analysis of the cashew value chain in burkina faso · cashew trading and marketing is the least...

TRANSCRIPT

Analysis of the Cashew Value Chain in Burkina FasoAfrican Cashew initiative

Published by:Deutsche Gesellschaft fürInternationale Zusammenarbeit (GIZ) GmbHFondations internationalesPostfach 5180, 65726 Eschborn, GermanyT +49 61 96 79-1438F +49 61 96 79-80 1438E [email protected] www.giz.de

Place and date of publication:Burkina Faso, February 2010

Authors:Nasser Kankoudry Bila; Ousmane Djibo; Philippe Constant; Boureima Sanon

Responsible editor:Peter Keller (Director African Cashew initiative)African Cashew initiative (ACi)32, Nortei Ababio Street Airport Residential AreaAccra, GHANAT + 233 302 77 41 62 F + 233 302 77 13 63

Contact: [email protected]

Acknowledgement:This study has been implemented as part of the African Cashew initiative (ACi), a project jointly financed by various private companies, the Federal German Ministry for Economic Cooperation and Developmentand the Bill & Melinda Gates Foundation. ACi is implemented by the African Cashew Alliance (ACA), the German Development Cooperation GIZ, as a lead agency as well as FairMatchSupport and Technoserve.

This report is based on research funded by the Bill & Melinda Gates Foundation. The findings and conclusions contained within are those of the authors and do not necessarily reflect positions or policies of the Bill & Melinda Gates Foundation.

Design:creative republic // Thomas Maxeiner Visual Communikations, Frankfurt am Main/GermanyT +49 69-915085-60 I www.creativerepublic.net

Photos:© GIZ/ Rüdiger Behrens, Thorben Kruse, Claudia Schülein & iStock, Shutterstock, creative republic, Thomas Maxeiner

African Cashew Initiative is funded by:

and private partners

In cooperation with:Implemented by:

COOPERATIONBURKINA FASO

FEDERAL REPUBLIC OF GERMANY

Analysis of the Cashew Value Chain in Burkina FasoFebruary 2010

4 Table of contents

List of Tables ......................................................................................................4List of Figures ....................................................................................................5

Summary ...............................................................................................................8

1 Introduction .................................................................................................9

1.1 BriefoverviewofcashewproductionandprocessinginBurkinaFaso............................ 18

2 Analysis of the Value Chain ...............................................................18

2.1 IntroductiontothehistoryofcashewproductioninBurkinaFaso...................... 18

2.2 Illustrationofthevaluechainandmarketing....... 182.3 Descriptionofthecashewproductionsystem....... 222.4 Detaileddescriptionofcashewprocessing............ 242.5 Analysisofvaluechainserviceproviders.............. 262.5.1 Overviewofvaluechainserviceproviders............ 262.5.2 Overviewofcashewvaluechainfinancial

serviceproviders.................................................... 282.6 Institutionalandpolicygovernancechain............ 292.7 Cashewvaluechainstrengths,weaknesses,

opportunitiesandthreats...................................... 302.8 Overviewoforganisationshelpingtopromote

thecashewvaluechaininBurkinaFaso............... 31

3 Recommendations ....................................................................................34

List of Acronyms ...............................................................................................36Annex I: Documentation ................................................................................38

List of Tables

Table 1.1.1: Importanceofthecashewvaluechainforthenationaleconomy.................... 13

Table 1.1.2:Thegrowers................................................... 14

Table 1.1.3a:Theprocessingindustry............................... 14

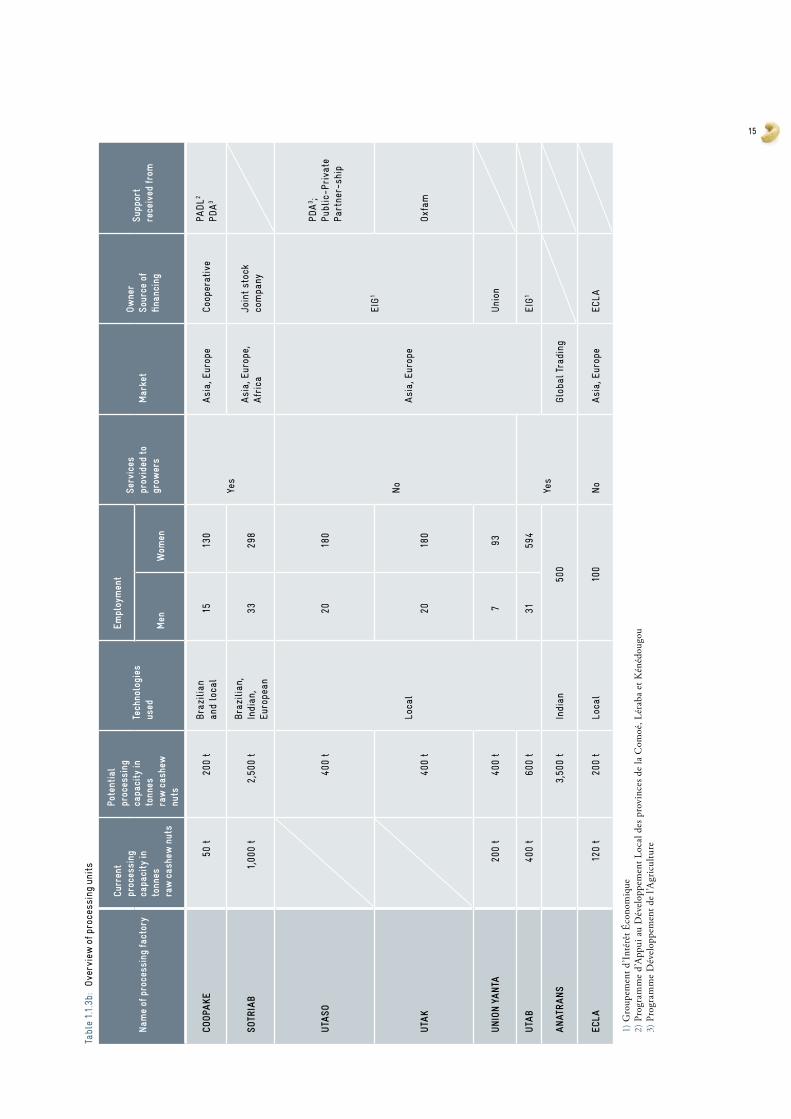

Table 1.1.3b:Overviewofprocessingunits...................... 15

Table 1.1.4:Tradersandtheiractivities........................... 16

Table 1.1.5:Policyframeforpromotionofthecashewvaluechain.................................................. 16

Table 2.2.1:CoststructureofdealersinrawnutsinCFAF(Source:SNVreport)....................... 21

Table 2.3.1: Totalnumberofcashewtrees,householdsandtotaloutput.............................................. 22

Table 2.4.1: Overviewofprocessingunits........................ 24

Table 2.5.1: Evaluationoftheneedforservicesamongthevaluechain’sstakeholders................................. 26

Table 2.5.2: Overviewofcashewvaluechainserviceproviders................................................................. 27

Table 2.5.3.:Overviewoftheorganisationoffinancialsupportforagriculturalactivities.................... 28

Table 2.6.2: Nationalpolicyaffectingvaluechainperformance............................................................. 29

Table 2.7.1:Summaryofstrengths,weaknesses,opportunitiesandthreats(SWOTanalysis)...................... 30

Table 2.8.1: Playershelpingtopromotethecashewvaluechain...................................................... 31

Table 3.1:Missinginformation........................................ 34

5 List of Figures

Figure 2.2.1:Thestakeholdersinthecashewvaluechain.................................................. 18

Figure 2.2.2: Illustrationandquantificationoftheexistingmarketingchain......................................... 21

Figure 2.2.3: Illustrationofthegrower,marketing,processingandexportprice............................................... 22

Figure 2.3:Mapofcashew-growingareasinBurkinaFaso................................................................. 23

Figure 2.4.1:Cashewproductsandtargetmarket............ 24

Figure 2.7.1: Illustrationofthedifficultiesfacingthecashewvaluechain...................................................... 30

Summary

ThisanalysisofthecashewsectorhasbeencarriedoutfortheACiproject.ThefederativeprojectisfundedbytheBill & Melinda Gates FoundationandimplementedinfiveAfricancountriesthatpro-duceandexportcashewnutswithlittlevalueaddedThelaunchofaprojectofthisscoperequiresustotakestockofwhatisknownaboutproduction,processing,marketingandexportinthepartici-patingcountries.TheaimofthisanalysisisthereforetoenhanceunderstandingofthecashewvaluechaininBurkinaFaso.

CashewtreeswerenotwellknowntothegeneralpublicinBurkinaFasobeforeindependence.Thefirstplantationswereintroducedaround1960bytheTropical Forest Technical Centre.Cashewtreeswerelongconsideredtobeaspeciesofforesttreeratherthanafruittree.Theywerefirstreallyusedforeconomicgainin1980,aspartoftheProjet Anacarde.In1997,thegovernmentlaunchedacashewsectordevelopmentprogrammewhoseobjectivewastoplant1,000,000trees.

AccordingtodatafromtheGeneral Agricultural Census,about45,000householdsinBurkinaFaso havetenormorecashewtrees;97%arelocatedinCascades,Sud-Ouest,Hauts-BassinsandCentre-Ouestregions,whichhave17,500,14,220,10,000and2,200growersrespectively.Theplantationsvaryinsizefrom0.5to50ha,withmostbetween2and5haor5and10ha.Mostcashewgrowersaremembersofvillageassociations,groups,unionsorcooperativesthathavewidelydifferingdegreesofactivity.Growersarenotasyetrepresentednationally.

8

9

Cashewtradingandmarketingistheleastwell-knownlinkinthecashewchain.Theharvestseasonlastsaboutfourmonths(JanuarytoMay).Marketinginvolvesavarietyofplayers:commercialcom-panies,localdealersandtheoccasionalforeignbuyer.ThecommercialcompaniesareusuallybranchofficessetupinBurkinaFasobyinternationaltradingcompaniesthatsellthecashewsdirectlytousersandbrokersinEurope,AsiaandAmerica.Localdealersarewholesalers;theyarefewinnumber(lessthan15),areknowntohaveconsiderablefinancialresourcesandlogisticalmeans,andhaveaperma-nentstaff.TheoccasionalforeignbuyersusuallycometoBurkinaFasofromMali,Guinea,GhanaandCôted’Ivoiretotopuporders.

Twootherimportantactorsareso-calledpisteursandcollecteurs.Whiletheformertravelroundtheproductionareasinsearchofnutstofillbuyerorders,thelatterarebasedinthevillages.Pisteursandcollecteursusuallysupplywholesaledealers,occasionalbuyersandexporters.Theyhavetieswithallthoseinvolvedinmarketing.

ProcessingisbasicallycarriedoutinsixunitsinCascadesandHauts-Bassinsregions.ThelargestcompanyisSOTRIABinBanfora,whichhasaprocessingcapacityofabout1,000t.Twootherunitswillbeoperationalin2010:one,basedinBoboDioulasso(Anatrans),istohaveaprocessingcapacityof3,500t;theother,basedinKampti,willbethefirstinSud-Ouestregionandwillhaveacapacityof400t.Inadditiontotheprocessingunits,numerousgroupsofsmall-scaleprocessorshavelongexistedintheDiéri,OrodaraandBoboDioulassoareas,andmorerecentlyinSissiliprovinceandSud-Ouestregion.

Three groupsareinvolvedinexportingcashews.Thefirst comprisesgebana AfriqueandBurkina-ture,whicharebasedinOuagadougouandhavechieflyEuropeanclients;theyexportcertifiedproducts(organicand/orfairtrade).The secondexportsstandardwhitekernels.Itcomprisesforthemostpartforwarderswhodelivertheoutputoftheprocessingunitstothecustomers;somecustomersbuythekernelsex-worksandarrangetheirowntransport.The thirdgroupexportsrawcashewnuts.Itconsistsessentiallyofwholesalers/exportersbasedinBoboDioulassoandOuagadougouwhoworkwiththecollecteurstostorethenutsanddeliverthemtoportusingtheirownmeansorviaforward-ers.Mostofthenationaloutput(roughly90%)isexportedintheformofrawnuts;verylittleisprocessedand/orconsumedlocally.

InBurkinaFaso,oneofthebiggestchallengesfacinggrowersistoimproveyields.Thismeansmasteringpreandpost-harvestproductiontechniques.Varietalresearchisneededandseedsmustbemadeavailable.

Themainquestionatmesolevelistheintegrationofservicesintothesector,withaviewtoprofessionalisingtheplayersandtoreachingtheminlargenumberseasilyandrapidly.Trainingaidsmustbepooled.Thisdoesnotmeanthatallaidsshouldbeidentical,butratherthattheyshouldcomplementeachotherandthattrainingapproacheshavetobestandardised.

Oneofthesector’smaindifficultiesremainsaccesstofinancing.Processorsstarteachseasonwithlessandlessoperatingfunds,oftenbecausetheyhavedifficultyrepayingexistingloansorevenbecausethefinancialinstitutionshavelittleinsightintoagriculturalactivities.Thebankswillingtograntsuchloansarefewandfarbetween.Investmentcreditseemsmorereadilyavailable,becausetheequipmentconstitutesaformofcollateral,buthereagain,veryfewbanksarewilling.Themaindifficultyfacinggrowersistoobtainseasonalcreditenablingthemtotendtheirplantationsandharvestthenuts.

12 1 Introduction

TheaimofthisanalysisofthecashewvaluechaininthecountriesparticipatingintheACiprojectistosynthesiseandsystematicallyexaminealltheinformationavailableoncash-ewsinordertoenhanceunderstandingoftheactivitiescarriedoutinthesector,gaugetheirimportanceforthenationalecono-myandmeasuretheirimpactonpovertyreduction,income-generationforsmall-scalegrowers,jobcreationandthesector’sintegrationintotheglobalmarket.

Theideaisthustobuildonthereferencedataavailableattheoutsetoftheprojectinordertoensurethevariousdevelopmentstructuresdonotduplicatetheiractivitiesandtofostersyner-gyandtherebyeffectiveness.Specifically,thestudyaimsto:

ÿ analysethecashewvaluechainatnationallevel,focusingontheproduction,processingandtradeofcashewnuts;

ÿ analyseongoingactivitiesandbringtolightnewpriorityactivities.

ThestudyisbasedontheGIZ ValueLinksapproachandthedataandexperiencesoftheAgricultural Development Programme (PDA).

Itwasconductedby:ÿ collectingthedocumentsavailableonthesubjectfrom

publicandprivateinstitutions(researchinstitutes,uni-versities,developmentprojectsandprogrammes,ministrytechnicaldepartments,processingandtradingunits,growerorganisationsatvariouslevels,etc.);

ÿ collectingadditionalinformationfromresourcepersonsandcashewsectorstakeholders;

ÿ analysing,weighingandcollatingthedataobtained(documentreviewandinterviews).

ThestudyalsointegratestheresultsoftheRapport de l’atelier sur la promotion des chaînes de valeur ajoutée de la filière anac-arde (Nasser Kankoudry, Ousmane Djiba, Philippe Constant, PDA-GIZ, May 2008)andtheDiagnostic de la filière anacarde au Burkina Faso pour une analyse des chaînes de valeurs (Nasser Kankoudry, PDA-GIZ, April 2008).

TheACiprojectcooperatescloselywiththePDA,whichisassistedbyGIZandhasidentifiedgrowthsectorsinneedofaid.ThecashewsectorisonethosereceivingsubstantialPDAPhase IIsupport.TheACiprojectthusconsolidatesandbroadensthePDAinitiativetoheightenthecompeti-tivenessoftheBurkinabecashewsector.

TheACihasalreadycarriedoutanumberofactivitiesinBurkinaFaso.Ithasprovidedsupportfortheimplementationoftrainingactivitiesinpost-harvesttechniquesforprocessingunitsthroughoutthecountry(TechnoServetraininginMay2009).OthertrainingprovidedbyTechnoServetoprocessingunitsaimedtoexplainthetechnicalsettingsofmachinesandimprovetheunits’management(June2009).Lastly,inJuly2009,theACiheldaplanningworkshopinwhichallthoseconcerned(PDA, ACi, ACA)participated.

Table 1.1.1: Importance of the cashew value chain for the national economy

Cashews Source

Human development index (global rank )

177 (out of 182)2009 Human Development Report (United Nations Development Programme)

GDP in US$US$ 17.96 billion (2008 estimate)

CIA World Factbook, 2008

Agricultural GDP in US$US$ 3.77 billion (2008 estimate)

CIA World Factbook, 2008

Agricultural GDP/ national GDP in %

29.1% CIA World Factbook, 2008

Total volume of cashews (raw cashew nuts) grown in Burkina Faso in t (2006)

25,000 t of cashew nuts

Total volume of cashews (raw cashew nuts) exported by Burkina Faso in t (2008)

Raw cashew nuts: net weight - 13,523 t; value - CFAF 1,294,957,386

White kernels: net weight - 259 t; value - CFAF 128,570,852

Customs services for 2008

Total volume of cashews (raw cashew nuts) produced worldwide in t (2007)

2.1 million (estimate for 2008: 2 million t) Red River Foods, Inc. (2008)

Cultivated land in ha 4 291 885 ha 65,800 haGeneral Directorate for Agricul-tural Forecasts and Statistics, 2007–2008

Total population (2008) 15 746 232 45,000 households CIA World Factbook, 2008

Population living under the poverty threshold in % (2004)

46.4% Not known CIA World Factbook, 2008

13 1.1 Brief overview of cashew production and processing in Burkina Faso

Table 1.1.2: The growers

Information on the growers Sources

Total number of cashew growers

45,076

of whom 97% are in the Cascades (17,500), Sud-Ouest (14,200), Hauts-Bassins (10,000) and Centre-Ouest (2,200) regions

Information provided by the specialised public agencies, notably the Agriculture Ministry, via the 2006 RGA

Plantation size by householdbetween 0.5 and 50 hamost are between 2-5 ha or 5-10 ha

2006 RGAFarmgate price for raw nuts (grower price) [USD/t] US$ 250 – US$ 875/t

Cashew-related income[in US$/year/ha]

US$ 150 – US$ 450/year/ha

Cashew revenues in terms of total income [as a % of total income]

No data

Cashew intercropping Cotton, karite, tubers, maize, vegetables

Data collected from the stakeholders

Other sources of incomeAnimal husbandry, trade, black-eyed peas, timothy grass, vegetables

Harvest period January to May

Number of cashew trees 13,194,223

2006 RGA

Productivity per cashew tree [in kg per tree

4 kg – 10 kg/tree

Average age of cashew trees [in years]

15 years

Cashew certification: certification system

ECOCERT and FLO

Inputs usedStandard: manure; triple fertiliserOrganic: organic manure; neem seed fertiliser; sawdust

Cost of inputs per ha (CFAF)Standard: CFAF 63,625 – CFAF 149,350/haOrganic: CFAF 57,500 – CFAF 96,500/ha

Land available for the expansion of cashew plantations [in terms of product competitiveness]

Strong potential

Table 1.1.3a: The processing industry

Information on the processing industry Sources

Processing capacity of all processing units in Burkina Faso

Currently used [in t /year]: 1,750 t

Data collected from the processors and stakeholders

Potential: 8,200 t/year

Processing units

Large, over 1,000 MT: ÿ Anatrans ÿ Sotriab

Medium-sized, between 500 and 1,000 MT

Small, less than 500 MT: ÿ UTASO ÿ UTAK ÿ Union Yanta ÿ UTAB ÿ ECLAcla

14

Tabl

e 1.1.3b

: O

verv

iew of p

roce

ssin

g un

its

Nam

e of

pro

cess

ing

fact

ory

Curr

ent

proc

essi

ng

capa

city

in

tonn

es

raw

cas

hew

nut

s

Pote

ntia

l pr

oces

sing

ca

paci

ty in

to

nnes

raw

cas

hew

nu

ts

Tech

nolo

gies

us

ed

Empl

oym

ent

Serv

ices

pr

ovid

ed to

grow

ers

Mar

ket

Owne

rSo

urce

of

fina

ncin

g

Supp

ort

rece

ived

from

Men

Wom

en

COOP

AKE

50 t

200

tBr

azilia

n

and

loca

l15

130

Yes

Asi

a, E

urop

eCo

oper

ativ

ePA

DL2

PDA

3

SOTR

IAB

1,00

0 t

2,50

0 t

Braz

ilia

n,

Indi

an,

Euro

pean

3329

8Asi

a, E

urop

e,Afr

ica

Join

t st

ock

com

pany

UTA

SO40

0 t

Loca

l

2018

0

No

Asi

a, E

urop

e

EIG

1

PDA

3 ; Pu

blic

-Priva

te

Part

ner-

ship

UTA

K40

0 t

2018

0Oxf

am

UNIO

N YA

NTA

200

t40

0 t

793

Uni

on

UTA

B40

0 t

600

t31

594

Yes

EIG

1

ANAT

RANS

3,50

0 t

Indi

an50

0Gl

obal

Tra

ding

ECLA

120

t20

0 t

Loca

l10

0No

Asi

a, E

urop

e EC

LA

1)G

roup

emen

td’In

térê

tÉco

nom

ique

2)P

rogr

amm

ed’

App

uia

uD

ével

oppe

men

tLoc

ald

esp

rovi

nces

de

laC

omoé

,Lér

aba

etK

énéd

ougo

u3)

Pro

gram

me

Dév

elop

pem

entd

el’A

gric

ultu

re

15

Table 1.1.4: Traders and their activities

Name of the company

Annual estimated turnover(CFAF/MT)

Cashew-related turnover(CFAF/MT)

Number of employees

Estimated annual sales in tonnes

Intermediary and presence in the country

Target market

Ham Co. 430 250 30 2,500 Yes Ghana, India

Sucotrop 700 400 50 3,500 Yes India

Safcod 650 450 60 3,500 Yes Benin, India

Watan - 500 64 4,000 Yes Inde, Ghana

Table 1.1.5: Policy frame for promotion of the cashew value chain

Sector policyPrice regulation

Export tax raw nuts

Export tax kernels

LabelExchange rate stability

Trade agreements and preferences

No No No No No EURO

United States African Growth Opportunity Act (AGOA)

French Accords de Partenariats Economiques (APE)

West African Economic and Monetary Union (WAEMU)

Economic Community of West African States (ECOWAS)

16

Someoftheagentsinterviewedappearedreluctanttoprovideinformationontheirincomeandcashew-relatedrevenuesandontheircustomers’names.Theyalldealinnotonlycashews

butalsootherlocalproducts,butdonotkeepseparateaccountsonthem.

18 2 Analysis of the Value Chain

2.1 Introduction to the history of cashew production in Burkina Faso

CashewtreeswerenotwellknowntothegeneralpublicinBurkinaFasobeforeindependence.Thefirstplantationswereintroducedaround1960bytheTropical Forest Technical Centre.Cashewtreeswerelongconsideredtobeaspeciesofforestratherthanfruittree,andthenutswereneverreallyharvestedforprofituntiltheProjet Anacarde.TheProjet Anacarde usedseedsimportedfromCasamanceandnorthernCôted’Ivoire.Itlastedfrom1981to1991andwasfinancedbytheFrench Development Agency(FDA)andtheCaisse de Stabilisation des Prix des Produits Agricoles (CSPPA).Inordertoobtainaddedvaluefromthesector,theprojectconductedworkshoptrialsofsimpleprocessingtechniquestoextractthekernelsanddevelopedshellingpliers.Thisledtotheestablishmentofthefirstvillageprocessingworkshop.ThewomenweretrainedtoshellthenutsusingrecycleddrainageoilinwhatwasBurkinaFaso’sfirstexperienceofcashewprocessing.In1997,thegov-ernmentlaunchedacashewsectordevelopmentprogrammewhosegoalwastoplant1,000,000trees.Thishasresultedinaproductionincreasesince2001–2002.Ofthetotaltargetof1,000,000trees,about500,000wereplantedinthewestandsouth-west.

2.2 Illustration of the value chain and marketing

Thecashewvaluechainhasmanyanddiversestakeholders,andtherelationsbetweenthemaretenuous.ThestakeholdersinvolvedinthefivemainlinksinBurkinaFaso’scashewsector(inputs,production,marketing/trading,processingandexport)aredescribedbelow.

Specific inputs

Thislinkappearsattwopointsinthechain:beforetheproduc-tionlink(classicinputssuchasseedsandplants)andaftertheprocessinglink(packaging,materialforprocessingunits,etc.).Growersobtainplants:eitherfromtheDRECVandDPECVnurseriesintheirareas,fromtheINERAstationinBanforaorfromseedlinggrowers;ortheygrowtheseedlingsthem-selves.INERAlaunchedamassselectionprojectforseeds,butlackofresourcespreventeditfromcoveringallareasofproduction.Growersselectseedsthemselvesorinsomecasesbuythemintheborderareas(Côted’IvoireandGhana).Asconcernspackaging,onlycartonscanbeproducedlocally;thebagsneededtovacuumpackkernelsareimported.AnumberofsuppliersinBérégadougou,BanforaandBoboDioulassomanufactureboilers,autoclaves,shellingtables,bladesandAtestadryersforsmallunits.Unitswithmorecapacitytendtogettheirequipmentfromabroad(GuineaBissau,India,Europe).

Production

Aswithmostagriculturalproducts,thislinkcoversthelargestnumberofstakeholders.AccordingtoRGAdata,about45,000householdsinBurkinaFasohavetenormorecashewtrees.Thisonlygivesafairlyapproximateideaoftherealnumberofgrowers,however(onecannotspeakofproductionifthehouseholdhasonly10or16trees).

Ofthe45,000growersreportedtoexistinBurkinaFaso,97%arelocatedinCascades,Sud-Ouest,Hauts-BassinsandCentre-Ouestregions,whichhave17,500,14,220,10,000and2,200growersrespectively.Theplantationsvaryinsizefrom0.5to50ha,withmostbetween2and5haor5and10 ha.Mostcashewgrowersaremembersofvillageassocia-tions,groups,unionsorcooperativesthathavewidelydifferingdegreesofactivity.Growersarenotasyetrepresentednational-ly.Inthepastseveralyears,verylargeplantations(upto300ha)havebeenestablishedbyagrofoodbusinesses.MostoftheseplantationsarelocatedinZiroandSissiliprovinces(Centre-Ouestregion);theirtotalnumberandsurfaceareaisunknown.

Marketing/ trading

Thisisthelinkthatisperhapsleastwellknown.Collecteurs havealwaysworkedasmiddlemen,collectingandtransportingtherawnutsfromtheregionsinwhichtheyaregrowntoGha-na,Côted’IvoireandBenin.Theyalsooffertheirservicestolocalwholesaleexportersofrawnuts,lessfrequentlytoproces-singunits.Thecollecteursalsocomefromneighbouringcountrieswhenthesupplyinthosecountriesfallsshortofdemand.

Therearevariousstakeholders:so-calledpisteurs andcollect-eurs,whoactasmiddlemenbetweenthegrowersandthegroupsofwholesaledealersandexporters;wholesaledealers,whooftenvisitthevillagestobuydirectlyfromthegrowers;nationalexportersandtherepresentativesofinternationalcompanies,whoarelesslikelytovisitthevillages;occasion-alsubregionalbuyers,whousuallycomefromMali,Guinea,GhanaandCôted’IvoiretotopupordersinBurkinaFasoandwhoalsobuyfromscout-agentsandwholesaledealers;occasionalinternationalbuyers,usuallyIndians.

Processing

In2009,processingwascarriedoutmainlyinsixunitsinCascadesandHauts-Bassinsregions.ThelargestcompanyisSOTRIAB,inBanfora,whichhasaprocessingcapacityofabout1,000t.Twootherunitswillbeoperationalin2010:one,basedinBoboDioulasso(Anatrans),istohaveaprocessingcapacityof3,500t;theother,basedinKampti,willbethefirstintheSud-

19 Figure 2.2.1: The stakeholders in the cashew value chain

Ouestregionandwillhaveacapacityof400t.Inadditiontotheseprocessingunits,numerousgroupsofsmall-scaleproc-

essorsas,andmorerecentlyinSissiliprovinceandSud-Ouestregion.

Intrants spécifiques Production Commercialisation Transformation Exportation

Semences sélectionnées localement ou importées

Pépinières privées

Pépinières DPECVa

Pépinière INERAb Banf.

Producteurs individuels

Collecteurs Exportateur d’amandes :Gebana Afrique,

Burkinature

b

Importateurs d’amandes :

Unités de trans-formation sous-

régionalesGrossistes

internationaux

Fournisseurs d’emballages locaux

et internationaux

Équipementierslocaux et internationaux

Exportateurs locaux de noix brutes :

Ets Velegda, SCEO, SUCOTROP, ADI

Products, Hamza et Cie…

Importateurs de noix brutes :Unités de trans-

formation du Bénin, de RCI et du Ghana

Compagnies indiennes

INERA, DRAHRH, DRECV, PADL/CLK, SNV, Helvetas BFd IRSATe, TechnoServe

INADES BFfINADES BFf

MEBF, ACA BF, PDA-GIZ, WOUOL, BKF 012, Gebana Afrique, Anatrans Génèse, SOTRIAB, consultants,

Ecocert, Flo-Cert, Services financiers, iCAg

MEBF, ACA BF, PDA-GIZ, WOUOL, BKF 012, Gebana Afrique, Anatrans Génèse, SOTRIAB, consultants,

Ecocert, Flo-Cert, Services financiers, iCAg

Services des douanes Services des douanes

MAHRH (DGPER, DGPV, DOPAIR, SP/CPSA) MCAPE /ONAC (Fasonorm, Tradepoint)h

CNRST/MESSRSi CNRST/MESSRSi

MCEV CNRST/MESSRSj MEF CNRST/MESSRSk

MACRO

MÉSO

MICRO

Plantation commune(Union Yanta)

Organisations de producteurs

Unité de trans formation : SOTRIAB , UTAB, UTAK, COOPAKE,

ECLA, YANTA (ANATRANS,

UTASO)c

Marché local

Transformatrices artisanales :

Bobo, Orodara, Diéri, Toussiana, Banfora,

Léo, Gaoua…

a)DPECVDirectionProvincialedel’EnvironnementetduCadredeVieb)INERAInstitutdel’EnvironnementetdesRecherchesAgricolesc)SOTRIABSociétédeTransformationIndustrielledel’AnacardeduBurkina;UTABUniondesTransformateursdel’AnacardedeBérégadougou;UTAKUnitedeTransfor-mationdel’AnacardeduKenedougou;UTASOUniondeTransformationdel’Ana-cardeduSud-Ouestd)INERAInstitutdel’EnvironnementetdesRecherchesAgricoles;DRAHRHDirectionProvincialedel’Agriculture,del’HydrauliqueetdesRessourcesHalieutiques;DRECVDirectionRégionaledel’EnvironnementetduCadredeVie;PADL/CLKProgrammed’AppuiauDéveloppementLocaldesprovinces;SNVSociétéNéerlandaisedeDéveloppemente)INADESBFInstitutAfricainpourleDéveloppementÉconomiqueetSocialf )IRSATInstitutdeRechercheenSciencesAppliquéesetTechnologiesg)MEBFMaisondel’EntrepriseduBurkinaFaso;ACABFAfricanCashewAlliance(AllianceAfricaineduCajou);PDA-GIZProgrammeDéveloppementdel’Agriculture/DeutscheGesellschaftfürTechnischeZusammenarbeit(CoopérationTechniqueAlle-mande);WOUOLsignifie«entraidemutuelle»enlanguelocaleTurka;BKF012NaturalResourceManagementintheBoboDioulassobasin,LuxembourgAgencyfor

DevelopmentCooperationProject;SOTRIABSociétédeTransformationIndustrielledel’AnacardeduBurkina;EcocertOrganismedeContrôleetdeCertificationpourl’AgricultureBiologique;iCAInitiativeduCajouAfricainh)MAHRHMinistèredel’Agriculture,del’HydrauliqueetdesRessourcesHalieu-tiques;DGPERDirectionGénéraledelaPromotiondel’EconomieRurale;DGPVDirectionGénéraledesProductionsVégétales;DOPAIRDirectiondel’OrganisationdesProducteursetdel’AppuiauxInstitutionsRurales;SP/CPSASecrétariatPerma-nentdelaCoordinationdesPolitiquesSectoriellesAgricoles;MCAPE/ONACMinis-terduCommerce,del’ArtisanatetdelaPromotiondel’Entreprise/OfficeNationalduCommerceExterieuri)CNRST/MESSRSCentreNationaldelaRechercheScientifiqueetTechnique/Min-istèredesEnseignementsSecondaires,SupérieursetdelaRechercheScientifiquej)MCEVCNRST/MESSRSMinisteredel’EnvironementETDUCadredeVie/CentreNationaledelaRechercheScientifiqueetTechniquek)MEFCNRST/MESSRSMinistèredel’ÉconomieetdesFinances/CentreNationaledelaRechercheScientifiqueetTechnique

Table 2.2.1: Cost structure of dealers in raw nuts (in CFAF)

Cost element Buyer, pisteur/collecteur Dealer, Wholesaler Export company

Purchase price 170 195 205

Misc. costs 12.56 7.5 2475

Transit costs 0 0 60

Cost price 182.56 202.5 289.75

Sale price (FOB) 195 205 305

Margin 12.44 2.5 15.25

Margin as a % of the sale price 6.38% 1.22% 5%

Source: SNV report/survey results

20 Export

Three groups areinvolvedinexportingcashews:ÿ Thefirst comprisesgebanaAfriqueandBurkinature,which

arebasedinOuagadougouandhavechieflyEuropeanclients;theyexportcertifiedproducts(organicand/orfairtrade),especiallywhitekernels.

ÿ Thesecond exportsstandardwhitekernels.Itcomprisesforthemostparttransitagentswhodelivertheoutputoftheprocessingunitstothecustomers;somecustomersbuythekernelsex-worksandarrangefortheirowntransport.

ÿ Thethird groupexportsrawcashewnuts.Itconsistsessentiallyofwholesalers/exportersbasedinBoboandOuagadougouwhoworkwiththecollecteurstostorethenutsanddeliverthemtoportbytheirownmeansorviatransitagents.

Thecustomsservicesprovidethefollowingexportfiguresfor2008:

ÿ rawcashewnuts–netweight:13,523t;value:CFAF1,294,957,386

ÿ whitekernels–netweight:259t;value:CFAF128,570,852

Theharvestseasonlastsaboutfourmonths(JanuarytoMay),buttherawnutsaremarketedallyearlong.Thislinkcom-prisesseveraltypesofstakeholder.Theygenerallydealinlocalproduceand,dependingontheseason,marketcashewsandotherproductssuchaskariteand/orcereals.Theycomeinthreemaincategories:commercialcompanies,localoperatorsandforeignoccasionalplayers.

ThecommercialcompaniesareusuallybranchofficessetupinBurkinaFasobyinternationaltradingcompanies.TheysellthecashewsdirectlytousersandbrokersinEurope,AsiaandAmerica.Theyusuallyhavesubstantialfinancialresources,logisticalmeansandsoundknowledgeoftheinternationalmarket.Theyaresuppliedmainlybylocalwholesalerswho

havesetupshopinsmalltownsintheproductionareaorinmajorurbancentres.Thewholesalersreceiveadvancepay-mentsfromthecompaniestoharvestandmarkettheproducts.Thelocaldealersarewholesalersandarefewinnumber(lessthan15).Theyareknownfortheirsubstantialfinancialre-sourcesandlogisticalmeans.Theycanmarketover1,000tperharvestseasonandemploypermanentstaff.

Theoccasional foreign buyersgenerallycomefromMali,Guinea,GhanaandCôted’IvoiretotopupordersinBurkinaFaso.TheyareusuallyIndianswhodonotbelongtotheexportcom-paniesalreadypresentbutwhotravelthroughBurkinaFasoontheirwaytoCôted’Ivoire.Theyalsobuyfromthepisteursandcollecteurs andwholesaledealers.

Lastly,thepisteurstravelroundtheproductionareasinsearchofnutstofillbuyerorders,andthecollecteursarebasedinthevillages.Theyusuallysupplywholesaledealers,occasionalbuy-ersandexporters.Theyhavetieswithallthoseinvolvedinmarketing.

Thereportonthe SNV sector study calculatedoperatingcostssoastoestablishprofitmarginsandaboveallthecostsgener-atedateachlevel.Thereporttakesaccountofthevarioustypesofstakeholderinvolvedinmarketing(pisteurs,groupsofcol-lecteurs,semi-wholesalers,occasionalbuyers,wholesalersandexportcompanies)andofthevariousoperationstheyconduct.

ThecompaniesexportingstandardcashewkernelstendtobebranchesofinternationaltradecompaniesandareoftenestablishedinneighbouringcountrieslikeCôted’IvoireandGhana.TheysellthekernelsdirectlytousersandtradersinEurope,AsiaandAmerica.Organic/fairtradekernelsareessentiallyproducedforexport,andonlyonecompany,gebana Afrique,hasinvestedintheirexportinBurkinaFaso.ThekernelsareexportedtothecountriesofEurope.

Processing units in Europe, America & Asia

Processing units in Europe, America & Asia

Small-scale processors & processing units in Burkina Faso

Processing units

8%

Collecteurs

91%

90%

ca. 9%

100%Cashew growers

90%

Export white kernels

Export raw nuts

Export white kernels

Local consumption

1%

< 1% < 1% < 1%

9%

90%

9% < 1%

Raw nuts brutes

Kernels

Worldwide consumers Worldwide consumers

Small-scale processors

21

Thefigure belowquantifiesthemarketingchaininBurkinaFaso.Mostoftheoutputisexportedintheformofrawnuts;verylittleisprocessedandconsumedlocally.

Figure 2.2.2: Illustration and quantification of the existing marketing chain

Grower raw nuts Marketing Export trade Export

Sale price/kg of kernels (CFAF) CFAF 170/kg CFAF 195 – 205/kg CFAF 1,470.50 – 2,500 CFAF 2,500 – 3,500

Production and farmgate sales

Middlemen and sales to wholesalers

Collecting and export sales

Loading and export

22

2.3 Description of the cashew production system

BurkinaFasocurrentlyhasabout200haofcertifiedorganiccashewplantationstendedbyfivegroupsofabout160growers.TheplantationsarelocatedinCascadesregionandallthegroupsaremembersoftheWOUOL association.Thegroupshaveonlyonecustomer,UTAB,aprocessingunitsetupinBérégadougou,Comoéprovince,thathasinvestedintheproductionoforganickernels.

Table 2.3.1 on page 23indicatesthetotalnumberofplantsandhouseholdsbyregion(plantationswithmorethan10trees).PhaseIoftheRGAdoesnotconsidersurfaceareasandyield,

butthesecanbeestimatedonthebasisoftwohypotheses:thefirstcalculatesthesurfaceareaontheprincipleof200plants/ha;thesecondestimatesaverageyieldat400kg/ha.Theofficialaverageyield,datingfromtheProjet Anacarde,isestimatedat600kg/ha,butcaution,andthefactthatthefieldsarenowpoorlytended,dictatesanestimatedyieldof400kg/ha.

2.3.1 Water and land factors Likemostagriculturalproducts,cashewsneedrain.Thesocio-culturalcontextdetermineshowtheplantationisrun,althoughanewnationallawwasadoptedonlandtenureinJune2009.

2.3.2 Cashew necessities Seedsarereadilyavailable,butlackofaccesstobankcreditremainsanobstacletoagriculturalinvestment.

2.3.3 Average size and spread of fields Theaverageplantationsizenationwideis2.9ha,withsomeaslargeas100ha.

2.3.4 Yield Nationwideyieldvariesbetweenanaverageof400and600kg/ha.

2.3.5 Harvest and between-harvest period TheharvestseasonrunsfromJanuarytoApril,thebetween-harvestperiodfromMaytoDecember.

2.3.6 Ecological impact of cashew production Usedforreforestation,cashewshelppreservetheenvironmentandsoilfertilitywithouttheneedforpesticides.Therearenostudiesontheenvironmentalimpactofprocessing.

2.3.7 Income and labour distribution by sex Theproductionlinkismadeupessentiallyofmen,whereastheprocessingunitsemploy,asapriorityandforthemostpart,women.

2.3.8 Use of cashew income Incomefromcashewgrowingisusedfirstforfamilyexpenses;later,dependingontheamount,someisinvestedinthefarm.

2.3.9 Relevance of poverty to the farms Dependingonthearea,cashewgrowingisthemainpoverty-reductionactivity.

2.3.10 Membership of grower organisations Therearemanysmallgroupsororganisationsatgrassrootslevelinthevillages,butnonationalcentralorganisation.

Figure 2.2.3: Illustration of the grower, marketing, processing and export price

Table 2.3.1: Total number of cashew trees, households and total output

Region Number of plants Households Surface area (ha) Output (t)

Boucle du Mouhoun 32,115 357 161 64

Cascades 5,561,964 17,575 27,810 11,124

Centre 42,924 122 215 86

Centre-Est 16,640 96 83 33

Centre-Nord 2,958 34 15 6

Centre-Ouest 256,859 2,217 1,284 514

Centre-Sud 17,838 183 89 36

Est 11,139 144 56 22

Hauts-Bassins 2,849,241 10,065 14,246 5,698

Nord 2,902 38 15 6

Plateau Central 558 14 3 1

Sahel 1,328 11 7 3

Sud-Ouest 4,367,761 14,220 21,839 8,736

Burkina Faso 13,194,223 45,076 65,821 26,328

Sources: preliminary results of the RGA: Phase 1/calculations

23

Figure 2.3.1: Map of cashew-growing areas in Burkina Faso

Theprimeregionsecologicallyforcashewsaretherefore:Cascades,Sud-Ouest,Hauts-BassinsandCentre-Ouest,inparticularZiroandSissiliprovinces.

Table 2.4.1: Cashew products and target market

Product Market

Standard fresh kernels Regional and international market (Ghana, Côte d’Ivoire, Asia, Europe, United States, Canada)

Certified organic fresh kernels

International market (Europe)

Roasted kernelsNational, subregional and international market

Cashew paste National and subregional market

Caramel Local market

Shell and kernel oils Being tested

Soap Local market

Table 2.4.2: Overview of processing units

Name of processing factory

Current processing capacity in

tonnes raw cashew

nuts

Potential processing capacity in

tonnesraw cashew

nuts

Technologies used

EmploymentServices

provided to growers

Market Owner

Source of financing

Support received

fromMen

Wom-en

COOPAKE 50 t 200 tBrazilian and local

15 130

Yes

Asia, Europe

Cooper-ative

PADLPDA

SOTRIAB 1,000 t 2,500 tBrazilian,

Indian, European

33 298Asia,

Europe,Africa

Joint stock

company

UTASO 400 t

Local

20 180

No Asia, Europe

EIG

PDA

UTAK 400 t 20 180 Oxfam

UNION YANTA 200 t 400 t 7 93 Union

UTAB 400 t 600 t 31 594

Yes

EIG

ANATRANS 3,500 t Indian 500Global

Trading

ECLA 120 t 200 t Locale 100 NoAsia,

EuropeECLA

24

ThecashewsareprocessedessentiallyinHauts-BassinsandCascadesregions.Womenplayanimportantpart,eitherassmall-scaleprocessorsorasworkersintheprocessingunits.Therearevariousproducts,eachonewithitsmarket,as set out below.

Small-scaleprocessingistheworkofwomeneitherasindivid-ualsororganisedinassociations.Thewomenobtainthenutsdirectlyfromthegrowers.Themainstepsinsmall-scaleprocess-ingare:heatembrittlementusingdrainageoilorsteam;shelling,orkernelextraction;peelingandcooking;seasoning.Thewomenperformeverystepoftheprocess.Thetechnologyusedisbasic.

Thewhiteorblanchedandseasonedkernelsaresoldonthemarketingrowingareastopackagersfromthebigtownsortoprocessingcompaniesanddealersthatexportthem.Locallysoldwhitekernelsaresubsequentlycookedbyotherwomenwhosupplythesamemarketsasthesmall-scaleprocessors.

Therearetwotypesofprocessingunit:semi-skilledandsemi-industrial.Thesemi-skilledunitsusefewmachinesandlocallymanufacturedmaterial.Thesemi-industrialunitsusesomefairlyadvancedtechnologyimportedfromthecountriesoftheNorth.TherawnutsareboughtfromgrowersorcomefromplantationsrentedfromtheStatewitharightofuseforthenuts.Thetable belowgivesanoverviewofindustrialprocess-inginBurkinaFaso.

2.4 Detailed description of cashew processing

25 Processingunitsusealmostthesameprocessasthesmall-scaleprocessors.Thedifferencesaretobefoundinthemate-rialemployed.Forexample,whereasthesmall-scaleproces-sorsembrittlethenutsinpots,thesemi-industrialunitsusevatsconnectedtoboilers.Theyshellthenutsusingsemi-mechanicalshellersthatarehandorhand-and-footoperated.Theyuseovensfordrying,butapplythesameapproachtopeeling.Sortingandweighinghavebeenautomatedinsomeunits.Theunitsemploybetween40and500workers;over90%arewomen,whoshell,peel,sortandpackagethekernels.Thewomenreceivepieceworkremunerationinlinewiththeiroutput.

Thereisarelativelywidegapbetweentheoreticalprocessingcapacityandrealoutput.Thereasonsare:therelativeinabilityoftheprocessorstofinanceproduction;poormasteryofop-timumproductiontechniques;littlecapacitytoprospecttheinternationalmarket.

Onlyoneunit–UTAB,inBérégadougou–hasenteredintotheproductionoforganickernels,anditsoutputisestimatedatnearly100t.Ithasonlyonecustomer,theexportcompanygebanaAfrique,inOuagadougou.ThetwobiggestunitsareUTABandSOTRIAB.

RecapitulationoftheprocessingindustryinBurkinaFaso:

2.4.1 Structure of the industry Theprocessinglinkcomprisesalargenumberofsmall-scalewomenprocessorsandsemi-industrialunits.Mostaremicroandsmallbusinesses(lessthan500t/year),exceptSOTRIAB(1,000t/year)and ,whichhasannouncedaneventualcapacityof3,500t/year.

2.4.2 Geographical distribution of processing units throughout the country

TheunitsareconcentratedinCascadesandHauts-Bassinsregions.

2.4.3 Market leaders and their market TheWOUOLnetworkandSOTRIABarethenationalleadersintermsofoutputandtechnique.

2.4.4 Ownership MostoftheunitsbelongtoEIGssuchasSOTRIABorjointstockcompanies.SOTRIABisalsoajointstockcompany.

2.4.5 Processing capacity Thepotentialprocessingcapacityoflocalunitsvariesfrom50to3,500tofrawnutsperyear.

2.4.6 Employees Mostoftheemployeesarewomen;staffsizevariesbetween100toover600people.

2.4.7 Technology used ThetechnologyisIndian,BrazilianandEuropeaninoriginbutisheavilyadaptedonsite.

2.4.8 Cooperation between units and growers Thegrowersusuallyhavetieswithunitsintheirareas.

2.4.9 Strategy for guaranteeing supply Suppliesareprovidedontrustandoralcontracts,butarealsorelatedtocollecteuropportunities

2.4.10 Strategy for guaranteeing quality Certainunitshavequalityagentsandprefercertaingrowingareas.

2.4.11 Processors’ experiences of cooperation with growers

Good,butalsosomebadexperiencesofcommitmentsnotkept.

2.4.12 Logistics, transportation and marketing InternationallogisticsfirmssuchasBOLLOREandMAERSKarehiredtotransporttheproductstotheports.

2.4.13 About gender and processing Theunitscompriseanoverwhelmingmajorityofwomenworkers.Womenaccountformorethan90%oflabourinthesector.

2.4.14 Economic evaluation of sustainability, competitiveness and scope for expansion

Thereissizeablescopeforexpandingprimaryandsecondaryproduction,andtheoptimalprocessinglevelhasyettobeattained.Atthesametime,alargepartoftheglobalmarketremainsaccessible.

MICRO

Input supplier Production Processing Export

ÿ variety recognition test

ÿ a greater number of competitive varieties

ÿ varietal research

ÿ training: growing techniques, plantation maintenance, harvesting and storing nuts

ÿ supplies of equipment (saws, pliers and jute bags)

ÿ support for harvest onset activities

ÿ training in management, contract performance

ÿ training in market prospection

ÿ training in leadership, negotiation and lobbying

ÿ harmonisation of means of acting on the production link

Training in maintenance

ÿ training in management tools and processing techniques

ÿ training in quality standards

ÿ support for the con version of by-products

ÿ training in the establishment of business plans

ÿ support for formalisation and structuring

ÿ training in advocacy and lobbying

ÿ establishment of guarantee funds for loans

ÿ promotion of joint packaging – harmonisation of means of acting on the production

ÿ structuring (certification process)

ÿ introduction of export certification

ÿ promotion of joint packaging

ÿ heightened awareness of the quality approach

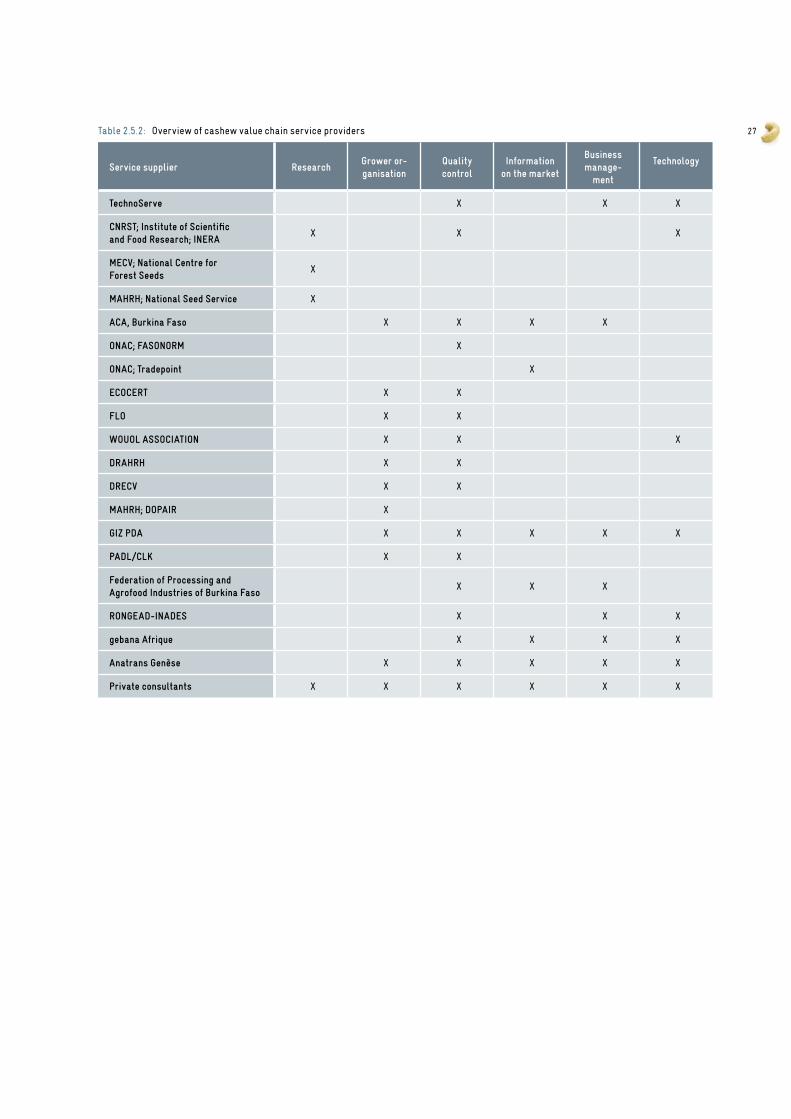

26 2.5 Analysis of value chain service providers

2.5.1 Overview of value chain service providers

InBurkinaFaso,oneofthebiggestchallengesfacinggrowersistoimproveyields.Thismeansmasteringpreandpost-harvestproductiontechniques.Varietalresearchisneededandseedsmustbemadeavailable.Inthecurrentcontext,inwhichthereareenoughplantations,anewvarietycanbeintroducedusinggraftingtechniques.Inordertocontrolcosts,andgiventhatthecontextismoreorlessthesamethroughoutthesubregion,varietalresearchshouldbeconductedtogetherwithothercountries.Masteringcropmanagementalsoimpliesathoroughgroundinginproductionequipment.Trainingkitsshouldgohandinhandwiththeoreticalandpracticaltraining.

Growersandprocessorsmustbeinstructedinoutputcontrol,managementtechniquesandmarketresearch,forthosearetheskillstheyneedtopenetratemarkets,especiallythehighlydemandingexternalmarket.

Theconceptofexportcertificationappliesinthemediumtermandrequireswork.Itinvolvesconcertedactionbyandunder-standingbetweenthestakeholders,whohavetoadoptbetterstructurestodefendtheircommoninterests.

Themainquestionatthemesolevelistheintegrationofservicesintothesector,withaviewtoprofessionalisingtheplayersandtoreachingtheminlargenumberseasilyandrapidly.Trainingaidsmustbepooled.Thisdoesnotnecessarilymeanthatallaidshavetobesystematicallyretooledtobeidentical,butratherthattheyshouldcomplementeachotherandthattrainingapproacheshavetobestandardised.

Thetable 2.5.2 on page 27providesanoverviewofcashewvaluechainserviceproviders.

Table 2.5.1: Evaluation of the need for services among the value chain’s stakeholders

Table 2.5.2: Overview of cashew value chain service providers

Service supplier Research Grower or-ganisation

Quality control

Information on the market

Business manage-

ment

Technology

TechnoServe x x x

CNRST; Institute of Scientific and Food Research; INERA

x x x

MECV; National Centre for Forest Seeds

x

MAHRH; National Seed Service x

ACA, Burkina Faso x x x x

ONAC; FASONORM x

ONAC; Tradepoint x

ECOCERT x x

FLO x x

WOUOL ASSOCIATION x x x

DRAHRH x x

DRECV x x

MAHRH; DOPAIR x

GIZ PDA x x x x x

PADL/CLK x x

Federation of Processing and Agrofood Industries of Burkina Faso

x x x

RONGEAD-INADES x x x

gebana Afrique x x x x

Anatrans Genèse x x x x x

Private consultants x x x x x x

27

Table 2.5.3.: Overview of the organisation of financial support for agricultural activities

Name of the financial institution Target group ProductExperience in the cashew sector

Regional Solidarity BankDealers Processors

Seasonal creditInvestment credit

UTASO, SOTRIAB, UTAK, UTAB

Banque Agricole et Commerciale du Burkina Dealers Processors Growers

Seasonal creditInvestment credit

No

National Federation of Credit Unions of Burkina Faso

Banque Commerciale du Burkina Dealers, Processors, Growers

Bank of Africa

Dealers Processors Growers

Seasonal creditInvestment credit

Sahel-Sahelian Bank for Investment and Commerce

ECOBANK

Banque internationale du Burkina (United Bank of Africa group)

28 2.5.2 Overview of cashew value chain financial service providers

Oneofthesector’smaindifficultiesremainsaccesstofinanc-ing.Processorsstarteachseasonwithlessandlessoperatingfunds,oftenbecausetheyhavedifficultyrepayingexistingloansorbecausethefinancialinstitutionshavelittleinsightintoagriculturalactivities.Thebankswillingtograntsuchloansarefewandfarbetween.Investmentcreditseemsmorereadilyavailable,becausetheequipmentconstitutesaformofcollateral,buthereagain,veryfewbanksarewilling.

Themaindifficultyfacinggrowersistoobtainseasonalcreditenablingthemtotendtheirplantationsandharvestthenuts.OneofthefewfinancialinstitutionswillingtoprovidesuchcreditistheNational Federation of Credit Unions of Burkina Faso.Thebigproblemhereistheavailabilityofguaranteefundsforgrowers.Thesameproblemarisesfororganisedgroupssuchasgrowerorganisationsthatwanttobuytheirmembers’outputinordertoresellit.

Thereareseveralexamplesofbestpracticeamongthefinan-cialinstitutions.TheRegional Solidarity Bank,forexample,partiallyfinancedtheestablishmentofunitssuchasthenewUTASOandUTAK.BothunitsarenetworkedwiththeWOUOLAssociation in Bérégadougou,whichhasfouryearsofexperienceincashewprocessing.UTASOwasf inancedaspartofapublic-privatepartnershipbetweenthePDA,theexportcompanygebana Afriqueandtheowneroftheprocessingunit.Itreceivedsupportforthesubmis-sionofafinancingrequesttothebank,whichapprovedthe

requestandprovidedCFAF30millionfortheconstructionofabuildingandsomeoftheequipment.Theunit,whichhasatheoreticalcapacityof400tofrawnuts,shouldbeoperationalverysoon.

UTAKreceivedthesameamountforconstructionandequip-ment.Therepaymentperiodisthreeyearsandtheinterestrate11%.Eachoftheseunitsaimstoimprovetheincomeofabout200people,90%ofwhomarewomenwithinthefirm,andtoobtainsuppliesfromanetworkofonethousandloyalgrowerswhoseincomeandproductioncapacityaretherebyalsoimproved.Thisexamplecanbeusedtoappreciatethemean-ingofatrueprivateinitiativeandtoreviewcertainmodesoffinancingusedbytheprocessingunitswhennegotiatingwiththebanks.

ThepartnershipbetweentheNGO GenèseandGlobal Trading,whichcanbeconstruedasforeignfinancing,isinfactcon-ductedwithlocalbanksandfacilitatedtheestablishmentofAnatrans,whichistheindustrialarmofGenèseandhasanannouncedcapacityof3,500tperyear.AnatransisajointventurebetweenGlobal TradingandtheformerBurkinabefirmSOPRAL.Itisbuildingaprocessingunitwithastoragewarehousethatcancontain3,500tofcashewnuts.Inthemeantime,Anatransbuysrawnutsfromthegrowersunderitswingsandsendsthemtofactoriesinneighbouringcoun-tries.Genèsetakescareoftrainingandprovidessupportforgrowerorganisationandcapacitybuilding.Global Tradingisengagedinapublic-privatepartnershipwithGIZwithregardtothecapacity-buildingaspect.

Table 2.6.2: National policy affecting value chain performance

Policy Description Implication for the value chain

Rural Development Strategy (SDR, 2003)

Burkina Faso’s vision with regard to: greater food security, higher revenues in rural areas, sustainable management of natural resources and stakeholder accountability.

Any strategy promoting the cashew sector must be aligned with the SDR objectives.

Sector Programme for Productive Rural Development

Programme arising from the Paris Declaration on harmonisation and alignment. It is to lead to a Medium-Term Expenditure Framework aimed at a shared basket so as to make support more efficient and effective.

Close cooperation between the technical and financial partners and harmonisation of approaches.

Coordination Framework for Rural Development Partners

Coordination framework for rural development partners based on key sector issues (financing, sector, action); priority of the Strategic Poverty-reduction Frame.

Close cooperation between the technical and financial partners and harmonisation of approaches. Common programme.

29 2.6. Institutional and policy governance chain

In1991BurkinaFasoembarkedonafar-reachingprogrammeofeconomicreformaimedatlayingthegroundworkforafree-marketeconomyinwhichtheprivatesectorwouldbethemainengineofgrowth.Themeasurestakentofulfilthatobjectiveare:

ÿ reformoftheagriculturalsector,notablybyredefiningtheroleoftheStateandadoptingastrategicorientationdoc-ument,astrategicoperationalplanforthedevelopmentoftheagriculturalsector(plantproduction)andaplanofactionandprogrammeofinvestmentinanimalhusbandry;anoil-seedcropactionplanwasalsodrawnup;

ÿ promotionoftheprivatesectorthrougheconomicliber-alisation(improvedregulatory,legalandcorporatetaxframework,adoptionofanindustrialdevelopmentstrategy,adoptionofatradesdevelopmentstrategy,etc.);

ÿ measurestoeasethebusinesstaxburdenontheformalsector;

ÿ theadoptionoftheInvestmentCode,whichisintendedtopromoteproductiveinvestmenttofurtherBurkinaFaso’seconomicandsocialdevelopment;advantagesrelatingto

businesscreation,investmentandoperationaregrantedtobusinessesrequestingthem;

ÿ intermsofexportpolicy,a2003studyfinancedbytheJoint Integrated Technical Assistance Programme (JITAP) forlessdevelopedandotherAfricancountries,onthede-velopmentofasectorstrategytodevelopandpromoteexportsandanationalexportmarketingplanforsesame,karite,groundnutsandcashewsinBurkinaFaso.Thisstrategy,whichisimplementedbyONAC,hasprovidedfreshmomentumoverallfortheoil-seedplantsector,whichincludescashews.

Giventhemanydimensionsofprivatesectordevelopment,thegovernmentoptedforaglobalstrategyreconcilingneedsforstructuralreformandeconomicrecoverywithaviewtobusinesscompetitiveness.Thoseprinciples,whichunderpineconomicpolicyonprivatesectorpromotion,strivetopro-moteeconomicgrowthandenhanceincomedistributionforlastingsocialstability.

Sincetheliberalisationoftheoil-seedproductsector,theexportofcashewnutsandkernelsisnolongertheobjectofspecialattentiononthepartofthecustomsservices.

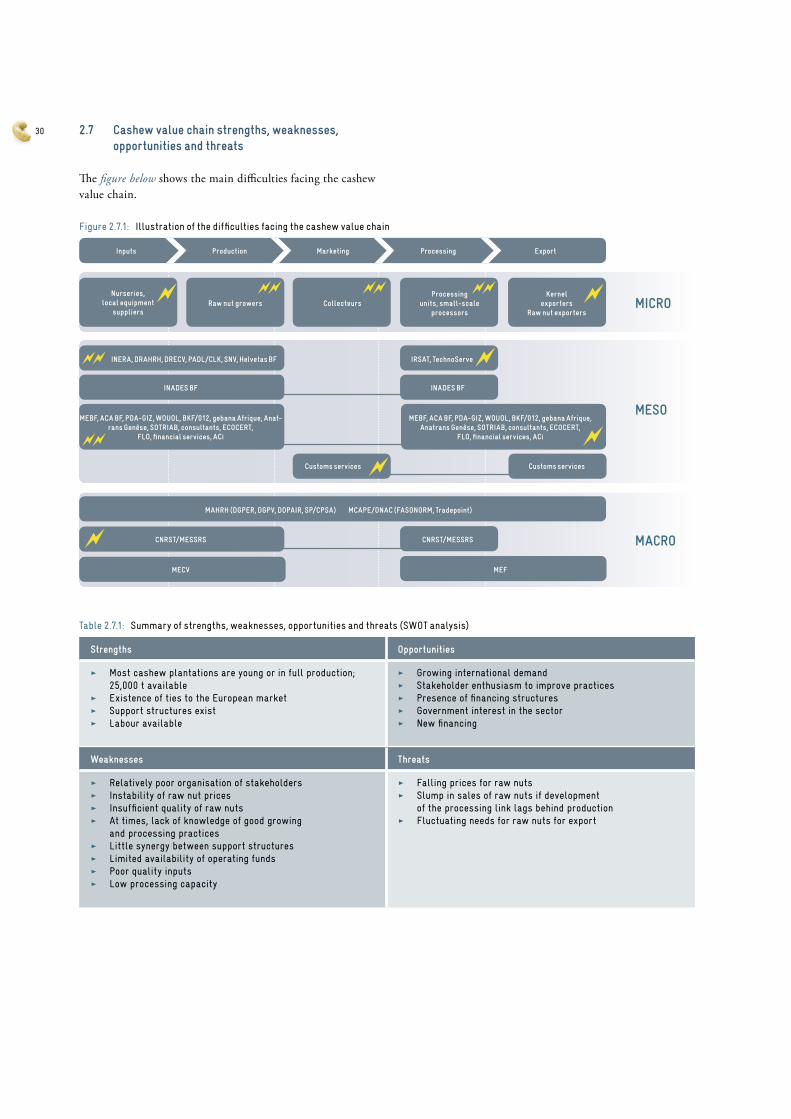

Table 2.7.1: Summary of strengths, weaknesses, opportunities and threats (SWOT analysis)

Strengths Opportunities

ÿ Most cashew plantations are young or in full production; 25,000 t available

ÿ Existence of ties to the European market ÿ Support structures exist ÿ Labour available

ÿ Growing international demand ÿ Stakeholder enthusiasm to improve practices ÿ Presence of financing structures ÿ Government interest in the sector ÿ New financing

Weaknesses Threats

ÿ Relatively poor organisation of stakeholders ÿ Instability of raw nut prices ÿ Insufficient quality of raw nuts ÿ At times, lack of knowledge of good growing

and processing practices ÿ Little synergy between support structures ÿ Limited availability of operating funds ÿ Poor quality inputs ÿ Low processing capacity

ÿ Falling prices for raw nuts ÿ Slump in sales of raw nuts if development

of the processing link lags behind production ÿ Fluctuating needs for raw nuts for export

30 2.7 Cashew value chain strengths, weaknesses, opportunities and threats

The figure belowshowsthemaindifficultiesfacingthecashewvaluechain.

Figure 2.7.1: Illustration of the difficulties facing the cashew value chain

MACRO

MESO

MICRO

Inputs Production Marketing Processing Export

Nurseries, local equipment

suppliersRaw nut growers Collecteurs

Processing units, small-scale

processors

Kernel exporters

Raw nut exporters

INERA, DRAHRH, DRECV, PADL/CLK, SNV, Helvetas BF IRSAT, TechnoServe

INADES BF INADES BF

MEBF, ACA BF, PDA-GIZ, WOUOL, BKF/012, gebana Afrique, Anat-rans Genèse, SOTRIAB, consultants, ECOCERT,

FLO, financial services, ACi

MEBF, ACA BF, PDA-GIZ, WOUOL, BKF/012, gebana Afrique, Anatrans Genèse, SOTRIAB, consultants, ECOCERT,

FLO, financial services, ACi

Customs services Customs services

MAHRH (DGPER, DGPV, DOPAIR, SP/CPSA) MCAPE/ONAC (FASONORM, Tradepoint)

CNRST/MESSRS CNRST/MESSRS

MECV MEF

Table 2.8.1: Players helping to promote the cashew value chain

Programme/project/ organisation

Main partners (govern-ment, NGO, donors)

Geographical area Main activities to promote the cashew value chain Remarks

PDA GIZSud-Ouest and Est regions

ÿ Production ÿ Processing ÿ Marketing ÿ Support for initiatives intended to improve

the circulation of information among private and public players

Supports ACi

PAMER NGO

Hauts-Bassins, Cascades, Boucle du Mouhoun, Est and Centre Est regions

ÿ Support for processing micro-enterprises in the form of training and advice intended to build capacity and improve ties to other links in the chain

MEBF NGO Nationwide ÿ Facilitate access to business support

services available on the market

BAME Bobo Dioulasso ÿ Production ÿ Processing ÿ Marketing

SNV ÿ Support for stakeholders at all links in the

form of training, advice on organisational and institutional capacity building

PADL/CLK ÿ Support (training, advice) for input suppliers

and growers

Christian Relief and Development Organisation (Organisation Chrétienne de Secours et de Dévelop-pement) CREDO

NGOSissili and Ziro provinces

ÿ Support for all links in the chain

ECOCERT ÿ Specialised in organic/fair trade certification

INADES

NGO, food sovereign-ty, fair trade

ÿ Training ÿ Peasant communication ÿ Support for control of agricultural sectors ÿ Organisation ÿ Structuring of the rural world ÿ Market access ÿ Technical capacity building ÿ Financing in the rural world ÿ Work to influence policies

31 2.8 Overview of organisations helping to promote the cashew value chain in Burkina Faso

SeveralNGOanddonorinitiativesandprogrammesareintendedtopromotethecashewsector,ruraldevelopmentorruralmicro-businesses.Cooperationbetweenthevarious

programmesandprojectscancreatesynergyandfosterde-velopmentofthecashewvaluechain.The table belowgivesanoverviewofthemostextensiveprojectsandprogrammes.

34

ÿ thelegalvacuumandabsenceofregulatoryprovisionsinrespectofagriculturalsectors;

ÿ poorcoordinationbetweenindirectplayers:supportstructuresactingonthevaluechainhavenoframeofreferenceforcoordinationamongthemselvesorwiththestakeholders;theresultingincoherentactioncaninturnhavenegativerepercussionsonsectorperformance;

ÿ growerunawarenessoforfailuretousecropmanagementtechniquesandlackoftechnicalguidanceforstakehold-ers(i.e.,thesequenceofoperationsapplicabletocashewtrees;thetechniqueforregeneratingplantationsviaprun-ing;theapplicationoforganicmanure;failuresystemati-callytoclearscrubfromtheplantations,whichoftenresultsinbushfiresthataredetrimentaltothequalityofsurvivingnuts;thepoorpost-harveststorageconditionsofnutsbygrowersandwholesaledealers;lackofknow-ledgeandknow-howaboutprotectingplantationsfromphytopathologiesandparasites;thelowproductivityofthevarietiesused;problemsofaccesstosuitableinputsandequipment;failuretomakeproductiveuseofby-products;thestakeholders’poormanagementcapacity);

ÿ theinabilityofnationalstakeholderstoearnremunerativepricesbecausenutsfromplantationsinBurkinaFasoareconsideredsmallbythemajorinternationalbuyers(thesizealsoinfluencesthesizeandweightofthekernelsobtained);

ÿ lackofsteamembrittlementequipmentamongsmall-scaleprocessors;

ÿ thestakeholders’failuretoincorporatequalityasagoal;ÿ problemsofaccesstoappropriatepackagingmaterials;ÿ slumpingsalesandpoorcirculationoftradeinformation.

3 Recommendations

TheentirecashewvaluechaininBurkinaFasocurrentlysuf-fersfromanumberofinformationgaps.Asconcernsgrowers,reliabledataismissingoneconomicpotentialandproductionfigures(realsurfaceareaofplantations,treeproductivitybyagroecologicalarea).Whenitcomestotradeandexport,theflowofnutsfromorleavingneighbouringcountriesisuncon-trolled,bothintermsofquantityandquality.Likewisetheturnoverofdealersandexportersandtheirexactnumberremainunknown,aboveallbecauseoftheinformalnatureofthesector.

Table 3.1: Missing information

Value chain stakeholders

Missing information

Growers

ÿ Plantation surface area ÿ Productivity of trees by agroecological

area ÿ Qualitative typology of products by

agroecological area ÿ Characteristics of existing varieties

and their performance

Processing industry

ÿ Ecological impact of processing (water consumption, energy, roads, environmental impact)

Dealers and exporters

ÿ Flow of nuts from or leaving neighbouring countries

ÿ Number of dealers

Lastly,activitiesintendedtosupportthecashewvaluechaincouldtacklethefollowingshortcomings:

ÿ thestakeholders’lackoforganisation,whichisanim-pedimenttocoordinationandtodecisionsandactiononsharedmeasuresonpricesandmarketentryandexitconditions;

36 List of Acronyms

ACA AfricanCashewAlliance

ACI AfricanCashewinitiative

AGOA AfricanGrowthOpportunityAct

BAME Officeforthepromotionofmicro-enterprises

BKF/012 NaturalResourceManagementintheBoboDioulassoBasin,LuxembourgAgencyfor

DevelopmentCooperationproject

CFAF FrenchCommunityofAfricafranc

CNRST NationalCentreforScientificandTechnicalResearch

CREDO ChristianReliefandDevelopmentOrganisation

DGPER GeneralDirectorateforthePromotionoftheRuralEconomy

DGPV GeneralDirectorateforPlantProduction

DOPAIR DirectoratefortheOrganisationofGrowersandforSupportforRuralInstitutions

DPECV ProvincialDirectoratesfortheEnvironmentandEnvironmentalLivingConditions

DRAHRH RegionalDirectoratesforAgriculture,WaterandHalieuticResources

DRECV RegionalDirectoratesfortheEnvironmentandEnvironmentalLivingConditions

ECLA Êtrecommelesautres,cashewprocessingunit

ECOCERT Controlandcertificationbodyfororganicproduce

EIG EconomicInterestGrouping

FASONORM DirectorateforStandardisationandQualityPromotion

FLO FairtradeLabellingOrganisationsInternational

FOB Freeonboard

GDP Grossdomesticproduct

GIZ DeutscheGesellschaftfürTechnischeZusammenarbeitGmbH

ha hectare

INADES AfricanInstituteforEconomicandSocialAdvancement

INERA InstituteontheEnvironmentandAgriculturalResearch

IRSAT InstituteofResearchinAppliedScienceandTechnology

37 MAHRH MinistryofAgriculture,WaterandHalieuticResources

MCAPE MinistryofCommerce,TradesandBusinessPromotion

MEBF Maisondel’EntrepriseduBurkinaFaso

MECV MinistryoftheEnvironmentandEnvironmentalLivingConditions

MEF MinistryoftheEconomyandFinance

MESSRS MinistryofSecondaryandPost-secondaryEducationandScientificResearch

MT Metrictonnes

NGO Non-governmentalorganisation

ONAC NationalExternalTradeOffice

PADL/CLK ProgrammetoSupportLocalDevelopment/Comoé,LérabaandKénédougouprovinces

PAMER RuralMicro-enterpriseSupportProject

PDA AgriculturalDevelopmentProgramme

RGA GeneralAgriculturalCensus

SNV NetherlandsDevelopmentOrganisation

SOTRIAB BurkinaFasoIndustrialCashewProcessingCompany

SP/CPSA PermanentSecretariat,CoordinationofAgriculturalSectorPolicies

t Tonnes

UTAB UnionofBérégadougouCashewProcessors

UTAK KénédougouCashewProcessingUnit

UTASO Sud-OuestCashewProcessingUnit

WOUOL "mutual aid"inthelocalTurkalanguage

38

Notes

ÿ Rapport de l’atelier sur la promotion des chaînes de valeur ajoutée de la filière anacarde (NasserKankoudry,OusmaneDjiba,PhilippeConstant),PDA–GIZ,May2008.

ÿ Diagnostic de la filière anacarde au Burkina Faso pour une analyse des chaînes de valeur(NasserKankoudry),PDA–GIZ,April2008.

ÿ Study of the cashew value chain in Burkina Faso;SNV,July2006. ÿ Recensement général d’agriculture: résultats préliminaires, Phase 1;MAHRH,2008. ÿ Market study of the dynamics of the output of cashew nut processing in the area;coveredbyPAMER. ÿ Report on the study of the organisation of growers in four sectors;PDA,May2007.

Annex I : Documentation

39

Published by:

Deutsche Gesellschaft fürInternationale Zusammenarbeit (GIZ) GmbH

International Foundations

Postfach 518065726 Eschborn, Germany