american health lawyers association · pdf filebusiness tactics and its relatively unregulated...

TRANSCRIPT

1 1

New Barbarians at the Gate?What Private Equity Wants From Medical Practices & How to Advise Clients

Peter A. Pavarini, Esq.

Co-Leader, Global Health Law Practice

Squire Patton Boggs (US) LLP

(614) 365-2712

Michael F. Schaff, Esq.

Chair, Corporate & Healthcare Practices

Wilentz, Goldman & Spitzer P.A.

(732) 855-6047

AMERICAN HEALTH LAWYERS ASSOCIATION

Physicians and Hospitals Law Institute

Orlando, Florida - February 1-3, 2017

2 2

• The Private Equity Business Model

• Why Are Private Equity Firms Interested in Medicine?

• The Typical Terms of a Private Equity Deal

• Regulatory Issues Presented By Private Equity Deals

• Legal Traps and How to Avoid Them

• What Does the Influx of Private Equity Mean For Physicians and Other Healthcare Providers?

• Questions and Comments

Agenda for Today’s Session

3 3

• A Class of Capital: Generally invested in privately-owned companies that are not traded on an exchange

• Unlike Venture Capital: PE firms seek mature (not early stage) companies that appear under-valued or under-performing, but have significant growth potential

• More Than Capital: PE firms also provide the business acumen necessary to improve the company’s prospects and increase its value

• PE Funds: Obtain their funds from institutions, sovereign wealth funds, pension funds, and high net-worth individuals seeking above market rates of return

What Is “Private Equity”?

4 4

• Private Equity Investors first gained public attention with KKR’s private equity takeover of RJR Nabisco in 1988, memorialized in the bestseller Barbarians at the Gate.

• PE Has Been Subject to Criticism for its use of ruthless business tactics and its relatively unregulated profile.

• PE Funds Took Off in the 1990s with the repeal of the Glass-Steagall Act and other laws deregulating banking and financial services.

• Healthcare Didn’t Get Much Early Attention because it didn’t offer as many opportunities for PE’s “buy-and-build” strategy

• Enactment of the ACA Dramatically changed the landscape for PE investors.

Brief History of Private Equity

5 5

Healthcare PE Has Mushroomed. The provider sector represents

half of the value invested by PE firms in healthcare in recent years.

Trends Supporting This Level of Investment.

• Growing ability to diagnose, monitor and treat chronic disease

• Historic fragmentation presents an opportunity for consolidation

• Provider organizations are often sub-par in operational efficiency

• Despite mistakes made with PPMs in the 1990s, PE firms see value in IPAs, CINs, and other physician organizations

• Some PE firms have an appetite for taking risk in high-cost areas of health

• Status of PCPs has been elevated by CMS reforms and use of HIT

• PE firms expect there will be a re-sale market for physician service companies in the next few years

How Private Equity Is Being Used In the Delivery of Healthcare Services

6 6

DaVita’s 2012 Acquisition of Healthcare Partners

(portfolio company of PE firm Summit Partners)

confirmed the strategic value of integrating all points of

care around a well-managed medical organization.

Other Examples of this trend:

• Optum’s acquisition of ProHealth (370 doc group in Conn.)

• DaVita’s acquisition of Everett Clinic (20 location multi-specialty group in Washington State)

Recent Examples

7 7

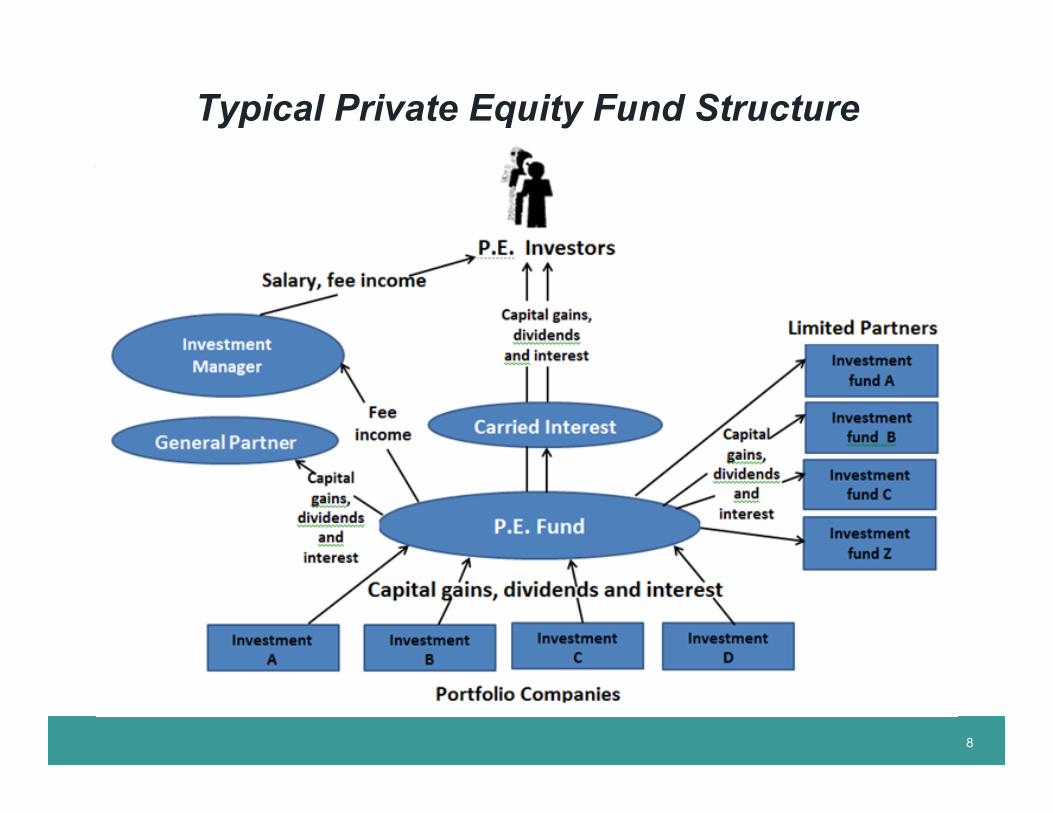

Legal Structure. PE firms are typically limited partnerships

in which the firm is the general partner and the investors are

limited partners.

Above Market ROIs. Given the inherent risk and illiquidity of

private companies, investors are generally looking for internal

rates of return around 30%.

Time Commitment. Investors are expected to make a

financial commitment of up to 10 years, with penalties for

early withdrawal and some allowance for extension of that

term. PE firms generally commit to invest the funds they

raise within the first 3 to 5 years or else return the

uncommitted capital to investors.

The PE Business Model

8 8

Typical Private Equity Fund Structure

9 9

Segregation of Transactional Risk. Each PE fund is a

special purpose entity, and each deal is funded and/or

operated through a separate corporation.

Financial Terms. PE firms typically use the “2 and 20”

model, in which the GP charges a flat 2% management fee

on all funds committed by the LPs. The GP receives 20% of

all investment profits once a “hurdle rate of return” has been

achieved. LPs get the remaining 80% in addition to the return

of their capital offset by bad investments & fees paid to the

GP.

Carried Interest. Profits realized by the fund’s GP are called

“carried interest”, and presently are taxed at capital gains

rates.

The PE Business Model

1010

Use of Leverage. Much of the payment for the acquisition of

an interest in a portfolio company is borrowed by the PE firm

from investment banks, hedge funds and other lenders.

Source of Profits. PE funds generally do not expect to

receive current earnings from their portfolio companies.

Rather they seek to profit from the sale of their interests

either through an IPO or by sale to another party.

Financial Controls. In order to improve the performance

portfolio companies, PE firm impose strict controls to

enhance revenues, operating margins and cash flows.

The PE Business Model

1111

Some or All of the Medical Practice? Practices are often

comprised of several business units or classes of assets – what’s

for sale?

Form of Investment. Equity (CPOM?), Debt, Asset Purchase,

Contractual, JV or New Business

Controlling or Non-Controlling?

• Often depends on management philosophy of PE firm

• Some are satisfied or even prefer a minority stake if the proper controls are in place

• Keep the owners interested in the success of their practice

Terms of a Non-Controlling Interest

Directors and Officers

Management

Typical Terms of PE Investment in a Medical Practice

1212

Capital Support.

• Asset purchase vs. share purchase

• Current value vs. enterprise value

• Can deal be financed?

• Debt instruments used by PE

Return on Investment.

• Gains from 1) revenue improvements, 2) cost reductions, 3) increased multiple of earnings, and 4) financial engineering

• Terms that maximize investors’ return upon exit

Physician Compensation and Benefits

• Largest component of budget

• No medical group want deals that would diminish earnings; improved margins must come from somewhere else

• However, compensation plan may be revised to reflect market and to improve physician performance

Typical Terms of PE Investment in a Medical Practice

1313

Profit Distributions to Physicians

• PE investors may be willing to wait, but physicians aren’t so patient

• When will new profits be shared with physicians?

• Source of the profits will determine timing and amount of distributions

Profit Distributions to PE Fund

• Most of the return to PE investors comes in the form of gains, including carried interest upon the fund’s exit from the investment

• The notable exception is the management fee paid to the PE fund’s manager which is typically in the 1.5 to 2.0% range

Typical Terms of PE Investment in a Medical Practice

1414

Restrictive Covenants

• Limits on Medical Practice

- Restrictions against business activities contrary to investors’ interests

- Requirement to use the services of company funded by the PE firm

- Restrictions on relations with third party payers and vendors (hospitals?)

- PE firms don’t seek to control patient referrals; however, care should be taken to avoid the appearance of relationships that would violate fraud and abuse laws

• Limits on Individual Physicians

- Restrictions on professional services individual physicians may offer patients, both during and following the investment term

- Consider state law implications

• Limits on the PE Firm

- PE firms expect great freedom in other investments that may make while in a relationship with a medical organization

- Medical group can ask for some degree of exclusivity in the relevant market, especially when the group has a dominant market position

.

Typical Terms of PE Investment in a Medical Practice

1515

Exit Rights

• Liquidating the PE Fund’s Investment

- PE firms place great importance on exit rights

- PE fund managers are skilled at timing exits to maximize profits

- Two most common exits are initial public offerings (IPOs) and sale to another company that sees strategic value in the offering

- Under certain circumstances, the medical group would be required to buy-back the PE firm’s interest

• Rights Associated with a PE Firm’s Exit

- Usual buy-sell provisions

– Restrictions on transfer

– Put and call options

– Drag-along rights

- Special rights for PE funds with a minority position

– Dividend preferences

– Conversion rights

– Anti-dilution protections

– Tag-along rights

Typical Terms of PE Investment in a Medical Practice

1616

Regulatory Issues Presented By PE Deals

What regulatory issues should be considered in structuring PE/ medical practice transactions?

Corporate Practice of Medicine Laws (“CPOM”)

• In general, the CPOM prohibits a business corporation or unlicensed individual from providing or employing a physician to provide medical services.

• The underlying purpose of the CPOM was to protect the public and physicians from abuses that could result from commercial exploitation of the practice of medicine.

1717

Regulatory Issues Presented By PE Deals

CPOM:

• Typically limits those who can practice medicine to individuals licensed to provide medical services in the state in which the services are delivered.

• Prohibits non-licensed persons, including business entities, from employing physicians to practice medicine on their behalf.

• If a physician is employed by a non-medical PE firm, this structure may not comply with applicable CPOM state laws.

• Ownership of a medical practice is also restricted in CPOM jurisdictions.

• States that have CPOM laws vary on how revenue is allowed to be distributed, as some states only allow revenue to be paid to licensed physicians.

1818

Regulatory Issues Presented By PE Deals

CPOM:

• CPOM statutes typically require medical professionals to practice through certain types of business entities, which often are distinguished as “professional” entities, such as professional corporations, professional limited liability companies and professional services organizations.

• State penalties for CPOM violations vary

‾ criminal misdemeanors

‾ monetary penalties

• States have injunctive authority and may be authorized to order redress to consumers through refunds of fees or other costs.

• Payors use CPOM violations as a reason for non-payment of medical claims.

19

State Fee Splitting Laws

Typically, State fee-splitting laws prohibit professionals from sharing the professional component of their fees with non-professionals.

New York. New York Education law § 6531 authorizes the suspension, revocation or annulment of a physician’s license if such physician “directly or indirectly requested, received or participated in the division, transference, assignment, rebate, splitting or refunding of a fee for, or has directly requested, received or profited by means of a credit or other valuable consideration as an omission, discount or gratuity, in connection with the furnishing of professional care or service…”

Regulatory Issues Presented By PE Deals

20

State Fee Splitting Laws – New York (con’t)

‾ Fee-splitting is also prohibited by the state Board of Regents regulations promulgated at 8 N.Y.C.R.R. § 29.1(b). In its pertinent part, the regulation prohibits any fee-splitting arrangement or agreement whereby the amount received in payment for furnishing space, facilities, equipment or personnel services used by a professional licensee constitutes a percentage of, or is otherwise dependent upon, the income or receipts of the licensee from such practice.

Regulatory Issues Presented By PE Deals

21

Licensure Requirements

• If a medical entity holds any licenses, certifications or accreditations, the transaction with the PE Firm may trigger change of ownership, notification or other filing requirements.

• Parties should review all licenses, certifications, permits and accreditations held by the medical practice, such as:

‾ State Departments of Health licenses

‾ Facility license

‾ Medicare/Medicaid provider enrollments

‾ Laboratory license

‾ X-Ray registrations

‾ MRI machine registrations

‾ Pharmacy license

Regulatory Issues Presented By PE Deals

22

State Insurance Laws

• In the 1990’s the National Association of Insurance Commissioners addressed certain healthcare risk-bearing financial arrangements and concluded that if the arrangement involves the assumption of risk and thus subject an entity to regulation as an insurance provider or managed care organization.

• Under certain circumstances, an entity may be subject to regulation as an insurance company or managed care organization if it engages in financial risk bearing arrangements.

• If the PE model includes risk based or shared savings arrangements with payors, state insurance laws must be reviewed.

Regulatory Issues Presented By PE Deals

23

State Insurance Laws

• If subject to state insurance laws, it may be required to register, or obtain licensure or certifications as:

‾ Third-party Administrator

‾ Organized Delivery System

‾ Health Maintenance Organization

‾ Licensed Insurance Company

• If the arrangement is determined to be subject to state insurance laws as a Licensed Health Plan or other regulated entity it may be required to meet other state requirements such as:

‾ Financial solvency requirements

‾ Capital reserve requirements

‾ Reporting obligations

Regulatory Issues Presented By PE Deals

24

Federal Securities Law Issues (on Rollovers)

• Often a PE firm will request or require that one or more of the physicians roll over part of the proceeds or ownership interest into the new entity.

• The rollover of a portion of a physician’s proceeds or ownership is subject to both state and federal securities laws and regulations.

• The SEC’s Regulation D is a federal law that is commonly used as an exception to registering securities.

• The Rule 504 offering (commonly called the “small offering exception”) allows a security offering to avoid registration if the value is less than $1 million dollars in a 12 month period.

Regulatory Issues Presented By PE Deals

25

Federal Securities Law Issues (on Rollovers)

• Rules 505 and 506 offerings have higher caps on the total value of the offering, however the purchasers of the offerings should be sold to “accredited investors”.

• An “accredited investor” is someone whose individual net worth or joint net worth with their spouse exceeds $1 million, or an individual whose income in the past two years exceeded $200,000.

• If the physician is an accredited investor, then registration of the offerings under federal securities law may be able to be avoided under Regulation D.

• It is important to also be aware of state law, as compliance with federal security law does not automatically result in compliance with state security law.

Regulatory Issues Presented By PE Deals

26

State Securities Law Issues

• Securities sold within a state are subject to the state’s securities laws and regulations – so called “blue sky law.”

• In general, securities cannot be offered or sold within a state unless the offer and sale is registered under that particular state’s laws or an exemption from registration exists.

• Securities laws vary considerably from state to state, although most states have exemptions similar to the federal Regulation D offering.

• Some states, such as California, exempt professional corporations from compliance with state securities registration requirements.

Regulatory Issues Presented By PE Deals

27

Payor Related Issues

• Managed care contracts may need to be renegotiated. Any change of ownership may trigger a termination of payorcontracts.

• In and out of network relationships should be assessed when deciding to make any changes to payor agreements.

• The PE firm may have better reimbursement rates already in existence through other agreements, so the practice payorcontracts need to be reviewed to ascertain which agreements.

• The parties need to address the effect of future recoupment for overbillings for pre-closing services.

• Medicare and Medicaid provider numbers may need to be changed depending on the type of transaction and the structure of the relationship between the PE firm and the medical facility.

Regulatory Issues Presented By PE Deals

2828

Antitrust Laws

• Federal and state antitrust laws must be carefully reviewed and considered when a PE firm seeks to invest in a medical practice.

• The principal federal statutes that apply to medical activities and to physician-controlled provider networks are:

− The Sherman Act § 1 and 2,

− The Clayton Act § 7, and

− The Federal Trade Commission Act § 5.

Regulatory Issues Presented By PE Deals

2929

Use of Management Service Organizations (“MSO”) as an Alternative Investment Strategy

• Use of a MSO for a PE’s investment in a medical practice.

• An MSO is set up as either an LLC or corporation that is owned in whole or in part by the PE firm, separate from the medical practice itself. In CPOM states, the medical practice continues to be owned entirely by licensed physicians.

Regulatory Issues Presented By PE Deals

30

MSO

• The medical practice enters into a Management Services Agreement with the MSO, which provides the practice with non-clinical administrative services or practice management tools, such as:

− Billing,

− Accounting,

− Purchasing office supplies and equipment,

− Providing office space,

− Management,

− Human resources, or

− Non-clinical personnel.

Regulatory Issues Presented By PE Deals

3131

MSO

• The MSO is paid a fee for providing these services to the medical practice. The fee should be fair market value and commercially reasonable for the services provided.

• The MSO services must not interfere with the professional’s medical (clinical) judgment or otherwise result in MSO control over the medical aspects of the medical practice.

Regulatory Issues Presented By PE Deals

3232

State example – New York

• In the Matter of Andrew Carothers, M.D., P.C., the court held that a non-physician owned entity was engaged in the corporate practice of medicine. Their decision focused on findings that:

− The nominal physician-owner of the PC in question was not engaged in that PC’s professional practice, and

− The non-physician owners of the MSO were the de facto owners of the PC and exercised substantial control over the PC.

Regulatory Issues Presented By PE Deals

3333

MSO

• New York Attorney General (NY AG) and with Aspen Dental Management Inc. (ADMI) agreed to an Assurance of Discontinuance after NY AG investigation into ADMI's business practices.

• Without admitting or denying wrongdoing, ADMI agreed to pay a civil penalty of $450,000 to resolve allegations that its relationships with numerous New York dental practices constituted the unauthorized CPOD and improper fee splitting. ADMI also agreed to implement certain business practice guidelines in its relationships with dental practices.

Regulatory Issues Presented By PE Deals

3434

Examples of the guidelines agreed to in Aspen Dental are as follows:

− Hiring of clinical staff is to be done at the sole discretion of the licensed professionals of the practice;

− All medical decisions are to be made solely at the discretion of the licensed professionals of the practice;

− The bank account which all medical services are paid would be owned by the practice and the practice shall have full access to the accounts; and

− All fees paid by the practice to the MSO shall be listed as separate operating expenses of the practice on all budgets and profit/loss statements.

Regulatory Issues Presented By PE Deals

3535

What taxation issues are involved in a PE/Medical Practice transaction?

Stock vs. Asset Deal

• It is important to consult with a tax advisor early in the transaction to ensure all decisions are made with a complete understanding of the tax consequences.

• Stock Sale by the individual physician owner

− The sale of stock is taxed at the capital gains tax rate

− Avoids double taxation

− Liabilities will remain with the medical practice which then become the responsibility of the PE firm

− The need to obtain third party consents may be avoided

Regulatory Issues Presented By PE Deals

3636

• Asset Sale

− The sale of assets is usually taxed as ordinary income

− Step-up tax basis for the buyer on the purchased assets

− Allows a PE firm to amortize intangibles over fifteen years.

− Liabilities associated with the practice will usually not transfer to a PE firm unless assumed by the buyer

− Third party consents may be triggered relating to the assignment of vendor and third party contracts

Regulatory Issues Presented By PE Deals

3737

Personal Goodwill- A personal asset that depends on the continued presence of a particular individual and may be attributed to the individual owner’s personal skill, training or reputation.

− Existence is based on the fact that patients choose the individual physician. Assumption is if individual were not there, the patients would go elsewhere.

− Seller taxed as capital gains

Regulatory Issues Presented By PE Deals

3838

Enterprise Goodwill- An asset of the business and may be attributed to a business by virtue of its existing arrangements with supplies, customers or others, and its anticipated future customer base due to factors attributable to the business.

− Existence is based on the fact that people come to the enterprise.

− Loss of key individuals would not materially impact company.

− May be based on location, staff, website, facilities, and reputation/brand of the entity (as opposed to an individual’s reputation). Sales generated from company sales team.

− Non-compete exists between selling shareholder or member and company.

Regulatory Issues Presented By PE Deals

39

• Carried Interest

− Carried interest is a contractual right that allows the general partner of a PE firm to share in the profits of the firm while only being taxed on those profits as a net capital gain. This allows the general partner to obtain profits from the firm and avoid paying ordinary income tax on the distributions.

− PE firm general managers typically pass some of these profits onto the investment managers, who are then also only taxed at the capital gains rate on the profits rather than ordinary income.

− The concept of carried interest has been highly disputed as of late, and may be susceptible to tax reform in the near future, as President Trump has been outspoken about his goal to close the carried interest “loophole”.

Regulatory Issues Presented By PE Deals

4040

What do these transactions look like in actual practice?

Real Life Examples

• A dental practice management company, funded by a PE firm, acquired the non-clinical assets of a large multi-site dental practice for $80 million dollars. The dental practice management company entered into a long term MSO agreement with the dental practice.

• An anesthesia management company, owned by a PE firm, loaned $90 million dollars to a “friendly physician” to purchase the stock of a large anesthesia practice. The anesthesia practice subsequently entered into an MSO agreement with the anesthesia management company.

Regulatory Issues Presented By PE Deals

4141

Real Life Examples

• A dermatology practice sold its non-clinical assets to an MSO which was owned by a PE firm. Some of the physician-owners of the dermatology practice also rolled over some of their purchase price to become owners of the MSO.

• A radiologist sold the stock of his radiology practice to another radiologist for $45 million dollars. The purchaser radiologist was funded by a PE firm, and an MSO was established by the PE firm to provide administrative services for the radiology practice.

Regulatory Issues Presented By PE Deals

4242

Speculative Funding for Innovations in Medicine

• Precision medicine (a broad concept that incorporates personalized and genetic medicine) has attracted significant capital investment, including from PE firms.

• As the payer environment is transforming towards value, investors are increasing attention to pharmaceutical and diagnostic companies developing precision medicine products and services for segmented markets with higher potential rewards.

• In recent years, PE firms have invested in life science companies and support organizations to develop and commercialize precision medicine products and therapies for value-based care.

How PE Is Investing In the Future of Medicine

4343

• Is Private Equity Incompatible With Medical Practice? Arguments For:

• Professionalism is compromised by emphasis is on profitability

• The involvement of PE compromises the patient-physician relationship

• The transition from fee-for-service care to value-based care is impeded by the introduction of speculative capital

• The short-time horizons of PE Firms are at odds population health

• Private equity will strengthen payers at the expense of providers

Arguments Against:

• The commercialization of medicine pre-dated PE investment

• At one-fifth of the economy, healthcare is ripe for consolidation

• Many practices lack the capital to modernize their practices, especially in the area of information technology

• For doctors unwilling to give up their independence to large health systems, PE offers another financial partner

What Does PE Mean For Physicians and Other Healthcare Providers?

4444

• PE Investors Don’t Want to Own Physicians – Rather They Seek to Leverage Patient Flows

Primary Care Is Particularly Enticing:

• Keeping large populations of patients healthy and managing their use of higher cost services will generate better returns of investment than volume-based treatment models.

• Doctors can remain autonomous, but by organizing and capitalizing their clinical activities, gains can be maximized in the new payment environment.

• PE can help physicians form companies to manage “downstream risk” from health plans with care coordination and data analytics

Specialty Medical Practices Present Different Opportunities

• Hot areas are dermatology, behavioral health and consumer-driven care

• Specialties like anesthesiology and others associated with hospital service lines that can be outsourced are subject to consolidation

• Value-based payment like bundles and percent of premium arrangements present opportunities similar to those available to PCPs

What Does PE Mean For Physicians and Other Healthcare Providers?

4545

• Are Hospitals and Institutional Providers Threatened?

PE Firms Are Just Doing What Hospitals Have Attempted For Years:

• The business deals attracting PE are not different than those sought by hospitals and health systems since the 1980s (e.g., consolidations, joint ventures, and other deals done under the banner of “integration).

• PE firms generally face fewer regulatory hurdles than entities faced with self-referral prohibitions and tax-exemption issues.

PE Firms Are Also Interested in Hospitals and Health Facilities

• Although PE investment in for-profit hospitals and systems has diminished some, some operations remain of interest, such as, laboratories, urgent care centers, ACOs, population health back offices.

• If non-profits can navigate the complexities of working with for-profits, there’s no intrinsic reason why PE funds can’t be another source of capital.

What Does PE Mean For Physicians and Other Healthcare Providers?

4646

New Barbarians At the Gate?Private Equity and Medicine

Peter A. Pavarini

Squire Patton Boggs (US) LLP

Michael F. Schaff

Wilentz, Goldman & Spitzer P.A.

Questions and Comments