american rescue plan: tax implications

TRANSCRIPT

www.caltax.com | E-mail: [email protected] | Phone: 714-776-7850 | Fax: 714-776-9906

Your California solution since 1975

American Rescue Plan:Tax Implications

This publication is distributed with the understanding that the

authors and publisher are not engaged in rendering legal, accounting

or other professional advice and assume no liability in connection

with its use. Tax laws are constantly changing and are subject to

differing interpretation. In addition, the facts and circumstances in

your particular situation may not be the same as those presented

here. Therefore, we urge you to do additional research and ensure

that you are fully informed before using the information contained in

this publication. Federal law prohibits unauthorized reproduction of

the material in Spidell’s American Rescue Plan: Tax Implications

manual. All reproduction must be approved in writing by Spidell

Publishing, Inc.®

This is not a free publication. Purchase of this electronic

publication entitles the buyer to keep one copy on his/her computer

and to print out one copy only. Printing out more than one copy —

and any electronic distribution of this publication — is prohibited by

international and United States copyright laws and treaties. Illegal

distribution of this publication will subject the purchaser to penalties

of up to $100,000 per copy distributed.

AMERICAN RESCUE PLAN: TAX IMPLICATIONS

Course objectives: This course reviews tax implications of the American Rescue Plan Act (ARPA), signed into law on March 11, 2021, and providing relief to individuals and businesses impacted by COVID-19. Topics discussed include: unemployment insurance and Pandemic Unemployment Assistance; economic impact payments; ARPA modifications to the Child Tax Credit, Child and Dependent Care Tax Credit, Premium Tax Credit, Earned Income Credit; expansion of paid sick leave and paid family leave; Employee Retention Credit; COBRA continuation coverage; Restaurant Revitalization Fund; Paycheck Protection Program; and more.

After completing this course, you will be able to:

Determine whether filing MFS will benefit a married couple by maximizing the exclusion for unemployment compensation

Recall how to reconcile the Child Tax Credit on the 2021 tax return

Recall how the ARPA affects filing decisions for separated taxpayers claiming the Earned Income Credit

Identify how employer credits for paid leave are applied under the ARPA

Determine eligibility for a Restaurant Revitalization Fund grant

Category: Taxes Recommended CPE Hours: CPAs — 1 Tax

EAs — 1 Federal Tax CRTPs — 1 Federal Tax

Level: Basic Prerequisite: None Advance Preparation: None Expiration Date: March 2022

American Rescue Plan: Tax Implications

©2021 i Spidell Publishing, Inc.®

Table of Contents April 15 deadline extended for individual returns only ........................................................................... 1 Individual income tax provisions .................................................................................................................. 1

Unemployment Insurance/Pandemic Unemployment Assistance ..................................................... 1 Gross income exclusion ....................................................................................................................... 1 Expanded UI benefits extended ......................................................................................................... 3

Another round of economic impact payments ....................................................................................... 4 Payment amounts ................................................................................................................................. 4 How payments determined ................................................................................................................ 5 Reducing AGI ....................................................................................................................................... 6 UI exclusion bonus ............................................................................................................................... 7 Using MFS to maximize UI exclusion and other benefits ............................................................... 8 Dependent loophole closing? ........................................................................................................... 19 Social Security numbers required .................................................................................................... 19 Deceased taxpayers ............................................................................................................................ 19 Ineligible individuals ......................................................................................................................... 20 Direct deposits .................................................................................................................................... 20

Child tax credit .......................................................................................................................................... 20 Phaseout of increased credit ............................................................................................................. 20 Refundable credit ............................................................................................................................... 21 Advance payment of credit ............................................................................................................... 21 Reconciliation ...................................................................................................................................... 23 Safe harbor .......................................................................................................................................... 23

Dependent care assistance ....................................................................................................................... 24 Increase in credit amount .................................................................................................................. 24 Refundable .......................................................................................................................................... 26 Exclusion increased ............................................................................................................................ 26

Earned income tax credit expansion ....................................................................................................... 26 Taxpayers without qualifying children ........................................................................................... 27 Separated taxpayers ........................................................................................................................... 27 Earned income .................................................................................................................................... 27 Investment income cap ...................................................................................................................... 28

Premium tax credit.................................................................................................................................... 28 2020 repayment requirement repealed ............................................................................................ 28 Enhanced credit for 2021 and 2022 .................................................................................................. 28

Student loan forgiveness exclusion ........................................................................................................ 31 Business tax provisions .................................................................................................................................. 31

Paid sick and family leave employer credits ......................................................................................... 31 Expansion of paid sick and family leave credits ............................................................................ 31 Claiming the employer credits ......................................................................................................... 32 Denial of double benefit .................................................................................................................... 32 Extended limitations period ............................................................................................................. 33

American Rescue Plan: Tax Implications

Spidell Publishing, Inc.® ii ©2021

Employee retention credit ........................................................................................................................ 33 Recovery start-up businesses ............................................................................................................ 34 Severely financially distressed employers ...................................................................................... 34 Extended limitations period ............................................................................................................. 34 Allocating wages for PPP loan recipients ....................................................................................... 34

Why Forms 941-X may be necessary for 2020 ....................................................................................... 36 Payroll companies sleeping on the job ............................................................................................ 36

Revenue raising measures ....................................................................................................................... 37 COBRA continuation coverage .................................................................................................................... 37

Premium subsidies .................................................................................................................................... 37 Gross income exclusion ..................................................................................................................... 38 Premium reimbursements ................................................................................................................. 38 Double benefits disallowed............................................................................................................... 38

Continuation coverage premium assistance credit .............................................................................. 38 Ordering rules ..................................................................................................................................... 38 Advance credit .................................................................................................................................... 38 Denial of double benefit .................................................................................................................... 39 Extension of statute of limitations .................................................................................................... 39

Loan and grant programs ............................................................................................................................... 39 Restaurant Revitalization Fund grants .................................................................................................. 39

Tax treatment ...................................................................................................................................... 39 Amount of the grant .......................................................................................................................... 39 Business opened in 2019 .................................................................................................................... 39 Business opened in early 2020 .......................................................................................................... 40 Brand new businesses ........................................................................................................................ 40 Grant cap ............................................................................................................................................. 40 Eligible entity ...................................................................................................................................... 40 Certification ......................................................................................................................................... 40 Use of funds ........................................................................................................................................ 40 Covered period ................................................................................................................................... 41 Priority in awarding grants ............................................................................................................... 41

Shuttered venue operator grants ............................................................................................................ 41 Paycheck protection program ................................................................................................................. 41

Additional covered nonprofit entities ............................................................................................. 42 Employee caps .................................................................................................................................... 42 Affiliation rules waived ..................................................................................................................... 42

Targeted EIDL advance ............................................................................................................................ 42 Appendix .......................................................................................................................................................... 43

American Rescue Plan: Tax Implications

©2021 1 Spidell Publishing, Inc.®

AMERICAN RESCUE PLAN: TAX IMPLICATIONS President Biden signed the American Rescue Plan Act (ARPA) on March 11, 2021, providing

much needed relief to those impacted by COVID-19, and even to some who weren’t.

APRIL 15 DEADLINE EXTENDED FOR INDIVIDUAL RETURNS ONLY

The IRS announced that it is moving the April 15, 2021, filing deadline to May 17, 2021, for individual taxpayers (including Schedule C filers) only. However, the extension does not apply to estimated tax payments for the first quarter of 2021. These payments are still due April 15, 2021.

Taxpayers do not have to request an extension for the one-month delay, but if returns are not filed by May 17, they must file for an extension by that date.

The March 15 filing deadline for calendar-year partnerships and S corporations was not extended, nor was the April 15 filing deadline for C corporations or trusts.

The IRS announcement is available at:

Website www.irs.gov/newsroom/tax-day-for-individuals-extended-to-may-17-

treasury-irs-extend-filing-and-payment-deadline

INDIVIDUAL INCOME TAX PROVISIONS

UNEMPLOYMENT INSURANCE/PANDEMIC UNEMPLOYMENT ASSISTANCE

Gross income exclusion The ARPA provides for an exclusion of up to $10,200 of unemployment compensation for taxpayers

with up to $150,000 of modified AGI for the 2020 taxable year only. (ARPA §9042; IRC §85(c))

Added benefits

In addition to the exclusion of the UI benefits from taxable income, the exclusion reduces taxpayers’ AGI, which can increase other benefits that are phased out or calculated based on AGI, including economic impact payments and Premium Tax Credits (see below for more information on these calculations).

For purposes of computing the $150,000 limit, any unemployment compensation received is excluded from the AGI computation, and the AGI is computed after the:

• Exclusions for Social Security benefits, education savings bonds, and employer provided adoption assistance; and

• Deductions for retirement savings contributions, student interest payments, higher education tuition payments, and passive activity losses.

American Rescue Plan: Tax Implications

Spidell Publishing, Inc.® 2 ©2021

Caution

The law states that the unemployment compensation is excluded from modified AGI for these purposes. However, the IRS worksheet is currently including the unemployment compensation in the calculation. We have reached out to multiple contacts to clarify this issue. If the unemployment income pushes your client’s modified AGI over $150,000, we recommend that you wait until this issue is clarified to file the returns. For married couples, you could consider filing MFS to solve this problem. We will discuss this in more detail below.

To view the IRS worksheet to calculate the modified AGI, go to:

Website www.irs.gov/faqs/irs-procedures/forms-publications/new-exclusion-of-up-to-10200-of-

unemployment-compensation

Planning Pointer

The $150,000 AGI threshold applies regardless of filing status, so married taxpayers filing joint returns are subject to the same threshold as single taxpayers. However, if the couple files married filing separate, each return will be subject to the $150,000 threshold, and each return can exclude up to $10,200 of unemployment compensation. It may benefit some couples to file MFS to maximize the exclusion of up to $20,400 of the unemployment compensation. However, you must consider the following items:

• You cannot amend a MFJ return to MFS. If the couple’s 2020 return was filed prior to the enactment of the ARPA, absent further guidance from the IRS, you must file the MFS returns as superseding original returns prior to the May 17, 2021 filing deadline unless a valid extension is filed, in which case the return may be superseded up until the extended due date;

• Filing the MFS return is a bit more complicated, as all community property income must be split between the two returns, but your software should help you with this; and

• You must take into account the other impacts of filing MFS:

o MFS taxpayers can't take the student loan interest deduction, the tuition and fees deduction, the education credits, or the Earned Income Credit; and

o MFS taxpayers who live together can’t take the Child and Dependent Care Credit or the Credit for the Elderly or the Disabled, and they can’t claim the $25,000 passive activity loss allowance for rental property.

As we work our way through the material, you will see how maximizing the benefit of the UI exclusion can also help increase other benefits available to the taxpayers. See page 8 for a full example showing these benefits on a sample tax return.

American Rescue Plan: Tax Implications

©2021 3 Spidell Publishing, Inc.®

Example of splitting the return

Jason and Amanda are a married couple with modified AGI of $180,000 on their 2020 MFJ return. Each spouse received unemployment compensation of $15,000. On their MFJ return, they do not qualify to exclude any of the unemployment compensation because their AGI is over the $150,000 threshold.

If instead Jason and Amanda file MFS, assuming all of their income is community income, they now each have modified AGI of $90,000, and both spouses will qualify for an unemployment compensation exclusion of $10,200.

This exclusion is welcome relief for those taxpayers who faced unexpected tax bills when they discovered that the state agencies issuing the payments failed to withhold taxes on the additional $600/$300 weekly Pandemic Unemployment Assistance (PUA) benefits that were paid. In addition the tax withheld on the regular unemployment was only 10%. However, according to some news reports, the $10,200 amount represents about 17 weeks of benefits, so many taxpayers who’ve been receiving benefits throughout the pandemic will still pay tax on a portion of their UI benefits (even if their AGI is less than $150,000).

Practice Pointer

Note the following:

• When these materials went to press, the IRS was advising taxpayers not to file an amended return to claim this benefit. What we don’t know is at what point the IRS and software providers will be able to process returns claiming the exemption. Unless the IRS is able to compute this exclusion for taxpayers who had previously filed returns, those taxpayers will be required to file amended or superseded returns to claim this new benefit exclusion.

• While many “one-time” tax benefits often are extended year after year, it’s unclear whether this is one benefit that will be renewed for 2021 taxable year. There was a lot of controversy over whether to provide tax-free unemployment benefits when workers making comparable amounts are required to pay taxes on their W-2 wages. However legislators wanted to address the issue that millions of recipients were unaware that no withholding was being taken on the additional $300/$600 of weekly benefits and were facing “surprise” tax liabilities. You should advise your clients that they may not be so lucky next year and to plan accordingly.

Expanded UI benefits extended The COVID-19-related unemployment insurance and pandemic assistance programs are

extended for an additional 25 weeks through September 6, 2021. (ARPA §9011 et seq.) The additional $300 in weekly benefits is also extended. (ARPA §9013)

Comment

The ARPA also authorizes $2 billion to be expended by the federal and state governments on fraud prevention, promoting equitable access, and ensuring timely payment of UI benefits. (ARPA §9032)

American Rescue Plan: Tax Implications

Spidell Publishing, Inc.® 4 ©2021

ANOTHER ROUND OF ECONOMIC IMPACT PAYMENTS

A third round of economic impact payments (EIPs) is authorized. (ARPA §9601; IRC §6428B) Like the EIPs authorized under the CARES Act and Consolidated Appropriations Act of 2021, the payments will be automatically sent out to taxpayers. However, the EIPs authorized under the American Rescue Plan Act are different than those authorized under the CARES Act and CAA in that:

• The amount of the payments are higher ($1,400 per taxpayer and dependent); • Adult dependents qualify under the ARPA; • The AGI phaseout ranges are much smaller; • The advance payments are based on a taxpayer’s 2020 AGI (2019 if no 2020 return has been

filed); and • The payments are considered advance credits against the taxpayer’s 2021 tax liability rather

than the 2020 liability, so the reconciliation will be made on the 2021 tax return.

In its current form, the bill does not prevent debt collectors from levying a bank account that contains an EIP. The first two rounds of EIPs were protected from garnishment ― but the special rules that Democrats used to pass the latest bill did not allow them to include the protections this time. However, it is likely legislation will be introduced and enacted quickly to fix this problem.

Comment

According to various news accounts, the payments have already started going out.

Payment amounts The payments are equal to $1,400 per eligible individual ($2,800 for MFJ) plus $1,400 per

dependent (as defined under IRC §152). (IRC §6428B(a))

Comment

This is a significant expansion from the prior EIPs that were issued, not only in the amount of the payment, but in expanding the number of dependents that may receive the EIPs. The prior EIPs were limited to dependents under age 17, so taxpayers were not receiving payments for some high school and most college student dependents or adult dependents such as parents. Households with these adult dependents will be receiving much higher payments this round.

The amount of the credit is phased out (but not below zero) for taxpayers with income above the phaseout thresholds as follows (IRC §6428B(d)):

2021 Economic Impact Payment AGI and Phaseout Levels

Filing Status Phaseout begins at … Credit phased out at …

Married filing joint $150,000 $160,000

Head of household $112,500 $120,000

Single and married filing separate $75,000 $80,000

These phaseouts are calculated differently from the prior two phaseouts. Previously the credit was phased out by 5% of every dollar by which the taxpayer’s AGI exceeded the thresholds. For this round of payments, the taxpayer’s total credit on the return (including amounts for dependents) is

American Rescue Plan: Tax Implications

Spidell Publishing, Inc.5©2021 ®

reduced by a percentage that is calculated using a ratio that takes the AGI amount over the threshold (up to the credit phaseout amount) and divides it by the following dollar amounts:

• $10,000 for MFJ; • $7,500 for HOH; and • $5,000 for single and MFS.

Example of single taxpayer

Jane is a single taxpayer with no dependents, and a 2019 AGI of $76,000. She has not yet filed her 2020 tax return. Her 2021 EIP will be $1,120, calculated as follows:

Amount over threshold: $76,000 - $75,000 = $1,000

2021 EIP reduction:

$1,400 × $1,000 $5,000

= $280

2021 EIP: $1,400 - $280 = $1,120

Example of MFJ taxpayers

Jack and Jill are married, with two dependent children. Their 2019 AGI was $157,000. They have not yet filed their 2020 tax return. Their 2021 EIP of $5,600 ($1,400 × 4) will be reduced to $1,680, calculated as follows:

Amount over threshold: $157,000 - $150,000 = $7,000

2021 EIP reduction:

$5,600 × $7,000

$10,000 = $3,920

2021 EIP: $5,600 - $3,920 = $1,680

How payments determined Payments will be based on a taxpayer’s 2019 AGI, unless a taxpayer has filed a 2020 return (and

the IRS has processed the return). If the IRS bases the payment on a taxpayer’s 2019 AGI, and the taxpayer subsequently files a 2020 return showing a lower AGI amount, the IRS may remit an additional payment to the taxpayer based on the 2020 return, but only if the 2020 return is filed bythe “additional payment determination date.” (IRC §6428B(g)(5))

The additional payment determination date is the earlier of:

• 90 days after the 2020 calendar year filing deadline (August 15, 2021); or• September 1, 2021.

American Rescue Plan: Tax Implications

Spidell Publishing, Inc.® 6 ©2021

Comment

Although the filing due date was extended until May 17, 2021, we are not sure if the 90 days will be extended from July 14 until August 15. So we suggest you file 2020 returns before July 14, 2021 if you wish the IRS to use the 2020 income to compute the economic impact payment.

No payments will be made after December 31, 2021.

Practice Pointer

For purposes of issuing additional payments, the act states that a tax return will not be treated as “filed” until the return has been “processed” by the IRS. (IRC §6428B(g)(7)) Taxpayers who would qualify for higher EIPs as a result of a drop in their 2020 AGI should consider filing their returns early to ensure that their returns are processed in time to receive the additional payment.

Conversely if a taxpayer’s AGI is going to be higher in 2020, they may want to consider delaying filing their return in order to maximize the amount of their available rebate. Like the first and second round of EIPs, taxpayers will not have to repay amounts if the amount of the rebate based on 2020 or 2021 AGI is more than what was actually paid based on 2019 AGI.

Reducing AGI Since the EIPs are based on AGI, for a taxpayer who is above the threshold, consider accelerating

deductions into 2020 (or 2021) to reduce the AGI below the phaseout amounts.

Suggestions include:

• Make a deductible contribution to an IRA; • For a bigger benefit, establish a pension plan and make a contribution for 2020; • Maximize §179 and bonus depreciation deductions; and • If applicable, be sure to claim:

o The above-the-line charitable contribution; and o Student loan interest and tuition and fees deduction.

American Rescue Plan: Tax Implications

©2021 7 Spidell Publishing, Inc.®

Example of making IRA contribution

Betsy is 72 years old and still working part-time. Her 2020 AGI is $80,000. She did not receive any EIP, as her income in 2019 was over $125,000, and her 2020 return had not been filed when the 2021 EIPs were issued. Based on the $80,000 AGI for 2020, her economic impact credit for 2020 will be:

First payment $1,200 – (($80,000 – $75,000) × 0.05) $ 950 Second payment $600 – (($80,000 – $75,000) × 0.05) 350 Total $1,300

She will not receive a 2021 EIP because her payment is phased out at $80,000 AGI.

However, if she contributes $5,000 to a deductible IRA, her AGI will go down to $75,000, and her economic impact credits for 2020 will be:

First payment $1,200 Second payment 600 Total $1,800

She will claim a $500 Recovery Rebate Credit on her 2020 return. She will also receive a 2021 EIP of $1,400.

Thus, Betsy will receive an extra $1,900 in combined EIPs as sort of a “bonus” on her contribution.

UI exclusion bonus

Example of UI exclusion

Robert was unemployed for part of 2020 but was able to return to work later in the year. Before applying the new UI exclusion, his 2020 AGI was $85,000 including all of his UI income. He did not receive any EIPs as his income in 2019 was over $125,000, and his 2020 return had not been filed when the 2021 EIPs were issued. Based on the $85,000 AGI for 2020 (prior to the UI exclusion), his economic impact credit for 2020 was calculated as follows:

First payment $1,200 – (($85,000 – $75,000) × 0.05) $700 Second payment $600 – (($85,000 – $75,000) × 0.05) 100 Total $800

He would not be eligible to receive a 2021 EIP because his payment is phased out at $80,000 AGI.

After we exclude his $10,200 of UI, his AGI will go down to $74,800, and his economic impact credits for 2020 will be:

First payment $1,200 Second payment 600 Total $1,800

The $1,000 additional amount will be claimed as a Recovery Rebate Credit on his 2020 return. He will also receive a 2021 EIP of $1,400.

Thus, Robert will receive an extra $2,400 in addition to the tax he saves on his UI income.

American Rescue Plan: Tax Implications

Spidell Publishing, Inc.® 8 ©2021

Practice Pointer

If the IRS is able to compute the UI exclusion for taxpayers who have already filed their returns, it is not clear if they will also recompute the additional Recovery Rebate Credit. This is something you will want to verify for your clients.

Using MFS to maximize UI exclusion and other benefits As we previously discussed, even though filing as MFS can limit some benefits on a married

couple’s tax returns, the reduced AGI can still provide a large benefit for your clients.

Example of MFS

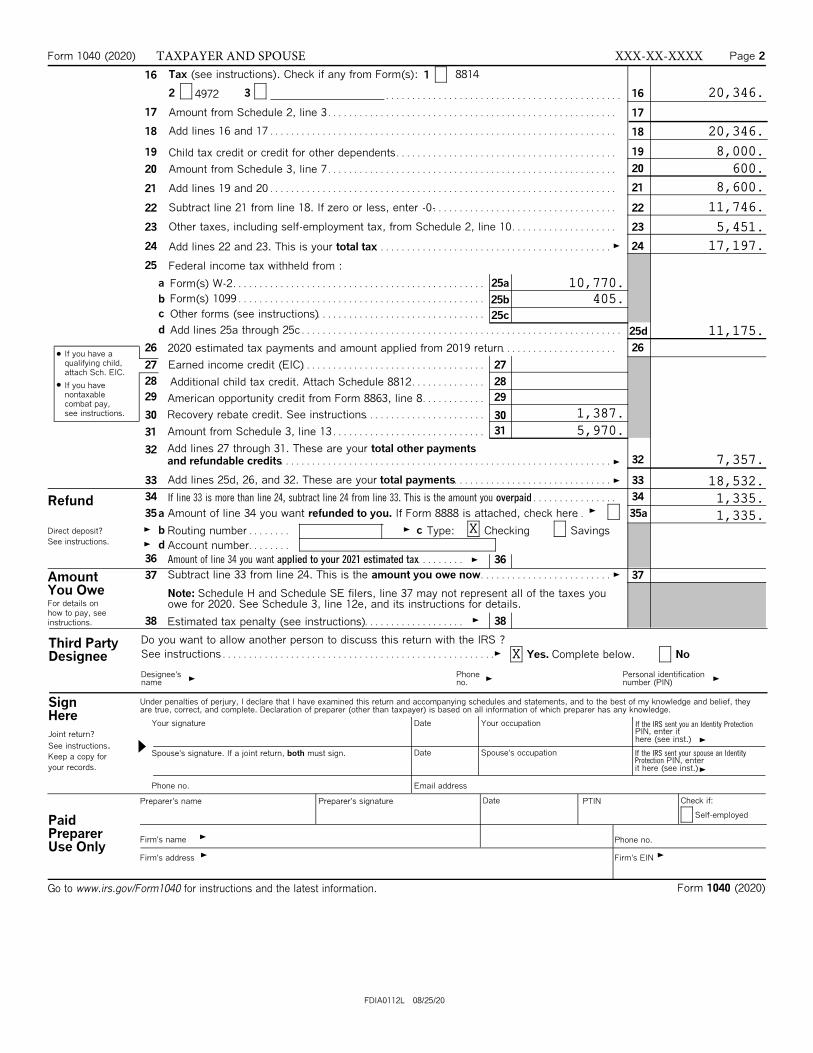

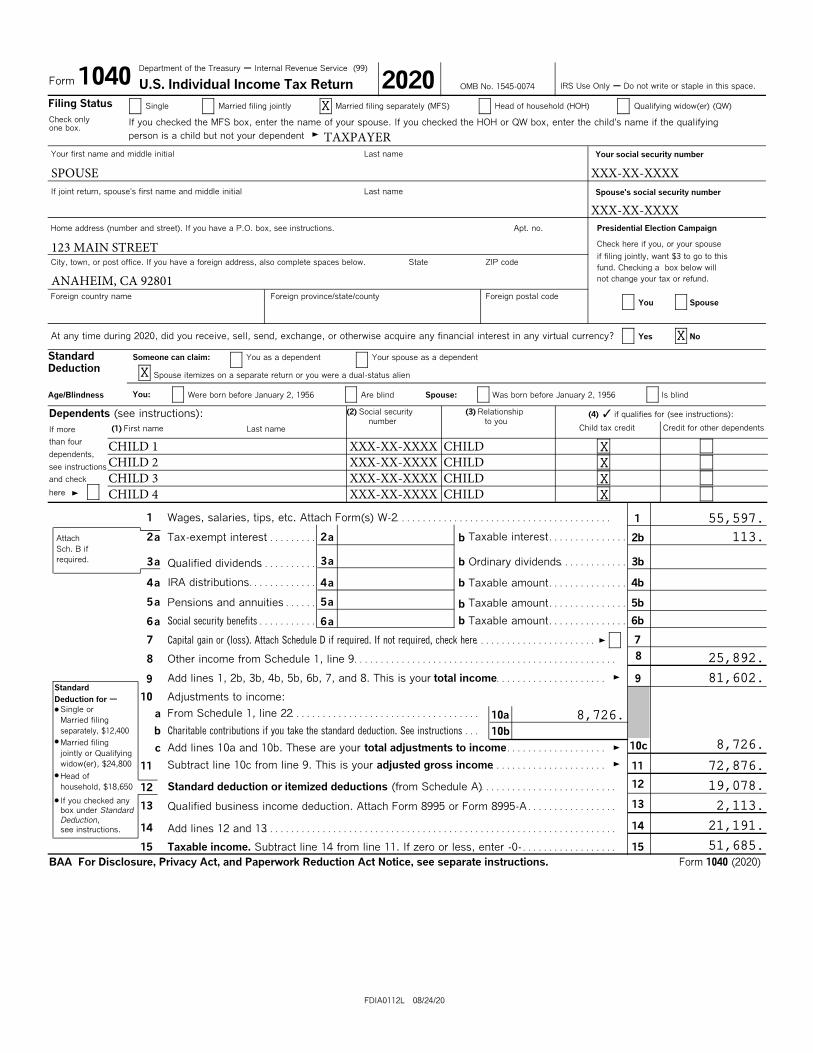

Louis and Lexi are a married couple with four children. For 2020, if the couple files MFJ, their modified AGI is more than $150,000, so they do not qualify for the UI exclusion. Filing MFJ they would have a federal tax liability of $17,197, with a Recovery Rebate Credit of $1,387.

If instead, the couple files MFS, they each reduce their modified AGI to less than $150,000, and they each qualify for a $10,200 UI exclusion. They will lose their $600 dependent care credit, but their tax liability is reduced to $14,150, and their Recovery Rebate Credit for 2020 is increased to $3,766. Additionally, if you claim all four dependents on Lexi’s return, her 2020 AGI is less than $75,000, and she will then qualify for a 2021 EIP of $7,000 ($1,400 for her and each of the four dependents.)

Filing MFS saves them more than $13,000 (see the following spreadsheet and sample 1040s for the calculations).

Taxpayer and Spouse

MFJ vs. MFS comparison

Calculated with UI exclusion

1040 line MFJ Taxpayer Spouse Notes/Comments

Income

1 Wages 111,194 55,597 55,597

2b Interest 230 117 113

Sch. 1 Schedule C 38,578 19,286 19,291

Sch. 1 Passthrough income 15 8 7

Sch. 1 Unemployment comp. 33,589 6,595 6,594

9 Total income 183,606 81,603 81,602

Adjustments to income

Sch. 1 1/2 SE Tax 2,726 - 2,726 SE tax charged to wife only

Sch. 1 SEP IRA contribution 6,000 - 6,000 SEP IRA charged to wife only

10c Total adjustments 8,726 - 8,726

11 AGI 174,880 81,603 72,876

Itemized deductions

Sch. A SALT 10,000 5,000 5,000

Sch. A Mtg. interest 21,039 10,520 10,519

Sch. A Contributions 7,118 3,559 3,559

12 Total itemized ded. 38,157 19,079 19,078

13 199A deduction 5,970 3,857 2,113 Only wife has QBI reduction from 1/2

of SE tax

14 Total deductions 44,127 22,936 21,191

15 Taxable income 130,753 58,667 51,685

16 Tax 20,346 8,699 7,159

Credits

19 Child tax credit 8,000 - 7,159

Sch. 3 Dependent care credit 600 - Dependent care credit not allowed on

MFS return

21 Total credits 8,600 - 7,159

22 Income tax (net of credits) 11,746 8,699 -

Sch. 2 SE tax 5,451 - 5,451 SE tax charged to wife only

24 Total tax 17,197 8,699 5,451

25d Withholding Eliminated to illustrate tax savings

28 Add'l child tax credit - - 841

30 Recovery Rebate Credit 1,387 - 3,766

Form 7202 FFCRA SE credits 5,970 - 5,970 7202 only for wife only

32 Total other payments 7,357 - 10,577

33 Total payments 7,357 - 10,577

37 (34) Amount due (refund) 9,840 8,699 (5,126)

Tax savings 6,267

MFS

(99)Department of the Treasury ' Internal Revenue Service

Form 1040 2020 IRS Use Only ' Do not write or staple in this space.U.S. Individual Income Tax Return OMB No. 1545-0074

Filing Status Head of household (HOH) Qualifying widow(er) (QW)Single Married filing jointly Married filing separately (MFS)

Check only If you checked the MFS box, enter the name of your spouse. If you checked the HOH or QW box, enter the child's name if the qualifyingone box.

person is a child but not your dependent G

Last name Your social security number

Last name Spouse's social security number

Apt. no. Presidential Election Campaign

Check here if you, or your spouse

if filing jointly, want $3 to go to thisState ZIP code

fund. Checking a box below will

not change your tax or refund.

Foreign country name Foreign province/state/county Foreign postal codeYou Spouse

At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency? Yes No

Standard Someone can claim: You as a dependent Your spouse as a dependent

DeductionSpouse itemizes on a separate return or you were a dual-status alien

You:Age/Blindness Were born before January 2, 1956 Are blind Spouse: Was born before January 2, 1956 Is blind

(2) Social security (3) Relationship (4) b if qualifies for (see instructions):Dependents (see instructions):number to you

Child tax credit Credit for other dependents(1) First name Last nameIf more

than four

dependents,

see instructions

and check

here G

1 Wages, salaries, tips, etc. Attach Form(s) W-2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Taxable interest . . . . . . . . . . . . . . .2 2a aTax-exempt interest. . . . . . . . . .Attach b 2bSch. B if

required. 3a3a Ordinary dividends. . . . . . . . . . . . . 3bbQualified dividends. . . . . . . . . . .

IRA distributions. . . . . . . . . . . . .4 Taxable amount . . . . . . . . . . . . . . .a 4 4ba b

5a 5aPensions and annuities . . . . . . Taxable amount . . . . . . . . . . . . . . . 5bb

Taxable amount . . . . . . . . . . . . . . . 6bbSocial security benefits . . . . . . . . . . .6 6a a

7 7Capital gain or (loss). Attach Schedule D if required. If not required, check here. . . . . . . . . . . . . . . . . . . . . . . G

88 Other income from Schedule 1, line 9. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Add lines 1, 2b, 3b, 4b, 5b, 6b, 7, and 8. This is your total income. . . . . . . . . . . . . . . . . . . . . G 99Standard

10 Adjustments to income:Deduction for 'Single or? From Schedule 1, line 22. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .a 10aMarried filing

separately, $12,400 Charitable contributions if you take the standard deduction. See instructions . . .b 10b?Married filing 10cAdd lines 10a and 10b. These are your total adjustments to income. . . . . . . . . . . . . . . . . . . c Gjointly or Qualifying

widow(er), $24,800 Subtract line 10c from line 9. This is your adjusted gross income. . . . . . . . . . . . . . . . . . . . . . G11 11?Head of

12household, $18,650 Standard deduction or itemized deductions (from Schedule A). . . . . . . . . . . . . . . . . . . . . . . . . .12If you checked any? 1313 Qualified business income deduction. Attach Form 8995 or Form 8995-A . . . . . . . . . . . . . . . . . box under StandardDeduction,

1414 Add lines 12 and 13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .see instructions.

Taxable income. Subtract line 14 from line 11. If zero or less, enter -0- . . . . . . . . . . . . . . . . . .15 15

BAA For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Form 1040 (2020)

FDIA0112L 08/24/20

174,880.

38,157.

130,753.

111,194.

230.

5,970.

183,606.

Your first name and middle initial

TAXPAYER XXX-XX-XXXXIf joint return, spouse's first name and middle initial

SPOUSE XXX-XX-XXXXHome address (number and street). If you have a P.O. box, see instructions.

123 MAIN STREET

X

City, town, or post office. If you have a foreign address, also complete spaces below.

ANAHEIM, CA 92801

44,127.

8,726.

72,182.

X

8,726.

CHILD 1 XXX-XX-XXXX CHILD XCHILD 2 XXX-XX-XXXX CHILD XCHILD 3 XXX-XX-XXXX CHILD XCHILD 4 XXX-XX-XXXX CHILD X

Form 1040 (2020) Page 2

Tax (see instructions). Check if any from Form(s): 8814116

2 3 164972 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17 Amount from Schedule 2, line 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Add lines 16 and 17 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18 18

1919 Child tax credit or credit for other dependents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20Amount from Schedule 3, line 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

21Add lines 19 and 20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

Subtract line 21 from line 18. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22 22

Other taxes, including self-employment tax, from Schedule 2, line 10 . . . . . . . . . . . . . . . . . . . .23 23

2424 Add lines 22 and 23. This is your total tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G

25 Federal income tax withheld from :

a 25aForm(s) W-2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Form(s) 1099 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .b 25b

c Other forms (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25c

d Add lines 25a through 25c . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25d

26 262020 estimated tax payments and amount applied from 2019 return. . . . . . . . . . . . . . . . . . . . . .If you have a?qualifying child, Earned income credit (EIC). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27 27attach Sch. EIC.

28 28Additional child tax credit. Attach Schedule 8812 . . . . . . . . . . . . . .If you have?nontaxable 29 29American opportunity credit from Form 8863, line 8. . . . . . . . . . . . combat pay,see instructions. Recovery rebate credit. See instructions. . . . . . . . . . . . . . . . . . . . . . .30 30

31Amount from Schedule 3, line 13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Add lines 27 through 31. These are your total other payments 3232and refundable credits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G

Add lines 25d, 26, and 32. These are your total payments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 33G

34 34If line 33 is more than line 24, subtract line 24 from line 33. This is the amount you overpaid . . . . . . . . . . . . . . . .RefundG35 a Amount of line 34 you want refunded to you. If Form 8888 is attached, check here. . 35a

Direct deposit? b cG GRouting number . . . . . . . . Type: Checking SavingsSee instructions. dG Account number. . . . . . . .

36 Amount of line 34 you want applied to your 2021 estimated tax. . . . . . . . . 36G

Subtract line 33 from line 24. This is the amount you owe now. . . . . . . . . . . . . . . . . . . . . . . . . 37 37GAmountYou Owe Note: Schedule H and Schedule SE filers, line 37 may not represent all of the taxes you For details on owe for 2020. See Schedule 3, line 12e, and its instructions for details.how to pay, see

38 38Ginstructions. Estimated tax penalty (see instructions). . . . . . . . . . . . . . . . . . .

Do you want to allow another person to discuss this return with the IRS ?Third PartySee instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes. Complete below. NoGDesigneeDesignee's Phone Personal identification

G G Gname no. number (PIN)

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, theySignare true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

HereYour signature Date Your occupation If the IRS sent you an Identity Protection

PIN, enter itJoint return?here (see inst.) GSee instructions. A Date Spouse's occupation If the IRS sent your spouse an IdentitySpouse's signature. If a joint return, both must sign.Keep a copy for Protection PIN, enter

your records. it here (see inst.)G

Phone no. Email address

Date Check if:Preparer's name PTIN

Self-employedPaidPreparer GFirm's name Phone no.Use Only

G GFirm's address Firm's EIN

Form 1040 (2020)Go to www.irs.gov/Form1040 for instructions and the latest information.

FDIA0112L 08/25/20

TAXPAYER AND SPOUSE XXX-XX-XXXX

20,346.

20,346.

8,000.

600.

8,600.

11,746.

5,451.

17,197.

10,770.405.

11,175.

1,387.

5,970.

7,357.

18,532.

1,335.

1,335.X

X

Preparer's signature

OMB No. 1545-0074SCHEDULE 1Additional Income and Adjustments to Income(Form 1040)

2020A Attach to Form 1040, 1040-SR, or 1040-NR.

Department of the Treasury AttachmentA Go to www.irs.gov/Form1040 for instructions and the latest information.Internal Revenue Service 01Sequence No.

Name(s) shown on Form 1040, 1040-SR, or 1040-NR Your social security number

Part I Additional Income

1Taxable refunds, credits, or offsets of state and local income taxes . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Alimony received . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2a2a

b Date of original divorce or separation agreement (see instructions) G

3 Business income or (loss). Attach Schedule C . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Other gains or (losses). Attach Form 4797. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4 4

Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E. . . . . .5 5

6Farm income or (loss). Attach Schedule F. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

7 7Unemployment compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

GOther income. List type and amount8

8

9 Combine lines 1 through 8. Enter here and on Form 1040, 1040-SR, or 1040-NR,line 8 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Part II Adjustments to Income

10 Educator expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Certain business expenses of reservists, performing artists, and fee-basis government officials.

11Attach Form 2106. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Health savings account deduction. Attach Form 8889. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12 12

Moving expenses for members of the Armed Forces. Attach Form 3903 . . . . . . . . . . . . . . . . . . . . . .13 13

Deductible part of self-employment tax. Attach Schedule SE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1414

15Self-employed SEP, SIMPLE, and qualified plans. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Self-employed health insurance deduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1616

17 Penalty on early withdrawal of savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18a18a Alimony paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Recipient's SSN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . b G

c Date of original divorce or separation agreement (see instructions) G

19 19IRA deduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Student loan interest deduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20 20

21 Tuition and fees deduction. Attach Form 8917 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

22 Add lines 10 through 21. These are your adjustments to income. Enter here and on Form 1040,1040-SR, or 1040-NR, line 10a. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

BAA For Paperwork Reduction Act Notice, see your tax return instructions. Schedule 1 (Form 1040) 2020

FDIA0103L 08/26/20

TAXPAYER AND SPOUSE XXX-XX-XXXX

8,726.

2,726.

6,000.

0.

38,578.

15.

33,589.

72,182.

STATEMENT 2

(99)Department of the Treasury ' Internal Revenue Service

Form 1040 2020 IRS Use Only ' Do not write or staple in this space.U.S. Individual Income Tax Return OMB No. 1545-0074

Filing Status Head of household (HOH) Qualifying widow(er) (QW)Single Married filing jointly Married filing separately (MFS)

Check only If you checked the MFS box, enter the name of your spouse. If you checked the HOH or QW box, enter the child's name if the qualifyingone box.

person is a child but not your dependent G

Last name Your social security number

If joint return, spouse's first name and middle initial Last name Spouse's social security number

Apt. no. Presidential Election Campaign

Check here if you, or your spouse

if filing jointly, want $3 to go to thisState ZIP code

fund. Checking a box below will

not change your tax or refund.

Foreign country name Foreign province/state/county Foreign postal codeYou Spouse

At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency? Yes No

Standard Someone can claim: You as a dependent Your spouse as a dependent

DeductionSpouse itemizes on a separate return or you were a dual-status alien

You:Age/Blindness Were born before January 2, 1956 Are blind Spouse: Was born before January 2, 1956 Is blind

(2) Social security (3) Relationship (4) b if qualifies for (see instructions):Dependents (see instructions):number to you

Child tax credit Credit for other dependents(1) First name Last nameIf more

than four

dependents,

see instructions

and check

here G

1 Wages, salaries, tips, etc. Attach Form(s) W-2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Taxable interest . . . . . . . . . . . . . . .2 2a aTax-exempt interest. . . . . . . . . .Attach b 2bSch. B if

required. 3a3a Ordinary dividends. . . . . . . . . . . . . 3bbQualified dividends. . . . . . . . . . .

IRA distributions. . . . . . . . . . . . .4 Taxable amount . . . . . . . . . . . . . . .a 4 4ba b

5a 5aPensions and annuities . . . . . . Taxable amount . . . . . . . . . . . . . . . 5bb

Taxable amount . . . . . . . . . . . . . . . 6bbSocial security benefits . . . . . . . . . . .6 6a a

7 7Capital gain or (loss). Attach Schedule D if required. If not required, check here. . . . . . . . . . . . . . . . . . . . . . . G

88 Other income from Schedule 1, line 9. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Add lines 1, 2b, 3b, 4b, 5b, 6b, 7, and 8. This is your total income. . . . . . . . . . . . . . . . . . . . . G 99Standard

10 Adjustments to income:Deduction for 'Single or? From Schedule 1, line 22. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .a 10aMarried filing

separately, $12,400 Charitable contributions if you take the standard deduction. See instructions . . .b 10b?Married filing 10cAdd lines 10a and 10b. These are your total adjustments to income. . . . . . . . . . . . . . . . . . . c Gjointly or Qualifying

widow(er), $24,800 Subtract line 10c from line 9. This is your adjusted gross income. . . . . . . . . . . . . . . . . . . . . . G11 11?Head of

12household, $18,650 Standard deduction or itemized deductions (from Schedule A). . . . . . . . . . . . . . . . . . . . . . . . . .12If you checked any? 1313 Qualified business income deduction. Attach Form 8995 or Form 8995-A . . . . . . . . . . . . . . . . . box under StandardDeduction,

1414 Add lines 12 and 13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .see instructions.

Taxable income. Subtract line 14 from line 11. If zero or less, enter -0- . . . . . . . . . . . . . . . . . .15 15

BAA For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Form 1040 (2020)

FDIA0112L 08/24/20

81,603.

19,079.

58,667.

55,597.

117.

3,857.

81,603.

Your first name and middle initial

TAXPAYER XXX-XX-XXXX

XXX-XX-XXXXHome address (number and street). If you have a P.O. box, see instructions.

123 MAIN STREET

X

City, town, or post office. If you have a foreign address, also complete spaces below.

ANAHEIM, CA 92801

X

22,936.

25,889.

X

SPOUSE

Form 1040 (2020) Page 2

Tax (see instructions). Check if any from Form(s): 8814116

2 3 164972 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17 Amount from Schedule 2, line 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Add lines 16 and 17 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18 18

1919 Child tax credit or credit for other dependents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20Amount from Schedule 3, line 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

21Add lines 19 and 20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

Subtract line 21 from line 18. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22 22

Other taxes, including self-employment tax, from Schedule 2, line 10 . . . . . . . . . . . . . . . . . . . .23 23

2424 Add lines 22 and 23. This is your total tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G

25 Federal income tax withheld from :

a 25aForm(s) W-2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Form(s) 1099 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .b 25b

c Other forms (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25c

d Add lines 25a through 25c . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25d

26 262020 estimated tax payments and amount applied from 2019 return. . . . . . . . . . . . . . . . . . . . . .If you have a?qualifying child, Earned income credit (EIC). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27 27attach Sch. EIC.

28 28Additional child tax credit. Attach Schedule 8812 . . . . . . . . . . . . . .If you have?nontaxable 29 29American opportunity credit from Form 8863, line 8. . . . . . . . . . . . combat pay,see instructions. Recovery rebate credit. See instructions. . . . . . . . . . . . . . . . . . . . . . .30 30

31Amount from Schedule 3, line 13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Add lines 27 through 31. These are your total other payments 3232and refundable credits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G

Add lines 25d, 26, and 32. These are your total payments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 33G

34 34If line 33 is more than line 24, subtract line 24 from line 33. This is the amount you overpaid . . . . . . . . . . . . . . . .RefundG35 a Amount of line 34 you want refunded to you. If Form 8888 is attached, check here. . 35a

Direct deposit? b cG GRouting number . . . . . . . . Type: Checking SavingsSee instructions. dG Account number. . . . . . . .

36 Amount of line 34 you want applied to your 2021 estimated tax. . . . . . . . . 36G

Subtract line 33 from line 24. This is the amount you owe now. . . . . . . . . . . . . . . . . . . . . . . . . 37 37GAmountYou Owe Note: Schedule H and Schedule SE filers, line 37 may not represent all of the taxes you For details on owe for 2020. See Schedule 3, line 12e, and its instructions for details.how to pay, see

38 38Ginstructions. Estimated tax penalty (see instructions). . . . . . . . . . . . . . . . . . .

Do you want to allow another person to discuss this return with the IRS ?Third PartySee instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes. Complete below. NoGDesigneeDesignee's Phone Personal identification

G G Gname no. number (PIN)

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, theySignare true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

HereYour signature Date Your occupation If the IRS sent you an Identity Protection

PIN, enter itJoint return?here (see inst.) GSee instructions. A Date Spouse's occupation If the IRS sent your spouse an IdentitySpouse's signature. If a joint return, both must sign.Keep a copy for Protection PIN, enter

your records. it here (see inst.)G

Phone no. Email address

Date Check if:Preparer's name PTIN

Self-employedPaidPreparer GFirm's name Phone no.Use Only

G GFirm's address Firm's EIN

Form 1040 (2020)Go to www.irs.gov/Form1040 for instructions and the latest information.

FDIA0112L 08/25/20

TAXPAYER XXX-XX-XXXX

8,699.

8,699.

0.

8,699.

8,699.

5,386.203.

5,589.

5,589.

3,149.

39.

X

Preparer's signature

OMB No. 1545-0074SCHEDULE 1Additional Income and Adjustments to Income(Form 1040)

2020A Attach to Form 1040, 1040-SR, or 1040-NR.

Department of the Treasury AttachmentA Go to www.irs.gov/Form1040 for instructions and the latest information.Internal Revenue Service 01Sequence No.

Name(s) shown on Form 1040, 1040-SR, or 1040-NR Your social security number

Part I Additional Income

1Taxable refunds, credits, or offsets of state and local income taxes . . . . . . . . . . . . . . . . . . . . . . . . . .1

Alimony received . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2a2a

b Date of original divorce or separation agreement (see instructions) G

3 Business income or (loss). Attach Schedule C . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Other gains or (losses). Attach Form 4797. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4 4

Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E. . . . . .5 5

6Farm income or (loss). Attach Schedule F. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

7 7Unemployment compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

GOther income. List type and amount8

8

9 Combine lines 1 through 8. Enter here and on Form 1040, 1040-SR, or 1040-NR,line 8 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Part II Adjustments to Income

10 Educator expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Certain business expenses of reservists, performing artists, and fee-basis government officials.

11Attach Form 2106. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Health savings account deduction. Attach Form 8889. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12 12

Moving expenses for members of the Armed Forces. Attach Form 3903 . . . . . . . . . . . . . . . . . . . . . .13 13

Deductible part of self-employment tax. Attach Schedule SE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1414

15Self-employed SEP, SIMPLE, and qualified plans. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Self-employed health insurance deduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1616

17 Penalty on early withdrawal of savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18a18a Alimony paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Recipient's SSN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . b G

c Date of original divorce or separation agreement (see instructions) G

19 19IRA deduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Student loan interest deduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20 20

21 Tuition and fees deduction. Attach Form 8917 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

22 Add lines 10 through 21. These are your adjustments to income. Enter here and on Form 1040,1040-SR, or 1040-NR, line 10a. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

BAA For Paperwork Reduction Act Notice, see your tax return instructions. Schedule 1 (Form 1040) 2020

FDIA0103L 08/26/20

TAXPAYER XXX-XX-XXXX

0.

19,286.

8.

16,795.

-10,200.

25,889.

UCE

(99)Department of the Treasury ' Internal Revenue Service

Form 1040 2020 IRS Use Only ' Do not write or staple in this space.U.S. Individual Income Tax Return OMB No. 1545-0074

Filing Status Head of household (HOH) Qualifying widow(er) (QW)Single Married filing jointly Married filing separately (MFS)

Check only If you checked the MFS box, enter the name of your spouse. If you checked the HOH or QW box, enter the child's name if the qualifyingone box.

person is a child but not your dependent G

Last name Your social security number

If joint return, spouse's first name and middle initial Last name Spouse's social security number

Apt. no. Presidential Election Campaign

Check here if you, or your spouse

if filing jointly, want $3 to go to thisState ZIP code

fund. Checking a box below will

not change your tax or refund.

Foreign country name Foreign province/state/county Foreign postal codeYou Spouse

At any time during 2020, did you receive, sell, send, exchange, or otherwise acquire any financial interest in any virtual currency? Yes No

Standard Someone can claim: You as a dependent Your spouse as a dependent

DeductionSpouse itemizes on a separate return or you were a dual-status alien

You:Age/Blindness Were born before January 2, 1956 Are blind Spouse: Was born before January 2, 1956 Is blind

(2) Social security (3) Relationship (4) b if qualifies for (see instructions):Dependents (see instructions):number to you

Child tax credit Credit for other dependents(1) First name Last nameIf more

than four

dependents,

see instructions

and check

here G

1 Wages, salaries, tips, etc. Attach Form(s) W-2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

Taxable interest . . . . . . . . . . . . . . .2 2a aTax-exempt interest. . . . . . . . . .Attach b 2bSch. B if

required. 3a3a Ordinary dividends. . . . . . . . . . . . . 3bbQualified dividends. . . . . . . . . . .

IRA distributions. . . . . . . . . . . . .4 Taxable amount . . . . . . . . . . . . . . .a 4 4ba b

5a 5aPensions and annuities . . . . . . Taxable amount . . . . . . . . . . . . . . . 5bb

Taxable amount . . . . . . . . . . . . . . . 6bbSocial security benefits . . . . . . . . . . .6 6a a

7 7Capital gain or (loss). Attach Schedule D if required. If not required, check here. . . . . . . . . . . . . . . . . . . . . . . G

88 Other income from Schedule 1, line 9. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Add lines 1, 2b, 3b, 4b, 5b, 6b, 7, and 8. This is your total income. . . . . . . . . . . . . . . . . . . . . G 99Standard

10 Adjustments to income:Deduction for 'Single or? From Schedule 1, line 22. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .a 10aMarried filing

separately, $12,400 Charitable contributions if you take the standard deduction. See instructions . . .b 10b?Married filing 10cAdd lines 10a and 10b. These are your total adjustments to income. . . . . . . . . . . . . . . . . . . c Gjointly or Qualifying

widow(er), $24,800 Subtract line 10c from line 9. This is your adjusted gross income. . . . . . . . . . . . . . . . . . . . . . G11 11?Head of

12household, $18,650 Standard deduction or itemized deductions (from Schedule A). . . . . . . . . . . . . . . . . . . . . . . . . .12If you checked any? 1313 Qualified business income deduction. Attach Form 8995 or Form 8995-A . . . . . . . . . . . . . . . . . box under StandardDeduction,

1414 Add lines 12 and 13. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .see instructions.

Taxable income. Subtract line 14 from line 11. If zero or less, enter -0- . . . . . . . . . . . . . . . . . .15 15

BAA For Disclosure, Privacy Act, and Paperwork Reduction Act Notice, see separate instructions. Form 1040 (2020)

FDIA0112L 08/24/20

72,876.

19,078.

51,685.

55,597.

113.

2,113.

81,602.

Your first name and middle initial

SPOUSE XXX-XX-XXXX

XXX-XX-XXXXHome address (number and street). If you have a P.O. box, see instructions.

123 MAIN STREET

X

City, town, or post office. If you have a foreign address, also complete spaces below.

ANAHEIM, CA 92801

X

21,191.

8,726.

25,892.

X

8,726.

CHILD 1 XXX-XX-XXXX CHILD XCHILD 2 XXX-XX-XXXX CHILD XCHILD 3 XXX-XX-XXXX CHILD XCHILD 4 XXX-XX-XXXX CHILD X

TAXPAYER

Form 1040 (2020) Page 2

Tax (see instructions). Check if any from Form(s): 8814116

2 3 164972 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

17 Amount from Schedule 2, line 3 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Add lines 16 and 17 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .18 18

1919 Child tax credit or credit for other dependents . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20Amount from Schedule 3, line 7 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20

21Add lines 19 and 20 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .21

Subtract line 21 from line 18. If zero or less, enter -0-. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .22 22

Other taxes, including self-employment tax, from Schedule 2, line 10 . . . . . . . . . . . . . . . . . . . .23 23

2424 Add lines 22 and 23. This is your total tax. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G

25 Federal income tax withheld from :

a 25aForm(s) W-2. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Form(s) 1099 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .b 25b

c Other forms (see instructions). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25c

d Add lines 25a through 25c . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25d

26 262020 estimated tax payments and amount applied from 2019 return. . . . . . . . . . . . . . . . . . . . . .If you have a?qualifying child, Earned income credit (EIC). . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .27 27attach Sch. EIC.

28 28Additional child tax credit. Attach Schedule 8812 . . . . . . . . . . . . . .If you have?nontaxable 29 29American opportunity credit from Form 8863, line 8. . . . . . . . . . . . combat pay,see instructions. Recovery rebate credit. See instructions. . . . . . . . . . . . . . . . . . . . . . .30 30

31Amount from Schedule 3, line 13 . . . . . . . . . . . . . . . . . . . . . . . . . . . . .31

Add lines 27 through 31. These are your total other payments 3232and refundable credits. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . G

Add lines 25d, 26, and 32. These are your total payments. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33 33G

34 34If line 33 is more than line 24, subtract line 24 from line 33. This is the amount you overpaid . . . . . . . . . . . . . . . .RefundG35 a Amount of line 34 you want refunded to you. If Form 8888 is attached, check here. . 35a

Direct deposit? b cG GRouting number . . . . . . . . Type: Checking SavingsSee instructions. dG Account number. . . . . . . .

36 Amount of line 34 you want applied to your 2021 estimated tax. . . . . . . . . 36G

Subtract line 33 from line 24. This is the amount you owe now. . . . . . . . . . . . . . . . . . . . . . . . . 37 37GAmountYou Owe Note: Schedule H and Schedule SE filers, line 37 may not represent all of the taxes you For details on owe for 2020. See Schedule 3, line 12e, and its instructions for details.how to pay, see

38 38Ginstructions. Estimated tax penalty (see instructions). . . . . . . . . . . . . . . . . . .

Do you want to allow another person to discuss this return with the IRS ?Third PartySee instructions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . Yes. Complete below. NoGDesigneeDesignee's Phone Personal identification

G G Gname no. number (PIN)

Under penalties of perjury, I declare that I have examined this return and accompanying schedules and statements, and to the best of my knowledge and belief, theySignare true, correct, and complete. Declaration of preparer (other than taxpayer) is based on all information of which preparer has any knowledge.

HereYour signature Date Your occupation If the IRS sent you an Identity Protection

PIN, enter itJoint return?here (see inst.) GSee instructions. A Date Spouse's occupation If the IRS sent your spouse an IdentitySpouse's signature. If a joint return, both must sign.Keep a copy for Protection PIN, enter

your records. it here (see inst.)G

Phone no. Email address

Date Check if:Preparer's name PTIN

Self-employedPaidPreparer GFirm's name Phone no.Use Only

G GFirm's address Firm's EIN

Form 1040 (2020)Go to www.irs.gov/Form1040 for instructions and the latest information.

FDIA0112L 08/25/20

SPOUSE XXX-XX-XXXX

7,159.

7,159.

7,159.

7,159.

0.

5,451.

5,451.

5,384.202.

5,586.

841.

3,766.

5,970.

10,577.

16,163.

10,712.

10,712.X

X

Preparer's signature

OMB No. 1545-0074SCHEDULE 1Additional Income and Adjustments to Income(Form 1040)

2020A Attach to Form 1040, 1040-SR, or 1040-NR.

Department of the Treasury AttachmentA Go to www.irs.gov/Form1040 for instructions and the latest information.Internal Revenue Service 01Sequence No.

Name(s) shown on Form 1040, 1040-SR, or 1040-NR Your social security number

Part I Additional Income

1Taxable refunds, credits, or offsets of state and local income taxes . . . . . . . . . . . . . . . . . . . . . . . . . .1

Alimony received . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 2a2a

b Date of original divorce or separation agreement (see instructions) G

3 Business income or (loss). Attach Schedule C . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 3

Other gains or (losses). Attach Form 4797. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .4 4

Rental real estate, royalties, partnerships, S corporations, trusts, etc. Attach Schedule E. . . . . .5 5

6Farm income or (loss). Attach Schedule F. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .6

7 7Unemployment compensation. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

GOther income. List type and amount8

8

9 Combine lines 1 through 8. Enter here and on Form 1040, 1040-SR, or 1040-NR,line 8 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9

Part II Adjustments to Income

10 Educator expenses . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

11 Certain business expenses of reservists, performing artists, and fee-basis government officials.

11Attach Form 2106. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Health savings account deduction. Attach Form 8889. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .12 12

Moving expenses for members of the Armed Forces. Attach Form 3903 . . . . . . . . . . . . . . . . . . . . . .13 13

Deductible part of self-employment tax. Attach Schedule SE. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1414

15Self-employed SEP, SIMPLE, and qualified plans. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .15

Self-employed health insurance deduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1616

17 Penalty on early withdrawal of savings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

18a18a Alimony paid . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Recipient's SSN . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . b G

c Date of original divorce or separation agreement (see instructions) G

19 19IRA deduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

Student loan interest deduction. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .20 20

21 Tuition and fees deduction. Attach Form 8917 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

22 Add lines 10 through 21. These are your adjustments to income. Enter here and on Form 1040,1040-SR, or 1040-NR, line 10a. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

BAA For Paperwork Reduction Act Notice, see your tax return instructions. Schedule 1 (Form 1040) 2020

FDIA0103L 08/26/20

SPOUSE XXX-XX-XXXX

8,726.

2,726.

6,000.

19,291.

7.

16,794.

-10,200.

25,892.

UCE

American Rescue Plan: Tax Implications

©2021 19 Spidell Publishing, Inc.®

Dependent loophole closing? A big loophole under the previous EIP programs had to do with dependents who were claimed

on one taxpayer’s return during 2019 but on another taxpayer’s return on 2020. In this situation, an EIP advance was sent to the taxpayer who filed the return in 2019, and then the taxpayer who claimed the dependent on the 2020 return could claim a “Recovery Rebate Credit” for that dependent on the 2020 return.

This loophole may be closing with this latest round of EIPs. The ARPA directs the IRS to issue “regulations or other guidance to ensure to the maximum extent administratively practicable that, in determining the amount of any [credit or refund] an individual is not taken into account more than once, including by different taxpayers and including by reason of a change in joint return status or dependent status between the taxable year for which an advance refund amount is determined and the taxable year for which a credit under is determined.” (IRC §6428B(h)(2))

Social Security numbers required As with the first two rounds of EIPS, the credit (including the advance credit) is only available to

taxpayers with Social Security numbers. (IRC §6428B(e)(2)) For taxpayers filing a joint return and/or claiming a dependent qualifying child, the return must also include the spouse’s Social Security number and any qualifying child’s Social Security number if they are included on the return.

The only exceptions are:

• If one spouse is a member of the Armed Forces, then a Social Security number need only be provided for one of the spouses; and

• If the credit is taken for a qualifying child who is adopted or placed for adoption, the adoption taxpayer identification number should be used.