american wind en ergy association u.s. wind industry third ......market report a product of awea...

TRANSCRIPT

American Wind Energy Association U.S. Wind Industry Third Quarter 2018

Market Report

A product of AWEA Data Services

Released October 25, 2018

The U.S. wind industry installed 612 megawatts (MW) in the third quarter of 2018, bringing year-to-date installations to 1,644 MW. There are now 90,550 MW of installed wind capacity in the United States.

Project developers reported a combined 37,965 MW of wind capacity under construction or in advanced development as of the end of the third quarter, a 28% year-over-year increase. Construction activity reached a new record of 20,798 MW after construction started on 2,180 MW in the third quarter.

Project developers announced 2,467 MW of PPAs signed during the third quarter, contributing to a total of 7,550 MW contracted year-to-date in 2018. PPA activity for the year exceeds total PPA volumes in each of the past four years and marks the most active year for corporate and non-utility PPAs.

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 2

Table of ContentsThird Quarter Hightlights 3U.S. Wind Power Capacity Growth U.S. Annual and Cumulative Wind Power Capacity Growth 4 Quarterly U.S. Wind Power Capacity Installations 5 New Wind Power Capacity Installations in Third Quarter 2018, by State 6

2018 Wind Power Capacity Installations, Top States 7

U.S. Wind Power Cumulative Installed Capacity, by State 8

Wind Power Capacity Under Construction or in Advanced Development 9 Wind Power Capacity Under Construction 10 Wind Power Capacity Under Construction, by State Member Version Only

Wind Power Capacity in Advanced Development, by State Member Version Only

Wind Power Capacity Under Construction or in Advanced Development, Top States Member Version Only

Wind Power Capacity in Advanced Development Member Version Only

Wind Power Procurement Activity

Wind Power Capacity Offtake Status Member Version Only

Power Purchase Agreements Signed in 2018 Member Version Only

Map of Power Purchase Agreements Signed in 2018 Member Version Only

Mergers & Acquisition Activity Member Version Only

Wind Turbine Market Trends

Wind Turbine Manufacturer Market Member Version Only

Turbine Technology Trends Member Version Only

Regional Turbine Technology Trends Member Version Only

U.S. Offshore Wind Energy Activity Member Version Only

Appendices

Map of Projects Online during 2018, Under Construction, or in Advanced Development 23

Utility-Scale Wind Projects Completed during 2018 24

Utility-Scale Wind Projects Under Construction Member Version Only

Utility-Scale Wind Projects in Advanced Development Member Version Only

2018 Power Purchase Agreements Member Version Only

2018 Project Acquisition Activity Member Version Only

Electric Utility Renewable Energy Requests for Proposals (RFPs) Member Version Only

AWEA Data Services 42

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 3

Third Quarter Highlights

2018 Wind Project Installations• The U.S. wind industry installed 612 MW of new wind power capacity during the third quarter of 2018, a 15% increase in installations over the third quarter of

2017. Year-to-date the industry has commissioned 1,644 MW of wind power capacity.

• A total of 11 new wind projects were commissioned across seven states during the third quarter. Texas led with 216 MW installed, followed by Oklahoma (199 MW), and Ohio (108 MW).

• In addition to new capacity additions, developers completed 329 MW of partial repowerings across three projects in the third quarter.

• There are now 90,550 MW of cumulative installed wind capacity in the United States, with more than 54,000 wind turbines operating in 41 states plus Guam and Puerto Rico.

Wind Capacity Under Construction or in Advanced Development• Construction activity reached a new record of 20,798 MW at the end of the third quarter, with an additional 17,167 MW in advanced development. The combined 37,965

MW represent a 28% year-over-year increase.

• Projects totaling 2,180 MW started construction and a further 2,327 MW entered advanced development during the third quarter, a combined 4,507 MW in new announcements.

• At the regional level, 33% of combined activity is located in the Midwest, 21% in Texas, 20% in the Mountain West and 15% in the Plains states.

• Seven states now have more capacity under construction or in advanced development than currently operating.

Wind Power Procurement Activity • Project developers announced 2,467 MW of new PPAs in the third quarter, bringing year-to-date activity to 7,550 MW. PPA activity in the first three quarters

already exceeds total PPA volumes in each of the past four years.

• Utilities signed contracts for 1,522 MW of wind capacity in the third quarter, with Eversource Energy, National Grid, and Unitil procuring 800 MW from the Vineyard Wind offshore project.

• Corporate and other non-utility customers signed 38% (945 MW) of capacity contracted in the third quarter, including eight first time wind buyers. Through the first three quarters alone, 2018 is already the most active year for corporate and non-utility PPAs, surpassing the record previously set in 2015.

Turbine Technology Trends• GE Renewable Energy turbines represent 63% of the U.S. wind turbine market in the first three quarters of 2018, while Vestas represents 26% and Goldwind

represents 10%.

• The third quarter witnessed the entry of the first 4 MW onshore wind turbines in the U.S. with orders announced by both Senvion and Vestas.

• The majority of projects under construction or in advanced development have selected turbines with a nameplate capacity between 2 MW and 3 MW, while about 30% of projects where turbines have been reported are using turbines rated 3 MW or larger.

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 4

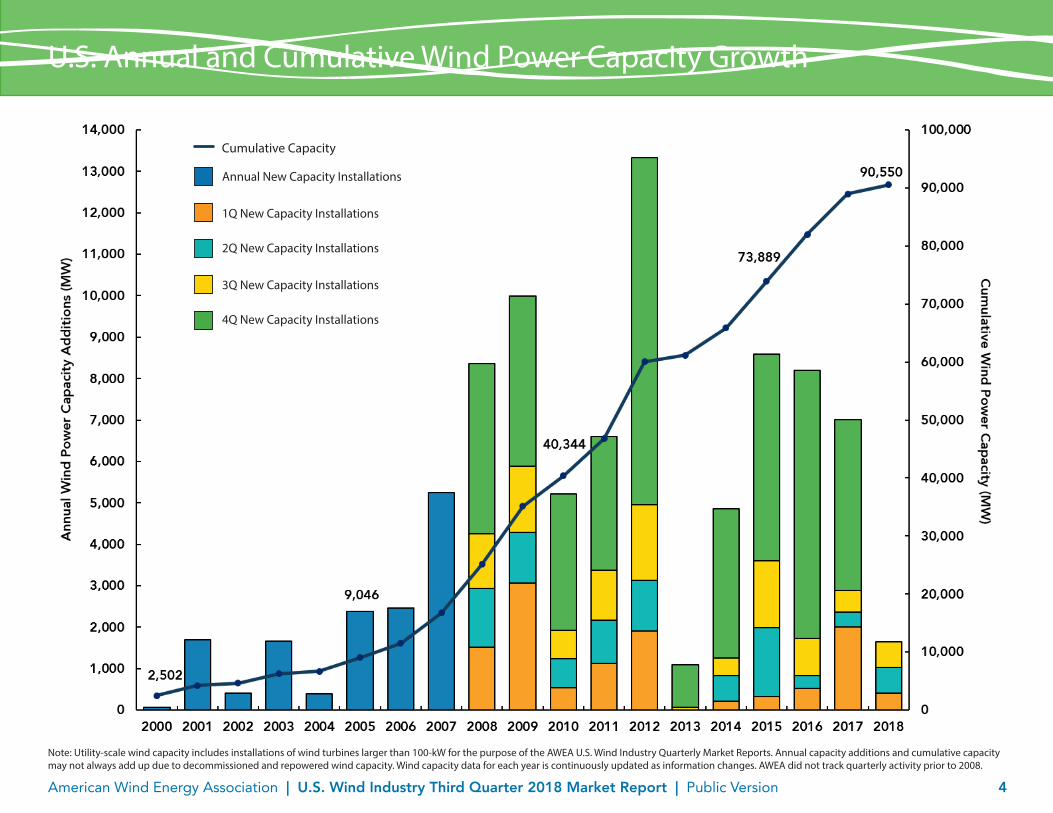

Note: Utility-scale wind capacity includes installations of wind turbines larger than 100-kW for the purpose of the AWEA U.S. Wind Industry Quarterly Market Reports. Annual capacity additions and cumulative capacity may not always add up due to decommissioned and repowered wind capacity. Wind capacity data for each year is continuously updated as information changes. AWEA did not track quarterly activity prior to 2008.

U.S. Annual and Cumulative Wind Power Capacity Growth

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

201820172016201520142013201220112010200920082007200620052004200320022001

Cumulative Capacity

Annual New Capacity Installations

1Q New Capacity Installations

2Q New Capacity Installations

3Q New Capacity Installations

4Q New Capacity Installations

4,195 4,6036,268 6,665

9,04611,512

16,765

25,135

35,128

40,344

46,777

60,065

Win

d Po

wer

Cap

acity

(MW

)

61,135

65,872

73,889

82,005

88,97390,551

Cumulative Capacity

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 5

Quarterly U.S. Wind Power Capacity Installations

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

2018201720162015201420132012201120102009

Win

d Po

wer

Cap

acity

(MW

)

3,072

1,221

1,589

4,116

539704 673

3,299

1,1181,050

1,207

3,230

1,912

1,213

1,834

8,382

2 0 70

1,016

217

1Q

2Q

3Q

4Q

619419

3,603

333

1,6611,603

4,998

520310

895

6,478

2,000

357534

4,125

406

626 612

• The U.S. wind industry installed 612 MW of wind power capacity during the third quarter of 2018, a 15% increase in installations over the third quarter of 2017.

• Year-to-date installations are down 43% compared to the first three quarters of 2017, but are roughly on par with 2016 installation activity.

• In addition to new capacity additions, developers completed 329 MW of partial repowerings across three projects in the third quarter.

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 6

New Wind Power Capacity Installations in Third Quarter 2018, by State

RI CT

MA

HI

ALMS

AR

LA

GA

KYVA

NC

SC

FL

NV

MO

IL IN

WI MI

NY78

ME

MN

KS

TX216

AZ

CA3

CO

DE

ID

MD

MT

NE7

NH

NJ

SD

OH108

OK199

PA

UT

VT

OR

WA

WV

WY

AK 1

0 to 100 MW

>100 MW to 250 MW >250 MW to 500 MW >500 MW to 1,000 MW >1,000 MW

TN

GU

IA

ND

NM

PR

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 7

0100 200 300 400 500 600 700 800 900

Minnesota

Alaska

Massachusetts

Iowa

Montana

Nebraska

Michigan

New York

Ohio

Illinois

California

Oklahoma

Texas

1Q 2018 Installations

Wind Power Capacity (MW)

2Q 2018 Installations

3Q 2018 Installations

464200

199

131

132

108

78

44

30

25

216

4

2

1

1

2018 Wind Power Capacity Installations, Top States

• Developers commissioned a total of 11 new wind projects totaling 621 MW across seven states during the third quarter.

• Texas led in third quarter installations with 216 MW, followed by Oklahoma (199 MW), and Ohio (108 MW). Texas and Oklahoma also lead in installations year to date in 2018.

• Alaska commissioned its first wind turbine since 2013, while New York saw the largest project built in the state since 2013.

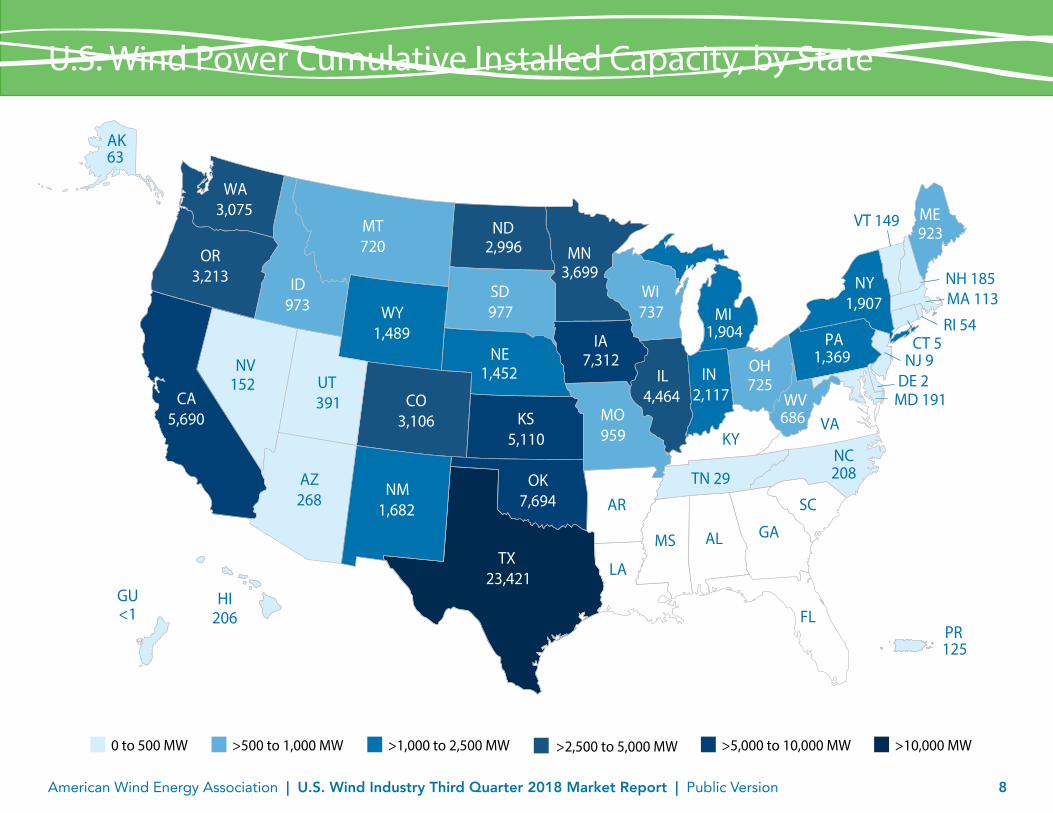

• Texas continues to lead the nation with 23,421 MW of cumulative installed capacity.

• While Oklahoma strengthened its second place ranking in the third quarter, Iowa is on track to surpass Oklahoma and reclaim the second spot by the end of the year.

StateTotal Installed Capacity (MW)

2018 Capacity Additions (MW)

Texas 23,421 880

Oklahoma 7,694 199

Iowa 7,312 4

California 5,690 135

Kansas 5,110 0

Top Five States by Cumulative Installed Wind Power Capacity

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 8

RI 54 CT 5

MA 113

HI206

ALMS

AR

LA

GA

KYVA

NC

SC

FL

NV152

MO959

IL4,464

IN2,117

WI737 MI

1,904

NY1,907

ME923

IA7,312

MN3,699

KS5,110

ND2,996

AZ268

CA5,690

CO3,106

DE 2

ID973

MD 191

MT720

NE1,452

NH 185

NJ 9

NM1,682

SD977

OH725

OK7,694

PA1,369

TN 29

TX23,421

UT391

VT 149

OR3,213

WA3,075

WV686

WY1,489

PR125

AK63

0 to 500 MW

>500 to 1,000 MW >1,000 to 2,500 MW >5,000 to 10,000 MW >10,000 MW

GU<1

208

>2,500 to 5,000 MW

U.S. Wind Power Cumulative Installed Capacity, by State

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 9

• There are now 37,965 MW of wind power capacity under construction (20,798 MW) or in advanced development (17,167 MW), a 28% year- over-year increase.

• Project developers announced 4,507 MW in combined new activity during the third quarter, with projects totaling 2,180 MW starting construction and 2,327 MW entering the advanced development phase.

• While advanced development activity trended higher than construction activity at the beginning of the year, the last two quarters saw a number of projects move into the construction phase.

• Wind projects currently under construction have been underway for an average of three quarters, while projects in advanced development have been underway for an average of one year. Nearly 50% of the 37,965 MW underway started construction or entered advanced development in 2018.

Wind Power Capacity Under Construction or in Advanced Development

Under Construction End of Quarter Advanced Development End of Quarter Combined Total

Win

d Po

wer

Cap

acity

(MW

) 25,819

23,977

21,344

23,280

18,279

15,231

29,63428,668

33,449

37,794 37,965

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

3Q182Q181Q184Q173Q172Q171Q174Q163Q162Q161Q16

Announcement Year

5,060

7,405

9,479

9,222

Current Construction and Advanced Development Pipeline by Announcement YearConstruction and Advanced Development Activity over Time

0

5,000

10,000

15,000

20,000

201820172016Pre 2016

4,507 MW in new announcements

Under Construction Advanced Development

9,222

9,069

5,470

7,4052,360

3,392

780

267

Win

d Po

wer

Cap

acity

(MW

)

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 10

Wind Power Capacity Under Construction

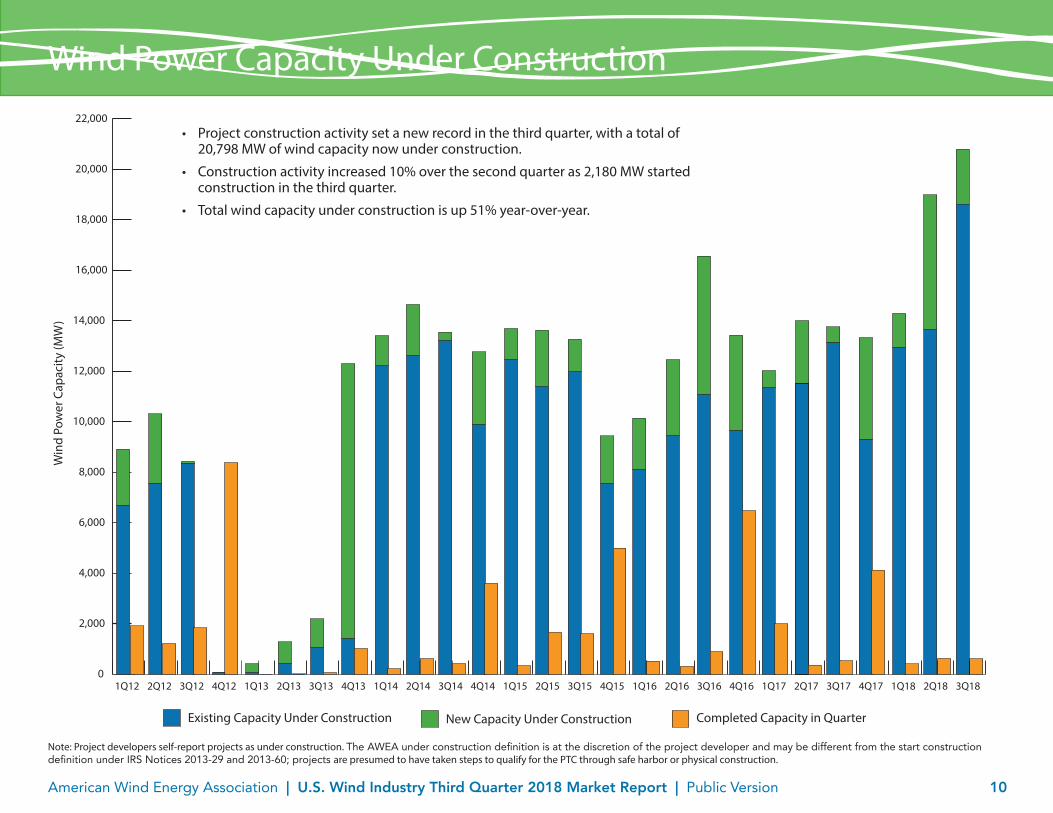

Note: Project developers self-report projects as under construction. The AWEA under construction definition is at the discretion of the project developer and may be different from the start construction definition under IRS Notices 2013-29 and 2013-60; projects are presumed to have taken steps to qualify for the PTC through safe harbor or physical construction.

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

3Q182Q181Q184Q173Q172Q171Q174Q163Q162Q161Q164Q153Q152Q151Q154Q143Q142Q141Q144Q133Q132Q131Q134Q123Q122Q121Q12

Win

d Po

wer

Cap

acity

(MW

)

Existing Capacity Under Construction New Capacity Under Construction Completed Capacity in Quarter

• Project construction activity set a new record in the third quarter, with a total of 20,798 MW of wind capacity now under construction.

• Construction activity increased 10% over the second quarter as 2,180 MW started construction in the third quarter.

• Total wind capacity under construction is up 51% year-over-year.

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 11

Wind Power Capacity Under Construction, by State

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 12

Wind Power Capacity in Advanced Development, by State

Note: AWEA defines a project as in advanced development if it has not yet started construction, but has either signed a PPA, announced a firm turbine order, or been announced to proceed under utility ownership.

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 13

Wind Power Capacity Under Construction or in Advanced Development, Top States

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 14

Wind Power Capacity in Advanced Development

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 15

Wind Power Capacity Offtake Status

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 16

Power Purchase Agreements Signed in 2018

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 17

Map of Power Purchase Agreements Signed in 2018

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 18

Mergers & Acquisitions Activity

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 19

Wind Turbine Manufacturer Market

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 20

Turbine Technology Trends

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 21

Regional Turbine Technology Trends

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 22

• Demand for offshore wind energy continued in the third quarter, with new PPAs and announcements for solicitations totaling up to 2,000 MW of offshore capacity.

• New Jersey opened a solicitation in September for 800 MW of offshore wind, the first solicition for the state to help meet its target of 3,500 MW of offshore wind by 2030.

• In the same month, Rhode Island utility Narragansett Electric issued an RFP for 400 MW renewable energy, which is open to offshore wind.

• New York also announced that the state will hold its first large-scale solicitation for 800 MW of offshore by the end of 2018.

• In August, National Grid USA, Eversource Energy, and Unitil Corp filed contracts with the Massachusetts Public Utilities commission for 800 MW of the Vineyard Wind project. The three utilities will buy energy and RECs from Vineyard Wind at a total levelized price of 6.5 cents per kilowatt hour, the lowest offshore wind PPA price in the U.S. to date. Vineyard Wind was selected as the winner of Massachusetts’ first major offshore wind solicitation earlier this year.

• Also in August, Dominion Energy filed with Virginia for approval to build the 12 MW Coastal Virginia Offshore Wind project and Ørsted signed a subcontract with Siemens Gamesa Renewable Energy for two 6-MW SWT-6.0-154 turbines for the project.

• In addition, EDF Renewables and Fishermen’s Energy of New Jersey filed an application for approval of the Nautilus Offshore Wind Project off of New Jersey from the New Jersey Board of Public Utilities.

U.S. Offshore Wind Energy Activity

State RFP Project Winners

RFP State Project NameProject Capacity

(MW) Project Developer Project Location Power Purchaser

Massachusetts Vineyard Wind 800 Avangrid Renewables; Copenhagen Infrastructure Partners Offshore Massachusetts Eversource Energy, National Grid, Unitil

Rhode Island Revolution Wind 400 Deepwater Wind Area of Mutual Interest between RI & MA National Grid

Connecticut Revolution Wind 200 Deepwater Wind Area of Mutual Interest between RI & MA Eversource Energy and United Illuminating Co

Maryland Maryland Offshore Wind Project 248 U.S. Wind Inc Offshore Maryland Maryland PSC (ORECs)

Maryland Skipjack Wind Farm 120 Deepwater Wind Offshore Delaware Maryland PSC (ORECs)

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 23

Map of Projects Online during 2018, Under Construction, or in Advanced Development

Projects Online 2Q 2018

Projects Under Construction or in Advanced Development

Projects Online 1Q 2018 Projects Online 3Q 2018

HI

AK

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 24

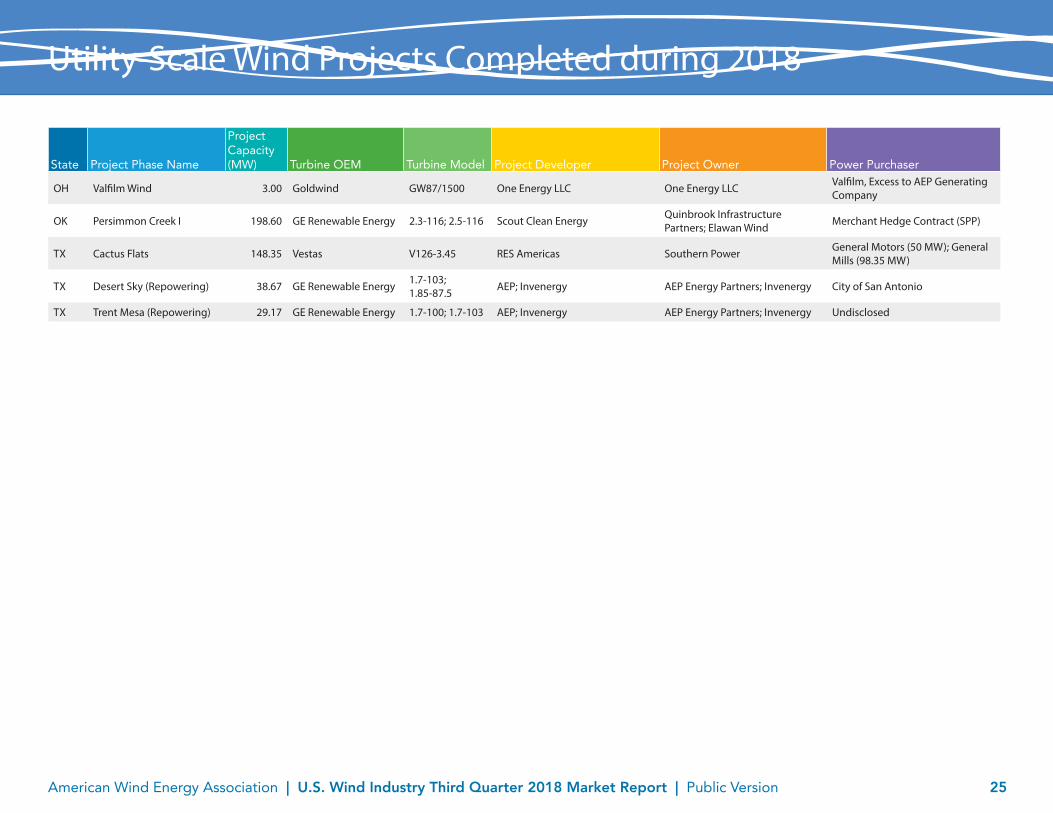

Utility-Scale Wind Projects Completed during 2018

State Project Phase Name

Project Capacity (MW) Turbine OEM Turbine Model Project Developer Project Owner Power Purchaser

First Quarter 2018

CA Tule 131.10 GE Renewable Energy 2.3-107 Avangrid Renewables Avangrid Renewables Southern California Edison

IA Prairie II 4.00 (of 168.00) Vestas V110-2.0 RPM Access Wind Development;

MidAmerican Energy MidAmerican Energy MidAmerican Energy Co

MA Otis Wind Energy Project 1.50 VENSYS VENSYS 82 SunCommon; Town of Otis Town of Otis Town of Otis, Excess to Eversource Energy

MI Cross Winds Energy Park II 43.70 GE Renewable Energy 2.3-116 Consumers Energy Consumers Energy Consumers Energy

MN White Earth Tribe 0.75 Refurbished Zond White Earth Nation White Earth Nation Minnkota Power Coop

MT Big Timber 25.00 GE Renewable Energy 1.7-100 BayWa r.e. Wind LLC BayWa r.e. Wind LLC NorthWestern Energy

TX Flat Top 200.00 Vestas V110-2.0 Innergex Renewable Energy Innergex Renewable Energy; BlackRock

Merchant Hedge Contract (ERCOT) (170 MW); Merchant Hedge Contract, Resold to QTS Realty Trust (30 MW)

Second Quarter 2018

IL Bishop Hill III 132.00 GE Renewable Energy 2.3-116; 2.5-116 Invenergy Invenergy WPPI Energy

NE Kimball Wind Farm 30.00 GE Renewable Energy 2.5-116 Aspenall Energies Aspenall Energies Municipal Energy Agency of NE

TX Rattlesnake Wind 160.00 Goldwind GW109/2500 Goldwind Americas;RES Americas Goldwind Americas Merchant Hedge Contract (ERCOT)

TX Santa Rita 300.00 GE Renewable Energy 2.5-116 Invenergy BHE Renewables Kimberly-Clark (125 MW);City of Denton, TX (175 MW)

TX UL Advanced Wind Turbine Test Facility 3.57 Goldwind GW 3MW(S) Goldwind Americas West Texas A&M University Xcel Energy

Third Quarter 2018

AK Bethel Wind Turbine 0.90 EWT Americas DW-52-900 Alaska Village Electric Coop Alaska Village Electric Coop Alaska Village Electric Coop

CA Correctional Training Facility 1.7 GE Renewable Energy 1.7-100 Foundation Windpower Foundation Windpower Correctional Training Facility,

Excess to Pacific Gas & Electric

CA Salinas Valley State Prison 1.7 GE Renewable Energy 1.7-100 Foundation Windpower Foundation Windpower Salinas Valley State Prison, Excess to Pacific Gas & Electric

NE Perennial Wind 6.90 GE Renewable Energy 2.3-116 Bluestem Energy Solutions Bluestem Energy Solutions Perennial Public Power Dist

NY Arkwright Summit 78.40 Vestas V110-2.0 EDP Renewables North America LLC

EDP Renewables North America LLC

Bloomberg (20 MW); Merchant (NYSERDA) (58.4 MW)

OH Northwest Ohio 105.00 GE Renewable Energy 2.5-116 Trishe Resources, Inc.; Starwood Energy Starwood Energy General Motors

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 25

Utility-Scale Wind Projects Completed during 2018

State Project Phase Name

Project Capacity (MW) Turbine OEM Turbine Model Project Developer Project Owner Power Purchaser

OH Valfilm Wind 3.00 Goldwind GW87/1500 One Energy LLC One Energy LLC Valfilm, Excess to AEP Generating Company

OK Persimmon Creek I 198.60 GE Renewable Energy 2.3-116; 2.5-116 Scout Clean Energy Quinbrook Infrastructure Partners; Elawan Wind Merchant Hedge Contract (SPP)

TX Cactus Flats 148.35 Vestas V126-3.45 RES Americas Southern Power General Motors (50 MW); General Mills (98.35 MW)

TX Desert Sky (Repowering) 38.67 GE Renewable Energy 1.7-103; 1.85-87.5 AEP; Invenergy AEP Energy Partners; Invenergy City of San Antonio

TX Trent Mesa (Repowering) 29.17 GE Renewable Energy 1.7-100; 1.7-103 AEP; Invenergy AEP Energy Partners; Invenergy Undisclosed

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 26

Utility-Scale Wind Power Projects Under Construction

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 27

Utility-Scale Wind Power Projects Under Construction

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 28

Utility-Scale Wind Power Projects Under Construction

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 29

Utility-Scale Wind Power Projects Under Construction

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 30

Utility-Scale Wind Power Projects Under Construction

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 31

Utility-Scale Wind Power Projects in Advanced Development

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 32

Utility-Scale Wind Power Projects in Advanced Development

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 33

Utility-Scale Wind Power Projects in Advanced Development

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 34

Utility-Scale Wind Power Projects in Advanced Development

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 35

2018 Power Purchase Agreements

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 36

2018 Power Purchase Agreements

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 37

2018 Project Acquisition Activity

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 38

2018 Project Acquisition Activity

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 39

2018 Project Acquisition Activity

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 40

2018 Project Acquisition Activity

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 41

Electric Utility Renewable Energy Requests for Proposals (RFPs)

Member Version Only

American Wind Energy Association | U.S. Wind Industry Third Quarter 2018 Market Report | Public Version 42

This Report is Powered by WindIQ

WindIQ is your comprehensive database of all online, under construction, and advanced development wind projects and wind-related manufacturing facilities in the United States, with interactive web

mapping features.

All current AWEA Business and Utility members can access WindIQ at www.awea.org/windiq or www.windiq.awea.org.

For additional AWEA industry data & analysis, please visit www.awea.org/marketreports where you can download previous versions of the Quarterly Market Reports and the latest Annual Market Report.

The AWEA U.S. Wind Industry Third Quarter 2018 Market Report can be accessed at www.awea.org/2018marketreports.

AWEA Data Services