an exploratory analysis of the effect of the “buy it now” option on sellers' revenues in...

TRANSCRIPT

An exploratory analysis of the effectof the ‘‘buy it now’’ option on sellers’revenues in silent auctionsKaren Page*Department of Management and Marketing, University of Wyoming, USA

� This paper tests three competing hypotheses regarding the effect of a ‘‘buy it now’’ option

in silent auctions: that the option has a positive, negative, or neutral effect on the seller’s

revenues. These hypotheses were tested on 4 years of data from a university art museum’s

silent auctions. The results indicate that the ‘‘buy it now’’ option has a significant negative

effect on the seller’s revenues. Possible explanation, implications, and limitations are

discussed.

Copyright # 2009 John Wiley & Sons, Ltd.

Introduction

Auctions, both live and silent, are a popularfundraising tool used by nonprofit organiz-ations (Engers and McManus, 2007; Carpenteret al., 2008). Auctions have been the domain ofeconomists and social scientists as they havestudied the structure, history, and processes ofauctions (e.g., Klemperer, 2004), seller, bid-der, and public welfare (e.g., Mathews, 2006;Ubbels and Verhoef, 2008), and bidder andseller behavior (e.g., Engelbrecht-Wiggans andKatok, 2006; Gattiker et al., 2007). This paperextends the research on the structural andbehavioral aspects of auctions to examine theeffect on seller’s welfare of the ‘‘buy it now’’option popular in silent auctions.

Auctions

An auction is a competitive mechanism forallocating scarce goods. In the for-profitcontext, it is the purest of markets: a sellerwishes to obtain as much money as possible,and a buyer wants to pay as little as necessary.An auction offers the advantage of simplicity indetermining market-based prices. It is efficientin the sense that an auction usually ensuresthat resources accrue to those who value themmost highly and ensures also that sellersreceive the collective assessment of the value.What is unique about the auction is that oncethe seller’s reserve is met, the price is set not bythe seller, but by the bidders.Two general frameworks have been used in

auction theory to study bidding behavior: the‘‘common value’’ model and the ‘‘independentprivate value’’ model. In a common valueauction, the value of the prospect is the samefor all bidders, but none of the bidders know

International Journal of Nonprofit and Voluntary Sector MarketingInt. J. Nonprofit Volunt. Sect. Mark. 14: 193–204 (2009)Published online 14 January 2009 in Wiley InterScience(www.interscience.wiley.com) DOI: 10.1002/nvsm.349

*Correspondence to: Dr Karen Page, Department ofManagement and Marketing, University of Wyoming,1000 E. University Ave., Dept 3275, Laramie, Wyoming82072, USA.E-mail: [email protected]

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

precisely what that value is. Auctions formineral leases, failed banks, distressed proper-ties, and treasury securities are commonexamples of common value auctions; the onlypurpose of purchasing the prospect is toexploit it for future economic gain.In an independent private value auction,

each bidder knows what the value of theprospect is to him or herself but does not knowwhat the value is to each of the other bidders.Art and rare book auctions are generallyviewed as independent private value auctionsbecause of the assumption that the bidders arepurchasing the prospect for their own plea-sure, eclat or other, noncommercial motive.Many auctions have both common and

private value elements. For example, to theextent that people purchase art for investmentand future resale, they are bidding onunknown common value. Ability to integratea mineral lease into existing infrastructure or toapply proprietary exploration or developmenttechnology to a lease could also increaseprivate value to some bidders.

Types of auctions

The most vivid form of auction is a live, oralascending (English) auction conducted by atalented auctioneer who can incite a biddingfrenzy. Perhaps the most notorious example ofthis type of auction was in 193 A.D. when thePraetorian Guard killed Emperor Pertinax andoffered the crown, along with the RomanEmpire, to the highest bidder (Cassady, 1967).The winning bid was 6250 drachmas for eachguardsman.A popular derivative of the live auction is the

silent auction, in which bids are placedsequentially in writing with full knowledgeof previous bids. Yahoo and eBay are examplesof ascending silent auctions, though thewinner in Yahoo pays the highest bid, whilethe winner in eBay pays the second highest bidplus an incremental amount. Live oral andsilent auctions can also be conducted in thedescending ‘‘Dutch’’ fashion by starting at ahigh price and decreasing it until a bidderagrees to the price, at which time the auction isover (Subramanian and Zeckhauser, 2004).

In contrast to the open auctions are sealedbid auctions in which all bids are sealed untilthey are opened at the same time, thuspreventing bidders from adjusting their bidsin response to other bids. The most commonclosed bid auctions are the first-price andsecond-price sealed-bid auction where theamount paid by the winner is the highestbid or the second highest bid, respectively(Beltran and Santamarıa, 2006). Other sealedbid auctions include the ‘‘all-pay auction,’’ inwhich every bidder pays his or her bid, the‘‘sad losers’’ auction, in which every bidderexcept the winner pays his or her bid, and the‘‘Santa Claus auction,’’ in which the auctioneertakes the payment from the winner and givesback a portion of it to all bidders, including thewinner (Beltran and Santamarıa, 2006).

‘‘Buy it now’’

A relatively recent innovation in auctions is the‘‘buy it now’’ option, which allows bidders tobuy the item at a fixed price that is much largerthan the seller’s reserve price and generally,though not always, higher than the item’svalue. Lucking-Reiley (1999, p. 245) noted thatthe ‘‘buy it now’’ option essentially allows ‘‘thebidder to buy an early end to the auction bysubmitting a sufficiently high bid.’’ Auctionscan be designed with a permanent ‘‘buy itnow’’ option in which the option is availablefor the entire duration of the auction or atemporary ‘‘buy it now’’ option in which theoption may end before the auction ends.

Seller’s in commercial auctions like eBaybenefit from the ‘‘buy it now’’ option by gettingtheir money sooner and perhaps getting moremoney than they would through a sequentialauction. Seller’s in charity auctions do not gettheir money sooner with the ‘‘buy it now’’option than they would without the option,but rely instead on maximizing revenues.

Auctions in nonprofit fundraising

The nonprofit sector employs 7% of the work-force (Kelly, 1998) and accounts for 5.2% ofgross domestic product and 8.3% of wages and

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

194 Karen Page

salaries paid in the United States (UrbanInstitute, 2006). In 2004, this sector accountedfor approximately $1.4 trillion in revenue and $3trillion dollars in assets (Urban Institute, 2006).Private contributions represent approximately$175 billion annually (Urban Institute, 2006).People give to charities for many reasons,

including affinity for the cause, personalnetworks, public recognition, and the desireto help effect positive outcomes (Hartsook,1998). Specific to the athletic context, primarymotives for donating to college athleticprograms include supporting and improvingthe athletic program, receiving tickets, helpingstudent-athletes, deriving entertainment andenjoyment, supporting and promoting theuniversity (non-athletic programs), receivingmembership benefits, repaying past benefitsreceived, helping and enhancing the com-munity, and psychological commitment (Glad-den et al., 2005). In a recent neurologicalstudy, researchers found that giving to charitytriggers the same ‘‘warm glow’’ that peopleexperience when they sate their hunger orsocialize with friends (Preston, 2007). The factthat Wyoming, which has no state income tax,had the highest per-taxpayer charitable con-tributions of any state (National Council ofNonprofit Corporations, 2006) suggests thattax deductibility is not a primary motivator.Nevertheless, empirical data suggest that taxdeductibility of gifts reinforces charitablegiving (Kelly, 1998).Although fundraising has always been a key

activity of nonprofit organizations, it was notuntil the early 20th century that nonprofitentities employed systematic efforts to achievetheir fundraising objectives (Kelly, 1998).These systematic efforts include product sales(e.g., Girl Scout cookies), planned gifts uponthe death of the donor, direct solicitation bymail, phone, and in person, and special events,including auctions (Roth and Ho, 2005). Theauction potentially adds a new motivation forgiving: desire for the auctioned item. In July of2008, for example, the cash-strapped LabourParty in Great Britain auctioned a tennis matchwith Tony Blair, lunch with Sir Alex Ferguson,the manager of Manchester United, and the

opportunity to become a character in anAlastair Campbell novel (Mulholland, 2008).Nonprofit fundraising auctions generally

take on the form of a live, oral auction withan auctioneer, or a silent auction where thebids are either submitted without knowledgeof competing bids or in an open, ascending bidformat where all previous bids are known. Insome cases, both oral and silent formats may beused at the same event. It is with the silentformat that the ‘‘buy it now’’ feature issometimes used.

Theory and hypotheses

In a theoretical paper, Budish and Takeyama(2001) analyzed an auction with a permanent‘‘buy it now’’ option. They considered asituation in which two bidders have indepen-dent private valuations that take on one of twopossible values. In this scenario, when biddersare risk averse, an optimally set buyout pricecan increase the expected revenue of theseller. They concluded that a risk neutral sellerwill find such an option beneficial.In an empirical paper, the effect of eBay’s

‘‘buy it now’’ option on bidder behavior wasinvestigated by conducting auctions of Amer-ican Eagle silver dollars with and without thefunction (Standifird et al., 2004). The studyfound that eBay buyers did not use the ‘‘buy itnow’’ option even when ‘‘buy it now’’ priceswere set below prevailing market prices. Theentertainment, or ‘‘hedonic,’’ benefit associatedwith eBay auctions may explain this somewhatcounterintuitive finding. It is also possible thatthe lack of scarcity of the merchandise obviatedscarcity as amotivating fact for ‘‘buying it now.’’Are we to believe theory, which suggests that

the ‘‘buy it now’’ option should increase theseller’s revenues, or the single case of AmericanEagle silver dollars, which suggests that the ‘‘buyit now’’ option is irrelevant to bidding, or is therea third possibility that the ‘‘buy it now’’ optioncan backfire and reduce seller’s revenues?

H1: Buy it now will increase revenues

There is an ancient Chinese saying: ‘‘Precious-ness is derived from scarcity’’ (wu yi xi wei

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

Effect of the ‘‘buy it now’’ option 195

gui) (Yao and Li, 2005). Yao and Li (2005)argue that ‘‘possession of a luxury good carriessocial and other values in addition to its ownintrinsic consumption value.’’ In other words,scarcity has an economic utility of its own. Inaddition to the intrinsic desirability of scarceitems, Cialdini (1993) notes that when some-thing becomes less accessible, the freedom tohave it may be lost. According to psychologicalreactance theory, people respond to the loss offreedom by wanting to have it more (Brehmand Brehm, 1981). This includes the freedomto have certain goods and services. Cialdini(1993) also notes that people are most attractedto scarce resources when they compete withothers for them, a condition certainly presentin an auction.The ‘‘buy it now’’ option creates scarcity by

removing the potential time to bid on an item;without the ‘‘buy it now’’ option, bidders haveuntil the auction closes to make the purchase.The concept of scarcity, then, would suggestthat people would be willing to pay more foran item when there is a very real possibilitythat their chance to purchase the item willdisappear under the ‘‘buy it now’’ option.The concept of uncertainty also supports

the notion that a ‘‘buy it now’’ option willincrease revenues to the seller. Uncertainty isconsidered synonymous with anxiety (Roget’sNew Millenium Thesaurus, 2008), or to be acause of anxiety (American Heritage Diction-ary, 2006). Anxiety is, for most people, anunpleasant state they seek to resolve (Wolfe,2005). According to Cialdini (1993), peoplewho face uncertainty are more likely to lookfor external cues regarding appropriate beha-vior to resolve their anxiety. In a ‘‘buy it now’’scenario, the uncertainty is whether or notsomeone else will buy the item at the ‘‘buy itnow’’ price or whether the item will sellconsistent with a traditional English auction.The outside cue to resolve this uncertainty andeliminate the associated anxiety is to ‘‘buy itnow’’ rather than to watch the bidding unfold.Because scarcity increases the perceived

value of an item and uncertainty triggersanxiety, the seller’s revenues should beenhanced by a ‘‘buy it now’’ option where

the ‘‘buy it now price’’ is greater than the valueof the item:

Hypothesis 1 (H1): A ‘‘buy it now’’ option

in a silent auction will increase the seller’s

revenues.

H2: Buy it now will decrease revenues

Even if the bidders resolve their uncertainty bypaying the ‘‘buy it now’’ option price, thisstrategy may ultimately backfire for the seller.In silent auctions, bidders who are biddingsequentially tend to stay in the bidding area orreturn to the bidding area to check on theirbids until bidding closes. This gives them theopportunity to spend time with other itemsthat they otherwise might not notice or bid on.Accordingly, they have more opportunities tobid and enhance the seller’s revenues throughtheir participation. With the ‘‘buy it now’’option, however, buyers do not need to remainin the area to protect their bids; they are free toleave and enjoy less crowded quarters. Accord-ingly, the seller may gain revenues on someitems but lose even more from the loss of bidsthat otherwise might have been made.

It is also possible that the anxiety aroused bythe uncertainty triggered by a ‘‘buy it now’’auctionwill motivate people to escape or avoidthe source of the anxiety (Kipfer, 2006). Inother words, people may avoid the anxiety-triggering stimulus to reduce the anxiety ratherthan resolve the anxiety by paying the ‘‘buy itnow’’ price.

In addition to the motivational effects, the‘‘buy it now’’ option has a structural effect onthe auction. Because the ‘‘buy it now’’ optionlocks in a price, it prevents bidders fromplacing bids above the ‘‘buy it now’’ price evenif they choose to do so. Thus, for example, if anitem has a value of $500 and there is no ‘‘buy itnow’’ option, then bidders could potentiallyplace bids well beyond the value of the item.With the ‘‘buy it now’’ option, bidders arecapped at the first price that meets or exceedsthe ‘‘buy it now’’ price.

The ‘‘buy it now’’ structure may alsodecrease the number of bidders by closing

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

196 Karen Page

the bidding on items before latecomers have achance to participate. To the extent thatarriving late is correlated with status, whichmay be correlated with wealth, the ‘‘buy itnow’’ option may preclude deeper pocketsfrom fully engaging in the auction.The potential reduction in number of

bidders and the effective cap on prices wouldbe expected to have a negative impact on theseller’s revenues.

Hypothesis 2 (H2): A ‘‘buy it now’’ option

in a silent auction will have a negative

effect on the seller’s revenues.

H3: Buy it now will have no effect on

revenues

Standifird et al. (2004) found that eBay buyersdid not use the ‘‘buy it now’’ option even when‘‘buy it now’’ prices were set below prevailingmarket prices. The authors opined that theentertainment value associated with eBayauctions may explain this finding. AlthoughMollenberg (2004) found that less than half ofonline auction shoppers are experientialoriented, this still leaves a large portion ofauction shoppers who do shop auctions for theexperience. This is consistent with the anthro-pological arguments that shopping is all aboutthe experience of saving (Miller, 1998), con-sumers’ imagination and fantasy (Campbell,1987), and the thrill of the hunt (Bardhi, 2003).To the extent that participants attend the

auction for the entertainment value, theywould likely ignore the ‘‘buy it now’’ priceand engage in traditional bidding. Accordingly,the ‘‘buy it now’’ option would be expected tohave a neutral effect on the seller’s revenues(except to the extent it places a cap on the price).

Hypothesis 3 (H3): A ‘‘buy it now’’ option

in a silent auctionwill have no effect on the

seller’s revenues.

Data and methods

Data

The data are comprised of 4 years of biddinginformation from a state university art

museum’s silent auctions that are part of anannual black tie fundraising event. These werefestive occasions with fine food and dancing.Attendees include university officials, alumni,representatives of local banks and otherinstitutions, and philanthropists from acrossthe state. In the bidding process, the bidderswere anonymous; they bid by number ratherthan name.The data are for 2004, when there was no

‘‘buy it now’’ option, and 2005–2007 wheneach item had a ‘‘buy it now’’ price. The eventwas virtually the same except for the variablestested. Each year, 218–316 items were offeredin the silent auction in eight categories: Art;Boys Toys; Fabulous Finds; Great Getaways;Jewelry; Fine Gifts; Ladies Luxuries; and Sports.The value of the items ranged from $15 forCloisonne hummingbirds to $20 000 for aweek at a fully staffed Tuscany villa. ‘‘Buy itnow’’ premiums ranged from�4% to an outlierof 563% for a ball signed by the universitywomen’s basketball team and a dinner with theteam (this was expected to be a popular itembecause the team had won the NIT Champion-ship the year before). Omitted from theanalyzed data were items for which therewas no stated value, such as a miniaturefootball helmet signed by university’s headfootball coach. One extreme outlier, where thesold price was 33 times the value, was alsoomitted. This was in 2007 for a $300 breastcancer awareness purse that sold for $10 000;clearly the buyer had intended to donate$10 000 and had found significant private valuein the item. In addition, this is one of the 5% ofthe items that year that did not have a ‘‘buy itnow’’ price.

Variables

The objective of this study was to determinewhether the ‘‘buy it now’’ option increases theaverage price of items in a silent auction andwhether there are diminishing returns to the‘‘buy it now’’ price. Accordingly, the depen-dent variable is the actual winning bid, oramount paid, for each item, in proportion tothe value of the item (sold price/value).

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

Effect of the ‘‘buy it now’’ option 197

The independent variables are (1) whetheror not the ‘‘buy it now’’ option was available ornot (comparing 2004 to 2005–2007) and (2)the ‘‘buy it now’’ price in proportion to theactual value of the item (bid/value).The control variables are the ratio of the

minimumbid to the value of the item to controlfor any anchoring based on the minimum bid,the category of item (Art; Boys Toys; FabulousFinds; Great Getaways; Jewelry; Fine Gifts;Ladies Luxuries; and Sports), and the Con-sumer Confidence Index (Swivel, 2008),which is a measure of the degree of optimismon the state of the economy that consumersexpress through their activities of savings andspending. This index is a measure of howconfident US citizens are, for example, aboutretaining their jobs and having disposableincome in the future.

Methods

Four statistical models were used to test thehypotheses. First, a two-group mean-compari-son t-test was used to determine whether themeans of the sold price/value ratio were

significantly different between the no ‘‘buy itnow’’ year (2004) and the ‘‘buy it now’’ years(2005–2007). Second, an ANOVA with anassociated regression was used to compare thevariances of means among sold price/valueratios for each year. Third, an ordinary leastsquares regression was used to regress the soldprice/value ratio on the pre- and post-‘‘buy itnow’’ period and the control variables (theratio of the minimum bid to value, the categoryof item, and the Consumer Confidence Index).Fourth, an ordinary least squares linearregression was used to analyze the effect ofthe ‘‘buy it now’’ premium on the sold price/value ratio for the years in which the ‘‘buy itnow’’ option was used. All models were runusing Stata 10.

Results

Descriptive statistics

Table 1 presents descriptive statistics andcorrelations for continuous key study vari-ables. The value of the items auctioned rangedfrom $15 to $20 000, with a mean value of$407. The minimum bids ranged from $8 to

Table 1. Descriptive statistics and correlations for key study variables (valid N (listwise)¼ 878)

Variable Mean SD Minimum Maximum 1 2

1 Value 406.57 1011.44 15.00 20 000.00 1.00002 Minimum bid 199.97 485.96 8.00 6800.00 0.9527� 1.00003 Buy it now price 489.64 1183.82 20.00 22 000.00 0.9882� 0.9680�

4 Sold price 235.67 644.36 0.00 12 500.00 0.6631� 0.7102�

5 Buy it now premium 128.62 27.29 96% 663% �0.0558 �0.04906 Ratio of sold price to value 80.49 111.93 0.00 33.33 �0.0805� �0.1731�

7 Ratio of minimum bid to value 0.53 0.09 0.13 2.13 �0.0677� 0.01568 Consumer Confidence Index 95.12 6.47 87.30 102.90 0.0205 0.0250

3 4 5 6 7 8

1 Value2 Minimum bid3 Buy it now price 1.00004 Sold price 0.7843� 1.00005 Buy it now premium �0.0026 �0.0249 1.00006 Ratio of sold price to value �0.1599� 0.4395� 0.2851� 1.00007 Ratio of minimum bid to value �0.0616 �0.0149 0.4349� 0.3096� 1.00008 Consumer Confidence Index �0.0292 0.0073 �0.5783� �0.0550 �0.0478 1.0000

Source: University of Wyoming Art Museum.�p< .05.

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

198 Karen Page

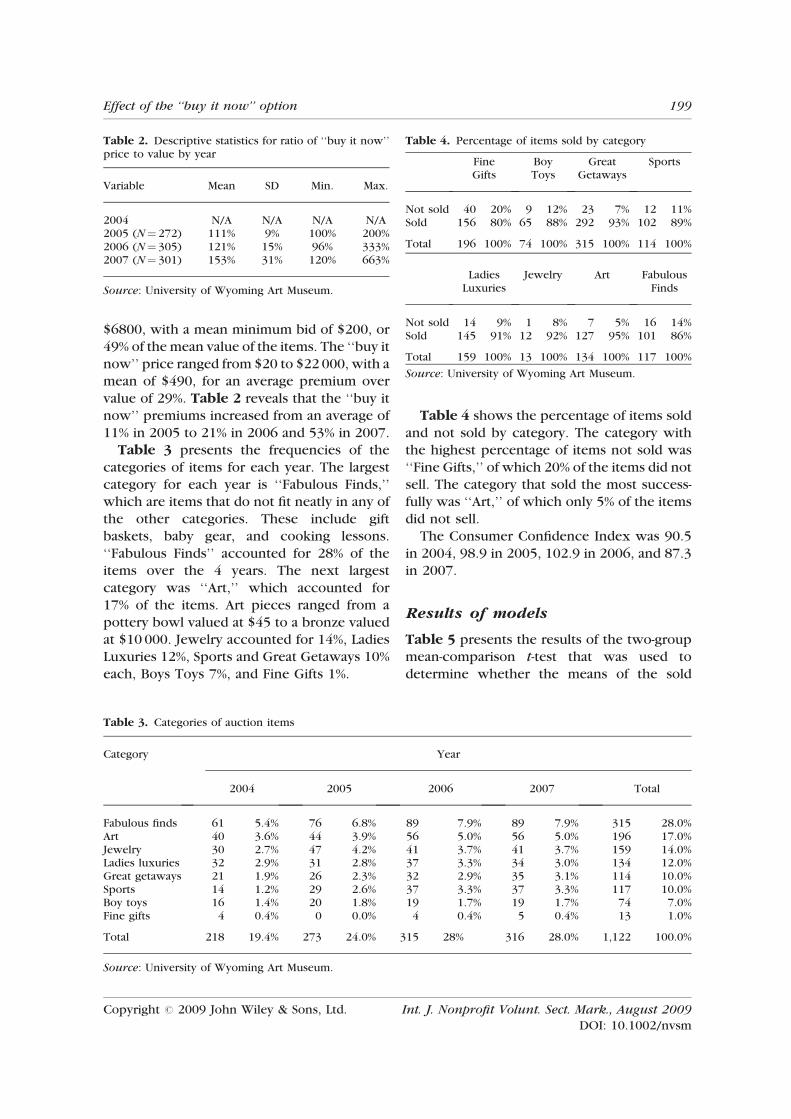

$6800, with a mean minimum bid of $200, or49% of the mean value of the items. The ‘‘buy itnow’’ price ranged from $20 to $22 000, with amean of $490, for an average premium overvalue of 29%. Table 2 reveals that the ‘‘buy itnow’’ premiums increased from an average of11% in 2005 to 21% in 2006 and 53% in 2007.Table 3 presents the frequencies of the

categories of items for each year. The largestcategory for each year is ‘‘Fabulous Finds,’’which are items that do not fit neatly in any ofthe other categories. These include giftbaskets, baby gear, and cooking lessons.‘‘Fabulous Finds’’ accounted for 28% of theitems over the 4 years. The next largestcategory was ‘‘Art,’’ which accounted for17% of the items. Art pieces ranged from apottery bowl valued at $45 to a bronze valuedat $10 000. Jewelry accounted for 14%, LadiesLuxuries 12%, Sports and Great Getaways 10%each, Boys Toys 7%, and Fine Gifts 1%.

Table 4 shows the percentage of items soldand not sold by category. The category withthe highest percentage of items not sold was‘‘Fine Gifts,’’ of which 20% of the items did notsell. The category that sold the most success-fully was ‘‘Art,’’ of which only 5% of the itemsdid not sell.The Consumer Confidence Index was 90.5

in 2004, 98.9 in 2005, 102.9 in 2006, and 87.3in 2007.

Results of models

Table 5 presents the results of the two-groupmean-comparison t-test that was used todetermine whether the means of the sold

Table 2. Descriptive statistics for ratio of ‘‘buy it now’’price to value by year

Variable Mean SD Min. Max.

2004 N/A N/A N/A N/A2005 (N¼ 272) 111% 9% 100% 200%2006 (N¼ 305) 121% 15% 96% 333%2007 (N¼ 301) 153% 31% 120% 663%

Source: University of Wyoming Art Museum.

Table 3. Categories of auction items

Category Year

2004 2005 2006 2007 Total

Fabulous finds 61 5.4% 76 6.8% 89 7.9% 89 7.9% 315 28.0%Art 40 3.6% 44 3.9% 56 5.0% 56 5.0% 196 17.0%Jewelry 30 2.7% 47 4.2% 41 3.7% 41 3.7% 159 14.0%Ladies luxuries 32 2.9% 31 2.8% 37 3.3% 34 3.0% 134 12.0%Great getaways 21 1.9% 26 2.3% 32 2.9% 35 3.1% 114 10.0%Sports 14 1.2% 29 2.6% 37 3.3% 37 3.3% 117 10.0%Boy toys 16 1.4% 20 1.8% 19 1.7% 19 1.7% 74 7.0%Fine gifts 4 0.4% 0 0.0% 4 0.4% 5 0.4% 13 1.0%

Total 218 19.4% 273 24.0% 315 28% 316 28.0% 1,122 100.0%

Source: University of Wyoming Art Museum.

Table 4. Percentage of items sold by category

FineGifts

BoyToys

GreatGetaways

Sports

Not sold 40 20% 9 12% 23 7% 12 11%Sold 156 80% 65 88% 292 93% 102 89%

Total 196 100% 74 100% 315 100% 114 100%

LadiesLuxuries

Jewelry Art FabulousFinds

Not sold 14 9% 1 8% 7 5% 16 14%Sold 145 91% 12 92% 127 95% 101 86%

Total 159 100% 13 100% 134 100% 117 100%

Source: University of Wyoming Art Museum.

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

Effect of the ‘‘buy it now’’ option 199

price/value ratio was significantly differentbetween the no ‘‘buy it now’’ year (2004) andthe ‘‘buy it now’’ years (2005–2007). Thisanalysis reveals that the mean sold price/valueratio is actually significantly greater in 2004than in the other 3 years (t¼ 4.306, p< .0001),supporting H2, which posits that the ‘‘buy itnow’’ option has a negative effect on theseller’s revenues. An examination of the datashows that in fact the 2004 mean was greaterthan the mean for each individual subsequentyear (see Table 6). In other words, this analysissuggests that the ‘‘buy it now’’ option decreasedoverall auction revenues. These results are evenmore pronounced when all sold price/valueratios greater than 1.5 were removed.Table 7 presents the results of the ANOVA

with associated regression that was used tocompare the variances of means among soldprice/value ratios for each year. The results ofthe ANOVA show that there were significantdifferences between the mean variances foreach post-‘‘buy it now’’ year (2005–2007) assuggested in Table 6 above. The results of theassociated regression show that mean variancefor 2004 was significantly higher than 2007,the dropped year, but that 2005 and 2006were

not significantly different than 2007. Indepen-dent tests of mean differences between (1)2005 and 2007 and (2) 2006 and 2007 revealno significant differences (see Table 8).

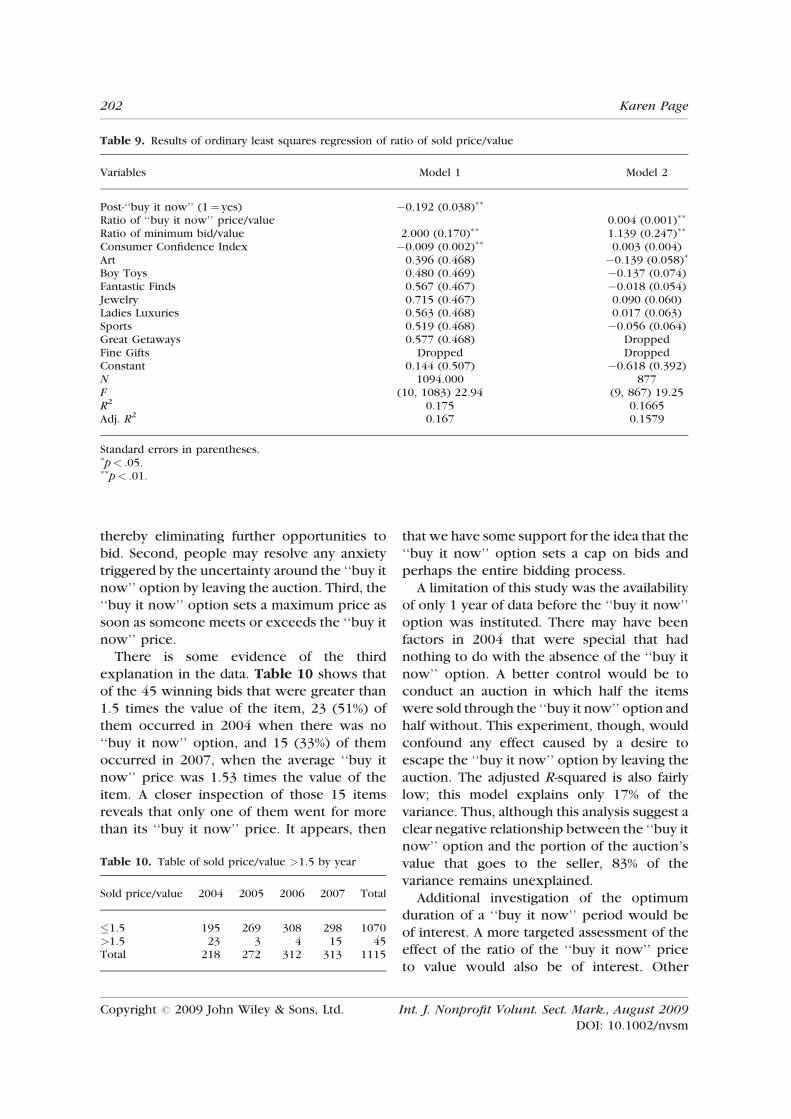

Table 9 presents the results of the ordinaryleast squares linear regression used to analyzethe effect of the ‘‘buy it now’’ option on thesold price/value ratio (Model 1) and the effectof the actual ‘‘buy it now’’ price/value ratio onthe sold price/value ratio (Model 2). Model 1shows that the ‘‘buy it now’’ option (coded‘‘0’’ for 2004 and ‘‘1’’ for 2005–2007) isnegative and significant (b¼�0.192, p< .001),further supporting H2. In other words, the‘‘buy it now option’’ decreases the seller’scapture of overall value in a consequential way.The sold to value ratios in the years that had the‘‘buy it now option’’ (.83) were on average15% less than the sold to value ratios in the yearthat did not have the option (.98). Further,Model 2 shows that the minimum bid/valueratio was positive and significant (b¼ 2.000,p< .001). Thus, the higher the minimum bid,the higher the ultimate selling price. TheConsumer Confidence Index was also signifi-cant but negative (b¼�0.009, p< .001),contrary to intuition. Wyoming’s counter-cyclical economy may explain this.

Model 2 shows that in the years that the ‘‘buyit now’’ option was in place, the higher the‘‘buy it now’’ price/value ratio, the higher thesold price/value ratio. In other words, a higher‘‘buy it now’’ price relative to the value of theitem garnered a higher price. As in Model 1, thecoefficient for the minimum bid/value ratio waspositive and significant (b¼ 0.004, p< .001).However, the actual effect was very marginal;for every 1% increase in ‘‘buy it now’’ price/

Table 5. Two-sample T test with equal variances of pre- and post-‘‘buy it now’’ sold price/value ratios

Group Obs. Mean SE SD 95% CI

Pre-‘‘buy it now’’ 218 0.92 0.04 0.63 0.86 1.00Post-‘‘buy it now’’ 897 0.74 0.18 0.53 0.71 0.78

Pr(T< t)¼ 0.0000t¼ 4.306Degrees of freedom¼ 1113

Table 6. Descriptive statistics of sold price/value ratioby year

Year Obs. Mean SD Min. Max.

2004 218 0.91 0.62 0.00 5.332005 272 0.78 0.50 0.00 6.782006 312 0.71 0.44 0.00 4.002007 314 0.73 0.61 0.00 6.58

Source: University of Wyoming Art Museum.

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

200 Karen Page

value, there is a .004% change in the sold price/value. In real terms, for an item with a$500 value, a $5 increase in ‘‘buy it now’’ pricewould translate to increased revenues to theseller of $.02. The Consumer Confidence Indexwas not significant in this model. Alsomarginallysignificant was the effect of Art (b¼�0.139,p< .05), compared to Great Getaways and FineGifts, the dropped variables; Art retrievedrelatively less value than those categories.

Discussion, implications, andlimitations

The results of this study clearly suggest that‘‘buy it now’’ options may not in the best

interest of sellers. While intuition mightsuggest that a ‘‘buy it now’’ price that providesa healthy built-in premiumwould boost overallrevenues, these results suggest that this is notthe case. Indeed, even in 2007, where theaverage ‘‘buy it now’’ price was 1.53 times thevalue of the items, the average sold price wasonly .73 times the value of the items, comparedto an average sold price of .92 times the valuein 2004.While this study supports H2 (a ‘‘buy it

now’’ option in a silent auction will have anegative effect on the seller’s revenues), we donot know exactly why. There are threepossible explanations. First, people may exitthe auction once they have won an item,

Table 8. Two-sample T test with equal variancescomparing 2007 sold price/premium ratio to 2005 and 2006

Group Obs. Mean SE SD 95% CI

2005 272 0.783 0.030 0.497 0.723 0.8422007 313 0.733 0.035 0.614 0.666 0.802

Pr(T< t)¼ 0.147t¼ 1.049Degrees of freedom¼ 583

2006 312 0.920 0.040 0.630 0.830 1.0002007 313 0.730 0.030 0.610 0.660 0.800

Pr(T< t)¼ 0.6969t¼�0.516Degrees of freedom¼ 623

Table 7. ANOVA and regression of sold price/value by year

Source SS df MS

Model 6.29 3 2.10 Number of obs¼ 1115Residual 331.51 1111 0.30 F(3, 1111)¼ 7.03Total 337.80 1114 0.30 Prob> F¼ 0.0001

R-squared¼ 0.0186Adj R-squared¼ 0.0160Root MSE¼ .54 625

Coef. SE t P> T 95% CI

Constant 0.73 0.03 23.77 0.00 0.67 0.792004 0.18 0.05 3.83 0.00 0.09 0.282005 0.05 0.05 1.08 0.28 �0.04 0.142006 �0.02 0.04 �0.51 0.61 �0.11 0.062007 (Dropped)

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

Effect of the ‘‘buy it now’’ option 201

thereby eliminating further opportunities tobid. Second, people may resolve any anxietytriggered by the uncertainty around the ‘‘buy itnow’’ option by leaving the auction. Third, the‘‘buy it now’’ option sets a maximum price assoon as someone meets or exceeds the ‘‘buy itnow’’ price.There is some evidence of the third

explanation in the data. Table 10 shows thatof the 45 winning bids that were greater than1.5 times the value of the item, 23 (51%) ofthem occurred in 2004 when there was no‘‘buy it now’’ option, and 15 (33%) of themoccurred in 2007, when the average ‘‘buy itnow’’ price was 1.53 times the value of theitem. A closer inspection of those 15 itemsreveals that only one of them went for morethan its ‘‘buy it now’’ price. It appears, then

that we have some support for the idea that the‘‘buy it now’’ option sets a cap on bids andperhaps the entire bidding process.

A limitation of this study was the availabilityof only 1 year of data before the ‘‘buy it now’’option was instituted. There may have beenfactors in 2004 that were special that hadnothing to do with the absence of the ‘‘buy itnow’’ option. A better control would be toconduct an auction in which half the itemswere sold through the ‘‘buy it now’’ option andhalf without. This experiment, though, wouldconfound any effect caused by a desire toescape the ‘‘buy it now’’ option by leaving theauction. The adjusted R-squared is also fairlylow; this model explains only 17% of thevariance. Thus, although this analysis suggest aclear negative relationship between the ‘‘buy itnow’’ option and the portion of the auction’svalue that goes to the seller, 83% of thevariance remains unexplained.

Additional investigation of the optimumduration of a ‘‘buy it now’’ period would beof interest. A more targeted assessment of theeffect of the ratio of the ‘‘buy it now’’ priceto value would also be of interest. Other

Table 10. Table of sold price/value >1.5 by year

Sold price/value 2004 2005 2006 2007 Total

�1.5 195 269 308 298 1070>1.5 23 3 4 15 45Total 218 272 312 313 1115

Table 9. Results of ordinary least squares regression of ratio of sold price/value

Variables Model 1 Model 2

Post-‘‘buy it now’’ (1¼ yes) �0.192 (0.038)��

Ratio of ‘‘buy it now’’ price/value 0.004 (0.001)��

Ratio of minimum bid/value 2.000 (0.170)�� 1.139 (0.247)��

Consumer Confidence Index �0.009 (0.002)�� 0.003 (0.004)Art 0.396 (0.468) �0.139 (0.058)�

Boy Toys 0.480 (0.469) �0.137 (0.074)Fantastic Finds 0.567 (0.467) �0.018 (0.054)Jewelry 0.715 (0.467) 0.090 (0.060)Ladies Luxuries 0.563 (0.468) 0.017 (0.063)Sports 0.519 (0.468) �0.056 (0.064)Great Getaways 0.577 (0.468) DroppedFine Gifts Dropped DroppedConstant 0.144 (0.507) �0.618 (0.392)N 1094.000 877F (10, 1083) 22.94 (9, 867) 19.25R2 0.175 0.1665

Adj. R2 0.167 0.1579

Standard errors in parentheses.�p< .05.��p< .01.

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

202 Karen Page

experimental approaches might allow testingof specific theoretical constructs. For example,an experimental design that would impose the‘‘buy it now’’ only after a period of openbidding might help isolate any ‘‘late comer’’effect.Because the effect size in this investigation

was substantial, further study with the goal ofenhancing revenues of charitable fundraisingactivities could be of substantial value, particu-larly as adverse economic conditions pressurereceipts from donor and while at the sameincreasing the need for services of nonprofitorganizations.

Conclusion

The purpose of this paper was to examine therelationship between a ‘‘buy it now’’ optionand auction revenues. The results suggest thatthe ‘‘buy it now’’ option in silent auctionsactually harms sellers. More work needs to bedone to determine whether this effect is due toanxiety caused by the uncertainty, the exodusof participants after they have placed a ‘‘buy itnow’’ option bid or seen their chosen itemsalready purchased, the lack of entertainmentvalue associated with the auction, or for someother reason.

Biographical notes

Dr Karen Page received her JD from theUniversity of Denver, MA in Economics fromthe University of Colorado, and MA and PhDfrom the Stanford University Graduate Schoolof Business. Dr Page is an assistant professor inthe Department of Management and Marketingat the University of Wyoming, where she tea-ches StrategicManagement, Negotiations, Finan-cing New Ventures, and OrganizationalBehavior.

References

American Heritage Dictionary. 2006. Houghton

Mifflin: Boston.

Bardhi F. 2003. Thrill of the hunt: thrift shopping

for pleasure. Advances in Consumer Research

30: 375–376.

Beltran F, Santamarıa N. 2006. A measure of the

variability of revenue in auctions: a look at the

revenue equivalence theorem. Journal of

Applied Mathematics and Decision Sciences

2006(4): 1–14.

Brehm SS, Brehm JW. 1981. Psychological Reac-

tance: A Theory of Freedom and Control. Aca-

demic Press: New York.

Budish EB, Takeyama LN. 2001. Buy prices in online

auctions: irrationality on the internet? Economics

Letters 72: 325–333.

Campbell C. 1987. The Romantic Ethic and Spirit of

Modern Consumerism. Basil Blackwell: London.

Carpenter J, Holmes J, Matthews HP. 2008. Charity

auctions: a field experiment. Economic Journal

118: 92–113.

Cassady R. 1967. Auctions and Auctioneering.

University of California: Berkeley.

Cialdini RB. 1993. Influence. Quill: New York.

Engelbrecht-Wiggans R, Katok E. 2006. E-sourcing

in procurement: theory and behavior in reverse

auctions with noncompetitive contracts. Man-

agement Science 52: 581–596.

Engers M, McManus B. 2007. Charity auctions.

International Economic Review 48: 953–994.

Gattiker TF, Huang X, Schwarz JL. 2007. Nego-

tiation, email, and internet reverse auctions:

how sourcing mechanisms deployed by buyers

affect suppliers’ trust. Journal of Operations

Management 25: 184–202.

Gladden JM, Mahony DF, Apostolopoulou A. 2005.

Toward a better understanding of college athletic

donors: what are the primary motives? Sport

Marketing Quarterly 14: 18–30.

Hartsook RF. 1998. 77 reasons why people give.

Fund Raising Management 29(10): 16–19.

Kelly KS. 1998. Effective Fund-Raising Manage-

ment. Lawrence Erlbaum: Philadelphia.

Kipfer BA. 2006. Roget’s Thesaurus (6th edn).

Harper: New York.Klemperer P. 2004. Auctions: Theory and Practice.

Princeton University Press: Princeton.

Lucking-Reiley D. 1999. Using field experiments to

test equivalence between auction formats: magic

on the internet. American Economic Review 89:

1063–1080.

Mathews T. 2006. Bidder welfare in an auction with

a buyout option. International Game Theory

Review 8: 595–612.

Miller D. 1998. A Theory of Shopping. Cornell

University Publishing: Ithaca.

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

Effect of the ‘‘buy it now’’ option 203

Mollenberg A. 2004. Internet auctions inmarketing:

the consumer perspective. Electronic Markets

14: 360–371.

Mulholland H. 2008. Cash-strapped Labour

auctions off game of tennis with Tony Blair.

guardian.co.uk, Friday 11 July 2008. http://

www.guardian.co.uk/politics/2008/jul/11/labour.

tonyblair

National Council of Nonprofit Corporations. 2006.

The United States Nonprofit Sector.

Preston C. 2007. Brain research suggests ’neural

reward’ for charitable donors. Chronicle of Phi-

lanthropy 19(18): 16.

Roth S, Ho M. 2005. The Accidental Fundraiser: A

Step-by-Step Guide to Raising Money for Your

Cause. Chardon Press: Indianapolis.

Seligman MEP, Walker EF, Rosenhan DL. 2001.

Abnormal Psychology, (4th edn). W.W. Norton

& Company, Inc.: New York.

Standifird SS, Roelofs MR, Durham Y. 2004. The

impact of eBay’s buy-it-now function on bidder

behavior. International Journal of Electronic

Commerce 9: 167–176.

Subramanian G, Zeckhauser R. 2004. For sale, but

how? auctions vs, negotiations. Negotiation 20:

3–5.

Swivel.com. 2008. Consumer Confidence Index. http:

//www.swivel.com/data_columns/show/8751077

Ubbels B, Verhoef ET. 2008. Auctioning conces-

sions for private roads. Transportation

Research Part A: Policy and Practice 42: 155–

172.

Urban Institute. 2006. The Nonprofit Sector in

Brief: Facts and Figures from the Nonprofit

Almanac 2007.

Wolfe BEE. 2005. Understanding and Treating

Anxiety Disorders: An Integrative Approach to

Healing the Wounded Self. American Psycho-

logical Association: Washington, DC.

Yao S, Li K. 2005. Pricing superior goods: utility

generated by scarcity. Pacific Economic Review

10: 529–538.

Copyright # 2009 John Wiley & Sons, Ltd. Int. J. Nonprofit Volunt. Sect. Mark., August 2009

DOI: 10.1002/nvsm

204 Karen Page