all about interest rates federal reserve bank of new york college fed challenge student seminar...

TRANSCRIPT

All About Interest RatesFederal Reserve Bank of New YorkCollege Fed Challenge Student Seminar

October 9, 2007

Raymond StoneStone & McCarthy Research Associates

* This presentation incorporates graphics from Money, Banking and Financial Markets, 8th edition, Frederic Mishkin

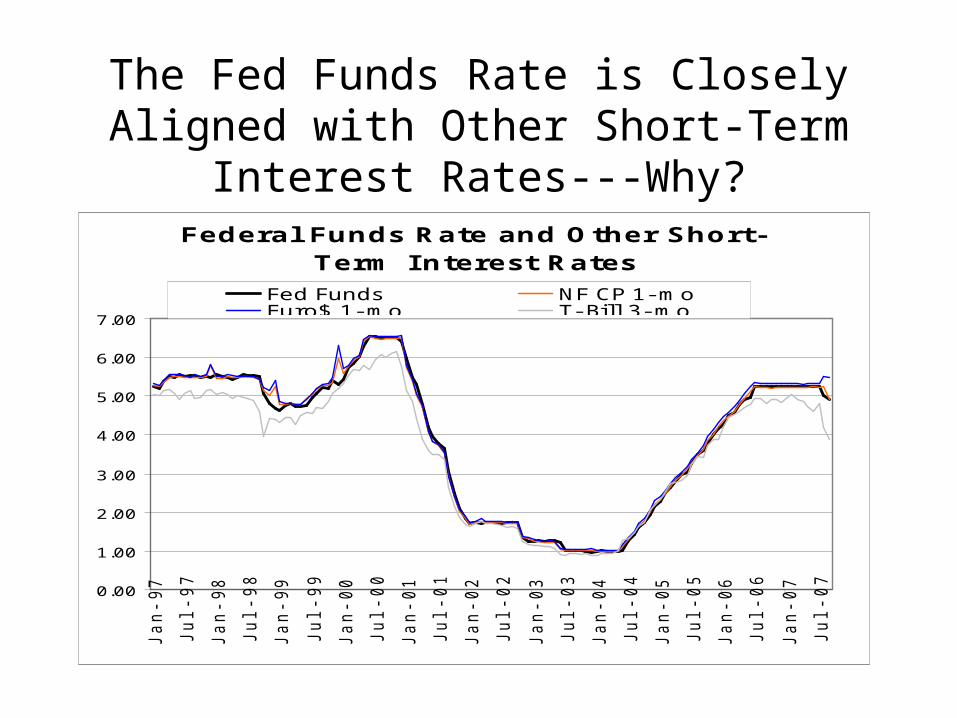

The Fed Funds Rate is Closely Aligned with Other Short-Term Interest Rates---Why?

Federal Funds Rate and Other Short -Term I nterest Rates

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

Jan-9

7

Jul-97

Jan-9

8

Jul-98

Jan-9

9

Jul-99

Jan-0

0

Jul-00

Jan-0

1

Jul-01

Jan-0

2

Jul-02

Jan-0

3

Jul-03

Jan-0

4

Jul-04

Jan-0

5

Jul-05

Jan-0

6

Jul-06

Jan-0

7

Jul-07

Fed Funds NF CP 1- moEuro$ 1- mo T- Bil l 3- mo

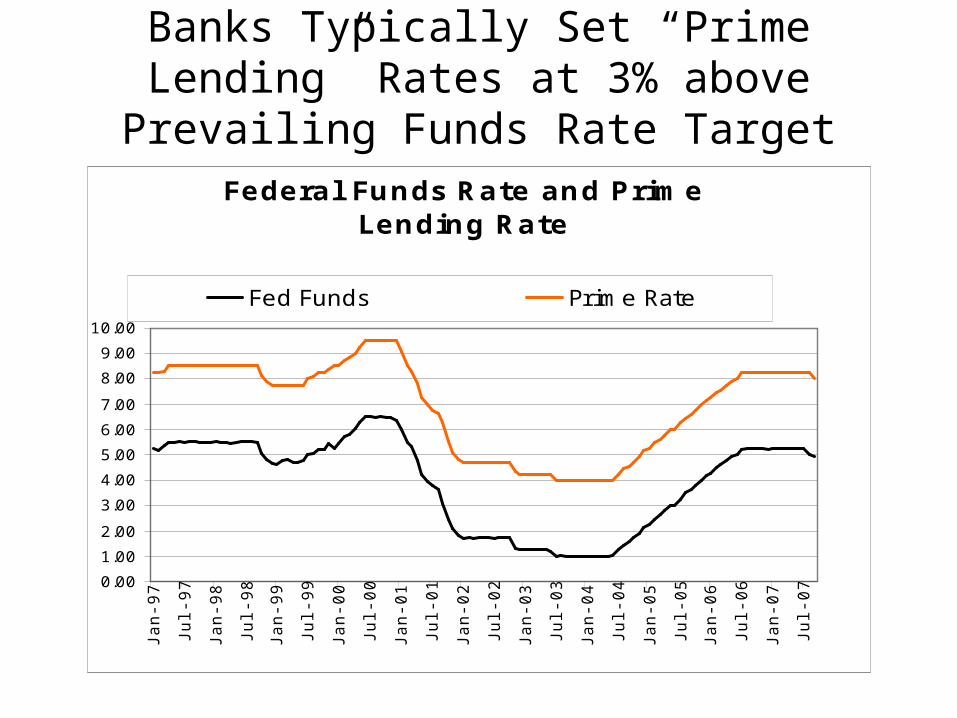

Banks Typically Set “Prime Lending” Rates at 3% above Prevailing Funds Rate Target

Federa l Funds Rat e and Prim e Lending Rat e

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jan-9

7

Jul-97

Jan-9

8

Jul-98

Jan-9

9

Jul-99

Jan-0

0

Jul-00

Jan-0

1

Jul-01

Jan-0

2

Jul-02

Jan-0

3

Jul-03

Jan-0

4

Jul-04

Jan-0

5

Jul-05

Jan-0

6

Jul-06

Jan-0

7

Jul-07

Fed Funds Prime Rate

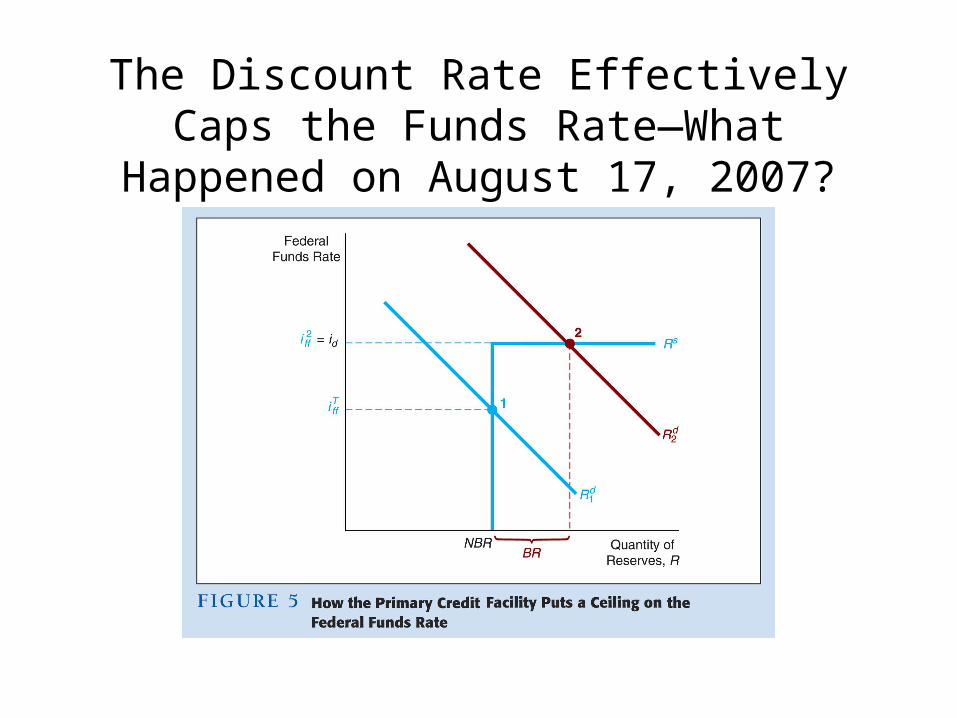

The Discount Rate Effectively Caps the Funds Rate—What Happened on August 17, 2007?

How Does the Fed Funds Rate Target Impact on Longer-Term Interest Rates?

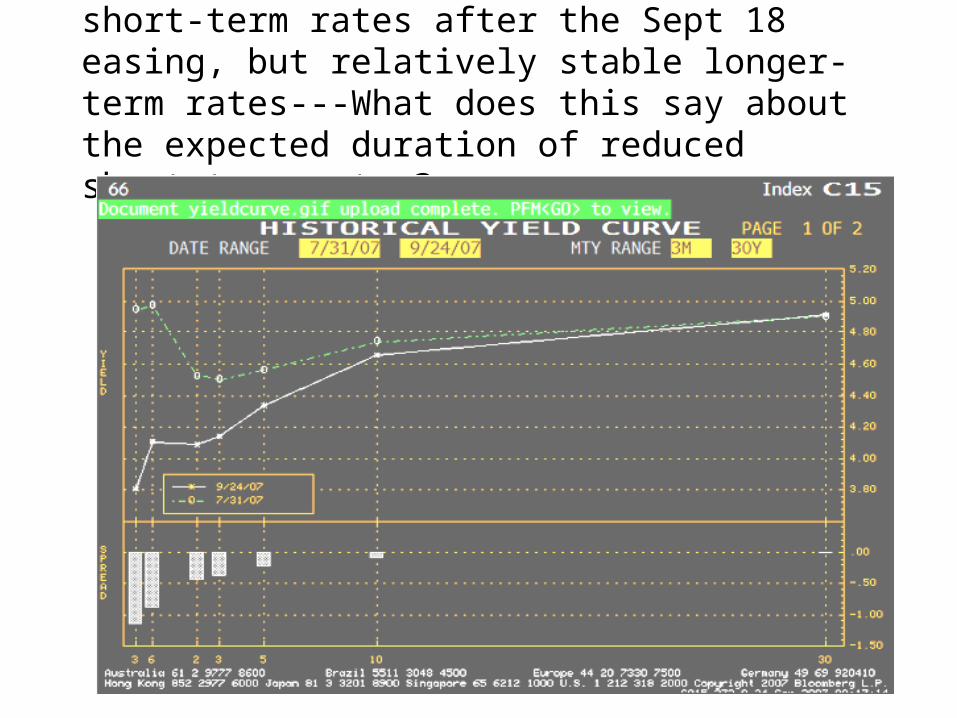

• The Expectations Theory of the Yield Curve--The interest rate on a long-term bond will equal an average of the short-term interest rates that people expect to occur over the life of the long-term bond

Expectations Theory—Note the drop in short-term rates after the Sept 18 easing, but relatively stable longer-term rates---What does this say about the expected duration of reduced short-term rates?

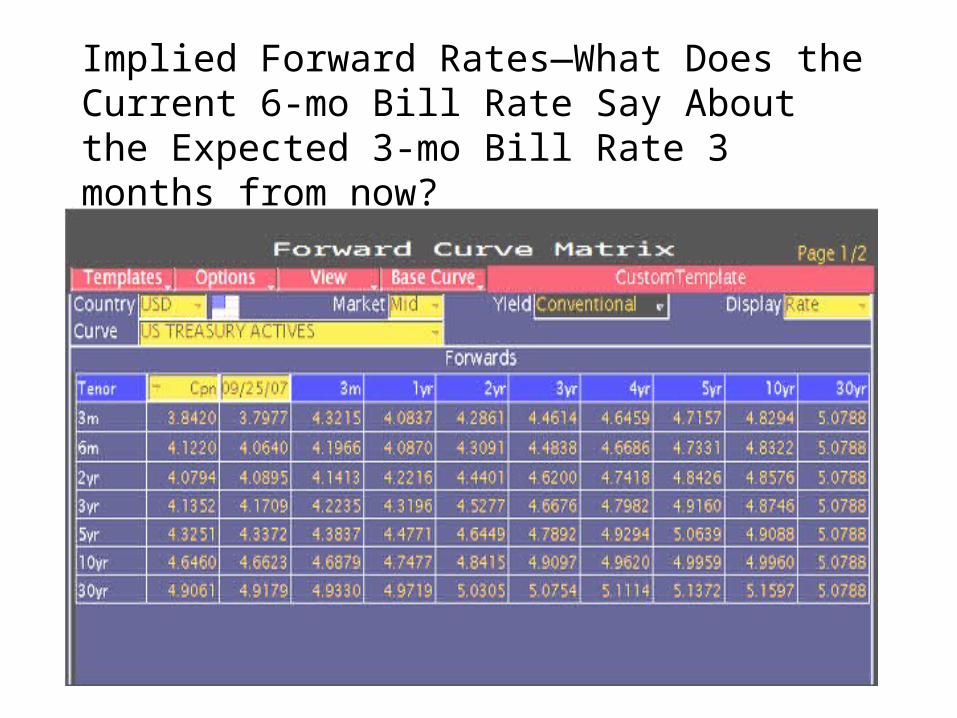

Implied Forward Rates—What Does the Current 6-mo Bill Rate Say About the Expected 3-mo Bill Rate 3 months from now?

Fed Transparency and the Expectations Theory of the Yield Curve

• A transparent Fed renders a zero recognition lag. After each FOMC meeting a statement is issued announcing the Fed Funds Target

• A transparent Fed, wherein the goals are clearly delineated, and wherein some forward looking guidance to future policy is provided, renders a more timely adjustment of long-term rates.

• A transparent Fed, via the Expectations Theory of the Yield Curve, improves the efficiency of monetary policy

The Federal Funds Rate and its impact on other short-term interest rates influences the following:• Adjustable Rate Mortgage (ARM) rates, and the

affordability of homeownership

• The cost of other big ticket purchases wherein the financing costs may be driven by Commercial Paper rates. Example: factory auto financing incentives

• Business borrowing, especially for things such as inventory management

• The foreign exchange value of the dollar and the demand for US exports, and US demand for imported goods—the Trade Balance

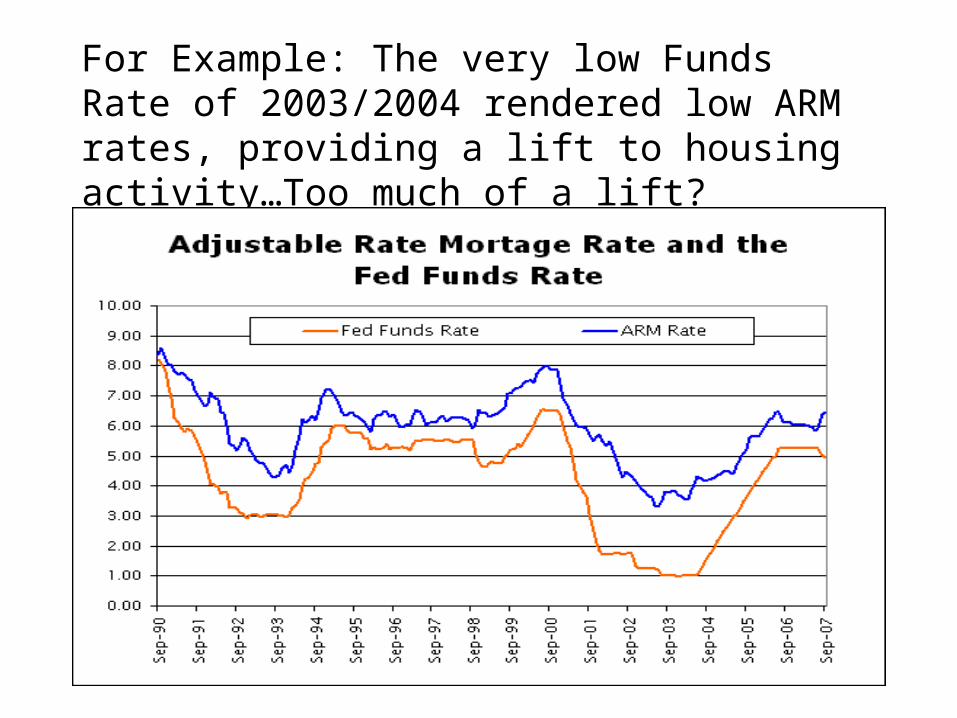

For Example: The very low Funds Rate of 2003/2004 rendered low ARM rates, providing a lift to housing activity…Too much of a lift?

The Fed’s influence on long-term interest rates via the Expectations Theory of the Yield Curve influences the following:

• Fixed Rate Mortgage Rates and the affordability of homeownership

• Corporate Bond Yields and ultimately Capital Spending

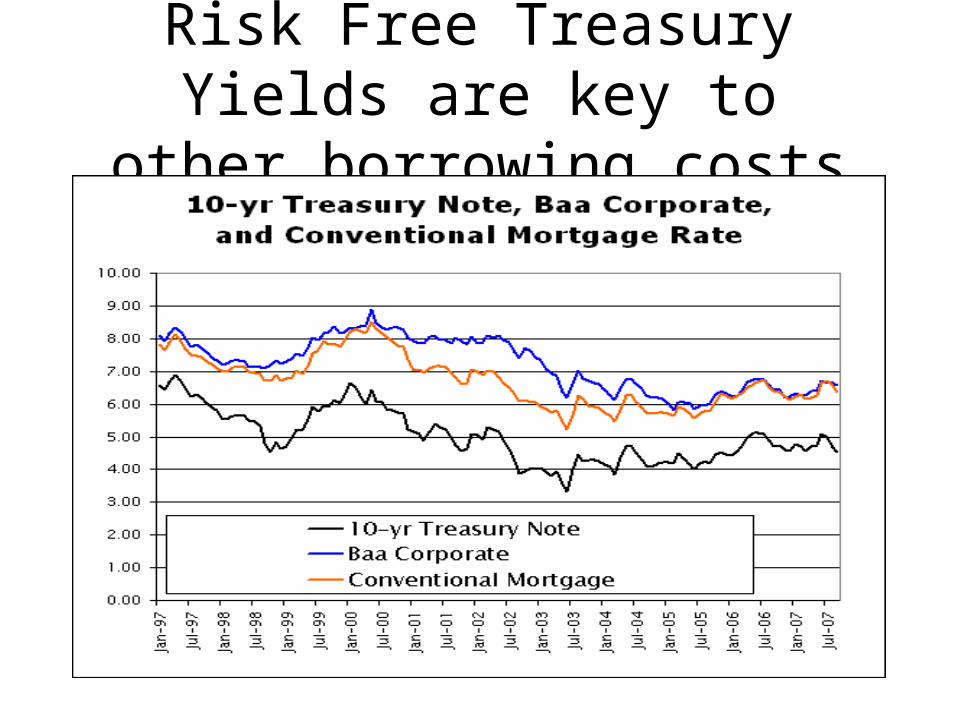

Risk Free Treasury Yields are key to other borrowing costs

Interest Rates influence Asset Prices or “Wealth” and ultimately influence household spending• Lower mortgage rates tend to spur home

purchases and provide a lift to home prices• Lower business borrowing costs improve

corporate profitability thereby giving a lift to “equity valuations”

• Lower interest rates render lower discount rates in the present value of future cash flows equation, resulting in both higher stock and bond prices

• Might the level of interest rates contribute to “Asset Bubbles”?

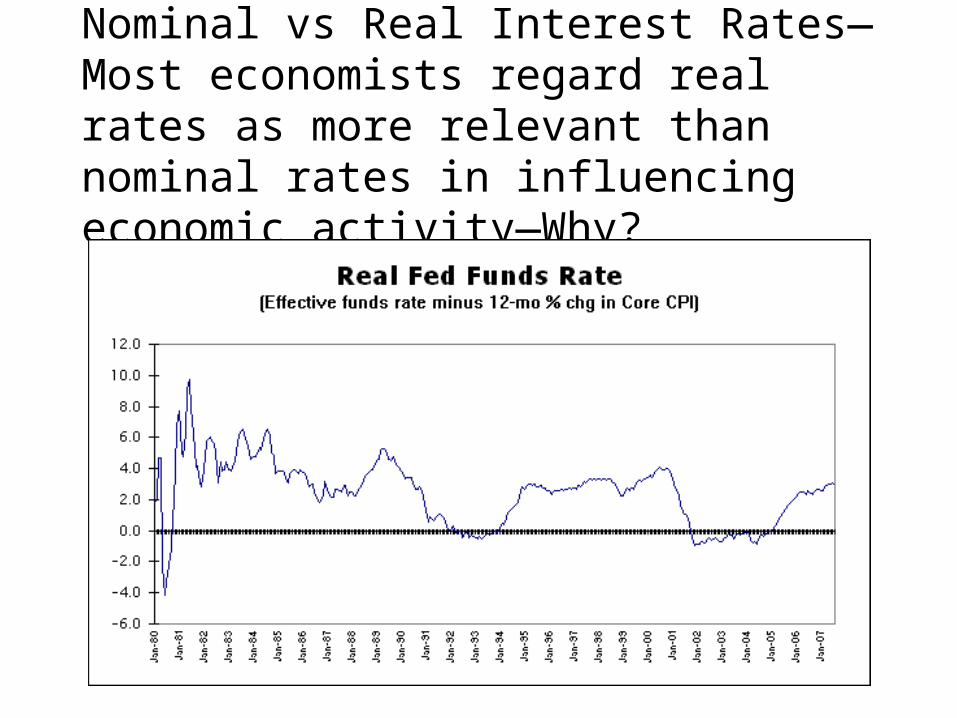

Nominal vs Real Interest Rates—Most economists regard real rates as more relevant than nominal rates in influencing economic activity—Why?

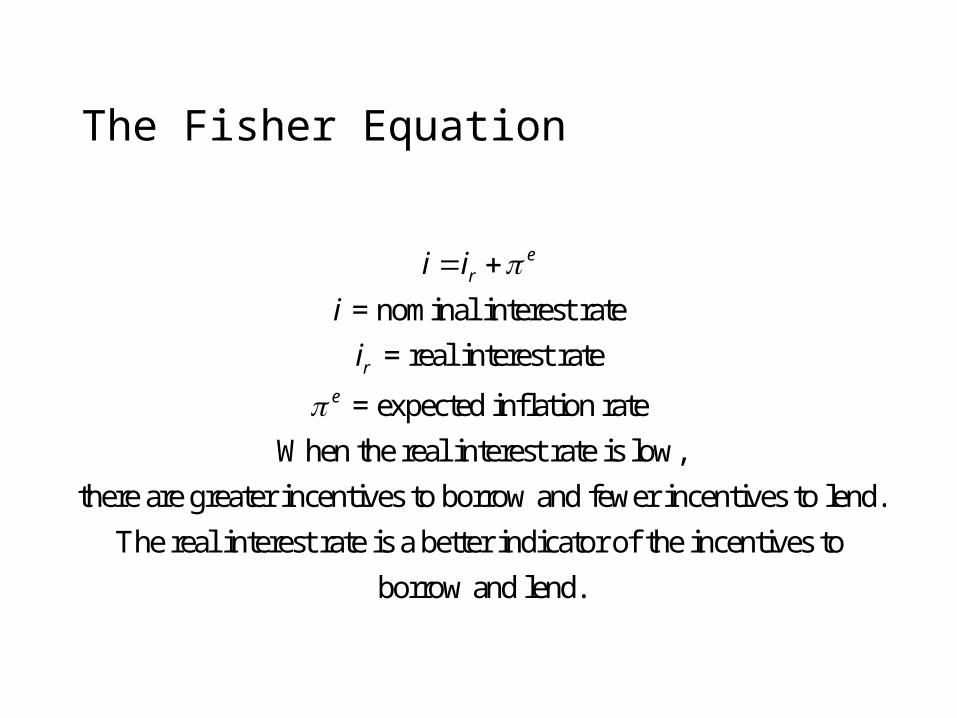

The Fisher Equation

= nominal interest rate

= real interest rate

= expected inflation rate

When the real interest rate is low,

there are greater incentives to borrow and fewer incentives to lend.

The real inter

er

r

e

i i

i

i

est rate is a better indicator of the incentives to

borrow and lend.

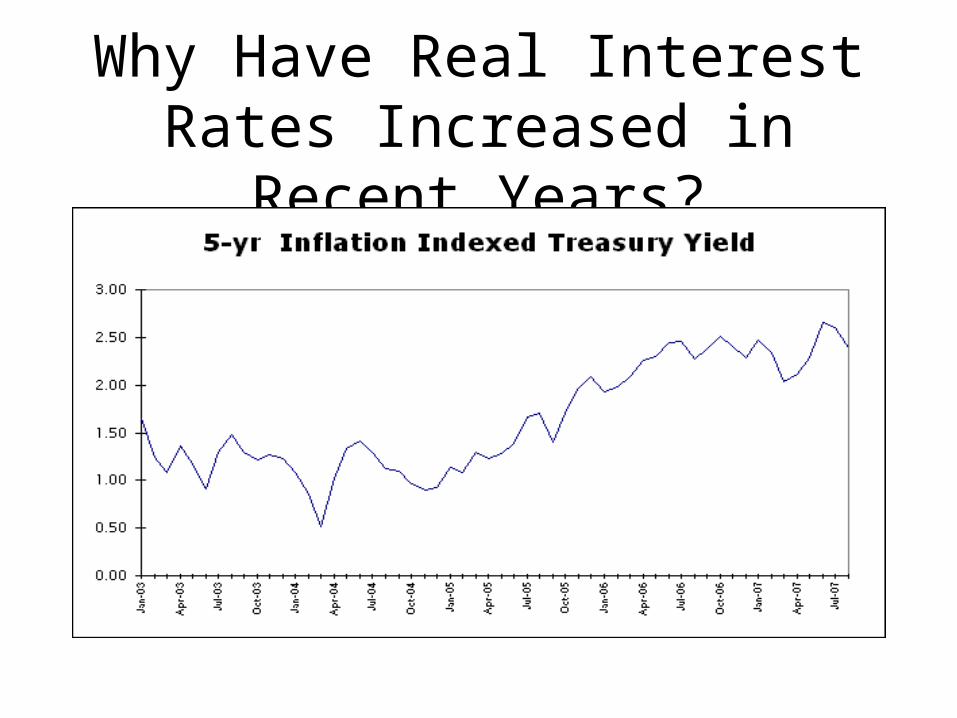

Why Have Real Interest Rates Increased in Recent Years?

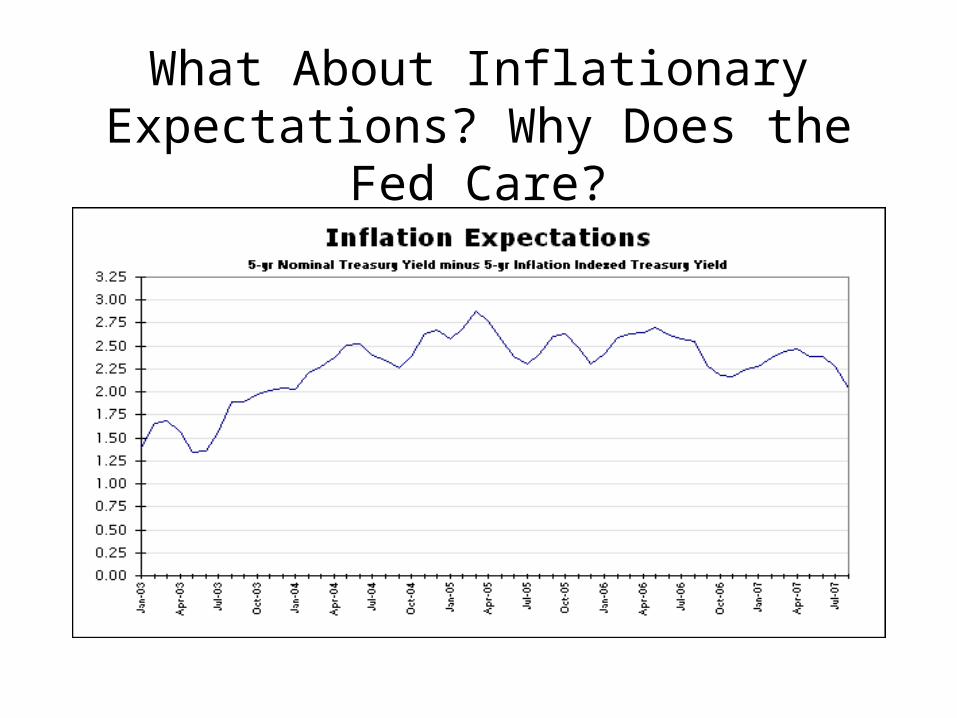

What About Inflationary Expectations? Why Does the Fed Care?

Related Topics—Significance of Inverted Yield Curve

• Was the inverted yield curve that prevailed in 2006 and into July 2007 a harbinger of recession?

• Some say maybe…see: The Yield Curve as a Leading Indicator, Arturo Estrella, (FRBNY Oct 2005) http://www.newyorkfed.org/research/capital_markets/ycfaq.html#Main

Others Were More Dismissive of the Inverted Curve

• Greenspan felt that long-term rates were held unusually low by a variety of special factors..He called this a “Conundrum”

• Bernanke felt that long-term rates were lower than otherwise due to the “Global Savings Glut”

Is the Fed Responsible for Fueling Speculative Excesses in Housing?

• John Taylor (Taylor Rule) feels that the Fed kept rates too low for too long. Had the Fed followed the Taylor Rule during the 2003/2005 the housing boom and burst would have been more contained.

• Both Greenspan and Bernanke regard the improbable but corrosive effects of the Deflationary risks in 2003 as justification for taking the funds rate down to 1%, and for keeping rates low for a “considerable period”.

• Greenspan and Bernanke note that long term rates failed to rise as the Fed began raising the funds target, and that this fostered stronger housing activity than otherwise.