alternate direction implicit method for a stochastic … ait...stochastic local volatility model...

TRANSCRIPT

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Alternate Direction Implicit Method for aStochastic Local Volatility Model:

High Performance Computing Platforms Comparison

Zaid AIT HADDOUManchester Business School

May 15, 2013HPCFinance conference

Tampere

1 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Outline

1 Stochastic Local Volatility ModelWhy a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

2 Alternate Direction Implicit Scheme: ADIWhat is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

3 ResultsVolatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

4 Conclusion

2 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Why a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

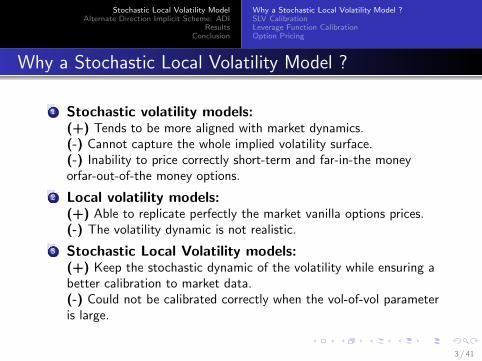

Why a Stochastic Local Volatility Model ?

1 Stochastic volatility models:(+) Tends to be more aligned with market dynamics.(-) Cannot capture the whole implied volatility surface.(-) Inability to price correctly short-term and far-in-the moneyorfar-out-of-the money options.

2 Local volatility models:(+) Able to replicate perfectly the market vanilla options prices.(-) The volatility dynamic is not realistic.

3 Stochastic Local Volatility models:(+) Keep the stochastic dynamic of the volatility while ensuring abetter calibration to market data.(-) Could not be calibrated correctly when the vol-of-vol parameteris large.

3 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Why a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

Why a Stochastic Local Volatility Model ?

1 SLV model:

SLV is a combination of a Local & Stochastic Volatility model

Implemented SLV

dSt = rStdt + L(St , t)√νtStdW

1t (1)

dνt = k(θ − νt) + ξ√νtdW

2t (2)

dW 1t .dW

2t = ρdt

L(St , t): is the leverage function and it represents theweight of local volatility in the model.

4 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Why a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

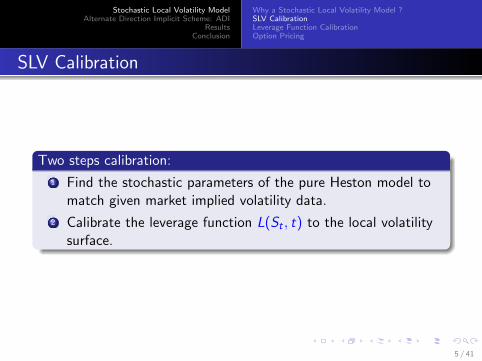

SLV Calibration

Two steps calibration:

1 Find the stochastic parameters of the pure Heston model tomatch given market implied volatility data.

2 Calibrate the leverage function L(St , t) to the local volatilitysurface.

5 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Why a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

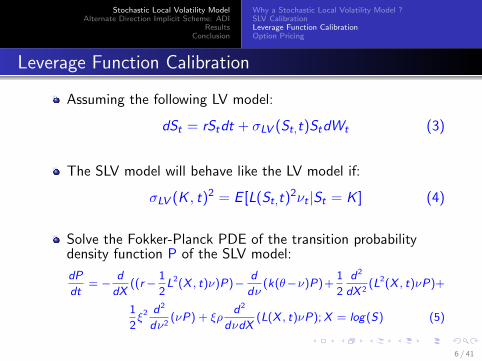

Leverage Function Calibration

Assuming the following LV model:

dSt = rStdt + σLV (St,t)StdWt (3)

The SLV model will behave like the LV model if:

σLV (K , t)2 = E [L(St,t)2νt |St = K ] (4)

Solve the Fokker-Planck PDE of the transition probabilitydensity function P of the SLV model:

dP

dt= − d

dX((r− 1

2L2(X , t)ν)P)− d

dν(k(θ−ν)P)+

1

2

d2

dX 2(L2(X , t)νP)+

1

2ξ2 d2

dν2(νP) + ξρ

d2

dνdX(L(X , t)νP);X = log(S) (5)

6 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Why a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

Leverage Function Calibration

Figure : Initial probability distribution for the forward Fokker-Planck PDE

7 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Why a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

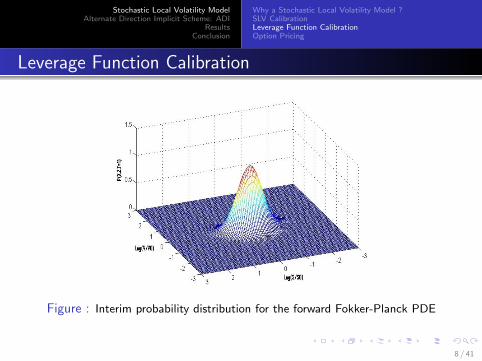

Leverage Function Calibration

Figure : Interim probability distribution for the forward Fokker-Planck PDE

8 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Why a Stochastic Local Volatility Model ?SLV CalibrationLeverage Function CalibrationOption Pricing

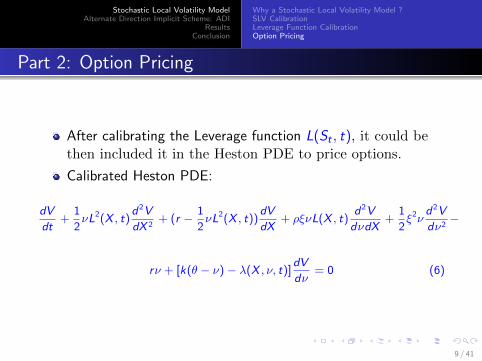

Part 2: Option Pricing

After calibrating the Leverage function L(St , t), it could bethen included it in the Heston PDE to price options.

Calibrated Heston PDE:

dV

dt+

1

2νL2(X , t)

d2V

dX 2+ (r − 1

2νL2(X , t))

dV

dX+ ρξνL(X , t)

d2V

dνdX+

1

2ξ2ν

d2V

dν2−

rν + [k(θ − ν) − λ(X , ν, t)]dV

dν= 0 (6)

9 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

What is ADI ?

ADI is a finite difference method used to solve PDEs in two ormore dimensions

Different type of ADI schemes: Peaceman-Rachford,Douglas-Rachford and Craig-sneyd, etc.

The advantage of the ADI method is that the equations thathave to be solved in each step have a simpler structure andcan be solved efficiently with a simple tridiagonal matrixalgorithm.

10 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

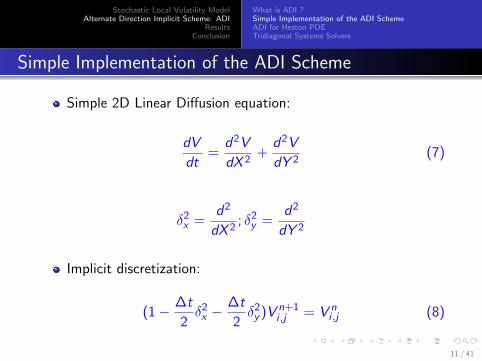

Simple Implementation of the ADI Scheme

Simple 2D Linear Diffusion equation:

dV

dt=

d2V

dX 2+

d2V

dY 2(7)

δ2x =

d2

dX 2; δ2

y =d2

dY 2

Implicit discretization:

(1− ∆t

2δ2x −

∆t

2δ2y )V n+1

i ,j = V ni ,j (8)

11 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

Simple Implementation of the ADI Scheme

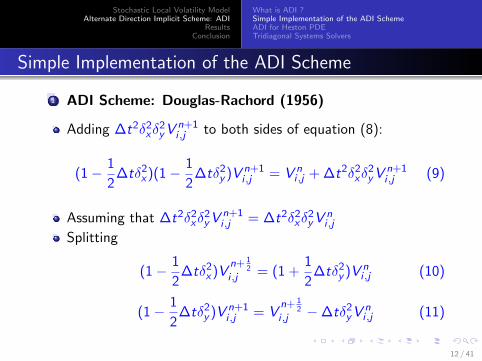

1 ADI Scheme: Douglas-Rachord (1956)

Adding ∆t2δ2xδ

2yV

n+1i ,j to both sides of equation (8):

(1− 1

2∆tδ2

x)(1− 1

2∆tδ2

y )V n+1i ,j = V n

i ,j + ∆t2δ2xδ

2yV

n+1i ,j (9)

Assuming that ∆t2δ2xδ

2yV

n+1i ,j = ∆t2δ2

xδ2yV

ni ,j

Splitting

(1− 1

2∆tδ2

x)Vn+ 1

2i ,j = (1 +

1

2∆tδ2

y )V ni ,j (10)

(1− 1

2∆tδ2

y )V n+1i ,j = V

n+ 12

i ,j −∆tδ2yV

ni ,j (11)

12 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

ADI for Heston PDE

Using Crank Nicolson discretization instead of its implicitcounterpart.

Following the same logic explained in the previous example:

(1− 1

2∆tA1)V

n+ 12

i ,j = (1 + A0 +1

2∆tA1 +

1

2∆tA2)V n

i ,j (12)

(1− 1

2∆tA2)V n+1

i ,j = Vn+ 1

2i ,j − 1

2∆tA2V

ni .j (13)

We deal with the mixed derivative term A0 only explicitly.

13 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

Simple Implementation of the ADI Scheme

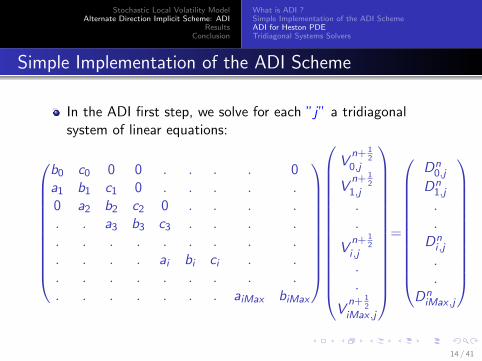

In the ADI first step, we solve for each ”j” a tridiagonalsystem of linear equations:

b0 c0 0 0 . . . . 0a1 b1 c1 0 . . . . .0 a2 b2 c2 0 . . . .. . a3 b3 c3 . . . .. . . . . . . . .. . . . ai bi ci . .. . . . . . . . .. . . . . . . aiMax biMax

Vn+ 1

20,j

Vn+ 1

21,j

.

.

Vn+ 1

2i ,j

.

.

Vn+ 1

2iMax ,j

=

Dn0,j

Dn1,j

.

.Dni ,j

.

.DniMax ,j

14 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

Simple Implementation of the ADI Scheme

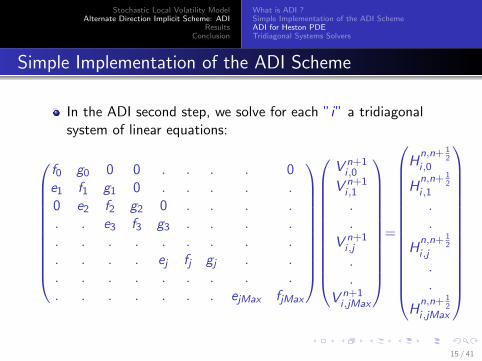

In the ADI second step, we solve for each ”i” a tridiagonalsystem of linear equations:

f0 g0 0 0 . . . . 0e1 f1 g1 0 . . . . .0 e2 f2 g2 0 . . . .. . e3 f3 g3 . . . .. . . . . . . . .. . . . ej fj gj . .. . . . . . . . .. . . . . . . ejMax fjMax

V n+1i ,0

V n+1i ,1

.

.

V n+1i ,j

.

.

V n+1i ,jMax

=

Hn,n+ 1

2i ,0

Hn,n+ 1

2i ,1

.

.

Hn,n+ 1

2i ,j

.

.

Hn,n+ 1

2i ,jMax

15 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

Thomas algorithm

1 Thomas algorithm:

Forward elimination:

c′i =

cibi

; i = 1

ci

bi − c′i−1ai

; i = 2, 3, ..., n − 1(14)

d′i =

dibi

; i = 1

di − d′i−1ai

bi − c′i−1ai

; i = 2, 3, ..., n − 1(15)

16 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

Thomas algorithm

1 Thomas algorithm:

Backward substitution:

Vn = d

′n

Vi = d′i − c

′iVi+1

(16)

1 Characteristics:

Complexity O(N).The fastest serial algorithm.

17 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

Cyclic reduction

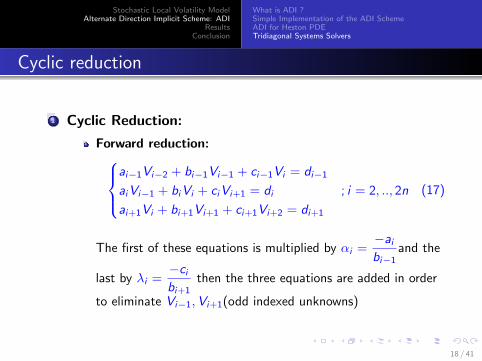

1 Cyclic Reduction:

Forward reduction:ai−1Vi−2 + bi−1Vi−1 + ci−1Vi = di−1

aiVi−1 + biVi + ciVi+1 = di ; i = 2, .., 2n

ai+1Vi + bi+1Vi+1 + ci+1Vi+2 = di+1

(17)

The first of these equations is multiplied by αi =−aibi−1

and the

last by λi =−cibi+1

then the three equations are added in order

to eliminate Vi−1,Vi+1(odd indexed unknowns)

18 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

Cyclic reduction

1 Cyclic Reduction:

Forward reduction:

a(1)i Vi−2 + b

(1)i Vi + c

(1)i Vi+2 = y

(1)i ; i = 2, .., 2n (18)

Backward substitution:We use the even-indexed unknowns found through the forwardreduction in order to solve all odd-indexed unknowns.

2 Characteristics:

Complexity O(N)Each step of the CR algorithm could be parallelized.

19 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

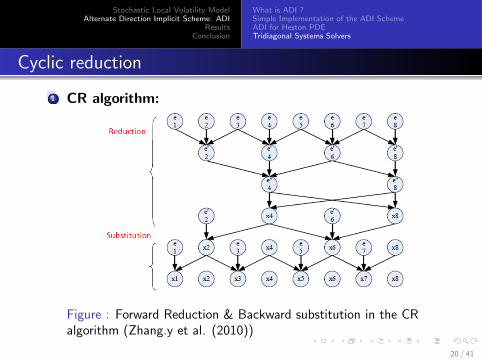

Cyclic reduction

1 CR algorithm:

Figure : Forward Reduction & Backward substitution in the CRalgorithm (Zhang.y et al. (2010))

20 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

What is ADI ?Simple Implementation of the ADI SchemeADI for Heston PDETridiagonal Systems Solvers

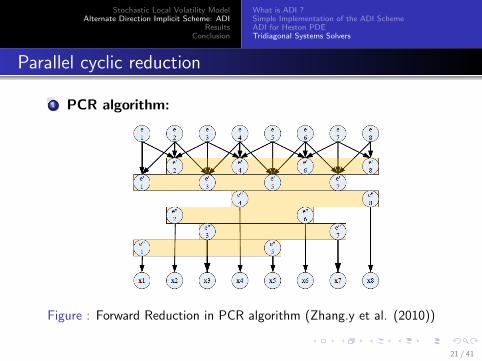

Parallel cyclic reduction

1 PCR algorithm:

Figure : Forward Reduction in PCR algorithm (Zhang.y et al. (2010))

21 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

Market Implied Volatility Surface

Figure : Implied Volatility Surface

22 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

Volatility curves (T=0.5 year)

Figure : Market volatility, Heston implied volatility and Local volatilitycurves for T=0.5

23 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

Leverage function surface

Figure : Leverage function surface

24 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

Call options pricing error

V0 ξ k θ S0 ρ r T

0.0713 0.4 1 0.2 120 0.3874 0.02 0.5

Table : Heston Parameters

Strike LV Heston SLV market price

180 0.0338 0.1532 0.0383 1.0665

100 0.0013 0.1648 0.0183 23.3577

Table : Pricing error according to different models

25 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

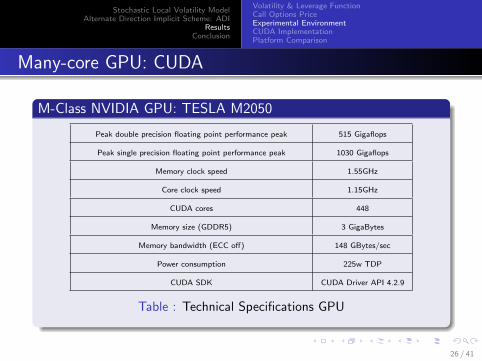

Many-core GPU: CUDA

M-Class NVIDIA GPU: TESLA M2050

Peak double precision floating point performance peak 515 Gigaflops

Peak single precision floating point performance peak 1030 Gigaflops

Memory clock speed 1.55GHz

Core clock speed 1.15GHz

CUDA cores 448

Memory size (GDDR5) 3 GigaBytes

Memory bandwidth (ECC off) 148 GBytes/sec

Power consumption 225w TDP

CUDA SDK CUDA Driver API 4.2.9

Table : Technical Specifications GPU

26 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

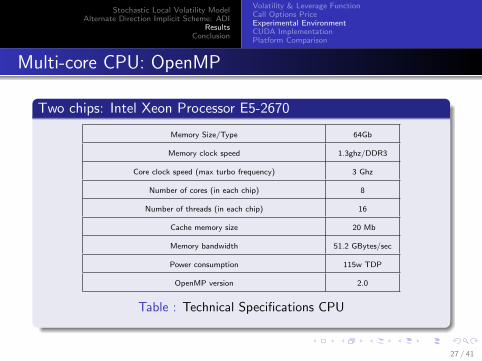

Multi-core CPU: OpenMP

Two chips: Intel Xeon Processor E5-2670

Memory Size/Type 64Gb

Memory clock speed 1.3ghz/DDR3

Core clock speed (max turbo frequency) 3 Ghz

Number of cores (in each chip) 8

Number of threads (in each chip) 16

Cache memory size 20 Mb

Memory bandwidth 51.2 GBytes/sec

Power consumption 115w TDP

OpenMP version 2.0

Table : Technical Specifications CPU

27 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

GPU implementation: Method 1

1 First method on GPU: Thomas-CUDA

All data arrays are stored linearly on the GPU global memory.Two kernels (each kernel solve one ADI step)Each thread build and solve one tridiagonal system usingThomas algorithm.The Transfer of the results from the GPU to the CPU happensonce after completing the time iterations.

2 Charasteristics:

Very easy to implement.Global memory is slow.For 2D ADI most GPU cores are idle.

28 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

GPU implementation: Method 2

1 Second method on GPU: PCR-CUDA

The lower, main and upper diagonals of the tridiagonal systemare all stored linearly in the GPU shared memory.Two kernels (each kernel solve one ADI step)Each tridiagonal system is solved and built by all the blockthreads using the PCR algorithm.The transfer of the results from the GPU to the CPU happensonce after completing the time iterations.

2 Charasteristics:

Harder to implement.Shared memory is fast.For 2D ADI, quite good use of GPU cores.

29 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

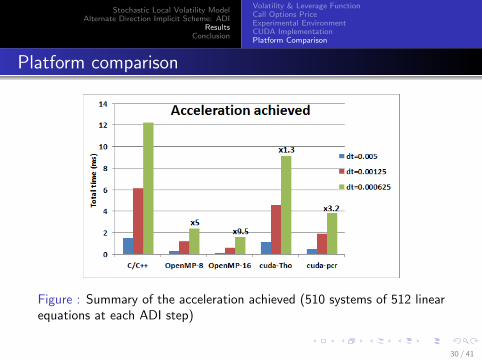

Platform comparison

Figure : Summary of the acceleration achieved (510 systems of 512 linearequations at each ADI step)

30 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

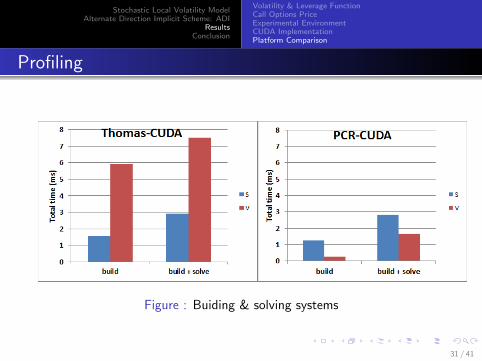

Profiling

Figure : Buiding & solving systems

31 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

Profiling

1 First Method: Thomas-CUDA

Poor performance in the V direction due to uncoalescedglobal memory access.

2 Second method: PCR-CUDA

Poor performance in the S direction due to uncoalescedglobal memory access.

32 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

Global memory access

coalesced global memory access:

Figure : Coalesced memory access

Uncoalesced global memory access:

Figure : Uncoalesced memory access

33 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

Profiling: Memory Optimization

Figure : Building systems optimization

34 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Volatility & Leverage FunctionCall Options PriceExperimental EnvironmentCUDA ImplementationPlatform Comparison

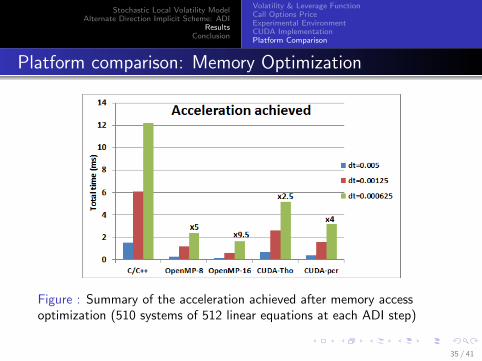

Platform comparison: Memory Optimization

Figure : Summary of the acceleration achieved after memory accessoptimization (510 systems of 512 linear equations at each ADI step)

35 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Conclusion

SLV models could be a good alternative for SV and LV models.

Calibration is not stable for large vol-of-vol

There are several sources that lead to inaccurate pricing in theSLV model using ADI:

Choice of the boundary conditionsApproximating the leverage function while solving the forwardKolmogorov PDE with ADI.

36 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Conclusion

Of course ! the GPU codes could still be optimized.

Coalesced global memory access is very important foroptimization.

GPU become much more competitive as we increase thedensity of the grids.

CUDA code requires a reasonable programming effort tooptimize performance !

OpenMP is very easy to implement !

37 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Questions ?

Thank you for your attention

38 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

References

“Tridiagonal solvers on the GPU and applications to fluid simulation”Nikolai Sakharnykh, GTC 2009

“Fast tridiagonal solvers on the GPU” Y. Zhang, J. Cohen, J.D. Owens,PPoPP 2010

“High performance finite difference PDE solvers on GPUs.” D. Egloff,http://download.quantalea.net/fdm gpu.pdf, Feb. 2010

“Foreign exchange option pricing: A Practitioner’s guide”,IAIN J. Clark,Wiley finance. 2010

“Calibrating and Pricing with Stochastic-Local Volatility Model” Tian. Y,Z. Zili, K. Fima, H. Kais

“On the Numerical solution of heat conduction problems in two and threespace variables”,J. Douglas, JR., H. H. Rachford, JR.

39 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Acknowledgement

Zaid ait Haddou is a Marie Curie fellow at the University ofManchester. The research leading to these results has receivedfunding from the European Community’s Seventh FrameworkProgramme FP7-PEOPLE-ITN-2008 under grant agreement numberPITN-GA-2009-237984.I would like to thank NAG, advice and technical support, and ChrisArmstrong and Jacques Du Toit (both from NAG) for povidingcodes and for many helpful comments and suggestions.My deepest gratitude goes also to my supervisor Prof. Ser-HuangPoon, in Manchester Business School, for her precious help andunderstanding during the whole project.Furthermore, I would like to acknowledge with much appreciationthe help provided by Mr. Erik Vynkier and also for having me onemonth in SWIP office in Edinburgh.I would like to also thank Mr. Daniel egloff for his technical helpand for providing the PCR solver CUDA code.

40 / 41

Stochastic Local Volatility ModelAlternate Direction Implicit Scheme: ADI

ResultsConclusion

Appendix

ADI for Heston PDE:

A0 corresponds to the mixed derivative term, A1 the spatialderivatives in S direction and A2 the spatial derivatives in Vdirection.

A0 =1

2∆tρσVjSiδsv (19)

A1 =1

2∆t[VjS

2i δss + rSδs − r ] (20)

A2 =1

2∆t[σVjδvv + [k(θ − Vj)− λ(Si ,Vj , t)]δv − r ] (21)

41 / 41