an overview of the financial system. characteristics of a good financial system diversifies risk...

TRANSCRIPT

An Overview of the An Overview of the Financial SystemFinancial System

Characteristics of a Good Financial SystemCharacteristics of a Good Financial System

Diversifies RiskDiversifies Risk

Defining RiskDefining Risk

In a world with no uncertainty, we could In a world with no uncertainty, we could make the following statement:make the following statement:

““Tomorrow, the temperature will be 35 Tomorrow, the temperature will be 35 degrees”degrees”

In an uncertain worlds, we can’t state In an uncertain worlds, we can’t state anything with certainty, only with degrees anything with certainty, only with degrees of probability.of probability.

““There is a 45% chance that it will be 35 There is a 45% chance that it will be 35 degrees tomorrow”degrees tomorrow”

Probability DistributionsProbability Distributions More generally, uncertainty is More generally, uncertainty is

characterized by a probability characterized by a probability distributiondistribution

Expected value (mu) refers to Expected value (mu) refers to the most likely event. the most likely event.

Standard Deviation (sigma) Standard Deviation (sigma) refers to the “spread” of refers to the “spread” of possible events. It is equal to possible events. It is equal to the expected value of squared the expected value of squared differences from the mean.differences from the mean.

StatisticsStatistics

Expected value is equal to the sum of each possible Expected value is equal to the sum of each possible event multiplied by its probability.event multiplied by its probability.

Prob(35) = .45 Prob(25) = .55Prob(35) = .45 Prob(25) = .55

E(Temperature) = .45(35) + .55(25) = 29.5E(Temperature) = .45(35) + .55(25) = 29.5

Variance is equal to the expected value of squared Variance is equal to the expected value of squared differences from the mean.differences from the mean.

Variance (Temp) = .45(35 – 29.5)^2 + .55(25-29.5)^2Variance (Temp) = .45(35 – 29.5)^2 + .55(25-29.5)^2

= 24.75= 24.75

Standard Dev. (Temp) = SQRT(24.75) = 4.97Standard Dev. (Temp) = SQRT(24.75) = 4.97

DiversificationDiversification

Suppose the chance of a cold winter is 40% (the chance Suppose the chance of a cold winter is 40% (the chance of a warm winter is 60%). You own an oil company. In a of a warm winter is 60%). You own an oil company. In a cold winter, you earn $100 in profit. In a warm winter, cold winter, you earn $100 in profit. In a warm winter, you lose $50.you lose $50.

E(Profit) = .40($100) + .60(-$50) = $10E(Profit) = .40($100) + .60(-$50) = $10

Variance (Profit) = .4(100-10)^2 + .6(-50 –10)^2 = 5,400Variance (Profit) = .4(100-10)^2 + .6(-50 –10)^2 = 5,400

Standard Deviation = 73.5Standard Deviation = 73.5

DiversificationDiversification Now, suppose you buy stock in Disney. If its warm, your Now, suppose you buy stock in Disney. If its warm, your

stock appreciates by $20. If its cold, Disney stock falls by stock appreciates by $20. If its cold, Disney stock falls by $10. You pay $15 for the stock.$10. You pay $15 for the stock.

E(Profit) = .4($100 - $10 - $15) + .6(-$50 + $20 - $15) = $3E(Profit) = .4($100 - $10 - $15) + .6(-$50 + $20 - $15) = $3Variance (Profit) = .4(75 - 3)^2 + .6(-45 - 3)^2 = 3,455Variance (Profit) = .4(75 - 3)^2 + .6(-45 - 3)^2 = 3,455Standard Deviation = 58.8Standard Deviation = 58.8

You’ve lowered your risk by 20%You’ve lowered your risk by 20%(At a cost of $7)(At a cost of $7)

Diversification & CorrelationDiversification & Correlation

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

Sta

nd

ard

Devia

tio

n

1 2 3 4 5 6 7

# of variables

Adding uncorrelated (Corr = 0) variables to a Adding uncorrelated (Corr = 0) variables to a portfolio lowers the risk attached to that portfolioportfolio lowers the risk attached to that portfolio

Diversification & CorrelationDiversification & Correlation

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.5 0 -0.5

Correlation (three variables)

Std. Dev.

Negative correlations (Corr < 0) enhance the Negative correlations (Corr < 0) enhance the power of diversificationpower of diversification

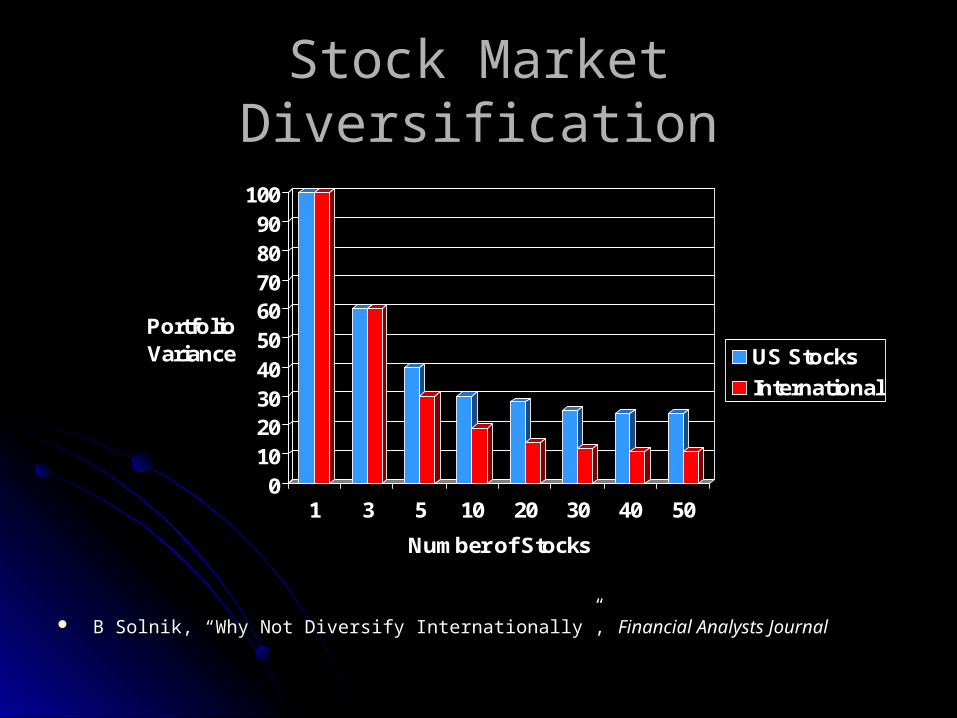

Stock Market DiversificationStock Market Diversification

0102030405060708090

100

Portfolio Variance

1 3 5 10 20 30 40 50

Number of Stocks

US Stocks

International

B Solnik, “Why Not Diversify Internationally”, B Solnik, “Why Not Diversify Internationally”, Financial Analysts Journal

Characteristics of a Good Financial SystemCharacteristics of a Good Financial System

Diversifies RiskDiversifies RiskCreates LiquidityCreates Liquidity

Enron: Sinner or Saint?Enron: Sinner or Saint?

In Dec. December In Dec. December 2001, Enron declared 2001, Enron declared bankruptcy – one of bankruptcy – one of the largest corporate the largest corporate failures in history. failures in history.

While Enron did a lot While Enron did a lot of things wrong, what of things wrong, what did it do right?did it do right?

Enron: Sinner or Saint?Enron: Sinner or Saint?

Enron’s core business Enron’s core business was to become the was to become the “middleman” in “middleman” in energy markets – this energy markets – this helped manage risk helped manage risk and improved and improved liquidity.liquidity.

Characteristics of a Good Financial SystemCharacteristics of a Good Financial System

Diversifies RiskDiversifies RiskCreates LiquidityCreates LiquidityProvides/Communicates InformationProvides/Communicates Information

Asymmetric InformationAsymmetric Information

Adverse SelectionAdverse SelectionPrior to a transaction taking place, one party Prior to a transaction taking place, one party

is missing vital information about the other is missing vital information about the other party (can’t tell the good eggs from the bad party (can’t tell the good eggs from the bad eggs!)eggs!)

Moral HazardMoral HazardAfter the transaction takes place, one party After the transaction takes place, one party

can’t observe the other’s actions (the good can’t observe the other’s actions (the good eggs might become bad eggs!)eggs might become bad eggs!)

An Adverse Selection ExampleAn Adverse Selection Example

Suppose you are shopping for a new car. There are 10 Suppose you are shopping for a new car. There are 10 cars on the lot.cars on the lot. 8 Cars are good (P = $1000)8 Cars are good (P = $1000) 2 Cars are Lemons (P = $100)2 Cars are Lemons (P = $100)

What price do you offer? (You can’t distinguish lemons What price do you offer? (You can’t distinguish lemons from good cars)from good cars)

Solution: Signaling or Regulation!Solution: Signaling or Regulation!

A Moral Hazard ExampleA Moral Hazard Example

Suppose a company has one bondholder ($100) Suppose a company has one bondholder ($100) and one stockholder. The company has two and one stockholder. The company has two possible projects to invest in: possible projects to invest in:

Project A: $100 profit with certaintyProject A: $100 profit with certainty Project B: 50% chance of $0 profit, 50% chance of Project B: 50% chance of $0 profit, 50% chance of

$200 profit.$200 profit.

Which project should the company invest in?Which project should the company invest in?

A Moral Hazard ExampleA Moral Hazard Example

Project A (Safe)Project A (Safe)Bondholders: $100Bondholders: $100

Stockholders: $0Stockholders: $0

With certaintyWith certainty

Project B (Risky)Project B (Risky)Bondholders: Bondholders: 50% chance of $0, 50% 50% chance of $0, 50%

chance of $100chance of $100E(B) = .5(100) + .5(0) =$50E(B) = .5(100) + .5(0) =$50

Stockholders: Stockholders: 50% chance of $050% chance of $0 50% chance of $10050% chance of $100

E(S) = (.5)(100) + .5(0) =$50E(S) = (.5)(100) + .5(0) =$50

A Moral Hazard ExampleA Moral Hazard Example

As a bondholder, you can’t always As a bondholder, you can’t always observe the stockholder actions, but you observe the stockholder actions, but you would prefer the stockholder to only take would prefer the stockholder to only take on low risk projects. on low risk projects.

How do you do this?”How do you do this?”MonitoringMonitoringOptimal ContractingOptimal Contracting

Why Do We Care?Why Do We Care?

With a financial system, your consumption With a financial system, your consumption expenditures are no longer restricted to equal expenditures are no longer restricted to equal your income (i.e., the financial system efficiently your income (i.e., the financial system efficiently transfers income between households)transfers income between households)

Financial Markets Transfer Savings from Financial Markets Transfer Savings from households to firms for the purpose of financing households to firms for the purpose of financing investment projectsinvestment projects

S = I + (G-T) + NXS = I + (G-T) + NX

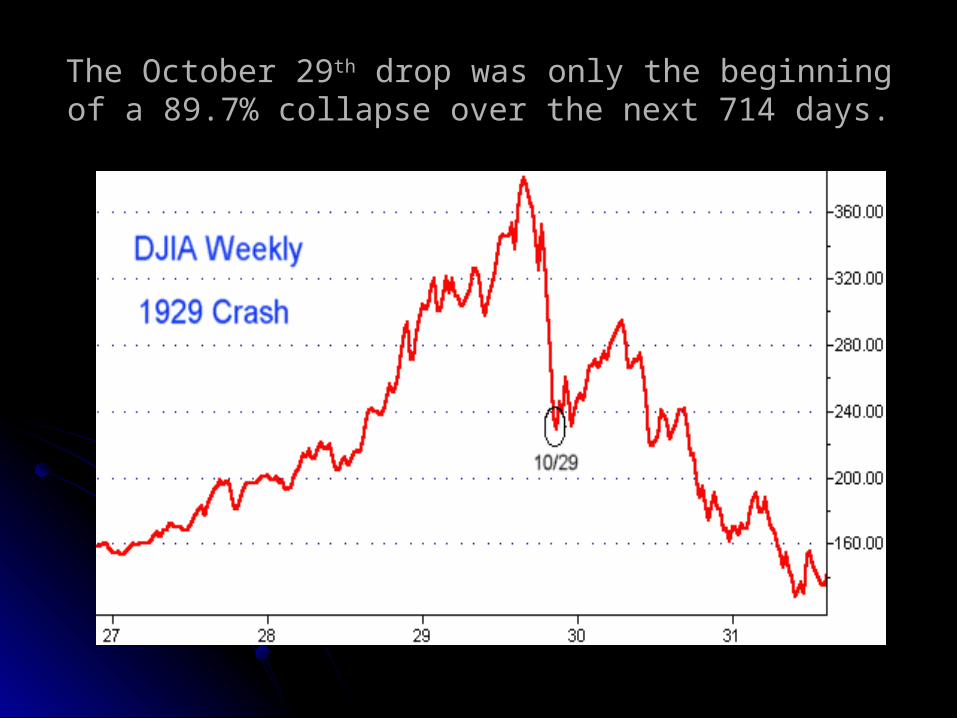

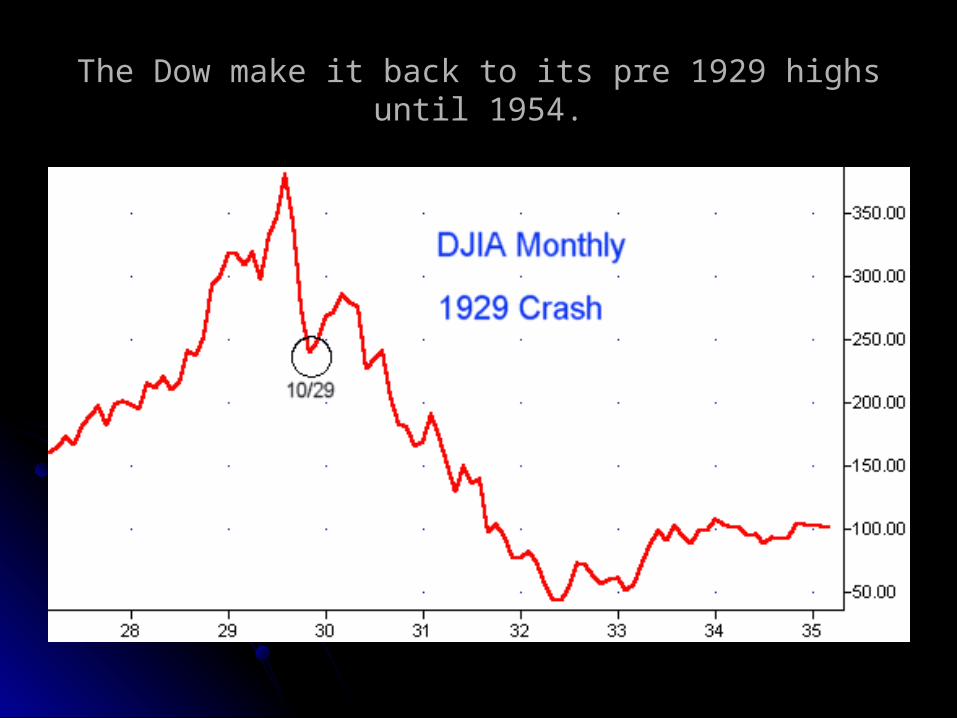

““Black Tuesday”Black Tuesday”

On Tuesday, On Tuesday, October 29,1929, October 29,1929, the Dow Jones the Dow Jones Closed at $230 – Closed at $230 – Down 23% from its Down 23% from its opening of $299 opening of $299 with huge volume with huge volume (16,410,030 shares)(16,410,030 shares)

The October 29The October 29thth drop was only the beginning of a 89.7% drop was only the beginning of a 89.7% collapse over the next 714 days.collapse over the next 714 days.

The Dow make it back to its pre 1929 highs until 1954.The Dow make it back to its pre 1929 highs until 1954.

““Black Monday”Black Monday”

On Monday, On Monday, October 19,1987 October 19,1987 The Dow fell from The Dow fell from $2246 to $1738 – $2246 to $1738 – 22.6% of its value 22.6% of its value

However, unlike the 1929 crash, the market quickly However, unlike the 1929 crash, the market quickly recovered – by September 1989, the Dow returned to its recovered – by September 1989, the Dow returned to its

pre-1987 levelspre-1987 levels

The PlayersThe Players

Securities Market Institutions Securities Market Institutions Contractual Savings Institutions (40%)Contractual Savings Institutions (40%) Investment Institutions (25%)Investment Institutions (25%)Government Institutions (10%)Government Institutions (10%)Depository Institutions (25%)Depository Institutions (25%)

______________________________________________________________

$30 Trillion in Debt and Equities$30 Trillion in Debt and Equities

Securities Market InstitutionsSecurities Market Institutions

Securities market institutions match up buyers with Securities market institutions match up buyers with sellers. (provide liquidity)sellers. (provide liquidity)

Securities market institutions also provide information Securities market institutions also provide information and analysis to help buyers and sellers of assetsand analysis to help buyers and sellers of assets

Primary Markets Primary Markets Secondary MarketsSecondary Markets

Investment Banking BrokersInvestment Banking Brokers

DealersDealers

ExchangesExchanges

Contractual SavingsContractual Savings

Contractual Savings Institutions are by far the Contractual Savings Institutions are by far the biggest participant in financial markets ($12 biggest participant in financial markets ($12 Trillion in assets)Trillion in assets)

Specialize in writing contracts to protect Specialize in writing contracts to protect policyholders from financial loss associated from policyholders from financial loss associated from specific events.specific events.

Insurance CompaniesInsurance Companies Property/Casualty ($1T) vs. Life($3T)Property/Casualty ($1T) vs. Life($3T) Mutual vs. StockMutual vs. Stock

Pension FundsPension Funds Defined Benefit vs. Defined ContributionDefined Benefit vs. Defined Contribution

Investment Institutions ($8T)Investment Institutions ($8T)

Investment Institutions represent the fastest growing Investment Institutions represent the fastest growing segment of financial markets segment of financial markets

The key service provided is low cost diversificationThe key service provided is low cost diversification Mutual FundsMutual Funds Money Market FundsMoney Market Funds Hedge Funds (LTCM)Hedge Funds (LTCM) Venture Capital FundsVenture Capital Funds

Government Institutions ($3T)Government Institutions ($3T)

Provision of Liquidity Provision of Liquidity Fannie MaeFannie Mae Freddie MacFreddie Mac Ginnie MaeGinnie Mae Sallie FaeSallie Fae

Regulation and OversightRegulation and Oversight Federal ReserveFederal Reserve SECSEC FDICFDIC

Depository Institutions ($8T)Depository Institutions ($8T)

The distinguishing characteristic of a The distinguishing characteristic of a depository institutions is the acceptance of depository institutions is the acceptance of deposits and the creation of loans.deposits and the creation of loans.

Commercial BanksCommercial BanksSavings & Loans (Thrifts)Savings & Loans (Thrifts)Credit UnionsCredit UnionsSavings BanksSavings Banks

Evolution of the Financial SystemEvolution of the Financial System

Financial InnovationFinancial Innovation Integration and GlobalizationIntegration and GlobalizationRegulationRegulationCompetitionCompetition