an intertemporal general equilibrium model of asset prices - a short...

TRANSCRIPT

An Intertemporal General EquilibriumModel of Asset Prices

A short review

by Cox, Ingersoll, and Ross

November 20, 2012

1 / 23

Introduction

• Merton (1973) analyzes a continuous time,consumption-based asset pricing model. It makesparametric assumptions on the price processes, andthere is no production in the economy.

• Lucas (1978) analyzes a discreet time,consumption-based model. It allows production, doesnot make parametric assumptions on how to priceassets, and is a general equilibrium model.

• There is a companion paper by the same authors thatdiscusses a specialization of the model in this paper.

2 / 23

The setup

The economy has

1. production processes; n of them

2. contingent claims; a lot of them, and the exactnumber is not important

Agents makes the following decisions

1. how to consume; {ct : t > 0} = c

2. how to invest in assets; {at : t > 0} = a

3. how to invest in claims; {bt : t > 0} = b

The economy equilibrates and determines

1. interest rate; r

2. expected rate of return of claims; β

3 / 23

Parametric assumptions of the economy

• The state variables Y has the dynamics

dY (t) = µ(Y, t)dt+ S(Y, t)dw(t)

• The production technology

I−1η dη(t) = α(Y, t)dt+G(Y, t)dw(t)

• The contingent claims

dF i(t) = [F i(t)βi(t)− δi(t)] + F i(t)hidw(t)

But note that β is an endogenous process.

4 / 23

The representative agent optimizes theinvestment and consumption

There is a state and time dependent utility function

U(ct, Yt, t),

and the agent makes the following decision at each t

1. at; investment in productive assets

2. bt; investment in auxiliary assets

3. ct; consumption

We refer to the triple (a, b, c) the control process andlabel it v = {vt : t ≥ 0}.

5 / 23

The wealth process balances the budget

Fix the control (a, b, c), the wealth process take thefollowing dynamics. For simplicity, let n = k = 1.

dWt = [atWt(α− r) + btWt(βt − rt) + rtWt − ct] dt+ atWt[g1dw1(t) + g2dw1(t)]

+ btWt[(h1dw1(t) + h2dw1(t)],

where the index 1 refers to the production asset andindex 2 refers to the contingent-claim asset.

The wealth process restricts the consumption andinvestment decision so that the budget constraint is notviolated.

6 / 23

The agent’s optimization problem

The agent solves the following stochastic control problem

supv

E[∫ ∞

0U(cs, Ys, s)ds

]subject to: W0 = w0 and Wt ≥ 0.

Use the hat to denote optimal policy, i.e. v denotes an

optimal control.

7 / 23

Solving agent’s problem (1): Dynamicprogramming principal (DPP)

Define the value function J as

J(t, w, y) = supv

E[∫ ∞

tU(cs, Ys, s)ds

]subject to: Wt = w and Yt = y

Then locally, the optimality condition becomes

J(t, w, y) = supv

E[∫ τ

tU(cs, Y

w,ys , s)ds+ J(τ,Ww,y

τ , Y w,yτ )

]

8 / 23

Solving agent’s problem (2): HJB-PDE

With DPP, Ito’s formula, and the assumption that J issmooth enough, we get the following non-linear PDE

supv

[LvJ + U(v, y, t)] = −Jt,

with some boundary conditions.

9 / 23

Solution of the PDE vs. solution to theoriginal stochastic control problem

lemma (1)

If J is a solution to the PDE and also J is C2, then

1. J is a value function.

2. the v s.t. LvJ +U(v, y, t) = −Jt is an optimal policy.

Note that the Bellman equation by itself is neithersufficient nor necessary.

To find the solution of the stochastic control problem:

1. Solve the PDE

2. Verification step

10 / 23

Solving agent’s problem (3): Resolution

Make the explicit assumption that the value solutiont, w, y 7→ J(t, w, y) exists and is unique.

lemma (2)

J(t, w, y) is increasing and strictly concave in w.

11 / 23

Towards an equilibrium

The equilibrium conditions are:

1.∑

i = ai = 1

2. bi = 0

Then, finding the solution to the agent’s problem andimposing the equilibrium conditions pin down thefollowing processes:

1. r; the interest rate

2. β; the expected return of claims

3. a investment strategy

4. c consumption

12 / 23

Key result (1): Interest rate

Theorem (1)

r(t, w, y) =

1. atα− −JwwJw

var(w)

w−

k∑i=1

−JwyiJw

cov(w, yi)

w

2. − Jwt + LJwJw

= −D[Jw]

Jw

3. atα+

[cov(w, Jw)

wJw

],

where the evaluation is w = Wt and y = Yt.

13 / 23

Key result (2): Determining β

Theorem (2)

(βi − r)F i =

1. [φWφYi · · ·φYk ][F iWFiY1 · · ·F

iYk

]T

2. − cov(F i, Jw)

F iJw

φ(·) is specified in equation (20).

14 / 23

Key result (3): Pricing contingent claims

Theorem (3)

The pricing formula F (t, w, y) satisfies the following PDE

LF (t, w, y) + δt = rtF (t, w, y),

where r is determined by Theorem (1) and L is thedifferential generator.

Note that this PDE and along with boundary conditions,which depends on each particular contingent claim, wouldyield the deterministic pricing formula F (t, w, y).

15 / 23

The equilibrium pricing formula is analogousto the Black-Scholes pricing formula)

In the BS setup, a contingent claim that pays h(XT ) atthe termination time T is priced at

F (t, s) = Et,x[e∫ Tt −rdsh(XT )

].

Then, a Feynman-Kac type argument would require thatF (t, s) would also satisfy the PDE

LF (t, s) = rF (t, s),

with terminal condition

f(T, s) = h(s), for all s.

16 / 23

Lemma 3 makes this connection precise

lemma (3)

The solution to the pricing PDE with the boundarycondition given in (34) can be calculated by the followingexpectation formula,

F (W,Y, t, T ) = E{ Θ(W (T ), Y (T ))[exp{−∫ T

tβudu}]1τ≥T

+ Φ(W (τ), Y (τ), τ)[exp{−∫ τ

tβudu}]1τ<T

+

∫ τ∧T

tδs[exp{−

∫ s

tβudu}]ds }.

17 / 23

Pricing in terms of marginal-utility-weightedexpected value

Theorem (4)

F (W,Y, t, T ) = E{ Θ(W (T ), Y (T ))JW (W (T ), Y (T ), T )

JW (W (t), Y (t), t)1τ≥T

+ Φ(W (τ), Y (τ), τ)JW (W (τ), Y (τ), τ)

JW (W (t), Y (t), t)1τ<T

+

∫ τ∧T

tδsJW (W (s), Y (s), s)

JW (W (t), Y (t), t)ds }.

Roughly, it states that the correct “pricing kernel” is theinter-temporal marginal rate of substitution:JW (W (s),Y (s),s)JW (W (t),Y (t),t) .

18 / 23

Comparing to the Lucas model of a single asset

The lucas model prices the asset with payment stream xtat

pt = Et ∞∑j=t

βju′(xj+1)

u′(xt)xj+1

.

Now consider a similar contingent claim in thecontinuous-time economy in which the asset pays thestream δt without a stopping rule. Then this asset ispriced at

pt = Et[∫ ∞

t

JW (W (s), Y (s), s)

JW (W (t), Y (t), t)δsds

].

The lack of a discounting factor here is due to theassumption on U(t, ·).

19 / 23

Let’s see an application/specialization

1. Restrict U to be log utility, state-independent, andtime-homogeneous after discounting in that

U(c, t) = e−∫ t0 rsdslog(c).

2. Let there be only one state variable with thefollowing dynamics

dY (t) = (ξY (t) + ζ)dt+ ν√Y (t)dw(t).

20 / 23

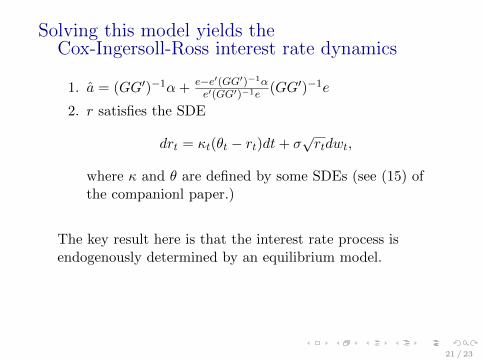

Solving this model yields theCox-Ingersoll-Ross interest rate dynamics

1. a = (GG′)−1α+ e−e′(GG′)−1αe′(GG′)−1e

(GG′)−1e

2. r satisfies the SDE

drt = κt(θt − rt)dt+ σ√rtdwt,

where κ and θ are defined by some SDEs (see (15) ofthe companionl paper.)

The key result here is that the interest rate process isendogenously determined by an equilibrium model.

21 / 23

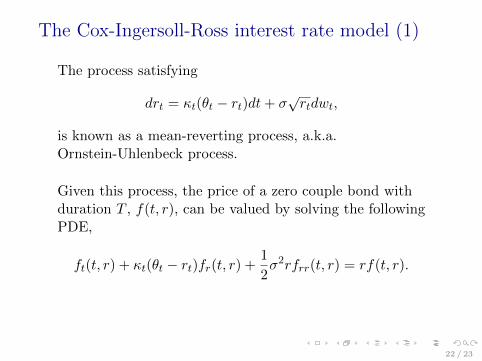

The Cox-Ingersoll-Ross interest rate model (1)

The process satisfying

drt = κt(θt − rt)dt+ σ√rtdwt,

is known as a mean-reverting process, a.k.a.Ornstein-Uhlenbeck process.

Given this process, the price of a zero couple bond withduration T , f(t, r), can be valued by solving the followingPDE,

ft(t, r) + κt(θt − rt)fr(t, r) +1

2σ2rfrr(t, r) = rf(t, r).

22 / 23

The Cox-Ingersoll-Ross interest rate model (2)

The solution turns out to be tractable and has a closedform

f(t, r) = exp{−rC −A},

for some constant deterministic functions C(t, T ) andA(t, T ). And this corresponds to an affine yield

Y (t, T ) =1

T − t(rC +A),

which is a comforting result for some folks.

23 / 23