am6

DESCRIPTION

nnTRANSCRIPT

CONTEMPORANEOUS RISK FACTORS AND THE PREDICTION OF

FINANCIAL STATEMENT FRAUD*

Christopher J. Skousen**

Assistant Professor

Department of Accounting

University of Texas at Arlington

College of Business, Room 409

701 S. West Street

Arlington, Texas 76019-0468

Phone: 817-272-3040

Fax: 817-272-5793

and

Charlotte J. Wright

Wilton T. Anderson Professor of Accounting

School of Accounting

William S. Spears School of Business

Oklahoma State University

Stillwater, OK 74078

Phone: 405-744-8611

Fax: 405-744-5180

August 24, 2006

*We thank Don Hansen, Carol Johnson, Dan Tilley, Derek Oler, Steven Kaplan,

and participants at the 2005 AAA Tenth Ethics Research Symposium, 2005

Brigham Young University 2nd

Accounting Research Symposium, and 2006 AAA

Annual Meeting for comments and helpful suggestions.

** Corresponding Author.

1

CONTEMPORANEOUS RISK FACTORS AND THE PREDICTION OF

FINANCIAL STATEMENT FRAUD

ABSTRACT

This study identifies the contemporaneous risk factors empirically related

to financial statement fraud. Extant research identifies a number of individual

factors related to fraud in various settings. In this study we examine an array of

potential fraud risk factors in order to identify a comprehensive set of coexistent

factors that are consistently linked to the incidence of financial statement fraud.

Further, using the identified fraud risk factors, we construct a robust fraud

prediction model. The analysis yields a number of significant factors related to

pressure and opportunity. Using the significant fraud risk factors we then

construct a fraud prediction model. The model correctly classifies fraud and no-

fraud firms approximately 69.77 percent of the time, a substantial improvement

over other fraud prediction models.

Key words: Fraud prediction, fraud detection, risk factors, SAS No. 99

Data Availability: All data are available from public sources.

2

1. INTRODUCTION

A growing body of empirical evidence indicates that there is a relationship

between various corporate governance-related issues and the incidence of

financial statement fraud. For example, fraud has been linked to concentration of

power (Dunn 2004), CEOs serving on boards of directors (DeChow, et al. 1996),

audit committee independence (Abbott et al. 2000), board of director composition

(Beasley 1996), and the existence of audit committees (Beasley 1996). Fraud has

also been linked to financial-related factors, such as sales growth and leverage

(Beneish 1997), inventory and return on assets (Summers and Sweeney 1998),

and the desire to obtain low-cost financing (DeChow, et al. 1996). As was

demonstrated in the recent fraud-related corporate failures, fraud risk factors do

not appear to exist in isolation. While extant research identifies a number of

factors related to fraud in various settings, we could find no studies that identify a

set of risk factors contemporaneous linked to financial statement fraud. In this

study we examine an array of potential fraud risk factors in order to identify a

comprehensive set of coexistent factors that are consistently linked to the

incidence of financial statement fraud. Further, using the identified fraud risk

factors, we are able to construct a robust fraud prediction model.

Cressey’s (1953) fraud risk theory provides the framework for

identification of firms’ fraud risk factors. Cressey contends that, in varying

degrees, pressure, opportunity and rationalization are always present when

3

financial statement fraud occurs. Cressy’s fraud risk factor framework is widely

accepted as evidenced by its adoption by the American Institute of CPA’s

(AICPA) in Statement on Auditing Standards (SAS) No. 99, “Consideration of

Fraud in a Financial Statement Audit”. SAS No. 99 requires auditors to evaluate

the potential presence of fraudulent behavior by assessing factors related to

pressure, opportunity and rationalization.

The first objective of this study is to identify a comprehensive set of

contemporaneous firm-related factors that are empirically related to financial

statement fraud. Using the examples cited in SAS No. 99 and relying on prior

fraud research, we develop fraud proxy variables representing various measures

of pressure, opportunity and rationalization. We test these variables using a

sample of fraud firms and a matched sample of no-fraud firms. This analysis

yields a number of significant factors related to pressure and opportunity. These

results indicate that (1) the proportion of independent audit committee members is

inversely related to the incidence of fraud; (2) when the proportion of ownership

held by managers already holding more than 5 percent of the outstanding shares

increases, the probability of fraud increases; (3) when the proportion of insider

ownership (management and directors) decreases, the probability of fraud

increases; (4) the frequency of fraud is higher among firms that do not have an

audit committee; and (5) when one individual holds both the CEO and Chairman

4

of the Board positions, the incidence of fraud is significantly higher than when the

two positions are held by different individuals.

The second objective of this study is to determine whether the fraud risk

factor framework can be utilized to construct a model capable of effectively

predicting fraud using publicly available information. Other fraud prediction

models have reported success rates of between 30 and 40 percent. We construct

a fraud prediction model using the five significant fraud risk factors identified in

our initial analysis. Using publicly available information, our model correctly

classifies fraud and no-fraud firms approximately 69.77 percent of the time.

Thus, our model substantially outperforms previously reported fraud prediction

models.

Our research contributes to the literature by identifying a comprehensive

set of contemporaneous risk factors consistently related to the incidence of

financial statement fraud and by using these factors to develop a fraud prediction

model that out performs models previously reported in the literature. The

remainder of this paper is organized as follows. Section II provides a brief review

of the relevant fraud literature. Section III contains a description of the research

design and sample selection. Section IV contains the empirical results and

sensitivity analysis. We summarize and conclude in Section V.

5

2. LITERATURE REVIEW AND EMPIRICAL PREDICTION

Cressey’s (1953) fraud risk factor theory is based largely on a series of

interviews conducted with people who had been convicted of embezzlement.

Cressy concludes that frauds generally share three common traits. First, the

embezzler had the opportunity to perpetrate fraud. Second, the individual

perceived a non-shareable financial need (pressure). Third, the individual

involved in a fraud rationalized the fraudulent act as being consistent with their

personal code of ethics. Thus, Cressy concludes that a “fraud triangle” consisting

of pressure, opportunity and rationalization is the key to identifying factors that

are, to some extent, always present in any given fraud. The AICPA adopted

Cressey’s fraud risk factor theory in SAS No. 99; however, according to the

AICPA, only one factor need be present in order for fraud to be committed. SAS

No. 99 requires the auditor to apply numerous new procedures aimed at

examining the firm environment and to evaluate expansive amounts of new

information in an effort to identify facts and circumstances that are indicative of

the existence of pressures, opportunities and/or rationalizations. Table 1 appears

in SAS No. 99 and provides examples of situations and circumstances that are

symptomatic of each fraud risk category.

Insert Table 1 about here

Extant fraud-related accounting research examines a few of the examples

cited in SAS No. 99 as being linked to fraud; however, we are aware of no

6

research that comprehensively examines a broad range of fraud risk factors by

empirically testing. Our study utilizes Cressey’s (1953) theory in identifying and

empirically examining a broad range of potential fraud risk factors. We test the

basic premise that:

FRAUD = f(Pressure, Opportunity, Rationalization) [1]

This relationship may also be stated in the form of an empirical prediction:

EP: The fraud risk factors (pressure, opportunity and rationalization) are

positively related to financial statement fraud.

It is our expectation that financial statement fraud is positively correlated with

factors related to pressure, opportunity and rationalization. We further anticipate

that this relationship is useful in predicting financial statement fraud.

3. RESEARCH DESIGN AND SAMPLE SELECTION

Since the fraud risk factors are not directly observable, it is first necessary

for us to develop proxy variables to measure pressure, opportunity and

rationalization. For this we rely on the fraud risk factor examples cited in SAS

No. 99 (Table 1) as well as prior fraud-related accounting research. Our choice of

proxy variables and the relevant research are described below.

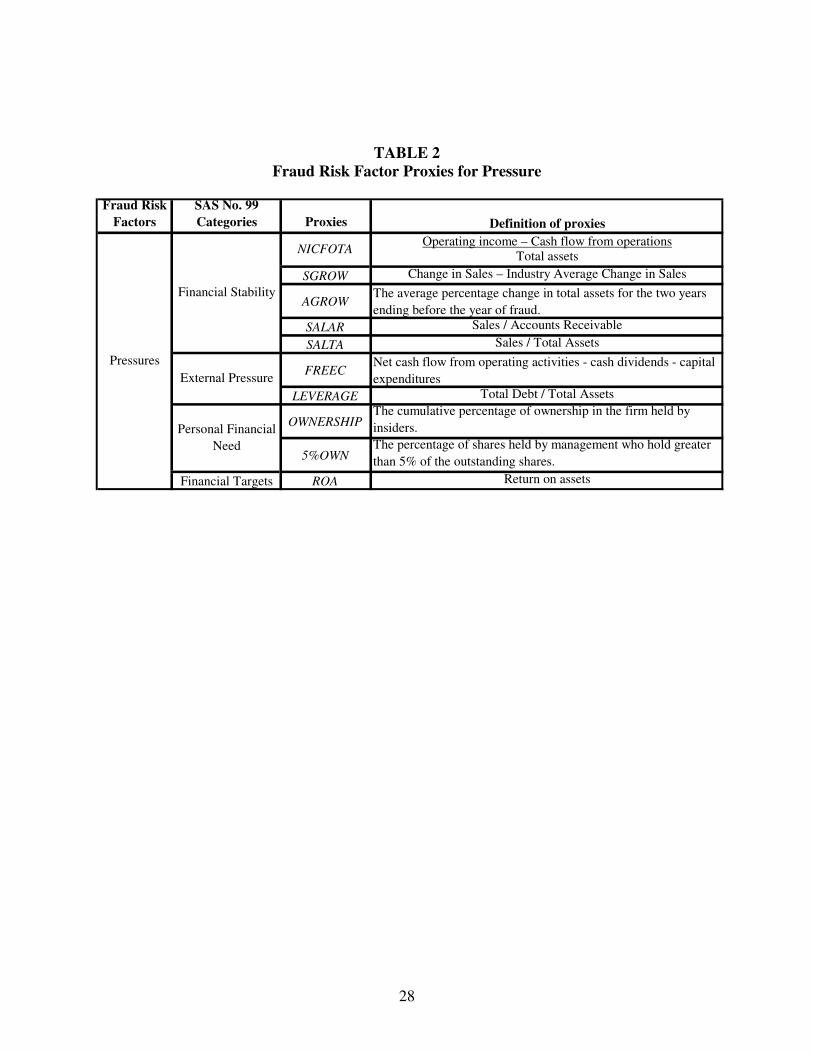

Fraud Risk Factor Proxies for Pressure

SAS No. 99 cites four general types of pressure that may lead to financial

statement fraud. These are financial stability, external pressure, managers’

7

personal financial situations, and meeting financial targets. Using these general

categories we identify five financial stability proxies, two external pressure

proxies, two personal financial need proxies and one proxy for financial targets.

These are described below.

Financial stability

SAS No. 99 suggests that when financial stability and/or profitability are

threatened by economic, industry, or entity operating conditions, managers face

pressure to commit financial statement fraud. Loebbecke et al. (1989) and Bell et

al. (1991) indicate that, in instances where a company is experiencing growth that

is below the industry average, management may resort to financial statement

manipulation to improve the firm’s outlook. Likewise, following a period of

rapid growth, management may resort to financial statements manipulation to

provide the appearance of stable growth. Accordingly, our proxy variables include

growth in sales (Beasley 1996; Summers and Sweeney 1998) and growth in assets

(Beneish 1997; Beasley et al. 2000). These are computed as:

SGROW = Change in Sales – Industry Average Change in Sales

AGROW = Percent change in Assets for the two years prior to

fraud.

SAS No. 99 suggests that financial stability may be affected by recurring

negative cash flows from operations or an inability to generate positive operating

8

cash flows in light of reported earnings growth. We use the following financial

stability ratio (Albrecht 2002) to relate cash flows to earnings growth:

NICFOTA = Operating income – Cash flow from operations

Total assets

Albrecht (2002) and Wells (1997) conclude that financial ratios involving

key income statement and balance sheet figures are useful in detecting fraud.

Persons (1995) suggests that sales to accounts receivable and sales to total assets

are useful in fraud detection. We include the following financial security proxies:

SALAR – Sales / Accounts receivables

SALTA – Sales / Total assets.

External pressure

The ability to meet exchange-listing requirements, repay debt or meet debt

covenants are widely recognized sources of external pressure. Vermeer (2003)

and Press and Weintrop (1990) report that, when faced with violation of debt

covenants, managers are more likely to utilize discretionary accruals. The extent

of leverage has also been associated with income increasing discretionary accruals

(DeAngelo et al.1994; DeFond and Jiambalvo 1991). Therefore, we include

leverage as a proxy for external pressure:

LEVERAGE = Total debt / Total assets

9

Dechow et al. (1996) note that when a firm has adequate internal funding,

managers are less likely to engage in fraud. We include free cash flow as an

additional measure of external pressure:

FREEC = Net cash flow from operating activities – cash dividends

– capital expenditures

Personal financial need

Beasley (1996), COSO (1999), and Dunn (2004) indicate that when

executives have a significant financial stake in a firm, their personal financial

situation may be threatened by the firm’s financial performance. We include

OWNERSHIP and 5%OWN as proxies for personal financial need:

OWNERSHIP = the cumulative percentage of ownership in the

firm held by insiders. Shares owned by management

divided by the common shares outstanding.

5%OWN = the cumulative percentage of ownership in the firm

held by management who hold 5 percent of the

outstanding shares or more divided by the common

shares outstanding.

Financial targets

Return on total assets (ROA) is a measure of operating performance that

shows how well assets have been employed. ROA is often used as a measure to

assess the performance of managers and thus potentially affects bonuses, wage

increases, etc. Summers and Sweeney (1998) report that ROA differs

significantly between fraud and no-fraud firms. Thus, we include ROA as a

financial target proxy.

10

ROA = Net Income before extraordinary items t-1

Total Assets t

Table 2 summarizes the fraud risk factor proxies for pressure.

Insert Table 2 about here

Fraud Risk Factor Proxies for Opportunity

SAS No. 99 cites four general categories of opportunities that may lead to

financial statement fraud. These are nature of industry, ineffective monitoring,

organizational structure, and internal control. Using these categories we identify

seven proxies for opportunity. These are described below.

Nature of industry

SAS No. 99 and Albrecht (2002) indicate that when a firm has significant

operations located in different international jurisdictions the opportunities for

fraud increase. We include FOROPS as a proxy for opportunity resulting from

significant foreign operations:

FOROPS = Percent of sales which are foreign. This is calculated

as total foreign sales divided by total sales.

Ineffective monitoring

Beasley et al. (2000), Beasley (1996), Dechow et al. (1996) and Dunn

(2004) observe that fraud firms consistently have fewer outside members on their

board of directors than do no-fraud firms. Therefore, we include BOUTP to proxy

for related to board composition.

BOUTP = Percentage of board members who are outside members.

11

Beasley et al. (2000) observe a reduced incidence of fraud among those

companies having an audit committee. Additionally, the larger audit committees

are associated with a lower incidence of fraud (Beasley et al. 2000). Consistently,

we use the following measures related to audit committees:

AUDCOMM = Indicator variable with the value of 1 if mention of

oversight by an internal audit committee; and 0

otherwise.

AUDCSIZE = The number of board members who are on the

audit committee divided by the board size.

Abbott and Parker (2001), Abbott et al. (2000), Beasley et al. (2000), and

Robinson (2002) identify a relationship between the independence of audit

committee members and the incidence of fraud. Therefore, we include IND as a

proxy for ineffective monitoring. We define an independent audit committee

member as a member who is not: a current employee of the firm, former officer or

employee of the firm or related entity, a relative of management, professional

advisor to the firm, officers of significant suppliers or customers of the firm,

interlocking director, and/or one who has no significant transactions with the firm

(Robinson 2002).

IND = The percentage of audit committee members who are

independent of the company.

Additionally, we include AUDMEET as a measure of the number of audit

committee meetings.

12

AUDMEET = The number of audit committee meetings held per

year.

Organizational structure

Loebbecke et al. (1989), Beasley (1996), Beasley et al. (1999), Abbott et

al. (2000), and Dunn (2004) conclude that, as a CEO accumulates titles, he/she is

in a position to dominate decision making. Since control of decision making may

provide an opportunity to commit fraud we include the following:

CEO = Indicator variable with a value of 1 if the chairperson of the

board holds the managerial positions of CEO or president;

and 0 otherwise.

Table 3 summarizes the fraud risk factor proxies for opportunity.

Insert Table 3 about here

Fraud Risk Factor Proxies for Rationalization

While rationalization is a necessary component of the fraud triangle, an

individual’s rationale is difficult to observe. Extant research indicates that the

frequency of audit failure and litigation increases immediately after a change in

auditor (Stice 1991; St. Pierre and Anderson 1984; Loebbecke et al.1989).

Therefore, we include auditor change as a proxy for rationalization:

AUDCHANG = a dummy variable for change in auditor where 1

= change in auditor in the 2 years prior to fraud

occurrence and 0 = no change in auditor.

Beneish (1997), Francis and Krishnan (1999), and Vermeer (2003) argue

that accruals are representative of management’s decision making and provide

13

insight into their financial reporting rationalizations. Francis and Krishnan (1999)

report that the excessive use of discretionary accruals may be cited in the audit

report. Accordingly, we include the following two variables to capture

rationalizations related to managements’ use of accruals:

AUDREPORT = a dummy variable for an audit where 1 = an unqualified

opinion and 0 an unqualified opinion with additional

language.

TATA = Total accruals divided by total assets, where total accruals are

calculated as the change in current assets, minus the change in

cash, minus changes in current liabilities, plus the change in

short-term debt, minus depreciation and amortization expense,

minus deferred tax on earnings, plus equity in earnings.

Table 4 summarizes the fraud risk factor proxies for rationalization.

Insert Table 4 about here

The full model that we use to test the empirical prediction is:

FRAUDi = α + β1NICFOTAi + β2SGROWi + β3AGROWi + β4SALARi

+ β5SALTAi + β6FREECi + β7LEVERAGEi + β8OWNERSHIPi

+ β95%OWNi + β10ROAi + β11FOROPSi + β12BOUTPi

+ β13AUDCOMMi + β14AUDCSIZEi + β15INDi + β16AUDMEETi

+ β17CEOi + β18AUDCHANGi + β19AUDREPORTi

+ β20TATAi + εi [2]

We test the model using both univariate analysis and logit regression.

Sample Selection

In order to evaluate our empirical prediction we first identify a set of firms

that had been accused of fraud by the Securities and Exchange Commission

(SEC). We define fraud firms as being those that were charged with violation of

14

Rule 10(b)-5 of the 1934 Securities Act or Section 17(a) of the 1933 Securities

Act and we examine the SEC Accounting and Auditing Enforcement Releases

(AAERs) issued between 1992 and 2001. Using this procedure we identified 113

fraud firms. Since it was necessary to obtain firms’ proxy and financial statement

data, it was necessary for firms’ financial data be available on the LexisNexis

SEC Filings & Reports website and COMPUSTAT for the year of the alleged

fraud as well as the two preceding years. This criterion resulted in elimination of

27 firms yielding a final sample of 86 fraud firms. The fraud firms come from a

variety of industries. Industry demographics of fraud firms are reported in Table

5. The fraudulent activities these firms were accused of occurred fairly evenly

over the 10-year period with the largest number occurring in 1997-1999.

Insert Table 5 about here

Next, in order to develop a control set of no-fraud firms, we first matched

based on industry membership (4 digit SIC code), year, and size (Net Sales +/-

30%) in the year prior to fraud (Beasley 1996). We then searched the SEC

AAERs to verify that none of the match firms had been the subject of SEC fraud-

related actions. Table 6 reports sample statistics for the fraud and no-fraud firms

including results of paired t-tests and Wilcoxon matched-pair sign-rank tests

indicating no significant differences between the two groups of firms.

Insert Table 6 about here

15

4. RESULTS

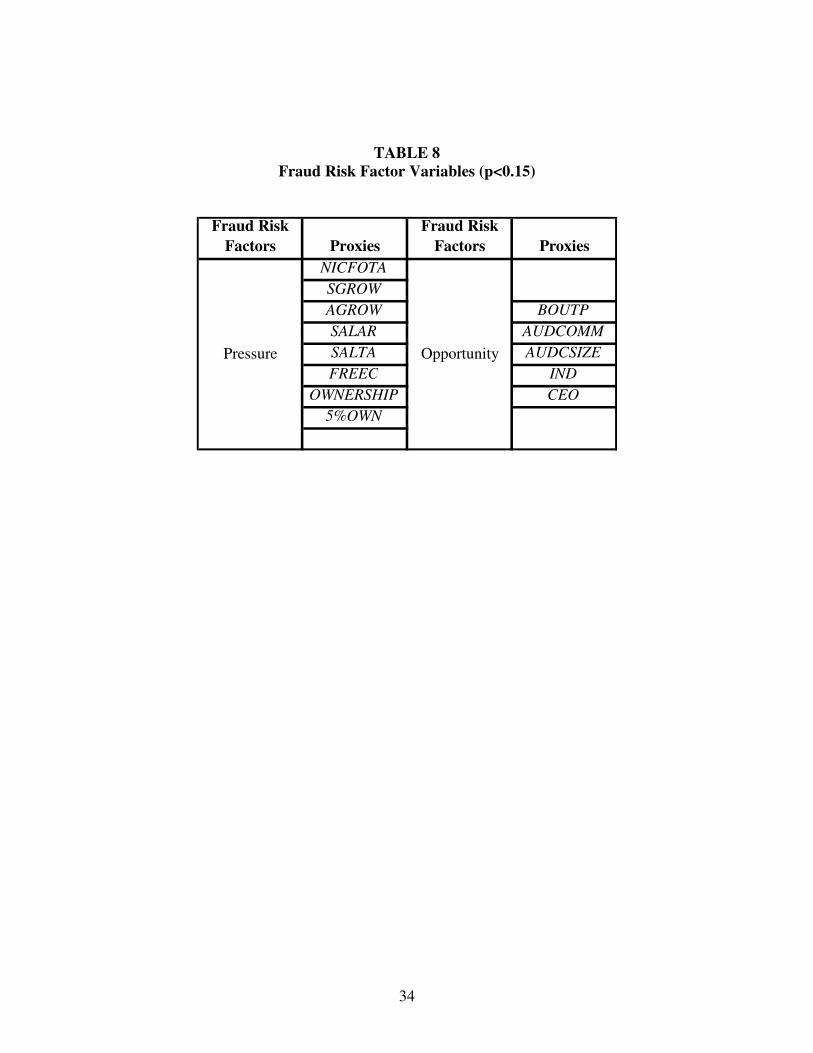

As an initial assessment of the proxy variables, we perform univariate

analysis. This analysis identifies eight pressure variables and five opportunity

variables that differ significantly between the fraud and no-fraud firms. No

rationalization proxy variables differed between the two groups. The univariate

analysis enables us to substantially reduce the number of explanatory variables

used in the logit regression. The results of the univariate analysis for all variables

are reported in Table 7.

Insert Table 7 about here

Following Hosmer and Lemeshow (2000) and Agrawal and Chadha

(2005) use conditional logit regression on the explanatory variables including

only the pressure and opportunity proxy variables identified in the univariate

analysis as having a p-value of 0.15 or less. The logit regression model is:

FRAUDi = β0 + β1NICFOTA + β2SGROW + β3AGROW + β4SALAR + β5SALTA + β6FREEC + β7OWNERSHIP+ β85%OWN + β9BOUTP + β10AUDCOMM + β11IND+ β12CEO + ε [3]

Table 8 lists, by type, the proxy variables that we use as explanatory variables in

the logit regression analysis.

Insert Table 8 about here

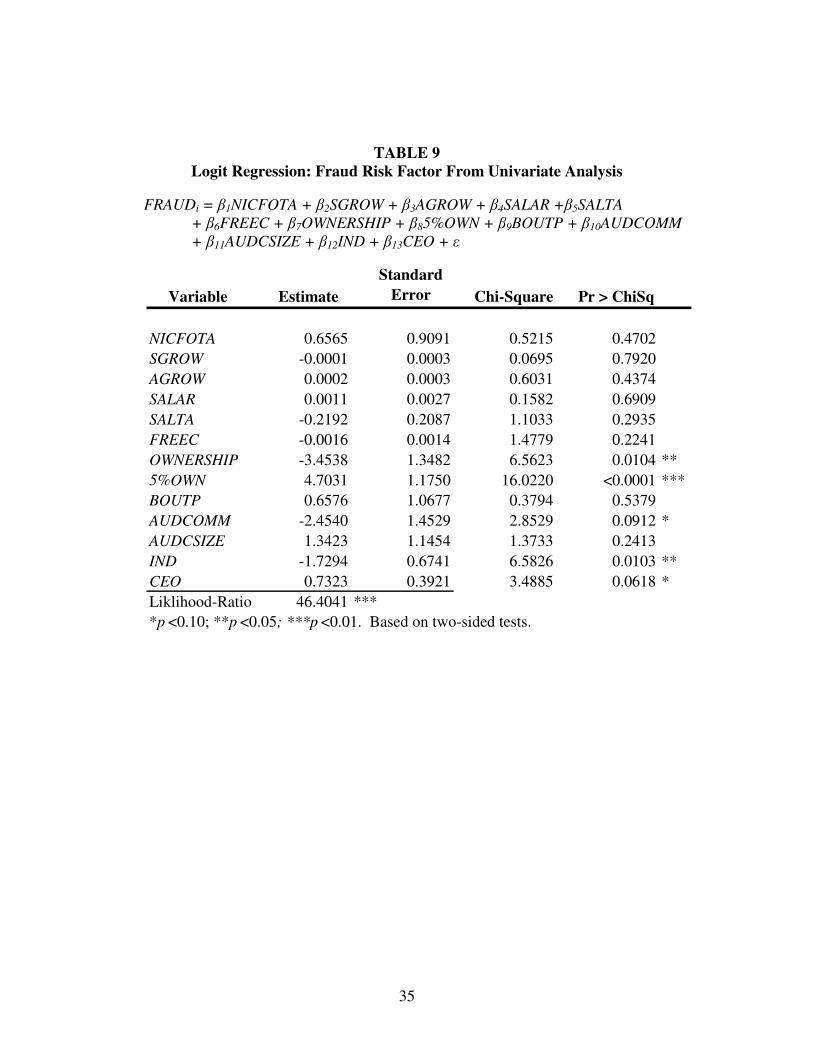

The results of the logit analysis are reported in Table 9. The model is

significant at p<0.01 as indicated by the likelihood ratio of 46.4041.1 Two

pressure variables (OWNERSHIP and 5%OWN) are significant (p<0.05, and

16

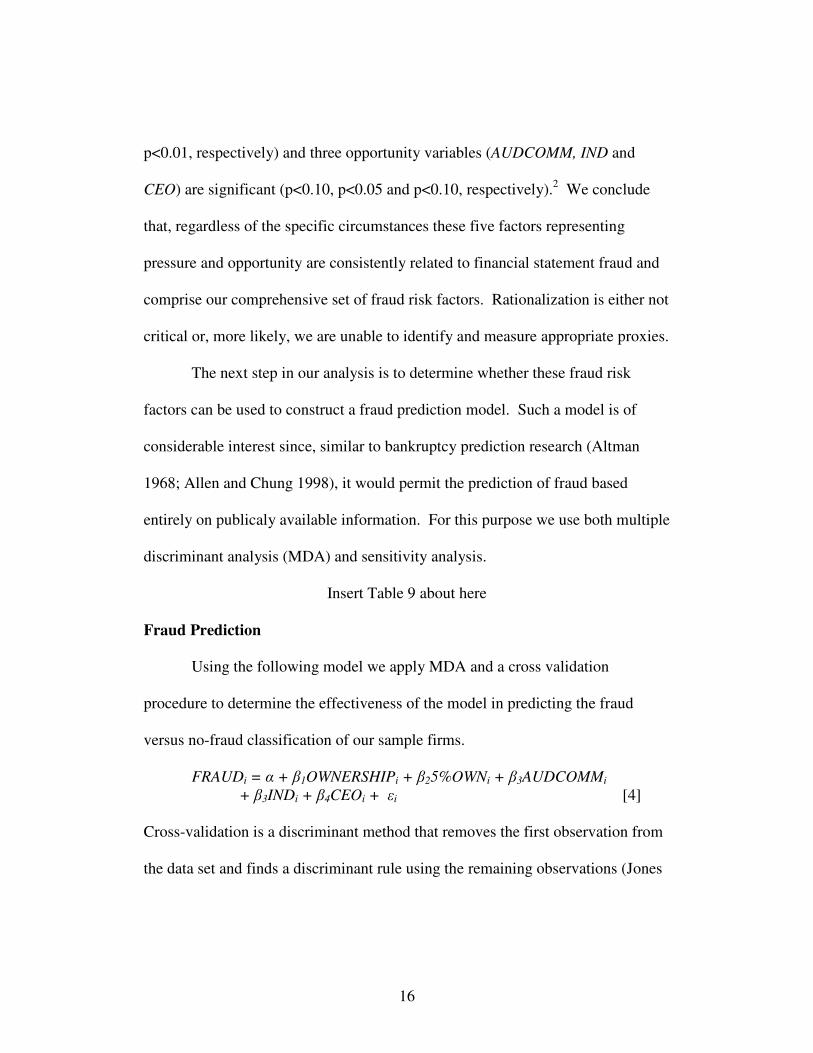

p<0.01, respectively) and three opportunity variables (AUDCOMM, IND and

CEO) are significant (p<0.10, p<0.05 and p<0.10, respectively).2 We conclude

that, regardless of the specific circumstances these five factors representing

pressure and opportunity are consistently related to financial statement fraud and

comprise our comprehensive set of fraud risk factors. Rationalization is either not

critical or, more likely, we are unable to identify and measure appropriate proxies.

The next step in our analysis is to determine whether these fraud risk

factors can be used to construct a fraud prediction model. Such a model is of

considerable interest since, similar to bankruptcy prediction research (Altman

1968; Allen and Chung 1998), it would permit the prediction of fraud based

entirely on publicaly available information. For this purpose we use both multiple

discriminant analysis (MDA) and sensitivity analysis.

Insert Table 9 about here

Fraud Prediction

Using the following model we apply MDA and a cross validation

procedure to determine the effectiveness of the model in predicting the fraud

versus no-fraud classification of our sample firms.

FRAUDi = α + β1OWNERSHIPi + β25%OWNi + β3AUDCOMMi + β3INDi + β4CEOi + εi [4]

Cross-validation is a discriminant method that removes the first observation from

the data set and finds a discriminant rule using the remaining observations (Jones

17

1987, Hair et al. 1995, and Kuruppu et al. 2003). This procedure develops a

model from n – 1 observations, and applies it to the observation not used in

developing the model. This process is repeated until all the firms in the sample

are used to assess the model’s accuracy. The cross-validation method is effective

at providing an unbiased estimate of a model’s misclassification rate (Hair et al.

1995) and is particularly useful in studies with small sample sizes since the entire

sample can be used to cross-validate the results (Kuruppu et al. 2003).

This analysis indicates that our model accurately classifies firms

approximately 69.77 percent of the time (the overall misclassification rate of the

model is 30.23). As reported in Table 10, the model correctly classifies no-fraud

firms 74.42 percent of the time and correctly classifies fraud firms 65.12 percent

of the time. These results are notable. Person (1995) and Kaminski et al. (2004)

develop fraud prediction models using financial ratios. These models suffer from

high misclassification rates. For example, in Person (1995) and Kaminski et al.

(2004) fraud firms are misclassified between 58 and 98 percent of the time.

Insert Table 10 about here

Sensitivity Analysis

Next, we use sensitivity analysis to assess the individual predictive ability

of each explanatory variable in our model (i.e., IND, 5%0WN, OWNERSHIP,

CEO and AUDCOMM). Sensitivity analysis tests each variable’s proportional

relationship to the probability of being in the fraud group while holding the other

18

variables in the model at their mean. Figures 1 through 5 report the results of the

sensitivity analysis.

The analysis of IND indicates that, as the proportion of audit committee

members who are independent increases, the probability of financial statement

fraud decreases. This result, as reported in Figure 1, indicates that, when the

independent audit committee members comprise 12 percent of the audit

committee, the probability of a firm being in the fraud group is approximately 29

percent. On the other hand, when 78 percent of the audit committee members are

independent, the probability of being in the fraud group decreases to 12 percent.

As IND increases to 100 percent, the probability of being in the fraud group

decreases to 9 percent.

Insert Figure 1 about here

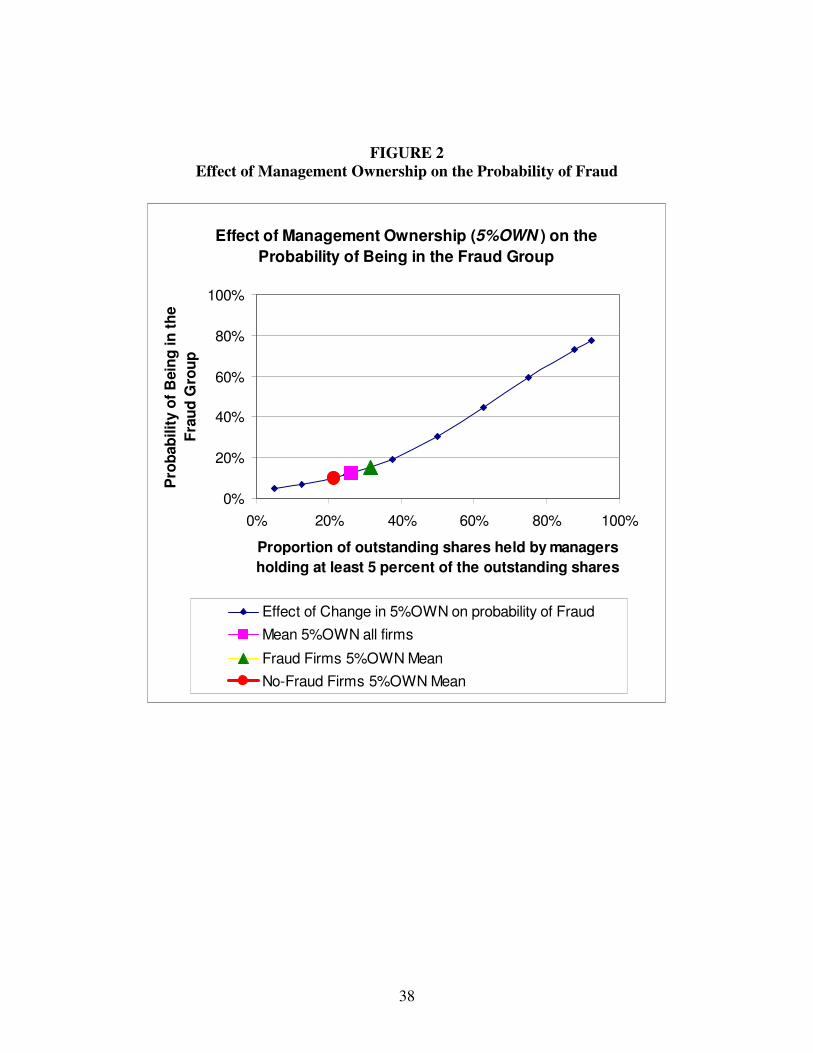

The analysis of 5%OWN reveals that a relationship exists between the

probability of a firm being in the fraud group and the proportion of managers who

own more than 5 percent of their firm’s shares. These results are reported in

Figure 2. When the proportion of ownership held by managers who hold more

than 5 percent of the outstanding shares increases, the probability of fraud

increases. When 5%OWN is approximately 12 percent of the firm’s outstanding

shares, the probability of a firm being in the fraud group is 7 percent. When

5%OWN increases to 75 percent, the probability of being in the fraud group

increases to 59 percent.

19

Insert Figure 2 about here

The analysis of OWNERSHIP indicates that when the proportion of insider

ownership (management and directors) decreases, the probability of being in the

fraud group increases. When insiders own 75 percent of the firm’s outstanding

shares, the probability of being in the fraud group is 2 percent. When

OWNERSHIP decreases to its mean value of approximately 20 percent, the

probability of fraud increases to 12 percent. The results appear in Figure 3.

Insert Figure 3 about here

The analysis of 5%OWN and OWNERSHIP indicates that management

ownership is a positive deterrence to fraud, so long as the ownership of the

remainder of the firm’s stock ownership is diffused. Thus, the larger the

percentage of shares held by managers, the lower the likelihood of fraud

occurring so long as individual managers do not hold a substantial portion of the

firm’s stock. In other words, when a large portion of a firm’s outstanding shares

are owned by management, the incidence fraud increases.3

Figure 4 reports the relationship between the incidence of fraud and

situations where a single individual holds both the CEO and Chairman of the

Board positions (CEO). When the CEO holds the Chairman of the Board position

(CEO = 1), the probability of being in the fraud group is 15 percent; otherwise

(CEO = 0) the probability of being in the fraud group is 8 percent.

Insert Figure 4 about here

20

The relationship between the occurrence of fraud and the existence of an

audit committee (AUDCOMM) is reported in Figure 5. When a firm has an audit

committee (AUDCOMM = 1), the probability of being in the fraud group is 11

percent; otherwise (AUDCOMM = 0) the probability of being in the fraud group is

40 percent.

Insert Figure 5 about here

5. CONCLUSION AND OBSERVATIONS

Extant fraud-related accounting research identifies an array of factors that

are related to the incidence of financial statement fraud in various settings.

However, these risk factors do not appear to exist in isolation. In any given fraud,

multiple risk factors are typically present. In this study, we examine an array of

potential fraud risk factors and identify a comprehensive set of coexistent factors

that are consistently linked to the incidence of financial statement fraud. Further,

using the significant risk factors we are able to develop a fraud prediction model

that outperforms previously reported models that attempt to predict fraud using

publicly available information.

Cressey’s (1953) fraud risk theory provides the framework for

comprehensive evaluation of firms’ fraud risk factors. Using the examples cited in

prior fraud research and in SAS No. 99, we develop proxy variables for pressure,

opportunity and rationalization. We test these variables using conditional logit

21

analysis and a sample of fraud firms (i.e., firms that were the target of SEC fraud

enforcement) and a matched sample of no-fraud firms. This analysis identifies

two pressure variables (OWNERSHIP and 5%OWN) and three opportunity

variables (AUDCOMM, IND, and CEO) as being significant fraud risk factors.

The second objective of this study is to construct a fraud prediction model

using the fraud risk factor framework. For this purpose we use both MDA and

sensitivity analysis. MDA determines whether the model can be used to

accurately categorize firms into the fraud and no-fraud groups. Using a cross

validation procedure our model correctly classifies no-fraud firms 74.42 percent

of the time and correctly classifies fraud firms 65.12 percent of the time. Overall,

the model correctly classifies firms 69.77 percent of the time (the overall

misclassification rate of the model is 30.23 percent). These results represent a

substantial improvement over other fraud prediction models that have reported

success rates of 30 to 40 percent (Persons 1995; Kaminski et al. 2004).

Bankruptcy prediction models using a similar approach yielded accuracy rates of

between 40 and 50 percent (Kuruppu et al. 2003).

As a final step we perform sensitivity analysis on each of the five

significant fraud risk factor proxy variables. This analysis tests each variable’s

proportional relationship to the probability of being in the fraud group while

holding the other variables in the model at their mean. These results indicate that,

(1) as the proportion of independent audit committee members increases, the

22

probability of financial statement fraud is reduced; (2) when the proportion of

ownership held by managers who hold more than 5 percent of the outstanding

shares increases the probability of fraud increases; (3) when the firm does not

have an audit committee, the likelihood of fraud increases; (4) when the

proportion of insider ownership (management and directors) decreases, the

probability of being in the fraud group increases; and (5) when one individual

holds both the CEO and Chairman of the Board positions the incidence of fraud is

significantly higher than when the two positions are held by different individuals.

This research contributes to the literature by examining and identifying a

set of risk factors that are contemporaneously related to the incidence of fraud and

by using these factors to develop a fraud prediction model. The development of a

fraud prediction model based upon the fraud risk factors is of interest to

academics, standard setters, and users of financial statement data since, similar to

bankruptcy prediction research (Altman 1968; Allen and Chung 1998), it permits

the prediction of fraud based entirely on publicaly available information.

23

ENDNOTES

1 In tests involving small to moderate samples the likelihood ratio test is appropriate for

determining overall fit (Greene 2000).

2 Tests using all fraud risk factor proxy variables yielded similar results.

3 Among the proxies, 5%OWN and OWNERSHIP were the highest correlated variables at 55%

level. None of the variables were significantly correlated.

24

REFERENCES

Abbott, L., Y. Park, and S. Parker. 2000. The effects of audit committee activity

and independence on corporate fraud. Managerial Finance 26 (11): 55-67

Abbott, L. and S. Parker. 2001. Audit committees and auditor selection. Journal of Accountancy 191 (6): 95-96

Agrawal, A. and S. Chadha, 2005. "Corporate Governance and Accounting

Scandals". Journal of Law and Economics 48 (2): Forthcoming.

Albrecht, W. 2002. Fraud Examination. Mason, OH: Thomson-SouthWestern.

Allen, D. and J. Chung. 1998. A review of choice of model and statistical

techniques in corporate distress prediction studies.” Accounting Research Journal 11 (1): 245-269.

Altman, E. 1968. Financial ratios, discriminant analysis and the prediction of

corporate bankruptcy. Journal of Finance 35: 1001-1016.

American Institute of Certified Public Accountants (AICPA). 2002. Consideration

of fraud in a financial statement audit. Statement on Auditing Standards No. 99.

New York, NY: AICPA.

Beasley, M. 1996. An empirical analysis of the relation between the board of

director composition and financial statement fraud. The Accounting Review 71

(4): 443-465.

Beasley, M., J. Carcello, and D. Hermanson. 1999. COSO's new fraud study:

What it means for CPAs. Journal of Accountancy 187 (5): 12-14.

Beasley, M., J. Carcello, D. Hermanson, and P. D. Lapides. 2000. Fraudulent

financial reporting: Consideration of industry traits and corporate governance

mechanisms. Accounting Horizons 14 (4): 441-454.

Bell, T., S. Szykowny, and J. Willingham. 1991. Assessing the likelihood of

fraudulent financial reporting: A cascaded logit approach. Working Paper, KPMG

Peat Marwick, Montvale, NJ.

25

Beneish, M. 1997. Detecting GAAP violation: Implications for assessing

earnings management among firms with extreme financial performance. Journal of Accounting and Public Policy 16 (3): 271-309.

Committee of Sponsoring Organizations of the Treadway Commission (COSO).

1999. Fraudulent Financial Reporting: 1987-1997 – Analysis of US. Public Companies. New York, NY: COSO.

Cressey, D. 1953. Other People’s Money; a Study in the Social Psychology of Embezzlement. Glencoe, IL, Free Press.

DeAngelo, H., L. DeAngelo, and D. Skinner. 1994. “Accounting choice in

troubled companies. Journal of Accounting and Economics 17 (1): 113-143.

Dechow, P., R. Sloan, and A. Sweeney. 1996. Causes and consequences of

earnings manipulation: An analysis of firms subject to enforcement actions by the

SEC. Contemporary Accounting Research 13 (1): 1-36.

DeFond, M. and J. Jiambalvo. 1991. Incidence and circumstances of accounting

errors. The Accounting Review 66 (3): 643-655.

Dunn, P. 2004. The impact of insider power on fraudulent financial reporting.

Journal of Management, 30(3) 397-412.

Francis, J. and J. Krishnan. 1999. Accounting accruals and auditor reporting

conservatism. Contemporary Accounting Research 16 (2): 135-165.

Greene, W. 2000. Econometric Analysis, Prentice Hall, Upper Saddle River, New

Jersey, 256

Hair, J., R. Anderson, R. Tatham, and W. Black. 1995. Multivariate Data Analysis, 4

th ed., Prentice Hall, Englewood Cliffs, NJ.

Hosmer, D. W. and S. Lemeshow, 2000. Applied Logistic Regression, Second

edition, New York, NY: John Wiley and Sons, Inc.

Jones, F. 1987. Current techniques in bankruptcy prediction. Journal of Accounting Literature 1: 131-164.

Kaminski, K., T. Wetzel, and L. Guan. 2004. Can financial ratios detect

fraudulent financial reporting? Managerial Auditing Journal 19 (1): 15-28.

26

Kuruppu, N., F. Laswad, and P. Oyelere. 2003. The efficacy of liquidation and

bankruptcy models for assessing going concern. Managerial Auditing Journal 18

(6/7): 577-590.

Loebbecke. J., M. Eining, and J. Willingham. 1989. Auditors’ experience with

material irregularities: Frequency, nature, and detestability. Auditing: A Journal of Practice & Theory 9 (Fall): 1-28.

Persons, O. 1995, Using financial statement data to identify factors associated

with fraudulent financial reporting. Journal of Applied Business Research 11 (3):

38-46.

Press, E. and J. Weintrop. 1990. Accounting constraints in public and private debt

agreements: Their association with leverage and impact on accounting choice.

Journal of Accounting and Economics 12:65-95.

Robinson, D. 2002. Audit Committee Composition and Financial Reporting Problems. Stillwater, Oklahoma: Oklahoma State University.

St. Pierre, K., and J. Anderson. 1984. An analysis of the factors associated with

lawsuits against public accountants. The Accounting Review 59 (2): 242-263.

Stice, J. 1991. Using financial and market information to identify pre-engagement

factors associated with lawsuits against auditors. The Accounting Review 66 (3):

516-533.

Summers, S. and J. Sweeney. 1998. “Fraudulently misstated financial statements

and insider trading: An empirical analysis.” The Accounting Review 73 (1): 131-

146.

Vermeer, T. 2003. The impact of SAS No. 82 on an auditor’s tolerance of

earnings management. Journal of Forensic Accounting 5: 21-34.

Wells, J. 1997. Corporate Fraud Handbook: Prevention and Detection.

Hoboken, New Jersey: Wiley

27

TABLE 1

Examples of Fraud Risk Factors from SAS No. 99 Relating to Financial Statement

Misstatements

Pressures Opportunities Rationalizations 1. Financial stability or

profitability is threatened by

economic, industry, or entity

operating conditions:

• High degree of competition or

declining profit margins

• High vulnerability to rapid changes

(i.e., technology, obsolescence, or

interest rates)

• Declines in customer demand

• Operating losses

• Recurring negative cash flows

from operations

• Rapid growth or unusual

profitability

• New accounting, statutory, or

regulatory requirements

2. Excessive pressure exists for

management to meet requirements

of third parties:

• Profitability/trend expectations

• Need to obtain additional debt or

equity financing

• Marginal ability to meet exchange

listing requirements or debt

repayment or other debt covenant

requirements

• Likely poor financial results on

significant pending transactions.

3. Management or directors’

personal financial situation is:

• Significant financial interests in the

entity

• Significant performance based

compensation

• Personal guarantees of debts

4. There is excessive pressure on

management or operating

personnel to meet financial targets

set up by directors or

management.

1. Industry provides opportunities

for

• Related-party transactions beyond

ordinary

• A strong financial presence or

ability to dominate a certain

industry sector that allows the

entity to dictate terms or

conditions to suppliers or

customers

• Accounts based on significant

estimates

• Significant, unusual, or highly

complex transactions

• Significant operations across

international borders environments

and cultures

• Significant bank accounts in tax-

haven jurisdictions

2. Ineffective monitoring of

management allows

• Domination of management by a

single person or small group

• Ineffective board of directors or

audit committee oversight

3. There is a complex or unstable

organizational structure

• Difficulty in determining the

organization or individuals that

have control of company

• Overly complex structure

• High turnover of senior

management, counsel, or board

4. Internal control deficient

• Inadequate monitoring of controls

• High turnover rates or employment

of ineffective accounting, internal

audit, or information technology

staff

• Ineffective accounting and

information systems.

1. Attitudes/rationalizations by

board members, management, or

employees that allow them to

engage in and/or justify

fraudulent financial reporting

• Ineffective communication,

implementation, support, or

enforcement of ethics

• Nonfinancial management's

excessive participation in

selection of accounting principles

or the determining estimates

• Known history of violations of

securities laws or other laws

• Excessive interest in maintaining

or increasing stock price

• Aggressive or unrealistic forecasts

• Failure to correct known

reportable conditions on a timely

basis

• Interest by management in

employing inappropriate means to

min. reported earnings for tax

• Recurring attempts by

management to justify marginal or

inappropriate accounting on the

basis of materiality

• Strained relationship with current

or predecessor auditor

o Frequent disputes with the

current or predecessor auditor

o Unreasonable demands on the

auditor, such as unreasonable

time constraints

o Restrictions on the auditor that

inappropriately limit access

o Domineering management

behavior in dealing with the

auditor

28

TABLE 2

Fraud Risk Factor Proxies for Pressure

Fraud Risk

Factors

SAS No. 99

Categories Proxies Definition of proxies

Operating income – Cash flow from operationsTotal assets

SGROW Change in Sales – Industry Average Change in Sales

AGROWThe average percentage change in total assets for the two years

ending before the year of fraud.

SALAR Sales / Accounts Receivable

SALTA Sales / Total Assets

FREECNet cash flow from operating activities - cash dividends - capital

expenditures

LEVERAGE Total Debt / Total Assets

OWNERSHIPThe cumulative percentage of ownership in the firm held by

insiders.

5%OWNThe percentage of shares held by management who hold greater

than 5% of the outstanding shares.

Financial Targets ROA Return on assets

Pressures

Financial Stability

NICFOTA

External Pressure

Personal Financial

Need

29

TABLE 3

Fraud Risk Factor Proxies for Opportunity

Fraud Risk

Factors

SAS No. 99

Categories Proxies Definition of proxies

Nature of

IndustryFOROPS Foreign Sales / Total Sales

BOUTP The percentage of board members who are outside members.

AUDCOMMA dummy variable where 1 = mention of oversight by an internal

audit committee and 0 = no mention of oversight.

AUDCSIZE The size of the audit committee scaled by board size.

INDThe percentage of audit committee members who are

independent of the company.

AUDMEET The number of audit committee meetings held.

CEO

Indicator variable with a value of 1 if the chairperson of the

board holds the managerial positions of CEO or president; 0

otherwise.

OpportunityIneffective

Monitoring

30

TABLE 4

Fraud Risk Factor Proxies for Rationalization

Fraud Risk

Factors

SAS No. 99

Categories Proxies Definition of proxies

AUDCHANG

A dummy variable for change in auditor where 1 = change in

auditor in the 2 years prior to fraud occurrence and 0 = no change

in auditor.

AUDREPORT

A dummy variable for an audit where 1 = an unqualified opinion

and 0 = an unqualified opinion with additional language.

TATA

Total accruals/total assets, where total accruals are calculated as

the change in current assets, minus the change in cash, minus

changes in current liabilities, plus the change in short-term debt,

minus depreciation and amortization expense, minus deferred tax

on earnings, plus equity in earnings.

Rationalization Rationalization

31

TABLE 5

Industry Representation of Fraud Firms

SIC Code Industry Title

Number of

Fraud Firms

Percent of

Sample

13 Crude Petroleum & Natural Gas 1 1.16%

15 Operative Builders 1 1.16%

16 Heavy Construction Other Than Building Construction 1 1.16%

20 Food and Kindred Products 1 1.16%

22 Knitting Mills 1 1.16%

23 Apparel & Other Finished Products of Fabrics 4 4.65%

27 Periodicals: Publishing or Publishing & Printing 1 1.16%

28 Chemicals & Allied Products 3 3.49%

31 Footwear 1 1.16%

34 Metal Products 3 3.49%

35 Computers & Communication Equipment 10 11.63%

36 Electrical Equipment 6 6.98%

37 Truck & Bus Bodies, Transportation Equipment 2 2.33%

38 Controlling, Surgical, & Photographic Devices 7 8.14%

50 Wholesale-Computers, Electrical, & Software 4 4.65%

51 Wholesale-Drugs & Petroleum Products 2 2.33%

53 Retail-Variety Stores 1 1.16%

56 Retail-Shoe Stores 1 1.16%

58 Retail-Eating Places 1 1.16%

59 Retail- Catalog, Drug Stores and Proprietary Stores 5 5.82%

73 Services-Business, Computer, & Equipment 24 27.91%

79 Services-Miscellaneous Amusement and Recreation 2 2.33%

80 Services-Health Services 4 4.65%

TOTAL 86 100.00%

32

TABLE 6

Sample Statistics

($ in hundreds of thousands)

Fraud Firms No-Fraud Firms

Mean Mean

[Median] [Median]

(Standard Deviation) (Standard Deviation)

Total Assets 1,420.10 797.91

[108.52] [88.90]

(4,414.39) (2,892.58)

n=86 n=86

Net Sales 1,627.76 1,049.42

[93.62] [93.21]

(5,537.39) (4,137.71)

n=86 n=86

Note: Paired t-tests and Wilcoxon matched-pair sign-rank tests indicated no significant differences

(p=0.10) between the fraud and no-fraud firms based on total assets and net sales.

33

TABLE 7

T-tests and Wilcoxon Sign-Rank Tests

Variable Mean Std Dev Mean Std Dev T Value Pr > |t | Z Pr > |Z|

NICFOTA -0.04 0.15 -0.03 0.28 -0.290 0.772 -1.824 0.034

SGROW -39.17 362.12 81.87 1250.00 -0.860 0.391 -1.429 0.077

AGROW 155.30 663.76 333.56 1679.90 -0.920 0.362 -1.814 0.035

SALAR 11.78 25.99 20.02 113.07 -0.660 0.511 2.075 0.019

SALTA 1.42 1.49 1.19 0.88 1.250 0.214 1.983 0.024

FREEC 15.89 170.69 -9.16 112.47 1.140 0.258 3.236 0.001

LEVERAGE 0.20 0.25 0.21 0.22 -0.220 0.826 -0.785 0.216

OWNERSHIP 0.23 0.20 0.20 0.19 0.950 0.345 1.069 0.143

5%OWN 0.21 0.21 0.32 0.23 -3.040 0.003 -3.173 0.001

ROA -4.25 34.23 -9.40 42.61 0.870 0.383 0.522 0.301

FOROPS -0.02 0.37 0.04 0.18 -1.170 0.245 0.664 0.254

BOUTP 0.69 0.18 0.64 0.19 1.510 0.132 1.717 0.043

AUDCOMM 0.99 0.11 0.88 0.32 2.850 0.005 2.793 0.003

AUDCSIZE 2.84 0.99 2.64 1.29 1.130 0.262 1.173 0.121

IND 0.88 0.25 0.68 0.39 3.880 <0.001 3.719 <0.001

AUDMEET 2.04 1.81 1.86 1.70 0.650 0.515 0.646 0.259

CEO 0.59 0.49 0.71 0.46 -1.600 0.111 -1.593 0.056

AUDCHANG 0.09 0.29 0.12 0.32 -0.500 0.621 -0.494 0.311

AUDREPORT 0.19 0.39 0.26 0.49 -1.030 0.304 -0.814 0.208

TATA -3.57 22.69 -93.85 851.02 0.980 0.328 -0.801 0.212

Wilcoxon t

Approximation

NO-FRAUD

FIRMS FRAUD FIRMS t-statistic

34

TABLE 8

Fraud Risk Factor Variables (p<0.15)

Fraud Risk

Factors Proxies

Fraud Risk

Factors Proxies

NICFOTA

SGROW

AGROW BOUTP

SALAR AUDCOMM

SALTA AUDCSIZE

FREEC IND

OWNERSHIP CEO

5%OWN

Pressure Opportunity

35

TABLE 9

Logit Regression: Fraud Risk Factor From Univariate Analysis

FRAUDi = β1NICFOTA + β2SGROW + β3AGROW + β4SALAR +β5SALTA + β6FREEC + β7OWNERSHIP + β85%OWN + β9BOUTP + β10AUDCOMM + β11AUDCSIZE + β12IND + β13CEO + ε

Variable Estimate

Standard

Error Chi-Square Pr > ChiSq

NICFOTA 0.6565 0.9091 0.5215 0.4702

SGROW -0.0001 0.0003 0.0695 0.7920

AGROW 0.0002 0.0003 0.6031 0.4374

SALAR 0.0011 0.0027 0.1582 0.6909

SALTA -0.2192 0.2087 1.1033 0.2935

FREEC -0.0016 0.0014 1.4779 0.2241

OWNERSHIP -3.4538 1.3482 6.5623 0.0104 **

5%OWN 4.7031 1.1750 16.0220 <0.0001 ***

BOUTP 0.6576 1.0677 0.3794 0.5379

AUDCOMM -2.4540 1.4529 2.8529 0.0912 *

AUDCSIZE 1.3423 1.1454 1.3733 0.2413

IND -1.7294 0.6741 6.5826 0.0103 **

CEO 0.7323 0.3921 3.4885 0.0618 *

Liklihood-Ratio 46.4041 ***

*p <0.10; **p <0.05; ***p <0.01. Based on two-sided tests.

36

TABLE 10

Discriminate Analysis and Fraud Prediction

FRAUDi = α + β1OWNERSHIPi + β25%OWNi + β3AUDCOMMi + β4INDi + β5CEO + εi

No-Fraud % Fraud % Total Error

No-Fraud % 74.42 25.58 30.23

Fraud % 34.88 65.12

Cross-validation Method

37

FIGURE 1

Effect of Independent Audit Committee Membership on the

Probability of Fraud

Effect of Independence of Audit Committe Members

on the Probability of Being in the Fraud Group

0%

5%

10%

15%

20%

25%

30%

35%

40%

0% 20% 40% 60% 80% 100%

Proportion of Audit Committee Members that are

Independent of the Firm

Pro

bab

ilit

y o

f B

ein

g in

th

e

Fra

ud

Gro

up

Effect of Change in IND on probability of Fraud

Mean IND all firms

Fraud Firms IND Mean

No-Fraud Firms IND Mean

38

FIGURE 2

Effect of Management Ownership on the Probability of Fraud

Effect of Management Ownership (5%OWN ) on the

Probability of Being in the Fraud Group

0%

20%

40%

60%

80%

100%

0% 20% 40% 60% 80% 100%

Proportion of outstanding shares held by managers

holding at least 5 percent of the outstanding shares

Pro

bab

ilit

y o

f B

ein

g in

th

e

Fra

ud

Gro

up

Effect of Change in 5%OWN on probability of Fraud

Mean 5%OWN all firms

Fraud Firms 5%OWN Mean

No-Fraud Firms 5%OWN Mean

39

FIGURE 3

Effect of Ownership on the Probability of Fraud

Effect of Inside Ownership (OWNERSHIP ) on the

Probability of Being in the Fraud Group

0%

5%

10%

15%

20%

25%

30%

35%

40%

0% 20% 40% 60% 80% 100%

Proportion of Outstanding Shares Held by Insiders

(Directors, Managers, etc.)

Pro

bab

ilit

y o

f B

ein

g in

th

e

Fra

ud

Gro

up

Effect of Change in OWNERSHIP on probability of Fraud

Mean OWNERSHIP all firms

Fraud Firms OWNERSHIP Mean

No-Fraud Firms OWNERSHIP Mean

40

FIGURE 4

Effect of CEO/Chairman of the Board Positions on the Probability of Fraud

Effect of CEO and Chairman of the Board Position

being held by the same Individual (CEO ) on the

Probability of Being in the Fraud Group

0%

10%

20%

30%

40%

50%

Dummy Variable, where a value of 1 indicates the CEO

holds the Chairman of the Board title and a value of 0

indicates the title is not held.

Pro

bab

ilit

y o

f B

ein

g in

th

e

Fra

ud

Gro

up

The Effect of holding both the CEO and Chairman of the Board

Position at the same time on the probability of Fraud

10

41

FIGURE 5

Effect of having an Audit Committee on the Probability of Fraud

Effect of having an Audit Committee (AUDCOMM ) on

the Probability of Being in the Fraud Group

0%

10%

20%

30%

40%

50%

Dummy Variable, where a value of 1 indicates existence of

an Audit Committee and a value of 0 indicates no audit

committee.

Pro

bab

ilit

y o

f B

ein

g in

th

e F

rau

d

Gro

up

The Effect of having an Audit Committee on the probability of

Fraud.

10