an overview on indian insurance sector & icici...

TRANSCRIPT

An overview on Indian insurance sector & ICICI Lombard Lloyd’s Market Development Team

February 6, 2012

2

Initial years of liberalizationYr 2001 Yr 2010 Yr 2012

Standard products : Fire, Marine, MotorProduct

67% under ambit of tariff Concept of cross-subsidy

Pricing

Majority sourcing trough 4,000 govt. owned company offices Agency was the only optional distribution channel

Channels

Ageing work-force Varying degrees of technical expertise

People

Lack of service innovation Cashless claim settlement unheard

Service

Conventional processes entailing intensive paper work(at policy issuance and most importantly even claims )

Process

No of players: 4 ; Premium : USD 2.14 bn (CAGR: 14%); GDP pen’n: 0.5 %

Industry characterized by moderate growth and oligopoly driven market environment

3

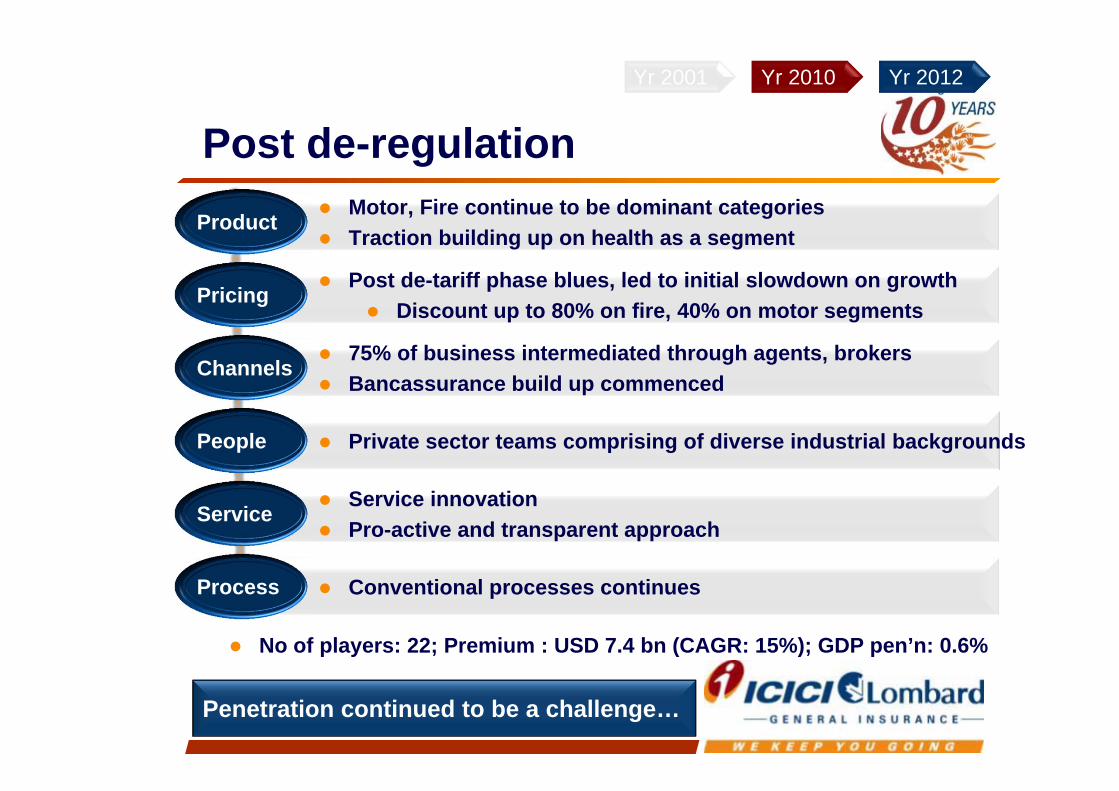

Post de-regulationYr 2001 Yr 2010 Yr 2012

Motor, Fire continue to be dominant categories Traction building up on health as a segment

Product

Post de-tariff phase blues, led to initial slowdown on growth Discount up to 80% on fire, 40% on motor segments

Pricing

75% of business intermediated through agents, brokers Bancassurance build up commenced

Channels

Private sector teams comprising of diverse industrial backgroundsPeople

Service innovation Pro-active and transparent approach

Service

Conventional processes continuesProcess

No of players: 22; Premium : USD 7.4 bn (CAGR: 15%); GDP pen’n: 0.6%

Penetration continued to be a challenge…

4

0.3

60

2.1

150

Mumbai Floods Hurricane Katrina

Insurance LossEconomic Loss

Lower penetration compared to international benchmarks

Lowest amongst the four BRIC nations

Source: Swiss Re, Sigma, Data of 2009

Instances of large catastrophesContribution by insurance sector to

the economic losses in India have been lower than other countries

In USD bn

40%15%

5

Current overview

6

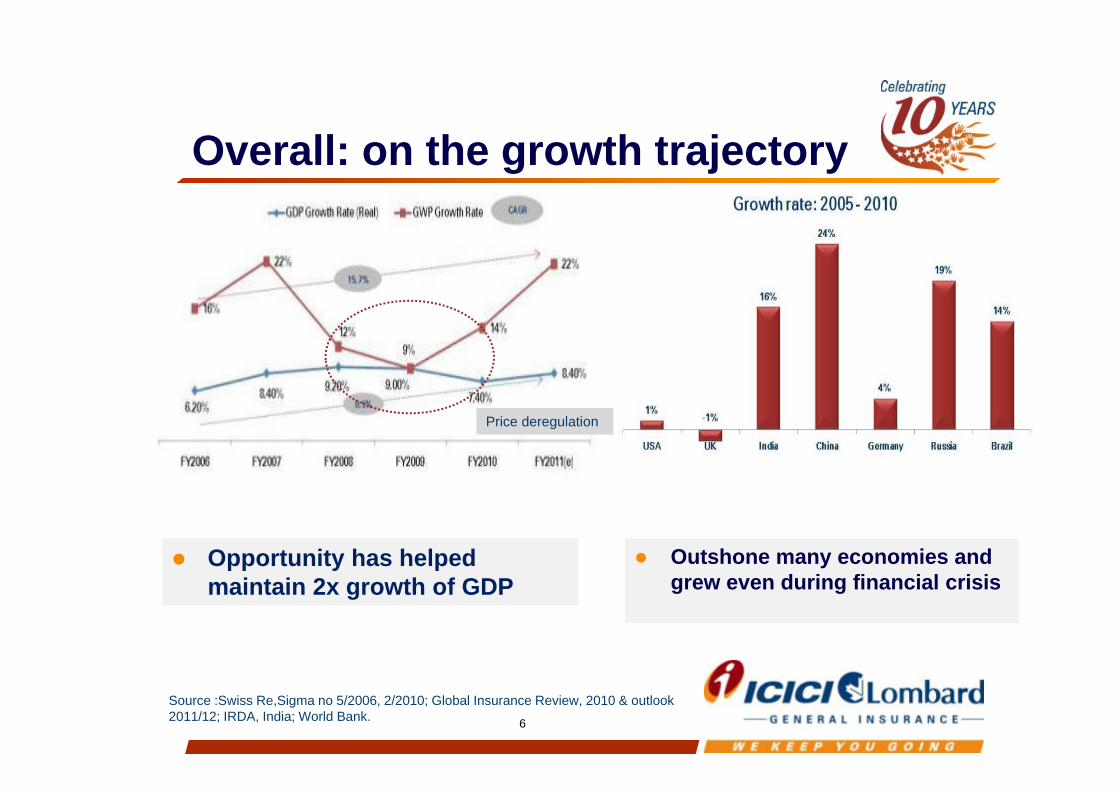

Overall: on the growth trajectory

Outshone many economies and grew even during financial crisis

Source :Swiss Re,Sigma no 5/2006, 2/2010; Global Insurance Review, 2010 & outlook 2011/12; IRDA, India; World Bank.

Opportunity has helped maintain 2x growth of GDP

Price deregulation

7

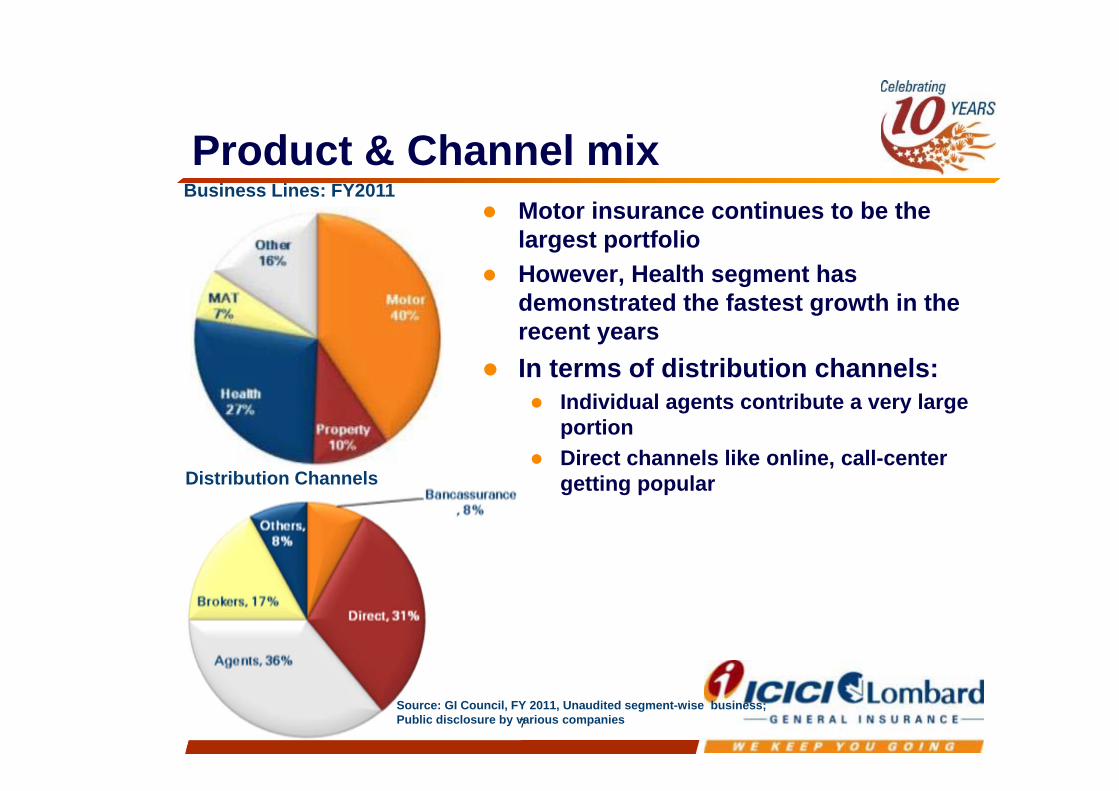

Product & Channel mix Motor insurance continues to be the

largest portfolio However, Health segment has

demonstrated the fastest growth in the recent years

In terms of distribution channels: Individual agents contribute a very large

portion Direct channels like online, call-center

getting popular

Business Lines: FY2011

Distribution Channels

Source: GI Council, FY 2011, Unaudited segment-wise business; Public disclosure by various companies

8

Insurance market opportunity in IndiaFavoring demograph-ics

• Over 1.2 billion people, one of the largest market• 2/3rd of population < 35 yrs

• Largest segment in 15-50 age group presents a favorable “youth bulge”

• Over 1.2 billion people, one of the largest market• 2/3rd of population < 35 yrs

• Largest segment in 15-50 age group presents a favorable “youth bulge”

Fast growing economy

Lower insurance penetration

• Large investments in industrial and infrastructure projects

• USD 1000 bn in next 3 years and global aspirations of corporate India

• Increasing consumer spending, Increasing income levels

• Large investments in industrial and infrastructure projects

• USD 1000 bn in next 3 years and global aspirations of corporate India

• Increasing consumer spending, Increasing income levels

• Very low insurance penetration at 0.6% of the GDP• Large growth opportunity

• Government support to push insurance penetration in form of social schemes; tax breaks and subsidies

• Very low insurance penetration at 0.6% of the GDP• Large growth opportunity

• Government support to push insurance penetration in form of social schemes; tax breaks and subsidies

Regulatory interventions acting as further catalyst to growthRegulatory interventions acting as further catalyst to growth

9

Exploring the opportunities

Under penetration across all

lines of personal products

Less than 10%

penetration in health

20% cars uninsured

Less than 5% homes

insured

80% Two wheelers uninsured

RetailCost effective distribution for low ticket insurance products will be key to increasing penetration

Profit & Quality

Customer loyalty

Risk based pricing

Diversified channels

Diversified products

WholesaleProfit and quality are key tenets for a sustained growth

10

Company overview

11

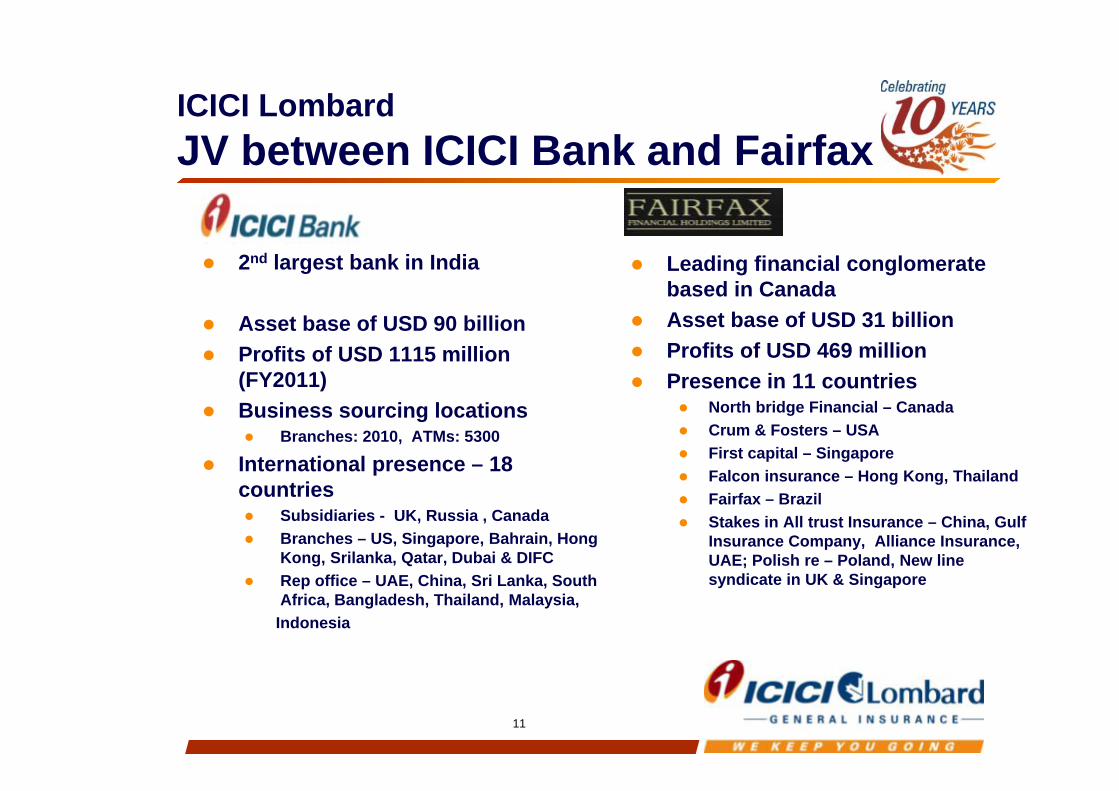

ICICI LombardJV between ICICI Bank and Fairfax

2nd largest bank in India

Asset base of USD 90 billion Profits of USD 1115 million

(FY2011) Business sourcing locations

Branches: 2010, ATMs: 5300

International presence – 18 countries Subsidiaries - UK, Russia , Canada Branches – US, Singapore, Bahrain, Hong

Kong, Srilanka, Qatar, Dubai & DIFC Rep office – UAE, China, Sri Lanka, South

Africa, Bangladesh, Thailand, Malaysia, Indonesia

Leading financial conglomerate based in Canada

Asset base of USD 31 billion Profits of USD 469 million Presence in 11 countries

North bridge Financial – Canada Crum & Fosters – USA First capital – Singapore Falcon insurance – Hong Kong, Thailand Fairfax – Brazil Stakes in All trust Insurance – China, Gulf

Insurance Company, Alliance Insurance, UAE; Polish re – Poland, New line syndicate in UK & Singapore

12

ICICI Group

13

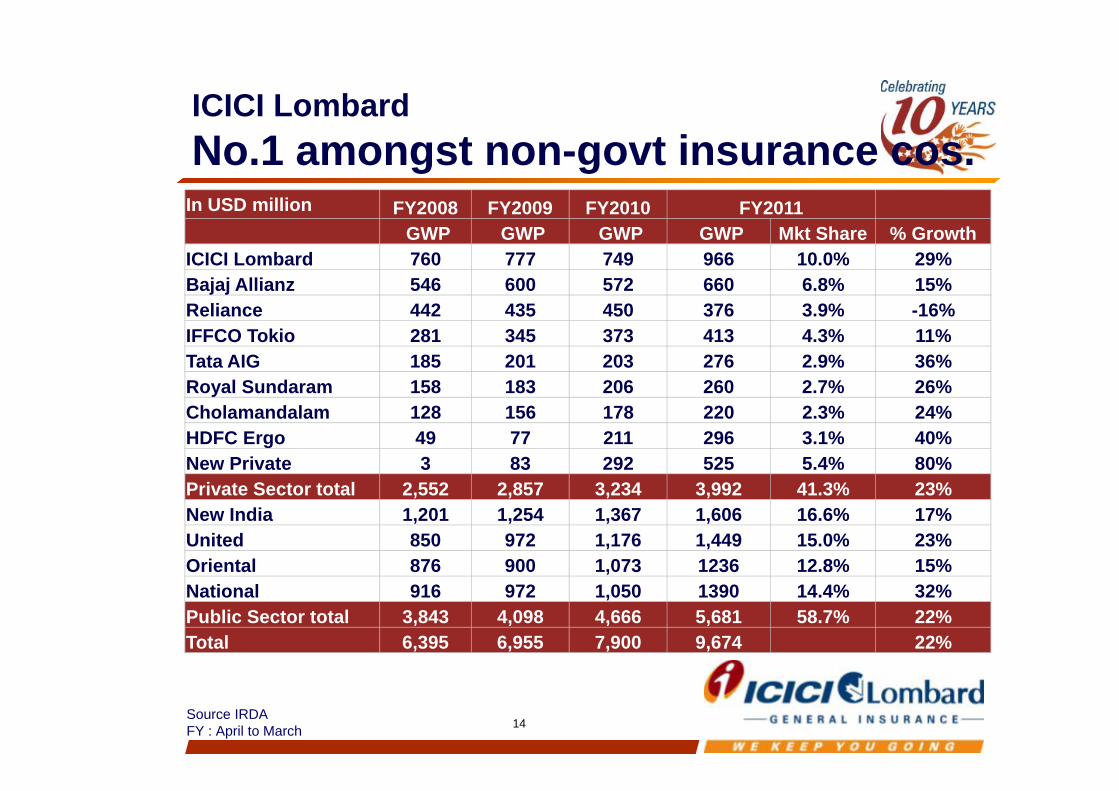

ICICI LombardOur successes Largest private insurance company in India Gross Premium of 966 mn USD in FY 2011

10% overall market share ; 24% of the private sector Credentials

Voice of Customer Choice Award 2011 (Frost and Sullivan) - Best Vehicle Insurer

Golden Peacock Award, 2011 for innovation for our contribution to mass health insurance programs

No. 1 Auto insurance company on customer satisfaction index: JD Power, Asia Pacific

Asia’s No 1 Insurer on Innovation : Asia Ins Review Most customer responsive insurance brand: ET- Avaya ISO 9001 certification for Operation’s, Motor Claims iAAA rating for highest claims paying ability: ICRA

14Source IRDAFY : April to March

In USD million FY2008 FY2009 FY2010 FY2011GWP GWP GWP GWP Mkt Share % Growth

ICICI Lombard 760 777 749 966 10.0% 29%Bajaj Allianz 546 600 572 660 6.8% 15%Reliance 442 435 450 376 3.9% -16%IFFCO Tokio 281 345 373 413 4.3% 11%Tata AIG 185 201 203 276 2.9% 36%Royal Sundaram 158 183 206 260 2.7% 26%Cholamandalam 128 156 178 220 2.3% 24%HDFC Ergo 49 77 211 296 3.1% 40%New Private 3 83 292 525 5.4% 80%Private Sector total 2,552 2,857 3,234 3,992 41.3% 23%New India 1,201 1,254 1,367 1,606 16.6% 17%United 850 972 1,176 1,449 15.0% 23%Oriental 876 900 1,073 1236 12.8% 15%National 916 972 1,050 1390 14.4% 32%Public Sector total 3,843 4,098 4,666 5,681 58.7% 22%Total 6,395 6,955 7,900 9,674 22%

ICICI LombardNo.1 amongst non-govt insurance cos.

15

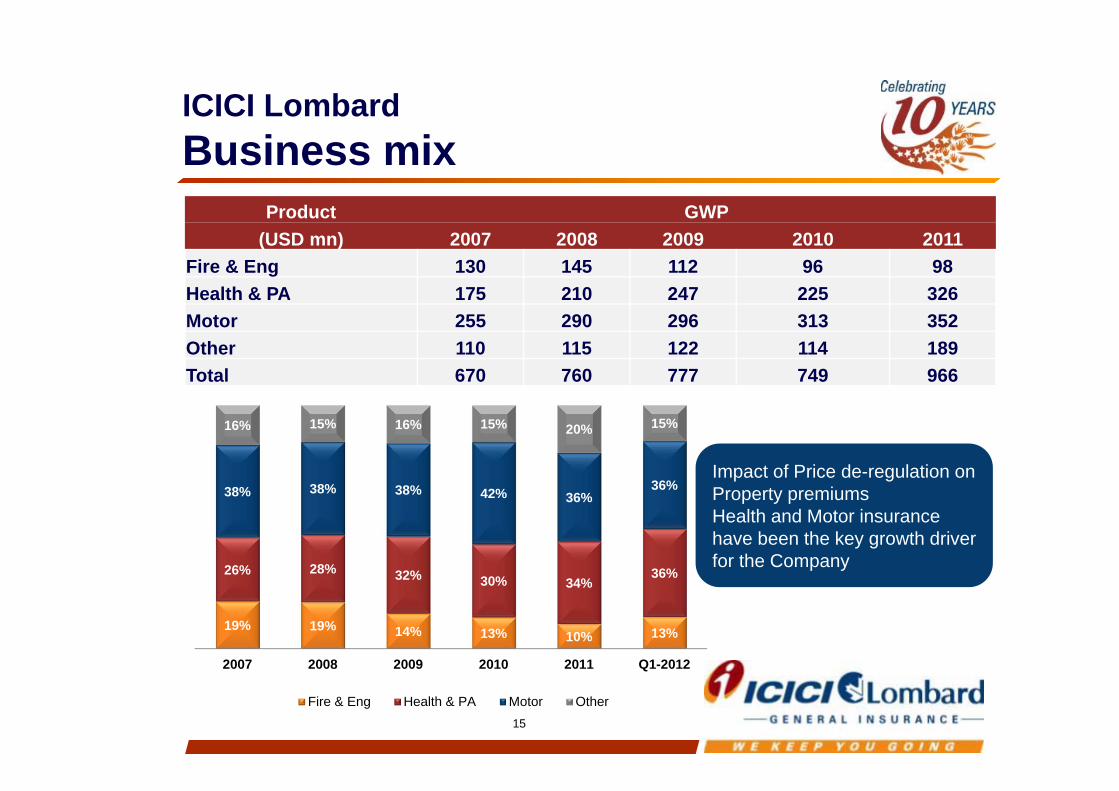

ICICI LombardBusiness mix

Impact of Price de-regulation on Property premiumsHealth and Motor insurance have been the key growth driver for the Company

Product GWP(USD mn) 2007 2008 2009 2010 2011

Fire & Eng 130 145 112 96 98Health & PA 175 210 247 225 326Motor 255 290 296 313 352Other 110 115 122 114 189Total 670 760 777 749 966

19% 19% 14% 13% 10% 13%

26% 28% 32% 30% 34%36%

38% 38% 38% 42% 36%36%

16% 15% 16% 15% 20% 15%

2007 2008 2009 2010 2011 Q1-2012

Fire & Eng Health & PA Motor Other

16

76.9%

18.2%

4.8%

PSUs, 77.8%

Pvt Others, 17.6%

IL, 4.5%

59.1%

31.5%

9.5%

PSUs58.7%

Pvt Others 31.2%

IL10.1%

Industry profitability

Inner circle: FY 2010Outer circle: FY 2011

GWPFY 2010: ` 349.84 billionFY 2011: ` 425.67 billion

U/w Losses (2011 pool LR 153%)FY 2010: ` (59.25) billionFY 2011: ` (104.72) billion

U/w Losses (2011 pool LR 127%)FY 2010: ` (59.25) billionFY 2011: ` (72.59) billion

76.9%

18.2%

4.8%

PSUs, 85.9%

Pvt Others, 12.2%

IL, 1.9%

* Premium and losses do not include mono-line companies

17

ICICI LombardLeadership in India

Distribution Customer Service

Risk management Technology

18

CorporateCorporate

GovernmentGovernment Weather, Health -USD 125 millionWeather, Health -USD 125 million

Manufacturers DealersManufacturers Dealers

6 mfrs, 2300 dealers200 million USD6 mfrs, 2300 dealers200 million USD

Banks/ FIsBanks/ FIs 38 banks/FI USD 90 million 38 banks/FI USD 90 million

WebsiteCall centerWebsiteCall center

13 partners USD 40 million13 partners USD 40 million

Agents, BrokersAgents, Brokers16000 + agent/brokerAll lines - 235 million USD16000 + agent/brokerAll lines - 235 million USD

Corporate – USD 200 millionCorporate – USD 200 million

Specialize in multi-channel distribution N

o. 1

in th

ese

chan

nels

Distribution Customer Service

Risk management Technology

19

• Health: In-house service for 95% of the portfolio Servicing 500 claims/day; Network of 4,065 hospitals

Motor: In-house surveyors; ISO:9001 certified unit

Periodic research to measure “Voice of customer dashboard” measuring service, transaction experience, Net Promoter Score

Work with the global best for corporate offerings Cunningham Lindsey- property losses United Health Care & International SOS - Overseas

travel claims W.K.Webster’s –Marine losses

Focus on Quality service

Distribution Customer Service

Risk management Technology

20

Merged underwriting & claims set-up Strong actuarial team (trained from best of universities)

Prudent underwriting with strong focus on value at risk and moral hazard Risk based approach to business development

Spread of risk across panel of quality re-insurers Conservative level of catastrophic protection

Risk management

Strong controls including risk containment unit (RCU) Fraud control critical given the large volumes of

policies/claims

Distribution Customer Service

Risk management Technology

21

Pioneered internet sales in India for insurance Rural POS machines for delivery of inclusive

insurance solutions (Weather; Health for BPL segments)

POS machines at grocery stores/gas stations for 2w insurance

Series of home-grown applications for productivity, service, delivery improvements

NASSCOM Award for the best technology in insurance company

Pioneered internet sales in India for insurance Rural POS machines for delivery of inclusive

insurance solutions (Weather; Health for BPL segments)

POS machines at grocery stores/gas stations for 2w insurance

Series of home-grown applications for productivity, service, delivery improvements

NASSCOM Award for the best technology in insurance company

360º use of Technology

Distribution Customer Service

Risk management Technology

22

RSBY: OverviewHospitalization expenses of `30,000 ($ 600) per family

Up to five members on a floater basis 727 pre-defined surgical packages including

Maternity, Newborn Care & Day Care All Pre-existing Diseases covered from day 1

Premium of `30 (60c) per family per year Balance premium : Government funded ($15)

Both Public and Private hospitals are empanelledOn the spot delivery of Smart Card

23

RSBY: Unique features Biometric smart card is issued to each

beneficiary family using the portable infrastructure

Photograph of the head of the family Fingerprints of all family members

Each empanelled hospitals have the card reader installed and are connected to the server at district level System driven approvals for inpatient treatment of the

beneficiary Allows regular data flow on service utilization Biometric enabled smart card ensures that only the real

beneficiary can use it

24

Health – Bottom of pyramid (RSBY) Hospitalization expenses of Rs 30,000 per family

Up to five members on a floater basis 727 pre-defined surgical packages including

Maternity, Newborn Care & Day Care All Pre-existing Diseases covered from day 1

Premium of Rs 30 per family per year Balance premium : Government funded Cost of Smart Card borne by the Central

Government Both Public and Private hospitals are

empanelled On the spot delivery of Smart Card

25

Reinsurance perspective

26

Reinsurance: current scenario Limited participation in the treaties

Across the board (bouquet) approach key reason Proportional programs do not have event limits

In case of change in structure (prop to non prop) first opportunity to longstanding partners Support on CAT, Aviation, Energy and Liability

prog. Current engagement primarily on Fac basis

Terrorism, Marine DSU, Aviation ,Liability and Energy

27

Future opportunities Increased participation on specialty lines

Weather, Aviation , Liability and Energy Health a growing segment - New product ideas

Social schemes Retail opportunities

Large size of CAT program opens new opportunity

Innovative Catastrophe cover to Govt

28

Advantages and challengesLloyds & India Advantages

Financial security Ability to provide innovative solutions

Hindrances Lack of local presence

Understanding of business dynamics and requirement

Holistic requirements from Indian market perspective

29

Thank you

30

India is an important and growing reinsurance market for Lloyd's, even though foreign reinsurers can currently only write Indian reinsurance business on a cross-border basis. In just the three year period from 2007 to 2010, Lloyd's gross written premiums in India grew by almost 150%, from $73 million $182 million.

The top classes Lloyd's writes in India are offshore energy, property catastrophe, terrorism, cargo and aviation xl risks. As the economy expands, the opportunities and appetite for new specialist areas have been growing.

Over the last few years, the Lloyd's market has been working with the Indian insurance regulator, the IRDA, to find ways for Lloyd's unique structure to be accounted for in anticipation of changes that could allow more foreign involvement in the Indian market.

Lloyd's has lobbied extensively with the international (re)insurance community for a bill to allow entry of foreign reinsurers in India via branches, but those proposals have yet to be passed.