airline deregulation in the united states deregulation in the united states russell w. damtoft u.s....

TRANSCRIPT

AIRLINE DEREGULATION IN THE UNITED STATES

Russell W. DamtoftU.S. Federal Trade Commission

Bogota, Colombia

September 14, 2011

The views expressed herein are those of the speaker and do not necessarily represent the views of

the Federal Trade Commission or any individual Commissioner

Overview

• The Origins of Regulation

• The Experience under Regulation

• The Move to Deregulate

• Effects of Deregulation

The origins of regulation

• In the 1920s, passenger air transport

was inherently unprofitable

– Low aircraft capacity

– High operating costs

– Unreliable operations

• Initial routes were subsidized to carry

airmail

– Passengers were incidental

– Non-mail services allowed, but most failed

• Subsidies developed a needed service

that the market could not yet provide

– Contrast: state ownership or operating

subsidies in other countries3

Consolidation and a whiff of scandal

• 1930: to reduce airmail subsidies, postal

authorities pressured airmail operators

to:

– Increase reliance on passenger revenue

– Consolidation leads to domination by four

domestic and one international airline

• 1934: Favoritism, pressure, and

collusion alleged in award of airmail

routes

• “Scandal” leads to brief window for

new entry4

Advances in Technology

• Meanwhile, technological

improvements made it possible

to operate airline service

profitably

• New and innovative market

participants emerged

• Was there still a rationale for

government intervention?

5

“Perfect Storm” leads to Regulation

• Mid-1930’s: Pressures for Congress to regulate

airline industry:

– Incumbent airlines seek relief from competition

– Political reaction to perceived collusion and

favoritism

– Change of political control

– High profile crashes fuel public interest

• 1938: Pervasive regulation adopted along model

for railroad regulation.

• Civil Aeronautics Board regulates:

– Entry (new airlines and new routes)

– Exit (abandonment of routes)

– Mergers

– Fares

– Safety6

Competition in the Regulated Era

• 1940s-50s: technology advances reliability, capacity,

range, and speed – and profitability, further

diminishing basis for regulation

• Demand for air travel grows and replaces rail

• CAB still allows only one carrier per route except on

select routes where believes market will support

limited competition

• Profitable routes cross-subsidize less traveled routes

• Competition limited to scheduling, equipment, and

amenities

• Fares remain regulated to guarantee a rate of return

– Little incentive to cut costs

– Airlines agree to generous labor and pension costs 7

Near-Absolute Barriers to Entry

• CAB rebuffs all requests for trunk level entry

– Demand and potential supply skyrocket after World War II

– 79 applications for new service; all are denied

– Attempted entry by non-scheduled carriers ruthlessly

suppressed

– New entry allowed for local service carriers to serve small

communities under restrictions that protect incumbents

• Natural experiment with intrastate services

– Intrastate service beyond federal jurisdiction

– States allow entry in California and Texas, which have

substantial intrastate markets

– Intrastate carriers successfully challenge incumbents with

low fare, innovative service

8

International Services

• After World War II, most international services operated

by state-owned carriers

– Prominent exception: United States

• “Flag” carriers governed by foreign policy purposes rather

than market demands

• Chicago Convention of 1944 sets stage for a network of

bilateral aviation treaties that:

– Define airline “citizenship” by ownership

– Establish routes flown

– Determine capacity

– Fix fares

– Decisions typically driven by foreign policy and domestic political

goals9

1970s: Doubts about Regulation

• Future FTC Commissioners Miller and Douglas

and others use intrastate experience to question

rationale for regulation

• Academic studies show that absence of barriers to

entry and economies of scale debunk validity of

railroad model

• Alfred Kahn and others show that theory of

contestable markets applies to airlines

• Political consensus emerges for deregulation

10

1978-1983: Dawn of Deregulation• After transitional period, restrictions to domestic entry,

exit, and fares are lifted

– Safety regulation remains

– Subsidies for service to small communities

– CAB itself is abolished

• New entry from:

– Expansion by intrastate and local service airlines

– Charter airlines enter scheduled markets

– Entirely new airlines

• International service remains regulated

– Governed by existing treaties

– Foreign governments protect national carriers

– Attempted entry by Laker fails amid epic antitrust battle11

1983-1993: Established carriers respond

• “Fortress hubs” dominate major airports

– Consolidation among incumbents unchallenged

– Rise of hub-and-spoke systems

– Fares 18-27% higher at such hubs

• Barriers to entry at major airports through:

– Landing slot allocation at key airports

– Long-term gate leases

• Incumbents carriers compete more

effectively

– Frequent flyer programs discourage switching

– Code-sharing to retain passengers at local service

and international levels

– Yield management12

1993-2001: Rise of low cost carriers

• Expansion and maturity of new entrants

and low cost carrier model

• Second wave of new entry

• Legacy carriers feel pain

– Loss of market share

– Financial stress due to higher labor and

pension costs

– Exit by some established carriers

– Strong economy helps others survive

13

2001-2011: Tectonic plates shift

• Current phase began ten years ago this week

• Industry stressed by

– 9/11 and aftermath

– Economic downturn

– Increased fuel costs

• Decline of legacy carriers continue

– Many seek relief in bankruptcy

• Low cost carriers continue to gain share

14

Shifts in International Policies

• Most national carriers privatized

• Declining relevance of “flag carrier” model

• Applicability of domestic deregulation to

international markets

• Regional experiments lead to results similar to

U.S. experience

– U.S./Canada

– Trans-Tasman deregulation

– Open skies in United Arab Emirates

– Transatlantic open skies (Netherlands, U.K.)

– EU phased deregulation 15

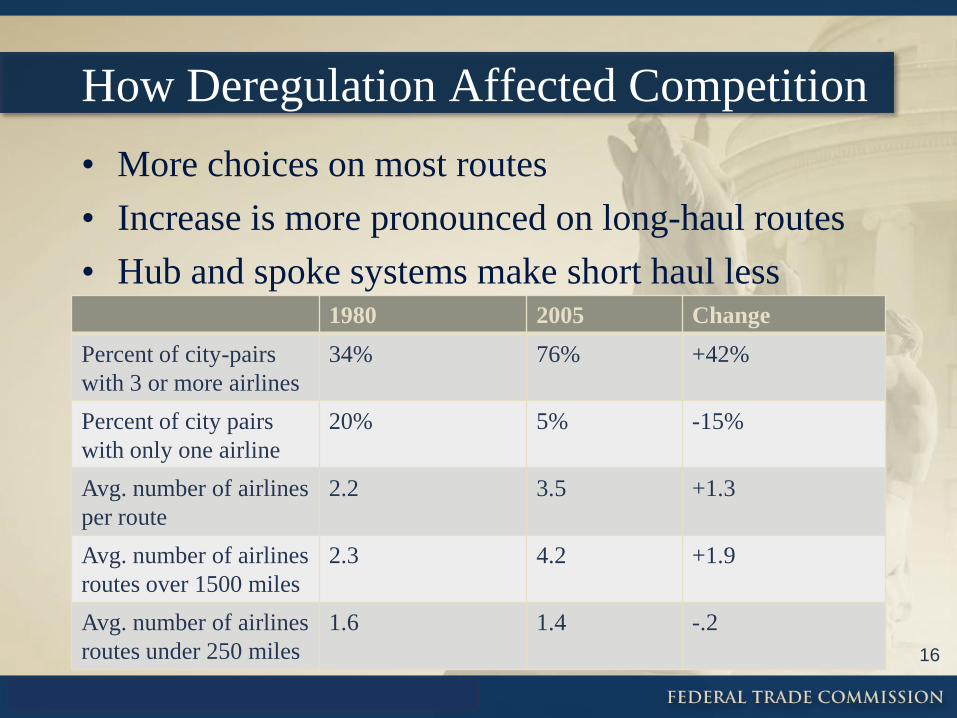

How Deregulation Affected Competition

• More choices on most routes

• Increase is more pronounced on long-haul routes

• Hub and spoke systems make short haul less

competitive

16

1980 2005 Change

Percent of city-pairs

with 3 or more airlines

34% 76% +42%

Percent of city pairs

with only one airline

20% 5% -15%

Avg. number of airlines

per route

2.2 3.5 +1.3

Avg. number of airlines

routes over 1500 miles

2.3 4.2 +1.9

Avg. number of airlines

routes under 250 miles

1.6 1.4 -.2

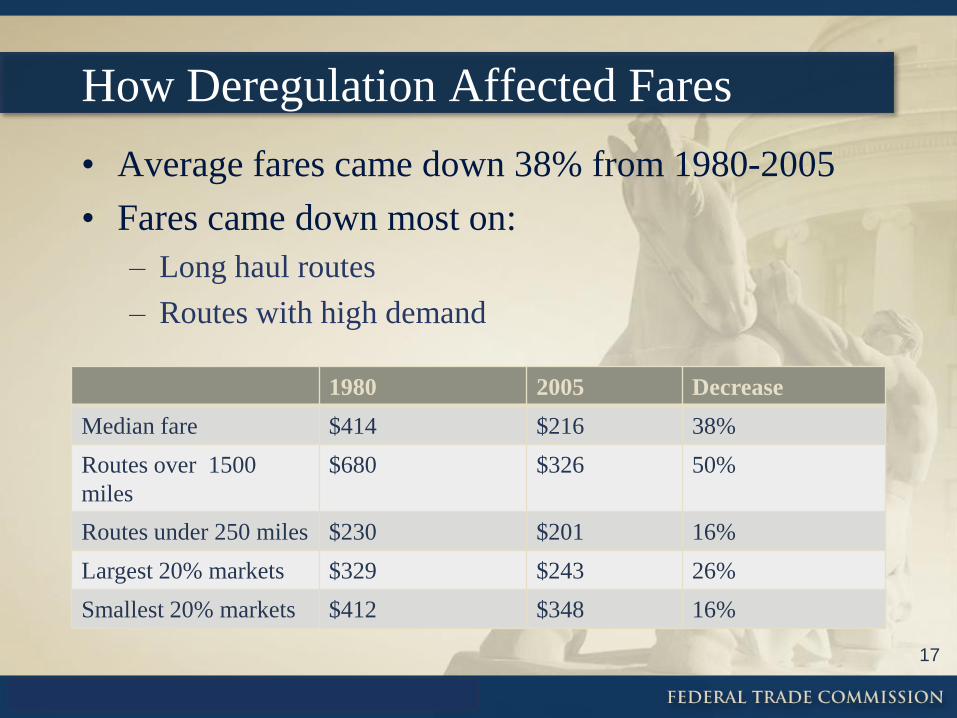

How Deregulation Affected Fares

• Average fares came down 38% from 1980-2005

• Fares came down most on:

– Long haul routes

– Routes with high demand

17

1980 2005 Decrease

Median fare $414 $216 38%

Routes over 1500

miles

$680 $326 50%

Routes under 250 miles $230 $201 16%

Largest 20% markets $329 $243 26%

Smallest 20% markets $412 $348 16%

Deregulation Effects on Consumer Behavior

• Expansion of consumption: revenue

passenger miles increase from 188 billion to

584 billion

• Low fares create incentives to travel

• Marginal shift from automobile travel

• Busses lose competitive force

18

The Effect on Small Communities

• After World War II, subsidized service added for

many communities

• Many have low traffic

– Shift of economic activity to cities reflected in rural

airport traffic

– New highways allow easy access to larger airports

with better service

– In some cases, up to 90% of local traffic uses distant

airports

– Low cost carriers cannot achieve scale needed to

profitably serve small airports

• Airlines reduce or drop service to small cities as

subsidies and incentives to cross-subsidize decline

19

The Impact on Safety

• Skeptics had predicted that competitive

pressure would cause airlines to cut costs

and compromise safety

• In fact, safety continues to improve

– Fatalities decline, in some years to zero

– Accidents per mile decrease

• Deregulation creates incentives for safety

20

The effect on employment

• Overall level of employment increases

• Overall wages remain stable

• Wages as percent of revenue decrease

• Wages at legacy carriers decrease

• Legacy carriers drop pensions, work rules,

in bankruptcy proceedings

21