White

303 292 7935

Presented by

Copyright © 2015 Moye White LLP. All rights reserved.31

Summary

Unique Players

Unique Requirements

U.S. Interplay - Securities Law

U.S. Interplay – Private Placement

Continuing Obligations

Copyright © 2015 Moye White LLP. All rights reserved.32

Unique Players

NOMAD - Nominated Adviser

Approved by the Exchange

Assesses and advises the Company

Acts as the primary regulator while listed on AIM

Industry Experts

Oil and Gas

Mining

Copyright © 2015 Moye White LLP. All rights reserved.33

Unique Requirements

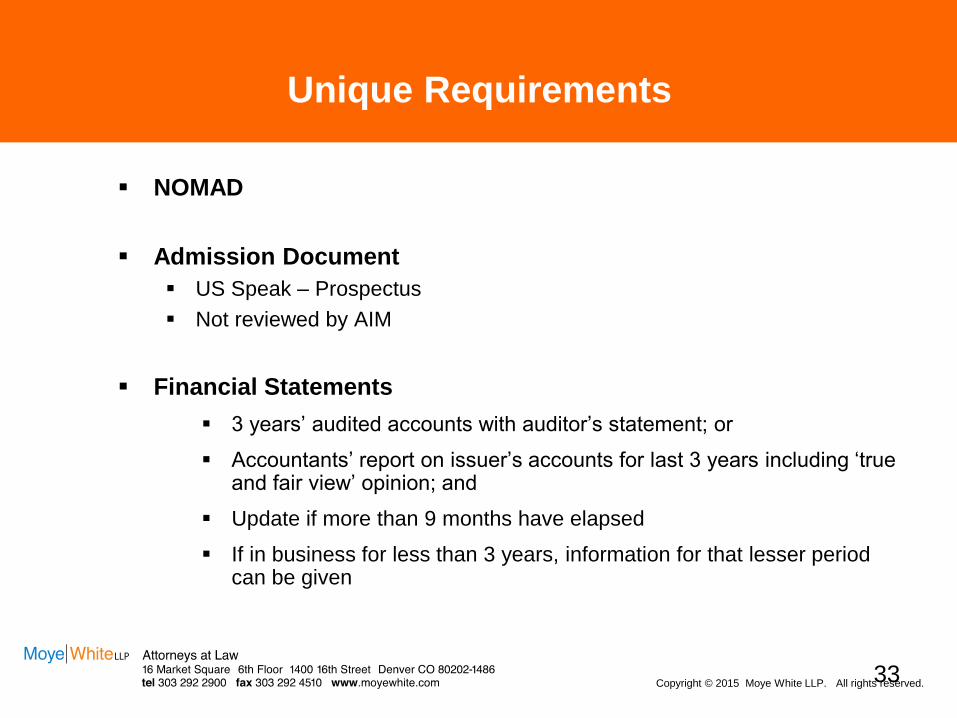

NOMAD

Admission Document

US Speak – Prospectus

Not reviewed by AIM

Financial Statements

3 years’ audited accounts with auditor’s statement; or

Accountants’ report on issuer’s accounts for last 3 years including ‘true and fair view’ opinion; and

Update if more than 9 months have elapsed

If in business for less than 3 years, information for that lesser period can be given

Copyright © 2015 Moye White LLP. All rights reserved.34

Unique Requirements

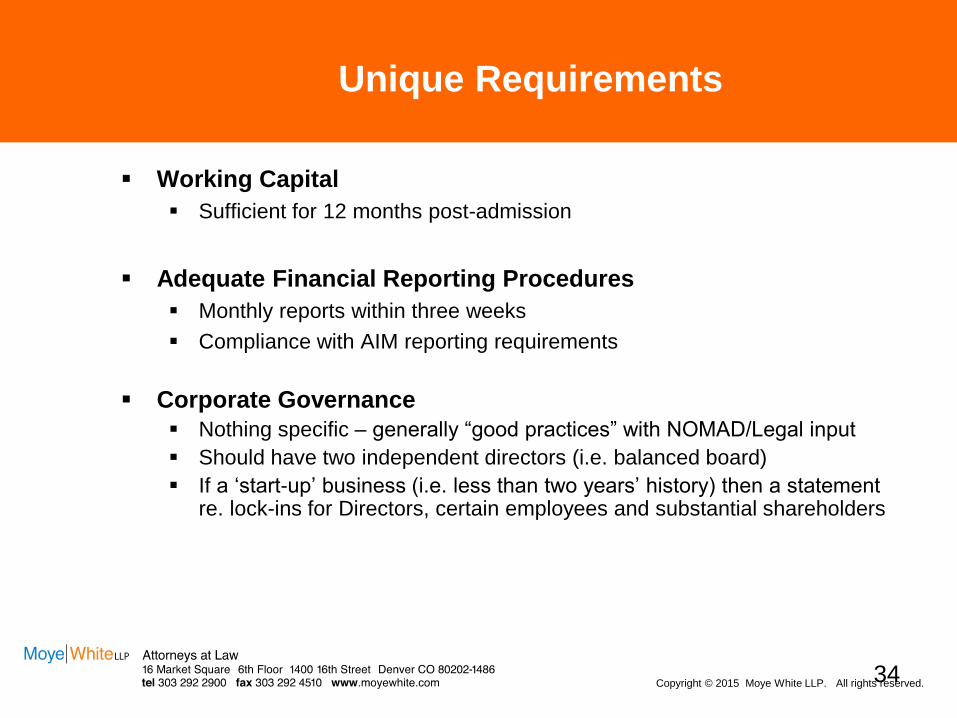

Working Capital

Sufficient for 12 months post-admission

Adequate Financial Reporting Procedures

Monthly reports within three weeks

Compliance with AIM reporting requirements

Corporate Governance

Nothing specific – generally “good practices” with NOMAD/Legal input

Should have two independent directors (i.e. balanced board)

If a ‘start-up’ business (i.e. less than two years’ history) then a statement re. lock-ins for Directors, certain employees and substantial shareholders

Copyright © 2015 Moye White LLP. All rights reserved.35

Unique Requirements

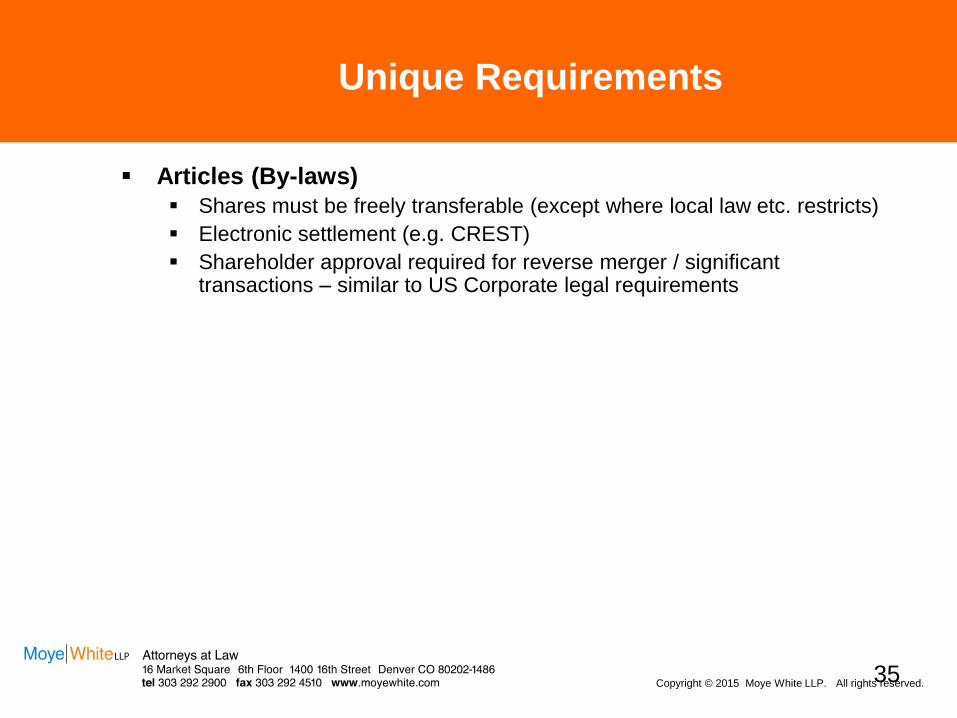

Articles (By-laws)

Shares must be freely transferable (except where local law etc. restricts)

Electronic settlement (e.g. CREST)

Shareholder approval required for reverse merger / significant transactions – similar to US Corporate legal requirements

Copyright © 2015 Moye White LLP. All rights reserved.36

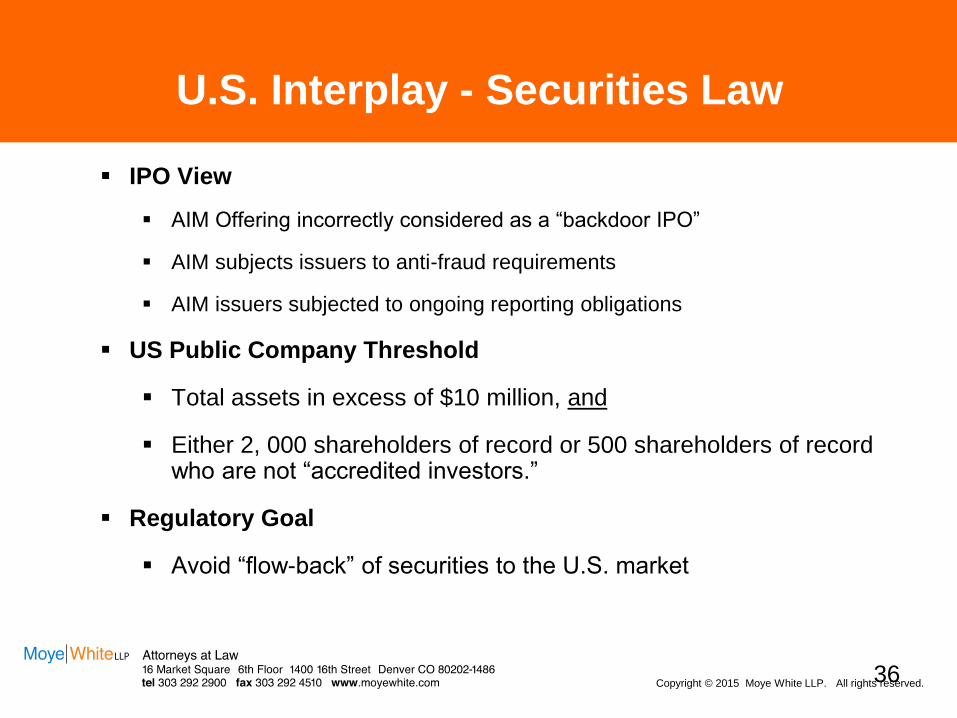

U.S. Interplay - Securities Law

IPO View

AIM Offering incorrectly considered as a “backdoor IPO”

AIM subjects issuers to anti-fraud requirements

AIM issuers subjected to ongoing reporting obligations

US Public Company Threshold

Total assets in excess of $10 million, and

Either 2, 000 shareholders of record or 500 shareholders of record who are not “accredited investors.”

Regulatory Goal

Avoid “flow-back” of securities to the U.S. market

Copyright © 2015 Moye White LLP. All rights reserved.37

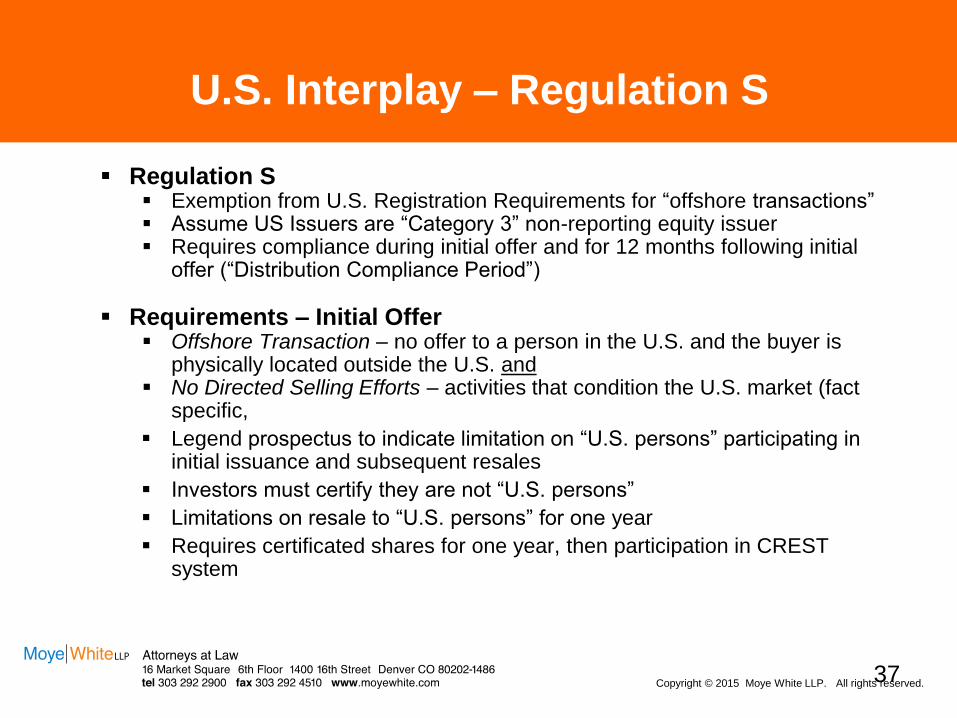

U.S. Interplay – Regulation S

Regulation S Exemption from U.S. Registration Requirements for “offshore transactions” Assume US Issuers are “Category 3” non-reporting equity issuer Requires compliance during initial offer and for 12 months following initial

offer (“Distribution Compliance Period”)

Requirements – Initial Offer Offshore Transaction – no offer to a person in the U.S. and the buyer is

physically located outside the U.S. and No Directed Selling Efforts – activities that condition the U.S. market (fact

specific,

Legend prospectus to indicate limitation on “U.S. persons” participating in initial issuance and subsequent resales

Investors must certify they are not “U.S. persons”

Limitations on resale to “U.S. persons” for one year

Requires certificated shares for one year, then participation in CREST system

Copyright © 2015 Moye White LLP. All rights reserved.38

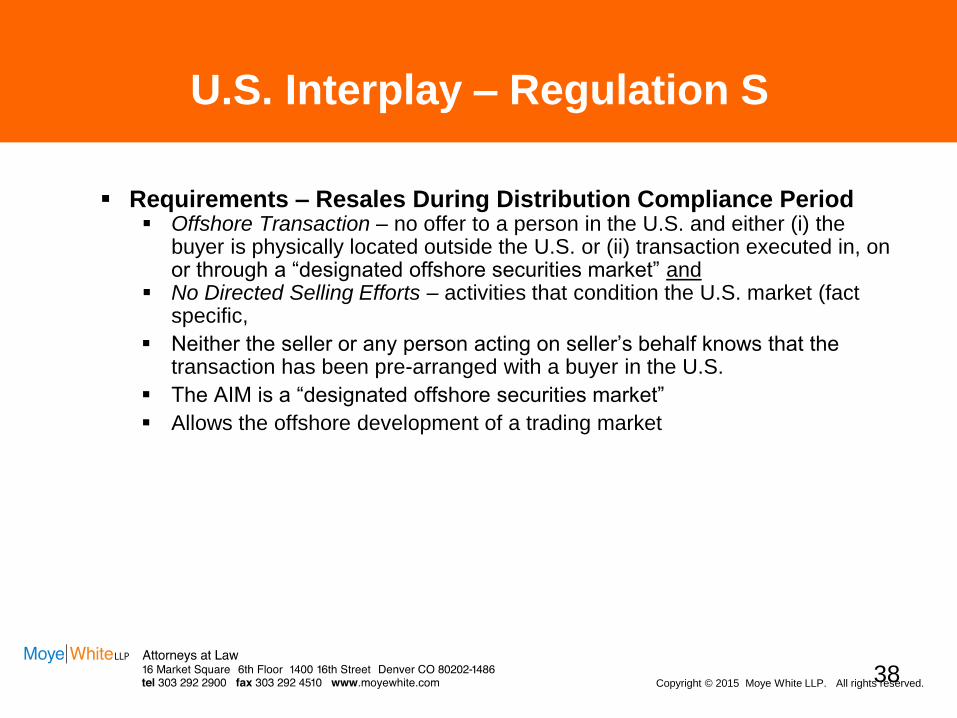

U.S. Interplay – Regulation S

Requirements – Resales During Distribution Compliance Period Offshore Transaction – no offer to a person in the U.S. and either (i) the

buyer is physically located outside the U.S. or (ii) transaction executed in, on or through a “designated offshore securities market” and

No Directed Selling Efforts – activities that condition the U.S. market (fact specific,

Neither the seller or any person acting on seller’s behalf knows that the transaction has been pre-arranged with a buyer in the U.S.

The AIM is a “designated offshore securities market”

Allows the offshore development of a trading market

Copyright © 2015 Moye White LLP. All rights reserved.39

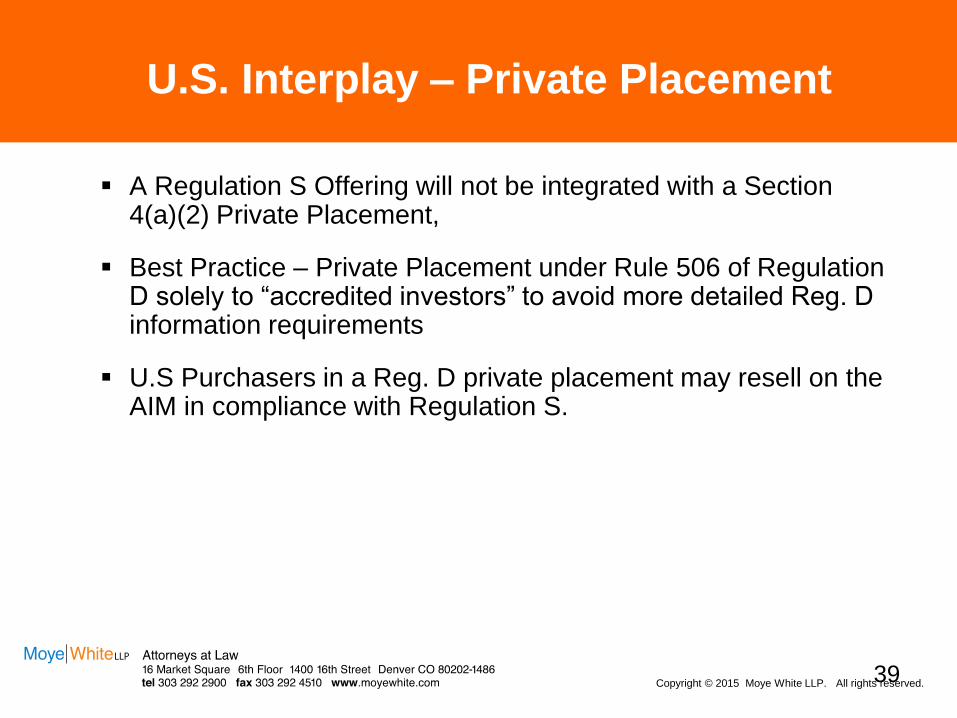

U.S. Interplay – Private Placement

A Regulation S Offering will not be integrated with a Section 4(a)(2) Private Placement,

Best Practice – Private Placement under Rule 506 of Regulation D solely to “accredited investors” to avoid more detailed Reg. D information requirements

U.S Purchasers in a Reg. D private placement may resell on the AIM in compliance with Regulation S.

Copyright © 2015 Moye White LLP. All rights reserved.40

Questions

www.croweclarkwhitehill.co.uk

The Role of the Reporting AccountantCrowe Clarke Whitehill LLPPaul Blythe, London

42Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

Contents

Introduction

Our role within the AIM adviser team

Financial information required for admission

Public information

Private information

Post admission filing requirements

Annual filings

Interims

Tax structuring

43Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

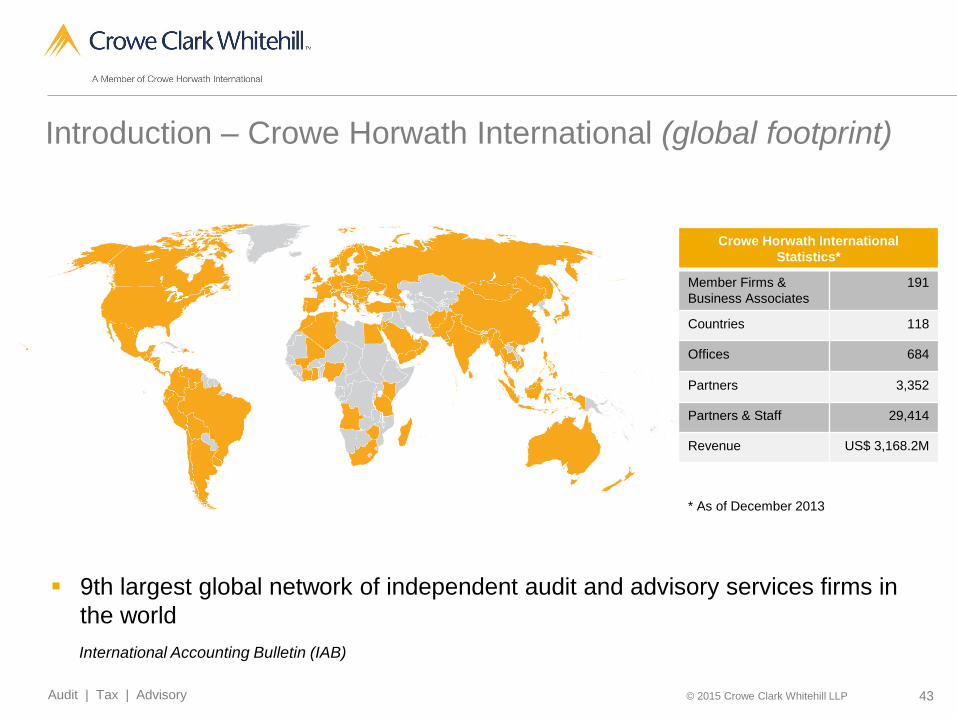

Introduction – Crowe Horwath International (global footprint)

Crowe Horwath International

Statistics*

Member Firms &

Business Associates

191

Countries 118

Offices 684

Partners 3,352

Partners & Staff 29,414

Revenue US$ 3,168.2M

* As of December 2013

9th largest global network of independent audit and advisory services firms in

the world

International Accounting Bulletin (IAB)

44Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

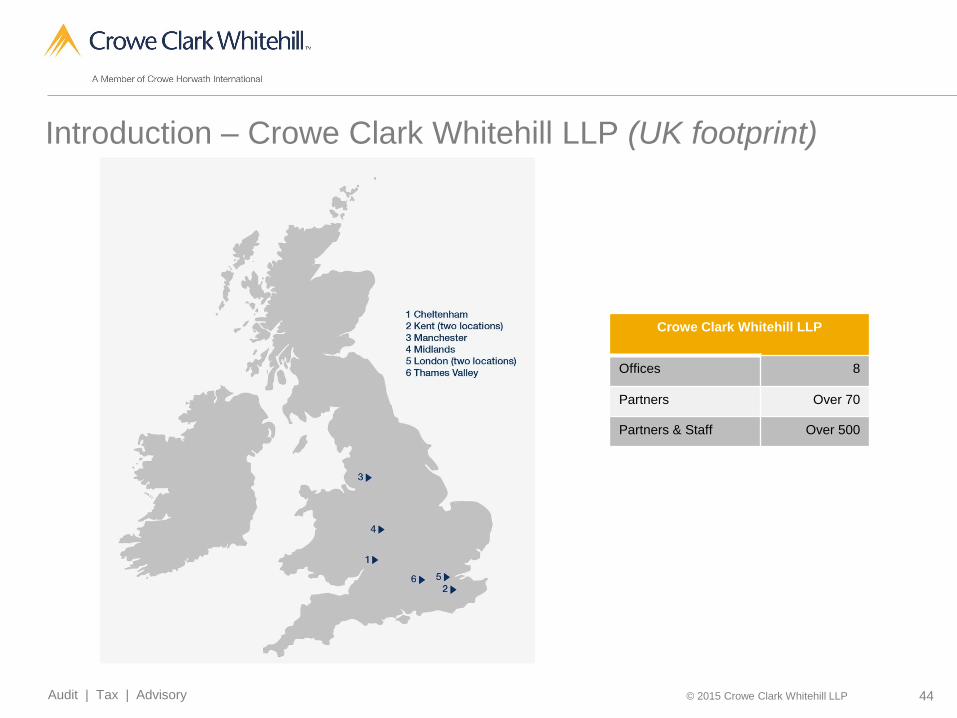

Introduction – Crowe Clark Whitehill LLP (UK footprint)

Crowe Clark Whitehill LLP

Offices 8

Partners Over 70

Partners & Staff Over 500

45Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

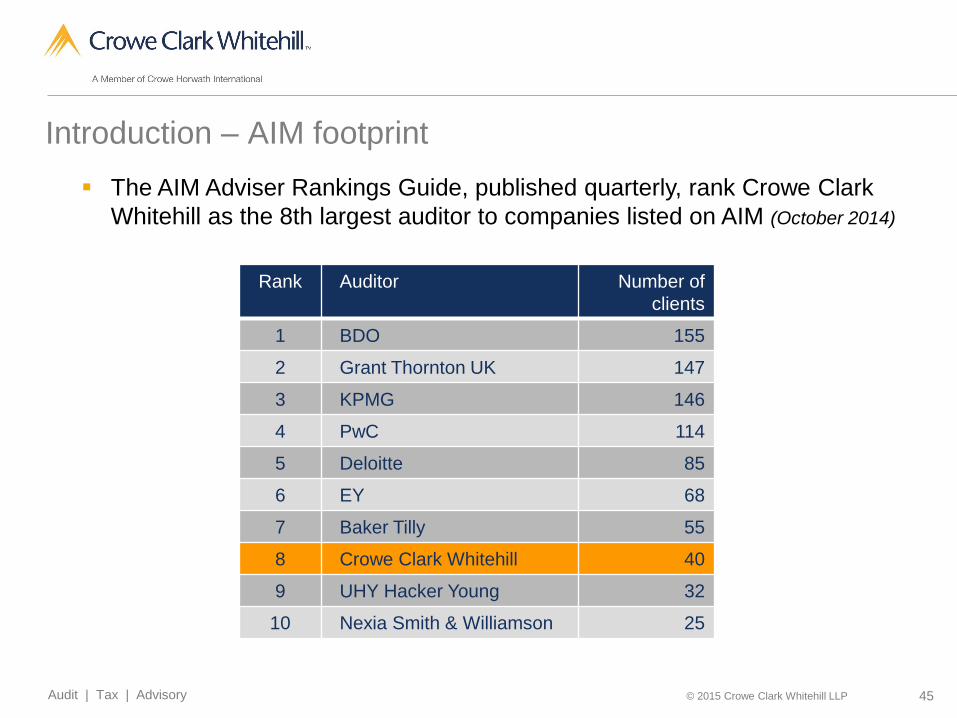

Introduction – AIM footprint

The AIM Adviser Rankings Guide, published quarterly, rank Crowe Clark

Whitehill as the 8th largest auditor to companies listed on AIM (October 2014)

Rank Auditor Number of

clients

1 BDO 155

2 Grant Thornton UK 147

3 KPMG 146

4 PwC 114

5 Deloitte 85

6 EY 68

7 Baker Tilly 55

8 Crowe Clark Whitehill 40

9 UHY Hacker Young 32

10 Nexia Smith & Williamson 25

46Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

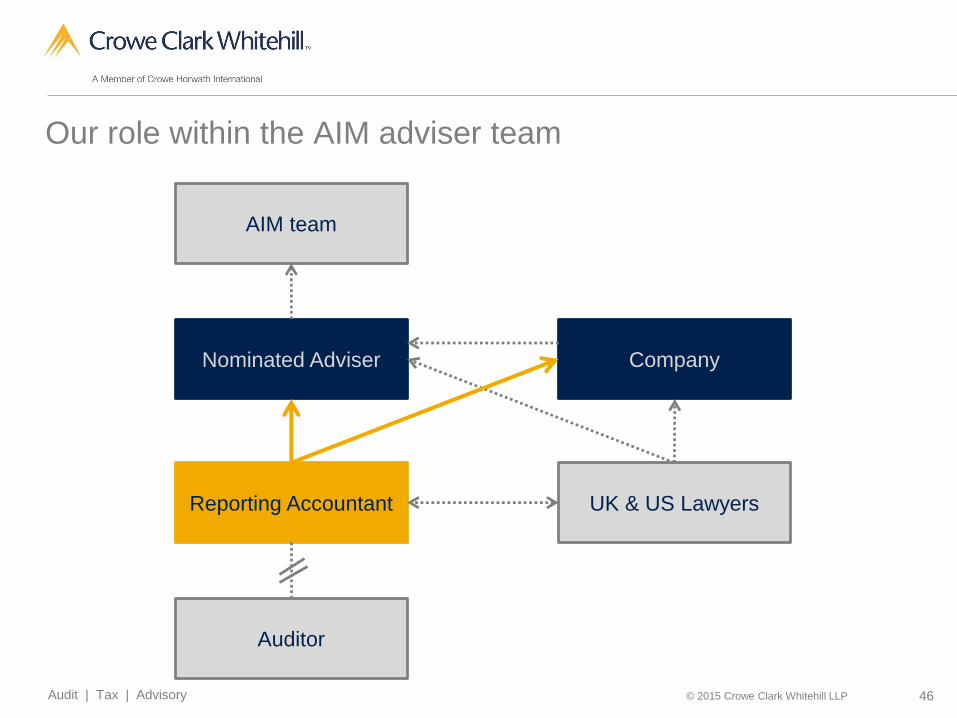

Our role within the AIM adviser team

Nominated Adviser

Reporting Accountant UK & US Lawyers

Company

Auditor

AIM team

47Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

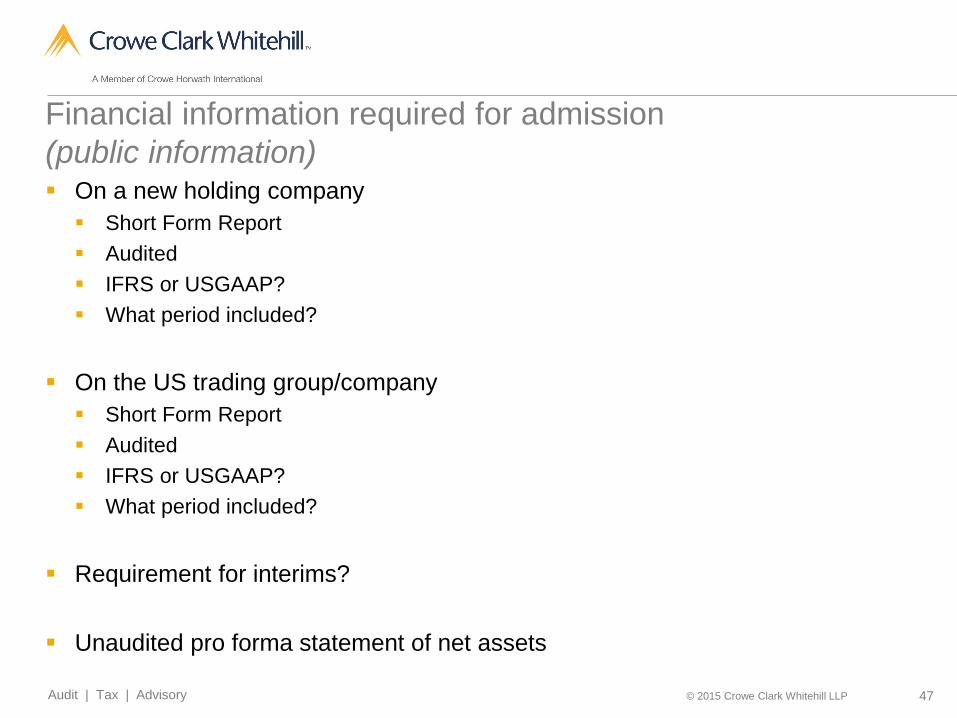

Financial information required for admission

(public information) On a new holding company

Short Form Report

Audited

IFRS or USGAAP?

What period included?

On the US trading group/company

Short Form Report

Audited

IFRS or USGAAP?

What period included?

Requirement for interims?

Unaudited pro forma statement of net assets

48Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

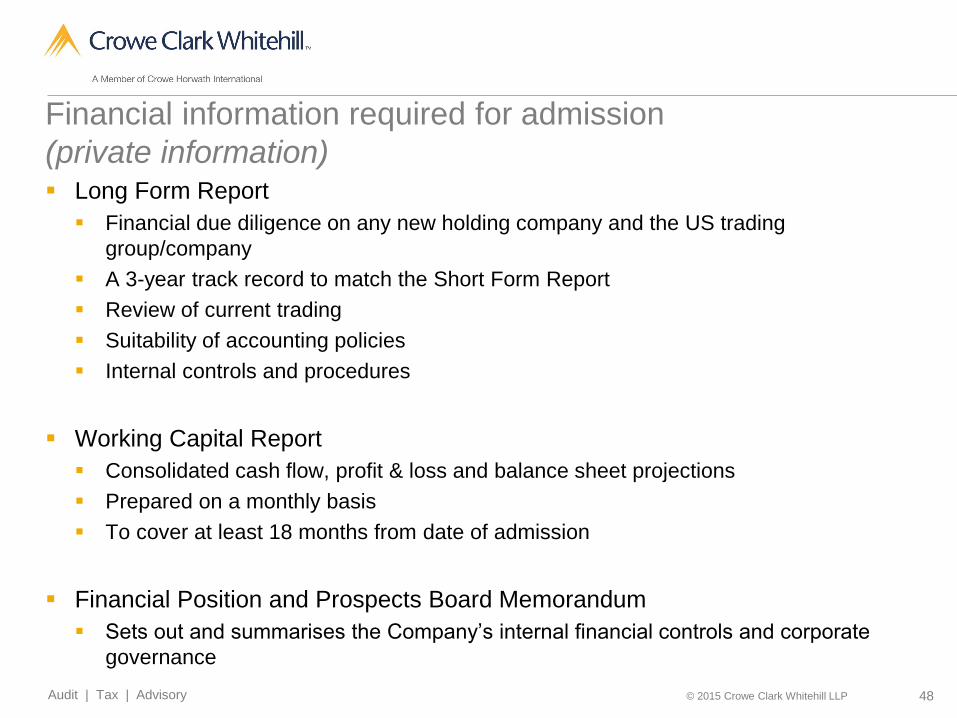

Financial information required for admission

(private information) Long Form Report

Financial due diligence on any new holding company and the US trading

group/company

A 3-year track record to match the Short Form Report

Review of current trading

Suitability of accounting policies

Internal controls and procedures

Working Capital Report

Consolidated cash flow, profit & loss and balance sheet projections

Prepared on a monthly basis

To cover at least 18 months from date of admission

Financial Position and Prospects Board Memorandum

Sets out and summarises the Company’s internal financial controls and corporate

governance

49Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

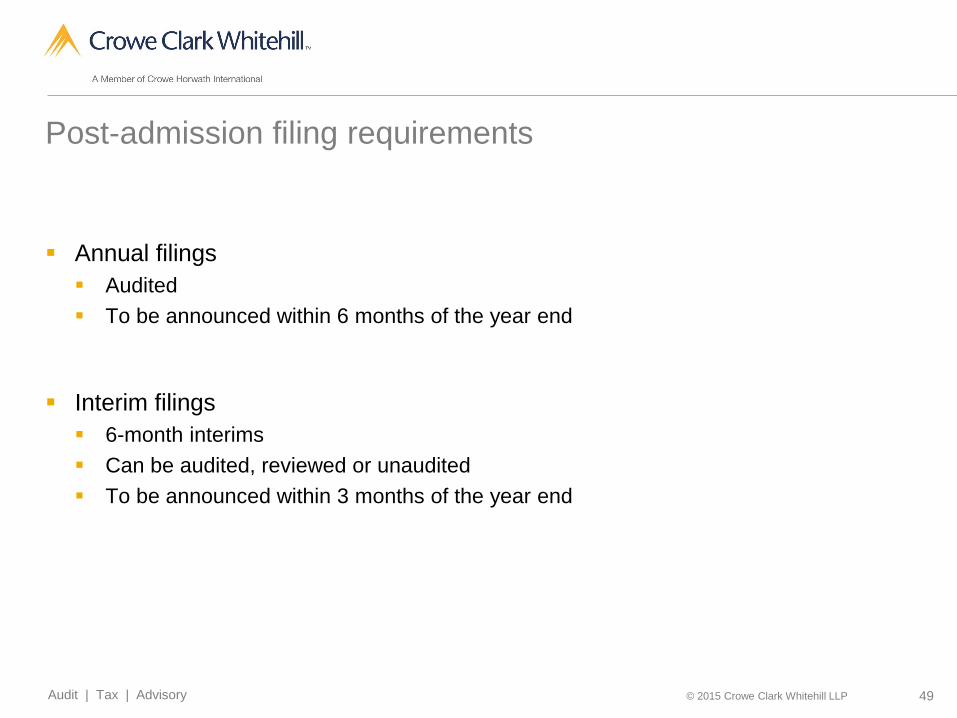

Post-admission filing requirements

Annual filings

Audited

To be announced within 6 months of the year end

Interim filings

6-month interims

Can be audited, reviewed or unaudited

To be announced within 3 months of the year end

50Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

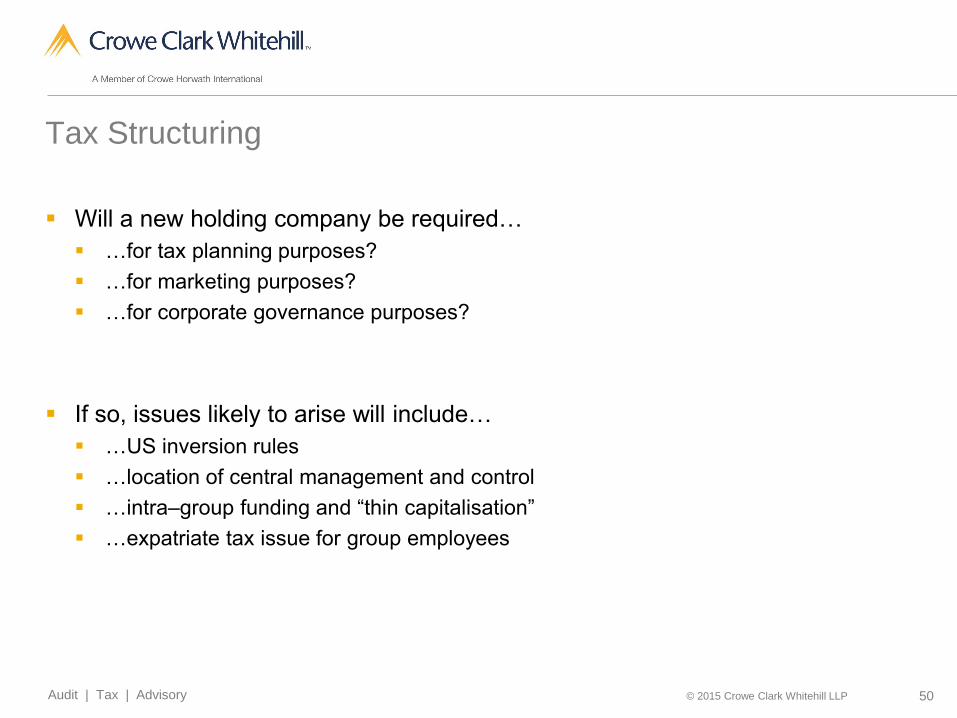

Tax Structuring

Will a new holding company be required…

…for tax planning purposes?

…for marketing purposes?

…for corporate governance purposes?

If so, issues likely to arise will include…

…US inversion rules

…location of central management and control

…intra–group funding and “thin capitalisation”

…expatriate tax issue for group employees

51Audit | Tax | Advisory © 2015 Crowe Clark Whitehill LLP

For more information, contact:

Paul Blythe, Partner, Corporate Finance

Direct +44 20 7842 7231

Mobile +44 7876 282 728

Visit www.crowehorwath.net/uk

Visit www.crowehorwath.net

Crowe Clark Whitehill LLP is a member of Crowe Horwath International, a Swiss verein (Crowe Horwath). Each member firm of Crowe Horwath is a separate and independent legal entity. Crowe Clark Whitehill LLP and its affiliates are not

responsible or liable for any acts or omissions of Crowe Horwath or any other member of Crowe Horwath and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath or any other Crowe Horwath member.

© 2015 Crowe Clark Whitehill LLP

Crowe Clark Whitehill LLP is registered to carry on audit work in the UK by the Institute of Chartered Accountants in England and Wales and is authorised and regulated by the Financial Conduct Authority.

www.croweclarkwhitehill.co.uk

Thank you!

Raising Capital on the London Stock Exchange:The AIM Exchange From an Energy PerspectiveJON HUGHES

PETRIE PARTNERS

JANUARY 20, 2015

DENVER, CO

Introduction

Commodity Price Environment Overview

Comparative Equity Market Performance

Energy Equity Activity on AIM vs. U.S. Exchanges

Pros and Cons of AIM Listing for Energy Companies

Conclusions

54

Discussion MaterialsTOPICS FOR DISCUSSION

Recent downturn in the energy markets is prompting energy companies of all sizes to explore creative solutions to continue to grow

Increased market volatility has made the successful execution of energy equity offerings more challenging and, in some cases, stalled them completely

Capital intensive nature of the industry likely to present significant challenges to smaller companies whose access to capital has tightened

Capital structure management will become a focal point for energy companies as margins decrease and fundraising flexibility is diminished across the industry

55

Discussion MaterialsINTRODUCTION

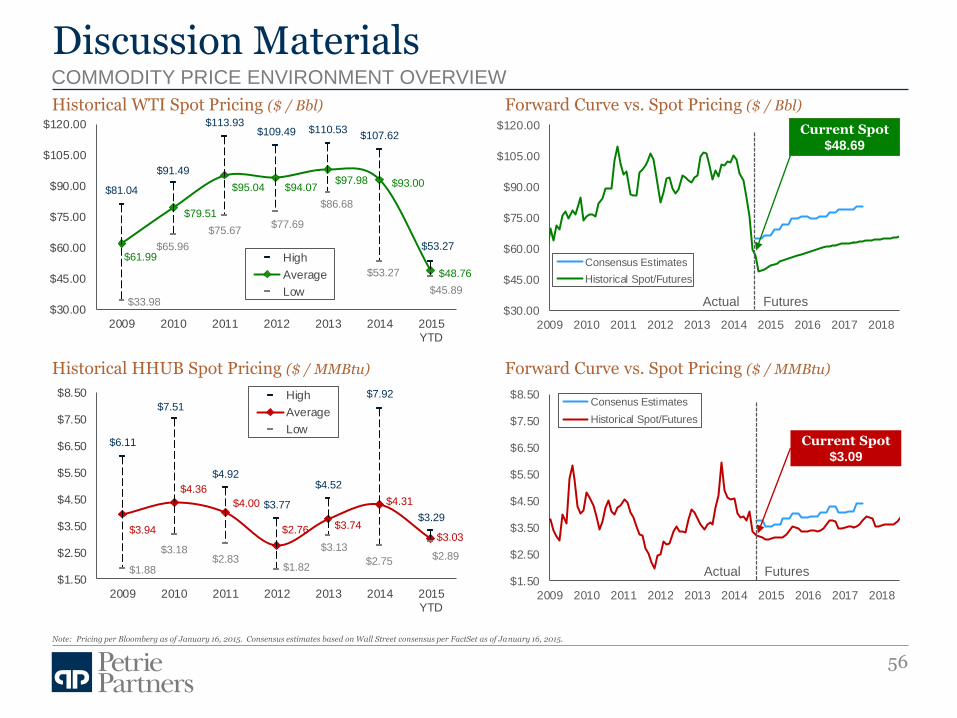

$30.00

$45.00

$60.00

$75.00

$90.00

$105.00

$120.00

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Consensus Estimates

Historical Spot/Futures

$1.50

$2.50

$3.50

$4.50

$5.50

$6.50

$7.50

$8.50

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Consenus Estimates

Historical Spot/Futures

Current Spot $3.09

Historical WTI Spot Pricing ($ / Bbl) Forward Curve vs. Spot Pricing ($ / Bbl)

Forward Curve vs. Spot Pricing ($ / MMBtu)

56

Discussion Materials

Historical HHUB Spot Pricing ($ / MMBtu)

COMMODITY PRICE ENVIRONMENT OVERVIEW

Note: Pricing per Bloomberg as of January 16, 2015. Consensus estimates based on Wall Street consensus per FactSet as of January 16, 2015.

Actual Futures

Actual Futures

$6.11

$7.51

$4.92

$3.77

$4.52

$7.92

$3.29$3.94

$4.36

$4.00

$2.76 $3.74

$4.31

$3.03

$1.88

$3.18$2.83

$1.82

$3.13

$2.75$2.89

$1.50

$2.50

$3.50

$4.50

$5.50

$6.50

$7.50

$8.50

2009 2010 2011 2012 2013 2014 2015YTD

High

Average

Low

$81.04

$91.49

$113.93$109.49 $110.53

$107.62

$53.27$61.99

$79.51

$95.04 $94.07 $97.98 $93.00

$48.76

$33.98

$65.96

$75.67$77.69

$86.68

$53.27

$45.89

$30.00

$45.00

$60.00

$75.00

$90.00

$105.00

$120.00

2009 2010 2011 2012 2013 2014 2015YTD

High

Average

Low

Current Spot $48.69

57

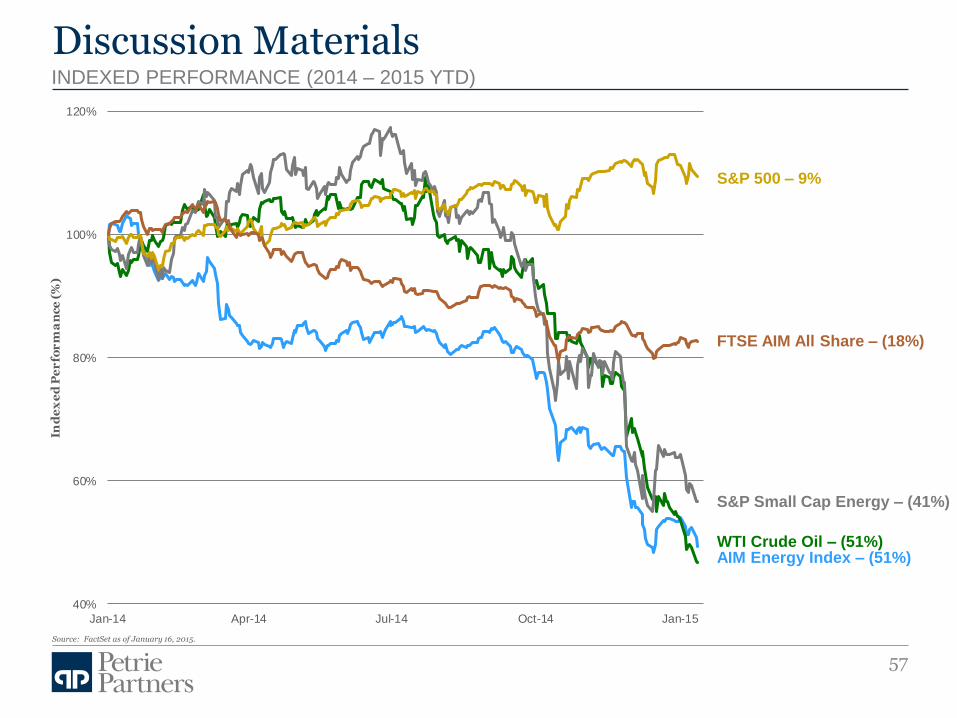

Discussion MaterialsINDEXED PERFORMANCE (2014 – 2015 YTD)

Source: FactSet as of January 16, 2015.

40%

60%

80%

100%

120%

Jan-14 Apr-14 Jul-14 Oct-14 Jan-15

Ind

ex

ed

Pe

rfo

rm

an

ce

(%

)

S&P 500 – 9%

FTSE AIM All Share – (18%)

S&P Small Cap Energy – (41%)

WTI Crude Oil – (51%)AIM Energy Index – (51%)

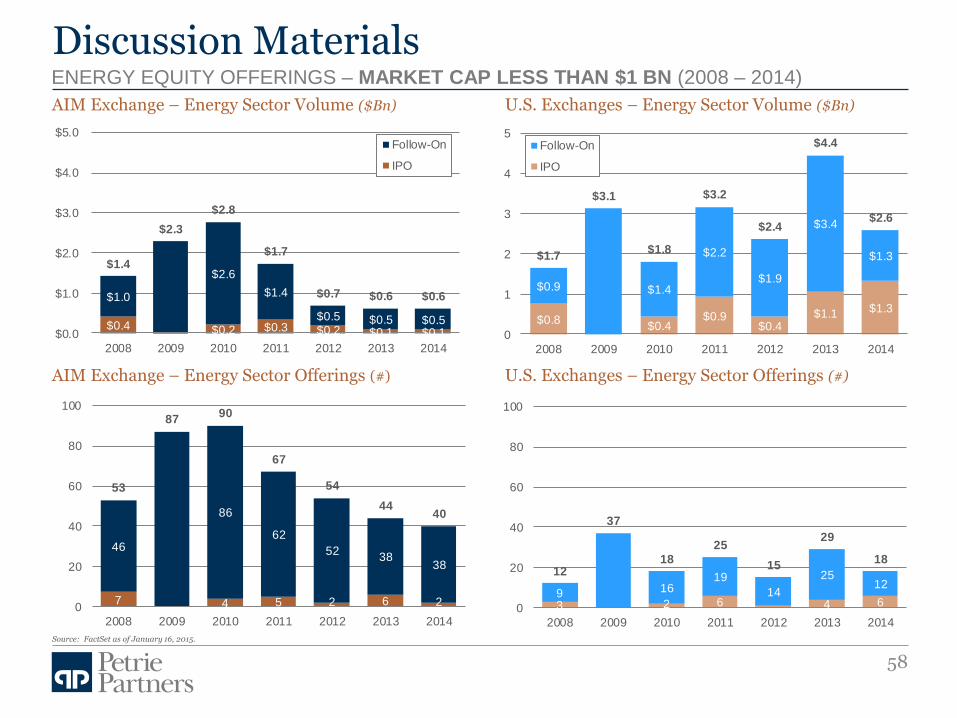

AIM Exchange – Energy Sector Volume ($Bn) U.S. Exchanges – Energy Sector Volume ($Bn)

U.S. Exchanges – Energy Sector Offerings (#)

58

Discussion Materials

AIM Exchange – Energy Sector Offerings (#)

ENERGY EQUITY OFFERINGS – MARKET CAP LESS THAN $1 BN (2008 – 2014)

$0.4 $0.2 $0.3 $0.2 $0.1 $0.1

$1.0

$2.6

$1.4

$0.5 $0.5 $0.5

$1.4

$2.3

$2.8

$1.7

$0.7 $0.6 $0.6

$0.0

$1.0

$2.0

$3.0

$4.0

$5.0

2008 2009 2010 2011 2012 2013 2014

Follow-On

IPO

53

8790

67

54

4440

46

86

62

5238

38

7 4 5 2 6 20

20

40

60

80

100

2008 2009 2010 2011 2012 2013 2014

$0.8$0.4

$0.9$0.4

$1.1 $1.3

$0.9 $1.4

$2.2

$1.9

$3.4

$1.3$1.7

$3.1

$1.8

$3.2

$2.4

$4.4

$2.6

0

1

2

3

4

5

2008 2009 2010 2011 2012 2013 2014

Follow-On

IPO

12

37

18

25

15

29

18

9 1619

14

2512

3 2 6 4 60

20

40

60

80

100

2008 2009 2010 2011 2012 2013 2014

Source: FactSet as of January 16, 2015.

59

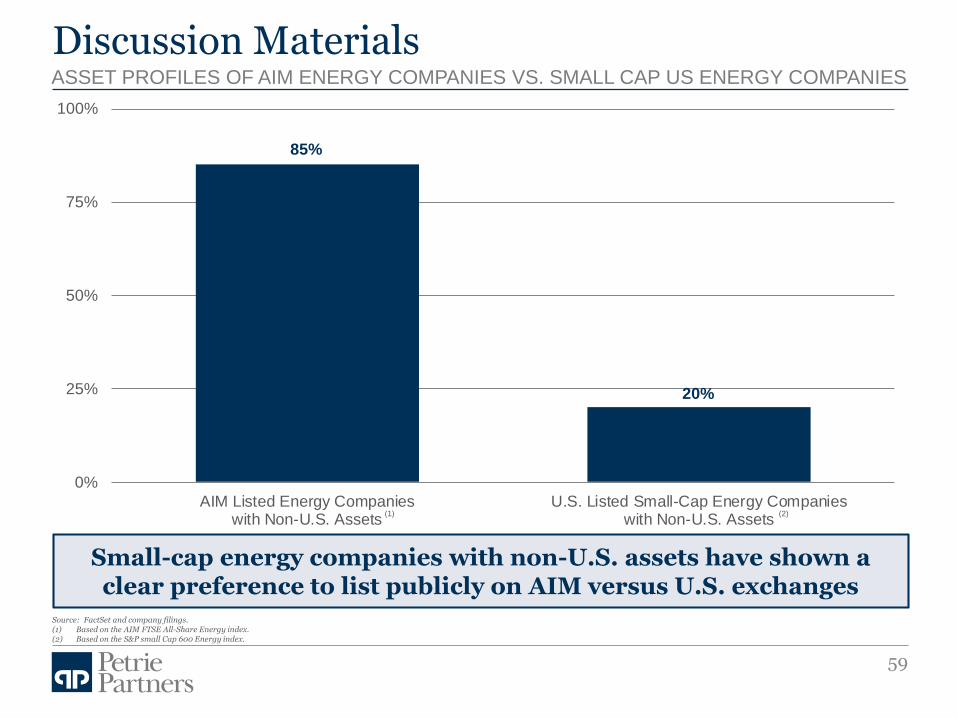

Discussion MaterialsASSET PROFILES OF AIM ENERGY COMPANIES VS. SMALL CAP US ENERGY COMPANIES

Source: FactSet and company filings.(1) Based on the AIM FTSE All-Share Energy index.(2) Based on the S&P small Cap 600 Energy index.

85%

20%

0%

25%

50%

75%

100%

AIM Listed Energy Companieswith Non-U.S. Assets

U.S. Listed Small-Cap Energy Companieswith Non-U.S. Assets

(1) (2)

Small-cap energy companies with non-U.S. assets have shown a clear preference to list publicly on AIM versus U.S. exchanges

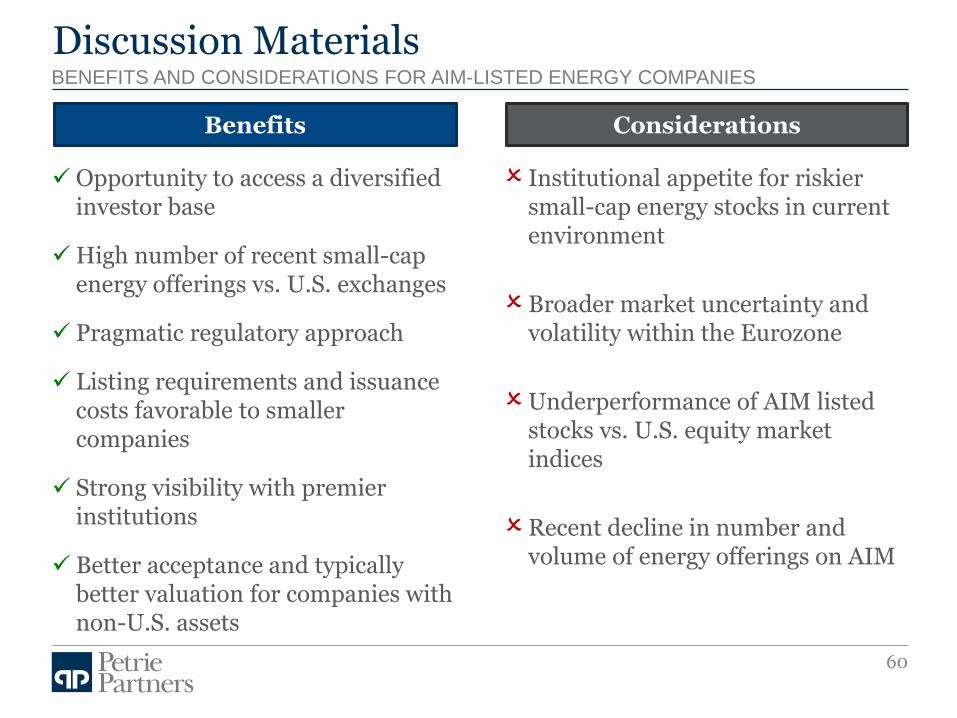

BENEFITS AND CONSIDERATIONS FOR AIM-LISTED ENERGY COMPANIES

60

Discussion Materials

Opportunity to access a diversified investor base

High number of recent small-cap energy offerings vs. U.S. exchanges

Pragmatic regulatory approach

Listing requirements and issuance costs favorable to smaller companies

Strong visibility with premier institutions

Better acceptance and typically better valuation for companies with non-U.S. assets

Institutional appetite for riskier small-cap energy stocks in current environment

Broader market uncertainty and volatility within the Eurozone

Underperformance of AIM listed stocks vs. U.S. equity market indices

Recent decline in number and volume of energy offerings on AIM

Benefits Considerations

Despite uncertainty and volatility in the broader market, energy companies will still seek to secure financing to prosecute their (reduced) capital programs – creative alternatives may drive successful execution

Continued commodity market headwinds may dampen investor appetite for high-risk equity within a volatile sector of the market

AIM offers favorable listing requirements and issuance fees among the lowest of all exchanges, potentially attracting a broader pool of small-cap issuers

AIM has been a preferred market for listing small capitalization energy companies with non-U.S. assets

61

Discussion MaterialsCONCLUSIONS