analysis: global cellular market trends and insight, q1 2012

TRANSCRIPT

© Wireless Intelligence 2012

Wireless Intelligence

Analysis: Global cellular market trends and insight, Q1 2012March 2012

© Wireless Intelligence 2012 2

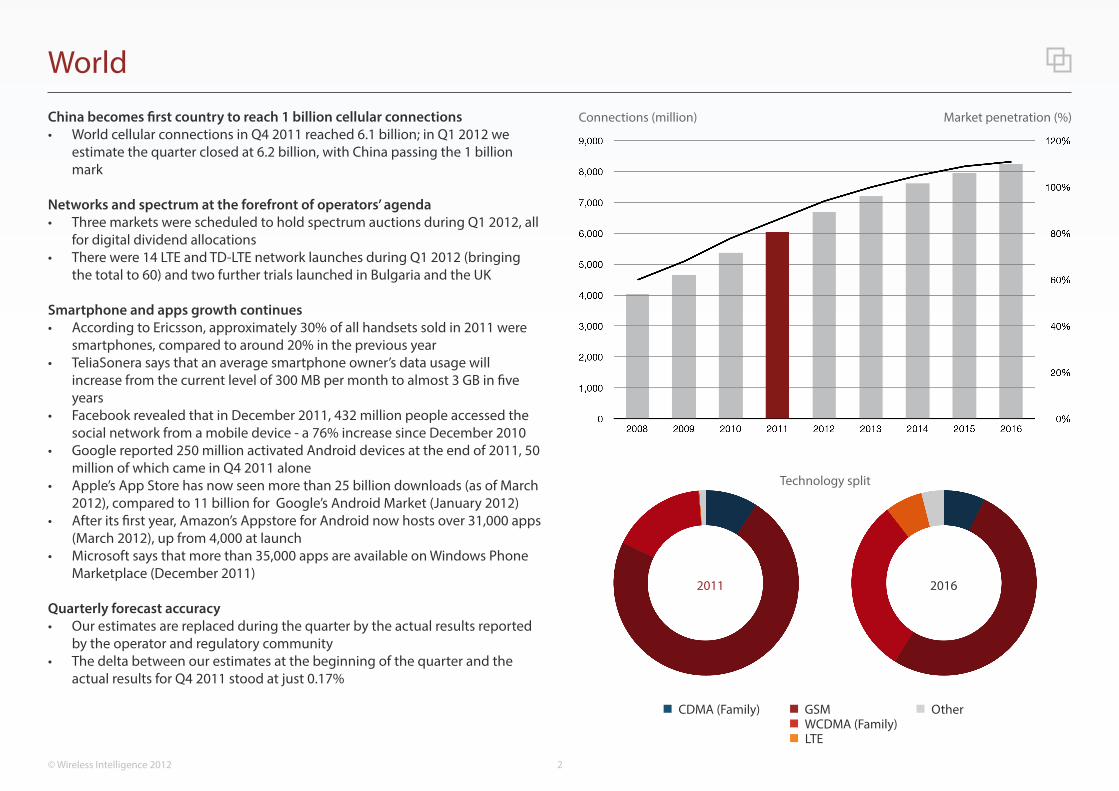

World

Connections (million) Market penetration (%)China becomes first country to reach 1 billion cellular connections• World cellular connections in Q4 2011 reached 6.1 billion; in Q1 2012 we

estimate the quarter closed at 6.2 billion, with China passing the 1 billion mark

Networks and spectrum at the forefront of operators’ agenda• Three markets were scheduled to hold spectrum auctions during Q1 2012, all

for digital dividend allocations• There were 14 LTE and TD-LTE network launches during Q1 2012 (bringing

the total to 60) and two further trials launched in Bulgaria and the UK

Smartphone and apps growth continues• According to Ericsson, approximately 30% of all handsets sold in 2011 were

smartphones, compared to around 20% in the previous year• TeliaSonera says that an average smartphone owner’s data usage will

increase from the current level of 300 MB per month to almost 3 GB in five years

• Facebook revealed that in December 2011, 432 million people accessed the social network from a mobile device - a 76% increase since December 2010

• Google reported 250 million activated Android devices at the end of 2011, 50 million of which came in Q4 2011 alone

• Apple’s App Store has now seen more than 25 billion downloads (as of March 2012), compared to 11 billion for Google’s Android Market (January 2012)

• After its first year, Amazon’s Appstore for Android now hosts over 31,000 apps (March 2012), up from 4,000 at launch

• Microsoft says that more than 35,000 apps are available on Windows Phone Marketplace (December 2011)

Quarterly forecast accuracy• Our estimates are replaced during the quarter by the actual results reported

by the operator and regulatory community• The delta between our estimates at the beginning of the quarter and the

actual results for Q4 2011 stood at just 0.17%

t2011

Technology split

2016

CDMA (Family)

LTE

OtherWCDMA (Family)GSM

© Wireless Intelligence 2012 3

Africa and Middle East

Connections (million) Market penetration (%)Q4 2010 Q3 2011 Q4 2011

Number of Connections (million)

Total 850.8 943.9 977.3

Contract 95.8 106.1 109.5

Prepaid 754.5 837.2 867.8

CDMA (Family) 22.1 22.2 21.8

GSM 755.0 813.7 833.9

WCDMA (Family) 72.8 107.1 120.8

Net Additions(million)

Total 41.3 37.8 33.5

Contract 3.6 2.8 3.4

Prepaid 37.7 34.9 30.5

Growth Rate, Sequential (%)

Total 5.1 4.2 3.5

Contract 3.9 2.7 3.2

Prepaid 5.3 4.4 3.6

Growth Rate, Year-on-Year (%)

Total 18.2 16.6 14.9

Contract 13.8 15.0 14.2

Prepaid 18.7 16.8 15.0

Market Penetration (%) 62.8 68.5 70.5

ARPU (US$) 10.95 10.41 10.25

2015

CDMA (Family)

LTEWCDMA (Family)GSM

2011

Technology split

2016

© Wireless Intelligence 2012 4

Africa and Middle East

SIM registration bites but Africa remains fastest-growing region

Connections growth dominated by Vodacom and MTN• Vodacom took the top two spots for subscriber gains in Africa – a 2.8 million

increase in South Africa and 1.4 million in Tanzania – citing promotional offerings and improved distribution

• In the Middle East, the largest absolute growth came from MTN Irancell, Iran which also added 1.4 million new connections

• In Africa, Orange Uganda lost 239,000 connections, followed by areeba (MTN) Guinea (191,000) and Orange Madagascar (131,000)

• In the Middle East, Zain Saudi Arabia saw its subscriber base cut by 2.4 million connections due to a clean-up of inactive subscribers

SIM registration deadlines pass in three more markets• The Ghanaian regulator, NCA, confirmed that over 1.5 million SIM cards had

been deactivated following 16 million registrations as of the March deadline• In Nigeria, a final deadline of December 31 was reached (having been

previously extended indefinitely) but the NCC estimates that some 14.5 million SIM cards have been doubled-counted during registration, out of 110 million total

• In Uganda, registration became mandatory in March and customers have a year to register with their operator

• In Saudi Arabia, regulators plan mandatory prepaid registration but have not set a deadline on the scheme’s introduction

M&A still on the agenda for the right price• Bharti Airtel is considering expansion into Cameroon and South Africa, while

MTN expressed an interest in acquiring licences in Angola and Ethiopia• Libya’s transitional government has indicated that it intends to review a

number of pan-African telecoms investments, and in particular investments carried out by LAP Green Network could be withdrawn

Licencing delays hinder interest• In Iraq, STC has removed itself from the running for the country’s fourth

national licence after delays in awarding the contract

Insight: Pricing increases brings competitive rebalance across the region

In Tanzania, Vodacom noted that pricing had increased for the first time after a long period of unsustainably low tariffs and a fierce price war. With the exception of Vodacom, all of the country’s operators have registered one or more quarters of subscriber declines in the past two years. With the latest increase in pricing however, growth has been redistributed among all but the market’s two smallest operators – Sasatel (Dovetel) and BOL Mobile (Benson Infomatics).

Vodacom’s successes in South Africa and Tanzania were mirrored by other operators such as Mobinil (ECMS) Egypt and Malitel (Sotelma) Somalia, capitalising on a newfound freedom to experiment with tariffing and promotional activity as the region withdraws itself from the intense voice competition discussed in our previous review. In particular, Malitel’s experimentation with dual-SIM offers (including a buy-one-get-one-free promotion with credit) and time of day tariffing (‘endless nights’ allows unlimited on-net airtime between 11pm and 8am) have allowed the operator to generate over 700,000 additional connections. In contrast, pricing remains a concern in Burkina Faso and Gabon where sharp declines in prices have has led to attempts to rejuvenate usage with per-second billing and on-net promotions similar to ‘favourite number’ offers.

Presidential and parliamentary elections in the Democratic Republic of Congo impacted on operators’ results to varying degrees in the quarter. Vodacom announced net additions of 336,000 connections ”despite uncertain political conditions”, however Tigo (Millicom) cited a ”negative impact” to economic activity in the market as well as ”difficult trading conditions” which resulted in a loss of almost 100,000 connections.

In the Middle East, aggressive competition in Bahrain coupled with high penetration produced ”expected” results for Batelco who attributed its year-closing loss of 13,000 connections to the first full year of operation for the country’s third operator, Viva (Saudi Telecom). Both operators are also trialling LTE and Viva plans to launch commercial services by March, having established a small-scale network in Bahrain city centre.

© Wireless Intelligence 2012 5

Americas

Connections (million) Market penetration (%)Q4 2010 Q3 2011 Q4 2011

Number of Connections (million)

Total 567.0 615.0 632.7

Contract 100.6 113.3 118.0

Prepaid 466.4 501.7 514.7

CDMA (Family) 21.9 16.4 15.1

GSM 490.0 514.0 520.2

WCDMA (Family) 45.6 74.0 86.3

Net Additions(million)

Total 21.7 18.2 17.6

Contract 4.4 4.9 4.7

Prepaid 17.2 13.2 13.0

Growth Rate, Sequential (%)

Total 4.0 3.1 2.9

Contract 4.6 4.6 4.2

Prepaid 3.8 2.7 2.6

Growth Rate, Year-on-Year (%)

Total 11.7 12.8 11.6

Contract 17.8 17.9 17.4

Prepaid 10.5 11.7 10.4

Market Penetration (%) 95.5 102.8 105.4

ARPU (US$) 12.78 12.22 12.46

CDMA (Family)

LTE

OtherWCDMA (Family)GSM

2011 2016

Technology split

© Wireless Intelligence 2012 6

Americas

Region records fastest 3G connections growth for second quarter running

Brazil the growth engine as 3G goes from strength-to-strength• Of the 158 operators active at the end of Q4 2011, 147 reported positive

quarterly net additions representing a total of 23.2 million connections, while the remaining 11 operators recorded subscriber losses totalling 5.8 million

• Some 86.7% or 15.1 million of the region’s total net additions for the quarter came in Brazil, where TIM added 4.9 million subscribers, Vivo (Telefónica) 4.5 million, Claro (América Móvil) 2.9 million and Oi 2.6 million

• 4.7 million of the subscriber losses in the region can be attributed to a change in active subscriber policy by América Móvil in Mexico and Colombia

• The region had the world’s highest quarterly 3G growth at 10.9%

Further LTE launches imminent across region• Claro’s LTE network in Puerto Rico is due to go live in early 2012 supported by

vendor Alcatel-Lucent, following AT&T’s LTE launch in November 2011• Une (EPM) in Colombia is also expected to launch LTE in the first half of 2012,

and expects between 120,000 and 180,000 customers to sign up for the service during the first year of operation

• Mexico’s Telcel (América Móvil) has confirmed that it will launch its initial LTE network coverage to consumers in April 2012, with the first stage of rollout in 25 to 40 cities before coverage is extended across the entire country

Competition arrives in Costa Rica, more countries get HSPA networks• November 2011 saw both Claro (América Móvil) and Movistar (Telefónica)

enter the Costa Rican market with HSPA-only operations, challenging incumbent Kolbi (ICE)

• Also during Q4 2011, Digicel launched HSPA+ networks in Barbados, Cayman Islands and Panama, and the operator has since announced plans for a similar operation in Jamaica that will provide 80% population coverage initially

• Caribbean rival LIME (Cable & Wireless) has also implemented HSPA+ in the Cayman Islands and Jamaica, and expects its 21 Mb/s HSPA+ service to go live in the British Virgin Islands before end of Q1 2012

• Cable & Wireless also launched HSDPA in Bahamas through local arm BTC

Insight: Mexican regulators in spotlight as Televisa/Iusacell merger blocked

The regulation of the telecommunications sector in Mexico came under further scrutiny this quarter as the Organisation for Economic Cooperation and Development (OECD) published a report of its investigation into the country’s relatively low telecoms penetration. The report indicates that a lack of competition has led to above average prices for consumers and businesses, and subsequently slowed the adoption of new services and technologies. Wireless Intelligence data shows that as of Q4 2011, at 81.4% Mexico is ranked 150 of 230 countries worldwide in terms of mobile penetration – and in the Americas region only Cuba, Haiti, Bolivia and a few small island nations have fewer mobile phones per capita.

The market is dominated by América Móvil’s Telcel, which has an estimated 70% of the country’s mobile connections, while Telefónica’s Movistar controls 21%. According to the report, the average market share of the incumbent mobile operator across OECD countries is only around 40%, and it goes on to say that Telcel’s profit margins are much higher than the OECD average for incumbents, while capex is lower than in any other country on a per capita basis. To encourage competition the OECD recommends that, as well as reforming the court system and implementing wider public consultation processes, the government should give more power to the telecoms regulator COFETEL. This would include increasing its financial and administrative independence and allowing the body to impose much higher sanctions than at present to deter anti-competitive behaviour.

Interestingly, when competition regulator COFECO flexed its muscles earlier this year to prevent consolidation in the Mexican communications sector, it may actually have further restricted competition in the mobile market. A proposed merger between Iusacell and Mexico’s largest broadcaster Televisa (see Global cellular market trends and insight, Q2 2011) was rejected by the regulator in January on the grounds that the operator’s owner Ricardo Salinas Pliego also controls TV Azteca, the country’s second largest media outlet. Yet COFECO did not see any competition issues in the mobile sector arising from the deal, and as proceeds from Televisa’s investment were expected to be used to finance capex and thereby improve service quality and coverage, the move could actually have helped Iusacell to compete more effectively with Telcel and Movistar.

© Wireless Intelligence 2012 7

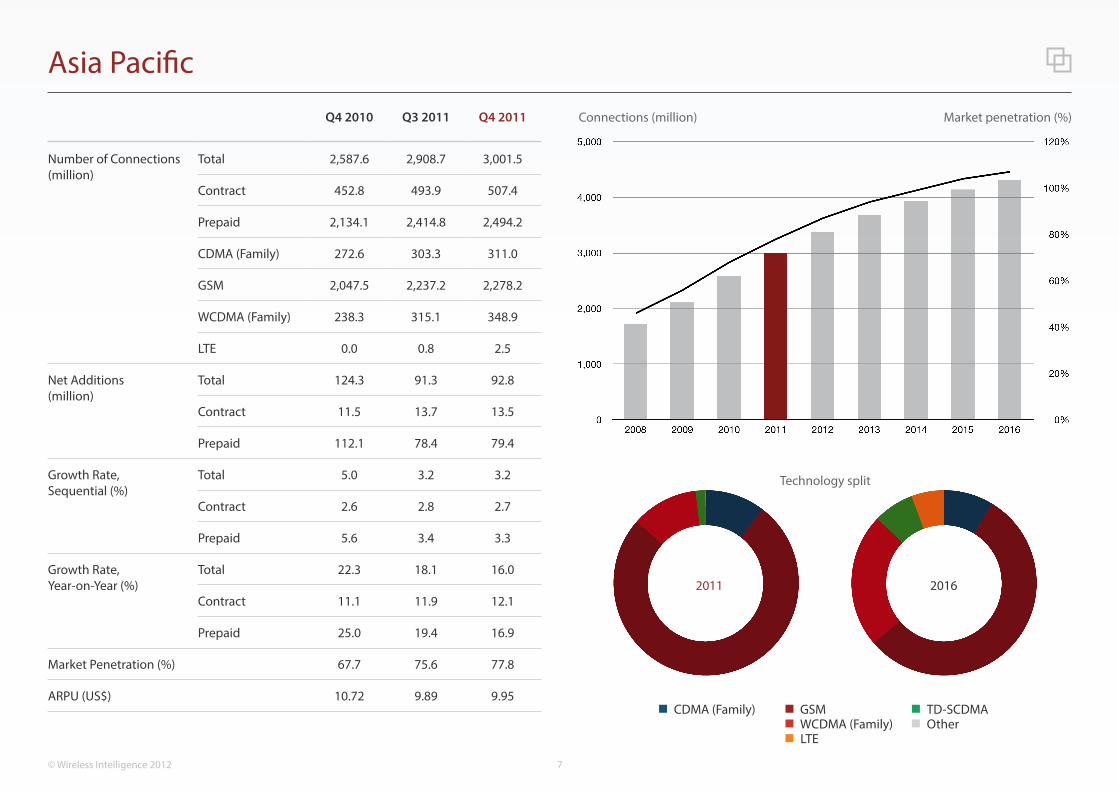

Asia Pacific

Connections (million) Market penetration (%)Q4 2010 Q3 2011 Q4 2011

Number of Connections (million)

Total 2,587.6 2,908.7 3,001.5

Contract 452.8 493.9 507.4

Prepaid 2,134.1 2,414.8 2,494.2

CDMA (Family) 272.6 303.3 311.0

GSM 2,047.5 2,237.2 2,278.2

WCDMA (Family) 238.3 315.1 348.9

LTE 0.0 0.8 2.5

Net Additions(million)

Total 124.3 91.3 92.8

Contract 11.5 13.7 13.5

Prepaid 112.1 78.4 79.4

Growth Rate, Sequential (%)

Total 5.0 3.2 3.2

Contract 2.6 2.8 2.7

Prepaid 5.6 3.4 3.3

Growth Rate, Year-on-Year (%)

Total 22.3 18.1 16.0

Contract 11.1 11.9 12.1

Prepaid 25.0 19.4 16.9

Market Penetration (%) 67.7 75.6 77.8

ARPU (US$) 10.72 9.89 9.95CDMA (Family)

LTE

TD-SCDMAOtherWCDMA (Family)

GSM

2011 2016

Technology split

© Wireless Intelligence 2012 8

Asia Pacific

Regional growth continues amidst consolidation and licence cancellations

Close to a hundred million subscribers added across the region• Of the 162 operators active at the end of Q4 2011, 148 registered positive

quarterly net additions representing a total of 117 million connections, while 13 operators recorded subscriber losses totalling 7.5 million

• Outside of China and India, the highest gains were recorded by XL and Telkomsel (2.9 million each) in Indonesia, and Viettel, Vietnam (2.5 million)

• The most significant loss in the region was in India where Tata DOCOMO’s connections base declined by 5.3 million, mainly as a result of data clean-up

• Meanwhile, Warid Telecom in Pakistan lost just over a million subscribers

Market undergoing consolidation in Philippines and Vietnam• Sun Cellular (Digitel) in Philippines has merged with rival Smart, after Smart’s

parent company PLDT acquired 98% of Digitel’s shares; the new operator has a combined 63.7 million connections

• E-Mobile (EVN Telecom) in Vietnam was merged into Viettel at the start of Q1

LTE gains ground in Eastern and South-Eastern Asia• StarHub’s LTE network went live in the financial district of Singapore in

December 2011; the operator expects 80% population coverage by end-2012• KT launched an LTE network in South Korea in January, while rival LG Uplus

has gained more than a million LTE subscribers since its launch in Q3 2011• Also in Q1 2012, Japan’s E-Mobile (eAccess) launched LTE in the Kanto area,

while SoftBank Mobile now has its own ‘4G’ network using the Advanced Extended Global Platform (AXGP) technology, based on the PHS system

India rocked by cancellation of 122 licences• In February India’s Supreme Court ruled that 122 licenses issued by former

telecom minister A Raja in 2008 to mobile operators were issued illegally• The cancellations will affect Aircel (in 14 circles), Idea Cellular (11), MTS (21),

Tata Docomo (3), Vodafone (7), Loop Mobile (12), Cheers Mobile (15), Uninor (15), S Tel (5) and Videocon (17); S-Tel and Cheers have since announced plans to cease operations

Insight: All change for True Corp. as 3G finally gets a foothold in Thailand

3G services are finally beginning to show encouraging growth in Thailand following their soft launch last year, with operators now aiming for a rapid migration of users from WCDMA to HSPA networks. The introduction of WCDMA technology to the country has been subject to numerous delays in terms of issuing licenses and importing equipment, and while 3G has been available on a ‘trial’ basis since 2008, Thailand’s first commercial WCDMA/HSPA network was only launched by market-leader AIS as recently as July 2011. Other operators quickly followed suit, and as a result 3G connections in Thailand doubled year-on-year to 4.2 million in Q4 2011 (of which an estimated 71.7% were HSPA, up from 36.7% a year earlier), although this still only represents 5.5% of the country’s total connections.

Hence with so much potential for further 3G growth in the country, operators have set bullish targets for mobile broadband connections – none more so than True Corporation, Thailand’s third-largest operator, which aims to more than quadruple the current HSPA customer base under its ‘True Move H’ brand to 4.0 million subscribers by the end of this year – which according to our forecasts would put it level with the significantly larger AIS in terms of HSPA connections. True Move H added 500,000 connections during 2011, boosted by True Corporation’s acquisition of rival Hutch in Q1 of that year. True is aiming to migrate 80% of Hutch’s subscribers on to HSPA before its planned shutdown of the latter’s legacy CDMA network this year.

True also plans to move all of its 400,000 initial trial 3G subscribers – currently signed up to the True Move brand – to True Move H, and we expect that the operator will phase out its WCDMA network by the end of 2012. Subsequently True is investing heavily in new HSPA infrastructure to meet projected demand, and expects to roll out 13,500 HSPA towers across 77 provinces in 2012. For the country as a whole we expect 3G connections to increase to 13.5 million by the end of 2012, equivalent to 16.4% of total. Some 87.9% of these 3G connections will be HSPA, and we predict that this proportion will rise to 98.7% of a total of 39.4 million 3G subscribers (41.5% of all connections) in 2015 in the absence of any significant CDMA competition.

© Wireless Intelligence 2012 9

Eastern Europe

Connections (million) Market penetration (%)Q4 2010 Q3 2011 Q4 2011

Number of Connections (million)

Total 510.7 529.0 537.0

Contract 107.3 110.2 111.8

Prepaid 403.3 418.7 425.1

CDMA (Family) 6.4 7.4 7.8

GSM 440.9 440.7 441.6

WCDMA (Family) 62.5 80.1 86.7

Net Additions(million)

Total 7.0 10.0 8.0

Contract 2.1 1.5 1.6

Prepaid 4.9 8.5 6.4

Growth Rate, Sequential (%)

Total 1.4 1.9 1.5

Contract 2.0 1.4 1.5

Prepaid 1.2 2.1 1.5

Growth Rate, Year-on-Year (%)

Total 5.0 5.0 5.2

Contract 6.0 4.8 4.3

Prepaid 4.7 5.1 5.4

Market Penetration (%) 125.2 129.6 131.5

ARPU (US$) 9.85 9.97 9.58

CDMA (Family)

LTE

OtherWCDMA (Family)GSM

2011 2016

Technology split

© Wireless Intelligence 2012 10

Eastern Europe

Eastern European markets are reaching higher maturity levels

Encouraging regional growth despite high level of market maturity• During 2011, 25 of 124 operators reported negative net additions, totalling a

net loss of 5.3 million connections• This is an improvement compared to 2010 which saw 27 operators reporting

negative net additions for a net loss of 11.4 million connections• Overall, regional annual connections growth in 2011 remained on a par with

that of 2010 at 5%• Regional penetration (131.5%) has for the first time overtaken that of

Western Europe (131.0%)• We expect that Eastern Europe will overtake Western Europe in terms of total

connections by the summer of 2012

Changes in prepaid data policy impacts operator connections growth• In Croatia, Vipnet (Telekom Austria) registered a net loss of 155,000

connections due to the deactivation of inactive prepaid cards• Meanwhile, rival Tele2 adjusted its prepaid customer base to remove 60,000

inactive customers while its customer base was also negatively impacted by seasonal churn in the prepaid segment

• In Albania, AMC (OTE) saw its installed base decline by 10% annually due to the company’s effort to clean up its customer base of inactive customers

Highly competitive markets affect OTE’s results• In Bulgaria, Globul (OTE) reported a 0.8% decrease in mobile revenues

between Q4 2010 and Q4 2011 due to intense competition in the business market segment and lower off-bundle customer spend

• In Albania, OTE reported a 19.1% decline in mobile revenues over the same period due to lower interconnection tariffs, intense competition in a highly fragmented market, and adverse macroeconomic conditions

• The operator’s struggle was partly offset by positive yearly revenue growth (3.9%) in Romania where it achieved positive cash flow on a full-year basis for the first time in its history

3G network coverage expansion continues in the region

3G connections in Eastern Europe represent 19% of the region’s total connections in Q1 2012 and we expect this to reach 22% by year end partly helped by operators’ efforts to improve network coverage. MTS launched its LTE network in Armenia in December 2011 in the centre of Yerevan with expansion planned for Gyumri, Vanadzor and other regional centres. The operator holds spectrum in the 2500-2520 MHz and 2620-2640 MHz bands in Yerevan and 2600-2640 MHz in the regions. Rival Orange (France Telecom) launched its 42.2 Mb/s HSPA+ network in Yerevan, Gyumri and Vanadzor last January. Albania’s OTE also launched its 42 Mb/s DC-HSPA+ network recently. The operator’s 3G network now covers 90% of the population and 70% of the landmass of the country.

In the Czech Republic, Vodafone is reportedly looking to upgrade half of its existing 3G network to support HSPA+ by March 2012. Rival O2 (Telefónica) rolled out its 3G network to cover 72% of the population in the course of 2011. At the end of last year, the operator’s 3G network was available to the population of 1,699 cities and municipalities all over the country. Meanwhile, T-Mobile (Deutsche Telekom) recently announced that it is shutting down its older UMTS-TDD network in favour of a more conventional UMTS-FDD network. T-Mobile’s 3G (including HSPA+) services are now available to 80% of the population of the Czech Republic compared to 37% at the beginning of 2011. In just one year, nearly 1,400 transmitters have been built and put into service – a record 265 base transceiver stations were set up in October alone.

Telenor upgraded 2,100 base stations for its mobile Internet network and installed 200 new ones during 2011 in Hungary, and rival T-Mobile launched its LTE network in January in the capital Budapest, covering around 40% of the city’s population.

In Slovakia, T-Mobile (Slovak Telekom) increased last February the number of municipalities covered by its DC-HSPA+ 42 Mb/s mobile broadband network to 15, while 21 Mb/s HSPA+ services have been expanded to a total of 210 locations. The operator is also expanding its 7.2 Mb/s HSDPA-based network in other areas, with the eventual aim of covering 80% of the population with WCDMA/HSPA services, up from around 60% at the beginning of 2011.

© Wireless Intelligence 2012 11

Western Europe

Connections (million) Market penetration (%)Q4 2010 Q3 2011 Q4 2011

Number of Connections (million)

Total 525.6 535.6 542.3

Contract 248.6 256.3 260.6

Prepaid 274.0 276.1 278.0

CDMA (Family) 0.6 0.6 0.6

GSM 320.6 296.6 291.7

WCDMA (Family) 204.4 238.1 249.6

LTE 0.02 0.3 0.5

Net Additions(million)

Total 6.3 5.8 6.8

Contract 4.4 3.5 4.4

Prepaid 1.7 2.2 1.9

Growth Rate, Sequential (%)

Total 1.2 1.1 1.3

Contract 1.8 1.4 1.7

Prepaid 0.6 0.8 0.7

Growth Rate, Year-on-Year (%)

Total 0.7 3.1 3.2

Contract 6.4 5.0 4.9

Prepaid -4.2 1.4 1.5

Market Penetration (%) 127.4 129.5 131.0

ARPU (US$) 30.61 29.52 28.76CDMA (Family)

LTE

OtherWCDMA (Family)GSM

2011 2016

Technology split

© Wireless Intelligence 2012 12

Western Europe

Competitive pressures lead to drastic cost-cutting initiatives

Southern Europe remains challenging despite high Q4 demand• 20 operators (out of 103) reported negative yearly net additions (mainly in

Nordic countries and Southern European markets), totalling a net loss of 1.7 million connections

• Greece, Portugal, Italy and Spain are among the top 10 slowest growing markets in the region in Q4 2011

• Southern European markets were affected by weakened macro-economic conditions and intense competitive pressures impacting pricing and usage

Smartphone penetration continues its rapid adoption• In Finland, 74% of all handsets sold in Q4 2011 were smartphones, compared

to 66% in Q3 2011 and 47% in Q4 2010• In France, Orange (France Telecom) sold over 420,000 smartphones during

the Christmas sales rush, a rise of 19% over the previous year• In the UK, O2 (Telefónica) reported that smartphone penetration jumped

from 29% to 36% between 2010-11 as more than 95% of handset sales in the contract segment were smartphones in Q4 2011; 3 (Hutchison) stated that 60% of customers own smartphones, up from just 30% a year ago; Vodafone reported 39% smartphone penetration along with a data attach rate of 84%

• Vodafone also reached 20% smartphone penetration in Germany in Q4 2011 (67% data attach rate), compared to 24% in Italy (47% data attach rate)

Operators to stop smartphone subsidies• Vodafone Spain reported a 27% increase in data revenue in Q4 2011 helped

by 49% contract smartphone penetration• Service revenues at Vodafone Spain declined by GBP 119 million annually• Data revenues are not fully offsetting declining voice revenues and handset

subsidies are dramatically impacting operating expenses• Vodafone Spain announced that smartphone subsidies are to be stopped

for new and upgrading clients – a move already implemented by Movistar (Telefónica) Spain and Free Mobile (Iliad) in France

Insight: Free Mobile disrupts the status-quo in French market

Since the launch of France’s fourth operator Free Mobile (Iliad) in mid-2012, incumbent operators have reported pressured quarterly results. SFR (Vivendi) has announced that Free Mobile’s launch caused a net loss of 208,000 connections between January 1 and February 29 despite ”excellent 2011 Christmas sales”. Similarly, Orange (France Telecom) announced a net loss of 201,000 customers between January 1 and the February 15. The operator stated that, during this period, Free Mobile’s launch caused the termination of over one million contracts, only partially offset by 837,000 new signings. Wireless Intelligence estimates that Free Mobile has reached its 3 million connections target within its first three months of operation.

The preparations made by Orange and SFR prior to the launch of the new entrant did not counter the impact of Free Mobile’s competitive pricing. In August 2010, both operators introduced new bundled offers to secure the retention of their multi-play customers and counter the success of Iliad’s broadband offer branded ‘Freebox Revolution’. Orange’s ‘Open’ and SFR’s ‘Multi-Packs’ bundled deals attracted 1.2 million customers each between August 2010 and December 2011. In October last year, both operators introduced web-only contract-free tariffs (without subsidies) branded ‘Sosh’ at Orange and ‘Red’ at SFR, yet they only attracted 28,000 customers each between October and December 2011.

Both SFR and Orange responded to Free Mobile’s tariffs immediately after launch. SFR had to adapt its ‘Red’ web-only tariffs and launched limited editions of its contract and bundled deals, while Orange had to re-invent its ‘Sosh’ tariffs which increased the customer base to 90,000 as of February 15.

Vivendi’s SFR blames Free Mobile for aggressively subsidising tariffs with asymmetric voice and SMS termination rates while pushing the majority of its traffic on to Orange’s 3G network. The latter expects that its roaming agreement with Free Mobile will generate EUR 1 billion over six years and that even though “traffic from Free Mobile customers could be substantially higher than expected”, it will not harm the service quality of Orange’s network.

© Wireless Intelligence 2012 13

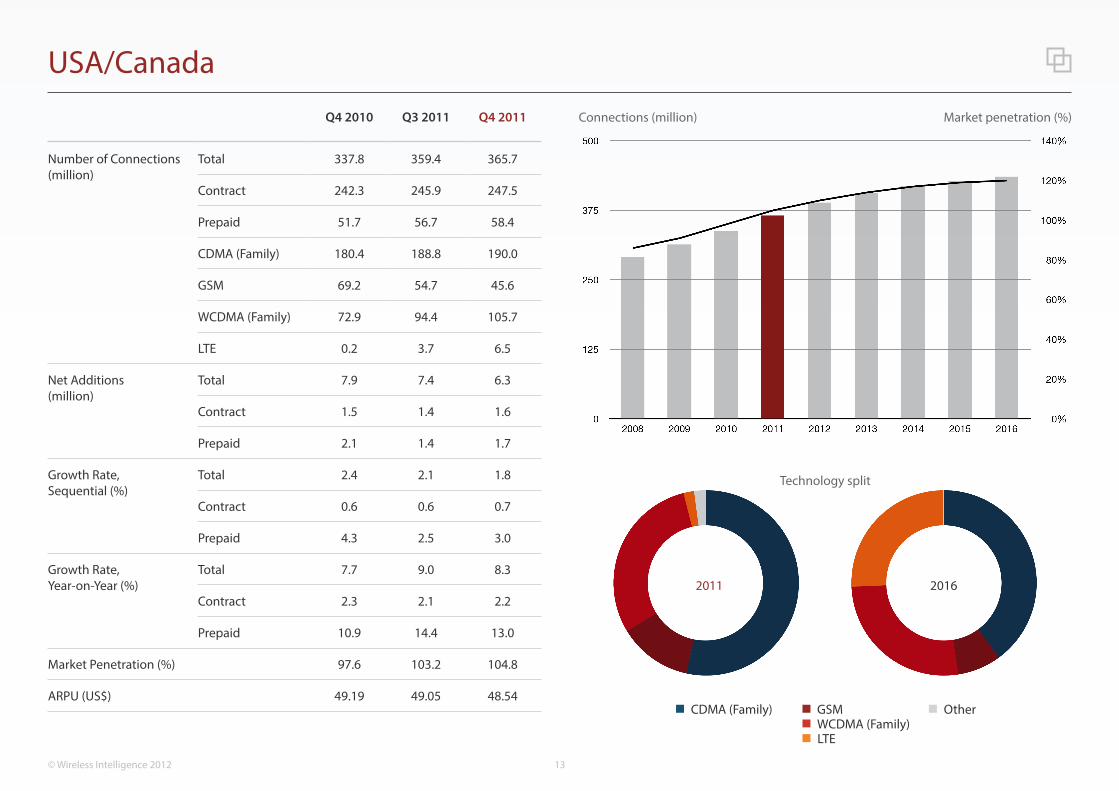

USA/Canada

Connections (million) Market penetration (%)Q4 2010 Q3 2011 Q4 2011

Number of Connections (million)

Total 337.8 359.4 365.7

Contract 242.3 245.9 247.5

Prepaid 51.7 56.7 58.4

CDMA (Family) 180.4 188.8 190.0

GSM 69.2 54.7 45.6

WCDMA (Family) 72.9 94.4 105.7

LTE 0.2 3.7 6.5

Net Additions(million)

Total 7.9 7.4 6.3

Contract 1.5 1.4 1.6

Prepaid 2.1 1.4 1.7

Growth Rate, Sequential (%)

Total 2.4 2.1 1.8

Contract 0.6 0.6 0.7

Prepaid 4.3 2.5 3.0

Growth Rate, Year-on-Year (%)

Total 7.7 9.0 8.3

Contract 2.3 2.1 2.2

Prepaid 10.9 14.4 13.0

Market Penetration (%) 97.6 103.2 104.8

ARPU (US$) 49.19 49.05 48.54CDMA (Family)

LTE

OtherWCDMA (Family)GSM

2011 2016

Technology split

© Wireless Intelligence 2012 14

USA/Canada

Smartphone sales surge drives record breaking quarter

iPhone dictates operator fortunes in Q4 2011• The iPhone-touting operator trio helped the US record 5.8 million net

additions in Q4; AT&T led the way with 2.5 million, followed by Sprint with its best quarter in six years with 1.6 million, and Verizon with 1 million

• T-Mobile lost 500,000 connections in Q4 as ‘not carrying the iPhone led to a significant increase in deactivations’

Smartphone sales set new records• AT&T reported a record with 9.4 million smartphone sales and 7.6 million

iPhone activations in Q4; smartphones were 80% of contract device sales• Verizon sold 7.7 million smartphones in Q4 (representing 70% of contract

device sales) and activated 4.3 million iPhones• Sprint sold 1.8 million iPhones in Q4, some 40% to new customers; 86% of

‘Sprint platform’ contract handset sales were smartphones• 11 million T-Mobile customers now use smartphones after 2.6 million

smartphone sales in Q4, a record 92% of total device sales• 35% of MetroPCS subscribers are on a smartphone plan and 40% of devices

sold in Q4 ran on Android

Connected devices hit bump in road• AT&T added 1 million connected devices in Q4 to surpass 13 million

connections; Sprint reached 2 million connected devices• Verizon reported the loss of 490,000 telematics connections in Q4, believed

to be related a change in policy regarding GM’s OnStar customers• T-Mobile’s connected devices declined to 2.4 million following 265,000

deactivations related to a single customer

LTE continues to gain momentum• Verizon sold 2.3 million LTE devices (1.6 million smartphones and 700,000

data devices) during Q4• 5% of Verizon’s customer base is now using its LTE network• Cricket (Leap Wireless) launched LTE in Tucson, Arizona in December• Telus Mobility launched LTE in 14 metropolitan areas in February

Insight: Operators focus efforts on refarming spectrum holdings

Current network deployment strategies are being driven by rapidly increasing data usage and growing fears of a looming capacity crunch. The failed play for T-Mobile by AT&T was largely justified as seeking to secure additional spectrum to boost network capacity. AT&T highlighted that its total wireless data traffic doubled in 2011, with data usage increasing by 40% annually from existing smartphone users. Similar reasoning is currently being put forward by Verizon in its pursuit of approval to acquire spectrum from SpectrumCo and Cox Communications. The operator has argued that without additional spectrum its LTE network will start to run out of capacity in some markets by 2013 and many more by 2015. Verizon expects data traffic on its LTE network to exceed that of its CDMA EV-DO network in early 2013, while by the end of 2015 LTE data traffic is projected to be five times the peak level carried on its EV-DO network.

The spectrum crunch is pushing operators to refarm their existing spectrum holdings. Sprint plans to deploy LTE using its 800 MHz spectrum where it is currently phasing out its iDEN service. The operator will initially use 1900 MHz spectrum for its LTE deployment in a narrow 5x5 MHz configuration but plans to move some of its CDMA traffic off this band to free up further capacity. AT&T is looking to refarm its 1900 MHz GSM spectrum for LTE and has contacted some of its customers urging them to upgrade their devices. T-Mobile has also revealed plans to refarm its 1900 MHz GSM spectrum for HSPA+ services. Verizon is similarly preparing the ground to refarm its spectrum by announcing plans to push customers onto its LTE network by mandating that all of the smartphones it sells this year must support LTE. The regional prepaid operators face similar spectrum pressures with MetroPCS admitting that its LTE network, which utilises 5x5 MHz channels in most markets, can only support a maximum of 4-5 million subscribers. Cricket (Leap Wireless), which is starting out on channels smaller than 5x5 in many markets, admitted that it will take it three to four years and ‘a lot of farming’ to offer LTE on 10x10 MHz channels.

Canadian operators have also been pushing for additional spectrum to be released. It was recently announced that the 700 MHz ‘digital dividend’ and 2500 MHz spectrum auction has been scheduled for the first half of 2013.

© Wireless Intelligence 2012 15

About Wireless IntelligenceWireless Intelligence is the definitive source of mobile operator data, analysis and forecasts, delivering the most accurate and complete set of industry metrics available. Relied on by a customer base of over 700 of the world’s mobile operators, device vendors, equipment manufacturers and leading financial and consultancy firms, the data set is the most scrutinised in the industry. With over 5 million individual data points – updated daily – the service provides coverage of the performance of all 940 operators and 800 MVNOs across 2,200 networks, 55 groups and 225 countries worldwide.

Whilst every care is taken to ensure the accuracy of the information contained in this material, the facts, estimates and opinions stated are based on information and sources which, while we believe them to be reliable, are not guaranteed. In particular, it should not be relied upon as the sole source of reference in relation to the subject matter. No liability can be accepted by Wireless Intelligence, its directors or employees for any loss occasioned to any person or entity acting or failing to act as a result of anything contained in or omitted from the content of this material, or our conclusions as stated. The findings are Wireless Intelligence’s current opinions; they are subject to change without notice. The views expressed may not be the same as those of the GSM Association. Wireless Intelligence has no obligation to update or amend the research or to let anyone know if our opinions change materially.

© Wireless Intelligence 2012. Unauthorised reproduction prohibited.

Please contact us at [email protected] or visit www.wirelessintelligence.com. Wireless Intelligence does not reflect the views of the GSM Association, its subsidiaries or its members. Wireless Intelligence does not endorse companies or their products. Wireless Intelligence operates under an Independence Charter. For full details please see www.wirelessintelligence.com/independence.aspx.

GSM Media LLC, 1000 Abernathy Road, Suite 450, Atlanta, GA 30328.

wirelessintelligence.com•[email protected]•twitter.com/wi

Joss Gillet Senior Analyst

Will CroftAnalyst

Jon GrovesAnalyst

Calum DewarAnalyst