an introduction to trusts presentation to step hungary 2013 conference budapest 11 june 2013 step...

TRANSCRIPT

An Introduction to Trusts

Presentation toSTEP Hungary

2013 ConferenceBudapest

11 June 2013

Ian Watson, TEPBarrister and New York Attorney

STEP Cross-Border Estates GroupSTEP Cross-Border Estates Group

3 Stone Buildings, Lincoln's Inn, London WC2A 3XL, Englandtel: +44 (20) 7242 4937 fax: +44 (20) 7405 389610 Rockefeller Plaza, 16th floor, New York, NY 10020-1903, USAtel: +1 (212) 713 7680, fax: +1 (212) 713 7679

www.3stonebuildings.com

Overview1. Welcome to STEP – a few words about C-

BEG

2. What is a Trust?

3. Why Use a Trust?

4. Are Trusts Secret?

5. Trusts and Tax

6. International Trends in Trusts

7. The Future

1. STEP and C-BEG

The Society of Trust and Estate Practitioners

Cross-Border Estates Group

2. What is a Trust?

No single law of trusts – different rules in England, Scotland, Ireland, each

of the United States, former British colonies in the Caribbean, Canada,

Australia, Hong Kong, Singapore, the Channel Islands, etc.

A structure to provide for family, continuing ownership and management

of assets and succession

Also business and commercial uses

Not a separate legal entity, rather a relationship among a Settlor, one or

more Trustees and one or more Beneficiaries

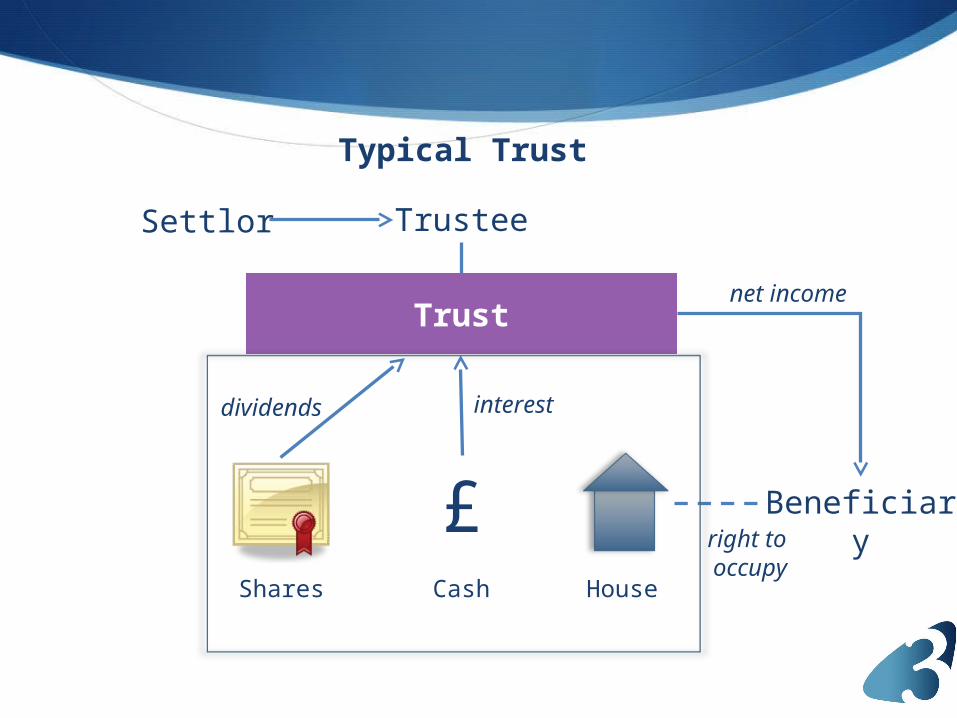

Typical Trust

Settlor Trustee

Trust

£ Beneficiary

Shares Cash House

interestdividends

net income

right to occupy

Traditional Features of a Trust

Legal ownership by Trustee

Trustee has fiduciary duty to act only in the interest of the Beneficiaries

Trustee may only invest in specified types of conservative assets

Trustee may have wide discretion to decide amounts distributed

Successive or overlapping beneficial interests (e.g., life interests v.

remainders)

Restrictions on Beneficiary’s right to alienate interest

Limited duration – the Rule Against Perpetuities

Rule Against Perpetuities

“An interest must vest or fail to vest within lives in being at the time it is

created plus 21 years”

Notoriously difficult to apply – and harsh result

Modified or abolished in many jurisdictions:

Fixed term: e.g., 80/90/100/150 years, etc., or

Unlimited duration

Limit generally did not apply to trusts with only charitable purposes

3. Why Use a Trust?

A variety of personal and commercial uses

Flexibility and administrative convenience

Pension Trust

Employer (Settlor)

Trustee

Pension Fund (Trust)

£Retired

Employees (Beneficiaries)

Shares Cash

interestdividends

income

Charitable Trust

Donors (Settlors)

Trustee

Trust

£Shares Cash

interestdividends

income

Charitable Causes

(Beneficiaries)

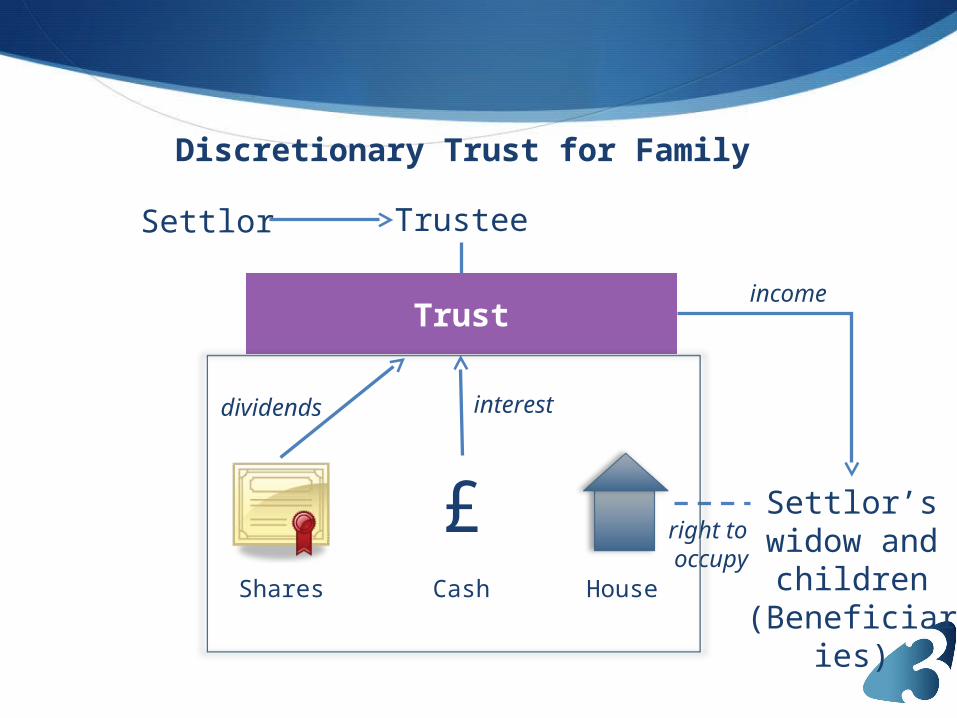

Discretionary Trust for Family

Settlor Trustee

Trust

£ Settlor’s widow and children

(Beneficiaries)Shares Cash House

interestdividends

income

right to occupy

Life Interest Trust for Spouse

Settlor Trustee

Trust

£

Settlor’s widow (Income

Beneficiary)

Shares Cash House

interestdividends

net income

right to occupy

Settlor’s children (Remainder Beneficiaries)

death of widow

capital

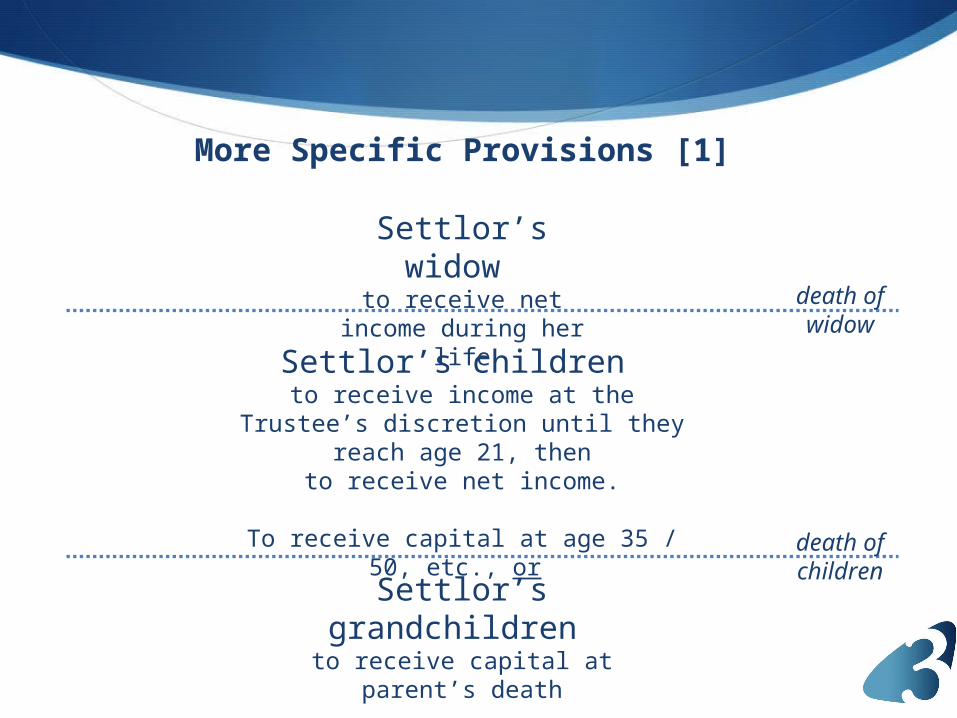

More Specific Provisions [1]

Settlor’s widow to receive net income

during her life

Settlor’s children to receive income at the Trustee’s

discretion until they reach age 21, thento receive net income.

To receive capital at age 35 / 50, etc., or

death of widow

death of children

Settlor’s grandchildren to receive capital at parent’s death

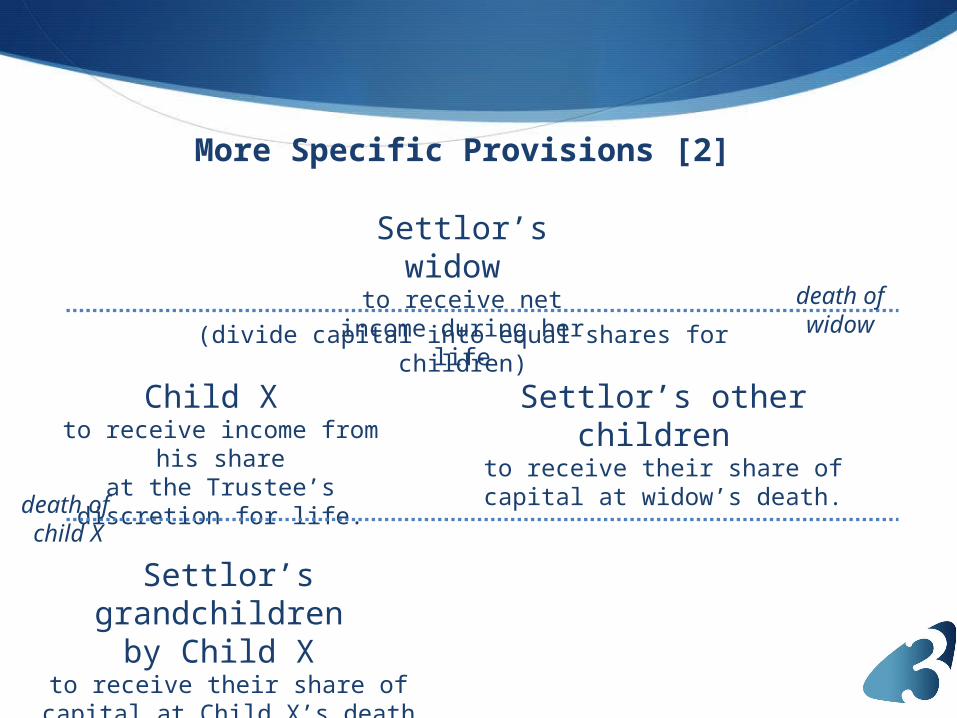

More Specific Provisions [2]

Settlor’s widow to receive net income

during her life

Child X to receive income from his shareat the Trustee’s discretion for life.

death of widow

death of child X

Settlor’s grandchildren by Child X

to receive their share of capital at Child X’s death

Settlor’s other children to receive their share of capital at

widow’s death.

(divide capital into equal shares for children)

Additional Discretion

Trustee or a Beneficiary may be allowed to deviate from default terms to

meet unexpected situations

Trustee’s overriding power of appointment

Beneficiary’s power of appointment

4. Are Trusts Secret?

Confidential, but not secret

Creation or existence of a trust may need to be disclosed (particularly if

“off-shore”)

Generally, details can be kept private (but wills may be in public record)

“[T]he obligation to keep taxpayer information confidential and only

release it in accordance with the law is a fundamental principle.”

(Engaging with High Net Worth Individuals on Tax Compliance, OECD, May

2009, p. 53).

5. Trusts and Tax

Not a vehicle for avoidance and hiding from tax authorities

Extensive disclosure requirements and tax costs for “offshore”

arrangements

Many different tax systems, but a general principle is to try to make trusts

“tax neutral” – i.e., taxed the same as if there were no trust

Some tax advantages may remain, depending on context and jurisdiction

Discretionary Trust for Family

Settlor Trustee

Trust

£ Settlor’s widow and children

(Beneficiaries)Shares Cash House

interestdividends

income

right to occupy

Typical UK Will Trusts

Nil Rate BandDiscretionary Trust

£325,000

Life interest TrustFor Spouse

Balance of estate

Death of spouse

Trust(s) for children,then grandchildren

Inheritance tax paid on death of spouse

Discretionary Trust for Family

Settlor Trustee

Trust

£ Settlor’s widow and children

(Beneficiaries)Shares Cash House

interestdividends

income

right to occupy

6. International Trends in Trusts The Hague Trusts Convention XXX of 1st July 1985

In force: Australia Canada (other than Ontario & Quebec) Italy Liechtenstein Luxembourg Malta Monaco The Netherlands San Marino Switzerland United Kingdom

Not yet in force: China Cyprus France United States

7. The Future

Growing popularity

Increased international recognition

Unpredictable changes in tax laws

For more information please contact:

Ian Watson, TEP3 Stone BuildingsLincoln’s InnLondon WC2A 3XLEnglandTel: +44 (20) 7242 4937Email: [email protected] 317 Chancery Lane

3 Stone Buildings, Lincoln's Inn, London WC2A 3XL, Englandtel: +44 (20) 7242 4937 fax: +44 (20) 7405 389610 Rockefeller Plaza, 16th floor, New York. NY 10020-1903, USAtel: +1 (212 ) 713 7680, fax: +1 (212) 713 7679

3stonebuildings.com