analyst report nissei build kogyo co., ltd

TRANSCRIPT

ANALYST NET Company Report

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

1/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report

is based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR

shall not be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading

of securities and other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited

without the written consent of the company.

ADVANCING TO A NEW GROWTH STAGE

A company with a unique business portfolio of systemized construction and parking

structures

Nissei Build Kogyo is an integrated manufacturer and construction company, particularly

strong in systemized construction and parking structures. Systemized construction,

including assembly of prefabricated homes, exploits the potential of standardized building

components or units, and a tightly organized factory production system, to speedily provide

standardized buildings. Nissei Build’s business portfolio is distinguished by being strong in

the capacity to supply structures of 1,000 m2 or less in gross floor area. The enormous

reconstruction demand after the Tohoku earthquake and tsunami of March 2011 enabled

Nissei Build to expand sales from ¥17,204 million in FY3/2011 (fiscal year ended March

2011) to ¥41,854million in FY3/2012. During the same period, ROE (return on equity)

improved significantly from 2.6% to 20.6%. Offsetting a subsequent drop in reconstruction

demand, Nissei Build recorded sales of ¥41,854 million and ROE of 13.0% in FY3/2014

due to successful alliance and M&A strategies.

Advancing to a new growth stage, driven by alliance and M&A strategies

Nissei Build has the ability to provide customers throughout the nation with solutions and

the technological capabilities to realize the maximum potential of available space. Led by

Atsuhiro Morioka, second- generation president, Nissei Build has been aggressive in (1)

executing M&A strategy, (2) executing alliance strategy, (3) growing in high-margin

stock-based (as opposed to flow-based) business, and (4) expanding overseas. The

company’s Systemized Construction business has high growth potential in the domestic

market, estimated to be about ¥700 billion in scale. It is believed that Nissei Build is

advancing into a new growth stage, which has not been fully discounted in its current stock

price.

Anticipating the company’s specific longer-term growth-oriented message

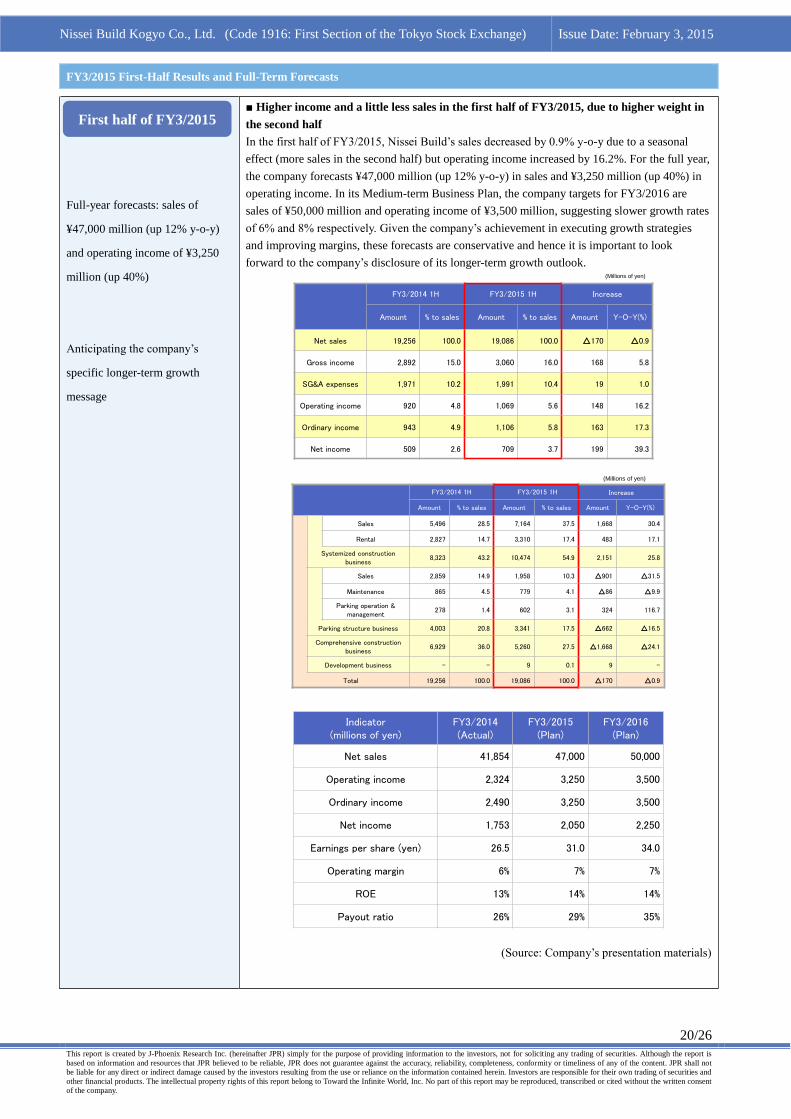

In the first half of FY3/2015, sales decreased by 0.9% y-o-y due to a seasonal effect (sales

tend to be higher in the second half) but operating income increased by 16.2%, led by

margin improvement. For the full year, the company forecasts ¥47,000 million (up 12%

y-o-y) in sales and ¥3,250 million (up 40%) in operating income. In its Medium- term

Business Plan, targets for FY3/2016 are sales of ¥50,000 million and operating income of

¥3,500 million, suggesting growth rates will slow down. In view of this, the company’s

longer-term growth outlook is of great interest.

Basic report

J-Phoenix Research Inc.

Osamu Miyashita, CFA

Basic corporate data

Location Ishikawa Pref.

Representative Atsuhiro Morioka

Established July 1961

Capital ¥7,002 mn

Listed Aug. 1978

URL www.nisseibuild..

co.jp

Industry sector Construction

Employees 478

Share information as of

Jan. 30, 2015

Stock price ¥281

52-week high ¥315

52-week low ¥219

Shares outstanding 71,113,200

Trading unit 1,000

Market cap ¥19,983 mn

DPS (est.) ¥9

EPS (est.) ¥31.00

PER (est.) 9.1x

BPS (actual) ¥221.66

PBR (actual) 1.28x

Fiscal term Sales ¥mn

YOY %

Operating income

¥mn

YOY %

Ordinary income

¥mn

YOY %

Net income ¥mn

YOY %

EPS ¥

Term-end closing share price ¥

High Low

March 2012 Actual 41,879 143.4 6,333 1,047.3 6,436 1,080.9 2,196 782.1 31.4 222 99

March 2013 Actual 25,487 -39.1 1,847 -70.8 1,979 -69.3 1,747 -20.4 26.1 212 108

March 2014 Actual 41,854 64.2 2,324 25.8 2,490 25.8 1,753 0.3 26.5 288 147

Apr.- Sep. 2013 Actual 19,256 71.9 920 69.3 943 60.0 509 45.4 7.7 217 147

Apr.-Sep. Sep. 2014 19,086 -0.9 1,069 16.2 1,106 17.3 709 39.3 10.9 315 219

March 2015 Est. 47,000 12.3 3,250 39.8 3,250 30.5 2,050 16.9 31.0 - -

* EPS, PER, BPS, and PBR are based on the number of shares outstanding, excluding that of the treasury stock.

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

2/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Nissei Build, founded in 1961,

built a nationwide network and

expanded businesses. Since

1996, Atushiro Morioka,

second-generation president, has

aggressively transformed the

company into an integrated

manufacturer.

Examples of systemized

construction structures

Examples of parking structures

■ Leadership of second-generation president and growth

Hiroshi Morioka founded Nissei Build as a garage manufacturing and sales company in 1961, with

17 employees. Over the following years the company has built a network of factories to provide

ability to supply its products nationwide, and was listed in the Second Section of the Osaka

Securities Exchange in 1978. Nissei Build then added more factories, expanded further, and was

listed in the First Section of the Tokyo Stock Exchange in 1996. In 1998, Atsuhiro Morioka became

the second president. Since then, Nissei Build has endeavored to realize organizational reform,

enhance its marketing and sales force, strengthen its group power, and promote its M&A strategy.

The company has been transformed into an integrated manufacturer with its core strength in

systemized construction and parking structures, and additionally, productive engagement in general

construction, development, and overseas businesses.

1961

The late Hiroshi Morioka founded Nissei Build as an assembly-type garage

manufacturing and sales company in Kanaiwa, Kanazawa City.

1968 Built a factory in Saitama Prefecture. Established the House Department.

1971 Built a factory in Fukuoka Prefecture.

1973 Built a factory in Iwate Prefecture.

1974 Established the Housing Section.

1978 Listed in the Second Section of the Osaka Securities Exchange

1979 Built a factory in Hokkaido Prefecture.

1980 Established the Building Material Business Section.

1981 Built a factory in Ishikawa Prefecture.

1988 Established the Parking Structure Business Section.

1989 Built a factory in Ehime Prefecture.

1991 Listed in the First Section of the Osaka Securities Exchange

1993 Established the Building Lease Business Department

1996 Listed in the First Section of the Tokyo Stock Exchange.

1998 Atsuhiro Morioka became the second-generation president.

1999 Established the Sales Management Division to control sections, which were

renamed from departments.

2000 Sections were integrated to the Housing Business Department and the Parking

Structure Business Department.

2007 Delisted from the First Section of the Osaka Securities Exchange and became

listed only in the First Section of the Tokyo Stock Exchange.

2008 Reformed the Organization with the aim of growing larger products and

enhancing business in the Greater Tokyo area.

2009 Established the Maintenance Department.

2010 Renamed the Tokyo Sales Office to Tokyo Branch Office to enhance business in

the Greater Tokyo area.

(Source: Prepared by JPR, based on company materials)

(Source: Prepared by JPR, based on company materials)

Corporate name Nissei Build Kogyo Co., Ltd.

Location 3-16-10 Kanaiwa-kita, Kanazawa City, Ishikawa Prefecture, Japan

Representative Atsuhiro Morioka, President

Established July 3, 1961

Capital 7,002 million yen

Employees 478 (as of March 31, 2014)

Fiscal term Ends March 31

Traded on Tokyo Stock Exchange (First Section)

Sales FY ended March 2014 ¥44,854mn (Consol.): ¥25,903mn (Non-consol.)

Business lines

• Sales of systemized construction (prefabricated houses, and unit houses); rental of prefabricated houses

• Sales, maintenance, and renewal of automated tower parking and multilevel parking

• Sales of parking facilities with ramps

• Construction and renovation construction of railways, civil engineering, and building works (by subsidiaries)

• Parking management and operation (by a subsidiary)

• Trading, brokerage, agency work, rental, and management of real estate (by a subsidiary)

• Comprehensive management and maintenance of commercial facilities, etc. (by a subsidiary)

• Planning, design, development, and management of software (by a subsidiary)

Corporate Profile and Business Characteristics

History and Corporate

Profile

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

3/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

■ Providing clients with full-range services, including construction, maintenance, and

facilities management

The Nissei Build Group (see chart below) provides full-range services, including construction,

maintenance, and facilities management throughout Japan, in alliance with major six partner

companies. Overseas, the company mainly operates parking structure businesses in Singapore,

Thailand, and China. Plans have been made to set up a joint venture in Vietnam, with a local oil

plant construction and sales company and others, to engage in construction, sales, and maintenance

of parking structures.

■ Four major businesses

Nissei Build has four major businesses: (1) Systemized Construction; (2) Parking Structures; (3)

General Construction; and (4) Property Development.

(Source: Company’s presentation materials)

Nissei Build Asia Pte. Ltd.

Capital: ¥490mn

Owned: 100%

Employees: 144

Business lines:

Railway constructionBuilding construction

Civil engineering

Renovation

construction

Nisse Build Kogyo

NB Construction Ozawa Construction NB Parking NB Investment NB Facilities NB Networks

Capital: ¥50mn

Owned: 100%

Employees: 18

Business lines:

Building constructionCivil engineering

Capital: ¥30mn

Owned: 100%

Employees: 14

Business lines:

Operation and

management of car-

parking and bicycle-

parking facilities

Capital: ¥30mn

Owned: 100%

Employees: 3

Business lines:

Trade, brokerage,

agency business,

rental, and

management of real

estate

Capital: ¥37mn

Owned: 100%

Employees: 5

Business lines:

General management

and maintenance of

commercial facilities,

etc.

Capital: ¥30mn

Owned: 100%

Employees: 2

Business lines:

Planning, design,

development &

management of

software

Country: SingaporeCapital: SGD1.54mnOwned: 100%Employees: 1Business lines:Sales of parking structuresOperation and management of

parking facilities

Nissei Build GroupConsolidated sales: ¥41,854mn (FY3/2014)

Group employees: 678

(as of the end of September, 2014)

Country: ChinaOwned: 40%Capital: RMB17mnEmployees: 4Business lines:Operation,

management, and maintenance of parking facilities

Space Value (Thailand)Co., Ltd.

Country: ThailandCapital: THB10mnOwned: 49%Employees: 9Business lines:Sales of parking structuresOperation and management

of parking facilitiesSales of systemized

construction

Asia Parking Investment Pte. Ltd.

Country: SingaporeCapital: SGD1.3mnOwned: 80%Employees: -Business lines:Development and

investment of parking facilities

Shanghai Tiandi Nissei Parking

Management Co., Ltd.

Overseas Group Companies

Domestic Group CompaniesCapital: ¥7,002mn

Employees: 478

Systemized construction

business

Parking structure business

General construction

business

Property development

business (FY3/2015)

Systemized construction: Frontage of 10-40m; Use of H-type lightweight steel frame

Building structures with standardized components and via systemized processes in a single process from design to factory fabrication to on-site construction.

Nissei Build is the only Japanese company to perform systemized construction by using H-type lightweight steel frame.

Prefabricated houses: Frontage of less than 10m; use of C-type steel frame.

Quick construction, low cost, and flexible response to customer needs.

Unit houses: Assemble units from factory-fabricated components.

Automated tower parking: Maximum use of limited space by using an elevator.

Multi-stacked parking; A product line-up of two- to six-storied structures.

Parking with ramps: Safe, convenient, and cost-effective parking.

Maintenance service.

Coin-operated parking structures.

Construction related to condominiums, large facilities, and railways.

Anti-seismic reinforcement, large-scale repair of condominiums.

Large-scale home centers, medical and welfare facilities, large-scale commercial buildings, etc.

Development of condominiums and road-side buildings.

Introduction to the

Nissei Build Group

Business Outline

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

4/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Representative products

Interior of “Nissei V Span-S”

H-type lightweight steel frames

used in systemized construction

by Nissei Build

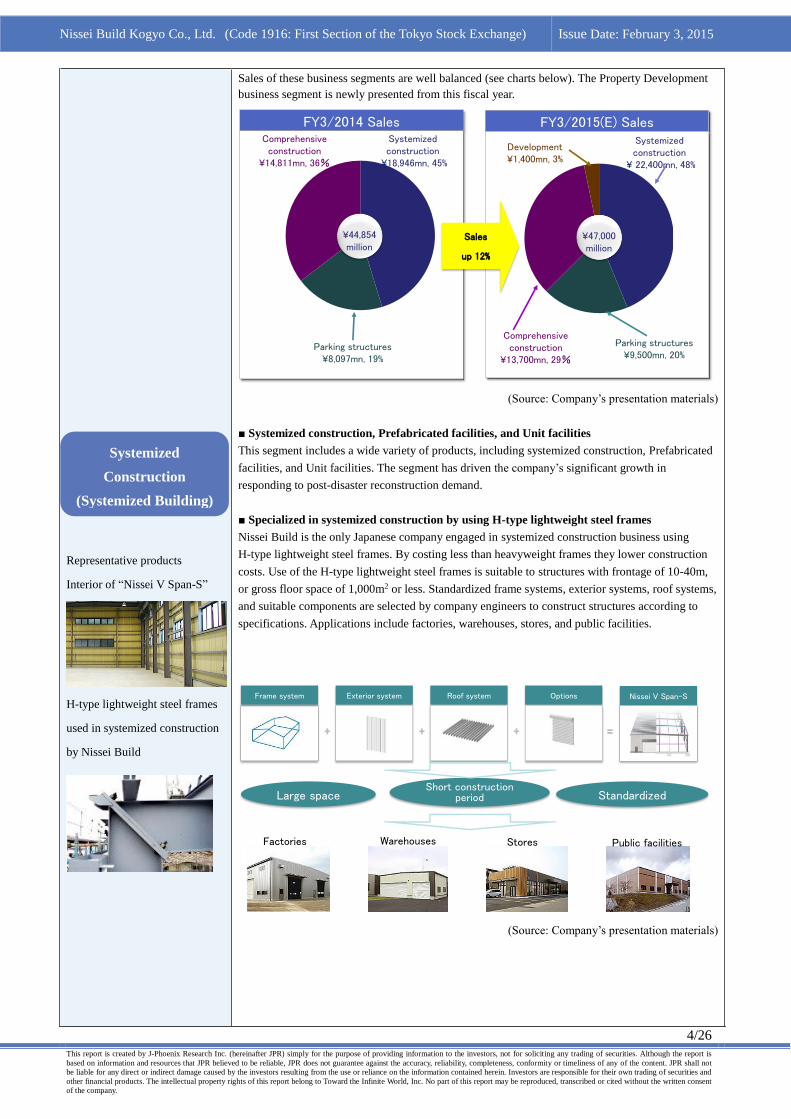

Sales of these business segments are well balanced (see charts below). The Property Development

business segment is newly presented from this fiscal year.

(Source: Company’s presentation materials)

■ Systemized construction, Prefabricated facilities, and Unit facilities

This segment includes a wide variety of products, including systemized construction, Prefabricated

facilities, and Unit facilities. The segment has driven the company’s significant growth in

responding to post-disaster reconstruction demand.

■ Specialized in systemized construction by using H-type lightweight steel frames

Nissei Build is the only Japanese company engaged in systemized construction business using

H-type lightweight steel frames. By costing less than heavyweight frames they lower construction

costs. Use of the H-type lightweight steel frames is suitable to structures with frontage of 10-40m,

or gross floor space of 1,000m2 or less. Standardized frame systems, exterior systems, roof systems,

and suitable components are selected by company engineers to construct structures according to

specifications. Applications include factories, warehouses, stores, and public facilities.

(Source: Company’s presentation materials)

FY3/2014 SalesSystemized construction

¥18,946mn, 45%

Parking structures¥8,097mn, 19%

Comprehensive construction

¥14,811mn, 36%

FY3/2015(E) SalesSystemized construction

¥ 22,400mn, 48%

Parking structures¥9,500mn, 20%

¥44,854million

¥47,000million

Comprehensive construction

¥13,700mn, 29%

Development ¥1,400mn, 3%

Sales

up 12%

Nissei V Span-SFrame system Exterior system Roof system Options

Large spaceShort construction

period Standardized

Factories Warehouses Stores Public facilities

Systemized

Construction

(Systemized Building)

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

5/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

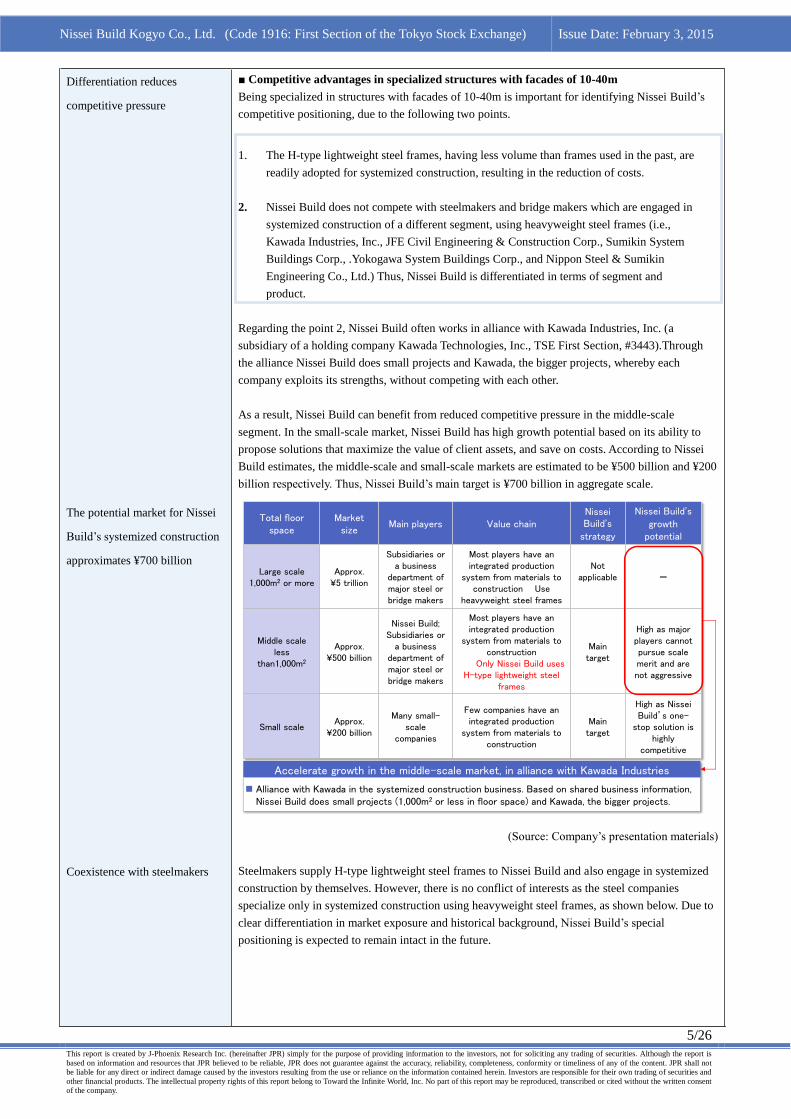

Differentiation reduces

competitive pressure

The potential market for Nissei

Build’s systemized construction

approximates ¥700 billion

Coexistence with steelmakers

■ Competitive advantages in specialized structures with facades of 10-40m

Being specialized in structures with facades of 10-40m is important for identifying Nissei Build’s

competitive positioning, due to the following two points.

1. The H-type lightweight steel frames, having less volume than frames used in the past, are

readily adopted for systemized construction, resulting in the reduction of costs.

2. Nissei Build does not compete with steelmakers and bridge makers which are engaged in

systemized construction of a different segment, using heavyweight steel frames (i.e.,

Kawada Industries, Inc., JFE Civil Engineering & Construction Corp., Sumikin System

Buildings Corp., .Yokogawa System Buildings Corp., and Nippon Steel & Sumikin

Engineering Co., Ltd.) Thus, Nissei Build is differentiated in terms of segment and

product.

Regarding the point 2, Nissei Build often works in alliance with Kawada Industries, Inc. (a

subsidiary of a holding company Kawada Technologies, Inc., TSE First Section, #3443).Through

the alliance Nissei Build does small projects and Kawada, the bigger projects, whereby each

company exploits its strengths, without competing with each other.

As a result, Nissei Build can benefit from reduced competitive pressure in the middle-scale

segment. In the small-scale market, Nissei Build has high growth potential based on its ability to

propose solutions that maximize the value of client assets, and save on costs. According to Nissei

Build estimates, the middle-scale and small-scale markets are estimated to be ¥500 billion and ¥200

billion respectively. Thus, Nissei Build’s main target is ¥700 billion in aggregate scale.

(Source: Company’s presentation materials)

Steelmakers supply H-type lightweight steel frames to Nissei Build and also engage in systemized

construction by themselves. However, there is no conflict of interests as the steel companies

specialize only in systemized construction using heavyweight steel frames, as shown below. Due to

clear differentiation in market exposure and historical background, Nissei Build’s special

positioning is expected to remain intact in the future.

Total floor space

Market size

Main players Value chainNissei Build’s

strategy

Nissei Build’s growth

potential

Large scale1,000m2 or more

Approx. ¥5 trillion

Subsidiaries or a business

department ofmajor steel or bridge makers

Most players have an integrated production

system from materials to construction Use

heavyweight steel frames

Not applicable -

Middle scaleless

than1,000m2

Approx. ¥500 billion

Nissei Build; Subsidiaries or

a business department ofmajor steel or bridge makers

Most players have an integrated production

system from materials to construction

Only Nissei Build uses H-type lightweight steel

frames

Main target

High as major players cannot pursue scale merit and are not aggressive

Small scaleApprox.

¥200 billion

Many small-scale

companies

Few companies have an integrated production

system from materials to construction

Main target

High as Nissei Build’s one-

stop solution is highly

competitive

Accelerate growth in the middle-scale market, in alliance with Kawada Industries

Alliance with Kawada in the systemized construction business. Based on shared business information, Nissei Build does small projects (1,000m2 or less in floor space) and Kawada, the bigger projects.

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

6/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Prefab house (image)

Nissei Build’s capabilities to

shorter construction time,

standardized formats, and lower

costs are highly acknowledged

by nationwide convenience

stores and other retail

franchisers

(Source: Company’s presentation materials)

■ Nissei’s prefab houses have facades of 10m or less

Prefabricated facilities (prefabs) are to manufacture pillars, beams, roofs, walls, and other

components of a building at off-site factories in advance and then assemble them on-site to

complete construction.

Nissei Build specializes in prefab housing having facades of 10m or less. Many components are

standardized, enabling high efficiency in both off-site factory production and on-site construction,

and ensuring that high standards of quality are satisfied. The rationalized entire processes from

design to production and construction helps lessen the overall work period and reduce construction

costs. Among the Nissei Build customers who benefit from this method are convenience store and

other retail business chains, including their franchisees, as chains require stores that are made

according to a high degree of standardization, resulting in cost reduction, more flexible store

development and reorganization. Nissei Build’s technological capabilities, ability to satisfy

customers, and nationwide presence are highly evaluated by those familiar with the company.

Steelmakers

Lightweight steel frames

Heavyweight steel frames

Bridge-related systemized construction

makers

Steelmaking-related systemized construction

makers

Only Nissei Build is insystemized construction

business, using lightweight steel frames

Frontage of 10-40m

Floor space of 1,000m2 or less

Frontage of 40m or more

Floor space of 1,000m2 or more

Due to different background, Nissei Build is differentiated from other makers, and has established a value chain optimal to its business characteristics, that acts to deter entrants from other groupings.

This has provided stability for the company.

Groundwork Pillar installation Beam and bracing installation

Exterior wall panel installation

Completion

Office buildings Stores Garages Public facilities

Short construction period Standardized

Coin-operated laundries

Systemized

Construction

(Prefabs)

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

7/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Installation of factory-made

finished products on site

Strong ability to propose

solutions and use technology for

effective use of space

■ Construction by the unit method of installing factory-made finished products on site

Nissei Build constructs structures by using the unit method of installing factory-made finished

products on site. The method accommodates various needs and allows construction in a short work

time. Flexibility of Unit facilities means more potential for modifying interior space to meet

specific requirements, and facilitate relocation and expansion.

■ Strength in applying systemized construction know-how

Parking structures are multilevel buildings and may be equipped with mechanical devices. By using

standardized components and applying systemized construction know-how, Nissei Build constructs

parking structures that satisfy a wide range of specific requirements and are completed and ready

for use in a short time. The two main types are a mechanical type and a drive-in type. Mechanical

parking can be either in the form of a tower or a multilevel facility. Nissei Build is leading the

industry with its innovative product offerings and ability to ensure effective use of space. Nissei

Build’s value-creating solutions and technological capabilities are well used in urban areas having a

perpetual shortage of parking space. Nissei Build’s parking structures are also attractive as facilities

that enable effective use of real estate and generate stable cash flow. Other attractive points for real

estate owners and investors are the company’s ability to forecast parking income based on its long

experience and integrated service including post-construction maintenance and operation.

Short construction period Standardized

Functional adaptability

Sheds Shelters Studios Toilets

Short construction period Standardized Flexible

Automated tower parking

タワー式

Parking with rampsMulti-stacked parking

Hotels Offices Condos Corporate offices

HospitalsCondos Corporate housing

Systemized

Construction

(Unit facilities)

Parking structure

business

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

8/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

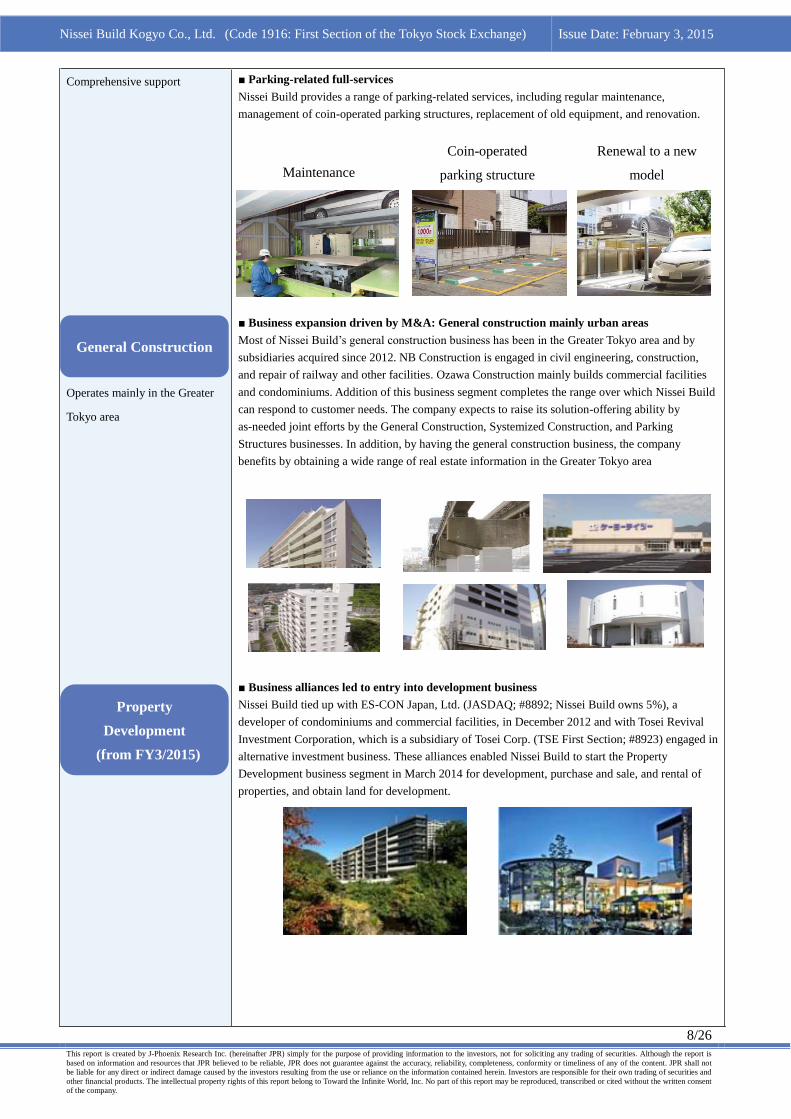

Comprehensive support

Operates mainly in the Greater

Tokyo area

■ Parking-related full-services

Nissei Build provides a range of parking-related services, including regular maintenance,

management of coin-operated parking structures, replacement of old equipment, and renovation.

■ Business expansion driven by M&A: General construction mainly urban areas

Most of Nissei Build’s general construction business has been in the Greater Tokyo area and by

subsidiaries acquired since 2012. NB Construction is engaged in civil engineering, construction,

and repair of railway and other facilities. Ozawa Construction mainly builds commercial facilities

and condominiums. Addition of this business segment completes the range over which Nissei Build

can respond to customer needs. The company expects to raise its solution-offering ability by

as-needed joint efforts by the General Construction, Systemized Construction, and Parking

Structures businesses. In addition, by having the general construction business, the company

benefits by obtaining a wide range of real estate information in the Greater Tokyo area

■ Business alliances led to entry into development business

Nissei Build tied up with ES-CON Japan, Ltd. (JASDAQ; #8892; Nissei Build owns 5%), a

developer of condominiums and commercial facilities, in December 2012 and with Tosei Revival

Investment Corporation, which is a subsidiary of Tosei Corp. (TSE First Section; #8923) engaged in

alternative investment business. These alliances enabled Nissei Build to start the Property

Development business segment in March 2014 for development, purchase and sale, and rental of

properties, and obtain land for development.

General Construction

Renewal to a new

model

Property

Development

(from FY3/2015)

Maintenance

Coin-operated

parking structure

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

9/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Maximizing value by means of

combining three elements,

satisfying owners’ needs, and

sensitivity to features of the site

and its location

“Space is Value” is a corporate

slogan

■ Solution-providing ability and technological capabilities: two strengths to maximize usage

of space

Nissei Build’s strength lies in solution-providing ability and technological capability, that enable

maximal usage of space, and customers throughout the nation can avail themselves of these

advantages.

(Source: Prepared by JPR, based on company interview)

■ Three elements of solution-providing ability: ability to combine businesses, understand

customer needs, and provide full-range support.

First, ability to combine. Nissei Build combines its business of Systemized Construction, General

Construction, and Parking Structures and proposes a one-stop solution to maximize usage of space.

The Systemized Construction business facilitates shorter work time, greater space, standardized

products, lower price, and receptiveness to scrap-and-build situations. The General Construction

business responds to lasting individual customer needs. The Parking Structure business can realize

effective use of spare space and improve convenience. By combining these businesses for specific

projects, Nissei can better achieve maximizing customer value, based on needs of landowners and

business operators, characteristics of properties, and location conditions.

(Source: Prepared by JPR, based on company interview)

The second element is to understanding customers’ needs. Based on information provided by

alliance partners, Nissei Build strives to properly understand needs of prospective customers who

are interested in its solutions, and to make actionable proposals. Typical customers are convenience

store chains, hospitals, and public facilities.

Solution Providing Ability Technological Capability

Solution Providing Abilities and Technological Capabilities which pursue the maximization of the value of the space of

the real-estate for the landlords and the business operators are available nation-wide

1) Ability of

combining various

solutions

2) Ability of

understanding

needs of clients

3) Providing one

stop supporting

services

1) Own designing

and

manufacturing

Capability

2) Capability of

realizing

combination of

various solutions

3) Nation-wide

capability to

provide the same

quality of service

and facilities

Space

Needs

&

Feature of Real-estate

&

Conditions of

Location

Value Realization through

Systemized Construction

structures

Value Realization through

General Construction

Value Realization through

Parking Structures

“Space is Value”

Business Model Characteristics

Two strengths

enabling

maximization of space

usage

Three elements of

solution-providing

ability

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

10/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Slashing the requirement for

skilled workers means Nissei

Build is less affected by the labor

shortage problem than

constructors using conventional

methods

The third element is provision of full-range support. Nissei Build is committed to provide a

one-stop, most-appropriate support for the constructed building.

(Source: Prepared by JPR, based on company interview)

■ Three elements of technological capability: provision of own design and production service,

ability to form combinations, and offering of the same level of capabilities nationwide

The first element is the company’s own design and production capabilities. In an integrated

manner, Nissei Build designs and manufactures steel frames, walls, roofs, and other building

components and devises control programs for tower parking facilities. Standardized mass

production helps lower costs and the construction technology reduce the need for veteran

construction workers, which enables restraint of overall costs and shortening of construction

periods.

The second element is ability to flexibly realize combinations. Depending on customer needs and

characteristics of sites and building requirements, Nissei Build can come up with a wide variety of

proposals by combining the specialties of Systemized Construction (i.e., “Nissei V Span-S,” prefab

houses and Unit facilities for sale or lease), General Construction, and Parking Structures

(mechanical, drive-in, coin-operated parking, or their combination) segments and by developing

proposals using its technological capabilities.

The third element is provision of identical-quality technical services of design, manufacturing, and

construction by Nissei Build’s own factories, partner building contractors, and sales offices across

Japan. The company is less affected by the labor shortage problem, compared to constructors using

conventional methods, as it does not require skilled workers. Moreover, it can fully respond to

market needs throughout the nation.

Design

Constru

ctio

n

Com

pletio

n

Ope

ration an

d m

anage

ment

Main

tenan

ce

Renew

al

Ope

ration an

d m

anage

ment

Dism

antle

ment

Three elements of

technological

capabilities

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

11/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Sustainable long-term

value-creating chain realized by

providing one-stop solutions

Enhanced ability to collect

information, through alliances

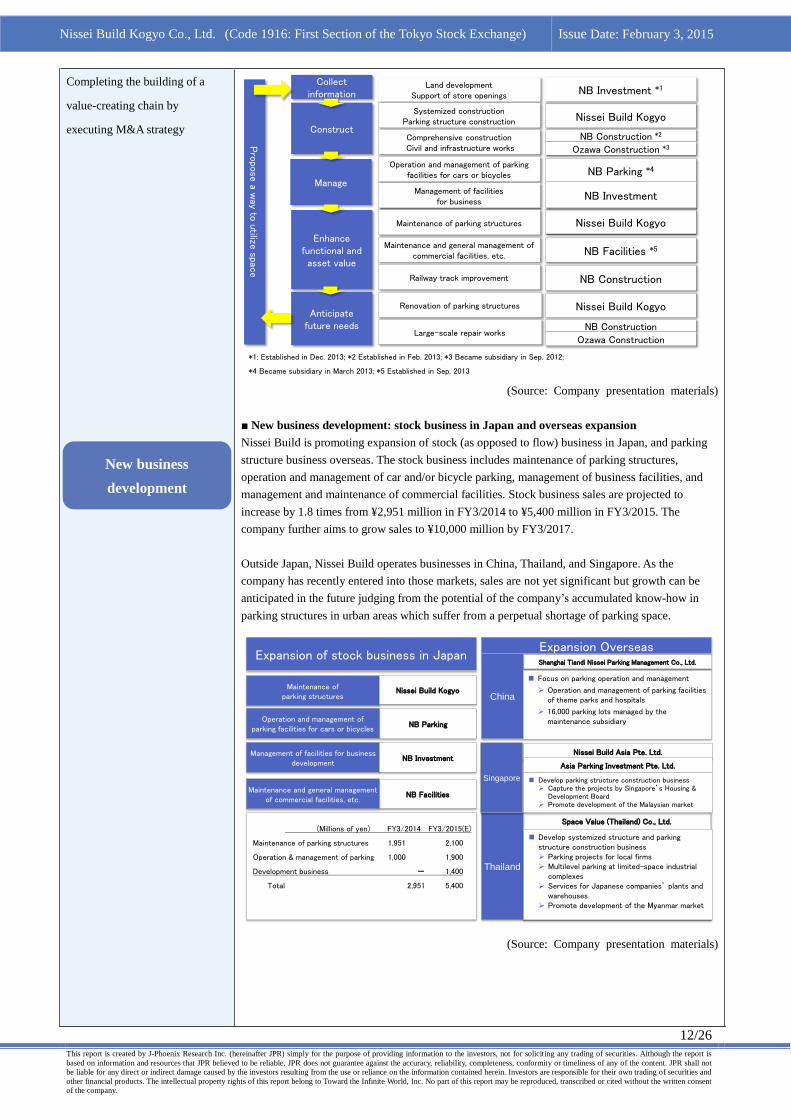

■Value-creating chain to maximize usage of space

With the aim of strengthening its strengths in making proposals and technological capabilities,

Nissei Build focuses on realizing a sustainable long-term value-creating chain by offering one-stop

solutions to customers. The sequence of this chain processes is as follows: collect information

construct manage enhance functional and asset value anticipate future needs provide

new ways to utilize space.

(Source: Company presentation materials)

To collect information is the first step of the value-creating chain. Nissei Build has enhanced this

step by making the following alliances since 2012.

(Source: Company presentation materials)

The Nissei Build Group has also established arrangements to realize all steps of the value-creating

chain, and does this by means of the above-mentioned M&A strategy. By having pursued this

since 2012, the entire structure has now been completed and is ready to be activated.

Nissei Build’s one-stop solution forms

a long-term sustainable value-creating chain

Through alliance partners, collect nation-wide information on land with development potential in connection with business activity

Provide realistic, convincing construction proposals, combined with comprehensive construction expertise

Manage

Enhance functional and asset value

Construct

Operate and manage the constructed property in optimal condition

Enhance the value of property through good facility management and maintenance

Anticipate future needs

Perform large-scale repair or renovation work in keeping with changing needs

Collect information

Pro

vide w

ays to u

tilize spac

e

GE Capital Japan

ORIX Corporation

ES-CON Japan Ltd

Luckland Co., Ltd.

Tosei Revival Investment Corporation

Business alliance for introduction of lease clients

Business alliance for introduction of lease clients

Business and capital alliance for development of condominiums and commercial facilities

Nissei Build owns a 5% stake

Business and capital alliance on development of new products and clients

Cross-shareholding of ¥50 million with Nissei Build

Business alliance on real estate development, renewal, and property management

Kawada

Industries, Inc.

Business alliance for systemized construction; Nissei Build does small projects (1,000m2 or less in floor space), Kawada does bigger projects

Clients of all sectors; financing

Store openings;

planning and design of

commercial facilities

Need for building renewals

Need for systemized construction

Type of information

Alliance partners DetailsStart time

Sep. 2012

Aug. 2012

Nov. 2012

Nov. 2012

Apr. 2013

Sep. 2013

How to create

corporate value

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

12/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Completing the building of a

value-creating chain by

executing M&A strategy

(Source: Company presentation materials)

■ New business development: stock business in Japan and overseas expansion

Nissei Build is promoting expansion of stock (as opposed to flow) business in Japan, and parking

structure business overseas. The stock business includes maintenance of parking structures,

operation and management of car and/or bicycle parking, management of business facilities, and

management and maintenance of commercial facilities. Stock business sales are projected to

increase by 1.8 times from ¥2,951 million in FY3/2014 to ¥5,400 million in FY3/2015. The

company further aims to grow sales to ¥10,000 million by FY3/2017.

Outside Japan, Nissei Build operates businesses in China, Thailand, and Singapore. As the

company has recently entered into those markets, sales are not yet significant but growth can be

anticipated in the future judging from the potential of the company’s accumulated know-how in

parking structures in urban areas which suffer from a perpetual shortage of parking space.

(Source: Company presentation materials)

Enhance functional and asset value

Anticipate future needs

Manage

Construct

Collect information

Nissei Build Kogyo

NB Construction *2

Ozawa Construction *3

NB Parking *4

NB Facilities *5

NB Investment *1Land developmentSupport of store openings

Systemized constructionParking structure construction

Comprehensive constructionCivil and infrastructure works

Operation and management of parking facilities for cars or bicycles

Management of facilities for business

Maintenance of parking structures

Maintenance and general management of commercial facilities, etc.

Railway track improvement

Renovation of parking structures

Large-scale repair works

Nissei Build Kogyo

Nissei Build Kogyo

NB Investment

NB Construction

NB Construction

Ozawa Construction

Pro

pose

a way to

utilize spac

e

*1: Established in Dec. 2013; *2 Established in Feb. 2013; *3 Became subsidiary in Sep. 2012;

*4 Became subsidiary in March 2013; *5 Established in Sep. 2013

Expansion of stock business in Japan

NB Facilities

Maintenance ofparking structures

Maintenance and general management of commercial facilities, etc.

Nissei Build Kogyo

NB Parking Operation and management of

parking facilities for cars or bicycles

(Millions of yen) FY3/2014 FY3/2015(E)

Maintenance of parking structures 1,951 2,100

Operation & management of parking 1,000 1,900

Development business - 1,400

Total 2,951 5,400

Management of facilities for business development

NB Investment

Expansion OverseasShanghai Tiandi Nissei Parking Management Co., Ltd.

Space Value (Thailand) Co., Ltd.

China

Thailand

Singapore

Nissei Build Asia Pte. Ltd.

Asia Parking Investment Pte. Ltd.

Focus on parking operation and management

Operation and management of parking facilities of theme parks and hospitals

16,000 parking lots managed by the maintenance subsidiary

Develop systemized structure and parking structure construction business Parking projects for local firms Multilevel parking at limited-space industrial

complexes Services for Japanese companies’ plants and

warehouses Promote development of the Myanmar market

Develop parking structure construction business Capture the projects by Singapore’s Housing &

Development Board Promote development of the Malaysian market

New business

development

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

13/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

■ Higher fixed-cost coverage ratio enhances value creation

The stock business has high growth potential. Target sales are ¥10,000 million in FY3/2017. This

business has a higher gross margin, 30-40%, than other businesses. Expansion of the stock business

will make the company’s profit structure more resilient and will better cover fixed costs.

(Source: Company’s presentation materials)

■ Business segments and segmentation

Business segments and segmentation, including non-consolidated subsidiaries, are summarized

below. Note, however, that NB Facilities, which is engaged in facility management, and overseas

subsidiaries are not consolidated.

(Source: Company presentation materials)

FY3/2015

¥5.4bn (E) in sales

Aim over ¥10bn in sales

in around FY3/2017• Accelerate sales by acquiring maintenance management

companies, as wide-range synergies in use of space can be expected

Maintenance and general management

of commercial facilities, etc.

• Accelerate sales by acquiring parking facility management companies, as wide-range synergies in use of space can be expected

Operation and management of

parking facilities for cars or bicycles

Management of business facilities

(Development business)

• Promotion of increase in management assets to include visible cash-flow parking facilities adjacent to convenience stores, and hospitals

• Focus on less economic sensitive projects with ensured exit strategy

FY3/2015 Sales Plan by Segment

Systemized construction business

¥22,400mn,

48%

販売事業12,41430%

Parking structure business

¥9,500mn, 20%

¥47,000million

Development business¥1,400mn, 3%

Comprehensive construction business

¥13,700mn, 29%

Systemized construction

Parking structures

Comprehensive construction

Development

Nissei Build Kogyo (Parent)

NB Construction

Ozawa Construction

NB Parking

NB Investment

Nissei Build Kogyo (Parent)

Nissei Build Kogyo (Parent)

Non-consolidated subsidiaries

Equity income affiliate

NB Facilities

Space Value (Thailand) Co., Ltd.

Nissei Build Asia Pte. Ltd.

Asia Parking Investment Pte. Ltd.

Shanghai Tiandi Nissei Parking Management Co., Ltd.

Business Segmentation

Financial implication

of stock business

expansion

Business segments and

segmentation

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

14/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

■ Nine directors and three auditors

Nissei Build has one outside director and two outside auditors.

President and Representative Director Atsuhiro Morioka

Senior Managing Director Naoki Morioka

Managing Director Yoshiaki Motoyoshi

Managing Director, General Manager of the

Production Division

Keiji Fujiwara

Director, General Manager of the Sales

Division

Masao Nawamaki

Director, General Manager of the

Engineering Division

Nobu Tanida

Director, Manager of the Greater Tokyo

Business Section and of the Kanto Block, the

Sales Division

Hideki Ueda

Director, General Manager of the

Maintenance Division

Koji Kotani

Director Junya Kikuchi (Outside Director)

Full-time Auditor Akihiro Matsumoto

Auditor Shouji Arakawa (Outside Auditor)

Auditor Mitsuhiro Tokuno (Outside Auditor)

(Source: Securities Filing; as of March 31, 2014)

■ Well-diversified shareholder structure

The ten largest shareholders are well diversified with financial institutions such as banks and

securities companies ranking at the top. The founder’s family, owning less than 10%, does not

have controlling interest. The composition of the board of directors and of the body of

shareholders indicates that corporate governance is functioning well with no great cause for

concern.

Major shareholders Shares owned

(Thousands)

Voting

rights

(%)

1 The Master Trust Bank of Japan, Ltd. (Trust

Account)

6,307 8.87

2 Japan Trustee Services Bank, Ltd. (Trust

Account)

5,594 7.87

3 Morioka International Ltd. 4,551 6.40

4 Hokuriku Bank, Ltd. 2,684 3.77

5 Hokkoku Bank, Ltd. 2,607 3.67

6 The Nomura Trust and Banking Co., Ltd.

(Investment Trust Account)

2,235 3.14

7 Nippon Life Insurance Company 2,055 2.89

8 BNP-Paribas Securities Services 1,660 2.33

9 Atsuhiro Morioka 1,423 2.00

10 Goldman Sachs International 1,367 1.92

(Source: Securities Filing; as of March 31, 2014)

■ Standard dividend policy

According to securities filings, Nissei Build’s basic dividend policy is to maintain stable

dividend payments and take into account a comprehensive range of factors, including financial

conditions and plans for future business development. The company also intends to secure

internal reserves for efficient investment for business growth and for future returning of profit.

The company’s payout ratio is not low at 30.4% in FY3/2014 and is expected to be about 30%

in the near future years.

Corporate Governance

Board of Directors

Major shareholders

Policy to return profits

to shareholders

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

15/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

■ Political, economic, and social environment based evaluation

Negative factors for Nissei Build include sustained high building material prices and concerns

over the rise in labor cost, caused by a labor shortage. In contrast, positive factors are the expected

rise of real estate prices mainly in the Great Tokyo area, ahead of the 2020 Tokyo Olympics, rising

benefits from land management induced by lower interest rates, and greater needs for property

management in anticipation of the January 2015 rise in the inheritance tax. As real estate tends to

be evaluated lower than cash in assessing value for inheritance tax, there is a growing need to

convert cash into real estate, as a way to reduce inheritance tax obligations.

■ Five force analysis: Strong and solid market positioning

As shown in the chart below, Nissei Build has established a strong positioning in all five forces.

(Source: Company’s presentation materials)

■ Assessment of management resources by VRIO analysis

Nissei Build is highly valued as it has established competent management resources in all four

factors: value, rareness, imitability, and organization.

(Source: Company’s presentation materials)

Competitive rivalryThreat of new entrants Threat of substitutes

Relationship with partners

Strong and solid relations with clients

Few companies offer one-stop solutions in Nissei Build’s targeted middle-and small-scale markets.

Limited competition

It is not easy to provide a comprehensive service with a nationwide production network such as that of Nissei Build.

Low risk

Nissei Build’s products replace conventional methods.

Low substitution risk

Clients such as convenience store chains highly regard Nissei Build’s capability to provide solutions based on understanding of the client’s business.

Clients are highly satisfied with Nissei Build’s systemized construction (for 1,000m2 or less) and parking structures.

Nissei Build has established strong relationships of trust with intermediate companies or agencies, who in turn are trusted by clients.

The life cycle maintenance enables to last long-term relationship.

Information providing partners: Alliances with Nissei Build invigorates their business

Building contractors in partnership: Profit from handling Nissei Build’s differentiated products

Steelmakers: Nissei Build established a strong relationships of trust as a large client to purchase lightweight steel frames

Strong and solid relations

Value

Nissei Build’s total solutions to maximize space value and satisfy client needs, which are available nationwide, have proven highly valuable to operators of chain stores.

Rarity

Nissei Build is the only company in Japan to do systemized construction by using H-type lightweight steel frame for structures of 10-40 m in frontage and 1,000m2 or less in gross floor space in Japan.

Very few companies provide one-stop solution for small-scale structures, from component fabrication to construction and maintenance.

Imitability

It is difficult to imitate systemized construction starting with component fabrication.

Nissei Build’s human resources who market total solutions and respond to client needs are difficult to replicate.

Organization

Nissei Build is organized to provide one-stop solutions from component fabrication to construction and maintenance for systemized construction of 1,000m2 or less.

Nissei Build is capable of proposing use of space of the target businesses and do actual construction as one-stop.

Business Model Evaluation

Evaluation concerning

external environments

Five force analysis

VRIO analysis

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

16/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Growth, driven first by

reconstruction demand, and then

M&A and alliance strategies

Growth was accelerated by

aggressive alliance strategy in and

after 2012

■ Assessment in growth

Nissei Build’s sales surged in FY3/2012, due to strong post-earthquake reconstruction demand,

after which sales increased due to the M&A and alliance strategies. Based on the company’s

forecasts up to FY3/2016, the expected compound annual growth rates in sales, operating income,

and net income from FY3/2010 to FY3/2016 are 17.0%, 42.1%, and 42.8% respectively.

(Source: Company’s presentation materials)

By business segment, the Parking Structure business recorded double-digit sales growth of 26.9%

y-o-y in FY3/2013, 39.0% in FY3/2014, and is estimated to grow 17.3% in FY3/2015. This

includes a strong contribution from the alliance strategy. The Systemized Construction segment is

projected to increase sales by 18.2% y-o-y for FY3/2015, with almost no negative impact from the

disappearance of reconstruction demand. Since 2012, growth has appeared boosted by business

expansion driven by aggressively making alliances.

(Source: Prepared by JPR, based on Securities Filing)

Indicators(millions of yen)

FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014FY3/2015

(Plan)FY3/2016

(Plan)

Net sales 18,367 17,204 41,879 25,487 41,854 47,000 50,000

Gross profit 3,305 3,148 9,591 5,271 6,356 7,650 8,300

SG&A expenses 2,911 2,596 3,258 3,423 4,031 4,400 4,800

Operating income 394 552 6,333 1,847 2,324 3,250 3,500

Ordinary income 477 545 6,436 1,979 2,490 3,250 3,500

Net income 242 249 2,196 1,747 1,753 2,050 2,250

0

10,000

20,000

30,000

40,000

50,000

60,000

Net Sales

0

500

1,000

1,500

2,000

2,500

Operating Income

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

Net Income(Millions

of yen)

(Millions

of yen)

(Millions

of yen)

Indicators

(millions of yen)FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014

FY3/2015

(Plan)

Net sales 18,367 17,204 41,879 25,487 41,854 47,000

Systemized

construction business11,367 11,327 37,288 18,236 18,945 22,400

Parking structure

business6,998 5,877 4,590 5,824 8,097 9,500

General construction

business0 0 0 1,426 14,811 13,700

Property development

business 0 0 0 0 0 1,400

Sales Growth Ratio -25.0% -6.3% 143.4% -39.1% 3.9% 18.2%

Systemized

construction business-0.4% 229.2% -51.1% 3.9% 18.2%

Parking structure

business-16.0% -21.9% 26.9% 39.0% 17.3%

General construction

business-7.5%

Financial analysis

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

17/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Operating margin is improving

from 5.6% in FY3/2014 to 7.0%

in FY3/2016

General Construction business

improves margin by selective

order-taking

■ Evaluation of margins, EPS, and payout ratio

After a spike in FY3/2012, margins have dropped with the fading away of reconstruction demand.

Operating margin is expected to gradually improve from 5.6% in FY3/2014 to 6.9% estimated for

FY3/2015 and 7.0% estimated for FY3/2016.

(Source: Company’s presentation materials)

Segment information reveals that General Construction, driven by M&A activities and added in

FY3/2013, has a lower margin compared to the Systemized Construction segment and the Parking

Structure segment. The General Construction segment became more selective in receiving orders

and the improved margin enabled a swing back to profits in FY3/2014.

(Source: Prepared by JPR, based on securities filing)

Ratios (millions of yen)

FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014FY3/2015

(Plan)FY3/2016

(Plan)

Gross margin 18.0% 18.3% 22.9% 20.7% 15.2% 16.3% 16.6%

SG&A expenses to sales

15.8% 15.1% 7.8% 13.4% 9.6% 9.4% 9.6%

Operating margin 2.1% 3.2% 15.1% 7.3% 5.6% 6.9% 7.0%

Ordinary margin 2.6% 3.2% 15.4% 7.8% 5.9% 6.9% 7.0%

Net margin 1.3% 1.4% 5.2% 6.9% 4.2% 4.4% 4.5%

0%

5%

10%

15%

20%

25%

Gross Margin

0%

1%

2%

3%

4%

5%

6%

7%

8%

Net Margin

0%

2%

4%

6%

8%

10%

12%

14%

16%

Operating Margin

Ratios (millions of yen) FY3/2013 FY3/2014

Sales

Systemized construction business 18,239 18,945

Parking structure business 5,824 8,097

General construction business 1,426 14,811

Consolidated 25,487 41,854

Segment

Profits

Systemized construction business 3,228 2,820

Parking structure business 397 287

General construction business -161 677

Adjustments -1,617 1,460

1,847 2,324

Profit Margin

Systemized construction business 17.7 14.9

Parking structure business 6.8 8.4

General construction business -11.3 1.9

Adjustments - -

Consolidated 7.2 5.6

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

18/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

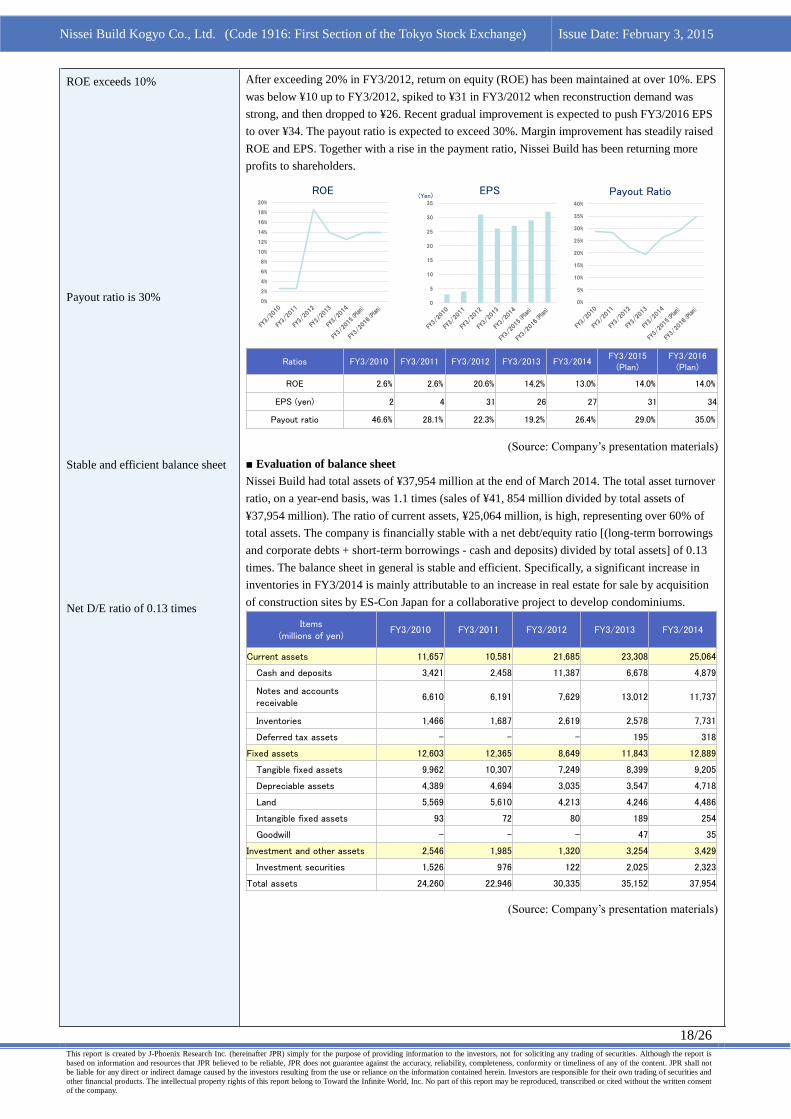

ROE exceeds 10%

Payout ratio is 30%

Stable and efficient balance sheet

Net D/E ratio of 0.13 times

After exceeding 20% in FY3/2012, return on equity (ROE) has been maintained at over 10%. EPS

was below ¥10 up to FY3/2012, spiked to ¥31 in FY3/2012 when reconstruction demand was

strong, and then dropped to ¥26. Recent gradual improvement is expected to push FY3/2016 EPS

to over ¥34. The payout ratio is expected to exceed 30%. Margin improvement has steadily raised

ROE and EPS. Together with a rise in the payment ratio, Nissei Build has been returning more

profits to shareholders.

(Source: Company’s presentation materials)

■ Evaluation of balance sheet

Nissei Build had total assets of ¥37,954 million at the end of March 2014. The total asset turnover

ratio, on a year-end basis, was 1.1 times (sales of ¥41, 854 million divided by total assets of

¥37,954 million). The ratio of current assets, ¥25,064 million, is high, representing over 60% of

total assets. The company is financially stable with a net debt/equity ratio [(long-term borrowings

and corporate debts + short-term borrowings - cash and deposits) divided by total assets] of 0.13

times. The balance sheet in general is stable and efficient. Specifically, a significant increase in

inventories in FY3/2014 is mainly attributable to an increase in real estate for sale by acquisition

of construction sites by ES-Con Japan for a collaborative project to develop condominiums.

(Source: Company’s presentation materials)

0%

5%

10%

15%

20%

25%

30%

35%

40%

Ratios FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014FY3/2015

(Plan)FY3/2016

(Plan)

ROE 2.6% 2.6% 20.6% 14.2% 13.0% 14.0% 14.0%

EPS (yen) 2 4 31 26 27 31 34

Payout ratio 46.6% 28.1% 22.3% 19.2% 26.4% 29.0% 35.0%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

ROE

0

5

10

15

20

25

30

35

EPS Payout Ratio(Yen)

Items(millions of yen)

FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014

Current assets 11,657 10,581 21,685 23,308 25,064

Cash and deposits 3,421 2,458 11,387 6,678 4,879

Notes and accounts receivable

6,610 6,191 7,629 13,012 11,737

Inventories 1,466 1,687 2,619 2,578 7,731

Deferred tax assets - - - 195 318

Fixed assets 12,603 12,365 8,649 11,843 12,889

Tangible fixed assets 9,962 10,307 7,249 8,399 9,205

Depreciable assets 4,389 4,694 3,035 3,547 4,718

Land 5,569 5,610 4,213 4,246 4,486

Intangible fixed assets 93 72 80 189 254

Goodwill - - - 47 35

Investment and other assets 2,546 1,985 1,320 3,254 3,429

Investment securities 1,526 976 122 2,025 2,323

Total assets 24,260 22,946 30,335 35,152 37,954

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

19/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

An increase in inventories is the

greatest cash-out item

(Source: Company’s presentation materials)

(Source: Prepared by JPR, based on Company’s disclosed materials. Figures based on term-end

differ from the aforementioned ones)

■ Cash flow

An increase in inventories is the greatest cash-out item in FY3/2014.

(Source: Company’s presentation materials)

Items(millions of yen)

FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014

Current liabilities 11,621 10,115 14,800 18,628 19,815

Notes and accounts payable 3,984 3,992 7,742 11,410 10,354

Short-term borrowings, bonds, etc.

4,999 3,717 1,666 2,359 4,394

Deferred tax liabilities - - - - -

Non-current liabilities 3,161 3,341 3,715 3,648 3,988

Long-term borrowings, bonds, etc.

2,251 2,247 2,705 2,091 2,298

Deferred tax liabilities - 7 2 144 77

Total liabilities 14,782 13,456 18,515 22,276 23,803

Net assets 9,478 9,490 11,819 12,875 14,151

Common stock 7,002 7,002 7,002 7,002 7,002

Capital surplus 1,913 1,913 1,913 1,913 1,913

Retained earnings 715 894 3,020 4,279 5,701

Treasury stock -123 -123 -126 -624 -625

Total shareholders’ equity 9,507 9,686 11,810 12,570 13,992

Net unrealized valuation gain, etc.

-29 -196 - 289 120

Subscription rights to shares - - 8 16 37

Minority interests - - - - -

Total liabilities and net assets 24,260 22,946 30,335 35,152 37,954

Own capital 9,478 9,490 11,810 12,859 14,113

Interest-bearing debt 7,250 5,964 4,371 4,450 6,692

Items FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014

ROE(on the basis of the year-end data, not compatible with the previous pages)

2.5% 2.6% 18.6% 13.9% 12.5%

ROA(on the basis of the year-end data, not compatible with the previous pages)

1.6% 2.4% 20.9% 5.3% 6.1%

Net D/E Ratio (Times) 0.40 0.36 -0.59 -0.18 0.13

Total Assets Turnover (Times) 0.76 0.75 1.38 0.73 1.10

Items(millions of yen)

FY3/2010 FY3/2011 FY3/2012 FY3/2013 FY3/2014

Operating cash flow 1,364 1,061 10,368 -50 -1,633

Pre-tax income 294 306 3,211 1,885 1,764

Depreciation 720 700 553 347 504

Amortization of goodwill - - - 76 18

Increase in accounts payable 1,248 419 -1,437 767 1,278

Decrease in inventories 1,500 -221 -932 155 -5,141

Decrease in accounts receivable -1,574 7 3,749 -1,084 -1,064

Subtotal 1,645 1,212 10,678 1,549 -1,658

Interest and dividends received 36 26 27 7 27

Interest expenses paid -163 -140 -96 -77 -75

Income taxes paid -153 -37 -50 -1,529 73

Investing cash flow -94 -646 235 -2,266 -2,248

Increase in tangible and intangible fixed assets

-71 -1,035 -296 -841 -1,397

Increase in investment securities -63 5 740 -1,258 -972

Financing cash flow -564 -1,367 -1,678 -2,364 1,744

Increase in borrowings and corporate bonds

-553 -1,283 -1,593 -1,346 2,117

Increase in treasury stock -1 0 -2 -498 -1

Dividends paid 0 -70 -68 -483 -329

Cash and cash equivalents 3,387 2,434 11,359 6,678 4,679

Nissei Build Kogyo Co., Ltd. (Code 1916: First Section of the Tokyo Stock Exchange) Issue Date: February 3, 2015

20/26

This report is created by J-Phoenix Research Inc. (hereinafter JPR) simply for the purpose of providing information to the investors, not for soliciting any trading of securities. Although the report is

based on information and resources that JPR believed to be reliable, JPR does not guarantee against the accuracy, reliability, completeness, conformity or timeliness of any of the content. JPR shall not

be liable for any direct or indirect damage caused by the investors resulting from the use or reliance on the information contained herein. Investors are responsible for their own trading of securities and

other financial products. The intellectual property rights of this report belong to Toward the Infinite World, Inc. No part of this report may be reproduced, transcribed or cited without the written consent

of the company.

Full-year forecasts: sales of

¥47,000 million (up 12% y-o-y)

and operating income of ¥3,250

million (up 40%)

Anticipating the company’s

specific longer-term growth

message