ambit insightsreports.ambitcapital.com/reports/ambitinsights_10aug2016.pdf · icici pru life n/a...

TRANSCRIPT

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Please refer to the Disclaimers at the end of this Report.

AMBIT INSIGHTS 10 August 2016

DAILY

Potential Sensex entrants by 2025

Company Name Ambit Stance

Mcap (US$ mn)

6M ADV (US$ mn)

Kotak Mah. Bank SELL 20,995 20.9

HCL Technologies BUY 17,239 29.4

Asian Paints BUY 16,452 15.8

IndusInd Bank BUY 10,574 23.2

Nestle India SELL 9,941 4.2

Eicher Motors SELL 8,973 18.9

Pidilite Inds. NR 5,548 7.9

Torrent Pharma. NR 3,801 3.6

Page Industries BUY 2,354 2.5

P I Inds. BUY 1,606 1.7

Cafe Coffee Day NR 743 0.5

Flipkart N/A N/A N/A

Paytm N/A N/A N/A

ICICI Pru Life N/A N/A N/A

Hind.Aeronautics N/A N/A N/A

Source: Bloomberg, Ambit Capital research

Note: NR indicates Not Rated, N/A indicates data not available since companies are not yet listed

For detailed discussion on these names, please refer our note on ’The Sensex in 2025’ dated June 22, 2015

Pre-IPO Note

RBL Bank (NOT RATED)

An uphill transition path ahead

(Click here for detailed note)

Updates

Cement

Don’t disembark yet

(Click here for detailed note)

Consumer Staples

Separating the Push from the Pull

Economy

The room for incremental rate cuts remains limited

Results Expectation

Thermax: (SELL, 33% downside)

Analyst Notes: Strategy: The HAWK looks at capital allocation Saurabh Mukherjea, CFA, +91 22 3043 3174

Capital allocation is arguably the most neglected aspect of investment analysis. Most investors agonise endlessly about P/E multiples. The more diligent ones use primary data sources to understand a company's competitive advantages. But very few investors properly scrutinise a company's cross-cycle capital allocation. This neglect arises from three factors: (a) cross-cycle capital allocation is a data-intensive, laborious exercise involving analysis of the uses and sources of cash over 10 years; (b) in such analysis, it's hard to disentangle the impact of the economic cycle from the impact of management skill; and (c) leaving aside the business cycle, it's hard to distinguish between management's skill and luck when it comes to the outcomes produced by capital allocation. As a result of investor neglect of capital allocation, companies with indifferent long-term track records get re-rated at the first sign of the economic cycle turning-contemporary examples would be ICICI, RIL and Ramco Cements. To help our clients readily access the 10-year capital allocation track records of the 1000 largest listed companies in India, we launched the HAWK last month. The website is hawk.ambit.co and your Ambit salesperson can give you the username and password. Source: Ambit Capital research

Please refer to our website for complete coverage universe

http://research.ambitcapital.com

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

An uphill transition path ahead

RBL Bank’s spectacular balance sheet growth (FY13-16 CAGR: 53%) has been driven by high reliance on the wholesale banking model. However, RoA/RoE appear to be hitting air-pockets on NIM and cost-income-ratio. The bank needs to build a granular balance sheet to lift NIM, but its already high cost-to-income ratio (disappointing given the current wholesale focus) and limited track record in that direction make the progress suspect. Asset quality trends are healthy so far, but concentration in sectors like construction and MFIs betrays a lack of strong niche. We struggle to justify a valuation more than 2x FY17BV using peer benchmarking, which supports an issue price of ~`205/share.

Explosive growth; but profitability is still underwhelming

Since the new management took charge in 2010, RBL Bank’s assets have grown 12x but with little change in its wholesale banking character. The bank compares well with peers on asset quality despite a few pockets of concentration in sectors like construction (6% of total exposure) and MFIs (5% of total exposure). RoAs have been unchanged at ~1% in recent years as NIM (3.1%) and cost-to-income (~60%) have become sticky. Wholesale model caps NIM outlook

Short-tenor wholesale lending limits yield on loans (~10.9%). Low-cost liability, unsurprisingly, has lagged rapid balance sheet growth. Poor mobilization of retail liabilities makes the bank seemingly carry excess SLR (26% of assets) to meet regulatory liquidity requirement. The resultant drag on spread is thus highest among peers. NIM (~3.1%), thus, will not increase unless granular high yielding asset book and low cost deposits franchise are beefed up. Limited progress in expanding distribution, yet high cost ratios

Cost-to-income ratio has been unchanged at 59-60% in last four years despite muted branch expansion. The cost model also indicates sub-scale front-line staff and material reliance on intermediaries for origination. Heavy use of ESOPs to reward management team would also come under pressure in IFRS accounting from FY19, which could have 5-6% impact on reported EPS. Benchmarking with peers on valuation

DCB Bank (similar profitability but superior earnings quality) and Yes Bank (early reliance on corporate & commercial banking) appear to be the closest peers. DCB trades at ~1.7x FY17 BV and Yes (with almost double the RoEs) trades at 3.0x. Thus, 2x should form the ceiling for valuations, in our view. At 2x FY17 BVPS (pre-money), RBL’s share price would be ~`205.

PRE-IPO NOTE August 10, 2016

RBL BankNOT RATED

Research Analysts

Ravi Singh

+91 22 3043 3181

Pankaj Agarwal, CFA

+91 22 3043 3206 [email protected]

Rahil Shah +91 22 3043 3239

Key financials Year to March FY12 FY13 FY14 FY15 FY16

Net Interest Income (̀ mn) 1,868 2,575 3,416 5,564 8,192

Operating Profits (` mn) 1,148 1,567 2,406 3,601 5,424

Net Profits (` mn) - adj 657 925 1,336 2,072 2,925

EPS (`) - adj 3.1 3.7 4.9 7.1 9.0

RoA (%) 1.26% 0.92% 0.86% 0.91% 0.88%

RoE (%) 5.9% 6.7% 7.4% 9.8% 11.2%

Div. payout ratio 11% 19% 31% 21% 20%

Source: Company, Ambit Capital research

BFSI

RBL Bank IPO: Fresh issue Net worth (FY16, ̀ mn) 29,882

No. of shares (FY16, mn) 325

BVPS (FY16, ̀ ) 92

Fresh issue (` mn) 11,000

Assumed issue price (`) 205

No. of fresh new shares (mn) 54

Dilution 17%

Net worth - post issue (` mn) 40,882

No. of shares - post issue (mn) 378

BVPS - post issue (`) 108

BV accretion 17%

P/B - pre issue (x) 2.2

P/B - post issue (x) 1.9

Note: The issue price of `205 is indicative price based on our expectation. The pre-IPO capital infusion in December 2015 took place at valuation of `200/share.

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Don’t disembark yet

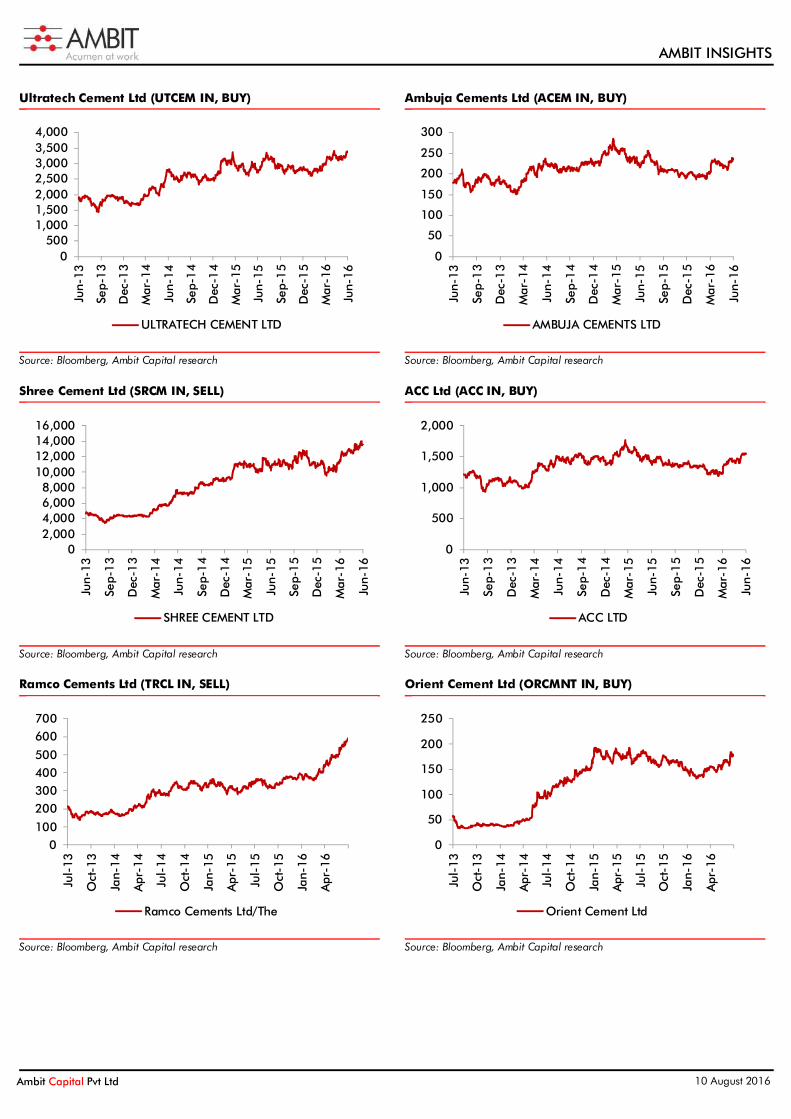

Sector’s recent outperformance (30% relative to Sensex) was driven by earnings acceleration after sharp downgrades in FY16. Whilst volume growth is stuck in mid-single-digit range and sharp increase in petcoke prices (since Mar 2016) will dilute power/fuel savings (by ~Rs100/tonne in 2HFY17), we expect pricing discipline to sustain as companies shift focus from market-share wars to cash flows and balance-sheet improvement. So, we expect 35% EBITDA CAGR over FY16-18 for six companies under coverage (vs -6% over FY13-16) and RoCE to improve to 20% in FY19 (11% in FY16). Current multiples (11-15x FY18E EV/EBITDA) should sustain as volume recovery and, more importantly, pricing recovery drive earnings growth, a missing feature in the past few years. Retain BUY on pan-India players for pricing-led earnings recovery; Orient is top mid-cap pick given highest operating/financial leverage.

All cylinders haven’t started firing yet Cement demand growth decelerated to 6% YoY in 1QFY17 (+13% YoY in 4QFY16); despite good monsoon we do not expect volume growth to exceed 6%/8% in FY17/FY18. Pricing has recovered in certain pockets (North/Central India) and we believe other weak markets like Maharashtra (pricing down –15% YoY) will follow as demand stabilizes and market-share battles recede. Though fuel price increase will inflate costs by ~3% as against 1QFY17, we expect costs/tonne to decline by 1-2% in FY17 led by operating leverage and fuel/freight mix optimization by cement companies. Changing focus – from scale to sustainability Recent channel interaction and annual report commentary suggest after satiating scale aspirations, companies now focus on deleveraging and cost efficiencies. Equipment vendors highlight recent orders were largely for efficiency enhancement/upgrade of machinery rather than new capacities. This shift will support pricing discipline, trim balance sheets and drive pre-tax RoCE recovery to 20% by FY19 (vs 12% in FY16). End of the capex and earnings downgrade cycle After sharp earnings downgrades in the last two years, we notice that consensus estimates for FY17 and FY18 have seen marginal upgrades (+1-7%) post 1Q results. We see more upgrades as we expect 30% EBITDA CAGR for coverage universe. We note that years of strong pricing were followed by sharp earnings upgrades by consensus (and vice versa); our estimates are 5-20% higher than consensus led by higher pricing assumption. Orient has lost favor with investors due to sharp realization/unitary EBITDA decline, but pricing recovery in core markets can drive sharp pick-up in EBITDA growth (akin to North-based players); Ambuja, ACC and UltraTech will also benefit from West region pricing recovery. Rich valuations will be supported by strong earnings momentum Front-line cement stocks currently trade at 11-15x FY18E EV/EBITDA – a significant premium to five-year averages. Post the recent outperformance, near-term returns may be capped for the pan-India cement companies but we note that valuation multiples appear deceptively expensive in periods of sharp earnings revival but multiples remain elevated so long as earning momentum remains strong. Reiterate BUY on UltraTech, ACC and Ambuja amongst large-caps; Orient Cement remains our top mid-cap pick.

SECTOR UPDATE August 10, 2016

CementPOSITIVE

Key Recommendations

UltraTech Cement BUY

Target Price: 4,172 Upside 10%

Ambuja Cement BUY

Target Price: 299 Upside: 11%

ACC BUY

Target Price: 1,873 Upside: 11%

Shree Cement SELL

Target Price: 10,914 Downside: 36%

Ramco Cement SELL

Target Price: 371 Downside: 34%

Orient Cement BUY

Target Price: 190 Upside: 16%

Research Analysts

Nitin Bhasin +91 22 3043 3241

Achint Bhagat, CFA

+91 22 3043 3178

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Consumer Staples Separating the Push from the Pull Ind AS has reclassified A&P spends into trade (push-based) and consumer oriented (pull-based) spends. According to us, factors that determine choice between push-based vs pull-based approaches are: rural exposure, commodity/value-added nature of products, ability to cross-sell brands and nature of sales channel. While both push and pull are necessary, pull-based spends tend to create sustainable demand while push-based drives more temporary demand. Analysis of FY16 accounts of companies under coverage suggests HUL/Marico have higher proportion of pull-based spends (80-85%) vs Dabur and GCPL (50-55%). Leveraging scale of brands to cross-sell, higher direct reach and control on channel with IT tools help HUL and Marico lower push spends and dedicate more spends for consumer-pull generation. In the longer term, as technology and GST neutralize distribution as a competitive advantage, we believe pull-oriented companies like HUL/Marico have a higher probability of growing ahead of market than push-oriented ones like GCPL/Dabur. BUY HUL (TP Rs990) and Marico (TP Rs330).

A&P reclassification under Ind AS – split of PUSH and PULL related spends Under Ind AS reporting standards, companies have had to split their Advertising and Promotion (A&P) spends into the following two components:

Spends to generate ‘push-based’ demand: All trade-related A&P spends now need to be netted off directly from sales (instead of reporting them as part of A&P spends and other expenses). These expenses include: a) discounts/rebates/promotions (foreign trips, gifts etc.) given to distributors or wholesalers; and b) visibility and listing fees paid to general and modern trade. These spends are intended to incentivise the channel partners to push the company’s products, i.e. through these spends, a staples company attempts to convince the retailer/ distributor to stock their products.

Spends to generate ‘pull-based’ demand: Once the trade-related spends are netted off from sales, what is reported under ‘A&P’ spends largely includes advertising costs and consumer promotion spends. These are intended to generate a consumer-pull for the products, i.e. these are advertising spends targeted at the consumer so that s/he comes to the retailer asking for the company’s products.

Pull promotions are done to bring the consumer to the retailer asking for the brand

Source: http://goo.gl/3Ve9Fs

POSITIVE Quick Insight

Analysis Meeting Note News Impact

Marico BUY Bloomberg Code: MRCO IN

CMP (Rs): 294

TP (Rs): 330

Mcap (Rs bn/US$ bn): 380/5.7

3M ADV (Rs mn/US$ mn): 293/4.4

HUL BUY Bloomberg Code: HUVR IN

CMP (Rs): 934

TP (Rs): 990

Mcap (Rs bn/US$ bn): 1,995/29.7

3M ADV (Rs mn/US$ mn): 1,330/19.8

Research Analysts

Ritesh Vaidya, CFA [email protected] Tel: +91 22 3043 3246

Rakshit Ranjan, CFA [email protected] Tel: +91 22 3043 3201

Dhiraj Mistry, CFA [email protected] Tel: +91 22 3043 3264

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Factors driving ‘push’ vs ‘pull’ based marketing spends A company needs to have a mix of both push and pull based A&P spends. The factors driving them are given below:

Higher rural exposure = higher push-based spends: In rural areas, the brand awareness of consumers is lesser than that seen in urban areas. Availability of the product plays a major role in driving sales in rural areas. Hence, companies try to do higher trade promotions to convince the distributor or wholesaler to stock and push their products vs that of the competitor. In case of urban consumers, the purchase decision is more evolved as he/she is more exposed to different forms of media. Hence, the company has to do higher advertising spends to create a pull for its products in urban areas.

For e.g, Dabur, which has higher rural exposure, tends to do higher push-based A&P spends. An exception to this rule is HUL - according to our channel checks, due to decades of brand-level investments by HUL, it has managed to create a pull for its brands even in rural areas.

Nature of new/existing products – commodity/value added: In order to drive sales of nascent brands, companies usually have to do higher trade spends to convince the trade to stock them. This is particularly true when the newly launched product is differentiated compared to the ones already there in the market. In case of a differentiated product launch, the company focuses mostly on pull-based spends to create demand for the product.

For e.g. the success of Fogg deodorants by Vini Cosmetics was driven entirely by pull-based spends. Our channel checks suggest that due to the innovation offered by Vini Cosmetics in Fogg (non-aerosol deodorants), the company spent almost its entire A&P budget on advertising in creating a pull for its product. The success of Fogg has meant that although Vini Cosmetics offers lower retailer and distributor margin, the retailer stocks its products as there consumer pull for the product.

On the other hand, in case of launch of a regional hair oil, due to less product differentiation, Dabur or Marico will have to support consumer promotions with an equivalent amount of trade promotions.

The same is also true for the existing product portfolio of a company. If the company hasn’t been to create sufficient brand equity for its existing brands and instead relied on trade push to drive its sales then it will have a high proportion of push-based promotions. For e.g., in the soaps and detergents category where there is less product differentiation at least at the mass end in rural areas, companies tend to rely on higher trade promotions to drive sales.

Ability to cross-sell brands: If a company has been able to create large brands with high consumer pull, the brand equity of these brands can be leveraged to convince the trade to stock new brands.

For e.g., ITC leverages its market dominance in the cigarettes category to convince the distributor/retailer to stock ITC’s other FMCG products.

Marico leverages the scale of Parachute and Saffola to convince the distributor/retailer to stock its other products as well.

HUL uses the scale of its soaps and detergents portfolio to drive sales of its other smaller brands to distributors.

In case of GSK and Colgate, the base variant contributes ~50% of sales. These companies use the strength of this variant to drive stocking of its other variants.

The money saved in trade spends by these companies is used in creating consumer pull through advertising spends.

However, Dabur which has focused on a multi-brand strategy instead of creating 1-2 large brands isn’t able to leverage the scale of its brands to the extent that a ITC/HUL/Marico are able to leverage.

“If Dabur can offer the rural sub-stockist/wholesaler higher rebate on sale of Babool then he will stock and push Babool over a Cibaca” - Distributor in North India

“A Parle distributor has to buy certain minimum quantity of the confectionaries if he wants to buy Parle G.” – Parle distributor in West India

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Exhibit 1: HUL, Marico have majority sales coming from large brands while Dabur has created several small brands

Number of brands having market size

Company >Rs20bn >Rs10bn >Rs5bn >Rs1bn

HUL 6 5 Marico 1 1 1 2

GCPL 2 3 1

Britannia 1 3 2 3

Dabur 3 14

GSK Consumer 1 Colgate 1 Source: Company, Ambit Capital research

Nature and sophistication of distribution channel: Higher the direct reach of a company lower are the trade spends needed. Hence, companies relying more on the wholesale channel have to do higher trade spends to drive sales. These companies give the wholesaler rebates to drive sales.

Companies which manage their sales in a better manner through the entire month have to rely less on trade spends to achieve their monthly sales targets. Some companies have a culture of dumping stock on to the distributors or the wholesale channel towards the end of the month by offering them higher trade rebates. These companies have high proportion of push-based promotions. On the other hand, companies which have migrated to better IT-supported Vendor Inventory Management systems are able to have a more even sales pattern through the pattern. So they don’t have to do higher trade spends to achieve sales targets.

For e.g., Marico has always focused on having a smoothened sales run-rate through the month. It makes use of several IT tools to achieve this. As a result, the company doesn’t have to dump stock towards the end of the month to achieve sales targets and hence has lower trade spends which can be used for pull-generating spends.

Pull helps in creating sustainable demand than Push

While both push and pull-based spends are needed, pull-based spends help in improving the equity of a company’s brands and hence help in creating sustainable demand for the brand. Once the brand attains critical mass, the pull-based spends can be reduced on the brand and instead used to push sales of some other brand. Push-based spends help in creating temporary demand and once they are withdrawn the sales of the brand reduce. Hence, the company will have to maintain push-based spends to drive sales of the brand.

Analysing ‘push’ vs ‘pull’ for stocks under our coverage HUL and Marico spend higher proportion of A&P on PULL-based spends; Dabur and GCPL spend lower

Using the reconciliation of A&P spends between IGAAP and Ind AS, we have calculated the push/pull spend split for companies for FY16 in the table below. As the reconciliation has been provided only for FY16, we cannot know the historical split of the A&P spends.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Exhibit 2: HUL, Marico, GSK Consumer and Colgate have higher proportion of pull spends; Dabur, GCPL and Britannia higher push-spends

Companies A&P split for FY16

% rural sales Pull-based Push-based

HUL 80% 20% ~45%

Marico – Consolidated 84% 16%

Standalone 83% 17% ~34%

International 89% 11%

GSK Consumer* 78% 22% ~25%

GCPL – Consolidated 54% 46%

Standalone 65% 35% ~25%

International 37% 63%

Dabur – Consolidated 55% 45%

Standalone 56% 44% ~50%

International 53% 47%

Britannia - Consolidated 59% 41%

Standalone 63% 37% ~30%

International 40% 60%

Colgate* 61% 39% ~35%

Source: Company, Ambit Capital research *Note: For GSK Consumer and Colgate the analysis is based on 1QFY16 as the companies haven’t yet reported Ind AS accounts for FY16

Some key points to note from the table above are:

Dabur, despite its higher proportion of rural spends, seems to be over-spending on push-based spends compared to peers. Push-based spends are high for Dabur in both its Indian and International business. Lack of 1-2 big brands and a higher wholesale channel focus seem to be contributing to Dabur’s higher push-based spends.

GCPL’s India business spends ~65% of total A&P spends on pull-based promotions. We believe these are higher due to push-based spends needed for its soaps portfolio where the company has little differentiation and is a distant #2 in the category. The international business has a high proportion of push-based A&P spends due to presence in geographies like Africa where there is lack of consumerism and hence companies have to rely on push to drive sales.

While Britannia has the advantage of being in a single category and also being the category leader, we believe the impulse consumption nature of biscuits means that Britannia has to spend more on trade. Higher focus on rural markets could also be driving push-based spends for the company.

Marico has a high proportion of pull-based spends as the company has followed a focused brand strategy, which has helped it create large brands in Parachute, Saffola and Nihar, enabling it cross-sell brands. Also, the sophistication of Marico’s sales system has ensured that it doesn’t have to offer higher trade discounts during the end of the month to achieve its sales targets.

Despite having among the highest rural exposures, HUL uses most of its A&P spends on pull. It has leveraged the scale of its brands and decades of brand-building to create a consumer pull for its brands.

Marico and HUL better placed on a long-term perspective

Based on the factors driving push and pull spends, we believe the proportion of their spends can be one of the factors which can help us in understanding if a company is more sales or marketing driven. As a result, Dabur’s marketing spends appear to be more sales-oriented, while Marico and HUL appear to be more marketing-oriented firms. Over the longer term, we believe technology and GST can partly dilute the extent to which distribution is a competitive advantage for staples companies by allowing faster access to market for any brand. In such a scenario, we believe companies with a pull-based tilt have a higher probability of growing ahead of the market than sales-oriented organisations.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

TOP BUYs – Marico and HUL Marico (BUY, TP Rs330, 13% upside)

Marico has maintained leadership in its core categories through: (a) a unique work culture which has enabled the firm to attract and retain high quality talent; (b) a high quality Board which is truly ‘independent’ in helping drive strategic decision-making; and (c) a strong focus on building supportive relationships with its distributors. Over the next five years, we expect the firm to successfully evolve around: (a) product innovation in the non-coconut oil portfolio; (b) nurturing high-quality talent; and (c) better use of IT and data analytics. We expect Marico to deliver FY16-20 sales/EPS CAGR of 18%/27% with RoCE improving from 33% to ~44% over the same period. Our DCF-based TP of Rs330 implies FY18E P/E of 35x.

HUL (BUY, TP Rs990, 6% upside)

The rollout of subsidies on the Direct Benefit Transfer (DBT) platform from FY17 is likely to result in an increase in disposable income for target households. Hindustan Unilever is best positioned to capitalize on these benefits due to: a) its highest proportion of rural sales, b) high exposure to the most-functional staples categories (like soaps, detergents, shampoos, and oral care), and c) the increase in the width and depth of its distribution network over the past 3-4 years. Given the benefit that HUL can derive from DBT-induced pick-up in rural demand from 2HFY17, we expect HUL to deliver sales/EPS growth of 15%/21% over FY16-FY20 with >100% RoCE. Our fair value of Rs990/share implies FY18E P/E of 36x

Exhibit 3: Relative valuations – HUL and Marico remain our TOP BUYs

Relative valuations

CMP Mcap Stance

Target Price

Up / Down

P/E based on CMP

EV/EBITDA ROCE (%) Implied P/E based on TP

Div. Yield (%)

Rev growth

EPS Growth

(Rs) (LC bn) FY17E FY18E FY17E FY18E FY17E FY18E FY17E FY18E FY16 FY16-19 FY16-19

Staples

HUL 934 2,022 BUY 990 6% 40.7 33.6 29.2 24.1 122.7 129.9 43.1 35.6 1.7% 14.7% 21.5%

Nestle 6,892 665 SELL 6,300 -9% 53.7 41.0 31.0 23.9 38.8 44.4 49.0 37.4 0.6% 17.5% 21.4%

GSK Consumer 6,266 264 SELL 5,650 -10% 36.5 32.2 33.0 27.6 28.7 28.3 32.9 29.0 1.1% 14.3% 11.9%

Colgate 971 264 SELL 895 -8% 39.0 33.0 24.5 20.3 60.2 61.0 35.9 30.4 1.0% 14.8% 17.3%

Godrej Consumer 1,530 521 SELL 1,116 -27% 37.9 34.2 28.3 24.3 17.0 16.2 27.7 25.0 0.4% 15.2% 14.6%

Dabur 289 509 SELL 292 1% 36.0 30.5 27.5 23.1 26.7 27.4 36.3 30.8 0.8% 16.1% 16.2%

Marico 294 380 BUY 330 12% 40.9 31.6 27.5 21.7 38.6 41.9 45.8 35.4 0.8% 17.5% 27.8%

Britannia 3,128 375 SELL 2,750 -12% 39.2 33.2 24.8 21.1 46.5 44.5 34.5 29.1 0.6% 15.8% 17.7%

ITC 248 2,989 BUY 292 18% 26.8 23.7 17.5 15.1 30.5 31.6 31.7 28.0 2.3% 14.5% 13.1%

Median -8% 39.0 33.0 27.5 23.1 38.6 41.9 35.9 30.4 0.8% 15.2% 17.3%

Source: Ambit Capital research

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Economy The room for incremental rate cuts remains limited As expected, the RBI kept the repo rate unchanged at 6.5% at its monetary policy review held yesterday. We reiterate our view that we expect limited rate cuts (0-25bps) to be administered over FY17. Even as there have been two positive changes that have transpired regarding the monetary policy framework in India recently, namely: (1) the monetary policy committee appears likely to be a relatively independent body given the stringent criteria laid out for the eligibility criteria for the choice of external members (click here for our 8th August note); and (2) the Government has re-instated the CPI inflation target of 4% (+/-2%) for the RBI, our main concern remains that the MPC as a group runs the risk of being less accountable as compared to a single Governor.

The event

In-line with our expectations, the RBI kept the repo rate unchanged at 6.5% at its monetary policy review held yesterday. The RBI also kept the CRR and SLR unchanged at 4% and 21.25% respectively. More importantly, the RBI reiterated its stance on liquidity, i.e. that the Reserve Bank intends to continue with its strategy of closing the underlying liquidity deficit over time so that the system moves to a position of structural balance. RBI to transition to the new monetary policy framework by the next review

The Governor in the press conference following the release of the policy statement made the point that the process of selecting the members of MPC has started and the next monetary policy scheduled for 4 Oct 2016 will be decided by the “Monetary Policy Committee” (MPC). The Governor made the point that apart from the Governor and the Deputy Governor in-charge of monetary policy, the RBI has appointed Dr. Michael Patra (i.e. Executive Director in-charge of monetary policy) as the third member of the MPC. As highlighted in our note dated Aug 08, 2016 the Government has appointed a selection committee for picking the external members and these members are likely to be announced by end-August 2016.

As highlighted in our note dated August 08, given that the eligibility criteria for the external members are highly restrictive (which debars public servants from being external members) only high quality economists or former RBI employees appear to have a chance of making it to the MPC as external members. Whilst this partially allays our worries regarding the independence of the MPC, the only concern now remains regarding accountability. Even as the MPC is required to explain to Parliament if it misses the target for 3 consecutive quarters, we worry about the accountability ‘in spirit’ as: (1) a group is likely to be less accountable as compared to a single governor keen to create a legacy with his personal credibility at stake; and (2) there is no real penalty for missing the inflation target.

What was the RBI’s rationale for maintaining status quo?

The policy statement made the point that, “The recent sharper-than-anticipated increase in food prices has pushed up the projected trajectory of inflation over the rest of the year. Moreover, prices of pulses and cereals are rising and services inflation remains somewhat sticky. The prospects for inflation excluding food and fuel are more uncertain; if the current softness in crude prices proves to be transient and as the output gap continues to close, inflation excluding food and fuel may likely trend upwards and counterbalance the benefit of the expected easing of food inflation.”

Quick Insight Analysis Meeting Note News Impact

Analysts

Ritika Mankar Mukherjee, CFA [email protected] Tel: +91 22 30433175

Sumit Shekhar [email protected] Tel: +91 22 3043 3229

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

What is the RBI’s view on GDP growth and inflation?

The RBI expects inflation to be around 5% YoY by the end-FY17 (unchanged from previous policy review) (vs Ambit’s estimate of average inflation of ~5.8% YoY in FY17) but highlighted upside risks to the same and made the point that, “Risks to the inflation target of 5% for March 2017 continue to be on the upside. Furthermore, while the direct statistical effect of house rent allowances under the 7th CPC’s award may be looked through, its impact on inflation expectations will have to be carefully monitored so as to pre-empt a generalisation of inflation pressures” (see exhibit below).

As regards GDP growth, the RBI kept its GDP forecast unchanged at 7.6% YoY for FY17 (vs Ambit estimate of 6.8% YoY) and made the point that, “Looking ahead, the momentum of growth is expected to be quickened by the normal monsoon raising agricultural growth and rural demand, as well as by the stimulus to consumption spending that can be expected from the disbursement of pay, pension and arrears following the implementation of the 7th PC’s award” (see exhibit below).

Exhibit 1: The RBI highlighted upside risk to its inflation forecast for FY17…

Source: RBI, Ambit Capital research

Exhibit 2: … whilst maintaining its GDP forecast for FY17 at 7.6% YoY

Source: RBI, Ambit Capital research

What is the RBI’s view on liquidity? The RBI highlighted that it will work towards provision of adequate liquidly in the system and made the point that, “Liquidity conditions eased significantly during June and July on the back of increased spending by the Government which more than offset the reduction in market liquidity because of higher-than-usual currency demand. The injection of durable liquidity through purchases under open market operations (OMOs), amounting to ₹ 805 billion so far, also helped in easing liquidity conditions, bringing the system-level ex ante liquidity deficit to close to neutrality” Further, the RBI made the point that as the liquidity deficit came close to neutrality due the above mentioned steps, the average daily liquidity operation switched from injection of Rs370bn in June to absorption of Rs141bn in July and Rs405bn in August. Where do we go from here? As highlighted earlier we expect limited rate cuts (to the tune of 0-25bps) to be administered over FY17 because: (1) inflation is likely to remain sticky at 5.5-6% in FY17, and (2) it would make sense for the RBI to signal to the Central Government (by not cutting rates) that its fiscal maths appear overly ambitious for FY17.

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Thermax: 1QFY17 results expectation (TMX IN, mcap US$1.6bn, SELL, TP Rs607, 33% downside)

Analyst: Bhargav Buddhadev, [email protected], +91 22 3043 3252

Thermax will announce its 1QFY17 results today. We expect revenue to decline by 8% YoY to Rs9.2bn led by lower opening order book at Rs37bn (down 15% YoY) in 1QFY17. Whilst we expect gross margin improvement of 140bps YoY due to fall in commodity prices, EBITDA margin should decline by 70bps YoY to 8.4% given unfavourable operating leverage. Consequently, we expect EBITDA/PBT/PAT to decline by 14% YoY to Rs771mn/Rs787mn/Rs527mn. Whilst our revenue estimate is in-line with consensus, our EBITDA estimate is 8% below consensus.

Thermax is trading at stretched valuations of 32x FY18 P/E and 3.8x FY18 P/B despite FY16-FY18 RoE at 11%, which is lower than cost of equity of 15%.

Key metrics to watch for: (1) order intake during the quarter; (2) status of the Thermax-Babcock Wilcox JV; and (3) cash conversion cycle.

Exhibit 1: Results expectations (Rs mn, unless specified)

Particulars Jun'16E Jun'15 Mar'16 YoY QoQ Comment

Sales 9,211 10,012 12,932 -8% -29% Decline in revenue led by lower opening order book at Rs37bn (down 15% YoY) in 1QFY17.

EBITDA 771 910 1,182 -15% -35% Whilst we expect gross margin improvement of 140bps YoY due to fall in commodity prices, we expect EBITDA margin to decline by 70bps YoY given the unfavourable operating leverage EBITDA margin (%) 8.4% 9.1% 9.1% -70bps -70bps

PBT 787 919 1,524 -14% -48% Trickle-down impact of lower EBITDA

APAT 527 617 1,112 -14% -53% Trickle down impact of lower PBT

Source: Company, Ambit Capital research

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Institutional Equities Team Saurabh Mukherjea, CFA CEO, Institutional Equities (022) 30433174 [email protected]

Research Analysts

Name Industry Sectors Desk-Phone E-mail

Nitin Bhasin - Head of Research E&C / Infra / Cement / Industrials (022) 30433241 [email protected]

Aadesh Mehta, CFA Banking / Financial Services (022) 30433239 [email protected]

Aakash Adukia Oil & Gas / Chemicals / Agri Inputs (022) 30433273 [email protected]

Abhishek Ranganathan, CFA Retail (022) 30433085 [email protected]

Achint Bhagat, CFA Cement / Home Building (022) 30433178 [email protected]

Anuj Bansal Mid-caps (022) 30433122 [email protected] Ashvin Shetty, CFA Automobile (022) 30433285 [email protected]

Bhargav Buddhadev Power Utilities / Capital Goods (022) 30433252 [email protected]

Deepesh Agarwal, CFA Power Utilities / Capital Goods (022) 30433275 [email protected] Dhiraj Mistry, CFA Consumer (022) 30433264 [email protected]

Gaurav Khandelwal, CFA Automobile (022) 30433132 [email protected] Girisha Saraf Mid-caps / Small-caps (022) 30433211 [email protected]

Karan Khanna, CFA Strategy (022) 30433251 [email protected]

Kushank Poddar Technology (022) 30433203 [email protected] Pankaj Agarwal, CFA Banking / Financial Services (022) 30433206 [email protected]

Paresh Dave, CFA Healthcare (022) 30433212 [email protected]

Parita Ashar, CFA Metals & Mining / Aviation (022) 30433223 [email protected]

Prashant Mittal, CFA Strategy / Derivatives (022) 30433218 [email protected]

Rahil Shah Banking / Financial Services (022) 30433217 [email protected]

Rakshit Ranjan, CFA Consumer (022) 30433201 [email protected]

Ravi Singh Banking / Financial Services (022) 30433181 [email protected]

Ritesh Gupta, CFA Oil & Gas / Chemicals / Agri Inputs (022) 30433242 [email protected]

Ritesh Vaidya, CFA Consumer (022) 30433246 [email protected] Ritika Mankar Mukherjee, CFA Economy / Strategy (022) 30433175 [email protected]

Ritu Modi Automobile (022) 30433292 [email protected]

Sagar Rastogi Technology (022) 30433291 [email protected]

Sumit Shekhar Economy / Strategy (022) 30433229 [email protected]

Utsav Mehta, CFA E&C / Industrials (022) 30433209 [email protected]

Vivekanand Subbaraman, CFA Media (022) 30433261 [email protected]

Sales

Name Regions Desk-Phone E-mail

Sarojini Ramachandran - Head of Sales UK +44 (0) 20 7614 8374 [email protected]

Dharmen Shah India / Asia (022) 30433289 [email protected]

Dipti Mehta India / USA (022) 30433053 [email protected]

Hitakshi Mehra India (022) 30433204 [email protected]

Krishnan V India / Asia (022) 30433295 [email protected]

Nityam Shah, CFA USA / Europe (022) 30433259 [email protected]

Parees Purohit, CFA UK / USA (022) 30433169 [email protected]

Praveena Pattabiraman India / Asia (022) 30433268 [email protected]

Shaleen Silori India (022) 30433256 [email protected]

Singapore

Pramod Gubbi, CFA – Director Singapore +65 8606 6476 [email protected]

Shashank Abhisheik Singapore +65 6536 1935 [email protected]

USA / Canada

Ravilochan Pola - CEO Americas +1(646) 361 3107 [email protected]

Production

Sajid Merchant Production (022) 30433247 [email protected]

Sharoz G Hussain Production (022) 30433183 [email protected]

Jestin George Editor (022) 30433272 [email protected]

Nikhil Pillai Database (022) 30433265 [email protected]

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Ultratech Cement Ltd (UTCEM IN, BUY)

Source: Bloomberg, Ambit Capital research

Ambuja Cements Ltd (ACEM IN, BUY)

Source: Bloomberg, Ambit Capital research

Shree Cement Ltd (SRCM IN, SELL)

Source: Bloomberg, Ambit Capital research

ACC Ltd (ACC IN, BUY)

Source: Bloomberg, Ambit Capital research

Ramco Cements Ltd (TRCL IN, SELL)

Source: Bloomberg, Ambit Capital research

Orient Cement Ltd (ORCMNT IN, BUY)

Source: Bloomberg, Ambit Capital research

0500

1,0001,5002,0002,5003,0003,5004,000

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

ULTRATECH CEMENT LTD

0

50

100

150

200

250

300

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

AMBUJA CEMENTS LTD

02,0004,0006,0008,000

10,00012,00014,00016,000

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

SHREE CEMENT LTD

0

500

1,000

1,500

2,000

Jun-

13

Sep-

13

Dec

-13

Mar

-14

Jun-

14

Sep-

14

Dec

-14

Mar

-15

Jun-

15

Sep-

15

Dec

-15

Mar

-16

Jun-

16

ACC LTD

0100

200300400500

600700

Jul-

13

Oct

-13

Jan-

14

Apr

-14

Jul-

14

Oct

-14

Jan-

15

Apr

-15

Jul-

15

Oct

-15

Jan-

16

Apr

-16

Ramco Cements Ltd/The

0

50

100

150

200

250

Jul-

13

Oct

-13

Jan-

14

Apr

-14

Jul-

14

Oct

-14

Jan-

15

Apr

-15

Jul-

15

Oct

-15

Jan-

16

Apr

-16

Orient Cement Ltd

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Marico Ltd (MRCO IN, BUY)

Source: Bloomberg, Ambit Capital research

Hindustan Unilever Ltd (HUVR IN, BUY)

Source: Bloomberg, Ambit Capital research

Thermax Ltd (TMX IN, SELL)

Source: Bloomberg, Ambit Capital research

0

50

100

150

200

250

300

Jul-

13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-

14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-

15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Marico Ltd

0

200

400

600

800

1,000

1,200

Jul-

13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-

14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-

15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Hindustan Unilever Ltd

0200400600800

1,0001,2001,400

Jul-

13

Sep-

13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-

14

Sep-

14

Nov

-14

Jan-

15

Mar

-15

May

-15

Jul-

15

Sep-

15

Nov

-15

Jan-

16

Mar

-16

May

-16

Thermax Ltd

AMBIT INSIGHTS

Ambit Capital Pvt Ltd 10 August 2016

Explanation of Investment Rating

Investment Rating Expected return (over 12-month)

BUY >10%

SELL <10%

NO STANCE We have forward looking estimates for the stock but we refrain from assigning valuation and recommendation

UNDER REVIEW We will revisit our recommendation, valuation and estimates on the stock following recent events

NOT RATED We do not have any forward looking estimates, valuation or recommendation for the stock POSITIVE We have a positive view on the sector and most of stocks under our coverage in the sector are BUYs

NEGATIVE We have a negative view on the sector and most of stocks under our coverage in the sector are SELLs Disclaimer This report or any portion hereof may not be reprinted, sold or redistributed without the wri tten consent of Ambit Capital. AMBIT Capital Research is disseminated and available primarily electronically, and, in some cases , in

printed form. Additional information on recommended securities is available on request. Disclaimer 1. AMBIT Capital Private Limited (“AMBIT Capital”) and i ts affiliates are a full service, integrated investment banking, investment advisory and brokerage group. AMBIT Capital is a Stock Broker, Portfolio Manager and

Depository Participant regis tered with Securities and Exchange Board of India Limited (SEBI) and is regulated by SEBI 2. AMBIT Capital makes best endeavours to ensure that the research analyst(s ) use current, reliable, comprehensive information and obtain such information from sources which the analyst(s) believes to be reliable.

However, such information has not been independently verified by AMBIT Capital and/or the analyst(s) and no representation or warranty, express or implied, is made as to the accuracy or completeness of any information obtained from third parties. The information, opinions , views expressed in this Research Report are those of the research analys t as at the date of this Research Report which are subject to change and do not represent to be an authority on the subject. AMBIT Capital may or may not subscribe to any and/ or all the views expressed herein.

3. This Research Report should be read and relied upon at the sole discretion and risk of the recipient. If you are dissatis fied with the contents of this complimentary Research Report or with the terms of this Disclaimer, your sole and exclusive remedy is to stop using this Research Report and AMBIT Capital or its affiliates shall not be responsible and/ or liable for any direct/consequential loss howsoever directly or indirectly, from any use of this Research Report.

4. If this Research Report is received by any client of AMBIT Capital or i ts affiliate, the relationship of AMBIT Capital/i ts affiliate with such client will continue to be governed by the terms and conditions in place between AMBIT Capital/ such affiliate and the client.

5. This Research Report is issued for information only and the 'Buy', 'Sell' , or ‘Other Recommendation’ made in this Research Report such should not be cons trued as an investment advice to any recipient to acquire, subscribe, purchase, sell, dispose of, retain any securi ties and should not be intended or treated as a substi tute for necessary review or validation or any professional advice. Recipients should consider this Research Report as only a single factor in making any inves tment decisions. This Research Report is not an offer to sell or the solicitation of an offer to purchase or subscribe for any investment or as an official endorsement of any investment.

6. This Research Report is being supplied to you solely for your information and may not be reproduced, redistributed or passed on, directly or indirectly, to any other person or published, copied in whole or in part, for any purpose. Neither this Research Report nor any copy of i t may be taken or transmitted or distributed, directly or indirectly within India or into any other country including United States (to US Persons ), Canada or Japan or to any resident thereof. The dis tribution of this Research Report in other jurisdictions may be strictly res tricted and/ or prohibited by law or contract, and persons into whose possession this Research Report comes should inform themselves about such restriction and/ or prohibition, and observe any such restrictions and/ or prohibition.

7. Ambit Capital Private Limited is regis tered as a Research Enti ty under the SEBI (Research Analysts ) Regulations, 2014. SEBI Reg.No.- INH000000313. Conflict of Interests 8. In the normal course of AMBIT Capital ’s business circumstances may arise that could result in the interes ts of AMBIT Capital conflicting with the interests of clients or one client’s interests conflicting with the interest of

another client. AMBIT Capital makes bes t efforts to ensure that conflicts are identi fied and managed and that clients ’ interests are protected. AMBIT Capital has policies and procedures in place to control the flow and use of non-public, price sensitive information and employees’ personal account trading. Where appropriate and reasonably achievable, AMBIT Capital segregates the activities of staff working in areas where conflicts of interest may arise. However, clients/potential clients of AMBIT Capital should be aware of these possible conflicts of interests and should make informed decisions in relation to AMBIT Capital’s services .

9. AMBIT Capital and/or i ts affiliates may from time to time have or solicit investment banking, investment advisory and other business relationships with companies covered in this Research Report and may receive compensation for the same.

Additional Disclaimer for U.S. Persons 10. The research report is solely a product of AMBIT Capital 11. AMBIT Capital is the employer of the research analyst(s) who has prepared the research report 12. Any subsequent transactions in securities discussed in the research reports should be effected through Enclave Capital LLC. (“Enclave”). 13. Enclave does not accept or receive any compensation of any kind for the dissemination of the AMBIT Capital research reports . 14. The research analys t(s) preparing the email / Research Report/ attachment is resident outside the United States and is/are not associated persons of any U.S. regulated broker-dealer and that therefore the analyst(s)

is/are not subject to supervision by a U.S. broker-dealer, and is/are not required to satis fy the regulatory licensing requirements of FINRA or required to otherwise comply with U.S. rules or regulations regarding, among other things, communications with a subject company, public appearances and trading securi ties held by a research analyst account.

15. This report is prepared, approved, published and dis tributed by the Ambit Capital located outside of the United States (a non-US Group Company”). This report is distributed in the U.S.by Enclave Capital LLC, a U.S. regis tered broker dealer, on behalf of Ambit Capital only to major U.S. institutional investors (as defined in Rule 15a-6 under the U.S. Securi ties Exchange Act of 1934 (the “Exchange Act”)) pursuant to the exemption in Rule 15a-6 and any transaction effected by a U.S. cus tomer in the securities described in this report must be effected through Enclave Capital LLC (19 West 44th Street, suite 1700, New York, NY 10036). In order to receive any additional information about or to effect a transaction in any security or financial instrument mentioned herein, please contact a regis tered representative of Enclave Capital LLC., by phone at 646 361 3107.

16. As of the publication of this report Enclave Capital LLC, does not make a market in the subject securi ties. 17. This document does not consti tute an offer of, or an invi tation by or on behalf of Ambit Capital or its affiliates or any other company to any person, to buy or sell any securi ty. The information contained herein has been

obtained from published information and other sources, which Ambit Capital or i ts Affiliates consider to be reliable. None of Ambit Capital accepts any liabili ty or responsibili ty whatsoever for the accuracy or completeness of any such information. All estimates, expressions of opinion and other subjective judgments contained herein are made as of the date of this document. Emerging securities markets may be subject to risks significantly higher than more established markets. In particular, the political and economic environment, company practices and market prices and volumes may be subject to significant variations. The abili ty to assess such risks may also be limited due to significantly lower information quantity and quality. By accepting this document, you agree to be bound by all the foregoing provisions.

Additional Disclaimer for Canadian Persons 18. AMBIT Capital is not registered in the Province of Ontario and /or Province of Québec to trade in securities and/or to provide advice with respect to securi ties. 19. AMBIT Capital's head office or principal place of business is located in India. 20. All or substantially all of AMBIT Capital's assets may be situated outside of Canada. 21. It may be difficult for enforcing legal rights against AMBIT Capital because of the above. 22. Name and address of AMBIT Capital's agent for service of process in the Province of Ontario is: Torys LLP, 79 Wellington St. W., 30th Floor, Box 270, TD South Tower, Toronto, Ontario M5K 1N2 Canada. 23. Name and address of AMBIT Capital's agent for service of process in the Province of Montréal is Torys Law Firm LLP, 1 Place Ville Marie, Suite 1919 Montréal, Québec H3B 2C3 Canada. Additional Disclaimer for Singapore Persons 24. This Report is prepared and distributed by Ambit Capital Private Limited and distributed as per the approved arrangement under Paragraph 9 of Third Schedule of Securi ties and Futures Act (CAP 289) and Paragraph

11 of the Firs t Schedule to the Financial Advisors Act (CAP 110) provided to Ambit Singapore Pte. Limited by Monetary Authority of Singapore. 25. This Report is only available to persons in Singapore who are institutional investors (as defined in section 4A of the Securities and Futures Act (Cap. 289) of Singapore (the “SFA”).” Accordingly, if a Singapore Person is

not or ceases to be such an ins titutional investor, such Singapore Person must immediately discontinue any use of this Report and inform Ambit Singapore Pte. Limited. Disclosures 26. The analyst (s ) has/have not served as an officer, director or employee of the subject company. 27. There is no material disciplinary action that has been taken by any regulatory authority impacting equity research analysis activities . 28. All market data included in this report are dated as at the previous s tock market closing day from the date of this report. 29. Ambit and/or its associates have financial interes t/equity shareholding in UltraTech Cement, ICICI Bank, Kotak Mahindra, Axis Bank, Yes Bank, DCB Bank, Federal Bank, DCB Bank, Marico, Thermax, HCL Tech & Eicher

Motors. 30. Ambit and/or it associates have actual/beneficial ownership of 1% or more in the securities of DCB Bank. 31. Ambit and/or it associates have received compensation for investment banking/merchant banking/brokering services from DCB Bank. Analyst Certif ication Each of the analys ts identi fied in this report certifies, with respect to the companies or securi ties that the individual analyses, that (1 ) the views expressed in this report reflect his or her personal views about all of the subject companies and securities and (2) no part of his or her compensation was, is or will be directly or indirectly dependent on the specific recommendations or views expressed in this report. © Copyright 2015 AMBIT Capital Private Limited. All rights reserved.

Ambit Capital Pvt. Ltd. Ambit House, 3rd Floor. 449, Senapati Bapat Marg, Lower Parel, Mumbai 400 013, India. Phone: +91-22-3043 3000 | Fax: +91-22-3043 3100 CIN: U74140MH1997PTC107598 www.ambitcapital.com