aki akitani deputy secretary general review of current economic trends in breeding & racing

TRANSCRIPT

Aki AKITANI

Deputy Secretary General

Review of Current Economic Trends in Breeding & Racing

New definition of ‘Crisis’

Crisis (by Oxford Dictionary)

‘A time of intense difficulty or danger’

危 機Ki Ki

危 crisis or danger

機 opportunity

Contents

• Analysis of Racing Data

2010 & First Half 2011

• Future Turnover Indicators

50000

60000

70000

80000

90000

100000

110000

120000

130000

2004 2005 2006 2007 2008 2009 2010

Number of Foals (2004-2010)

109,000 FoalsDecline by 7.1%

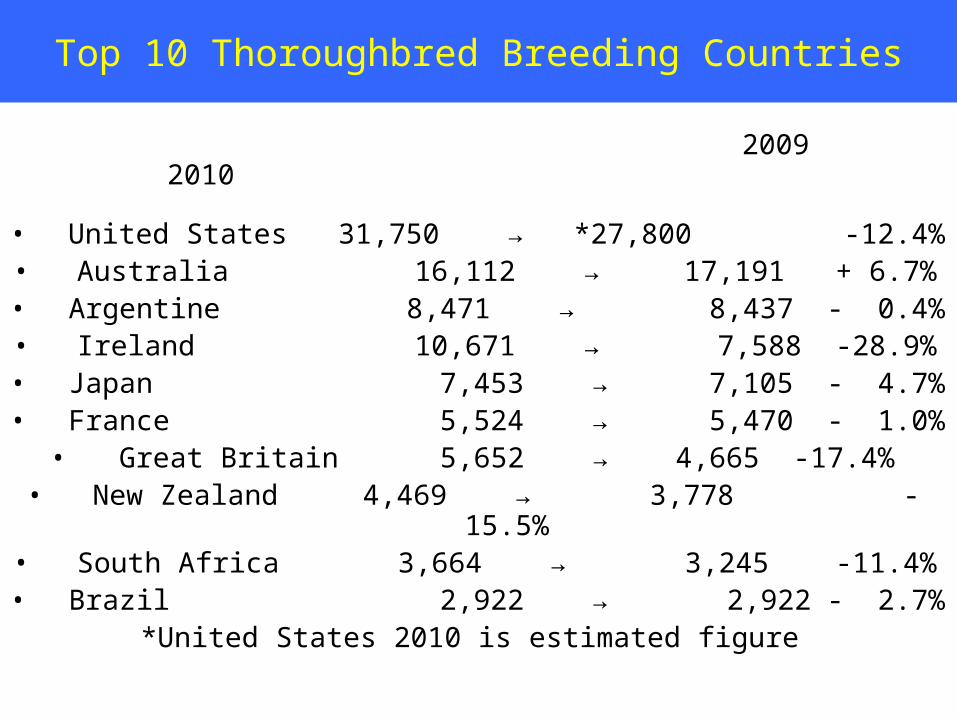

Top 10 Thoroughbred Breeding Countries

2009 2010

• United States 31,750 → *27,800 -12.4%• Australia 16,112 → 17,191 + 6.7%

• Argentine 8,471 → 8,437 - 0.4%• Ireland 10,671 → 7,588 -28.9%

• Japan 7,453 → 7,105 - 4.7%• France 5,524 → 5,470 - 1.0%

• Great Britain 5,652 → 4,665 -17.4%• New Zealand 4,469 → 3,778 -15.5%

• South Africa 3,664 → 3,245 -11.4%• Brazil 2,922 → 2,922 - 2.7%

*United States 2010 is estimated figure

0

20000

40000

60000

80000

100000

120000

140000

160000

180000

200000

2002 2003 2004 2005 2006 2007 2008 2009 2010

Number of Races 2002-2010 jumpflat

154,000 Flat 8,000 Jump

Decline by 3%

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2004 2005 2006 2007 2008 2009 2010

Prize Money 2004-2010 (billion euro)

2.86 Billion Euro+ 10.6%

-1.6%

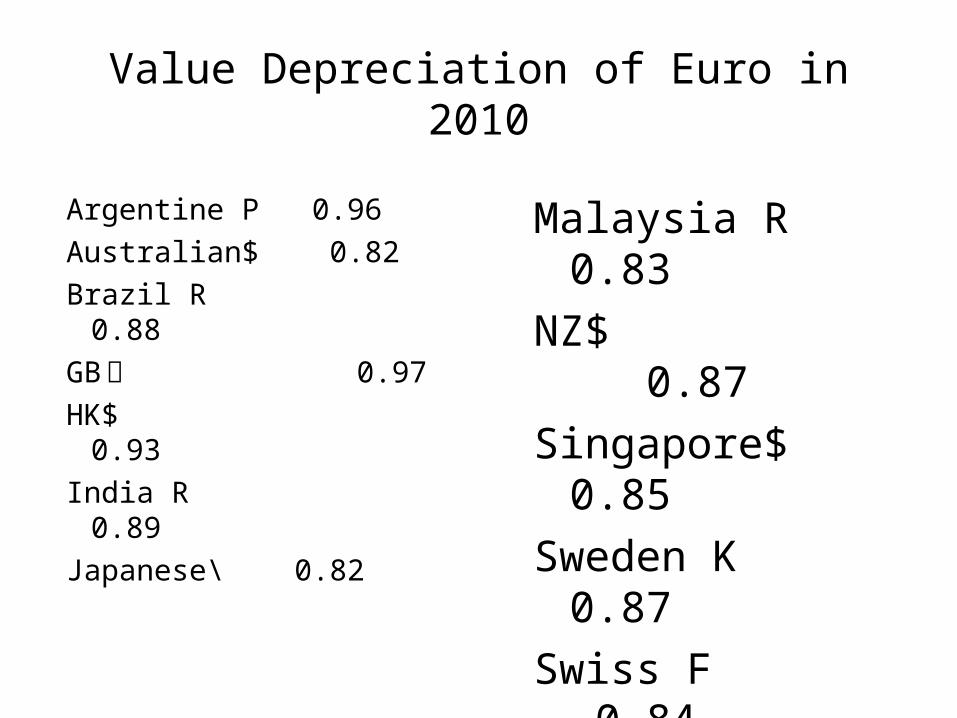

Value Depreciation of Euro in 2010

Argentine P 0.96

Australian$ 0.82

Brazil R 0.88

GB £ 0.97

HK$ 0.93

India R 0.89

Japanese\ 0.82

Malaysia R 0.83

NZ$ 0.87

Singapore$ 0.85

Sweden K 0.87

Swiss F 0.84

Turkey L 0.96

US$ 0.93

50

55

60

65

70

75

80

85

90

95

2002 2003 2004 2005 2006 2007 2008 2009 2010

Total Betting Turnover 2002-2010 (billion €)

€88 billion Increase by 5%

Decrease by 1.4%

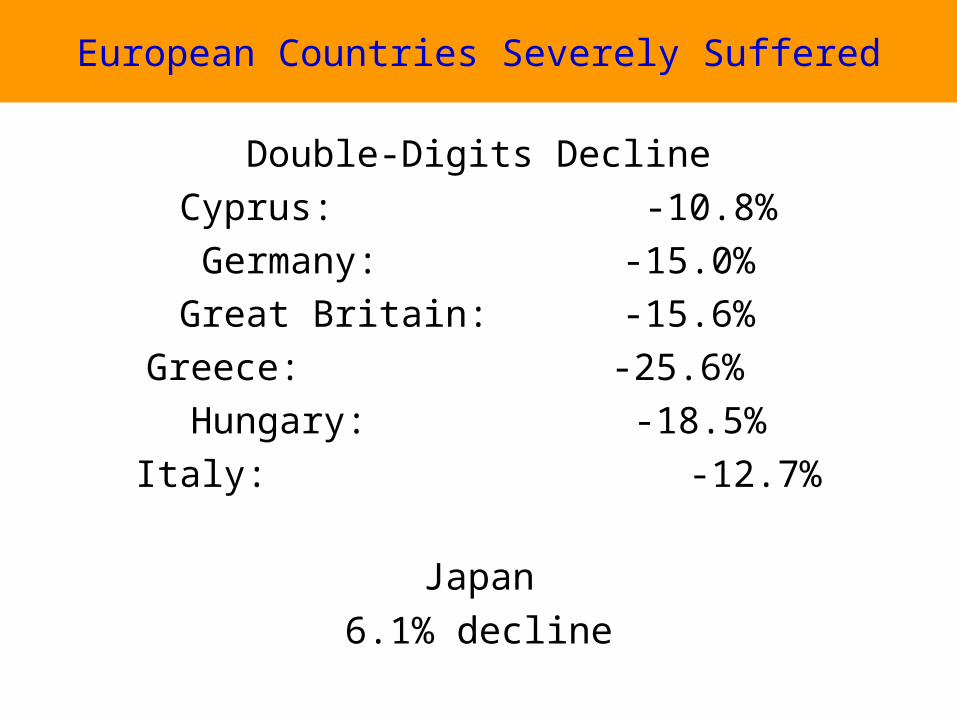

European Countries Severely Suffered

Double-Digits Decline

Cyprus: -10.8%

Germany: -15.0%

Great Britain: -15.6%

Greece: -25.6%

Hungary: -18.5%

Italy: -12.7%

Japan

6.1% decline

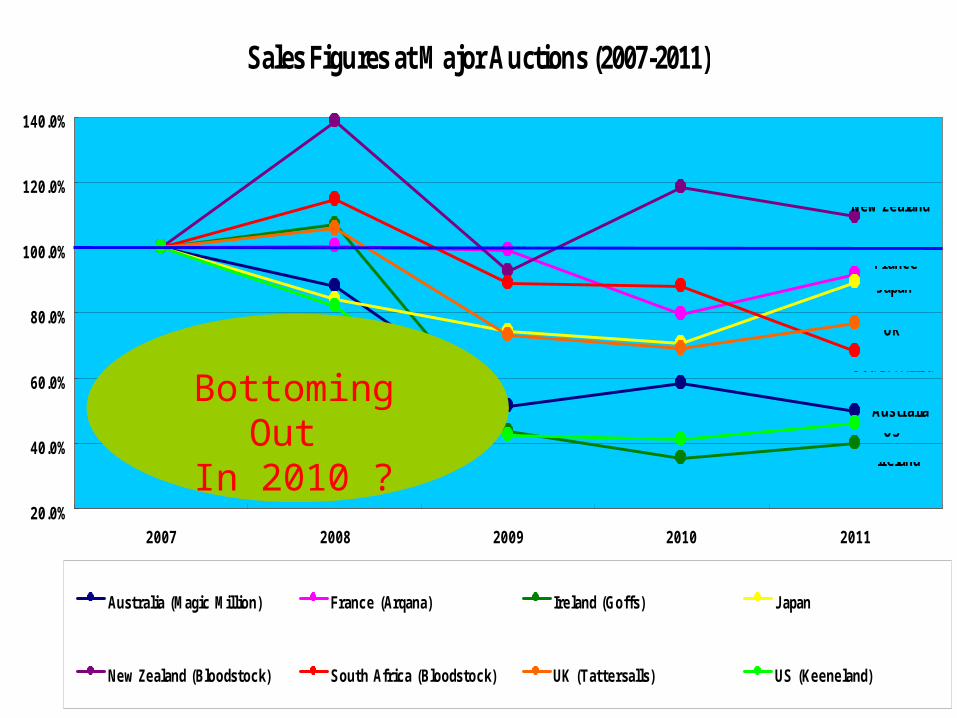

Sales Figures at Major Auctions (2007-2011)

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

2007 2008 2009 2010 2011

Australia (Magic Million) France (Arqana) Ireland (Goffs) J apan

New Zealand (Bloodstock) South Africa (Bloodstock) UK (Tattersalls) US (Keeneland)

Australia

New Zealand

South Africa

UK

J apanFrance

US

Ireland

Bottoming Out In 2010 ?

World WageringFirst Half of 2011

France (PMU) + 3.4 %

Hong Kong (Yearly) + 6.5 %

Italy - 17.8 %

Japan (JRA) - 10.4 %

Korea + 0.4 %

Singapore - 10.2 %

United States - 7.7 %

World Wagering/Gaming Outlook 2011

‘Overall we expect global horserace betting to be about on a par with 2010 -we were expecting it to be ahead by 1.5% before the earthquake.’

Simon Holliday H2 Gambling Capital

Racing Data Input On-Line

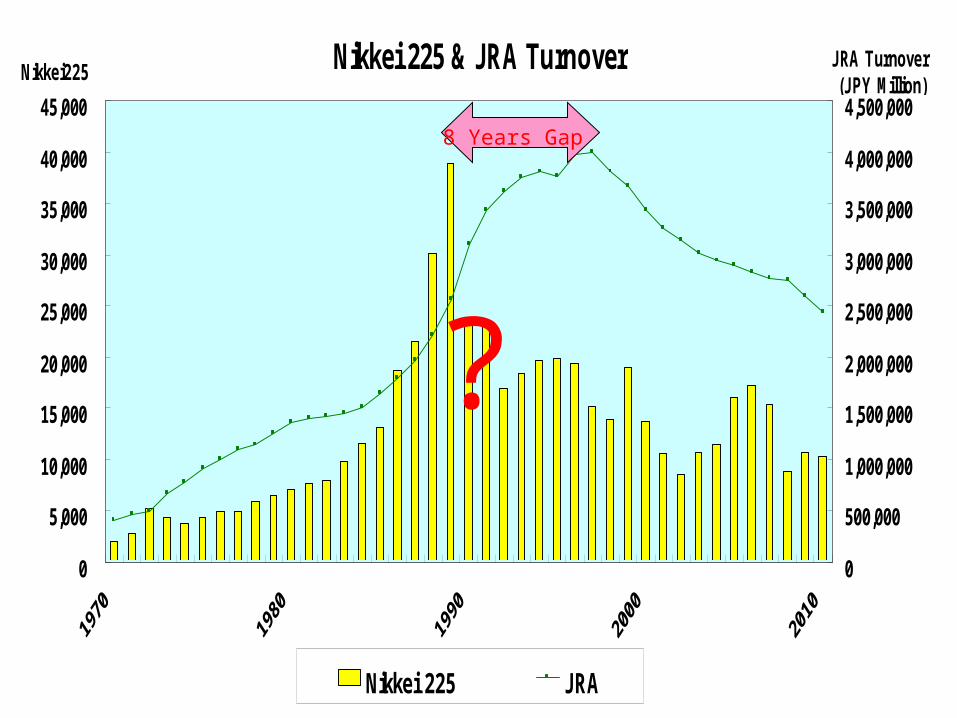

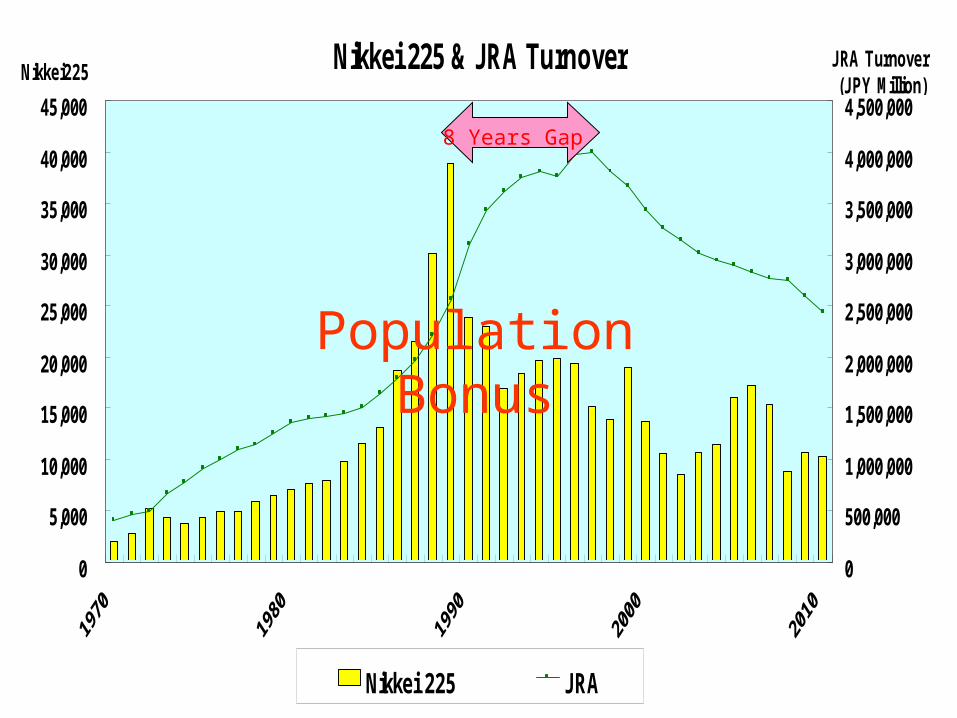

Nikkei 225 & JRA Turnover

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Nikkei225

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

J RA Turnover (J PY Million)

Nikkei 225 J RA

8 Years Gap

?

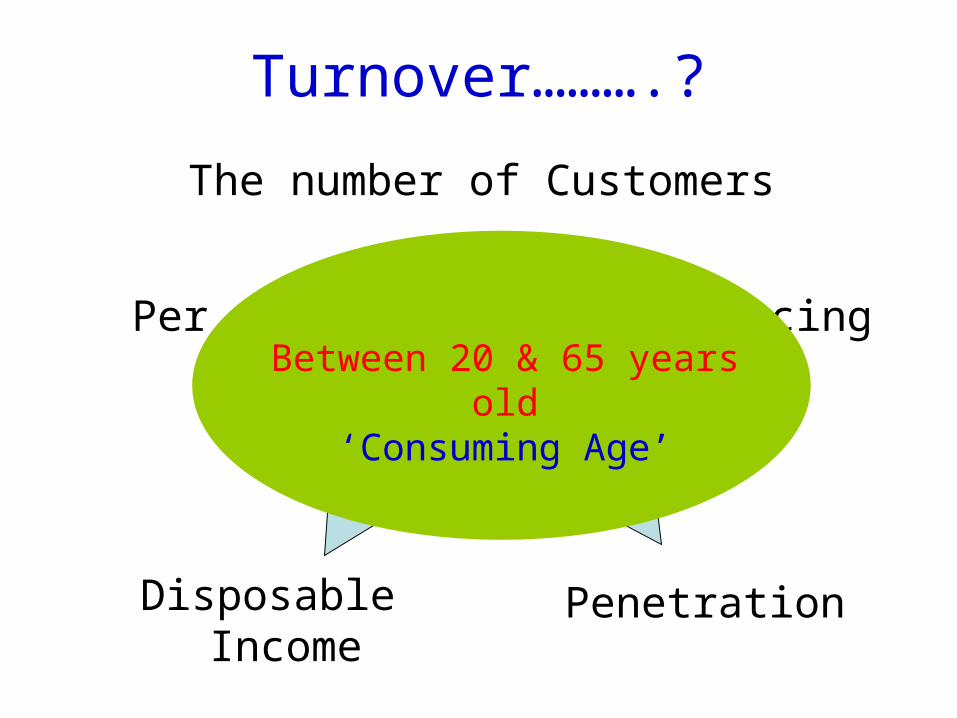

Turnover……….?

The number of Customers

X

Per Capita spending on Racing

Disposable Income Penetration

1st Session‘Racing Authorities/Pari Mutuel Operators

Still running the same race?’

Racing Authorities and Pari Mutuel OperatorsNeed promoting racing together

Racing Authorities needs to provide‘Racing Stories’

Turnover……….?

The number of Customers

X

Per Capita spending on Racing

Disposable Income Penetration

Between 20 & 65 years old‘Consuming Age’

104,665

111,940117,060

121,049 123,661 125,570 126,926 127,768 127,510

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

1970 1975 1980 1985 1990 1995 2000 2005 2009

Population Change 1970-2009 (x1,000)

Hit a PlateauIn 2004

0

2

4

6

8

10

12

0~4 5~9 10~14 15~19 20~24 25~29 30~34 35~39 40~44 45~49 50~54 55~59 60~64 65~69 70~74 75~79 80~84 85~

Demography 1970 (x millon)

Generation X

62,502,000

0

2

4

6

8

10

12

0~4 5~9 10~14 15~19 20~24 25~29 30~34 35~39 40~44 45~49 50~54 55~59 60~64 65~69 70~74 75~79 80~84 85~

Demography 1985 (x millon)

Generation XGeneration Y

73,552,000

Population Bonus

0

2

4

6

8

10

12

0~4 5~9 10~14 15~19 20~24 25~29 30~34 35~39 40~44 45~49 50~54 55~59 60~64 65~69 70~74 75~79 80~84 85~

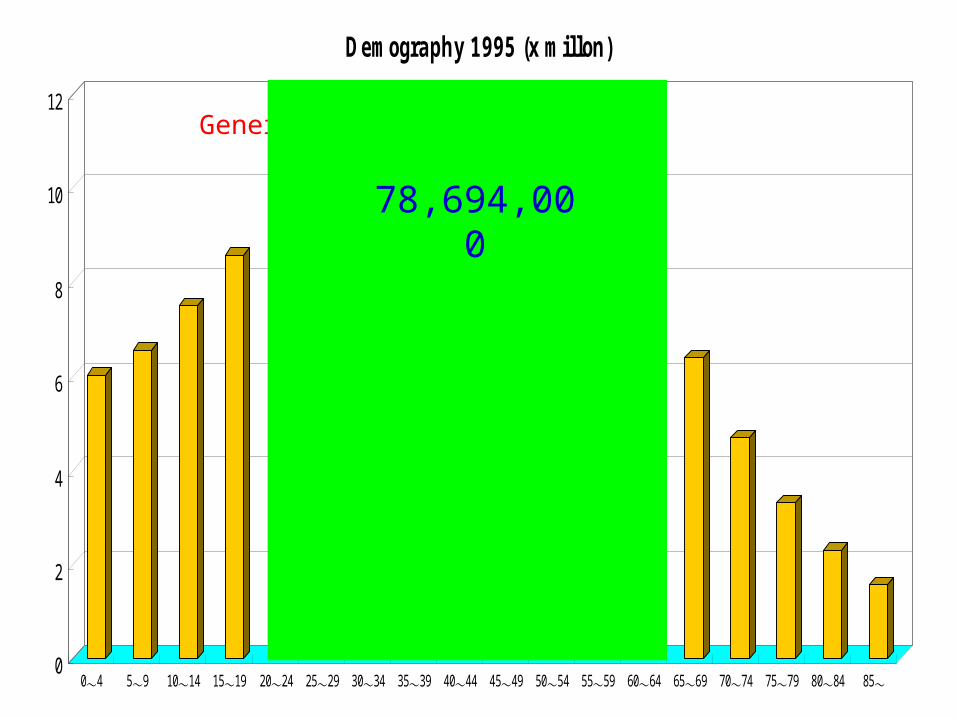

Demography 1995 (x millon)

Generation Y Generation X

78,694,000

Nikkei 225 & JRA Turnover

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Nikkei225

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

J RA Turnover (J PY Million)

Nikkei 225 J RA

8 Years Gap

Population Bonus

0

2

4

6

8

10

12

0~4 5~9 10~14 15~19 20~24 25~29 30~34 35~39 40~44 45~49 50~54 55~59 60~64 65~69 70~74 75~79 80~84 85~

Demography 2005 (x millon)

Generation Y Generation X

77,829,000

70,826,000by 2015

63,052,000by 2030

Financial Crisis in 2008

‘Crisis of the Century’

POPULATION

‘Crisis of our History’

B O N U S

China

In 2000 Census

125 million between 10 & 14

69 million between 0 & 4

45% less children in ten years

Longer term effect will be phenomenal

One Child Policy

Index (consuming age by disposable income) (no penetration)vs

JRA Turnover

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00INDEX

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00J RA Turnover

Index J RA

Customer Service Dept

Super IdolHorse

Mobile Phoneand others

What we have to do?

To know yourself

Population Bonus

Low Penetration &Disposable Income

Population Onus

High Penetration &Disposable Income

1 2

3 4

For Those Who are In Section Four

What you can do ?

Beyond Conventional MarketGeographically, Gender-wise, Generation-Wise

Efficiency

Diversification

‘Less is More’

Secure Other Sources of Income

New definition of ‘Crisis’

Crisis (by Oxford Dictionary)

‘A time of intense difficulty or danger’

危 機Ki Ki

危 crisis or danger

機 opportunity

Aki AKITANI

Deputy Secretary General

Review of Current Economic Trends in Breeding & Racing