aligning china’s economic and tax systems the role of

TRANSCRIPT

Revised 27.10.14

1

Aligning China’s Economic and Tax Systems

– The Role of China’s 1994 Tax Reform

Jeffrey Owens1

Introduction

Mr. ZHU Rongji, China’s former Premier, said that “with regard to the 1994 fiscal reform, no

matter what kind of comments you give, your comments can never be too aggressive” 2

.

Today I am looking at this reform from the perspective of a foreign tax policy scholar, and I

hope my views could also be taken as “never be too aggressive”.

I was leading the Fiscal Affairs Department of the OECD when China announced its 1994

fiscal reform plan 20 years ago. This reform was designed to be a comprehensive program

covering both fiscal system and taxation system. Many outside commentators were skeptical

as to whether China had the ability to implement this reform successfully.

As a strong supporter of China’s reform, I commented in numerous international conferences

that China’s 1994 fiscal reform would be a success. My confidence was partly based on my

belief that China needed such a radical reform, because its tax system at that time was a

barrier to China’s rapid economy development. Also my view was based upon China’s

success for over a decade in presiding over of the greatest structure transformation in history,

which showed that it had a highly competent government that thinks and acts strategically.

The State Administration of Taxation’s (SAT) strong execution capability and their

willingness to learn from the experience of other countries ensured that this reform would be

implemented, in spite of resistance from some local governments.

In this paper, I focus only on the reforms on the tax system in China’s 1994 fiscal reform,

which I call the “1994 Tax Reform”, ignoring the reforms to the fiscal system. In the first part,

I compare the reform with trends in the OECD countries. Then in the second part, I set out

five challenges facing the Chinese tax system over the next two decades.

I. Review of the 1994 Tax Reform

I.1 Necessity for Reform

China’s rapid economic development starting from the end of the 1970s set forth the basic

necessity for the 1994 Tax Reform. The piecemeal tax reforms conducted prior to 1994 were

unable to resolve the fundamental problems in China’s tax system. For example, China’s tax

system was too complex, having as many as 37 types of taxes in 1992. And, China’s tax-to-

1. Prof. Dr. Jeffrey Owens, Director of the WU Global Tax Policy Center, Institute for Austrian and International

Tax Law, Vienna University of Economics and Business (WU). Jeffrey completed his doctoral work at

Cambridge University in the United Kingdom in 1973, was the Head of the Fiscal Affairs Department and the

Director of the Centre for Tax Policy and Administration of the OECD for many years. Jeffrey established a

major taxation program at the OECD and extensively developed the OECD contacts with non-member countries.

Jeffrey has made numerous contributions to professional journals, has published a number of books and has been

the author of many OECD publications on taxation. Jeffrey's position at the OECD and his frequent participation

in international conferences, have provided him with a unique international perspective on tax policy.

The author would like to acknowledge the invaluable assistance provided by my colleague Na Li, Research

Associate and Ph.D. candidate at the Institute for Austrian and International Tax Law, in writing this article.

2. Premier ZHU’s statement in Chinese language was “对1994年的财税改革,无论怎么评价都不过分”, http://www.reformdata.org/index.do?m=wap&a=show&catid=346&typeid=&id=8375

Revised 27.10.14

2

GDP ratio in 1992 was only 12.05%3 , which was about one third of Brazil’s and the average

of the OECD countries4. Such a low tax-to-GDP ratio demonstrated that the compulsory

transfer to the Chinese government for public purpose was insufficient to finance future

development.

Therefore, a fundamental tax reform both of the tax structure and tax administration became a

necessity for China in early 1990s. Any tax reform should, on the one hand, increase the

amount of tax revenue in relation to GDP in order to finance China’s public expenditure and

support its economic development; and on the other hand, any reform should also ensure

sound public finances in respect of the efficient allocation of resources, the distribution of

income and macroeconomic stabilization.

I.2 An Overview of the 1994 Tax Reform

I.2.1 The Positive Aspects

The main lines of the 1994 Tax Reform followed trends in other countries. The Chinese

policy makers learned from the experience of these other countries, and then they adapted

those foreign experiences to a Chinese environment.

(1) Simplifying tax structure, but at the same time increasing the tax-to-GDP ratio

Up to the 1970s, tax policy was largely viewed as an instrument to raise revenue with

minimum distortions and to achieve a redistribution of income. Top marginal personal income

tax (PIT) rates in excess of 65% were the rule; top statutory corporate income tax (CIT) rates

rarely fell below 45% and tax codes, having multiple schedules, multiple rates and multiple

exemptions, tended towards complexity. A rethinking of global tax policy was initiated by the

perception that over-complex tax codes and regimes distort economic incentives of private

actors, are difficult to administer and provide wide opportunities for avoidance and evasion.

Accordingly, the OECD countries in the 1980s responded with tax reforms to simplify their

tax structures, for example, the United States’ tax reform in 1986 and the United Kingdom’s

tax reform in 1984. However, simplifying tax structure does not mean a decline of the tax-to-

GDP ratio. For example, the OECD countries’ average tax-to-GDP ratio was steady increased

from 32.4% in 1985 to 34.6% in 2012.

China reduced its taxes from 37 to 23 in the 1994 Tax Reform, which was a timely change.

And I am happy to see from the following two charts that both of China’s tax revenue and its

tax-to-GDP ratio increased since its implementation of the 1994 Tax Reform 5

. Although

China’s tax-to-GDP ratio is still lower than the average tax-to-GDP ratio at 34% across the

OECD countries, its ratio in 2012 already reached 19% and is ahead of India but behind that

of the other BRICS. Nevertheless, taking into account the non-tax revenue collected by the

local government in form of land sales revenue and government funds and administrative fees,

China’s compulsory payments as percentage of GDP might reach the ratio of some OECD

countries, such as South Korea, Australia and the United States6 .

3. According to China Statistics Year book 2013, China’s total tax revenue was RMB329.691billion for the year

of 1992. http://www.stats.gov.cn/tjsj/ndsj/2013/indexee.htm

4 . According to the OECD database, the tax-to-GDP ratio of OECD countries’ in 1992 was 33.6%.

http://stats.oecd.org/Index.aspx?DataSetCode=TABLE_I4

5. China Statistics Year book 2013, http://www.stats.gov.cn/tjsj/ndsj/2013/indexee.htm

6. Brys, B. et al. (2013), “Tax Policy and Tax Reform in the People's Republic of China”, OECD Taxation

Working Papers, No. 18, OECD Publishing. http://dx.doi.org/10.1787/5k40l4dlmnzw-en

Revised 27.10.14

3

(2) Establishing a new indirect tax system, with VAT as the primary tax and also

supplemented with business tax and exercise tax for certain specific services and

products.

Shifting from direct taxes to indirect taxes has been a trend in the past two decades in the

OECD countries as well as in the other parts of the world.

The following chart shows that the ratio of income taxes revenue, in particular the personal

income taxes, in the OECD countries have been declining after 1985, while the ratio of

consumption tax in the total tax revenue has been steadily increasing.7 VAT has been adopted

by more than 160 countries and became a major part of the consumption taxes in most of the

OECD countries, except for the United States.

7. OECD, Consumption Taxes: the Way of the Future, OECD Policy Brief, October 2007

China’s tax revenue from 1992 to 2012 (100

million RMB)

0,00

20000,00

40000,00

60000,00

80000,00

100000,00

120000,001

99

2

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

China’s tax-to-GDP ratio from 1992 to 2012

0%

5%

10%

15%

20%

25%

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

Revised 27.10.14

4

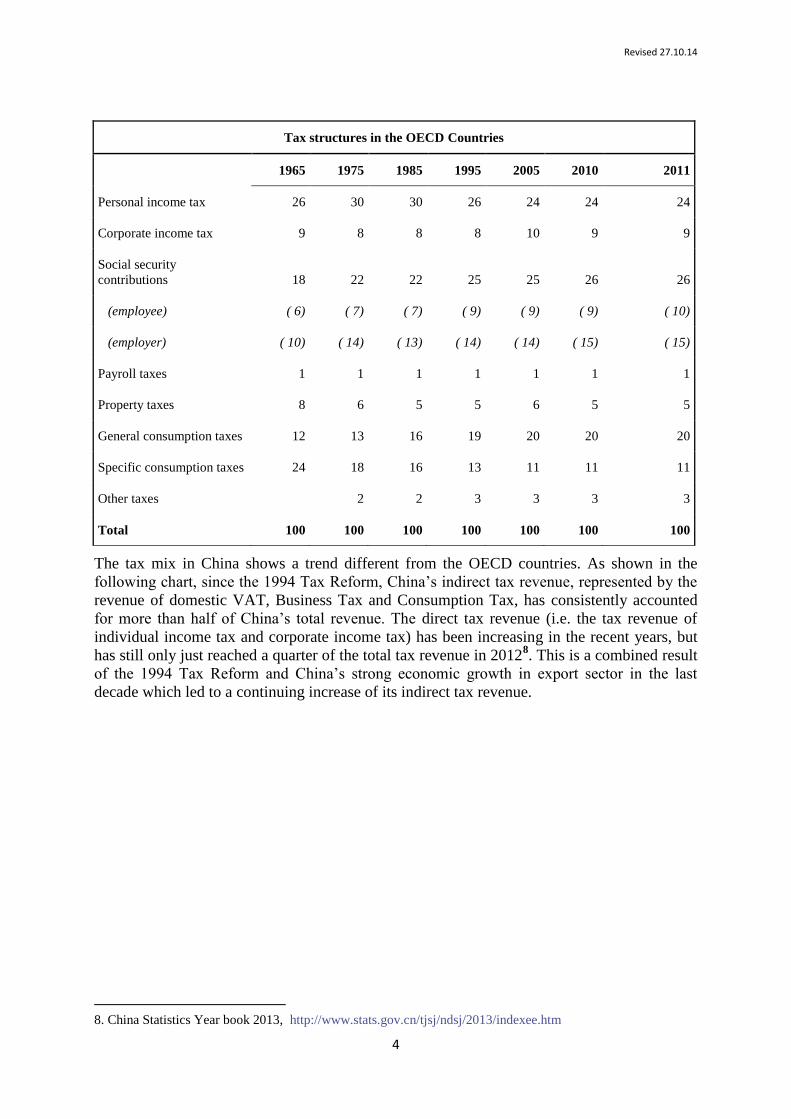

Tax structures in the OECD Countries

1965 1975 1985 1995 2005 2010 2011

Personal income tax 26 30 30 26 24 24 24

Corporate income tax 9 8 8 8 10 9 9

Social security

contributions 18 22 22 25 25 26 26

(employee) ( 6) ( 7) ( 7) ( 9) ( 9) ( 9) ( 10)

(employer) ( 10) ( 14) ( 13) ( 14) ( 14) ( 15) ( 15)

Payroll taxes 1 1 1 1 1 1 1

Property taxes 8 6 5 5 6 5 5

General consumption taxes 12 13 16 19 20 20 20

Specific consumption taxes 24 18 16 13 11 11 11

Other taxes

2 2 3 3 3 3

Total 100 100 100 100 100 100 100

The tax mix in China shows a trend different from the OECD countries. As shown in the

following chart, since the 1994 Tax Reform, China’s indirect tax revenue, represented by the

revenue of domestic VAT, Business Tax and Consumption Tax, has consistently accounted

for more than half of China’s total revenue. The direct tax revenue (i.e. the tax revenue of

individual income tax and corporate income tax) has been increasing in the recent years, but

has still only just reached a quarter of the total tax revenue in 20128. This is a combined result

of the 1994 Tax Reform and China’s strong economic growth in export sector in the last

decade which led to a continuing increase of its indirect tax revenue.

8. China Statistics Year book 2013, http://www.stats.gov.cn/tjsj/ndsj/2013/indexee.htm

Revised 27.10.14

5

(3) Establishing a uniformed individual income tax applicable to all Chinese residents

China’s relaxation of its internal migration rules in the 1980s led a significant amount of

farmers immigrating into coastal regions to become workers in manufacturing industries,

which probably played a significant role in the reduction of rural poverty. The 1994 Tax

Reform’s establishing a uniformed individual income tax, instead of the previous agriculture

tax applicable to farmers’ income, was a timely change following China’s economic and labor

policy.

(4) Separating the State Administration of Taxation from the Ministry of Finance

Recentralization of tax revenue was one of the major aims of the 1994 Fiscal Reform. In order

to ensure an efficient collection and administration of tax revenues, the Chinese government

decided to separate the State Administration of Taxation (SAT) from the Ministry of Finance.

Changing the SAT into an independent tax administration agency improved the efficiency of

tax administration, strengthened the execution power of Chinese central government and also

helped the central government to better control tax revenue.

I.2.2 The More Contentious Aspects

The VAT in the 1994 Tax Reform was designed as a production-type VAT with a narrow

base, which did not allow credit or refunds on purchases of capital goods such as equipment

or machines. This type of VAT discriminated against firms purchasing domestic made capital

goods whilst an import VAT exemption was allowed at the importing point for imported

capital goods. China has later gradually changed this into a consumption-type VAT during the

period from 2004 to 2009, as well as the present on-going reform to replacing business tax

with VAT, can be seen as the on-going improvement of the VAT system established in 1994

Tax Reform.

The dual corporate income tax system established in the 1994 Tax Reform enacted separate

income tax laws applicable to foreign investment companies and domestic companies. I

understand the policy purpose of this dual income system was to attract foreign investment.

This dual income did, however, discriminated against Chinese domestic firms and

consequently distorted the domestic firms’ investment and business. A significant amount of

Chinese investors set up ‘round-trip schemes’ with shell companies in tax havens and then use

these companies to reinvest back to China for the purpose to be eligible for enjoying the

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

taxrevenueof VAT,BT andCTtaxrevenueof CITand PIT

Ratio of China’s Indirect Tax and Direct Tax in its total Tax Revenue

Revised 27.10.14

6

preferential tax system to foreign investment9. This distortion remained until the corporate

income tax reform in 2008, which abolished the dual income system, introduced a uniformed

corporate income tax applicable to both domestic and foreign companies.

Tax reforms may cause a temporary loss of tax revenue and bring uncertainty to the taxpayers.

But the longer the waiting time for the improvement is, the higher the cost would be. This is

why the Chinese government decided to move fast, although this did lead to some

implementation problems.

II. Challenges Facing the Chinese Tax System over the Next Two Decades

Tax reform is an ongoing process and as China’s economic, social and physical environment

changes so will the tax system and tax administrations need to evolve to match these

developments. What then are the major forces which will shape the Chinese tax system and

the SAT’s role in administrating the system over the next two decades?

The Communist Party’s Politburo in June 2014 specified in its national plan that deepening

fiscal and tax reforms are the priorities and major tasks to be accomplished by 2016. China’s

tax reforms must be “reactive” to changes in its economic strategy. I see the following five

challenges rising over the next two decades:

1) Adapting the tax system to reflect that over the next two years China is likely to

become a net capital exporter as Chinese MNEs accelerated their expansion abroad

both in terms of FDI and portfolio investments;

2) Protecting the tax base in a more open environment where Chinese companies and

individuals are better place to exploit the joys of tax havens, but at the same time

encouraging voluntary compliance;

3) Examining the way that the tax system can help clean up the environment;

4) Using the tax system to address growing inequalities in the distribution of income and

wealth; and

5) Developing a new international tax governance structure which reflects China

emergence as a major player.

Each of these issues deserves an article in itself but since they are linked its helpful to provide

a board perspective on each in one article.

1. The move to a net capital exporter and maintaining the competitiveness of Chinese

enterprises

In October 2104, Mr. ZHANG Xiangchen, vice minister of Commerce stated that "it is just a

matter of time before China’s capital exports exceeded capital imports", and "if it doesn’t

happen this year it will happen in the very near future ". Right around the globe, Chinese

investors are buying up companies and assets and not just in the natural resource sector but in

sectors as diverse as chemicals to banks .With $4 trillion of foreign reserves and weak growth

and low asset prices in other markets this trend can only accelerate. In fact already today

China is the dominant trading partner of many African countries. In 2013, Chinese investor

spend more than $108 billion on foreign acquisitions and greenfield projects .This outflow of

9. According to the statistics released by the Ministry of Finance, by the year of 2012, the accumulated volume

of utilized FDI flowing to China over more than three decades has reached USD1.353 trillion. Three out of the

top ten sources are tax havens, namely the BVI (9.56%), the Cayman Islands (1.91%) and Samoa (1.47%),

ranking at the second, eighth and ninth respectively. Statistics on FDI in China (2013), accessible at

http://img.project.fdi.gov.cn//21/1800000121/File/201310/201310141023341793163.pdf, p. 13.

Revised 27.10.14

7

investment has been in part triggered by a slow-down in the domestic economy but also by a

loosening of regulations applying to outward bound investments.

Mr. LIAO Tizhong, Director General of International Taxation Department of SAT, has very

aptly characterized the change in the Chinese economy as moving not just from a capital

importing to exporting country but also moving from a factor driven to an innovation

economy and from being the world factory to the worlds market.

This new "normal" will imply profound changes in the approach of China to the taxation of

MNEs and will also raise new challenges for the SAT. China will have to ensure that its tax

system does not reduce the competitiveness of Chinese MNE operating abroad. This will

require accelerating the modernization of China approach to tax treaties as China becomes

both a residence country as well as a source country. China may also have to review its

approach to transfer pricing so that its regulations deal effectively not just with the transfer

pricing issues that arise on inward investment but also on outward investment, especially as

Chinese MNE have already got into the habit of using tax havens .

More generally China will need to reexamine its tax systems to see whether there are

structural features which may impede competitiveness, by:

Shifting part of the tax burden for direct to indirect taxes

Shifting the tax mix from direct tax to indirect tax is a trend in many countries. This shift can

be conducted in a revenue-neutral way and can boost competitiveness. By lowering unit labor

costs and changing the relative price of imports - since VAT bears on domestic consumption -

the idea is to foster exports and thus to improve the trade balance. As part of a broader

package of reforms involving labor, product and financial markets, a shift towards indirect

taxes might be helpful to enhance the flexibility of prices and wages, particularly important as

wages in China are expected to double in the next 8 years. Therefore, indirect taxes in many

countries are becoming a more important source of tax revenues.

In order to minimize economic distortions, the most efficient approach would be to levy VAT

at a uniformed rate or as few rates as possible on the broadest possible tax base. The model to

follow is not that of the EU with its high rates and narrow base but that of countries like

Chile, Korea, New Zealand or Singapore with their low rates and broad base. China’s on-

going VAT replacing Business Tax reform applies five tax rates (17%, 13%, 11%, 6% and

0%) to different industries and transactions. Such a multiple VAT rates design could causes

economic distortion to the business as well as increasing the administrative and compliance

difficulties. A long term goal should be to have a single standard rate with a reduced rate

applicable to certain specific public-benefits products.

Changing key features of taxes on income and profits

Many countries including China are increasingly competing as a location for foreign direct

investment (FDI), to attract skilled labor, jobs and R&D. As a result, corporate income tax

rates have been driven down, tax incentives and tax free zones are used heavily in spite of

their disputed effectiveness, and countries are reconsidering how to tax income earned

offshore.

Aggressive tax competition over an increasingly mobile tax base can be harmful to growth,

equity, and prosperity. Therefore, to get the full benefits of tax competition, the international

community needs to coordinate and to commit to certain “rules of the game”, just as it does in

the case of free trade. China should play a key role in the G20 debate, taking into account its

many years-experience in attracting foreign investment as well as its abolishment of foreign-

oriented tax incentives in its 2008 corporate income tax reform.

Revised 27.10.14

8

China will also have to balance the need to get Chinese MNE to comply with the need to

maintain their competitively as the operate abroad .This may require reviewing Chinese

position on transfer pricing since any rules will not only have to work for inward investment

but also outward investment. Also there will need to be recognition that China will have a

much bigger stake in having one set of globally accepted transfer pricing rules.

2. Protecting the tax base and minimizing tax disputes

As China moves from a closed to an open economy, as regulations on inward and outward

investment are relaxed and as the currency moves towards convertible so China will

increasingly encounter the typical challenges that OECD countries are facing: how to protect

the tax base in a more open environment.

This is the bad news for SAT, but the good news is that over the last 5 years many countries

have developed new tools to deal with offshore non-compliance and there is a new mood on

"zero tolerance" towards offshore evasion and a new willingness on the part of countries,

including traditional tax havens, to cooperate. So the SAT will be able to learn from these

experiences and to "ride" the new tiger of international cooperation.

In 2014 almost 14% of FDI transited via BVI, Caymans Islands and Samoa. Many "red chip"

Chinese companies chose these jurisdictions as the place to establish special purpose vehicles

as a first step to listing on foreign exchanges .Tax was not the only factor influencing this

choice: government regulations, a limited domestic capital market and foreign exchange

control all played their part. It’s also noteworthy that recently the proportion of FDI flowing

through these havens has fallen off, in part because of changes in regulations but also because

China now has Tax Information Exchange Agreements (TIEAS) with BVI and Caymans and

SAT has put in place more stringent residence requirements, introduce GAARS into its

treaties and has better information powers. It’s also interesting that these actions have led to

the yield from SAT cracking down on offshore evasion increasing from RMB 38.4 billion in

2008 to RMB 117.2 billion in 2012.

Offshore non-compliance is not be limited to companies (both Chinese and non-Chinese).

Rich Chinese citizens (and China now has as many billionaires as the average OECD country)

are discovering the joys of offshore tax heavens. This could pose a serious threat to the tax

base and undermine the confidence of Chinese citizens in the fairness of the tax system.

To address these issues the government will need a multi-prong approach embracing:

a. Improving the information and enforcement powers of SAT

Extending its network of tax information exchange agreements. Current China has

signed only 10 tax information exchange agreements, as against the United Kingdom

which has signed 29 bilateral tax information exchange agreement.

Looking at whether it wants to adapt a FATCA type approach as embedded on the

Model 11 type of intergovernmental agreements that a number of OECD countries

have signed.

Putting in place quickly the new G20 inspired rules on county by country reporting

and a master file for transfer pricing and identifying which countries want to move

from exchange on request to automatic exchange.

Setting up a system within SAT which would enable the easy matching of information

from abroad with domestic files and then using this information to put in place a more

sophisticated risk management program. And

Creating a unit within SAT to deal with “High Net Wealth” Individuals.

Revised 27.10.14

9

b. Improving closer cooperation between SAT and the government departments that deal

with money laundering and corruptions

Countries that have moved in this direction have found that is help counter more

effectively all forms of illicit activities. In the context of the current anti-corruption

campaign China may need to review how other law enforcement departments could

cooperate with SAT to counter all forms of illicit activities, including tax evasion. The

experience of OECD countries shows that tax administrations are very effective in

identifying bribes and money laundering since auditors are on the ground and have "a

nose" which is trained to " smell" out such activities. Also, experience shows that

Financial Intelligence Units often identify cases involving tax evasion. This is why most

OECD countries now have a seamless cooperation between these different departments, a

trend which has accelerated since the FATF make tax crimes a predicated offence.

c. Changing the relationship between SAT, MNEs and Tax advisors

Good tax compliance requires good enforcement plus good services. SAT needs to ask

if it has got the right balance here.

Moving towards a relationship with big taxpayers based upon the FTA developed

concept of cooperative compliance i.e. a relationship based upon transparency,

openness and trust. If Russia can move in this direction, so can China.

Seeing tax advisors as a partner that can be used as a bridge between the SAT and

small to medium-size enterprise, especially as these begin to go global using new

technologies.

Exploring the idea of joint auditors and gradually moving from just international tax

cooperation to tax coordination (e.g. playing an active role in the recently launched

JITSIC Network).

d. Providing SAT with the resources to deal with offshore non-compliance

The opportunities offered by the G20 initiatives can only be fully exploited if:

SAT is given more resources to work on the international tax issues. Currently these

resources are far below that of India or Brazil, not to speak of the G8 countries.

There is a greater centralization of decision making on international questions. In a big

country like China it is essential that wherever a taxpayer operates-from east-coastal

city of Shanghai to the far-west border of Kashi in Xinjiang, he knows that he is going

to get the same treatment.

e. Minimizing and resolving tax disputes

China has a good record of minimizing cross border tax disputes, although it can be expected

that as China moves to be a net capital exporter and the effects of the BEPS project kicks in so

the number and complexity of disputes will increase. This risks creating uncertainty for

business and exhausting the resources of the SAT. To minimize these risks requires SAT:

To review the incentives provided to tax auditors and to ensure that these are based

upon sophisticated performance management measures and not simple revenue

targets.

To reexamine domestic appeal procedures to ensure that these are impartial and

effective

To consider the use of independent mediators to resolve issues of facts in transfer

pricing cases

Revised 27.10.14

10

To use the Manual on Mutual Agreement Procedures (MAP) produced by the OECD

to improve its own MAP.

To consider on a selective basis whether it should include arbitration provisions in its

tax treaty.

f. Helping Chinese MNES understand their compliance obligations when they operate in

developing countries

Chinese MNE s are now the dominant investor in many less developed countries (LDCs) and

discussion with officials in these countries suggest that these enterprise are often not fully

aware of their compliance obligations, both as regards tax and non-tax issues. SAT could

reinforce its" education" program with these enterprises to ensure that Chinese companies are

seen as good corporate citizens in the countries within which they operate.

3. Social cohesion: the role of taxes in reducing inequalities

Growing inequality has become a global phenomenon. Countries as diverse as the United

States and India have seen the distribution of income and wealth reach levels that were last

seen in the 1920's. China has not been immune to this trend and today its Gini coefficient - the

traditional way that inequality is measured - is on par with that of the United States.

Organizations like the World Bank, the OECD and the IMF have recognized that this is not

just a social issue: it's also an economic issue. Recent studies have shown that as inequality

increases so social cohesion is undermined and it becomes more difficult to put in place

structural policy to achieve sustainable growth. Why has inequality increased? Two culprits:

the globalization of the economy has brought into the labor market more than a billion new

Chinese, India and other emerging economies workers which have tended to force down

wages for the lower income groups. At the same time new technologies are putting pressure

on the middle classes as computers take over more of their traditional jobs. All of this has

been combined with the development of a global market for highly skilled managers and

entrepreneurs which in turn has led to a "winner takes all mentality" and a rocketing of the

wages of what some have called "Davos" men: and yes they are usually men! These

underlying trends have been accentuated by tax / benefit systems becoming less progressive.

What can the Chinese government do to reverse these trends?

The main burden to reduce these inequalities must come from the regulatory and

benefit side of government. Empirical evidence shows that minimum wages and

social programs directed at low income groups can make a significant difference but

the key in the long run is better education and lifelong skill training.

Improve tax compliance by the higher income groups, especially in the offshore

sector, by directing more resources to implement the new exchange of information

agreements that have been put in place as a result of the G20 initiatives.

Reviewing the way that China taxes capital income. This could be done by initiating a

long term study which would examine the impact of introducing an inheritance and

gift tax, possible a Net Wealth Tax and more effective taxation of capital gains. Such

taxes should be seen not primarily as a source of revenue but as a way to show to the

average citizen that the government is serious about reducing inequalities.

Review the taxation of land and buildings to see how these property taxes can

contribute to reducing inequalities and at the same time proving a valuable source of

financing for lower levels of government. The current property tax project in China

can help here.

Revised 27.10.14

11

Re-examine specific sales taxes on products and services which are primarily

consumed by the rich (e.g. private planes, luxury hotels etc.).

4. Reducing pollution and improving the environment : the role of taxes

Given the new emphasis to protect the environment and to encourage a more efficient use of

energy, environmental taxes, such as ‘green tax’ or ‘carbon tax’, should be considered. An

environmental tax generally should be levied as directly as possible on the pollutant or action

causing the environmental damage. The scope of the environmental tax should ideally be as

broad as the scope of the environmental damage. Environmental taxes should also apply

uniformly with few exceptions in order to encourage abatement at the lowest-cost for

consumers and businesses. A tax applied on a uniform basis also minimizes the costs of

compliance for taxpayers and the costs of administration for government, and reduces the

opportunities for tax evasion. Finally, competitiveness concerns need to be carefully assessed,

and timing issues are crucial as well. The OECD countries are moving toward market-based

approaches such as emissions taxes and trading schemes, which request for a strong

institutional basis, adequate scale and appropriate government interventions. The SAT will

have a key role here.

By increasing the cost to a polluter of generating pollution, taxes also create a strong incentive

for firms to develop new innovations and for business and consumers to adopt existing ones.

This is especially the case for market-based innovations. However, the breakthrough

technologies that will lead to fundamental environmental improvements are less likely to be

developed under a tax-only regime than under a regime that includes particular incentives for

research and development. The long-term and more fundamental nature of such projects

creates uncertainty for investors as these projects entail a high probability of failure. In such

cases, environmental taxes may need to be supplemented by targeted direct subsidies and

incentives for R&D.

5. Developing a new international governance structure in the tax area: the role of

China

In 1994 China was very much an onlooker in the international tax world. It attended meetings

of the UN and the OECD but more in the role of a bystander. It followed but did not

substantially contribute to the global debate on taxation. Over the last two decades all this has

changed. Today SAT and Ministry of Finance officials are making their voice heard in

international fora. Yet, China’s role in international tax cooperation is still work in progress.

So what choices does China have over the next two decades? Or put another way where will

China take its tax football to play? The key issues for China are:

Does it try to create new institutions?

It could, for example, push for the newly created BRICS Bank in Shanghai to play a role in

taxation. BRICS Commissioners already meet on an annual basis and there have been some

attempts at coordinating the position of the BRICS on the G20 tax agenda. But in practice the

economic, political and social conditions of these five countries are so diverse as to make

practical cooperation a difficult task, although, this could change with the creation of the

BRICS Bank this year. China could push to change the status of the Study Group on Asian

Tax Administration and Research (SGATAR), which up to now has been a pretty low key

informal grouping pulling together Asian-Pacific countries. But to succeed here would require

having a strong secretariat as is found in other regional tax administrative organization such

as CIAT or ATAF. And, of course, this is not a tax policy forum. It could also try to set up a

tax department in the Asian Development Bank which currently does very little in the tax area.

Revised 27.10.14

12

How can it use more effectively standard setting global institutions like the OECD

and UN?

Already China plays a very active role in these two organizations. China’s relationship with

the OECD goes way back to beyond the 1994 tax reforms. But with the G20 BEPS initiative,

China has been put on the same footing as OECD countries: i.e. it is part of the decision

making process.

The question is whether this new institutional arrangement will continue after the BEPS

project is completed? As China moves towards the typical economic structure found in

OECD countries and in particular becomes a net exporter of capital, so will its tax interest

increasingly align with that of OECD countries. A trend that would be reinforced if OECD

continues to serve as the de facto secretariat for the G20 tax work .If the other BRICS also

decided to go in this direction this would create a very powerful grouping of countries –

OECD plus non OECD G20- accounting for more than 90% of the global economy. And it

would be a grouping that would have the capacity to set global tax rules and to see that these

are implemented consistently around the world, taking into account the interests of developing

countries. This is an attractive option for a country like China that is now the biggest exporter

in the world and whose companies are playing an increasingly important role in the world

economy.

As regards the UN, Mr. LIAO Tizhong was very active at the UN Tax Committee, and right

now Ms. WANG Xiaoyue is taking over Mr. LIAO’s position and continuing to contribute to

the Committee. China plays a lead role in its debates, especially on tax treaties and transfer

pricing. The UN group has the advantage of being an inclusive grouping bringing together

effectively all the countries in the world. But it is constrained by resources and by limited

agenda. Also, as China moves towards a developed country status so its interests will diverge

from that of a typical developing country.

Given these different options perhaps the sensible middle course for China is to pursue all of

them simultaneously: strengthen existing institutions in the Asian-Pacific region, use the

BRICS as an informal forum to try to coordinate the position of the 5 countries on the

international debate on taxation, push to maintain its new position at the OECD and to use the

Post BEPS period to initiate there a real debate on source versus residence taxation with the

aim of getting a real consensus on a set of adapted treaty rules and transfer pricing rules that

works for China and other emerging economies and OECD countries. And, at the same time

help build up a consensus to change the structure and financing of the UN group. For example,

China could encourage the BRICS to raise new funds for the UN Tax Committee. That would

enable an expansion of the mandate of the group so it could parallel the current tax mandate

of the OECD. China is well placed to play this role and, as can be seen from the active and

constructive role played by Chile and Mexico at the UN, there is no contradiction between

being close to the OECD and being a "good" UN member.

III. Conclusion

The starting point for this article was that whilst the 1994 reforms were a good starting point

for modernizing the Chinese tax system, much remained to be done. Progress has been made

in developing a unified corporate income tax. China is on the road to implement a true VAT

system and is reviewing its taxation of property. But over the next two decades, the Chinese

economy will undergo a second transformation as it moves up the technological chain and

becomes more of a service economy and a net capital exporter. The middle classes will

expand opening up new potential tax bases. Pressure will increase to have heavier taxes on the

rich as a way to reduce inequalities. Citizens will push for tax to play a role in cleaning up the

environment. Chinese MNEs will expect that the tax systems don’t put them at a competitive

Revised 27.10.14

13

disadvantage and that tax disputes with other countries are minimized and when they do arise

are quickly resolved. So my expectation is that the long march to adapting the tax system of

China will be an on-going process. I hope that in a modest way I can be part of that process.