akg presentation oct-2016-final_v2-compressed

TRANSCRIPT

CREATING VALUE THROUGH DISCIPLINED GROWTHInvestorPresentationOctober2016

This document has been prepared by Asanko Gold Inc. (the “Company”) solely forinformational purposes. This presentation is the sole responsibility of thecompany. Information contained herein does not purport to be complete and issubject to certain qualifications and assumptions and should not be relied uponfor the purposes of making an investment in the securities or entering into anytransaction. The information and opinions contained in the presentation areprovided as at the date of this presentation and are subject to change withoutnotice and, in furnishing the presentation, the company does not undertake oragree to any obligation to provide recipients with access to any additionalinformation or to update or correct the presentation.

No securities commission or similar regulatory authority has passed on the meritsof any securities referred to in the presentation, nor has it passed on or reviewedthe presentation. Cautionary note to United States investors - the informationcontained in the presentation uses terms that comply with reporting standards inCanada and certain estimates are made in accordance with National Instrument43-101 (“NI 43-101”) - standards for disclosure for mineral projects. Thepresentation uses the terms “other resources”, “measured”, “indicated” and“inferred” resources. United States investors are advised that, while such termsare recognized and required by Canadian securities laws, the SEC does notrecognize them. Under United States standards, mineralization may not beclassified as “ore” or a “reserve” unless the determination has been made thatthe mineralization could be economically and legally produced or extracted at thetime the reserve determination is made. United States investors are cautionednot to assume that all or any part of measured or indicated resources will ever beconverted into reserves. Further, “inferred resources” have a great amount ofuncertainty as to their existence and as to whether they can be mined legally oreconomically. It cannot be assumed that all or any part of the “inferred resources”will ever be upgraded to a higher category. Therefore, United States investors arealso cautioned not to assume that all or any part of the inferred resources exist, orthat they can be mined legally or economically.

Under Canadian rules, estimates of “inferred resources” may not form the basis offeasibility or pre-feasibility studies except in limited cases. Disclosure of “containedounces” is permitted disclosure under Canadian regulations; however, the SecuritiesExchange Commission (SEC) normally only permits issuers to report mineralizationthat does not constitute “reserves” as in place tonnage and grade without referenceto unit measures. Accordingly, information concerning descriptions ofmineralization, mineral resources and mineral reserves contained in thepresentation, may not be comparable to information made public by United Statescompanies subject to the reporting and disclosure requirements of the SEC.

The presentation may contain “forward looking statements” within the meaning ofthe United States private securities litigation reform act of 1995 and “forwardlooking information” with the meaning of applicable Canadian securities legislationconcerning, among other things, the size and the growth of the company’s mineralresources and the timing of further exploration and development of the company’sprojects. There can be no assurance that the plans, intentions or expectations uponwhich these forward looking statements and information are based will occur.“Forward looking statements” and “forward looking information” are subject to avariety of risks, uncertainties and assumptions, including those that are discussed inthe company’s annual information form. Some of the factors which could affectfuture results and could cause results to differ materially from those expressed inthe forward looking statements and information contained herein include: marketprices, exploitation and exploration successes, continued availability of capital andfinancing and general economic, market, business or governmental conditions.Forward looking statements and information are based on the beliefs, estimates andopinions of management at the date the statements are made and are subject tochange without notice. The Company does not undertake to update forward lookingstatements or information if management believes, estimates forward or opinions orother circumstances should change. The Company also cautions potential investorsthat mineral resources that are not material reserves do not have demonstratedeconomic viability.

2

FORWARD LOOKING INFORMATION

3

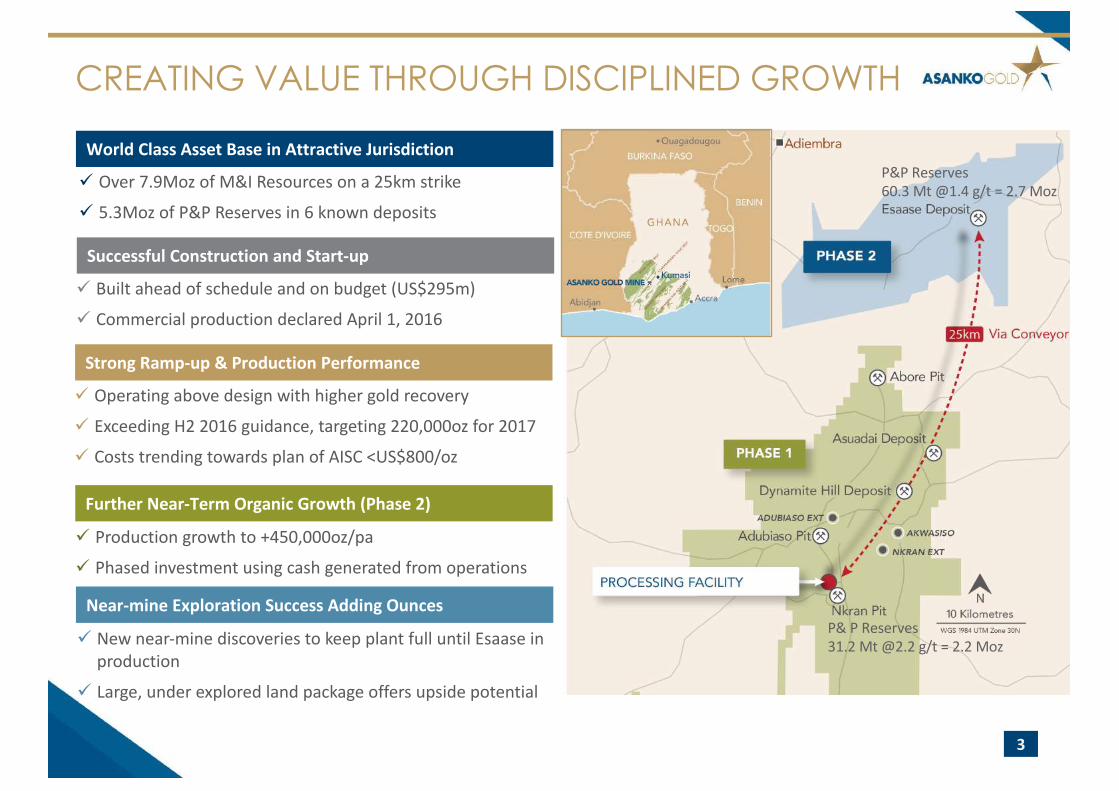

CREATING VALUE THROUGH DISCIPLINED GROWTH

ü Over7.9MozofM&IResourcesona25kmstrike

ü 5.3MozofP&PReservesin6knowndeposits

WorldClassAssetBaseinAttractiveJurisdiction

ü Operatingabovedesignwithhighergoldrecovery

ü ExceedingH22016guidance,targeting220,000ozfor2017

ü CoststrendingtowardsplanofAISC<US$800/oz

StrongRamp-up&ProductionPerformance

ü Newnear-minediscoveriestokeepplantfulluntilEsaaseinproduction

ü Large,underexploredlandpackageoffersupsidepotential

Near-mineExplorationSuccessAddingOunces

ü Productiongrowthto+450,000oz/pa

ü Phasedinvestmentusingcashgeneratedfromoperations

FurtherNear-TermOrganicGrowth(Phase2)

ü Builtaheadofscheduleandonbudget(US$295m)

ü CommercialproductiondeclaredApril1,2016

Successful ConstructionandStart-up

P&[email protected]/t=2.2Moz

P&[email protected]/t=2.7Moz

4

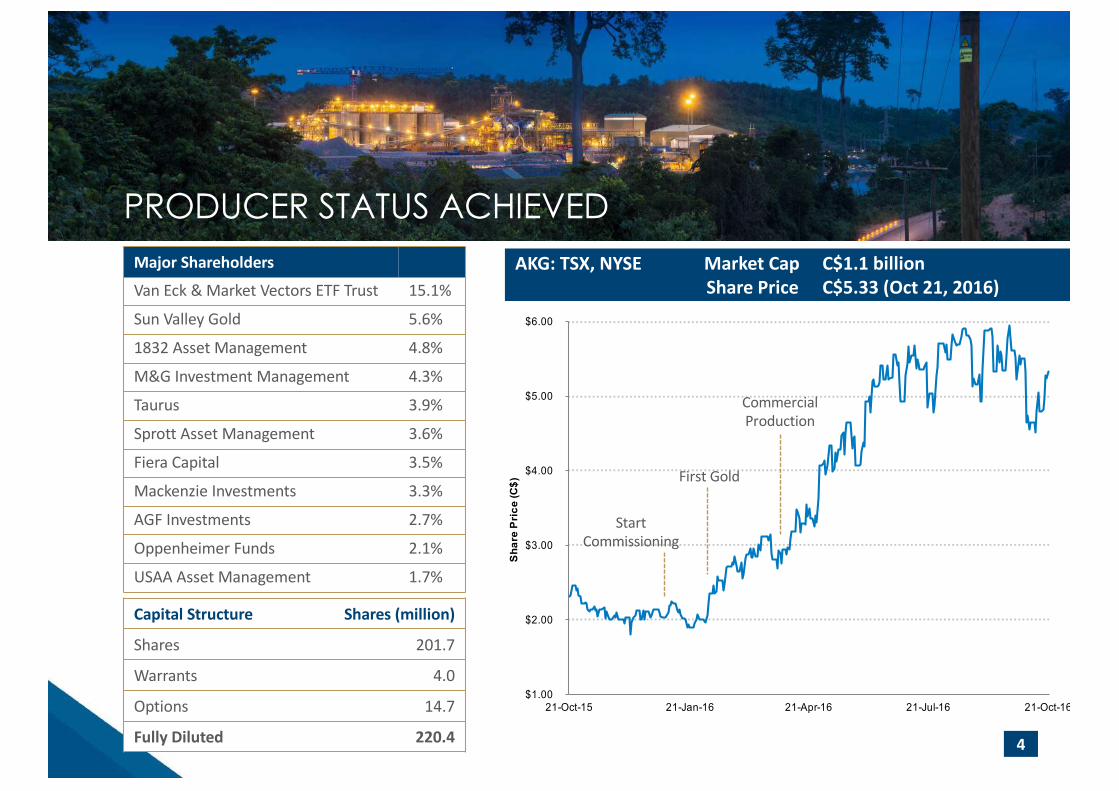

PRODUCER STATUS ACHIEVED

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

21-Oct-15 21-Jan-16 21-Apr-16 21-Jul-16 21-Oct-16

Sha

re P

rice

(C$)

AKG:TSX,NYSEMarketCap C$1.1billionSharePrice C$5.33(Oct21,2016)

StartCommissioning

FirstGold

CommercialProduction

Major Shareholders

VanEck& MarketVectorsETFTrust 15.1%

SunValleyGold 5.6%

1832AssetManagement 4.8%

M&GInvestment Management 4.3%

Taurus 3.9%

Sprott AssetManagement 3.6%

Fiera Capital 3.5%

MackenzieInvestments 3.3%

AGF Investments 2.7%

OppenheimerFunds 2.1%

USAA AssetManagement 1.7%

Capital Structure Shares(million)

Shares 201.7

Warrants 4.0

Options 14.7

FullyDiluted 220.4

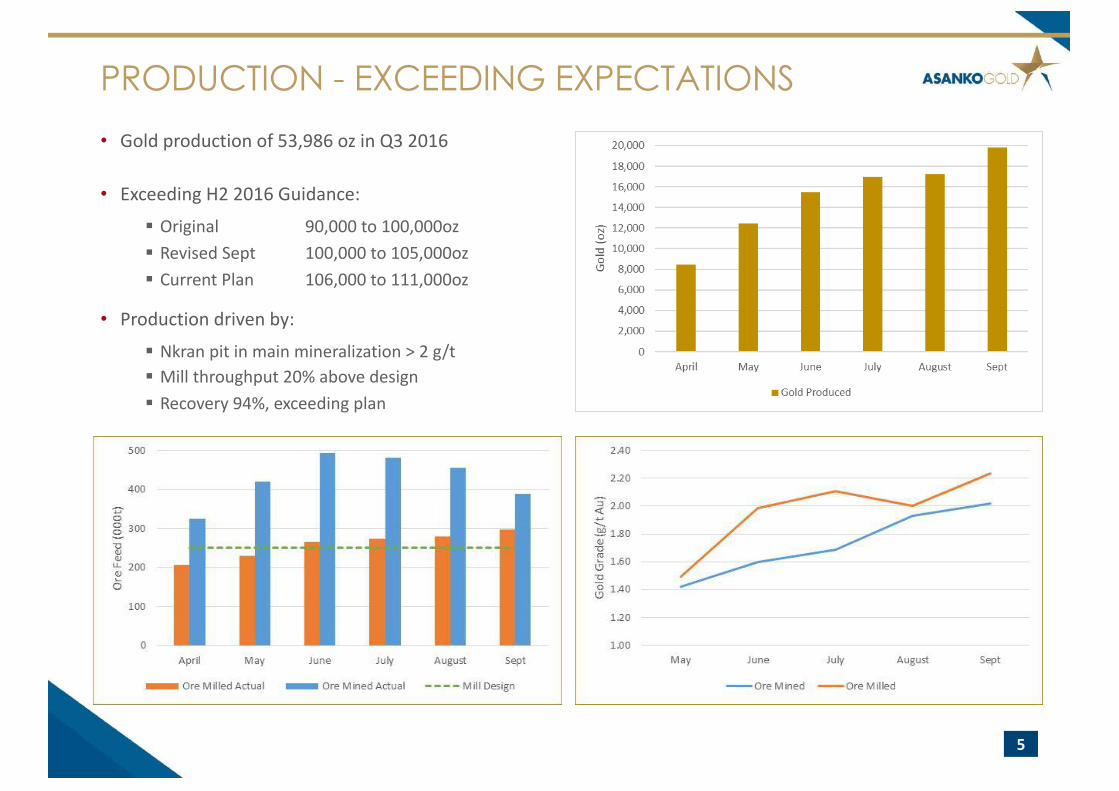

• Goldproductionof53,986oz inQ32016

• ExceedingH22016Guidance:§ Original 90,000to100,000oz§ RevisedSept 100,000to105,000oz§ CurrentPlan 106,000to111,000oz

• Productiondrivenby:§ Nkran pitinmainmineralization>2g/t§ Millthroughput20%abovedesign§ Recovery94%,exceedingplan

PRODUCTION - EXCEEDING EXPECTATIONS

5

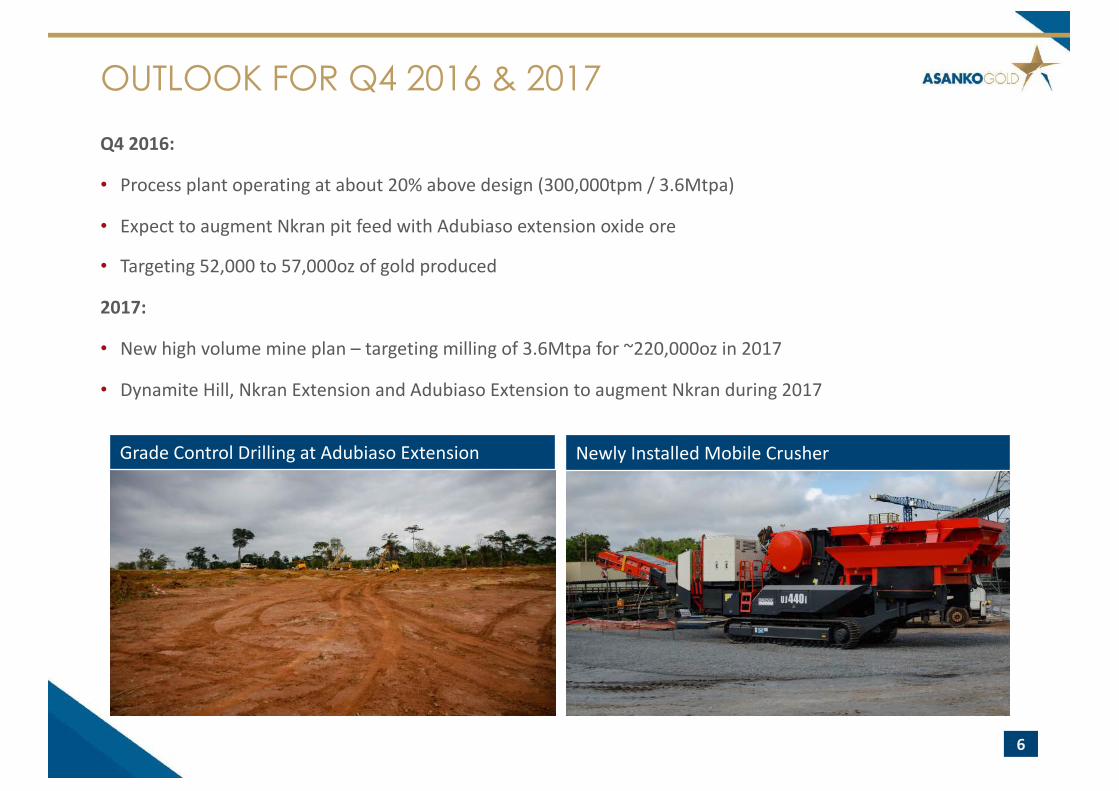

Q42016:

• Processplantoperatingatabout20%abovedesign(300,000tpm/3.6Mtpa)

• ExpecttoaugmentNkran pitfeedwithAdubiaso extensionoxideore

• Targeting52,000to57,000ozofgoldproduced

2017:

• Newhighvolumemineplan– targetingmillingof3.6Mtpafor~220,000ozin2017

• DynamiteHill,NkranExtensionandAdubiaso ExtensiontoaugmentNkran during2017

OUTLOOK FOR Q4 2016 & 2017

GradeControlDrillingatAdubiaso Extension NewlyInstalledMobileCrusher

6

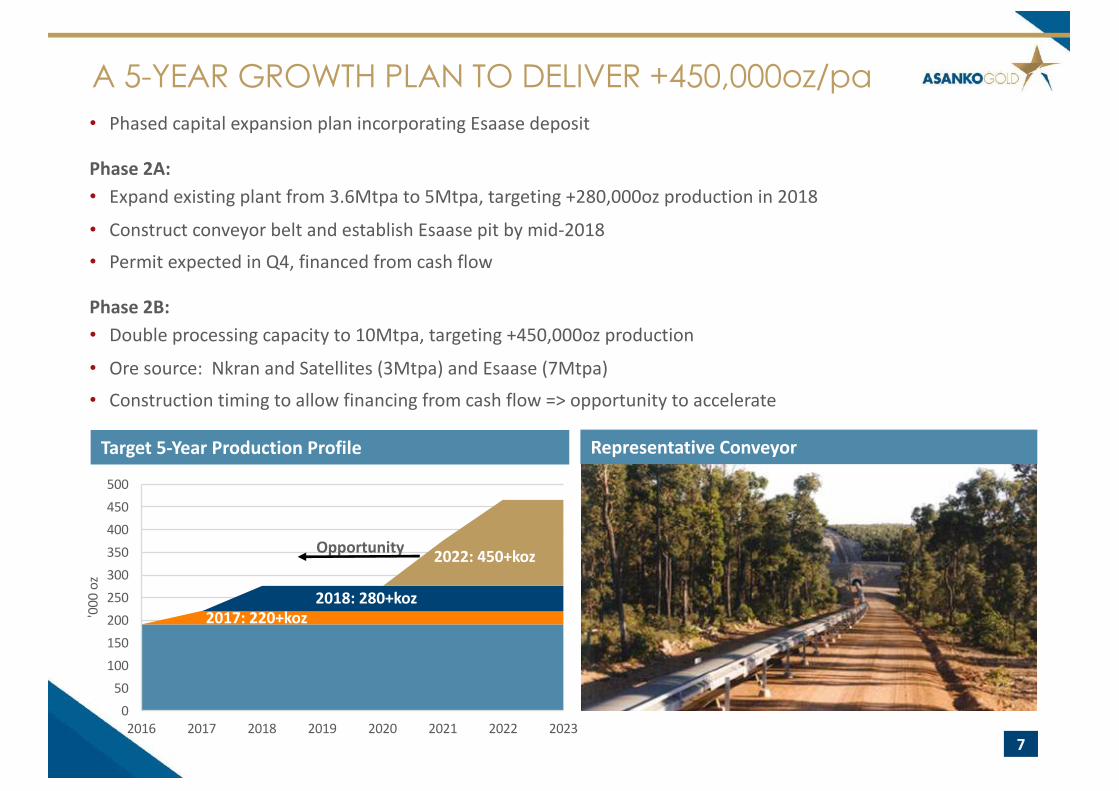

A 5-YEAR GROWTH PLAN TO DELIVER +450,000oz/pa• PhasedcapitalexpansionplanincorporatingEsaase deposit

Phase2A:• Expandexistingplantfrom3.6Mtpato5Mtpa,targeting+280,000ozproductionin2018

• ConstructconveyorbeltandestablishEsaase pitbymid-2018• PermitexpectedinQ4,financedfromcashflow

Phase2B:• Doubleprocessingcapacityto10Mtpa,targeting+450,000ozproduction

• Oresource:Nkran andSatellites(3Mtpa)andEsaase (7Mtpa)• Constructiontimingtoallowfinancingfromcashflow=>opportunitytoaccelerate

7

050100150200250300350400450500

2016 2017 2018 2019 2020 2021 2022 2023

'000oz

2017:220+koz2018:280+koz

2022:450+koz

Target5-YearProductionProfile RepresentativeConveyor

Opportunity

• Large,underexploredlandpackage

• Targetsexpectedtoprovideadditionalfeedtotheexistingplantin2017and2018untilEsaase conveyorcomplete

• Adubiaso ExtensionM&IResource

• 628,[email protected]/tfor38,[email protected]/tcut-off• MininginQ42016

• Nkran ExtensionM&IResource

• 758,[email protected]/tfor42,[email protected]/tcut-off• MininginH12017

• Akwasiso

• Non-complianthistoricalresourceof200,000oz@±2.0g/t

• 10,000mdrillingin2016• Firstsetofdrillingresultslookingexcellent• Completeresultsandmaidenresourcethisquarter

8

EXPLORATION SUCCESSRecentNear-MineDiscoveries

ImprovingLiquidity:

• Buildingcash:$11.6mCFfromoperationsinQ2,increasinginQ3

• VATrefundsuptodatetotheendofQ12016

• Nocashtaxfor2016and2017

• US$150mlong-termdebt- norepaymentuntilJuly2018

LIQUIDITY AND CAPITAL RESOURCES GROWING

Liquidity(US$m) June30th Sept 30th

Cash 34.5 57.5

Receivables 0.3 5.3

Unrefinedbullion 8.9 6.6

Total 43.7 69.4

9

ImprovingMargin:

• AdjustedAISCinQ2US$934/oz

• Target<US$800/oz lifeofmineaverageAISC

WellPositionedtoFinancePhase2AfromCashFlow

…Andourcommunities

• Strong,respectfulrelationships

• Creatingalegacybeyondthelifeofthemine

• Focusonhealth,financialliteracy,skillstraining

• PartnershipwithCODE’s“ReadingGhana”

• KeytosuccessinGhana

Lookingafterourpeople…

• Exceptionalsafetyrecord

• PeopleBasedSafetyprograminplace

• OnlyoneLTIinthepast12months

• 2.6millionLTIfreeman-hoursworked

• 0.17LTIFR(permillionmanhoursworked)

A RESPONSIBLE MINER

10

• DeliveredPhase1onbudgetandaheadofschedule• Operationsexceedingexpectations:

§ Q42016:52,000to57,000oz§ 2017: 220,000oz

• Staged,fullyfundedgrowthto+450,000oz/yr• Near-termcatalysts:• Phase2Apermitandapprovalforconstruction

• Newlife-of-mineplan(Phase2DFS)

11

ON THE ROAD TO SUCCESS

MineG&AUS$83

P/NAVComparison(AnalystConsensus)

1.39x

1.01x

0.86x

1.52x

1.32x 1.24x

1.10x 1.19x

1.03x 0.96x

0.88x

0.66x

Seniors Intermed. Juniors Randgold Endeavour B2Gold SEMAFO Guyana Torex Asanko Roxgold Pretium

AlexBuckInvestorRelations

N.AmericanToll-Free:18552467341Telephone:+44-7932-740-452Email:[email protected]

WayneDrierCorporateDevelopment

N.AmericanToll-Free:18552467341Telephone:+1-778-729-0614Email:[email protected]

CONTACT US

Appendices

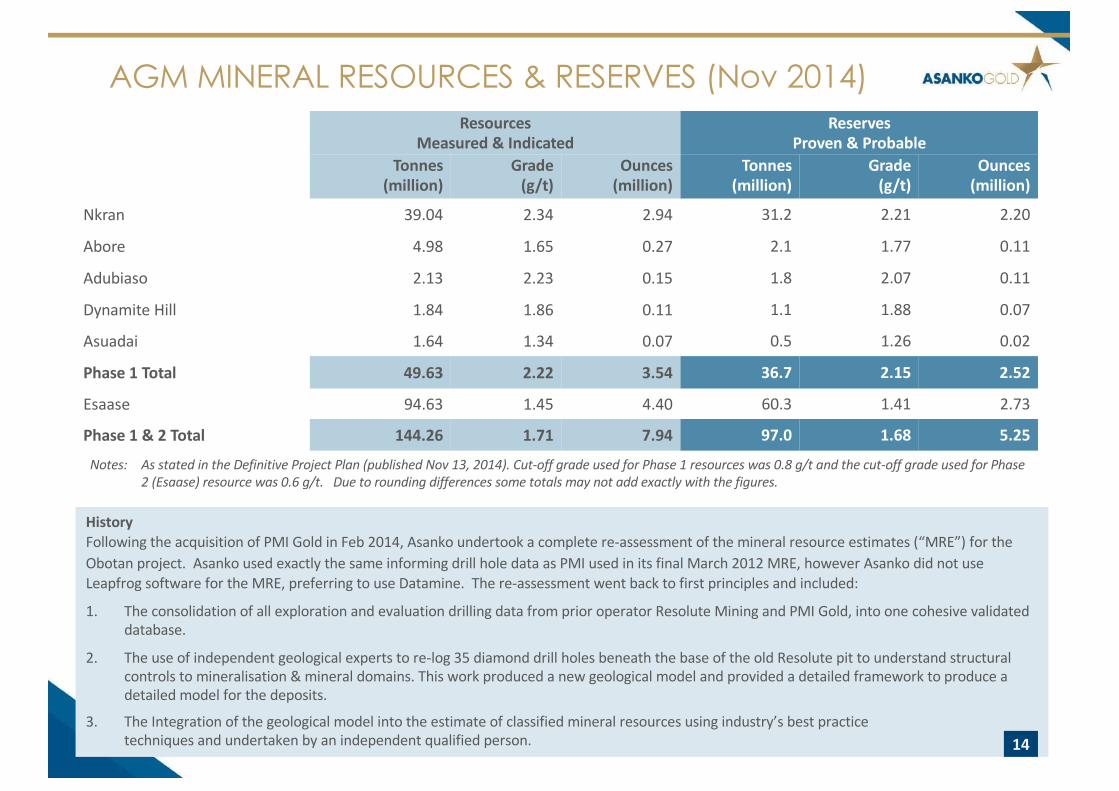

HistoryFollowingtheacquisitionofPMIGoldinFeb2014,Asanko undertookacompletere-assessmentofthemineralresourceestimates(“MRE”)fortheObotan project.Asanko usedexactlythesameinformingdrillholedataasPMIusedinitsfinalMarch2012MRE,howeverAsanko didnotuseLeapfrogsoftwarefortheMRE,preferringtouseDatamine. There-assessmentwentbacktofirstprinciplesandincluded:

1. TheconsolidationofallexplorationandevaluationdrillingdatafromprioroperatorResoluteMiningandPMIGold,intoonecohesivevalidateddatabase.

2. Theuseofindependentgeologicalexpertstore-log35diamonddrillholesbeneaththebaseoftheoldResolutepittounderstandstructuralcontrolstomineralisation&mineraldomains.Thisworkproducedanewgeologicalmodelandprovidedadetailedframeworktoproduceadetailedmodelforthedeposits.

3. TheIntegrationofthegeologicalmodelintotheestimateofclassifiedmineralresourcesusingindustry’sbestpracticetechniquesandundertakenbyanindependentqualifiedperson.

ResourcesMeasured& Indicated

ReservesProven&Probable

Tonnes(million)

Grade(g/t)

Ounces(million)

Tonnes(million)

Grade(g/t)

Ounces(million)

Nkran 39.04 2.34 2.94 31.2 2.21 2.20

Abore 4.98 1.65 0.27 2.1 1.77 0.11

Adubiaso 2.13 2.23 0.15 1.8 2.07 0.11

DynamiteHill 1.84 1.86 0.11 1.1 1.88 0.07

Asuadai 1.64 1.34 0.07 0.5 1.26 0.02

Phase1Total 49.63 2.22 3.54 36.7 2.15 2.52

Esaase 94.63 1.45 4.40 60.3 1.41 2.73

Phase1&2Total 144.26 1.71 7.94 97.0 1.68 5.25

14

AGM MINERAL RESOURCES & RESERVES (Nov 2014)

Notes: AsstatedintheDefinitiveProjectPlan(publishedNov13,2014).Cut-offgradeusedforPhase1resourceswas0.8g/tandthecut-offgradeusedforPhase2(Esaase)resourcewas0.6g/t.Duetoroundingdifferencessometotalsmaynotaddexactlywiththefigures.

15

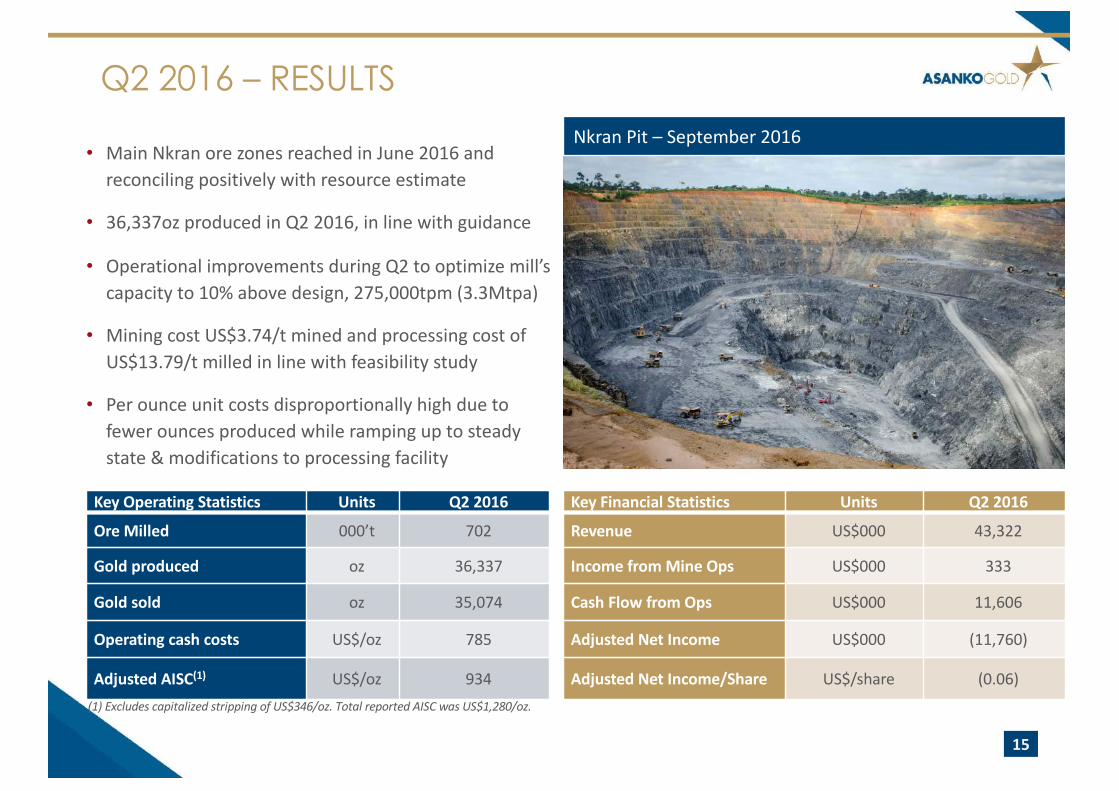

Q2 2016 – RESULTS

• MainNkran orezonesreachedinJune2016andreconcilingpositivelywithresourceestimate

• 36,337ozproducedinQ22016,inlinewithguidance

• OperationalimprovementsduringQ2tooptimizemill’scapacityto10%abovedesign,275,000tpm(3.3Mtpa)

• MiningcostUS$3.74/tminedandprocessingcostofUS$13.79/tmilledinlinewithfeasibilitystudy

• Perounceunitcostsdisproportionallyhighduetofewerouncesproducedwhilerampinguptosteadystate&modificationstoprocessingfacility

Key Operating Statistics Units Q22016

Ore Milled 000’t 702

Gold produced oz 36,337

Gold sold oz 35,074

Operating cash costs US$/oz 785

AdjustedAISC(1) US$/oz 934

Key Financial Statistics Units Q22016

Revenue US$000 43,322

Income fromMine Ops US$000 333

Cash Flow from Ops US$000 11,606

Adjusted Net Income US$000 (11,760)

AdjustedNetIncome/Share US$/share (0.06)(1)ExcludescapitalizedstrippingofUS$346/oz.TotalreportedAISCwasUS$1,280/oz.

Nkran Pit– September2016

16

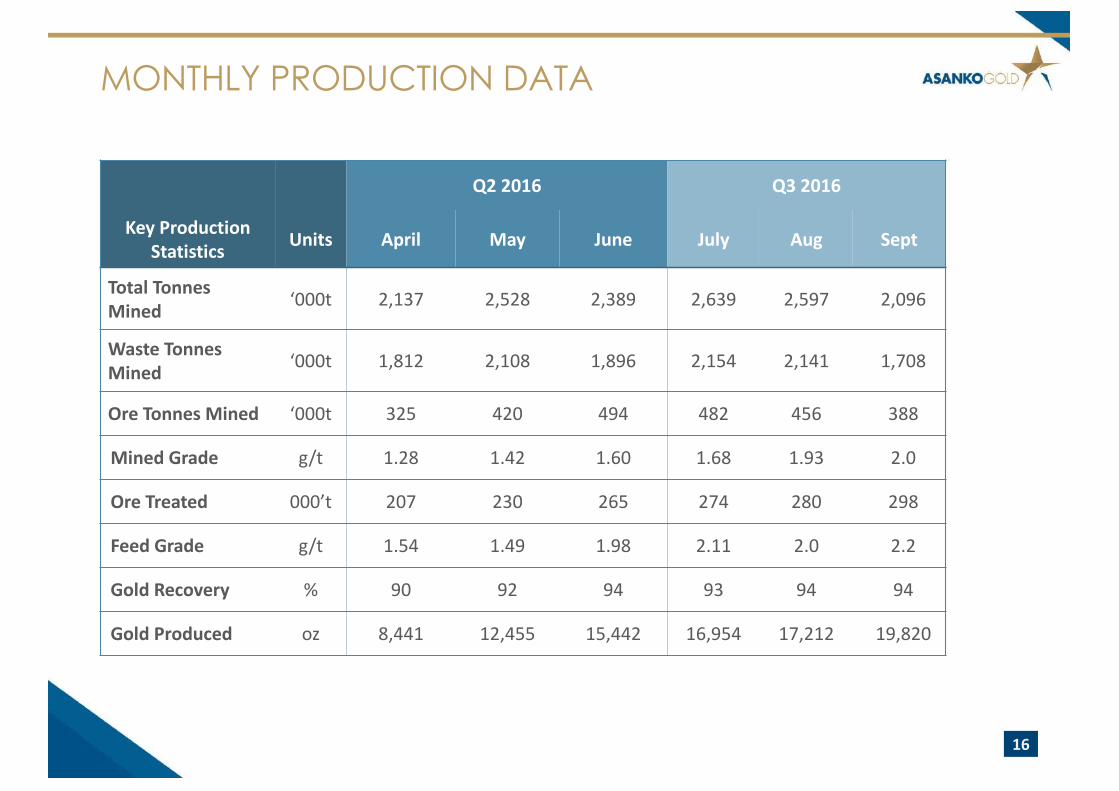

MONTHLY PRODUCTION DATA

Q22016 Q32016

KeyProductionStatistics Units April May June July Aug Sept

TotalTonnesMined ‘000t 2,137 2,528 2,389 2,639 2,597 2,096

WasteTonnesMined ‘000t 1,812 2,108 1,896 2,154 2,141 1,708

Ore Tonnes Mined ‘000t 325 420 494 482 456 388

MinedGrade g/t 1.28 1.42 1.60 1.68 1.93 2.0

Ore Treated 000’t 207 230 265 274 280 298

FeedGrade g/t 1.54 1.49 1.98 2.11 2.0 2.2

GoldRecovery % 90 92 94 93 94 94

GoldProduced oz 8,441 12,455 15,442 16,954 17,212 19,820

17

RED KITE PROJECT DEBT

ProjectLoanFacilityUS$150m

• LIBOR+6%witha1%LIBORminimum• 4millionwarrantsissuedatUS$1.83(approximatelyC$2.46)pershare,whichexpire3yearsfromdateofissue(Dec2015)

• 4yearrepaymentschedule,payablequarterly(First8payments– 11%;finalpayment– 12%)• Earlyrepaymentatanytimewithoutpenalty

• FullUS$150mdrawn• FirstquarterlyprincipalrepaymentdueonJuly1,2018• InterestrepaymentsfromJuly1,2016

• Nohedging,nocashsweep,norestrictionsonM&A

OfftakeAgreement:

• Asankotosellthefirst2.2MozofgoldproducedtoRedKite• RedKitetopayfor100%ofgoldvalue10businessdaysaftershipment

• 90%provisionalpaymentofestimatedvaluemade1businessdayafterdelivery• Salepricewillbeaspotpriceselectedduring9dayquotational periodfollowingshipment

• AsankohasoptiontoterminateOfftakeAgreementforaterminationfee,dependentonamountofgolddeliveredunderOfftakeAgreementattimeoftermination

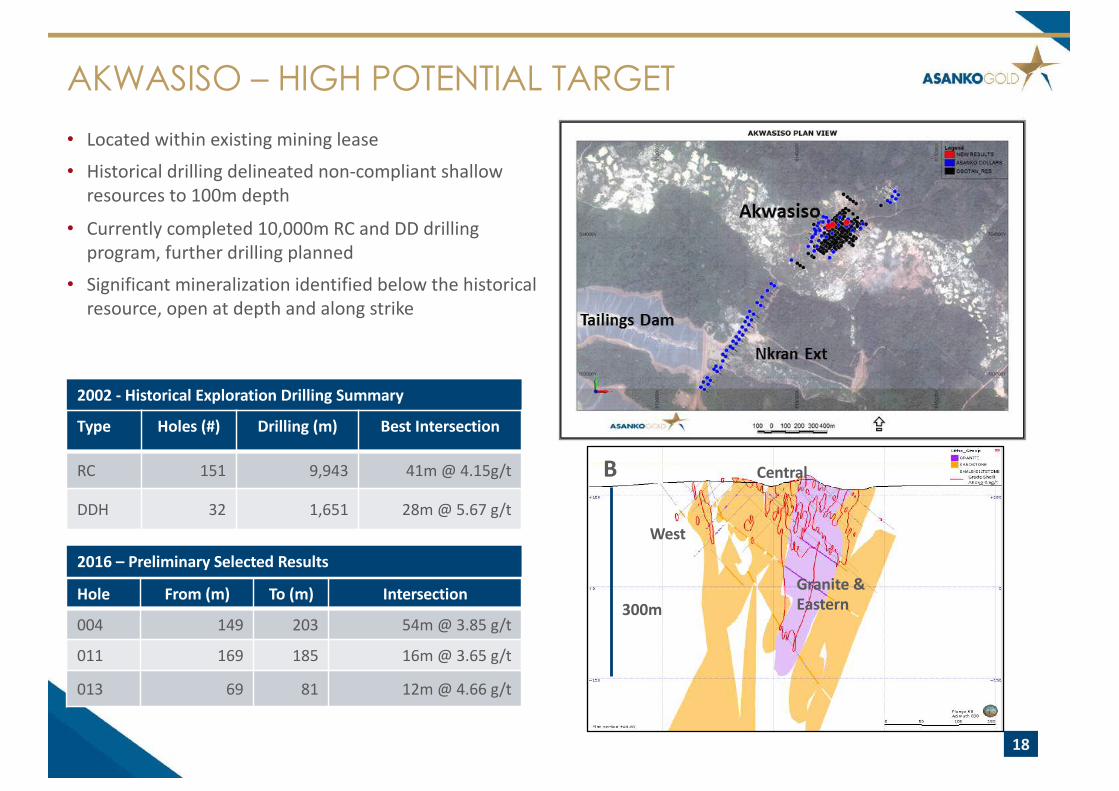

• Locatedwithinexistingmininglease• Historicaldrillingdelineatednon-compliantshallowresourcesto100mdepth

• Currentlycompleted10,000mRCandDDdrillingprogram,furtherdrillingplanned

• Significantmineralizationidentifiedbelowthehistoricalresource,openatdepthandalongstrike

AKWASISO – HIGH POTENTIAL TARGET

18

2002- HistoricalExplorationDrillingSummary

Type Holes(#) Drilling (m) BestIntersection

RC 151 9,943 [email protected]/t

DDH 32 1,651 [email protected]/t

Hole From(m) To (m) Intersection

004 149 203 54m@ 3.85g/t

011 169 185 16m@ 3.65g/t

013 69 81 12m@ 4.66g/t

2016– PreliminarySelectedResults

B

West

Central

Granite&Eastern300m