an appeal to students r.s.j. b.a. - alor - … rsj - the problem of money.pdfthe problem of money an...

TRANSCRIPT

Fair Use Claimed

Price 4/-(20p.)

AN APPEAL TO STUDENTSR.S.J. RANDS B.A.

THE PROBLEM OF MONEYAn Appeal to Students

by

R. S. J. RANDS, B.A.

A Brief Explanation of the New Economics.

The way to combat Inflation.

Published by

THE SOCIAL CREDIT PARTY

BCM/SOCRED, LONDON, W.C.1·

"A FLAW IN THE FINANCIAL SYSTEM."

" There is one way by which even the most ignorantlayman can tef that a financial system is not workinqproperly. If a substantial part of the communityneeds and cannot afford to buy a commodity whichother men can make in abundance but are unable tosell for lack of purchasers, the financial system thatcauses such a frustratinq state of affairs is not, what-ever experts may say. operating as it should."

An extract from Sir Arthur Bryant's•' The Lion and the Unicorn." Published byCollins, By kind permission of the author.

Demond a mdicaL change inour financiaL system and end the curse of debt.

Loans ere Like drugs;the more you take the more you have to take,

First published 1970.

©Copyright R. S, J. Rands.

Dedicated to my grandson, Martyn,

and to students everywhere .

CONTENTS

Foreword

Preface .,.

Acknowledgements

Chapter 1. The Present Situation

Chapter 2. The Basis of Modern Banking

Chapter 3. The Social Credit Solution

Chapter 4. The Export Trade

Chapter 5. The Guernsey Experiment

Chapter 6. General Aims and Conclusions",

Appendix

Bibliography

viii.

v.

vi.

9

14

19

26

32

35

43

56

FOREWORD

Man is not only a political, but also a commercialanimal, and has adopted what he has come to regardas an indispensable device for turning the wheels ofhis productive and distributive machinery. That deviceis money. In this erudite little book Mr. Rands dis-cusses the problem of money, and argues convincinglythat there is.an inherent defect in the existing monetarysystem, leading to the conclusion that there is a largeamount of purchasing power which is permanentlyretained in the productive system, and never reachesthe consumer.

Mr. Rands, in fact, restates in non-technical lan-guage, and with an attractive literary style, what isknown to monetary reformers as the "Douglasanalysis" of industrial accountancy. This establishesthat, inter alia, some accountancy costs, althoughcharged into prices, are not distributable as currentincome; that is to say, the price system is not self-liquidating. The book will serve as a refresher coursefor supporters of Social Credit, but must surely appealto open-minded students and other young people-as well as to the man-in-the-street who, not withoutreason, is confused about money and prices.

In addition to dealing with domestic money mech-anism, Mr. Rands takes a cool look at the externalsituation. Ideally, foreign trade should be balancedand reciprocal ... complementary rather than com-petitive. The weakness of the present financial appa-ratus is self-evident, and Mr. Rands advocates that itshould be replaced in so far as is practicable by asystem of international contra account, which willreduce or obviate dependence on a central gold orforeign currencies reserve. Here indeed is a ground-plan for improving international relations! This bookprovides a welcome shaft of light in the mental black-out where the problem of money is concerned. By anystandard it is an important achievement.

H. MARSH, Chairman,Social Credit Party

PREFACE

Students must be acutely aware of the fact thatScientists and Inventors are far more successful inachievements than Politicians and Economists. Thesuperiority of the former is surely due to the fact thatthey are mainly concerned with absolute accuracy andtruth, whereas the latter are influenced far more byprejudice and prestige, It is therefore not surprisingthat young people are rebelling against political andfinancial authorities who seem incapable of dealingproperly with the political and economic problems thatface them.

This book is an appeal to Students to challenge thepolicies of our orthodox financial authorities, whoseinterests depend on the maintenance of the presentfaulty system, which is resulting almost everywherein appalling taxation and increasing inflation. The abilityto expand production in this age of modern technologyshould, on the contrary, surely result in lower taxation,lower prices and less financial hardship.

Scientists have enabled men to make a fantasticlanding on the moon, but Politicians and FinancialExperts have so far failed to solve the much simplerproblem of how to devise a way of creating the neces-sary tickets (money) to enable us to meet the costsof the things we produce, or could produce in evengreater quantities than we do at present. There is, ofcourse, a limit to the amount of goods we can produceor services that can be rendered, which are governedby the quantity of materials and labour available. Theyshould not be governed by the supply of money,which can be altered as required. Where, however,economists still speak of "relative scarcity", we preferto speak of "relative plenty".

This book is not an attack on bankers, financiers andeconomists as such, but on the system they are work-ing. The men running our economic system are mostlyhonest and efficient, but the system itself is, webelieve, mainly false and ineffective.

Some students may be puzzled where such sums asthe equivalent of £10,000 million can be found toenable man to reach the moon, when similar sums forpossibly more important projects on earth are notforthcoming. This book is an attempt to solve such apuzzle. The author was equally mystified when he wastaught that the First World War could last only aboutthree months, as the vast daily expense would soonabsorb all savinqs and incomes, The fact that the warlasted over..four years led him to make a careful studyof the financial system, a study which revealed thatthe bulk of the money was created by the bankingsystem. We now hope that the reading of this bookwill inspire some students to study the monetarysystem and to search for the flaws that lead to somuch unnecessary distress and strife in the presentworld,

The key to modern problems - particularly the vitalones of the avoidance of bloody revolution, dictator-ships and a further World War - is money; and onehopes that these growing dangers will encouragestudents to study the problem of money, Until moneyis the slave, and not the master, of mankind, there islittle hope of genuine peace or freedom.

R, S, j, RANDS, S~nmoffiMarch, 1970.

ACKNOWLEDGMENTS

The author wishes to express his sincere thanks toMessrs. H. Marsh, C, J, Hunt, the late J, A. White,C. G. Kitchener, V. R, Hadkins and A. M. Wade,for their encouragement and valuable assistancein checking and amending his script; to his son-in-law, Mr. C, W. Boothroyd, for his careful scrutinyof the text and helpful suggestions for its clarifi-cation; to his daughter, Mrs. Betty Boothroyd, forher accurate and efficient typing; to his wife, Ena,for her patience and sympathetic support; and finallyto Mr. M, B, Reckitt, whose guidance early in theauthor's life and whose inspiration ever since havestimulated his interest in vital social and monetaryproblems.

Chapter 1: THE PRESENT SITUATION

Most students must be extremely puzzled at thepresent state of their country and of the world, andone can hardly be surprised that so many of them arerevolting against authorities and losing faith in poli-ticians and economists. It has been aptly said that,"those desiring to make a new world today have theright material at hand, for the existing world began inchaos!" Hardly anything seems to work properly.Where there should be peace between nations thereis war; where there should be co-operation in Industrythere is constant strife; where there should be econ-omic security in this age of Power Production there ismuch unnecessary poverty in our so-called "AffluentSociety",

Governments everywhere seem incapable of pre-venting financial crises or of halting inflation and ever-rising taxation; and, as a result. disillusionment leadsto the serious unrest which too often culminates insome form of dictatorship such as Communism ormilitary rule, Before, however, we lose faith in demo-cratic government completely, we should carefullyconsider whether there is not some cause for theconstant economic crises which the majority of poli-ticians and economists simply do not understand,There is indeed a very small minority who do under-stand, but they appear to have a vested interest inmaintaining a faulty system founded on debt,

Though it may not be easy to prove there is some-thing radically wrong with the modern monetary sys-tem, it is very easy to provide clear circumstantialevidence to this effect, for every worthwhile reform ishampered by lack of money, even though it is physic-ally possible to carry out such a reform. It is physicallypossible to abolish slums, to build more roads, houses,schools, hospitals, to increase the staffing of universi-ties, schools, hospitals, to extend research into disease,to lessen poverty, particularly among the aged; but in

9

all such aims, however honest the endeavours of ourpoliticians and councillors, they are frustrated by theTreasury on the plea that we cannot afford the cost ofmost of these projects; yet what is physically possibleshould be financially possible, since money can becreated or destroyed as required,

Even though this truth about money may seemmysterious to many people and may never be reallyunderstood, one can only repeat that circumstantialevidence bears witness to its truth, for whenever warsor preparations for wars, or vast space projects haveto be financed the necessary money is somehow forth-coming. Anyone daring to suggest making peace withHitler during the last war, because of a lack of money,would have been regarded as mad or stupid; and notuntil we regard as mad or stupid Governments thatrefuse to carry out important projects (because theywill not cause the money required to be created ratherthan borrowed) shall we halt the growing chaos inthe world, It must, of course, be admitted that creationsof money for war purposes are inflationary, since alarge proportion of production is blown to bits, butsimilar sums of money created for construction inpeacetime should not be inflationary, if scientificallycontrolled, since expanding production requires expand-ing money.

Most economic experts appear to assume that theproduction of goods ensures sufficient incomes tomeet the cost of such goods, and, when this obviouslydoes not happen, they contend this is due either to themaldistribution of incomes or some temporary causesuch as a slump, even though the equal distribution ofall incomes would leave U$ all poor, and slumps occurat alarmingly short intervals. Thus the leaders of ourmain political parties, believing that production is self-liquidating, implore the workers to increase productionif they desire higher incomes and a better standard ofliving; but if, as facts demonstrate, production doesnot ensure sufficient purchasing power to liquidatecosts, then increased production still leaves us short

10

of the required incomes to meet such costs. Moreover,apart from any mathematical proof of the flow of costsbeing greater than the flow of incomes, there is plentyof evidence of the truth of this statement. In otherwords, if we have sufficient money to meet the costsof all goods and services, why are there thousands ofbankruptcies every year? Why does Industry need tospend millions of pounds on advertising to induce usto purchase the goods and services we need? Why dowe need eyer-increasing Sales to tempt us to buy atreduced prices? Why do we depend on Hire Purchaseand, most important of all, why are so many Individ-uals and Industrial Concerns as well as Local andNational Authorities getting deeper and deeper intodebt? Hire Purchase debt is now over £1,000 million:Local debt is over £14,000 million; and National debt isnow over £33,000 million,

The widely accepted view that increased productivityis the way out of most of our economic difficultiesseems at first sight to be wise and sensible; but,though it appears so clearly possible, we need toconsider carefully why there is such a limited expan-sion in the realm of production, It is so obviouslypossible to expand, since there are thousands of idleor partially idle hands and machines capable of in-creasing production; and the modernisation of ourtechnical equipment with automation, electronics, etc,in this age of atomic power, if fully utilised with bettercredit facilities, could vastly augment our physicalwealth,

Surely the main reason for the increase of produc-tion being less than it might be is the fear of over-production, a fear which largely results from theknowledge that so-called over-production (mainlyunder-consumption) leads to slumps and unemploy-ment with a fall in wages and profits, Employees,fearing redundancy, tend to indulge in restrictivepractices, and employers guard their own interestswith mergers, rings, monopolies and agreements in

11

many cases to restrict production in order to maintainprices. Other nations, also, seeking to maintain asurplus in their Balance of Payments and to protecttheir industries, are compelled to put on tariffs to keepout those of our goods which compete with their owngoods. In short, the whole world is capable of vastlyincreased production, and yet failure to distribute suchwealth, through a lack of purchasing power, compelsthe restriction of production the whole world over anda reduction of world trade,

This lack of consuming power in every countryresults in economic warfare both at home and abroad,We still behave in developed countries as though wewere living in the age of scarcity, whereas potentialabundance stares us in the face, Animals will fightfiercely for food when there is a shortage but becometamer when there is plenty for all; and yet so-calledcivilised men, having reached the stage of relativeplenty for all in the developed countries, talk andbehave as though we still needed to struggle forexistence, Phrases such as: "Business is Business",'The Survival of the Fittest", "The Rat Race", whichare so common, denote that the jungle spirit is stillunnecessarily with us and permeates our thoughts,Fierce competition is resulting in the growth of biggerand bigger units exemplified in large corporations,nationalised industries, mergers, etc, and the crushingtoo often of the small business man, even where hisexistence is of great value to the community, Thoughit is true that some nationalised concerns and largecorporations may be more efficient and economic,there is a place for the smaller concerns, These, how-ever, must find it increasingly difficult to survive in aworld of unnecessarily fierce competition, due so oftento the general shortage of purchasing power; and itobviously pays financial institutions to back the largerconcerns, It is true that heavy borrowing by Govern-ment Authorities from the banking system for Nation-alised Industries and Public Services helps to ease theshortage of purchasing power, but only at the expense

12

of high bank interest, and increased taxes and, rates,etc., which in turn result in demands for higher wages,which lead inevitably to rising prices and a fall in thevalue of money (see graph in Appendix), The £ todayis worth less than 4/- compared with its value of 20/-in 1914.

Further consequences of our 'faulty financial systemare exemplified in ever-increasing fraud and avoidanceof taxation, ..in cheap, shoddy goods and the making ofthings that will not last to ensure greater employmentor the making of profits of a somewhat doubtfulvalidity, and in easier credit for profitable projects likeBingo Halls and Dog Race Tracks than for moreimportant projects like Medical Research and PlayingFields. Most of these foregoing facts surely indicatethat, apart from a lack of money for things that reallymatter, there is somehow a flow of costs in everyindustry greater than the incomes distributed by it inthe production of its goods. Why else are so manyindividuals, so many national and local authoritiesgetting, as we have seen, deeper and deeper into debt?

As this chapter has referred to the trend towardslarger units in industry, it would hardly be completewithout reference to the Common Market, Manypeople see entry into the Common Market as a pos-sible way out of our economic difficulties, but thesupporters of the Common Market have yet to satisfyus that the advantages of entering the Market 'aregreater than the disadvantages, This form of a largerunit, backed by financial interests, would no doubt bebeneficial-to some big business concerns but at theexpense, we fear, of bankrupting many small ones andat the expense also of higher food prices, which wouldbe alarming for so many people, In any case, whateverbenefits might result from entry into the CommonMarket the fatal flaw in the price system would stillremain, since the flow of prices would still exceed theflow of incomes in the whole area.

13

Chapter 2: THE BASIS OF MODERN BANKI'NG

Students and all who desire more than circum-stantial evidence to satisfy themselves that the flow ofprices exceeds the flow of incomes would benefit froma careful examination of business accountancy andbanking procedure. Too few people realise that thebulk of money is credit (cheque money) createdsimply by ledger entries in the banks, at no cost tothemselves other than the cost of administration, whilenotes and coins make up a very small percentage ofour purchasing power; and that the bulk of the moneycomes into being as advances to Industry and theGovernment, which advances are registered as a debtwhich has to be repaid with interest to the bankingsystem.

The practice of the Goldsmiths in the 17th centuryhelps to illustrate the basis of modern banking. Intimes of danger, as in the Civil War, people found thatthe strong rooms of the Goldsmiths were the safestplaces in which to leave their gold and silver. Receipts(1.0,U.'s) were issued by the Goldsmiths against thisgold and silver, and, finding these receipts would behonoured in cash whenever presented to the Gold-smiths, people began to use the receipts as money. Incourse of time the Goldsmiths found they had goldand silver lying idle, which they were able to lend,often at high rates of interest; and finally, as more andmore people were willing to accept the receipts, itdawned on the Goldsmiths that it was perfectly safeto issue more receipts (equivalent to modern bank-notes) than were covered by the gold and silver thathad been left with them for safe keeping. Thus creditwas created out of nothing except the faith of theircustomers that cash would be delivered on the presen-tation of the receipts, and until there was some crisiseverything went smoothly; but in a crisis there wasobviously not enough cash to meet the sudden demandand in this way many Goldsmiths went bankrupt.

14

To prevent such failures and with the developmentof banking and greater central control in the 19thcentury, commercial banks were gradually forbiddento issue their own notes; but to overcome this diffi-culty in the first half of the 19th century the banksbegan to create credit for their customers (chequemoney) by simply making ledger entries for theircustomers up to several times the amount of actualcash held by the bank (notes, coins, and balance withthe Bank of England); and today it is regarded asfeasible by the banking system to lend up to about12 times the actual amount of cash held, The clearingbanks in 1968 held just over £800 million in cash intheir tills and in balances at the Bank of Englandagainst deposits of over £10,000 million (i.e. about £8in cash against £100 of liabilities), The banks, how-ever, prefer to talk about credit creation in relation totheir liquid assets (cash and short-term bills such asTreasury Bills which they also obtain with creditcreated at no cost to themselves other than that ofadministration) and the custom of the banks is tokeep about 30 per cent of liquid assets against theirtotal liabilities,

To those who find this explanation of the creationof credit difficult to understand one can only reply thatall leading banking authorities and economists nowagree that credit is (see quotations from authorities inAppendix) created by ledger entries in the banks, andevery advance or purchase of securities by a bankresults in an increase of deposits somewhere in thebanking system; and the repayment of every advanceor the sale of securities results in a cancellation ofcredit in the books of the banks. In brief, money canbe created or destroyed as required; and in tracing itsbeqinninqs as advances to Industry with debts owingto the banking system, it should be possible to seewhy ever-rising debt is one of the main reasons whyinflation is inevitable under our present financialsystem. To use a simile, money can be turned on or

15

off like water- from a tap; if you turn on too much inrelation to the production of goods and services youget, "Inflation" (an overflow); if you turn on too littleyou get "Deflation" (a tiny trickle); if you adjust the.tap- until you have obtained the required flow you have,:'!:qµation", Inflation, as we all know, means risingprices because "too much money is chasing too few9q9;9~",but prices can also be too high because thenOw of costs-exceeds the flow of incomes in businessaccountancy: and to understand why costs in the mainexceed incomes and how to get "Equation" so thatwe' have the right amount of money in relation toI1hx~ical-wealth, students are seriously recommendedto study the Social Credit proposals of Major C, H,Douglas, who, when appointed by the British Govern-ment to overhaul the finances of the FarnboroughAeroplane works during World War 1, noticed, thatthe vast concern did not payout in salaries and wages.sufficient purchasing power to go anywhere nearequating with the final costs,

,This discovery caused Major Douglas to look intothe balance sheets of over 100 industrial firms, and inevery firm he found the same fault, This flaw in theaccountancy system caused him, as an engineer andmathematician, _to set out the reason in his famousA + B theorem, which demonstrates that everybusiness, has to recover two types of costs: "A" theiticornes it pays out within its own concern, such aswages, salaries and dividends, and "B" the paymentsmade' outside the firm, such as charges for rawmaterials, plant, machinery, taxation, interest on bankloans, rates, profit, reserves and depreciation, which!l1L1'St enter into COSltS (see fuller explanation inAppendix).,t,lf" as' this theorem sets out to prove, industry has

to collect more in prices (A + B) than it distributesin, incomes (A), then the proportion of the productsold in the retail market will be limited to the sum ofthe incomes distributed; in other words it will be

16'

equivalent to (A) and not to (A + '8). The remairiil19sum will have to be collected either -by selling goods,for export or by raising further loans to improve plant:and equipment. As this process 'goes on, more and:more loans are outstanding, there is increasingpressure on traders to discharge their debts, and-thisthey often try to do by raising prices, There seems.little doubt that increasing debt and inflation, mail'il'ycaused by creations of credit for armaments, publicworks, hire purchase and exports on loan have-helpedto prop up the faulty system, since they result irf the'distribution of more purchasing power without increas-ing the supply of consumption goods. Unfortunatelythe inevitable after-effects of all this are increasedtaxes and prices, plus a fall in our exports and in thevalue of our money, followed by Balance of Payments-crises, ,

As many people otherwise sympathetic towardsSocial Credit may be antagonized throug~h the effortsto understand the A + B theorem, we wish, at thispoint, to stress that the validity of the case for SocialCredit is in no way dependent upon the validity of thetheorem. The author is convinced of its accuracy, ashe attempts to show in the Appendix, but he realisesthat its complications too often lead to sterile dis-cussions. It should, however, be obvious to mostsympathetic readers, whether they accept the IX. +~Btheorem or not, that our present economic system is'prevented from breaking down only as a result of its'being propped up by ever-rising debt, ' ,

This propping up of our faulty financial systemwould not be necessary if we had sufficient moneytomeet the costs of goods and services produced,provided prices were regulated in such a way that anincrease of money did not of itself result in a rise ofprices. The Douglas Social Credit proposals aim toshow how this problem could be solved, They pointout the obvious fact that physical wealth is appreciat-ing faster than it is depreciating, as is made so clear

17

by the fact that we are 'steadily increasing the numberof our houses, roads, schools, hospitals, etc, When abusiness or a bank increases its physical assets-buildings, machinery, etc, it credits Itselt with theincrease, and yet a nation, when it increases its assets,writes up a debt. Our National Debt should in the mainbe a National Credit, if as a nation we arranged thecreation of credit only at the cost of administration(which would be less than 1 per cent) instead ofgoing cap in hand to bankers, who create it at highrates of interest, seldom less than 5 per cent and oftenmuch higher, If the national appreciation of physicalwealth, therefore, is greater than the depreciation, thenthe Nation should in some way be able to write up acredit against its increased assets in a similar way toa business, and distribute this credit to the communityin such a way that every individual gains as a share-holder in "Great Britain Ltd,"

We, therefore, have to emphasize that the mainproblem is how to inject sufficient money into theeconomy to enable consumption to match productionWITHOUT INFLATION. Too many people assume thatan increase of the money supply must inevitably resultin inflation, though it should be obvious that expandingproduction requires expanding money, Douglas on thispoint reminded us that there are conventional laws aswell as natural laws; the latter, like the law of gravity,cannot be altered, but conventional laws - such ascricket rules - can be altered if desired, e.q. the I.b.w.rule can be changed. Economic laws are usually con-ventional laws, and therefore can be altered if required,To expand purchasing power merely by increasingwages and salaries in production will, of course, in-'crease prices, and Social Credit sets out to show howextra money must be distributed to consumers apartfrom wages and salaries, with a compensated pricemechanism by which prices are actually reduced so'that inflation is avoided,

18

Chapter 3: THE SOCIAL CREDIT SOLUTION

Though it is not easy to explain briefly the SocialCredit plan for increasing purchasing power and de-creasing prices at the same time, yet the solution iscomparatively simple. On hearing about it for the firsttime one is naturally sceptical, and it is not surprisingthat critics will contend that there can be no simplesolution to a complicated problem like our economicsystem, Yet.when a complicated machine like a motor-car breaks down there is often a very simple reason,such as dirt in the carburettor or a leak in a pipe of theclutch cylinder, Exponents of Social Credit contendthat there is a serious leak in our business account-ancy, which is resulting in an ever-mounting flood ofdebt and in masses of goods and services beyond thereach of our purses; and they attempt to show howthis leak can be prevented to the benefit of everyone,except possibly the powerful financial interests,

It would be necessary to establish a National Mone-tary Authority (an independent body of statisticalexperts) responsible through Parliament to the com-munity for the purpose of estimating the value of thewhole of our National Assets (now too often regardedas National Debt), and even a mere 1 per cent of thetrue capital value would provide adequate Reserves asa basis for a future National Dividend. Then at inter-vals, possibly every six months, the Authority willestimate with the aid of modern computers to whatextent there has been an appreciation or depreciationin the value of National Assets.

This surplus of production over consumption (orappreciation of physical wealth over depreciation)would enable the National Monetary Authority toauthorise the creation of sufficient credit to' enableconsumer purchasing power to match the costs of allgooQs and services. Such credit would be created byledger entries in a National Credit Account (associatedwith the Central Bank) in exactly the same way as

19

credit is now' created by the banking system; butunder Social Credit, consumption would control moneyinstead of money controlling consumption, The creationof credit would then reside mainly with the NationalMonetary Authority; and the power of the privatebanks to create credit would have to be more strictlylimited by the Treasury than it is today. It might evenbe considered advisable that the banks should borrow,interest free, from the National Credit Account all thecredit required by them to finance industrial produc-tion, and that this credit should be returned to theNational Credit Account by the banks on the reductionof their clients' overdrafts, after deduction of bankadministrative costs,

As an illustration of the practical working of theSocial Credit Plan let us suppose that by means ofmodern computers the National Monetary Authorityhas discovered that over a period of say six monthsNational Production of all physical wealth is roughlyequivalent in value to £4,000 million and that NationalConsumption is roughly equivalent to' £3,000 million;this would then indicate that consumers requiredabout an extra £1,000 million of purchasing powerover a period of six months to enable them to meetthe costs of all goods and services, To. do this in sucha way that prices do net rise, the extra purchasingpower must not be added to wages and salarieswithin the productive system, as this would merelyincrease costs, but must be credited to consumers insome way, with some system of control (not fixing)of prices and incomes to prevent inflation, The wholeof this £1,000 million surplus could be passed to theconsumer in the form of a 25 per cent discount onconsumer goods and services over the six monthsperiod, until purchasing power was roughly equal toprices; but, as this would benefit those with high in-comes more than those with low incomes, it would befairer to distribute the surplus with a smaller discountto allow as well fer a National Dividend and reducedtaxes.

20

It must be stressed that the previous statistics areentirely hypothetical and might well be about five timesgreater than those given, They are merely the author'sattempt to illustrate the workings of Social Credit,Also. the surplus to be distributed as a discount or inany other way will vary every six months or so accord-ing to the relation of Production and Consumption, If,for instance, Consumption were greater than Produc-tion, there would have to' be some kind of sales taxinstead of a .disccunt on sales. It might well be that alimit might have to be fixed below which the Discountwould not operate, in order to relieve the retailer of alot of bookkeeping and unnecessary worry ever smallsums, e.g. the lowest limit might be a discount onsales of 2/- in the £, i.e. of 10 New Pence in theDecimal System beginning in 1971, Present-day ten-dencies to restrict production should disappear, sincethe community as a whole should benefit from in-creased production under Social Credit, with lowerprices, lower taxes and rates and eventually someform of a National Dividend, Such benefits could beintroduced in various ways, but we hope the followingattempt to explain how it might be done will make thesubject a little easier to understand:

(1) Allot a proportion of the assumed £1,000million surplus, say £200 million, as a subsidy toretailers to sell goods at a discount with the provisothat the retailer agrees to a percentage of profit on histurnover, The discount wouldbe settled by the NationalMonetary Authority for a certain period of time, saysix months, and let us imagine the discount was fixedat 10 per cent, i.e. 2/- in the £ or One New Penny inevery Ten New Pence, The public would benefit fromthe lower prices, and the retailer would, in due course.recover from his bank the amount of the discount onall his sales (which for accountancy purposes couldeasily be recorded from his sales invoices), The bankwould, in turn, recover the amount of the discountfrom the National Monetary Authority, which would

21

simultaneously destroy an equal amount of money byentering an equivalent figure in the debit column of theNational Credit Account, and so reduce the NationalCredit Fund by that amount. This form of subsidy toreduce prices differs from a current subsidy in that thelatter is taken from taxation and the former from thebalance in the National Credit Account,

(2) Another £200 million of the £1,000 millionsurplus could be allotted to the Public Sector forNational and Local expenditure and so lead to a reduc-tion of taxation and rates, which should further reduceprices. This would also considerably lessen, and webelieve eventually end, Government borrowing fromthe banking system, and so lessen the burden of theNational Debt.

(3) Finally, the remaining portion of the theoreticalsurplus - £600 million - could be distributed everysix months in the form of a National Dividend to atleast every adult member of the community, whichcould, in such an example in Britain, amount to about£2 a week. To begin with it might be consideredadvisable to pay this Dividend only to persons withvery small incomes, but with gradually increasingproductivity following the spread of automation, elec-tronics, etc" a National Dividend for at least everyadult would ease the difficult problem of redundancy,which must inevitably get more perplexing as labourpower is supplanted by automated machinery. TheNational Dividend should eventually be paid to every-one, since the power to produce physical abundancedoes not depend merely on employers, workers andshareholders, but also on what Douglas has describedas "the Cultural Heritage", i.e. the legacy of countlessinventions and discoveries down the ages from thesimple spade to the amazing modern computers andmechanical gadgets. Every individual should benefitfrom this common heritage as a shareholder for life,as it were, in Great Britain Ltd, and it would be a kindof "surplus value" for everyone,

22

Critics fear that with all these financial benefitspeople would sit back and do nothing, but such slack-ness would result in a fall in Production, which wouldreduce the various benefits, since there would be afall in the discount rate and in the National Dividend,In other words there would be less physical wealth todistribute, since under Social Credit money is relatedto goods and services, There is also an inducement towork rather" than slack, since increased productioncould rnean.jnore credit to finance an expansion ofpublic works: houses, schools, hospitals, roads, etc,The only limit to such expansion should be whetherthere is sufficient labour and materials for the workrequired. We can only repeat, what is of such gre'atimportance in any economic system, that there wouldbe an incentive to increase productivity, an incentivewhich we so much lack today, The worker shouldgradually cease to fear automation as it would resultin a higher standard of living with reduced hours oflabour, If, as seems inevitable, it means eventuallythat fewer jobs are available, then adequate redun-dancy payments would be possible and adequatetraining facilities for new jobs could be provided aswell as fresh housing accommodation; but in any casethere would always be the National Dividend as thebasis of economic security, To anyone who feels thatthe Discount Scheme, as explained above, wouldbe too cumbersome and difficult to put into practice,and yet is persuaded that an increase of money isrequired by consumers with some mechanism to pre-vent prices rising, one can only reply that when thereis sufficient demand from the public for some suchscheme then there is little doubt that a simpler methodcould soon be devised by competent accountants andbankers, In any case, however, the Co-operativeSociety stores have no difficulty at all in crediting everysale for the purpose of paying Dividends to theirmembers, and housewives and retailers are equallyfamiliarised, and at times almost overwhelmed, withvouchers for 3d off this and 6d off that!

23

The vast extension of public works such as abolish-ing slums, building roads, schools, hospitals, civiccentres, municipal sports centres and concert halls,made possible by increased credit would no doubtreduce unemployment considerably for many years;but in course of time the fact that automation mightmean that in many industries probably only about twomen would be needed to do the work of, say, 10 mustresult in greatly reduced hours of labour. Under thepresent financial system the management cannot affordto pay wages and salaries at existing rates to an in-creased staff at greatly reduced hours of work; butunder Social Credit, with the consumer helped byreduced prices, taxes and rates, in addition to aNational Dividend, the management would be betterable to recover the costs of an increased staff on fullwages but at a shorter working day, If, despite all suchpossible improvements, unemployment still continued,we need to be reminded that the object of Productionis Consumption and not Employment, which shouldbe obvious from the fact that jobs could be found formost people by scrapping machinery, For instance,roads built with spades or even salt spoons instead ofwith pneumatic drills and mechanical diggers wouldsoon decrease unemployment! The absurdity of suchan idea should help to make clear that the real objectof Production is Consumption and not Employment,

In any case it becomes increasingly clear thatgreater leisure is coming whether we like it or not, andthe sooner we start planning and educating people forthe leisure age the better it will be for us all. Vastnumbers of people do not seem to know how to useleisure wisely (and some probably never will) as ispatently clear in our restless and aimless world oftoday, but as the standard of living and housing con-ditions improve and education is adequately financedand directed towards teaching us how to live, insteadof how just to make a living, then increasing leisureshould become a blessing instead of being so often acurse, In this respect it must be remembered that there

24

are two types of so-called work: the first is connectedwith a job which enables one to earn a living, and thesecond is the kind of work one does in spare time,namely some form of hobby or recreation, When morepeople have the money and time to spend on hobbiesand recreation, and cultural and games facilities areproperly financed, then arts and crafts and recreationof all kinds should flourish. Modern young people,despite improvements in many ways, are often boredand frustrated because of limited opportunities todevelop their spiritual, mental and physical powers.

25

Chapter 4: THE EXPORT TRADE

Many people will agree that the Home Market couldbe stimulated by Social Credit in the ways suggestedabove, but yet they remain fearful about the result onour Export Trade. These fears will be seen to be un-justified once it is realised that far too much stress islaid on the necessity to export, In terms of real wealthevery export is a loss of goods to this country andevery import is a gain, It is true that under the ortho-dox system we gain more than we lose if we exportmore goods than we import, but to call this a "favour-able balance of trade" merely shows that orthodoxytakes the shadow for the substance. A gaining ofmoney without an exchange of goods to match themoney has an inflationary effect, as explained morefully later, Social Crediters, of course, realise the vitalnecessity of exporting sufficient to pay for the importswe need, but so much emphasis has been laid on ournecessity "to export or die" that the average studentmight well fail to spot the fallacies underlying so manyof the accepted views on our need to increase ourexports.

In the first place, for example, every state (creditorand debtor) aims to obtain a surplus in the balance oftrade. A creditor nation, after paying for imports withexports (visible and invisible) has to gain a surplusin order to be able to lend; and in the same way adebtor nation has to gain a surplus in order to be ableto pay its debts, Yet if some nations have a surplus,others must have a deficit and therefore it is clearlyimpossible for all nations to gain the surplus required.It is interesting at this point to note that we are toldby our experts that we need a surplus of about £500million a year in our Balance of Payments at the pres-ent time to enable us to meet our commitmentsabroad and to pay our debts abroad, which have risenby something like £3,000 million in the last four years,Many people are increasingly puzzled and disturbedby continual reminders, in the Press and Broadcasting,

26

of nations borrowing the equivalent of many millionsof pounds from mysterious bankers somewhere torepay similar sums owing plus interest, or to helpprevent a Balance of Payments Crisis. Almost thewhole world seems to be in pawn to Financial Inter-ests, and we vainly try to borrow ourselves out ofdebt, which appears to be the height of lunacy! Nationswith deficits (and there are many in this unhappyposition) are compelled to reduce their imports andlower their "standard of living with credit squeezes,factors which later react on other nations when theyfind they cannot sell so much to impoverishedcustomers.

In the second place, traders try to sell abroad goodsthey are unable to sell at home through lack of purchas-ing power, but in so far as there was insufficient pur-chasing power to buy these goods in the home marketthere will still be insufficient to buy the imports thatenter the country in exchange for the original exports,Every export market is, after all, the importing country'shome market with the same deficiency of purchasingpower, so that it is not surprising that exporters findthat obstacles are put in their way by protective de-vices such as tariffs and quotas,

In the third place, it pays financial interests toencourage exports, for this enables them to increasetheir loans abroad, as often high interest can beobtained. It is, indeed, claimed, and often rightly so,that such loans and investments increase our invisibleexports (in the shape of interest and dividends) andhelp our Balance of Payments; but we are seldomtold that too often only a small proportion of interestdue ever reaches us, since many debtors either fail topay what is due or are lent further money to enablethem to pay their debts, It is as well to remind our-selves that a large part of Germany's reparation pay-ments and debts after the First World War could bepaid only when they were lent the money by some oftheir victors! In our mad world it sometimes pays to

27

lose a war or be in debt! It is significant that the mainvanquished nations in World War II, Germany andJapan, are now two of the most successful tradingnations in the world!

There seems little doubt that of the thousands ofmillions of pounds invested abroad over the last 150years, a large proportion has been frozen credit, andtherefore never returned to us, and such money, in-stead of being wasted, could have enormously in-creased our assets at home in the form of morehouses, schools, hospitals, roads, etc, We haverecognised that investment abroad can earn us largeinvisible exports in the shape of interest or-dividends.but it is not sufficiently realised that on many occa-sions even larger visible exports could have beenearned if instead of investing the money abroad it hadbeen invested in modernising some industry at home,Exporting abroad without corresponding imports alsohelps to reduce unemployment, as incomes are paidout for jobs done in the exporting country yet the realwealth (the goods) is exported, Again, although thisalso helps to ease the lack of purchasing power in thehome market, it may lead to inflation because effectivedemand for goods has been increased without thesupply of goods awaiting consumption in the homemarket being similarly increased, Finally, an exportsurplus enables a creditor nation to get control of theconcerns and assets of another country if it so desires.

We have tried to show why shortage of money inthe home market induces traders to search for foreignmarkets, but a shortage of money for internationaltrade ("International Liquidity", in financial jargon)appears to be inevitable under the Bretton Woodsagreement of 1945, This was intended to stabilise theworld monetary system after the Second World War,for not only were parities arranged between curren-cies, but currencies were geared to', gold, yet the pro-duction of gold does not keep pace with the produc-tion of goods, The Bretton Woods scheme, therefore,

28

results in international trade being too often a strugglefor money rather than goods, and debtor nations inparticular are badly hit, since they are compelled torestrict imports, to deflate, and lower their standardof living to gain the necessary surplus to pay theirdebts, This shortage of International Liquidity, whichso often results in Balance of Payments crises in manynations, has caused Worl'd Bankers to introduce"Paper Gold" to increase the amount of credit inthe world; 'but until world trade is based on theexchange of goods for goods instead of, as so often,goods for money, it is very doubtful whether just anincrease of international credit will prevent Balanceof Payments crises, because the flow of priceseverywhere wi'" still be greater than the flow ofincomes.

Social Crediters would fix exchange rate's periodic-ally by agreement, prohibit the buying and selling ofcurrencies except for legitimate commerce and carryon overseas trade by a system of Contra Accounts,Money would then cease to be regarded as a com-modity and would become what it was intended tobe - a means of exchange, In this way we should bethinking in terms of essentials, such as food, fuel,clothing, shelter, etc" rather than in terms of gold.Gold puts obstacles in the way of expansion of creditand expansion of goods and services. In any caseit is surely a pernicious system that allows speculatorsand gamblers in currencies to upset the stability ofnations, Surely we have enough common-sense todevise a better system.

To illustrate the idea of Contra Accounts let ussuppose a British Exporter is selling goods to aFrench Importer, and that Exchange Controls havebeen established in each country. The British Exporterwould draw a Bill of Exchange for the amount due onthe French Importer and discount the Bill of Exchangewith his bank, which should be under obligation to re-discount it with the British Exchange Control. The

29

'1.I

1

British Exporter would, in this way, be paid in his owncurrency.

The French Importer, too, would pay for the goodsalso in his own currency through his own bank intothe French Exchange Control, and the British ExchangeControl would be given a blocked credit for theamount due. The principle is one to which we are allaccustomed in the retail trade, If you have a creditwith a shop, you cannot take it out in cash, but youclear it when you take goods, Only when a BritishImporter bought goods for a similar amount from aFrench Exporter would the original credit be cleared,The British Importer would pay the sums due in sterl-ing through his own bank into the British ExchangeControl, and the respective Exchange Controls couldcancel claims against one another, If, however, theBritish Exchange Control did not wish to make use ofthe blocked credit in France, then, after a fixed periodof time, say six or seven years, the French ExchangeControl would be allowed to cancel the credit andBritain would merely have made a gift of goods to theFrench, Thus, under a system of Contra Accounts,goods would be exchanged for goods instead of forsome form of money or acknowledgement of debt,The above example refers only to bilateral trade butnations would have representatives at an InternationalExchange Control to provide for multilateral trade andthe exchange of credits,

Contra Accounts should thus help to reduce econ-omic warfare; but in any case, if any nation managesits financial system so that inflation is avoided, thenits money will be regarded as valuable to overseasbuyers, since prices will be reasonable. We have triedto show that Social Credit demonstrates not only howinflation can be avoided but also how prices can bereduced. For these reasons the currency of a SocialCredit country should be acceptable and even wel-come to other nations. Thus in Britain the £ underSocial Credit would be entirely safe,

30

Our present financial authorities rightly stress theimportance of protecting the £, but under orthodoxfinance the protection of the £ is at the expense ofthe prosperity of the people, since, as we! have seen,inflation seems to be inevitable, This compels theGovernment to limit the expansion which is such avital necessity as population increases, for hiqherstandards of living are rightly demanded in this age ofcolossal power production, It is true that our presentLabour Government contends that increased produc-tivity and increased exports are main ways of over-coming these economic difficulties, but, as we haveseen, under orthodox finance there are various reasonswhy these important aims are never really achieved,The Government also seeks to limit inflation by itsPrices and Incomes Policy, which so far has not beenvery effective, since the steady fall in the value of the£ leads to strikes, from which the strikers usuallygain some or all of their demands for higher wages,which in turn lead to higher prices. The Treasury alsorequests the banks to reduce their loans and over-drafts to the private sector to reduce the spendingpower of the consumer; and, though the banks arereluctant to do this, yet advances to the public sectorare not checked in the same way, with the result thatbank deposits still increase with inflationary effects.

31

Chapter 5: THE GUERNSEY, EXPERIMENT

To those puzzled by the idea of the Communitycreating credit we recommend a careful study of theGuernsey Experiment, which began about 1815, Criticsof Money Reform often delight in scaring people byreferring to the massive printing of notes in Germanyafter the First World War, which resulted in appallinginflation, but such critics avoid telling us, or do, notrealise, that these notes were purposely over-issuedto create economic chaos as a protest against thePeace Treaty, and that they were not issued in rela-tion to goods and services, (This inflationary printingof notes, however, enabled them to abolish theirNational Debt, and this advantage, coupled later withthat of large loans from their victors after both WorldWars, enabled them to modernise their industrialequipment and set them well on the way to becomingtoday one of the leading industrial nations in theworld.)

In 1815, after the Napoleonic Wars, Guernsey wasso economically crippled that it was unable to raiseenough money even to pay interest due on debts orto raise sufficient from taxation to meet urgent needs,such as measures to protect the island from the sea,or to build a market place, a school, or roads, etc, Toovercome these difficulties someone suggested thatthe State should issue its own money in some formof scrip, and in due course the State issued £4,000 in£1 notes to build a market place, Every year £400 wasrecalled in rents and redeemed (in other words, can-celled out of existence) and so after 10 years thewhole £4,000 of notes was redeemed and there wasno State debt,

State notes were later issued to pay for the buildingof a school, a lighthouse, a road, etc, and were re-deemed from Customs Duties on wines and spirits, Inthis way money was created for useful purposes andthen cancelled, and in this way the' creation of

32

I

IIII

(money was related to the creation of physical wealth,It is interesting to note that after the First World Warthe State issue of notes was increased to £200,000and circulated alongside Bank of England notes. Asa result the world crisis of 1931 never really troubledGuernsey; there was practically no unemployment;and even now Income Tax is only about 4/- in the E.

This creation and cancellation of money in relationto important public projects should be of great interestto all, public servants, both National and Local, andshould be of particular interest to all people andassociations concerned with the vital problem of hous-ing, especially the problem of abolishing the slumsand housing the homeless, What a vast difference itwould make to the matter of housing if magnificentorganisations like "Shelter" were encouraged withallocations of sums of money considerably greaterthan anything they can raise from voluntary aid! Whata vast difference it would make to the Minister ofHousing and to Local Authorities if money could becreated (debt free) for housing in some similar wayto the Guernsey Experiment! Whereas the marketplace in Guernsey was built for, and only cost, £4,000,a Council House today can be built for £4,000 and yet,owing to the authorities having to borrow the moneyat high rates of interest for a period of 60 years, thefinal cost is now well over £16,000 as far as rate-payers or tenants are concerned, In other words rentsare almost double what they should be, for, if theState created the necessary £4,000 to pay the builders,etc, and recovered this amount in payments of rentover a period of about 20 years, the house wouldobviously have cost only about £4,000 instead of over£16,000 as it does at present, and, as a result, rentsin all Council Houses could be very greatly reduced,It is perhaps unnecessary to point out that the £4,000required to build the Council House could be createdby ledger entries in the Central Bank or a NationalCredit Office at the cost of clerical work instead of athigh rates of interest as at present; the credit would

33

be recalled through rents over a period of about 20years and cancelled out in the books of the CentralBank or National Credit Office in the same kind of wayas the notes were redeemed in Guernsey. It makeslittle difference whether notes or credit are used, but,as today most transactions are paid for by cheques, itis necessary to understand that money can just aseasily be made by bank ledger entries as by printingnotes, and just as easily cancelled out of existence inthe ledger as in the redeeming or destroying of thenotes,

Chapter 6: GENERAL AIMS AND CONCLUSIONS

34

We have tried to show why we can meet only aproportion of the costs of our goods and servicesproduced at home, and only a proportion of the goodsimported; but Social Credit is neither just a method ofobtaining more and more gadgets at lower prices norjust a method of ending unnecessary poverty. Thegeneral aim is "a state of welfare rather than a welfarestate"; the. former encourages individual freedom,while the latter tends to make us all subservient to anall-powerful State, A state of welfare naturally re-quires that we all have economic security, and to thatextent material prosperity is essential; but once moneyis our servant and not our master we can end somuch that is false in our present way of life, Insteadof, as at present, being educated mainly to earn aliving, we could be educated mainly to learn how tolive, and many of the grievances and fears of modernstudents should gradually disappear.

The greatest fear is probably the danger of anothergreat war, but under a sane money system we shouldnot have to indulge in economic warfare with othernations, as we could exchange goods for goods in-stead of so often exchanging goods for money or forthe mere acknowledgement of debts. In this way wecould gradually stifle one of the main causes of war,and the making of armaments to stimulate employ-ment would be unnecessary, Instead of insultingProvidence by discouraging good farming in the inter-est of cheap food (which so often leads to the neglectof "Mother Earth" and appalling soil erosion) we couldcreate credit to encourage agriculture both at homeand in the developing countries where hunger is sorife, In this way all mankind would benefit from theproper use of the soil, since the land is the mainsource of real wealth and should not be sacrificed inthe interest of finance. Government grants from richercountries and generous help from fine organisationslike Oxfam and Christian Aid for the poor countries

35

are helping them to help themselves in increasing theirfood production and making them less dependent onsupplies from abroad; but unfortunately many of thesebenefits are nullified because high interest rates havetoo often to be paid on loans from abroad, Moreover,under a sane money system, where money would berelated to physical resources, far greater aid could begiven through Government grants of credit than arenow possible, however generous the present aid fromGovernments or voluntary organisations may be, andas a result world production of food and raw materials- so vital with ever-increasing population - wouldbe vastly increased and the danger of revolutionsgreatly reduced, It has been aptly said that to meetthe "Population Explosion" the world needs "EarthControl" as well as "Birth Control"!

History shows that one of the main causes of thefall of the Roman Empire was the misguided treatmentof the small farmer in Italy, who could not competewith the cheap corn imported from North Africa, wherebad farming encouraged by financial interests causedthe soil erosion that resulted in the Sahara Desert; andit is interesting to note that the small farmer in Italywas also harmed by competition from the large farms("Iatifundia") which depended mainly on slave labour,whereas today our large farms increasingly rely onmechanical devices (modern slaves). Apart, too, fromreducing the flight of labour from the land, we could,by encouraging agriculture at home, maintain manyuseful small farms as well as improve our Balance ofPayments by something like £200 million a year, andat the same time improve the health of the nationthrough the greater consumption of fresh home-grownfood,

Conservation Year, 1970, reminds us that the healthof mankind also largely depends on man's rapid andeffective dealing with the problem of the pollutionof rivers, sea, air and land, The dangers of polluticnare probably as great as the dangers of war, and one

36

fears that the necessary .surns of money needed todeal with this tremendously urgent problem wouldnot be forthcoming except under Social Credit prin-ciples of finance,

It 'must be admitted that these Social Credit ideasare regarded as unsound by financial experts, butanyone hearing of these ideas forthe first time shouldnot let the views of the experts deter him from fur-ther study of.' SOCial Credit, since the experts havebeen proved wrong on so many occasions in this 20thcentury, They were proved wrong in the way theyadvised the Government as to the best way to payfor the First World War, since by using mainly bank-created credit we were left with a vastly increasedNational Debt; they were wrong in the policy of De-flation (as recommended by the Cunliffe Committeein 1918), which led to a serious slump; they werewrong in going back to the Gold Standard in 1925,which was largely responsible for the General Strikein 1926 and further unemployment; wrong in advocat-ing a reduction of wages and salaries and so causingunder-consumption at a time of over-production dur-ing the world crisis of 1929-31; wrong again in allow-ing loans to Hitler prior to the Second World Warand later financing this war largely by borrowing fromthe banks as in the First World War, and so onceagain vastly increasing the National' Debt; and nowmore recently even some experts themselves arebeginning to doubt the wisdom of the Bretton WoodsSettlement of 1945, which geared world trade to goldwhen the rate of gold production (made worse by thehoarding of gold) is far below the rate of the produc-tion of goods and services, thus causing a shortage ofmoney for world trade (International Liquidity), andcompelling nations to restrict vital expansion andlimit imports to prevent Balance of Payments crises.Leading World Bankers, who have, in the past, almostvenerated the Gold Standard, have now introduced"Paper Gold" - a form of international credit - as a

3:7'

way of trying to prevent the Balance. of Paymentscrises which appear to have been intensified' as aresult of the Bretton Woods Agreement of 1945.

The International Monetary Fund has authorised asfrom January t st. 1970, the allocation of $17,000million worth of "Paper Gold" (officially described as"S,D,R," - Special Drawing Rights) to its 114 mem-bers in the Western World. to be spread over threeyears. On January 1st Britain's Gold Reserves wereaccordingly increased, through our share of the as-signment, by £171 million, which artificial creation ofcredit enabled our Reserves to rise by £21 million inFebruary, 1970. "These imaginary assets can only besustained by confidence, but should help to illustratethe fact that money can be created by mere ledgerentries,

Some experts suggest raising the price of gold andby this method increasing the liquid reserves of thericher nations to finance the increasing volume ofworld trade. Doubling the price of gold would meanthat an ounce of gold, now officially equal to $35,would be equal to $70, This increase in liquid reserves,it is argued, would help to prevent constant currencycrises and also enable the richer nations to give moregenuine aid to the less fortunate nations of the world,Others advocate that the International Monetary Fundshould be developed into a Central Bank for the pres-ent central banks of the world and that this CentralBank should create credit for the lesser central banksby book entries in much the same way as the bankingsystem in general creates credit for its customers. .'

Probably these [ideas of "Paper Gold" and aCentral Bank for central banks would strengthen theBretton Woods scheme, but they would hardly lessenthe bad effects of inflation, even though they mightslightly improve the economic situation in the world.Nor do they do anythin~ to ensure that nations willhave sufficient purchasing power to enable the costs

38'

of goods produced in the home market to be met, foronly when the people of any State are able to buymore of the goods produced in their own country willthey then be in a better position to buy more goodsfrom abroad, provided there is, as we have tried, toshow, a system of Contra Accounts,

At this point, however, we must ernphasize thatSocial Crediters rate very highly the need for nationalself-sufficiency, whereas, under orthodox finance, ex-ternal borrowing has for Britain become an acceptedway of life, This is encouraged by the InternationalMonetary Fund, under Which, as loans are repaid,further drawing rights are granted. Thus externally,as well as internally, we live in a situation of incessantborrowing, We can neither rid ourselves of debt, norcan we control our own financial affairs, as is madeabundantly clear in the Chancellor's recent Letter ofIntent to the International Monetary Fund, in which,towards the close, he says: "The Government willconsult with the Fund from time to time, in accord-ance with the regular policies of the Fund on suchconsultations, about the course of the United Kingdomeconomy and any measures affecting the balance ofpayments that may be appropriate," This last, crushingsubmission to so-called financial experts deprives usof almost all financial freedom,

This brief account of the advice of orthodox fin-ancial experts since about 1914 and of the manyfailures resulting from such advice should give usgood reason for questioning the opinions of suchexperts. Yet such is the influence of the Money Powerthat exponents of the New Economics are seldom ableto get their views published in the National Press oron Television or Radio, There is a strange "Conspiracyof Silence" where Money Reform is concerned, or ifthe silence is strangely broken then the suggestedreforms are merely ridiculed and are never discussedfairly and dispassionately. Surely this refusal to allowpublication and, discusslon of new ideas is' a sign of

39.

weakness and fear. There is little doubt that most of,us are inclined to be conservative at heart and sus-picious of most new ideas, even though it is generaJlyrecognised that the unorthodox of today is the ortho-dox of tomorrow, For example, it took over 100 yearsfor the experts to accept the discovery that the worldwas round and not flat, and most modern discoveriesor inventions such as anaesthetics or aeroplanes. werefor a long while scoffed at by so-called experts.jlt isworth noting at this point that the late A. V. Roe,famous as one of the early pioneers in aeronautics,was also one of the early pioneers in Money Reform,and when asked, towards the latter part of his life,whether he was not worried at being described as acrank over currency reform, he replied that ever sincea leading National Newspaper, in the first decade ofthe 20th century, had ridiculed his belief in "heavierthan air" machines, he was naturally not disturbed atbeing described as a crank over currency reform!

Many will argue that, though experts are oftenwrong, there is little hope of putting things right untilthere is a "change of heart". There is certainly nodoubt that good economics will be good ethics, butgood ethics will not necessarily result in good econ-omics unless a moral outlook is combined with soundthought. Even a gathering of saints would not beexpected to know how to mend a leak in some partof the mechanism of a car, and much less could theybe expected to know how to mend a leak in ourindustrial accountancy system, However, it must beagreed that the more saintly we are the more likelywe are to want to know how best to change ourinsane financial system, and to this extent onenaturally looks to high-principled people to supportimpartial investigation of Social Credit ideas, At thesame time even the most honest folk are subcon-sciously inclined to "ride in blinkers" and see thingsas they want to see them, and for this reason evenmany ,of our best politicians are scared to challengethe orthodox financial system, as then In some mys-

4cf

terious way' promotion may be denied them, Ver,yfew politicians have had the courage to oppose theauthority of the Treasury, and for this reason they are,anyhow subconsciously, disposed to accept the viewsof orthodox experts.

Having tried to show that even many honest peopletend to be conservative and prejudiced or else to"ride in blinkers" (and even Labour Statesmen seemto have to bow to the dictates of International Fin-ance-in foolish attempts to borrow us out of debt)we are, therefore, appealing to the younger genera-tion to examine Social Credit before they becomeprejudiced or so busy in earning a living that they havenot the spare time to try to find out what is reallywrong with the economic system. There is no reasonto wait for a World Government before radical reformin the financial system can be achieved, and in anycase World Government at present would probablymean even greater domination by the Money Power,a likely state of affairs not sufficiently realised by largenumbers of honest people striving for peace in theworld, ,I n other words, anyone cou ntry could set anexample in Money Heform. which other countries wouldsoon follow once they saw the benefits that resultedfrom such a reform. Britain, preferably in co-operationwith the main members of the Commonwealth (andthere are already many supporters of Social Creditin Canada, Australia and New Zealand) could set suchan example, Though we may no longer be a first-classpower in the military sense and are too ready toacquiesce in the view that we are decadent and sloth-ful, we are still greatly respected for our heritage andgenius in many ways, such as our sense of justice,our world pioneering, our skill in the realm of inven-tions and the development of the idea of representativegovernment, and we could challenge and lead theworld in a better way than ever before if we coulddemonstrate the way of replacing National Debt byNational Credit, Associations, demonstrations,marches and dedicated work by modern youth in

41

such a cause could help to make us a first-rate powerin the best sense of that phrase and start a series ofevents that would be of benefit to all mankind. Sucha cause should appeal to youth and give them a senseof purpose in place of the present mood of despairand disillusionment which leads to so much dissipatedenergy, They would be the spearhead in an effort tooverthrow the most powerful vested interest in theworld - the Money Lords - and so help to bring toan end two of the greatest fears of mankind: the fearof Want and the fear of War.

The hope of ending such fears was eloquently ex-pressed by Sir Winston Churchill at the opening ofParliament on November 3, 1953: "There is no doubtthat if the human race are to have their dearest wishand be free from the dread of mass destruction theycould have, as an alternative, what many of themmight prefer, namely, the swiftest expansion ofmaterial well-being that has ever been within theirreach or even within their dreams. By material well-being I mean not only abundance but a degree ofleisure for the ma sses such as has never before beenpossible in our mortal struggle for life, These majesticpossibilities ought to gleam and be made to gleambefore the eyes of the toilers in every land and oughtto inspire the actions of all who bear responsibility fortheir guidance,"

42

APPENDIX .'A'THE APPENDIX

NATIONAL DEBT 1694-1969Graph illustrating rise in National Debt from about£1 million in 1694 to over £33,000 million in 1969,(5 THOUSANDMILLION

.'" , ..., >,

,

Over [33,000 minion

)

Present Day ~I,

,

o ver ",~""""l,, elter World War II. I

II

I I

I I, I I

I III

~ III

I I IOver [8,000 million ~ ~ I

"I

After World War I.

", I I I

I I II I 1

J: I IOver £800 million etter I I

About £1 million Nepclecnlc w~ I I

1694 : I I

10

1680 1700 1800 1900 1920 1940 1960 1980

It is argued that the interest on this debt is trans-ferred by the State to members of the community, andis therefore not as serious a problem as it appears. Itis, however, necessary to point out that there is littledoubt that the major portion of the interest goes tofinancial institutions, and that consequently the massof people are taxed in the interest of such financialinstitutions. 43

APPENDIX 18'

PURCHASING POWER OF THE £

The following figures show the approximate fall inthe internal purcha_sing power of the pound sterling,taking the value as twenty shillings in 1914.

The figures are based on movements in the cost-of-living index up to 1938 and on the consumer priceindex from 1938 to 1963, with a provisional figure for1964 based on the index of retail prices,

s. d. s. d. s, d. s. d.1914 20 0 1927 11 11 1940 10 3 1953 : 5 41915 16 4 1928 12 0 1941 9 3 1954 5 31916 13 8 1929 12 2 1942 8 6 1955 ' 5 01917 11 5 1'930 12 8 1943 8 2 1956 I 4:101918 9 11 1931 13 7 1944 8 0 1957 4 81919 9 4 1932 13 11 1945 7 10 1958 4 71920 8 0 1933 14 4 1946 7 7 1959 4 61921 8 10 1934 14 2 1947 7 1 1960 4 ' 61922 10 11 1935 14 0 1948 6 7 1961 4 51923 11 6 1936 13 7 1949 6 5 1962 4 31924' 11 5 1937 13 0 1950 6 3 1963 4 01925 11 5 1938 12 10 1951 5 9 1964 3 111926 11 7 1939 12 5 19q2 5 5(From "Hansard" Vol. 705, No, 44, January 22, 1965, and Vol.730. No, 47, July 5, 1966.)

The decline in the value of the £ continues, and ,in1969 is now worth hardly more than 3/-, comparedwith 20/- it! 1914,

44

\

APPENDIX IC'

, BANKS CREATE MONEY

The Encyclopaedia Britannica, under "Banking andCredit":

"Banks create credit, It is a mistake to suppose thatBank Credit i~ created to any important extent by thepayment of money into the Banks,"

The late Reginald McKenna, Chairman of the Mid-land Bank and an ex-Chancellor of the Exchequer,addressing shareholders of the bank (January 25,1924) said:

"The amount of money in existence varies only withthe action of the banks on increasing or diminishingdeposits. , . , Every bank loan and every purchaseof securities creates a deposit, and every repaymentof a bank loan and every bank sale destroys one,"

Macmillan Report, 1929-31 inquiry into bankingfinance and credit, P. 34, paragraph 74, states:

"It is not unusual to think of the deposits of a bankas being created by the public, through the deposit ofcash representing savings or amounts which are notfor the time being required to meet expenditure, Butthe bulk of the deposits arise out of the action of thebanks themselves, for by granting loans, allowingmoney to be drawn on an overdraft or purchasingsecurities, a bank creates a credit in its books whichis the equivalent of a deposit,"

Memoranda of Evidence (Vol. 1) submitted by theBank of England to Radcliffe Committee on Govern-ment Borrowing (1959):

The Controf of Bank Credit in the U,K, (page 9):

45

"Entries in the books of a bank have come to be (generally acceptable in place of cash (i.e, credit).

"Banks cannot create credit in this way without'limit. It has come to be accepted since 1946 that theyhold an amount close to 8 per cent of their depositsin cash - notes and coin - or balances on accountat the Bank of England. .

"As a general rule the banks will be very reluctantto see the ratio to their deposits of their cash plusother liquid assets - their "liquidity ratio" _: fallbelow 30 per cent."

APPENDIX 'D'

To those who refuse to face up to the suffering anddespair that largely result from our futile money systemon the ground that we live in an "Affluent Society",we would remind them of the following facts:(1) Millions of aged people are living either on or very

near the poverty line, and a large proportion ofthese require National Assistance,

(2) Millions of people are still living in slum condi-tions; thousands of families are homeless; millionsare living in drab and dilapidated homes (notregarded as slums),

(3) Many thousands go bankrupt every year.(4) Many thousands commit suicide every year,(5) Many thousands are in prison for debt,(6) Over half a million are unemployed,(7) Millions are struggling to make ends meet in this

age of galloping inflation, especially those withsmall fixed incomes,

(8) Foolish and disastrous economies are made wherehealth, education and vital public services areconcerned.

(9) A large number of charitable organisations appealfor money (which is not easy to acquire but easyto create) to gain the equivalent of food, clothing,warmth and shelter (which are physicallypossible) .

46 47

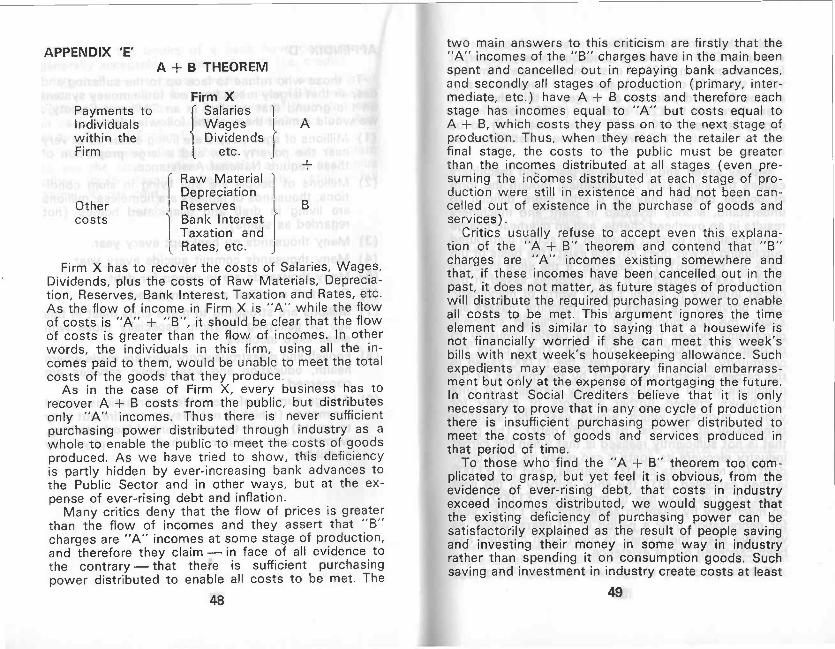

APPENDIX 'E'A + B THEOREM

Firm XPayments to f Salaries IIndividuals Wages Awithin the Dividends JFirm l etc,

+r Raw Material IDepreciation I

Other I Reserves t Bcosts 1 Bank Interest

Taxation andL Rates, etc, J

Firm X has to recover the costs of Salaries, Wages,Dividends, plus the costs of Raw Materials, Deprecia-tion, Reserves, Bank Interest, Taxation and Rates, etc,As the flow of income in Firm X is "A" while the flowof costs is "A" + "B", it should be clear that the flowof costs is greater than the flow of incomes, In otherwords, the individuals in this firm, using all the in-comes paid to them, would be unable to meet the totalcosts of the goods that they produce,

As in the case of Firm X, every business has torecover A + B costs from the public, but distributesonly "A" incomes. Thus there is never sufficientpurchasing power distributed through industry as awhole to enable the public to meet the costs of goodsproduced, As we have tried to show, this deficiencyis partly hidden by ever-increasing bank advances tothe Public Sector and in other ways, but at the ex-pense of ever-rising debt and inflation,

Many critics deny that the flow of prices is greaterthan the flow of incomes and they assert that "B"charges are "A" incomes at some stage of production,and therefore they claim - in face of all evidence tothe contrary - that there is sufficient purchasingpower distributed to enable all costs to be met, The

48

two main answers to this criticism are firstly that the"A" incomes of the "B" charges have in the main beenspent and cancelled out in repaying bank advances,and secondly all stages of production (primary, inter-mediate, etc.) have A + B costs and therefore eachstage has incomes equal to "A" but costs equal toA + B, which costs they pass on to the next stage ofproduction. Thus, when they reach the retailer at thefinal stage, the costs to the public must be greaterthan the incomes distributed at all stages (even pre-suming the incomes distributed at each stage of pro-duction were still in existence and had not been can-celled out of existence in the purchase of goods andservices) ,

Critics usually refuse to accept even this explana-tion of the "A + B" theorem and contend that "B"charges are "A" incomes existing somewhere andthat, if these incomes have been cancelled out in thepast, it does not matter, as future stages of productionwill distribute the required purchasing power to enableall costs to be met, This argument ignores the timeelement and is similar to saying that a housewife isnot financially worried if she can meet this week'sbills with next week's housekeeping allowance, Suchexpedients may ease temporary financial embarrass-ment but only at the expense of mortgaging the future.In contrast Social Crediters believe that it is onlynecessary to prove that in anyone cycle of productionthere is insufficient purchasing power distributed tomeet the costs of goods and services produced inthat period of time.