analysis of the potential for cultivation of fruit and ...ime.bg/var/images/horticulturebg.pdf ·...

TRANSCRIPT

INSTITUTE FOR MARKET ECONOMICS

2012

Analysis of the potential

for cultivation of fruit

and vegetables in

Bulgaria

P U B L I S H E D W I T H T H E S U P P O R T O F “ A M E R I C A F O R B U L G A R I A ” F O U N D A T I O N

Purpose of the study

The purpose of this study is to identify the perspective crops in the vegetable- and fruit-growing

sectors from the viewpoint of domestic demand and export potential.

Methodology

To determine which crops hold the greatest potential, we use two main indicators:

1) Domestic demand – the quantity of domestic demand is based on data of household

consumption and the demand of food processing companies. To minimize the possible

weaknesses of such data compilation, we use information for aggregate demand (production

+ import - export),

2) Export demand – taking into account that the greater part of the export of fruit and

vegetables (84% in 2011) is to other EU member states’ markets, we use data on the import

of fruits and vegetables in EU

We observe the dynamics of household consumption, the demand of raw materials in the processing

industry and the import of fresh fruits and vegetables for 10-year period (2002-2011), while also

considering the compound annual growth rate (CAGR). We analyze the crops that mark a positive

growth, could be cultivated in Bulgaria (in accordance with the environmental and climate

conditions) and their produced quantity is more than 1000 tons or BGN 1 mil. in net value. To

determine whether the Bulgarian producers have competitive advantage in growing these crops, the

formula for revealed competitive advantage RCA1, is applied. The RCA refers to the foreign trade

position of the country for the particular goods in comparison to its general foreign trade standing.

The crops with growth potential are identified as such based on examined demand increase on

domestic and EU market and on competition coefficient greater than zero, derived through the RCA

formula. In the matrix below the crops with better perspectives are placed it the upper right part of

the graph, while those with low or none potential are in the bottom left corner. An exemplary matrix,

complied this way, would look like this:

1 The applied in the study formula for RCA is developed by CPAII, 1998 and used by ITC 2000, as well as in the research project “Are the Mediterranean countries competitive in fresh fruit and vegetable exports?”, Nilsson, Fredrik O.L. Lindberg, Emma Surry, Yves R, Department of Economics, Swedish University of Agricultural Sciences, 2006.

-80,0%

-60,0%

-40,0%

-20,0%

0,0%

20,0%

40,0%

-10,0% -5,0% 0,0% 5,0% 10,0%

Introduction

The vegetable- and fruit-growing industries are going through a severe crisis in the last decade. For

the 2002-2011 period the production value of these two sectors has plummeted by more than 60%

at base prices. Their share in crop production and in agriculture as a whole decreases by 76% and

73% respectively. For the same time period, the land cultivated with vegetables dropped down by

61% and the land with perennial crops (fruit trees without vineyards) decreased by 30%. The

domestic production is insufficient to meet demand and this has turned the country from net

exporter to net importer of fruits and vegetables.

The neighbouring Turkey and Greece, where the warm weather lasts much longer, allows the import

of particular crops at lower prices for longer time periods during the year. This possibility, however,

pressures the Bulgarian production to either expand or to specialise in the areas of competitive

advantage.

In the last couple of years we observe retention in the land, used for some. We also observe

investment in new fruit plantations and slight increase in output. Although it is too soon to discuss

breaking the negative trend, the sector is at an important crossroad. In this context, this study might

be valuable in determining the crops with greater development perspective in the country.

Traditionally cultivated crops

Among the most widespread vegetables today, most of them are relatively recently brought to

Bulgaria’s market. Potatoes, tomatoes, pepper, beans and spinach have started to be cultivated on a

large scale less than 150 years ago. Cultures such as turnip, carrot, onion, garlic, cabbage, lentils,

peas, broad beans and cucumber have been grown for thousands of years on Bulgarian soils.

From the traditionally cultivated fruits most popular is the cultivation of plums, apples, peaches,

cherries, and in the past – mulberries.

The weather conditions in the country are suitable for cultivation of some unconventional fruits, such

as the kiwi for instance.

Domestic market

Three main factors influence the demand for fruits and vegetables for direct consumption or for

processing:

Seasonal – related to quantity and quality of the crop

Economic – related to the real disposable income of the population

Consumer habits – they change rather slowly but could considerably alter the structure of

the food demand.

Fruits

Household consumption

According to National Statistical Institute (NSI), the household consumption of fruits and vegetables

has increased for the 2002-2011 period. Despite the weaknesses in the household budgets research

study, it still provides a picture of the general tendencies in consumers’ attitudes.

The main conclusions to be drawn in relation to the fruit consumption are the following (see Graph

1):

The traditional for Bulgaria fruits such as grapes, pears, watermelons give way to the

southern and citrus fruits

Among the traditional fruits in the country, only apples score steady growth

If we check the information on household consumption with the data for production and

import, we observe an increase in the consumption of peaches, cherries, strawberries, kiwi

and some sorts of nuts (walnuts and almonds)

Regarding the preserved goods, the consumption of fruit juices has increased more than two

times for the last ten years. However, the consumption of jam and marmalade decreases.

Graph 1 – Household consumption of fruits

Source: NSI

An explanation of the results might be found in the increase of the purchasing power of the

population in the last ten years and in the widening accessibility to fruits and nuts, which in the past

were missing from the Bulgarian market or were too expensive.

Apples, cherries, peaches, nuts (walnuts, almonds) and kiwi are outlined as perspective for the

Bulgarian producers.

123,1% 117,6%

64,1%

50,0%

0,0% -14,3% -15,0% -23,9% -26,7% -31,3% -33,3%

Sou

ther

n fr

uit

s

Juic

es a

nd

syr

op

s

Ap

ple

s

Oth

er f

ruit

s

Nu

ts

Pe

ars

Mel

lon

s an

d w

ater

mel

lon

s

Can

ned

fru

its

Gra

pes

Pu

mp

kin

s

Jam

s an

d m

arm

alad

es

Household consumption change, 2002 - 2011

The data on household consumption does not reflect the factor of “private production”. Hence, the

increased consumption of some fruits might be attributed to deliveries by someone different from

industrial production (like family gardening).

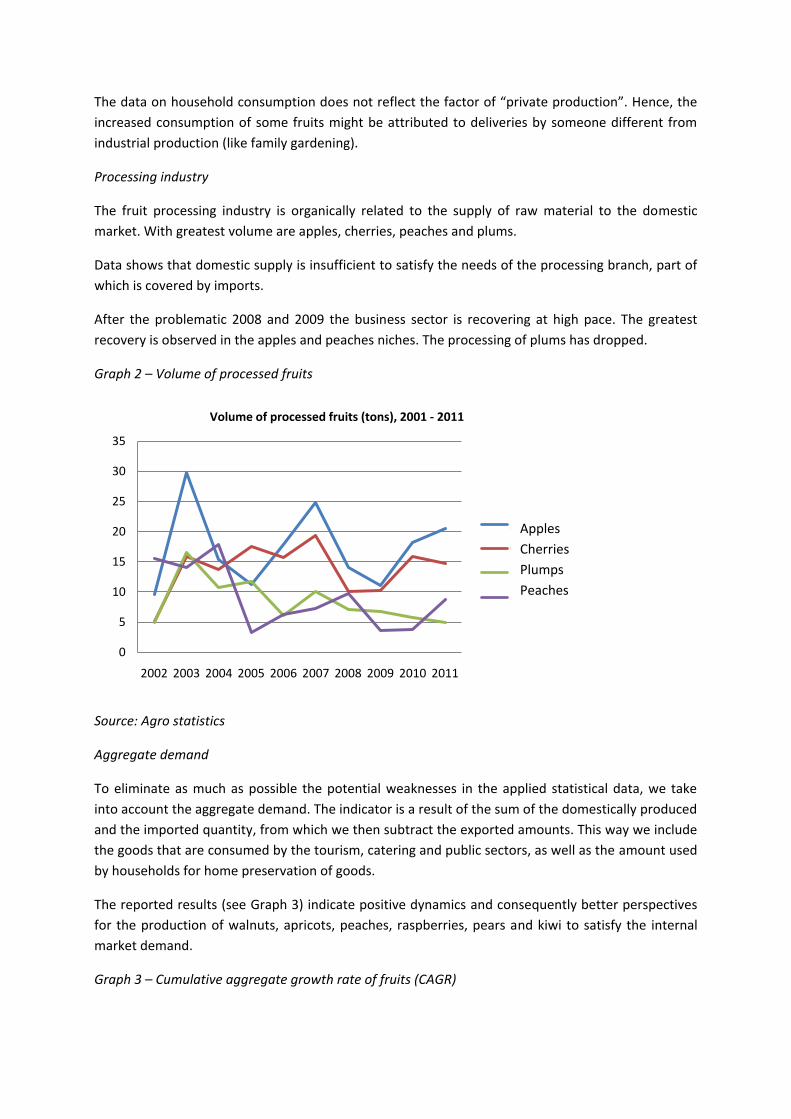

Processing industry

The fruit processing industry is organically related to the supply of raw material to the domestic

market. With greatest volume are apples, cherries, peaches and plums.

Data shows that domestic supply is insufficient to satisfy the needs of the processing branch, part of

which is covered by imports.

After the problematic 2008 and 2009 the business sector is recovering at high pace. The greatest

recovery is observed in the apples and peaches niches. The processing of plums has dropped.

Graph 2 – Volume of processed fruits

Source: Agro statistics

Aggregate demand

To eliminate as much as possible the potential weaknesses in the applied statistical data, we take

into account the aggregate demand. The indicator is a result of the sum of the domestically produced

and the imported quantity, from which we then subtract the exported amounts. This way we include

the goods that are consumed by the tourism, catering and public sectors, as well as the amount used

by households for home preservation of goods.

The reported results (see Graph 3) indicate positive dynamics and consequently better perspectives

for the production of walnuts, apricots, peaches, raspberries, pears and kiwi to satisfy the internal

market demand.

Graph 3 – Cumulative aggregate growth rate of fruits (CAGR)

0

5

10

15

20

25

30

35

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Volume of processed fruits (tons), 2001 - 2011

ябълки

череши

сливи

праскови

Apples

Cherries

Plumps

Peaches

Vegetables

Looking at the vegetables consumption, the consumption of the following goods appears to be

greater (see Table 4):

Mushrooms – with 75%

Cabbage – with 29%

Frozen vegetables, cucumbers and to a lesser degree - tomatoes

Growth is observed in niche crops such as cauliflower and broccoli if the household budgets

is compared to the export accounts

Decline is examined only in the preserved vegetables – pickled vegetables/pickles and juices

Table 4 – Household consumption of vegetables

Source: NSI

11,8

10,9

8,9

6,3

3,7

2,5

-0,5

-1,1

-4,3

-7,1

-10 -5 0 5 10 15

walnuts

apricots

peaches

raspberries

cherries

kiwi

apples

almonds

plums

strawberries

Rate of increase of total demand for fruit, 2002-2011, GACR

75,0%68,8%

29,3% 25,6% 24,4% 21,2%14,9%

9,2% 8,6%

-1,2% -4,8% -24,1% -44,4%

Mu

shro

om

s

Len

s

Cab

bag

e

Be

ans

Cu

cum

ber

s

Oth

er

Tom

ato

es

Po

tato

es

On

ion

s

Pep

pe

rs

Can

ne

d v

ege

tab

les

Pic

kles

Juic

es

Chnage of households' vegetable consumption, 2002-2011 г.

The shifts of beans and lentils consumption should not be considered as long term tendencies. Their

growth is concentrated in the last two years of the crisis. This focus is a disadvantage of the

household budgets study because a big portion of the interviewees belong to low income

households. Obviously, a considerable part of the population has increased the consumption of such

basic foods. However, there is enough evidence to assume as perspective for production

mushrooms, cucumbers, cabbage, tomatoes and onion, as long as they are cultivated and marketed

at (highly) competitive prices.

Processing industry

The key vegetable crops in demand of processing are pepper and tomatoes. From significance for the

processing branch are also aubergine, peas and gherkin, although their importance is declining in the

last couple of years. It should be noted here that potatoes and mushrooms have completely vanished

as goods in the processing sector.

Table 5 – Processed vegetables quantity

Source: Agro statistics

Aggregate demand

The data on the total quantity of vegetables delivered/imported to the domestic market differ from

the household consumption statistics. It signals for positive dynamics only in the peas, carrots and

mushrooms values.

0

5

10

15

20

25

30

35

40

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Processed vegetables quantity (t), 2002 - 2011

домати

пипер

патладжан

грах

Tomatoes

Peppers

Eggplant

Peas

-Table 6 – Cumulative aggregate growth rate of vegetables

External market

We apply the information on export in the EU for the last ten years to analyze the export potential.

The focus is on this particular market because a considerable part of Bulgarian exports of fruits and

vegetables goes to other countries of the Community. Moreover, the EU market due to its mere size

provides great opportunities for the Bulgarian farmers.

Table 7 – Growth of fruit imports in EU

Source: Eurostat

17,2

9

7,5

-2,8

-3,4

-6,4

-6,8

-7,3

-9,6

-15 -10 -5 0 5 10 15 20

peas

carrots

mushrooms

cucumbers

onions

tomatoes

peppers

cabbage

potatoes

CAGR of vegetables, 2002-2011

3,1% 2,9%2,4% 2,3% 2,2%

1,5% 1,4%1,0%

0,4%

-2,0%

Annual growth of fruit import in EU, 202 - 2011

Ras

pb

erri

es

Kiw

i

Ap

ple

s

Gra

pes

Wal

nu

ts

Stra

wb

erri

es

Pea

ches

Ch

erri

es

Ap

rico

ts

Plu

ms

The table identifies a significant growth in the demand of raspberries, kiwi, apples, desert grapes and

walnuts in EU.

Regarding the demand of vegetables, onion, mushrooms, cucumbers, pepper, cabbage and tomatoes

appear as the most popular goods in the EU for the last ten years.

Table 8 – Growth of vegetables imports in EU

Source: Eurostat

Bulgaria’s competitive advantages

In order to identify the competitive advantages of particular crops, we apply the Revealed

Competitive Advantage method (RCA) and we get the following results for fruit and vegetables:

Конкурентоспособност на отделните култури / Competitiveness of particular crops

Fruits RCA Vegetables RCA

Walnuts 14,0% Mushrooms 29,3%

Raspberries 5,0% Cucumbers 21,5%

Strawberries 2,2% Peas 3,2%

Plums 1,4% Cabbage -1,4%

Cherries 1,2% Carrots -3,8%

Apricots -0,2% Onion -4,5%

Peaches -1,8% Potatoes -5,7%

Grapes -2,5% Peppers -10,2%

Apples -11,1% Tomatoes -59,7%

Source: Own calculations

8,0%

5,2%3,9% 3,8% 3,2% 2,7%

1,7%0,7%

-8,9%

Annual growth of vegetables import in EU, 2002 - 2011

on

ion

s

mu

shro

om

s

cucm

ber

s

pep

per

cab

bag

e

tom

ato

es

carr

ots

pea

s

po

tato

es

Domestic market

In relation to meeting the internal market demand, walnuts, raspberries and cherries appear to hold

the greatest potential. Apricots, as well as peaches, also have market potential that needs to be

further developed.

Table 9 – Perspectives for the fruit-tree crops on domestic market

Source: Own calculations

With respect to vegetables, as most perspective are outlined mushrooms and peas, and to some

extend carrots and cucumbers.

Table 10 – Perspectives for vegetable crops on domestic market

Source: Own calculations

-15%

-10%

-5%

0%

5%

10%

15%

20%

-10% -5% 0% 5% 10% 15%

RC

A

динамика на вътрешния пазар

Оценка на конкурентните предимства при овощните култури за вътрешния пазар

малини

орехи

черешикайсии

праскови

сливиягоди

ябълки

-80%

-60%

-40%

-20%

0%

20%

40%

-15% -10% -5% 0% 5% 10% 15% 20%

RC

A

Internal market dynamics

Assessment of competitive advantages of vegetable crops on internal market

mushrooms

peascarrots

tomatoes

cucumbers

onions

cabbage

peppers

potatoes

Assessment of the competitive advantages of fruit-tree crops on

domestic market

walnuts

raspberries

cherries

peaches apricots

apples

plums

strawberries

Internal market dynamics

External market

Cultivation of walnuts, raspberries, strawberries, cherries and apricots stands out as one holding the

greatest potential for export to the EU.

Table 11 – Perspectives for fruit-tree crops on EU market

Source: own calculations

The crops with potential for export to the EU are mushrooms, cucumbers, peas and with some

reservations, cabbage, carrots and onion.

Source: own calculations

Summary of findings

As a result of our analysis, the examined crops can be divided into three groups:

-15%

-10%

-5%

0%

5%

10%

15%

20%

-3% -2% -1% 0% 1% 2% 3% 4%

RC

A

EU import dynamics

Assessment of competitive advantages of fruit-tree crops on EU market

walnuts

raspberriesstrawberries

cherriesapricots

peachesgrapes

apples

plums

-80%

-60%

-40%

-20%

0%

20%

40%

-10% -5% 0% 5% 10%

RC

A

EU import dynamics

Assessment of competitive advanatges of vegetable crops on EU market

mushroomscucumbers

peascabbage

carrotspeppers onions

tomatoes

potatoes

1. Most perspective crops – i.e. crops in the cultivation of which Bulgaria has competitive

advantage after its accession to the EU

2. Crops with certain potential – crops that require additional efforts and investments to

improve their production effectiveness; and/or that experience stable or increasing demand

on EU level, despite declining demand in Bulgaria

3. Crops with no potential - crops that need to undergo drastic improvement of effectiveness

(related to enormous investments, production optimization and cost reduction) and/or face

permanent decrease in demand.

Fruit

Most perspective With potential With no potential

1. Walnuts 1. Apricots Plums

2. Raspberries 2. Peaches Apples

3. Cherries 3. Grapes

4. Strawberries 4. Kiwi

*for which there is insufficient information to assess its competitiveness; yet, it is included because its

cultivation is possible and it enjoys strong demand

Vegetables

Most perspective With potential With no potential

1. Mushrooms 1. Carrots 1. Tomatoes

2. Cucumbers 2. Cabbage 2. Pepper

3. Peas 3. Onion 3. Potatoes

Note: The findings of the study should be considered in the context of the applied methodology and

not as absolute facts.

Contacts:

Nikolay Valkanov

Institute for Market Economics

Sofia, 10 „Patriarh Evtimii“ blvd, fl. 2

tel.: (2) 952 62 66

e-mail: [email protected]