an introduction to lean accounting - gianesin, canepari...

TRANSCRIPT

An Introduction to Lean Accounting

Asolo, 17 aprile 2009

© BMA Inc. 2009. All rights reserved.

The Philosophy of LeanMaximize competitive

advantage through operational excellenceoperational excellence

Improve the flow and you

© BMA Inc. 2009. All rights reserved.

yimprove profitability

Traditional thinking and lean thinking ad t o a t g a d ea t gare in conflict

Traditional Standard Lean

ASSUMPTIONS

Costing

ASSUMPTIONS

Thinking ASSUMPTIONS

• Profit comes from full utilization of resources

ASSUMPTIONS• Profit from maximizing

flow on pull from customers

• Direct labour is a variable cost and the most important conversion cost

customers.• Labour is fixed, and waste

is the most important cost• Control through visual

• Control the business thru detailed tracking

• All excess capacity is bad

Control through visual management and continuous attention to flow & waste

© BMA Inc. 2009. All rights reserved.

• Excess capacity provides flexibility

Why Lean Accounting?y g

• Traditional Standard Costing was developed for mass production

– The philosophy is that profitability is maximized when labor and machine utilization are maximized

• The focus of Standard costing is on lowest cost per item through economies of scalethrough economies of scale

• This does not apply in a high variability, multi-product environment

– Here profitability is maximized when the rate of flow is

© BMA Inc. 2009. All rights reserved.

maximized

What’s the problem?What s the problem?T diti l t tTraditional management systems:

– Actively work against Lean transformation & other lean improvements.

– Are expensive and wasteful.– Provide misleading, wrong, and harmful

information.M ti t l t d th thi– Motivate people to do the wrong things.

– Are complex and confusing to people.

Here’s a Few Simple Examples

© BMA Inc. 2009. All rights reserved.

p p

Actively work against lean manufacturing

Drill on CNC Machine

Batch 2500

Inspect & Pack

1 i t 4 i t1 minute 4 minutes

Machine on LatheGrind

4 minutes6 minutes

Total labor time: 15 minutesLabor cost: $5.00Overhead cost: $15.00

Lead Time: 6 weeksInventory 25 daysBatch size 2500

© BMA Inc. 2009. All rights reserved.

$Material Cost $1.50TOTAL COST: $21.50

On-Time delivery = 82%

Lean manufacturing changesLean manufacturing changesC t ll• Create a cell.

• Use an drilling machine with quick change over.• Reduce the batch size.• Reduce the lead time.• Reduce inventory.• Almost perfect delivery.Almost perfect delivery.• Created additional capacity on the CNC

machine.machine.

© BMA Inc. 2009. All rights reserved.

Lean improvementsLean improvements

Drill on Drilling Machine

Machine on Lathe Machine

4 minutes 4 minutes Lean Cell

Grind Inspect & Pack

4 minutes6 minutes

Total labor time: 18 minutesLabor cost: $6.00Overhead cost: $18.00

Lead Time: 2 daysInventory 5 daysBatch size 250

© BMA Inc. 2009. All rights reserved.

$Material Cost $1.50TOTAL COST: $25.50

On-Time delivery = 98%

The problemWe have made great improvement.

BUT th d t t h d thBUT…. the product cost has gone up and the project is in doubt.

In fact, the changes were highly beneficialhighly beneficial both operationally and financially.

It is the standard costing that is leading us i th di ti

© BMA Inc. 2009. All rights reserved.

in the wrong direction.

There is no “Standard” Cost!In a lean environment, the cost

of the product is related to of the product is related to flow…

•Waste affects cost so that there is no one ‘standard’ cost of a product•Cost varies with production scrap mix quality downtime etc•Cost varies with production, scrap, mix, quality, downtime etc

• If you control the flow, you control the cost

B i i fl th h th V l St

© BMA Inc. 2009. All rights reserved.

• By improving flow through the Value Streamwe improve capacity = flexibility

Performance MeasurementsPerformance Measurements

Traditional accounting performance measurements motivate non-lean actions.Measuring labor efficiency, machine utilization,

and overhead absorption leads to largeand overhead absorption leads to large batches and high inventory.

© BMA Inc. 2009. All rights reserved.

Transaction-based control t t t hsystems cost too much

Entering and administering transactions is wasteful and time-consuming.

EXAMPLE:A production plant with 150 people, 120 products, and revenue of p p p p , p ,$15M required over 4,000,000 transactions per year.

Job costing proc rement in entor controlJob costing, procurement, inventory control, accounts payable, accounts receivable:

38 equivalent heads spent processing and38 equivalent heads spent processing and using the transactions.

12 7% of revenue

© BMA Inc. 2009. All rights reserved.

12.7% of revenue

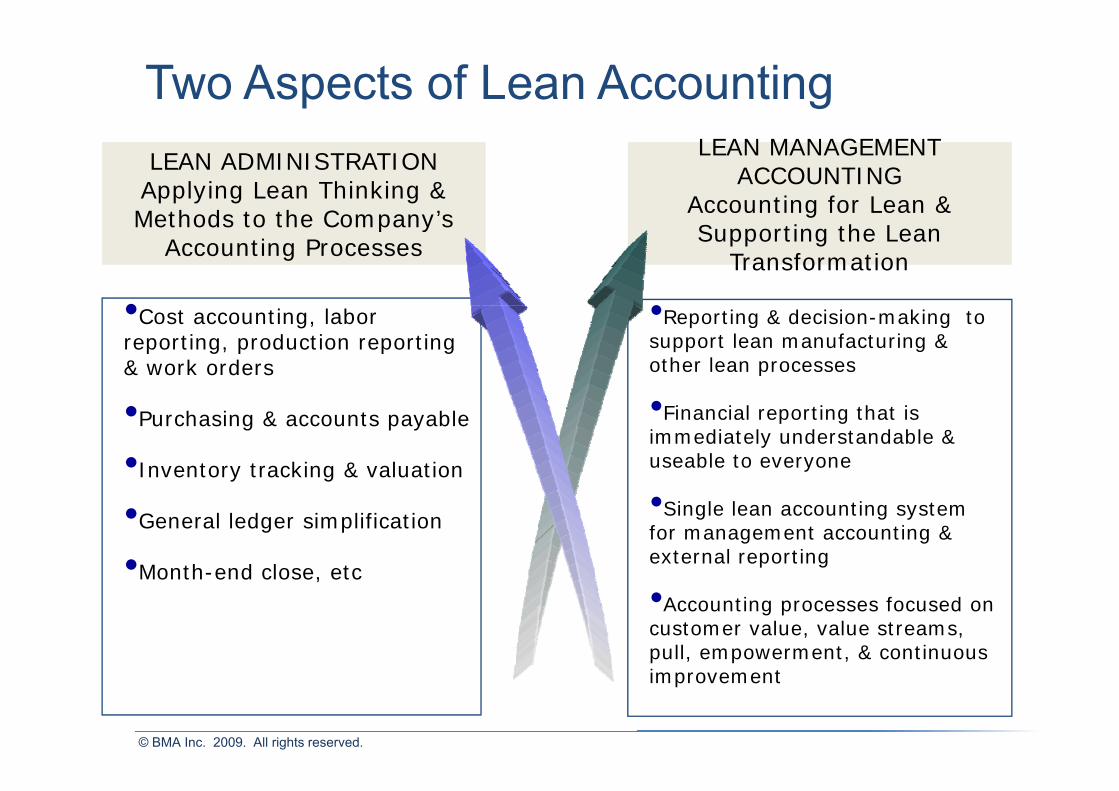

Two Aspects of Lean AccountingLEAN ADMINISTRATION

Applying Lean Thinking & Methods to the Company’s

LEAN MANAGEMENT ACCOUNTING

Accounting for Lean & Methods to the Company s Accounting Processes

gSupporting the Lean

Transformation

• ••Cost accounting, labor reporting, production reporting & work orders

•Reporting & decision-making to support lean manufacturing & other lean processes

•Purchasing & accounts payable

•Inventory tracking & valuation

•Financial reporting that is immediately understandable & useable to everyone

•General ledger simplification

•Month-end close etc

•Single lean accounting system for management accounting & external reporting

Month end close, etc•Accounting processes focused on customer value, value streams, pull, empowerment, & continuous

© BMA Inc. 2009. All rights reserved.

improvement

Lean is a People Process►The aim of lean is a production system that highlights

problems and a human system that produces people who are willing and able to identify and solve themare willing and able to identify and solve them

►Eliminating waste is done by people using

rigorous problem

►Behaviours that focus on

improvement & rigorous problem-solving methods

improvement & problem-solving

►Involving people►Lean is a set of

collaborative and inquisitive g p pin lean is at leastas important as

lean tools.

collaborative and inquisitive behaviours that result in a

culture of continuous improvement

All of this All of this requires Trustrequires Trust

© BMA Inc. 2009. All rights reserved.

improvement.

Lean Accounting has Seven AimsPerformance Performance

measures thatmeasures thatSupport relevant, Support relevant,

accurate & timelyaccurate & timelyElimination Elimination

ofofDrive the growth of Drive the growth of the business bythe business bymeasures that measures that

motivate leanmotivate lean––cell cell & value stream & value stream

measuresmeasures

accurate & timely accurate & timely decision making decision making

using contribution using contribution costingcosting

of of unnecessary unnecessary accounting accounting

transactionstransactions

the business by the business by increasing customer increasing customer value using Target value using Target

CostingCostingmeasuresmeasures costingcosting transactionstransactions CostingCosting

Value Stream Value Stream Costing, replacing Costing, replacing Standard Costing =Standard Costing =

Highlighting impact Highlighting impact of lean improvements of lean improvements

–– eliminate waste,eliminate waste,

Motivate lean Motivate lean behaviour in the behaviour in the

budgetingbudgeting

© BMA Inc. 2009. All rights reserved.

Standard Costing Standard Costing Value Stream Profit & Value Stream Profit &

Loss AccountLoss Account

eliminate waste, eliminate waste, improve capacity, improve capacity,

improve flowimprove flow

budgeting budgeting process process

Box ScoreCaspian CompanyPAMotorsMotors GOALCurrent 5-Feb 12-Feb 19-Feb 26-Feb 5-Mar 12-Mar 19-Mar 26-Mar 31-Mar

Units per Person 31.77 30.46 32.51 32.19 33.71 35.2

On-Time Shipment 96.2% 98.2% 98.5% 97.6% 97.2% 98.0%

NA

L

First Time Thru 42% 44% 43% 47% 54% 62%

Dock-to-Dock Days 12.50 11.9 10.94 9.33 8.90 8.0

Average Cost $115.78 $115.78 $114.62 $112.66 $111.74 $107.01

AP days - AR days 8 0 8 0 8 0 8 0 8 0 8 0

OPE

RA

TIO

N

AP days - AR days 8.0 8.0 8.0 8.0 8.0 8.0

Productive 22% 22% 22% 21% 21% 22%

Non-Productive 58% 58% 58% 41% 41% 37%

Available Capacity 20% 20% 20% 38% 38% 41%CA

PAC

ITY

Revenue $366,487 $321,499 $331,546 $325,481 $326,240 $325,000

Material Costs $112,196 $109,812 $113,243 $111,172 $111,431 $111,007

Conversion Costs $92,564 $95,743 $95,233 $99,463 $98,194 $94,039

AN

CIA

L

Inventory $310,622 $295,712 $271,857 $231,848 $221,163 $198,798

Value Stream Profit $161,727 $115,944 $123,070 $114,846 $116,615 $119,953

Value Stream ROS 44.13% 36.06% 37.12% 35.29% 35.75% 36.91%

46.00% Hurdle Rate -1.87% -9.94% -8.88% -10.71% -10.25%

FIN

A

© BMA Inc. 2009. All rights reserved.

46.00% Hurdle Rate 1.87% 9.94% 8.88% 10.71% 10.25%

Value Stream Profit and Loss Account

M t S t S P t

New Product D i

Support C t

TOTAL DIVISION

VALUE STREAMS

Motors Systems Spare Parts Design Costs DIVISION

Sales $326,240 $748,894 $453,215 $1,528,349Additional Revenue $0 $0 $12,422 $12,422

Material Costs $111,431 $232,774 $149,561 $87,909 $12,764 $594,439Conversion Costs $57,628 $70,406 $81,579 $203,769 $37,645 $451,027

Outside Process Costs $32,433 $22,991 $22,661 $7,531 $85,616Other Costs $16 040 $57 816 $29 459 $72 721 $176 036Other Costs $16,040 $57,816 $29,459 $72,721 $176,036

Tooling Costs $4,843 $12,544 $6,588 $23,975

Value Stream Profit $103,865 $352,363 $175,789 ($364,399) ($57,940) $209,678ROS 31.8% 47.1% 38.8% -23.7% -3.8% 13.7%ROS 31.8% 47.1% 38.8% 23.7% 3.8% 13.7%

$925,314$918,807($6,507)

Opening InventoryClosing InventoryInventory Change ($6,507)

$51,147

$152 024

Corporate Overhead

Division Profit

Inventory Change

© BMA Inc. 2009. All rights reserved.

$152,0249.9%Division ROS

Division Profit

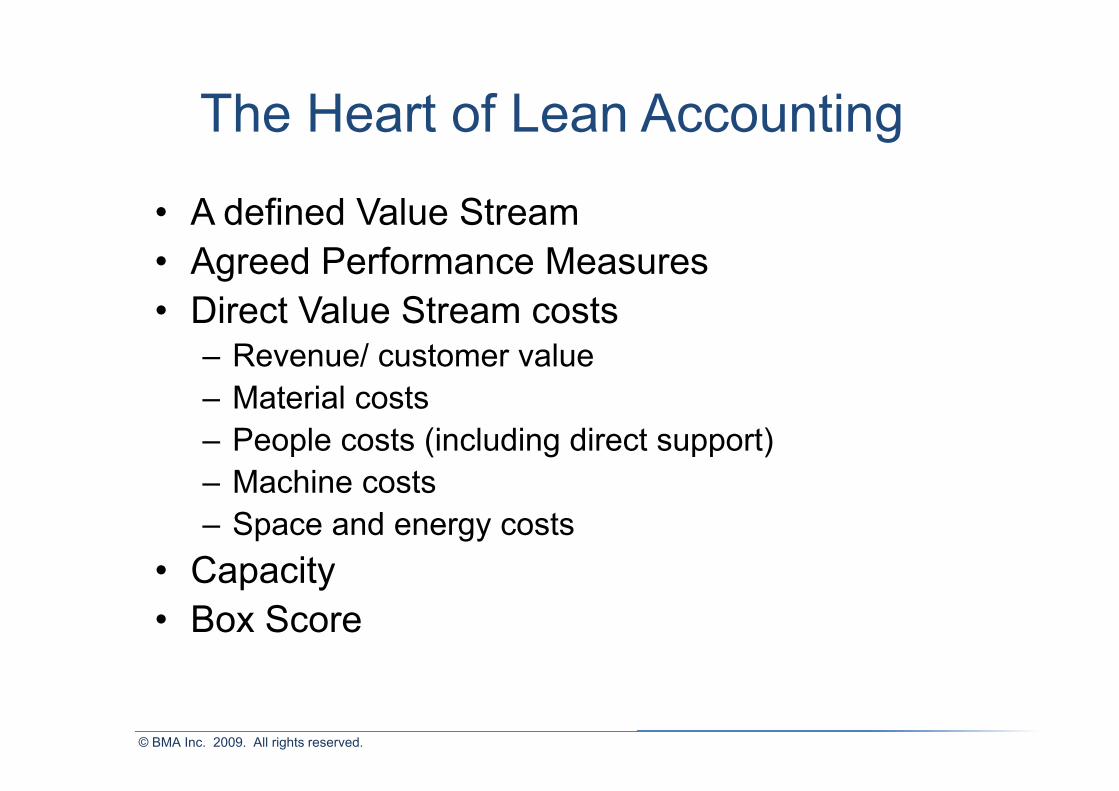

The Heart of Lean AccountingThe Heart of Lean Accounting

• A defined Value Stream• A defined Value Stream• Agreed Performance Measures• Direct Value Stream costs• Direct Value Stream costs

– Revenue/ customer valueMaterial costs– Material costs

– People costs (including direct support)– Machine costs– Machine costs– Space and energy costs

• CapacityCapacity• Box Score

© BMA Inc. 2009. All rights reserved.

The Value Stream

Managing by value streamManaging by value stream

© BMA Inc. 2009. All rights reserved.

What is a value stream?What is a value stream?“All of the actions, both value creating and non-

l ti i dvalue creating, required to bring a product from concept to launch andconcept to launch and from order to cash collection. These includecollection. These include actions to process information from the customer and actions to transform the product on it t th t ”

© BMA Inc. 2009. All rights reserved.

its way to the customer.”

Why do we organize by value stream?

F ti t l• Focus on creating customer value.• Accountability.• Departments can be “optimized” but we need to

optimize the flow through the value stream.• Develop lean thinking managers & specialists.

“As you get the kinks out of your physical production, order-taking, and product d l i ill b b i hdevelopment, it will become obvious that reorganizing by value stream is the best way to sustain your achievement.”

© BMA Inc. 2009. All rights reserved.

Lean Thinking, Womack & Jones

Steps in value stream definitionSteps in value stream definition

1. Identify product families with similar production flow.

2 Identify and minimize

5. Move forward and backwards through the value streams2. Identify and minimize

“monuments”3. Create a production flow

t i

value streams– Value added services– Purchasing and Sales &

Marketingmatrix– Product families on the Y-

axisM hi k t

Marketing– Administrative tasks

– Machines or work centers on the X-axis

4. Make sure the value t l t i l dstreams you select include

significant business.

© BMA Inc. 2009. All rights reserved.

Product process matrixProduct-process matrix

ging

atio

n

ents

ecei

ve c

astin

g/fo

rg

tial I

nspe

ctio

n

the

A

Axe

s 12

ofili

ng

Axe

s 14

eat T

reat

men

t

the

B

the

D

Axe

s 9

PC

e-Po

lish

olis

h

urfa

ce te

stin

g

atin

g

ssiv

atio

n

int

ll Sy

stem

Cal

ibra

alib

ratio

n C

ert

hipp

ing

& In

voic

e

stal

latio

n

n_Si

te C

ert

ocum

ent A

djus

tme

Re

Init

Lat

5 A

Pro

5 A

He

Lat

Lat

5 A

SP

Pre

Po

Su

Pla

Pa

Pa

Fu

Ca

Sh

Ins

On

Do

AA6 X X X X X XAA6-12 X X X X X X X X X X X XAA6-14 X X X X X X X X X X X XAB19 X X X X X X X X X X X X X X X X XAB21 X X X X X X XAB21 X X X X X X XAB21-2 X X X X X X X X X X X XAB33 X X X X X XAB39 X X X X X X XCenter A X X X X X X X X XCenter B X X X X X XCenter F X X X X X X XBi-Center X X X X X X X X X X X XM12-XX X X X X X XM12-Custom X X X X X XM13 X X X X X X X X XM13 Custom X X X X X X XM13-Custom X X X X X X XRes-Active A12 X X X X X X XRes-Acrive A13 X X X X X X X X X X X XRes-Active BB2 X X X X X XRes-Active BB7 X X X X X X XQual-Tite X X X X X X X X X

© BMA Inc. 2009. All rights reserved.

Qual-Tite Custom X X X X X XWilson 99 X X X X X X X X XWilson 101 X X X X X X

Product-process matrixt d f l tsorted for value streams

ng

on

nts

eive

cas

ting/

forg

in

al In

spec

tion

he A

xes

12

filin

g

xes

14

t Tre

atm

ent

he B

he D

xes

9

C Po

lish

sh

face

test

ing

ing

siva

tion

nt Sy

stem

Cal

ibra

tio

brat

ion

Cer

t

ppin

g &

Invo

ice

alla

tion

Site

Cer

t

umen

t Adj

ustm

en

Rec

e

Initi

a

Lat

h

5 A

x

Pro

f

5 A

x

Hea

t

Lat

h

Lat

h

5 A

x

SPC

Pre

-

Pol

is

Sur

f

Pla

ti

Pas

s

Pai

n

Ful

l

Cal

ib

Shi

p

Inst

a

On_

Doc

u

AA6-12 X X X - - - X - - - X X X X - - - - - X X X XAB19 X X X X X X X X X X X - - - X X X X X X - - - AA6-14 X X X X X X X X - - X - - - X - X - - X - - - AB21-2 X X X X X X X X - - X - - - X - X - - X - - - Bi-Center X X X X X X X X - - X - - - X - X - - X - - - Res-Acrive A13 X X X X X X X X - - X - - - X - X - - X - - - Center A X X - X - - X X - - X - - - X - X - - X - - - M13 X X - X - - X X - - X - - - X - X - - X - - - Qual-Tite X X - X - - X X - - X - - - X - X - - X - - - Wilson 99 X X - X - - X X - - X - - - X - X - - X - - -Wilson 99 X X X X X X X X X AB21 X X X - X - X - - - X - - - - - - - - X - - - AB39 X X X - X - X - - - X - - - - - - - - X - - - Center F X X X - X - X - - - X - - - - - - - - X - - - Res-Active A12 X X X - X - X - - - X - - - - - - - - X - - - Res-Active BB7 X X X - X - X - - - X - - - - - - - - X - - -

12 CM12-Custom X X X - X - X - - - - - - - - - - - - X - - - M13-Custom X X X X - - X - - - X - - - - - - - - X - - - AA6 X X X X - - X - - - - - - - - - - - - X - - - AB33 X X X X - - X - - - - - - - - - - - - X - - - Center B X X X X - - X - - - - - - - - - - - - X - - - M12-XX X X X X - - X - - - - - - - - - - - - X - - -

© BMA Inc. 2009. All rights reserved.

Res-Active BB2 X X X X - - X - - - - - - - - - - - - X - - - Qual-Tite Custom X X X X - - X - - - - - - - - - - - - X - - - Wilson 101 X X X X X X

Criteria for value streamsCriteria for value streams• Family of products with similar productionFamily of products with similar production

flow.• Include all the people & processes thatInclude all the people & processes that

support the value stream production process.• The value stream team a reasonable sizeThe value stream team a reasonable size• Minimize monuments

Machine/departments shared by more than one– Machine/departments shared by more than one value stream

• Extend value stream as close to the customerExtend value stream as close to the customer as possible and as close to the suppliers.

© BMA Inc. 2009. All rights reserved.

Here’s a typical value streamHere s a typical value streamTh t i l d d i th M t l t t i• These are steps included in the value stream

– Sales & Marketing*– Customer Service*

• Most value streams contain monuments. Machines or processes that are shared by more than one value stream.– Customer Service

– Purchasing – Materials handling – Parts fabrication

more than one value stream. – Short term: Work around them– Long term: Eliminate monuments

& “right size” the equipmentParts fabrication – Machining – Anodizing – Assembly

• In the early stages of value stream management you may find there

t h l ith th– Shipping – Maintenance – Production engineering

are not enough people with the right skills

– Short term: Have them work in more than one value stream

– Quality assurance – Cost accounting

more than one value stream– Long term: Cross-train people to

do different kinds of tasks.

© BMA Inc. 2009. All rights reserved.

There are some people or departments outside the value streams

Examples:– Plant or division manager– Financial accounting– Human resources– Information systems– Facilities management

© BMA Inc. 2009. All rights reserved.