alternative data integration, analysis and investment …com.estimize.public.s3.amazonaws.com/l2q...

TRANSCRIPT

YinLuo,CFAViceChairmanQuantitativeResearch,Economics,andPortfolioStrategy

QESDeskPhone:1.646.582.9230Luo.QES@wolferesearch.comAlternativeDataIntegration,

AnalysisandInvestmentResearch

L2QConference

DONOTFORWARD– DONOTDISTRIBUTE– DOCUMENTCANONLYBEPRINTEDTWICEThisreportislimitedsolelyfortheuseofclientsofWolfeResearch.PleaserefertotheDISCLOSURESECTIONlocatedattheendofthisreportforAnalystCertificationsandOtherDisclosures.ForImportantDisclosures,pleasegotowww.WolfeResearch.com/DisclosuresorwritetousatWolfeResearch,LLC,420LexingtonAvenue,Suite648,NewYork,NY10170

June20,2017

2

Agenda

Table ofContents

1.IntroducingLuo’sQESResearch

2.CrowdsourcingRevenueandEarningsEstimates

3.TextMiningUnstructuredCorporateFilingData

• TopRankedQuantitativeandMacroResearchTeam.Theteamhasbeenranked#1intheInstitutionalInvestor’sII-AllAmerica,II-Europe,andII-AsiasurveysintheQuantitativeResearchsector,andtoprankedinthePortfolioStrategyandAccounting&TaxPolicycategories.

• BigDataandMachineLearning.WefullyincorporateBigData(e.g.,textmining,newssentiment,satelliteimagery,securitieslending,crowdingsourcing)andmachinelearninginourresearch,asreflectedinourLEAPglobalstockselectionmodel.

• SystematicGlobalMacroResearch.OurresearchonNowcastingeconomicgrowthin>40countries/regionshasreceivedtremendousfeedbackfromclients.Stylerotationandfactortimingisacorecomponentofourglobalstockselectionmodels.Alternativedatasources(e.g.,newssentiment,real-timehiring,satelliteimagery,Googletrends)arealsofullyintegratedinourmacroresearch.

• UsefulToolsforFundamentalManagers.Inadditiontoresearch,wealsoprovideasuiteofusefultools,includingonlinescreeningandfactorperformancetracking,industry-specificmodeling,positionsizingandportfolioconstruction,andportfolioanalyticstodiscretionarymanagers.

• [email protected],ifyouareinterestedinourresearchandservices.

3

1.IntroducingLuo’sQESResearch

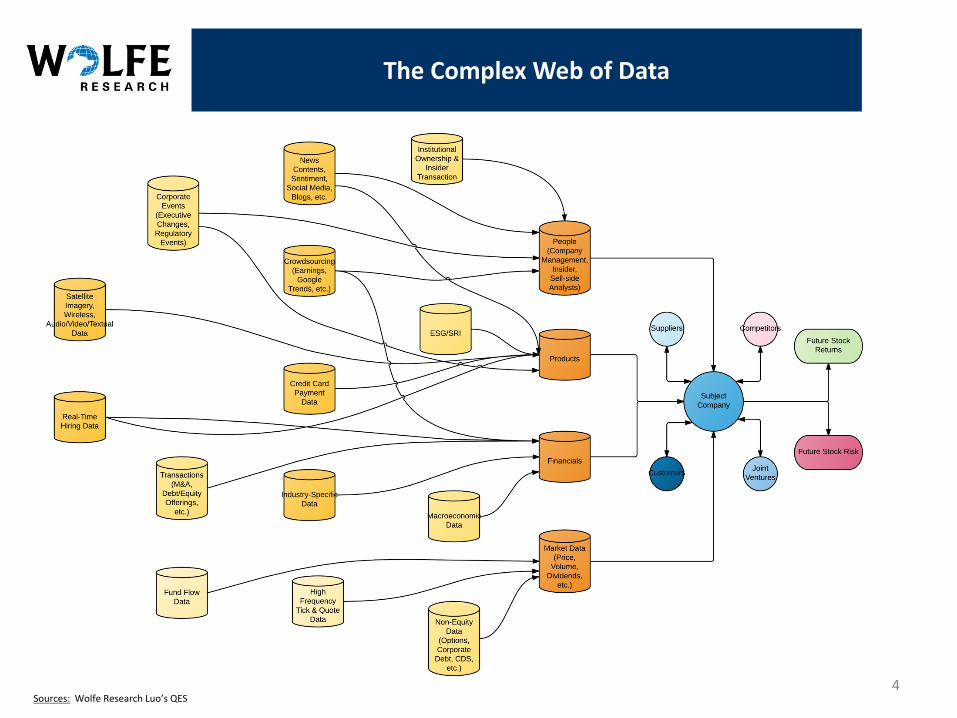

4Sources: WolfeResearchLuo’sQES

TheComplexWebofData

• AlternativeBigDataonEarningsandRevenueEstimate.Inthisresearch,westudyanalternativedatasourcebasedontheconceptofcrowdsourcing.Estimizeisanonlineplatformthatallowsindividualswithdifferentbackgroundtocontributetheirfinancialforecast.WefindEstimizeestimatestobenotonlymoreaccurateandtimelierthanthesell-side,butalsohighlycomplementarytotraditionalfactors.

• EstimizeFESModel.DivingintodetailedEstimizeestimates,wefindthataccuracycanbefurtherimprovedalongthreedimensions:thefreshnessoftheestimates,analystexperience,andanalystskill.WethenintroduceasmartEstimizeconsensuscalledFES(Freshness,Experience,andSkill).

• SmartStrategiesaroundEarningsAnnouncement.WeexplorethreedifferenttypeoftradingstrategiesaroundearningsreleasesusingtheEstimizedata.Thepre-earningsannouncementstrategybuysstocksbasedonearningsrevisionsintheweekbeforetheearningsreportingdate.PEAD(PostEarningAnnouncementDrift)strategyattemptstocapturethedriftalphaimmediatelyaftertheearningsannouncement,basedonearningssurprise.Lastly,weproposealowrisklong-onlystrategybyavoidingearningsriskandearningsuncertainty.

• EnhancedValueStrategies.Manyfundamentalandquantitativestrategiesexplicitlyorimplicitlyrelyonearningsandrevenueestimates.Forlong-termvalueinvestors,weshowhowEstimizedataandourFESmodelcanbeusedtoboostperformance.Intheend,wealsooverlayourenhancedvaluestrategywithalowrisktilt(byavoidingearningsuncertainty)tofurtherimprovereturnandreducerisk.

5

2.CrowdsourcingEarningsandRevenueEstimates

6Sources: Estimize,WolfeResearchLuo’sQES

a)TheBasicsofCrowdsourcing

ContributorstotheEstimizedatabase

OtherIndependent ResearchOtherAsset ManagerHedge FundVenture CapitalProprietary Trading FirmMutual FundFund of FundsPrivate EquityPension FundEndowment FundOtherBrokerFinancial AdvisorInvestment BankWealth ManagerInsurance FirmAcademiaStudentHealth CareInformation TechnologyFinancialsIndustrialsMaterialsConsumer StaplesConsumer DiscretionaryEnergyUtilitiesTelecommunication Services

Non Professional

Financial ProfessionalBuy Side

Sell Side

Independent

BreakdownofEstimizedata

Breakdownoffinanceprofessional

30%

25%

45%

Independent BuySide SellSide

46%

54%

FinanceProfessionals Non-professionals

• Earningsandrevenueestimatesareprobablythemostimportantdriversofstockreturnsandrisks.Unlikeconventionalsell-sideconsensus,Estimizecrowdsourcesestimatesfromawiderangeofcontributors.

7Sources: Estimize,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

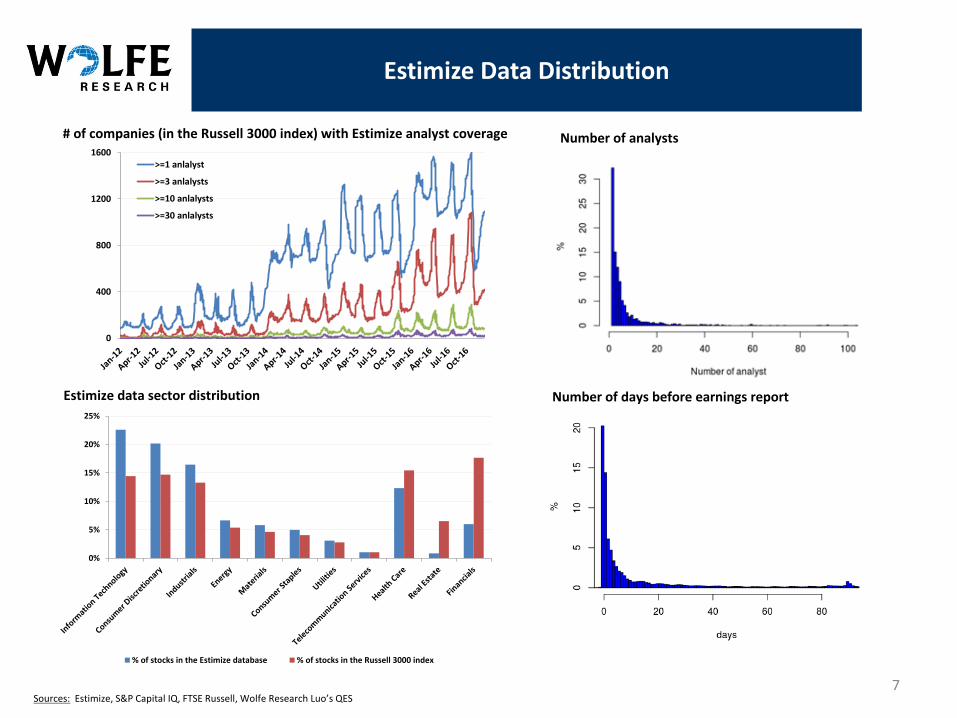

EstimizeDataDistribution

#ofcompanies(intheRussell3000index)withEstimizeanalystcoverage

Estimizedatasectordistribution

Numberofanalysts

0%

5%

10%

15%

20%

25%

%ofstocksintheEstimizedatabase %ofstocksintheRussell3000index

Numberofdaysbeforeearningsreport

0

400

800

1200

1600>=1anlalyst

>=3anlalysts

>=10anlalysts

>=30anlalysts

8Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

b)TheAccuracyofCrowdsourcedEstimates

EPSestimateaccuracy

EstimizeEPSaccuracybysector

Revenueestimateaccuracy

Estimizeaccuracy,domesticversusmultinationalfirms

0%

50%

100%

Sellsidemoreaccurate Estimizemoreaccurate

40.9% 39.4% 39.2% 38.6%

59.1% 60.6% 60.8% 61.4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

<10%exUS >10%exUS >20%exUS >50%exUS

Sellsidemoreaccurate Estimizemoreaccurate

43% 41% 40% 38% 36%

57% 59% 60% 62% 64%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

>=1analyst >=3analysts >=5analysts >=10analysts >=30analysts

Sell-sidemoreaccurate Estimizemoreaccurate

52% 51% 50% 49% 49%

48% 49% 50% 51% 51%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

>=1analyst >=3analysts >=5analysts >=10analysts >=30analysts

Sell-sidemoreaccurate Estimizemoreaccurate

9Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

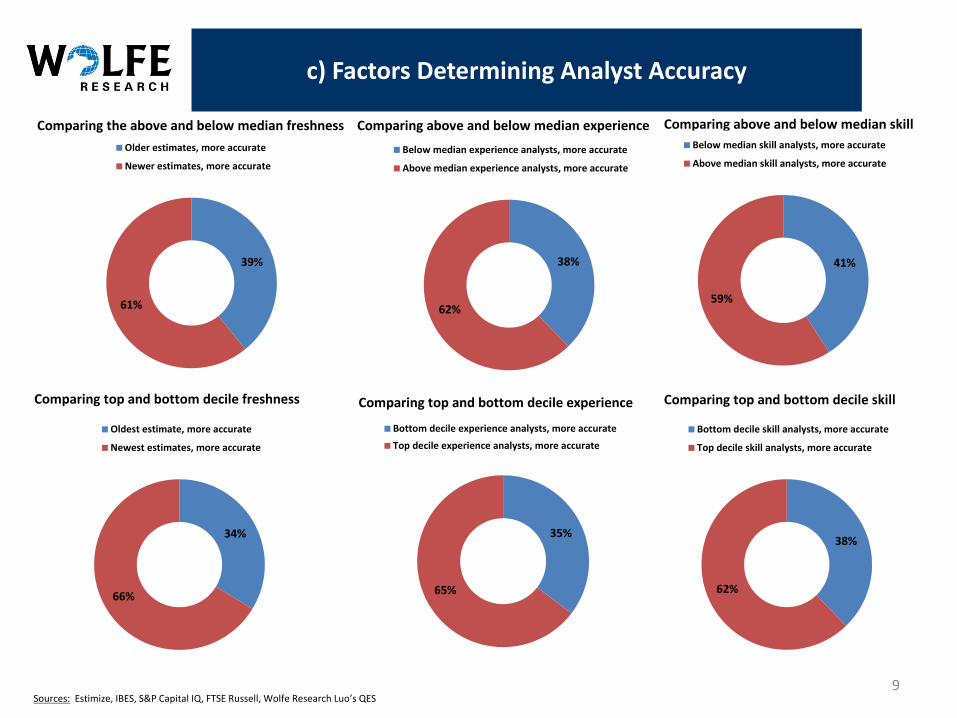

c)FactorsDeterminingAnalystAccuracy

Comparingtheaboveandbelowmedianfreshness

Comparingtopandbottomdecile freshness

Comparingaboveandbelowmedianexperience

Comparingtopandbottomdecile experience

Comparingaboveandbelowmedianskill

Comparingtopandbottomdecile skill

39%

61%

Olderestimates,moreaccurate

Newerestimates,moreaccurate

34%

66%

Oldestestimate,moreaccurate

Newestestimates,moreaccurate

38%

62%

Belowmedianexperienceanalysts,moreaccurate

Abovemedianexperienceanalysts,moreaccurate

35%

65%

Bottomdecileexperienceanalysts,moreaccurateTopdecileexperienceanalysts,moreaccurate

41%

59%

Belowmedianskillanalysts,moreaccurate

Abovemedianskillanalysts,moreaccurate

38%

62%

Bottomdecileskillanalysts,moreaccurate

Topdecileskillanalysts,moreaccurate

10Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

EstimizeFES(Freshness,Experience,andSkill)Model

Weightingtheestimatebythefreshness,analystexperience,andanalystskill

EstimizeFEDmodelversussingleweightingscheme

46%54%

Equalweight,moreaccurate

Weightedbyfreshness,moreaccurate

47%53%

Equalweight,moreaccurate

Weightedbyexperience,moreaccurate

47%53%

Equalweight,moreaccurate

Weightedbyskill,moreaccurate

52%48%

FESmodel,moreaccurate

Weightedbyfreshness,moreaccurate

54%46%

FESmodel,moreaccurate

Weightedbyexperience,moreaccurate

55%45%

FESmodel,moreaccurate

Weightedbyskill,moreaccurate

11Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

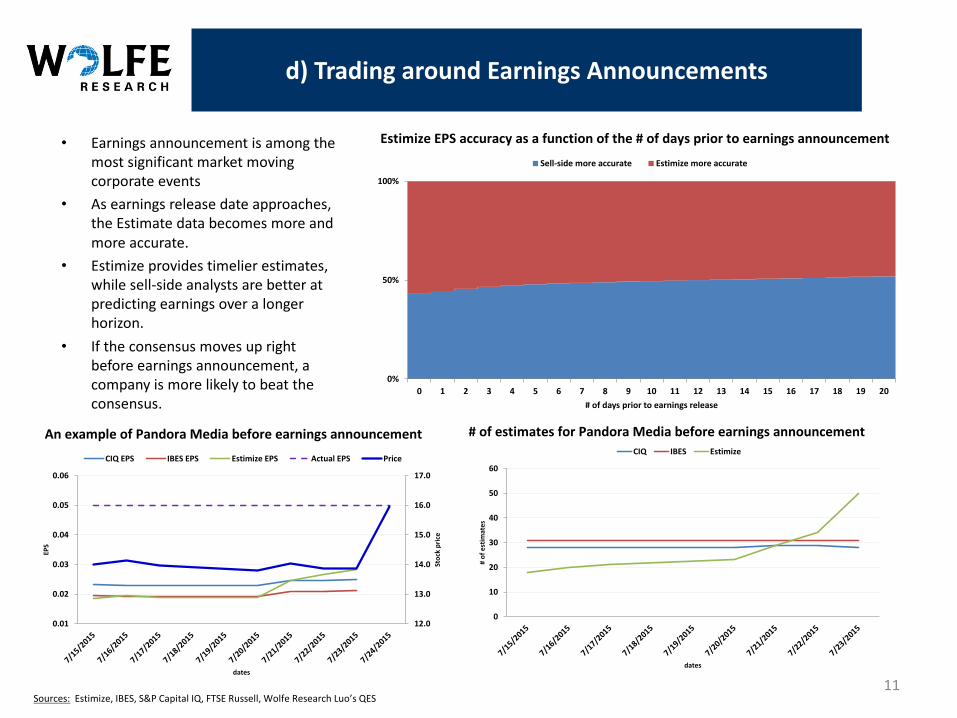

d)TradingaroundEarningsAnnouncements

EstimizeEPSaccuracyasafunctionofthe#ofdayspriortoearningsannouncement

AnexampleofPandoraMediabeforeearningsannouncement

0%

50%

100%

0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20#ofdayspriortoearningsrelease

Sell-sidemoreaccurate Estimizemoreaccurate

#ofestimatesforPandoraMediabeforeearningsannouncement

12.0

13.0

14.0

15.0

16.0

17.0

0.01

0.02

0.03

0.04

0.05

0.06

Stockprice

EPS

dates

CIQEPS IBESEPS EstimizeEPS ActualEPS Price

0

10

20

30

40

50

60#ofestim

ates

dates

CIQ IBES Estimize

• Earningsannouncementisamongthemostsignificantmarketmovingcorporateevents

• Asearningsreleasedateapproaches,theEstimatedatabecomesmoreandmoreaccurate.

• Estimizeprovidestimelierestimates,whilesell-sideanalystsarebetteratpredictingearningsoveralongerhorizon.

• Iftheconsensusmovesuprightbeforeearningsannouncement,acompanyismorelikelytobeattheconsensus.

12Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

Earningsrevisionspriortotheannouncementdateleadsannouncementdayreturn

PercentageofEPSchangesintheweekbeforeearningsannouncement

Averageexcessearningannouncementdayreturn

𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑅𝑒𝑣𝑖𝑠𝑖𝑜𝑛,,. =𝐸𝑃𝑆,,. − 𝐸𝑃𝑆,,.34

𝐸𝑃𝑆,,.34𝐸𝑁𝑅𝑃,,. =

𝐸𝑃𝑆,,. − 𝐸𝑃𝑆,,.34𝑃𝑟𝑖𝑐𝑒,,.

A) Most positive EPS revisions B) Most negative EPS revisions

0%

20%

40%

60%

80%

100%

120%

Sell-side EstimizeFES

top1% top2% top5% top10%

-80%-70%-60%-50%-40%-30%-20%-10%0%

Sell-side EstimizeFES

bottom1% bottom2% bottom5% bottom10%

13Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

PostEarningsAnnouncementDrift(PEAD)

Positiveearningssurprise,firstdayPEAD

ExcessreturnwhenEPSbeatsover40% ExcessreturnwhenEPSmissesover40%

Negativeearningssurprise,firstdayPEAD

0.0%

0.1%

0.2%

0.3%

0.4%

0.5%

0.6%

10%surprise 20%surprise 30%surprise 40%surprise

Estimize Sell-side

-0.7%

-0.6%

-0.5%

-0.4%

-0.3%

-0.2%

-0.1%

0.0%

10%surprise 20%surprise 30%surprise 40%surprise

Estimize Sell-side

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

day1 day2 day3

Estimize Sell-side

-0.8%

-0.6%

-0.4%

-0.2%

0.0%

0.2%

day1 day2 day3

Estimize Sell-side

• PEADismoresignificant,ifacompanybeats(ormisses)theEstimizeestimates.PEADdecaysawayaftertwodays.

• Benchmarkearningsyield. Forthebenchmarkfactor,weusetheconsensussell-sideEPS,bytakingasimpleaverageofCIQandIBES.

• StandardEstimizeearningsyield. Inthiscase,wereplacethesell-sideconsensuswiththeEstimizeestimateswhenwehaveatleastthreecontributorsintheEstimizedatabase.

• EstimizeFESearningsyield. InsteadofreplacingwiththestandardEstimizeestimates,weusetheFESmodelintroducedintheprevioussection.

14Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

e)Long-termInvestmentStrategies

Cumulative performance, long/short quintile portfolio on S&P500

𝐸𝑎𝑟𝑛𝑖𝑛𝑔𝑠𝑌𝑖𝑒𝑙𝑑 =𝐹𝑄1𝐸𝑃𝑆𝑃𝑟𝑖𝑐𝑒

Monthlyturnover Sharpe ratio, different transaction cost assumptions

0.9

1.0

1.1

1.2

1.3

Benchmarkearningsyield EstimizeAvgearningsyield

EstimizeFESearningsyield

0%10%20%30%40%50%60%70%80%90%100%

Benchmarkearningsyield

EstimizeAvgearningsyield

EstimizeFESearningsyield

0.0

0.1

0.2

0.3

0.4

0.5

Nocost 2bps 5bps

Benchmarkearningsyield EstimizeAvgearningsyield

EstimizeFESearningsyield

15Sources: Estimize,IBES,S&PCapitalIQ,FTSERussell,WolfeResearchLuo’sQES

EnhancedValueStrategies

Sharperatio,differentuniverse

Longonlyportfolioperformance,Russell3000universe SharpeRatio,LongonlyportfolioRussell3000universe

Sharperatio,monthlyversusdailyrebalance

0.0

0.5

1.0

1.5

2.0

2.5

3.0

EquallyweightedRussell3000 TopquintileEstimizeearningyield0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

EquallyweightedRussell3000 TopquintileEstimizeearningyield

0.00.20.40.60.81.01.21.4

S&P500 Russell3000 Russell3000sectorneutral

Baseline Estimize

0.00.20.40.60.81.01.21.4

Benchmarkearningsyield

EstimizeAvgearningsyield

EstimizeFESearningsyield

Russell3000universe,monthlyrebalance

Russell3000universe,dailyrebalance

• EnhancedearningsyieldusingEstimizedataperformsequallywellinbothlarge- andsmall-capuniverses.• Enhancedvaluestrategiesproducedecentperformanceinalong-onlycontext.

16

4.TextMiningUnstructuredCorporateFilingData

#ofEDGARFilings(Daily)

Average#ofWordsinthe10-KFilings

Sources: EDGAR,WolfeResearchLuo’sQES

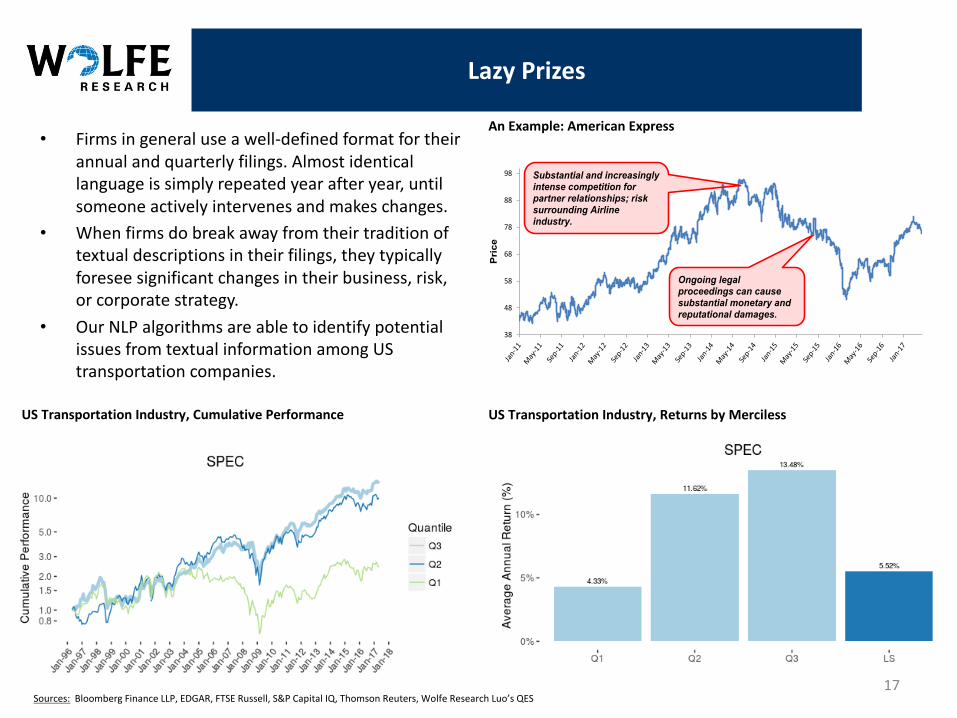

• Firmsingeneraluseawell-definedformatfortheirannualandquarterlyfilings.Almostidenticallanguageissimplyrepeatedyearafteryear,untilsomeoneactivelyintervenesandmakeschanges.

• Whenfirmsdobreakawayfromtheirtraditionoftextualdescriptionsintheirfilings,theytypicallyforeseesignificantchangesintheirbusiness,risk,orcorporatestrategy.

• OurNLPalgorithmsareabletoidentifypotentialissuesfromtextualinformationamongUStransportationcompanies.

17Sources: BloombergFinanceLLP,EDGAR,FTSERussell,S&PCapitalIQ,ThomsonReuters,WolfeResearchLuo’sQES

LazyPrizes

USTransportationIndustry,CumulativePerformance

38

48

58

68

78

88

98

Price

Substantial and increasingly intense competition for partner relationships; risk surrounding Airline industry.

Ongoing legal proceedings can cause substantial monetary and reputational damages.

USTransportationIndustry,ReturnsbyMerciless

AnExample:AmericanExpress

18Sources: BloombergFinanceLLP,FTSERussell,S&PCapitalIQ,ThomsonReuters,WolfeResearchLuo’sQES

SystematicProfilingEDGARComposite(SPEC)Model

SPECmodelrankIC SPECmodelLong/shortportfolioperformance

PortfolioSharperatioQuintileportfolioreturns

Long/shortmonthlyturnover RankICdecay

• Lastly,itisinterestingtonotethatourfactorhasalmostnoexposuretoclassicriskfactorssuchassize,betaorvolatility.

• OneofthemostimportantreasonsofrelyingonalternativeBigDatasourcesrestsonthediversificationbenefit,inthattheyareexpectedtohaveminimalcorrelationwithtraditionalfactors.

• Asexpected,oursignalsbasedonEDGARtextminingarealmostuncorrelatedtoanyofourtraditionalfactors.

• Finally,asauniquealphasource,theSPECmodelshouldcomplementandaddvaluetotraditionalfactors.

• Theperformanceofalltraditionalfactorsimprovesremarkably,whentheSPECisadded.Growthfactorswitnessthelargestimprovement.

• Improvementinrisk-adjustedperformanceisevenmoresignificant.

• TheSharperatioimprovesby50%forthemajorityoftheconventionalfactors.

19Sources: BloombergFinanceLLP,FTSERussell,S&PCapitalIQ,ThomsonReuters,WolfeResearchLuo’sQES

Interactionwithtraditionalfactors

FactorcorrelationswithEDGARcompositemodels

EarningsYield EarningsRevision Momentum 1MReversal ROE EPSgrowth Marketcap VolatilityComposite10K 11% 6% 4% 1% 10% -3% 11% -14%Composite10Q 8% 3% 3% 1% 7% -2% 8% -10%CompositeAll 11% 5% 5% 2% 11% -2% 11% -13%

0123456789

EarningsRevision

EarningsRevisioncomposite

EarningsYield

EarningsYield

composite

EPSgrowth EPSgrowthcomposite

Momentum Momentumcomposite

ROE ROEcomposite

CAGR

(%)

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

EarningsRevision

EarningsRevisioncomposite

EarningsYield

EarningsYield

composite

EPSgrowth EPSgrowthcomposite

Momentum Momentumcomposite

ROE ROEcomposite

Sharpe

ratio

AnnualizedreturnsofStylecompositesvsbasefactors

SharperatioofStylecompositesvsbasefactors

20

AnInteractiveWebPortal

21

DISCLOSURE SECTION

AnalystCertification:TheanalystofWolfeResearchprimarilyresponsibleforthisresearchreportwhosenameappearsfirstonthefrontpageofthisresearchreportherebycertifiesthat(i)therecommendationsandopinionsexpressedinthisresearchreportaccuratelyreflecttheresearchanalysts’personalviewsaboutthesubjectsecuritiesorissuersand(ii)nopartoftheresearchanalysts’compensationwas,isorwillbedirectlyorindirectlyrelatedtothespecificrecommendationsorviewscontainedinthisreport.

OtherDisclosures:WolfeResearch,LLCdoesnotassignratingsofBuy,HoldorSelltothestocksitcovers.Outperform,PeerPerformandUnderperformarenottherespectiveequivalentsofBuy,HoldandSellbutrepresentrelativeweightingsasdefinedabove.Tosatisfyregulatoryrequirements,OutperformhasbeendesignatedtocorrespondwithBuy,PeerPerformhasbeendesignatedtocorrespondwithHoldandUnderperformhasbeendesignatedtocorrespondwithSell.

WolfeResearchSecuritiesandWolfeResearch,LLChaveadoptedtheuseofWolfeResearchasbrandnames.WolfeResearchSecurities,amemberofFINRA(www.finra.org)isthebroker-dealeraffiliateofWolfeResearch,LLCandisresponsibleforthecontentsofthismaterial.AnyanalystspublishingthesereportsareduallyemployedbyWolfeResearch,LLCandWolfeResearchSecurities.

Thecontentofthisreportistobeusedsolelyforinformationalpurposesandshouldnotberegardedasanoffer,orasolicitationofanoffer,tobuyorsellasecurity,financialinstrumentorservicediscussedherein.Opinionsinthiscommunicationconstitutethecurrentjudgmentof theauthorasofthedateandtimeofthisreportandaresubjecttochangewithoutnotice.InformationhereinisbelievedtobereliablebutWolfeResearchanditsaffiliates,includingbutnotlimitedtoWolfeResearchSecurities,makesnorepresentationthatitiscompleteoraccurate.Theinformationprovidedinthiscommunicationisnotdesignedtoreplacearecipient'sowndecision-makingprocessesforassessingaproposedtransactionorinvestmentinvolvingafinancialinstrumentdiscussedherein.Recipientsareencouragedtoseekfinancialadvicefromtheirfinancialadvisorregardingtheappropriatenessofinvestinginasecurityorfinancialinstrumentreferredtointhisreportandshouldunderstandthatstatementsregardingthefutureperformanceofthe financialinstrumentsorthesecuritiesreferencedhereinmaynotberealized.Pastperformanceisnotindicativeoffutureresults.Thisreportisnotintendedfordistributionto,oruseby,anypersonorentityinanylocationwheresuchdistributionorusewouldbecontrarytoapplicablelaw,orwhichwouldsubjectWolfeResearch,LLCoranyaffiliatetoanyregistrationrequirementwithinsuchlocation.Foradditionalimportantdisclosures,pleaseseewww.wolferesearch.com\disclosures.

TheviewsexpressedinWolfeResearch,LLCresearchreportswithregardstosectorsand/orspecificcompaniesmayfromtimetotimebeinconsistentwiththeviewsimpliedbyinclusionofthosesectorsandcompaniesinotherWolfeResearch,LLCanalysts’researchreportsandmodelingscreens.WolfeResearchcommunicateswithclientsacrossavarietyofmediumsoftheclients’choosingincludingemails,voiceblastsandelectronicpublicationtoourproprietarywebsite.

Copyright©WolfeResearch,LLC2017.Allrightsreserved.Allmaterialpresentedinthisdocument,unlessspecificallyindicatedotherwise,isundercopyrighttoWolfeResearch,LLC.Noneofthematerial,noritscontent,noranycopyofit,maybealteredinanyway,ortransmittedtoordistributedtoanyotherparty,withoutthepriorexpresswrittenpermissionofWolfeResearch,LLC.

ThisreportislimitedforthesoleuseofclientsofWolfeResearch.Authorizedusershavereceivedanencryptiondecoderwhich legislatesandmonitorstheaccesstoWolfeResearch,LLCcontent.AnydistributionofthecontentproducedbyWolfeResearch,LLCwillviolatetheunderstandingofthetermsofourrelationship.