an introduction to: schroder isf* us small & mid (smid ... · schroder isf us small & mid...

TRANSCRIPT

An Introduction to:Schroder ISF* US Small & Mid (SMID) Cap Equity November 2006

For Professional Investors Only

Representing Schroders:

Jenny Jones – Executive Vice President and Portfolio Manager

John Harrington, CFA – Senior Vice President and Product Manager

*Schroder International Selection Fund is referred to as Schroder ISF throughout this presentation.

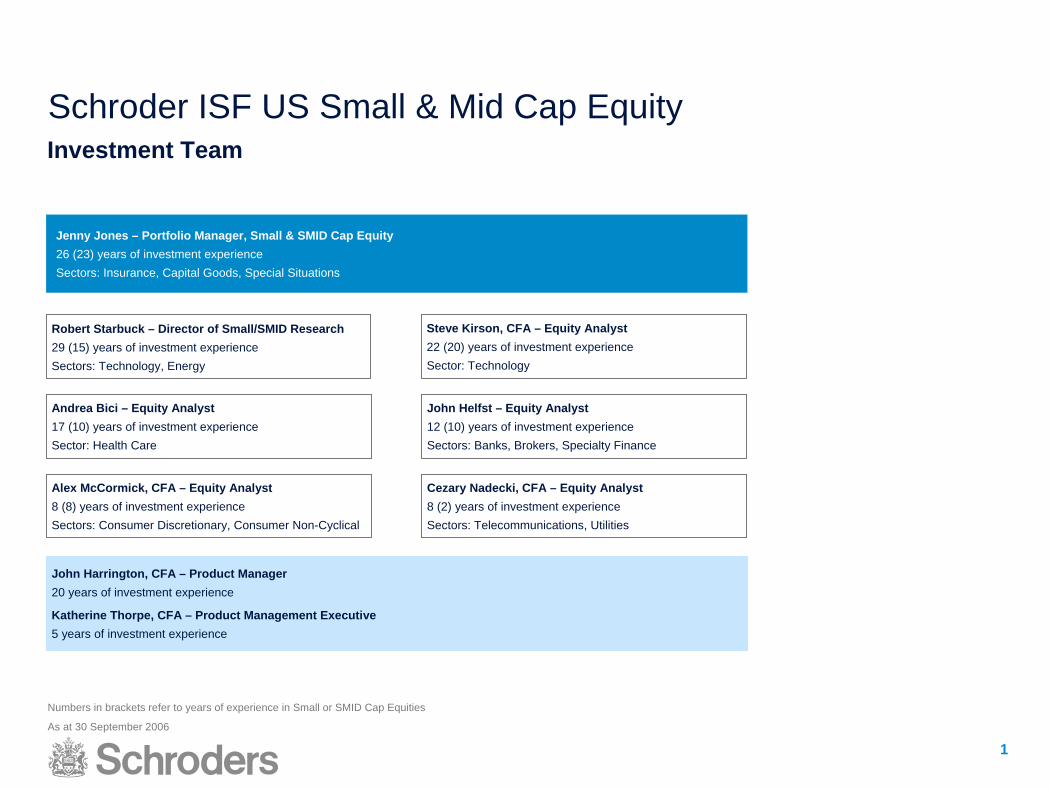

Schroder ISF US Small & Mid Cap EquityInvestment Team

Jenny Jones – Portfolio Manager, Small & SMID Cap Equity26 (23) years of investment experienceSectors: Insurance, Capital Goods, Special Situations

Steve Kirson, CFA – Equity Analyst22 (20) years of investment experienceSector: Technology

Robert Starbuck – Director of Small/SMID Research29 (15) years of investment experienceSectors: Technology, Energy

Andrea Bici – Equity Analyst17 (10) years of investment experienceSector: Health Care

John Helfst – Equity Analyst12 (10) years of investment experienceSectors: Banks, Brokers, Specialty Finance

Alex McCormick, CFA – Equity Analyst8 (8) years of investment experienceSectors: Consumer Discretionary, Consumer Non-Cyclical

Cezary Nadecki, CFA – Equity Analyst8 (2) years of investment experienceSectors: Telecommunications, Utilities

John Harrington, CFA – Product Manager20 years of investment experience

Katherine Thorpe, CFA – Product Management Executive5 years of investment experience

Numbers in brackets refer to years of experience in Small or SMID Cap Equities

As at 30 September 2006

1

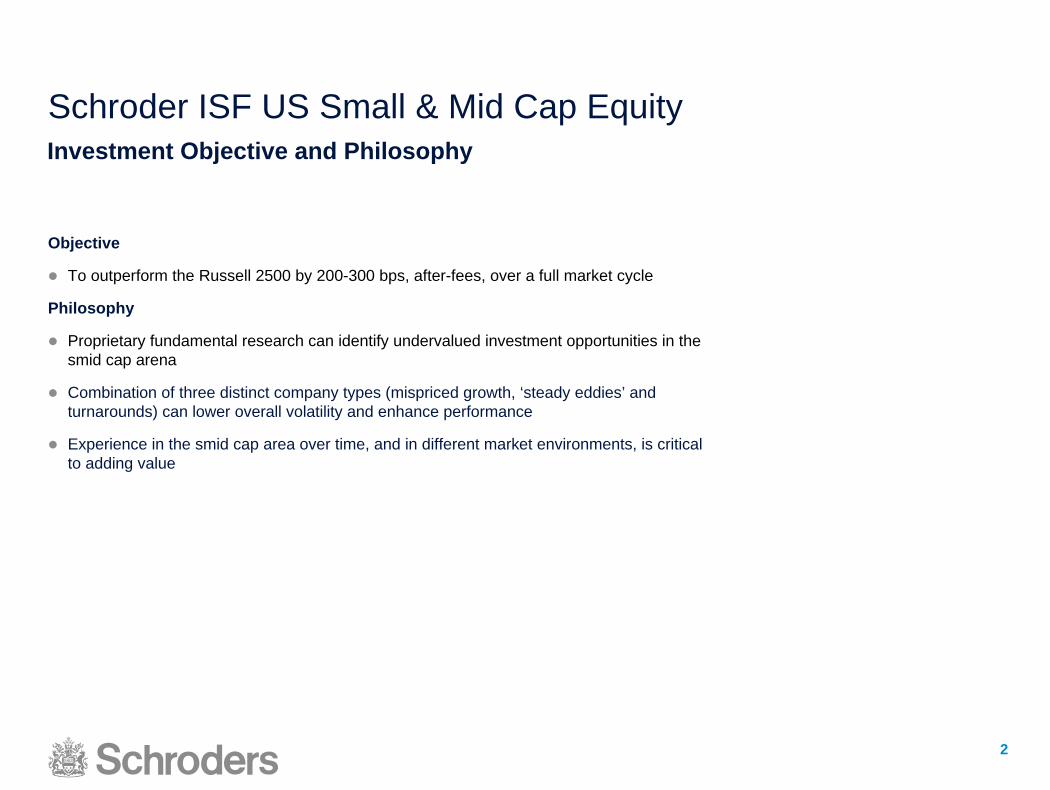

Schroder ISF US Small & Mid Cap EquityInvestment Objective and Philosophy

Objective

To outperform the Russell 2500 by 200-300 bps, after-fees, over a full market cycle

Philosophy

Proprietary fundamental research can identify undervalued investment opportunities in the smid cap arena

Combination of three distinct company types (mispriced growth, ‘steady eddies’ and turnarounds) can lower overall volatility and enhance performance

Experience in the smid cap area over time, and in different market environments, is critical to adding value

2

Schroder ISF US Small & Mid Cap Equity

200names

600 names

1,200 names

Investment Process

3

55-75 Stocks

SISF US Small & Mid Cap

Equity

Fine Tuning The List

Reducing The List

The Universe

Stocks with Market capitalizationUS$1bil –US$7 bil

Compelling financial metrics

Screenedresults

Turnaround candidates

Portfolio consideration

Liquidity profile

Valuation

Cross fertilization from small cap

Internal team meetings

Sell-side boutiques

Company managements

Input from competitors

Liquidity profile

HOLT screens

Superior businessmodels

Portfolio manager conviction

Company meetings

Conferences

Reasonable valuation

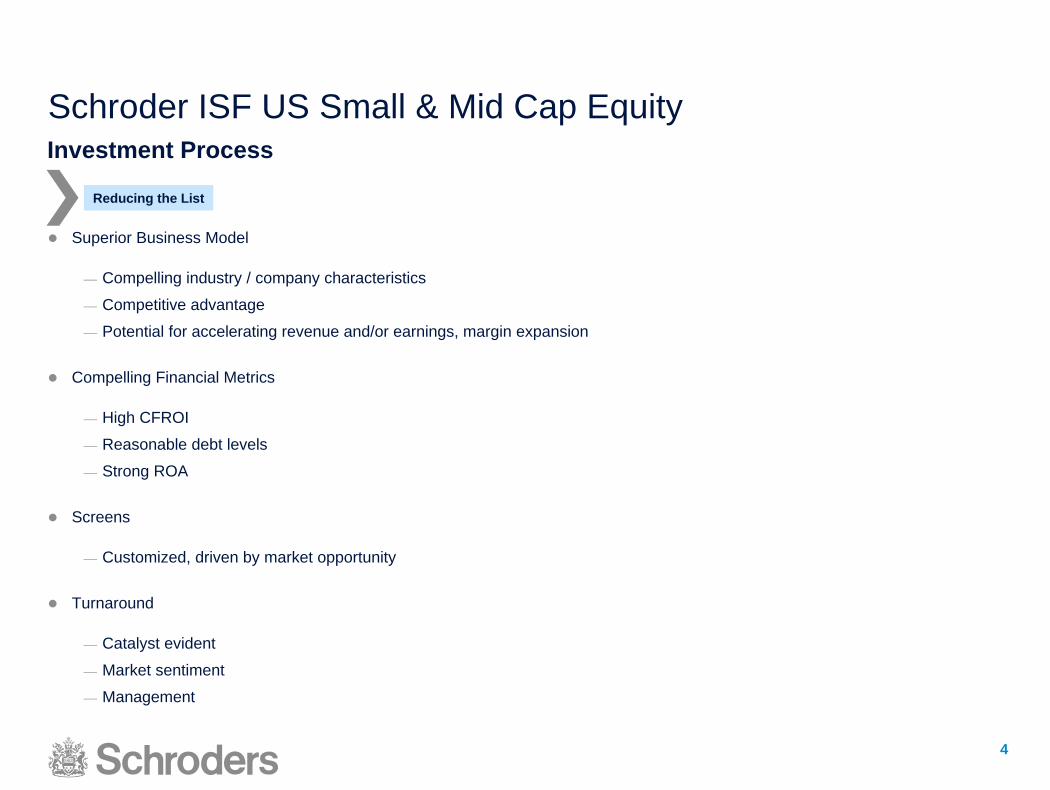

Schroder ISF US Small & Mid Cap EquityInvestment Process

Superior Business Model

— Compelling industry / company characteristics

— Competitive advantage

— Potential for accelerating revenue and/or earnings, margin expansion

Compelling Financial Metrics

— High CFROI

— Reasonable debt levels

— Strong ROA

Screens

— Customized, driven by market opportunity

Turnaround

— Catalyst evident

— Market sentiment

— Management

Reducing the List

4

Schroder ISF US Small & Mid Cap EquityInvestment Process

Fine tuning the list

Valuation

— P/E

— P/FCF

— EV/EBIT

— Discount to expected earnings growth (PEG)

Conviction /Judgment

— Upside/downside expectation

— Confidence in management

Portfolio Consideration

— Liquidity

— Exposure to industry

5

Schroder ISF US Small & Mid Cap EquityInvestment Process – Three Distinct Company Types

Mispriced Growth (50-60% of portfolio)

Companies that are exhibiting solid top and bottom line growth. Top line should be growing at 10%+, and bottom line at 15%+

Product or service that is at early stage of life cycle and end market demand is strong

Strong, talented management team

Balance sheet strength and improving cash flows

Steady Eddies (20-40% of portfolio)

A predictable, high quality company, with consistent results and low variability in revenue/earnings

Bottom line most likely growing at 8-12%

Strong free cash flow, strong balance sheet, consistently meets earnings estimates

Valuation may be higher than ‘mispriced growth’ stocks, due to consistency and lower risk

Turnarounds (5-20% of portfolio)

Out-of-favour in the market

Significant accounting or management issue

Restructuring

6

Schroder ISF US Small & Mid Cap EquityPortfolio Construction

Cash target 5% or less

Position size limited to 5%

Top ten positions >20%

Sector weights within 1000 basis points of benchmark weight

7

Schroder ISF US Small & Mid Cap EquitySell discipline

Three primary reasons that we sell a stock:

Reaches 90% of price target

Better idea

Negative change in fundamentals

8

Schroder ISF US Small & Mid Cap EquityTop Ten Holdings – 30 September 2006

Company Description % of Fund

VeriSign Inc. Provider of intelligent infrastructure services 3.0

Invitrogen Corp. Develops research tools for the life sciences industry 2.5

Scientific Games Corp. Lottery systems and services 2.4

Constellation Brands Inc. International producer and marketer of alcoholic beverages 2.2

Dresser-Rand Manufacturer of equipment for the oil and gas industries 2.1

Dover Corp. Manufacturers specialized industrial products and manufacturing equipment 2.0

Tektronix Inc. Supplier of monitoring products and solutions to technology companies 2.0

Thermo Electron Corp. Provider of analytical equipment for life science and environmental laboratories 1.9

Watson Wyatt Worldwide Inc. Global human capital consulting firm 1.9

Medicis Pharmaceutical Specialty pharmaceutical company focusing on dermatology products 1.9

Total 21.9

Source: Factset

9

Schroder ISF US Small & Mid Cap EquitySector Weights – 30 September 2006

%Portfolio vs Index

13.4

2.3 2.03.4

13.4

10.3

16.1

7.06.1

16.418.3

6.5

11.1

25.0

3.6

6.2

2.3

5.0

12.4

9.4

0

5

10

15

20

25

Health Care Technology Energy Materials ConsumerStaples

ProducerDurables

Autos &Transportation

Utilities ConsumerDiscretionary

FinancialServices

Schroder ISF US SMID Cap Equity Russell 2500

Source: Factset.

10

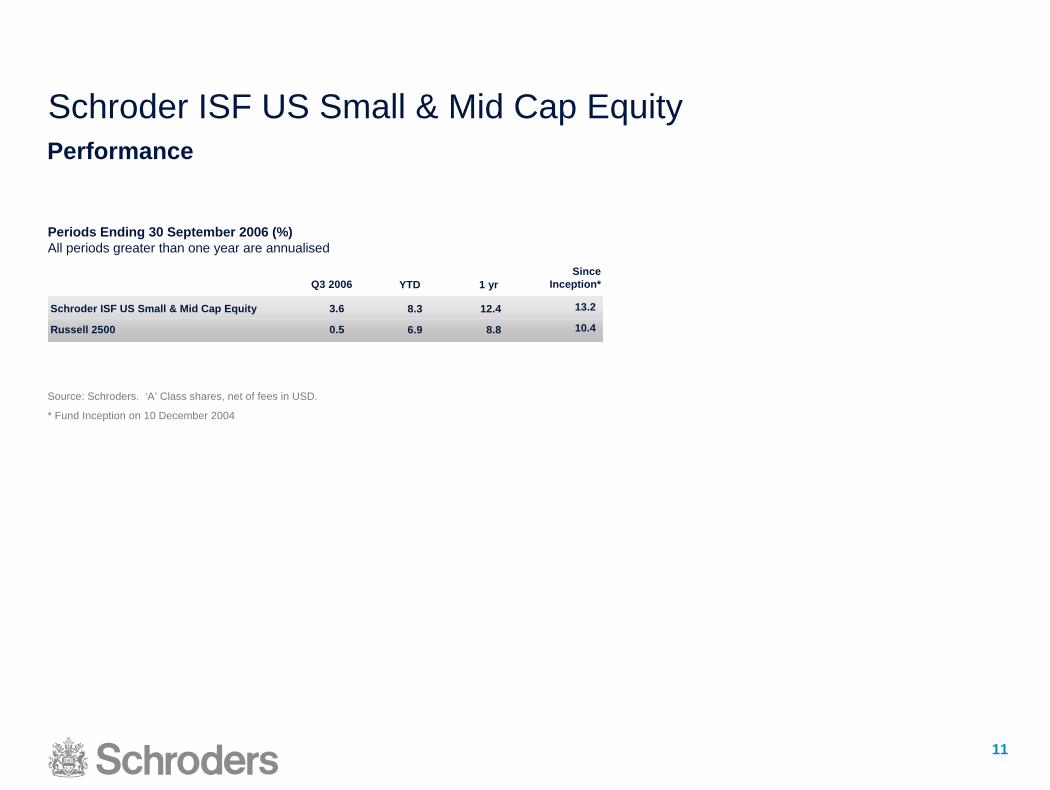

Schroder ISF US Small & Mid Cap EquityPerformance

Periods Ending 30 September 2006 (%)All periods greater than one year are annualised

Schroder ISF US Small & Mid Cap Equity

Russell 2500

Q3 2006

3.6

0.5

Since Inception*

13.2

10.4

YTD

8.3

6.9

1 yr

12.4

8.8

Source: Schroders. ‘A’ Class shares, net of fees in USD.

* Fund Inception on 10 December 2004

11

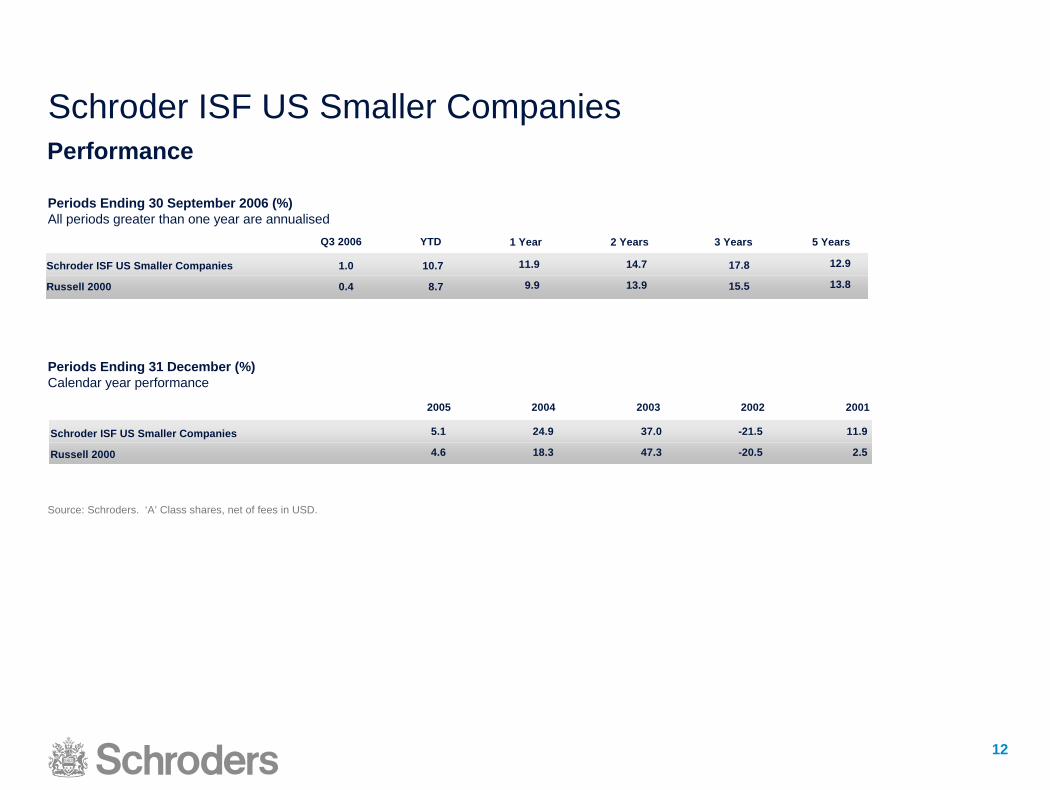

Schroder ISF US Smaller CompaniesPerformance

Periods Ending 30 September 2006 (%)All periods greater than one year are annualised

Schroder ISF US Smaller Companies

Russell 2000

YTD

10.7

8.7

1 Year

11.9

9.9

3 Years 5 Years2 Years

14.7

13.9

17.8

15.5

12.9

13.8

Q3 2006

1.0

0.4

Schroder ISF US Smaller Companies

Russell 2000

2005

5.1

4.6

2004

24.9

18.3

2003

37.0

47.3

2002

-21.5

-20.5

2001

11.9

2.5

Periods Ending 31 December (%)Calendar year performance

Source: Schroders. ‘A’ Class shares, net of fees in USD.

12

US Small Cap Performance relative to US competitors

Small Capitalization Accounts 3 Years Ending June 30, 2006

Annualized Return %

10.00

15.00

20.00

25.00

30.00

35.00

40.00

5.00 15.00 20.00 25.00

5.00

45.00

10.00

Annualized Standard Deviation

SIMNA Small Cap Core Russell 2000

Source: Callan Associates Inc.

13

US Small Cap Performance relative to US competitors

3 Years Ending June 30, 2006 Group: CAI Small Capitalization Style

0.0

25.0

50.0

75.0

100.0

125.0

150.0

175.0

SIM NA : USSmall Cap Co re

Russell 2000Index

Down Market Capture Up Market Capture

Down Market Capture

10th Percentile25th PercentileMedian75th Percentile90th Percentile

Member Count

SIMNA:US Small Cap CoreRussell 2000 Index A

158.94118.73

74.9146.7625.13

124

38.30100.00

B

Up Market Capture

118.95109.08

97.5991.0278.56

124

104.22100.00

A (38) A (41)

B (83)

B (32)

Statistics relative to Russell 2000

Source: Callan Associates Inc.

14

Schroder ISF US Small & Mid Cap EquitySummary

Highly experienced investment professionals

Successful Small Cap product

Core investment approach based on fundamental analysis of individual stocks

15

Appendix

16

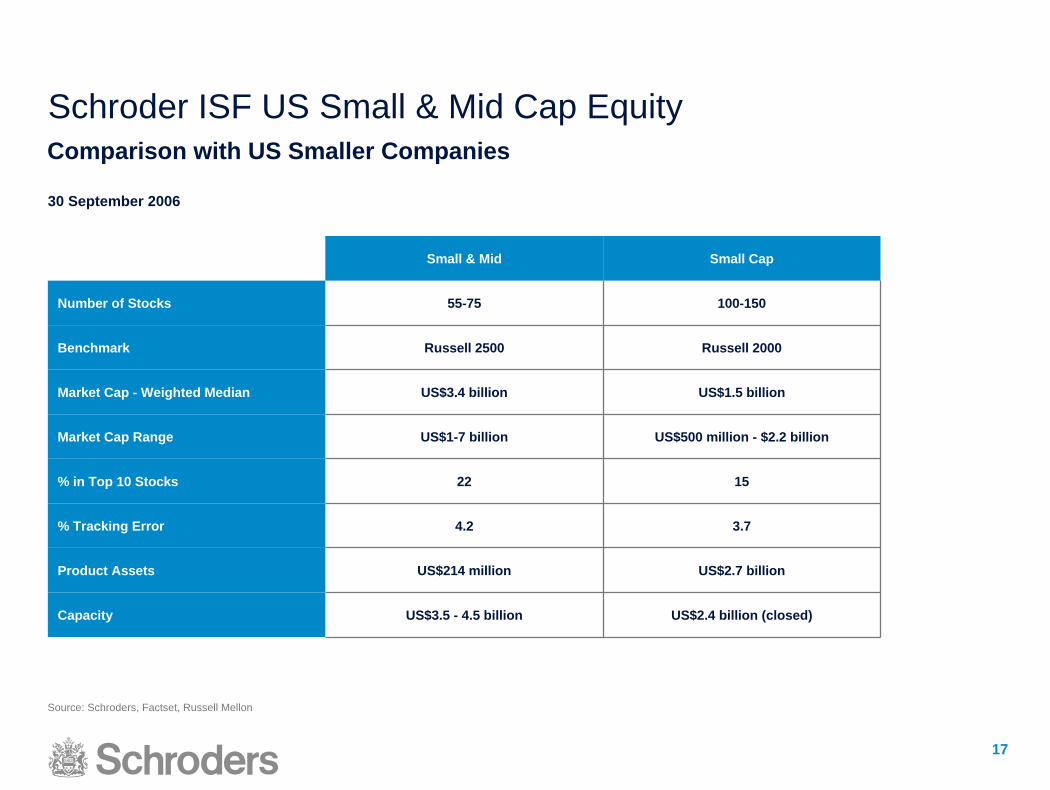

Schroder ISF US Small & Mid Cap EquityComparison with US Smaller Companies

30 September 2006

Small & Mid Small Cap

Number of Stocks 55-75 100-150

Benchmark Russell 2500 Russell 2000

Market Cap - Weighted Median US$3.4 billion US$1.5 billion

Market Cap Range US$1-7 billion US$500 million - $2.2 billion

% in Top 10 Stocks 22 15

% Tracking Error 4.2 3.7

Product Assets US$214 million US$2.7 billion

Capacity US$3.5 - 4.5 billion US$2.4 billion (closed)

Source: Schroders, Factset, Russell Mellon

17

The Case for SMID Cap Equity

18

US Small & Mid Cap EquityUS Equity Market Capitalisation Segments as of 30 September 2006

Number of Companies5% 1%

76%

13%

5%

Mid/Large (over $7bil)

Mid (SMID) ($2bil-$7bil)

Small (SMID) ($1bil-$2bil)

Small ($0.2bil-$1bil)

Micro (below $0.2bil)

450

700

650

1,800

6,750

Source: Factset

19

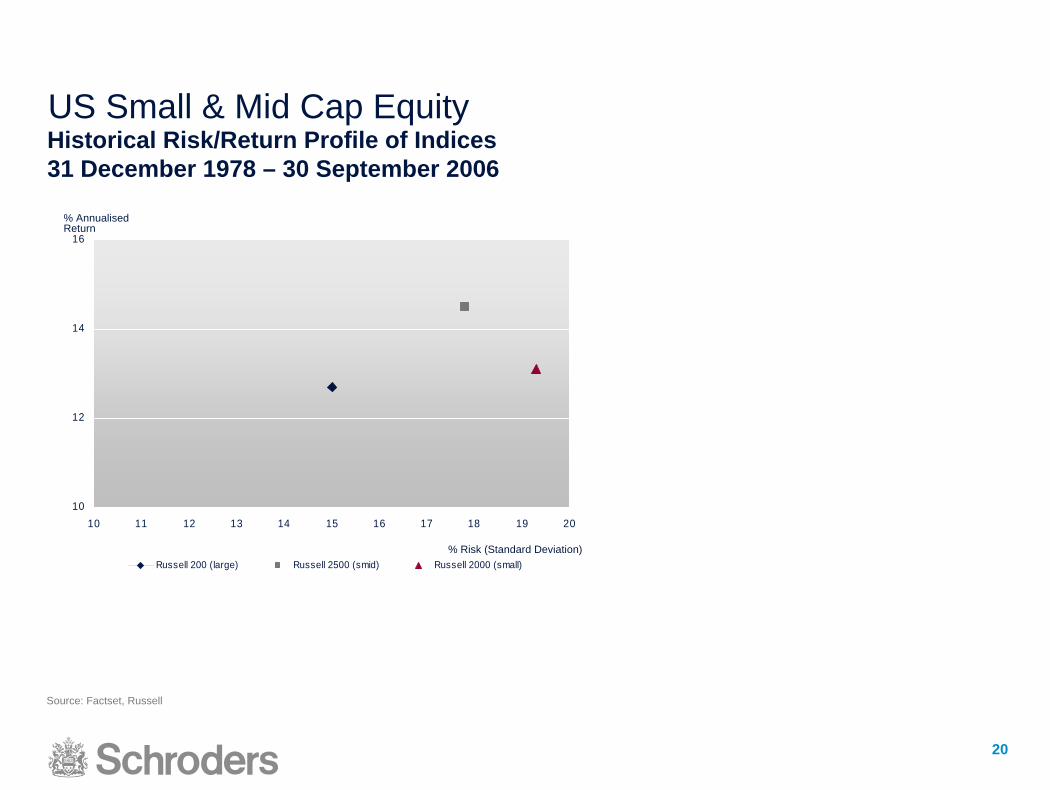

Historical Risk/Return Profile of Indices31 December 1978 – 30 September 2006

US Small & Mid Cap Equity

10

12

14

16

10 11 12 13 14 15 16 17 18 19 20

Russell 200 (large) Russell 2500 (smid) Russell 2000 (small)

% Annualised Return

% Risk (Standard Deviation)

Source: Factset, Russell

20

US Small & Mid Cap EquityCompany/Stock Attributes by Market Cap Segment

Market Cap Range Ownership Cost of Capital

Earnings Volatility Liquidity Volatility Analyst

Coverage Historical Returns

Less than US$2 billion Higher insider ownership High

Moderate

Low High

Low

+200 bps > Large

US$2 - $7 billion

Significant insider ownership, but growing, institutional shareholder base

2-6High

Lower 5-10

Lowest >15

Moderate Moderate +200 bps > Large

>US$7 billionMinimal insider ownership, mostly institutional shareholder base

High Lowest Large

Source: Schroders, Factset

21

Schroder ISF US Small & Mid Cap EquityPerformance Notes

This presentation does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of Schroder International Selection Fund (the “Company”). Nothing in this document should be construed as advice and is therefore not a recommendation to buy or sell shares.

Subscriptions for shares of the Company can only be made on the basis of its latest prospectus together with the latest audited annual report (and subsequent unaudited semi-annual report, if published), copies of which can be obtained, free of charge, from Schroder Investment Management (Luxembourg) S.A.

In accordance with the current prospectus, other than for the Schroder ISF Global Property Securities fund, the Company will seek UK distributor status for all distribution A and C shares.

An investment in the Company entails risks, which are fully described in the prospectus.

Past performance is not a guide to future performance and may not be repeated. Investors may not get back the full amount invested, as prices of shares and the income from them may fall as well as rise.

Exchange rate changes may cause the value of any overseas investments to rise or fall.Schroders has expressed its own views and opinions in this document and these may change.

Schroder ISF US Small & Mid Cap Equity is not within the scope of the European Union Directive 2003/48/EC (Taxation of Savings Income in the Form of Interest Payments), as implemented in Luxembourg Law.

This document is issued by Schroder Investment Management (Luxembourg) S.A., 5, rue Höhenhof, L-1736 Senningerberg, Luxembourg.

For your security, all telephone calls are recorded.

22