anatomy of procurement fraud

TRANSCRIPT

Anatomy of

Procurement Fraud

Presented byTom Caulfield

Introduction

Tom Caulfield

Procurement Integrity Consulting Services (PICS)

www.procurement-integrity.net

[email protected](540) 907-8654

Learning Objectives

• Understanding of the anatomy and elusiveness ofprocurement fraud.

• Understanding the various elements and methods ofcontracting.

• Introduction of the personalities of those that commitprocurement fraud and abuse.

• Understanding how to develop a procurement fraud risktheory.

• Introduction of the uniqueness of conducting aprocurement fraud investigation.

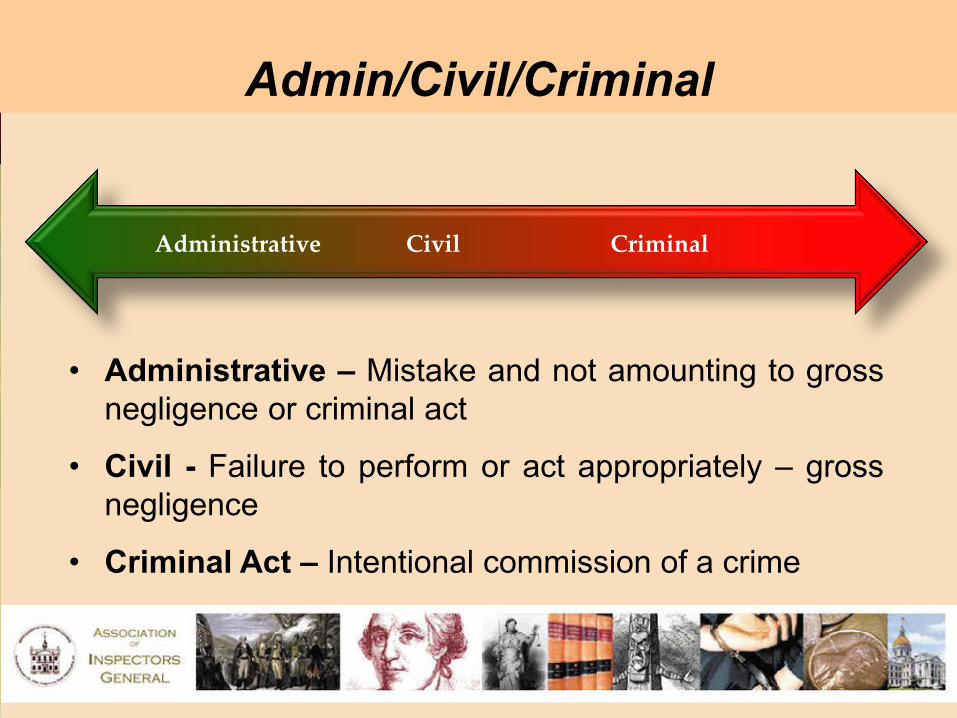

Admin/Civil/Criminal

Administrative Civil Criminal

• Administrative – Mistake and not amounting to grossnegligence or criminal act

• Civil - Failure to perform or act appropriately – grossnegligence

• Criminal Act – Intentional commission of a crime

Administrative

Breach of contract is a legal cause ofaction in which a binding agreement(contract) is not honored by one ormore of the parties by non-performance or interference with theother party's performance.

Civil Fraud

Gross negligence is the "lack ofdiligence or care" or "a conscious,voluntary act or omission in recklessdisregard of a legal duty and of theconsequences to another party, whomay typically recover exemplarydamages.

Criminal Fraud

• Fraud is an intentional misrepresentation of the truth,involving trickery and deception in order to illegallyenrich the fraudster.

• Fraud is cheating for profit.

• Fraud is characterized by acts of guile, trickery,concealment, or breach of confidence, whichare used to gain some unfair or dishonestadvantage.

Contract Fraud

What is it?

Contract Fraud

With Contract/Procurement Fraud, themisrepresentation of the truth willoccurs some where in the acquisitionprocess; by a fraudster(s) who has anoperational knowledge of your process.

Operational Knowledge

The connection of the fraudster can stemfrom a person providing services orproducts under the contract, a personmarketing the contract, a personoverseeing the performance/delivery ofthe contractor, or the person negotiatingthe contract price.

The Government Players!

Procurement Executive Program Contracting Officer (PCO) [CO] Administrative Contracting Officer (ACO) Contracting Officer Tech Rep (COTR) Contracting Officer Rep (COR) Contract Support Assistant (CSA) Source Selection Committee Members Program People Others

The Company Players!

Corporate Procurement Executive Contracting Officer (CO) Contract Support Assistant (CSA) Proposal Team Cost Team Program People Others

Who has the authority to award, modify,terminate, or add scope to a contract?

Authority!

Who will many times cause inappropriate changes to the scope of a contract?

Who to Control?

Can you have a Verbal Contract or Agreement?

Can you have a Verbal Contract or Agreement?

What about in your jurisdiction or organization?

Procurement fraud often starts out “underthe radar screen” with a systematic abuse oftrust sometimes combined with flawedinternal controls. If discovered, the tendencymay be to characterize it as isolatedinstance when a more thorough examinationwould uncover a pattern.

Radar Screen

Depending on the organization being victimized;the consequences of procurement fraud will alwaysinvolve the loss of money, but may also put at risk -personal safety, if the scheme involves defectiveproducts; counterfeit parts; or product substitution.

Contract Fraud

Unlike crimes against persons and property,which are clear from the beginning what thecrime is, procurement fraud is not so clear.

What was the true scheme?

False statement in the bid, false claims throughdouble billing, bribery, kickbacks, conflict ofinterest.

What is the True Scheme?

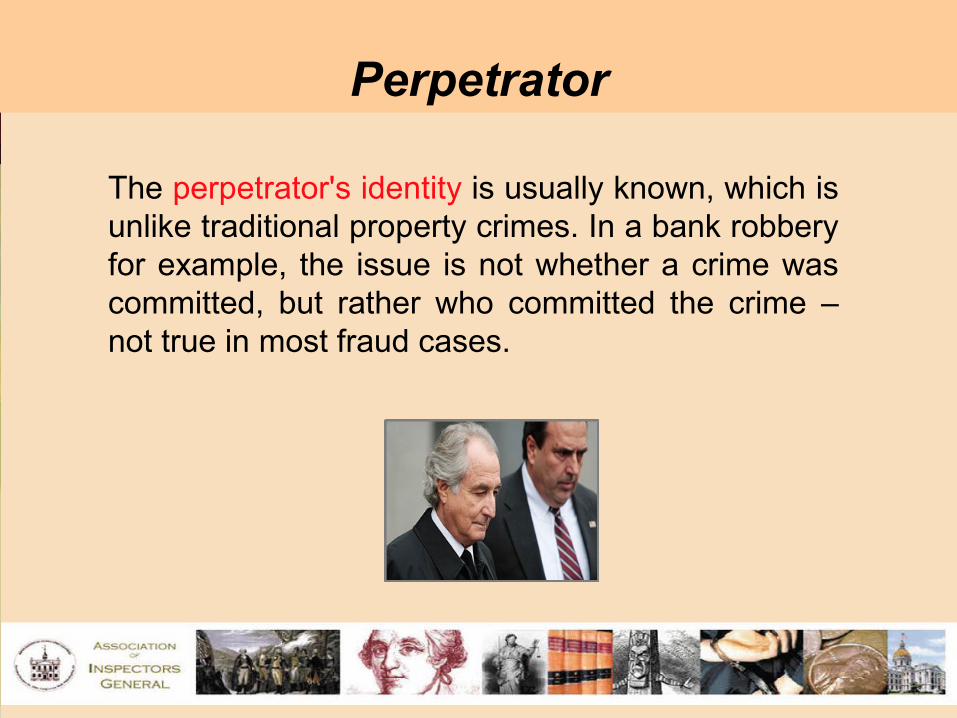

The perpetrator's identity is usually known, which isunlike traditional property crimes. In a bank robberyfor example, the issue is not whether a crime wascommitted, but rather who committed the crime –not true in most fraud cases.

Perpetrator

Adding to procurement fraud’s detection difficulty isthe veil of trust the fraudster normally carries with theemployees of the organization being victimized, asthe fraudster is usually connected to the procurementin some way, and therefore is interacting at somelevel with the organizational employees.

Veil of Trust!

As you can see, because of this veil of trust, thefraudster is often considered to be a “trusted agent”by the same people for whom the fraudster hasbreached the trust of. This “trusted agent” statushighlights the peculiar dichotomy of procurementfraud: these crimes cannot succeed without trust,but neither can business.

Trusted Agent

• One of the most common of all white-collar crimes.

• Increasingly more sophisticated.

• Many times being technology driven.

• Saddles the public and the private sectors with coststo reputations and balance sheets.

• Most distressingly, it undermines confidence in theorganizational structure and its management.

Procurement or Contract

Procurement Policies

Federal Acquisition Laws/Regulation State Acquisition Laws/Regulations Defense Federal Acquisition Regulation Agency Supplements Agency Policies

• Criminal Fraud• Civil Fraud• Contract administrative adjustment• Suspension• Debarment

Outcome Options

• Allowed by the contract.

• Government authorized.

• Mistake and therefore a breach of contract.

• Civil.

• Never Criminal

Favorite Defense Argument

• U.S. organizations up to 5 – 7 % of their revenues each year.

• 66% run for more than a year before they were detected.

• 13% ran for five years or longer before they were detected.

ACFE

Personality Risk Profiles

Personalities

Each fraudster and/or abuser can be reduced toone of five personality risk profiles and each one ismotivated differently, thus creating a differentstrategy for preventing and detecting their actions.

These deceitful acts occur for different reasons inthe mind of the fraudster or abuser, but each onesucceeds by compromising procurement policies,procedures, and/or requirements.

Personality Risk Profiles

1. Situational Fraudster

2. Deviant Fraudster

3. Multi-Interest Abuser

4. Well Intentioned Non-Compliance Employee

5. Disengaged Non-Compliance Employee

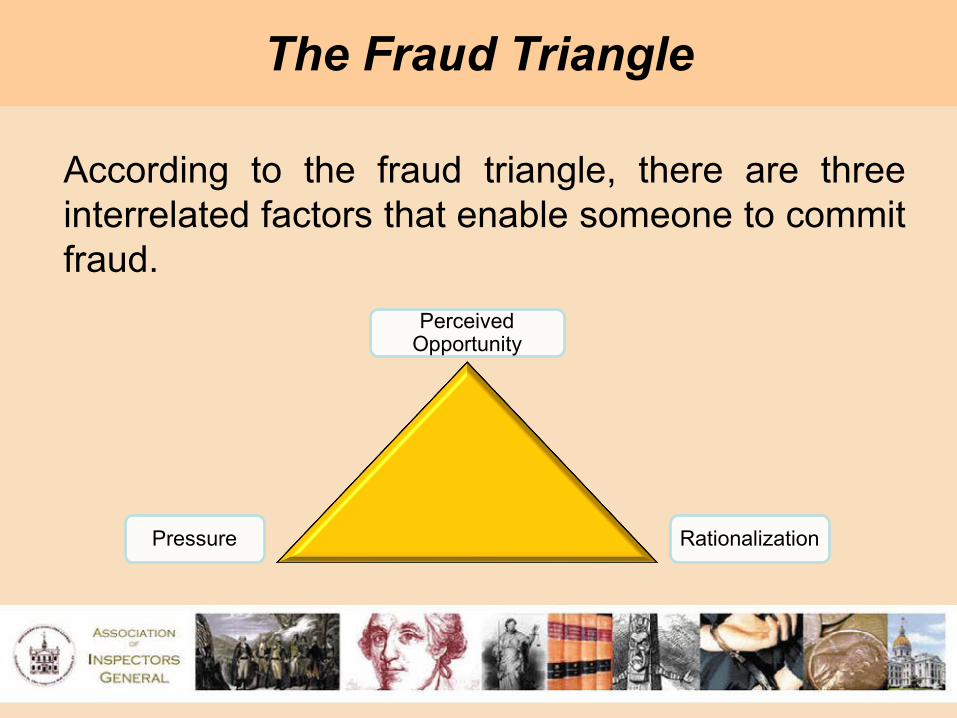

The Fraud Triangle

According to the fraud triangle, there are threeinterrelated factors that enable someone to commitfraud.

Perceived Opportunity

RationalizationPressure

Situational Fraudster

1. Situational Fraudster

2. Deviant Fraudster

3. Multi-Interest Abuser

4. Well Intentioned Non-Compliance Employee

5. Disengaged Non-Compliance Employee

• Labor mischarging by an individual• Theft of government/company items• Defective product

• Not bribes, gratuities, kickbacks, etc.

Situational Fraudster

The one most people will reference as thetraditional “Fraudster”, who is the employee thatseems to be frustrated at work; who hasrationalized his/her right to an illegal enrichment;and simply perpetrates the fraud scheme whenthe right occasion occurs; normally because of aweak internal control.

Deviant Fraudster

1. Situational Fraudster

2. Deviant Fraudster

3. Multi-Interest Abuser

4. Well Intentioned Non-Compliance Employee

5. Disengaged Non-Compliance Employee

Deviant Fraudster

Of a serious concern as this person can causethe greatest damage to an organization. Thistype of person is proactive; possibly perceived asone of the company’s hardest workers or bestcontractors; is always on the alert foropportunities to corrupt the system; and carrieswhat we call the "veil of trust" from others in theorganization.

Deviant Fruadster

Always proactive in their search for opportunitiesto commit fraud

Possibly perceived as one of the company’shardest workers or best contractors

Carries the "veil of trust" from othersin the organization

Sometimes described as a "wheeler-dealer"

Situational vs. Deviant

The situational fraudster is far more prevalent inany contract, but losses are far less.

If the deviant fraudster can bribe an organizationalofficial to allow fraudulent billing submissions with apromise of kickbacks, or a contractor implements afraudulent cost accounting scheme, the losses canbe in the millions.

Procurement Abuse

Procurement Abuse includes actions like: Misuse of authority or position; Misuse of access to sensitive procurement

information.

*All with the intent to advance one’s own interest orthose of a family member, friend, or particularcontractor.

Personality Risk Profiles

1. Situational Fraudster

2. Deviant Fraudster

3. Multi-Interest Abuser

4. Well Intentioned Non-Compliance Employee

5. Disengaged Non-Compliance Employee

Multi-Interest Abuser

Manipulates the procurement process to advancehis/her own interest and the interest of anotherperson. This is done not to obtain any financialadvantage for him/herself, but instead to help afriend in getting a contract, or to ensure the awardgoes to their desirable contractor, or even helpingfamily members.

Multi-Interest Abuser

This multi-interest abuser of the procurementprocess is the one who drafts contractspecifications to a specific contractor; orembellishes the need for a "sole-source"justification to avoid a fully competitive process; or"slants" technical evaluations to a specific bidder.

Multi-Interest Abuser

Again, this multi-interest abuser is not motivatedby any direct financial compensation, but stillraises significant risk to an organization.

Clearly if the inappropriate actions of this personwas motivated for personal financial gain then thisperson would be categorized as a procurementFraudster and not an Abuser.

Personality Risk Profiles

1. Situational Fraudster

2. Deviant Fraudster

3. Multi-Interest Abuser

4. Well Intentioned Non-Compliance Employee

5. Disengaged Non-Compliance Employee

Personality Risk Profiles

• Well Intentioned Non-Compliance Employee• Disengaged Non-Compliance Employee

The next two personality risk profiles are rarely talkedabout, but present a risk to the organization that isprobably harder to identify then the Fraudster orAbuser. These last two risk profiles fall into thecategory of the Procurement Non-ComplianceEmployees.

Well Intentioned Non-Compliance Employee

Believes his/her deviation from the procurementprocesses does not harm the organization and furtherbelieve they are helping the organization in obtaininggreater efficiency or obtaining better services.

This self-described well intentioned non-complianceemployee is an employee who has been with theorganization for years and has a good workingknowledge of procurement processes.

Well Intentioned Non-Compliance Employee

This employee will not identify the true scope of arequirement to ensure the contract remains under aparticular dollar threshold thereby allowing the awardto be expedited.

This is also the employee who knows what keydescriptions in an organizational purchasingdocument to use or not use to avoid a requiredprocurement process.

DisengagedNon-Compliance Employee

This is the employee who puts little or minimaleffort into a specific procurement step. Thisperson will not check a contractor's bond, ornot examine a contractor's past performancerecord, or not confirm a contractor's deliverableprior to approving payment.

Non-Compliance Employee

The non-compliance employee create unnecessaryexposure for your organization to fraud, litigationand may also waste company resources and lostfunds.

Most concerning is that these employees open thedoor and create opportunities for the Fraudsters.

What Is It ?

Basically = A mutual agreement betweentwo or more parties (government andprime contractor), which must be of lawfulsubject matter or objective, provide legalconsiderations, and results in mutualpromises and obligations.

Procurement Methods

1. Sealed Bidding2. Contracting by Negotiation3. Sole-Source & Single

SourceFederal Government (FAR) - 13 methodsNational Contract Management Association - 22 methods

Sealed Bids

• Prepare the invitation – What we need. • Publicize the invitation – Want to provide (ITB).• Receive no less than two responses – What it will

cost.• Open in public.• Evaluate and compare the responses.• Select the most appropriate response.

Contracting by Negotiation

• Competitive negotiation using RFPs – Contracting by negotiation is used when cost is

not the most important factor.– RFP is used to solicit pricing/descriptions.

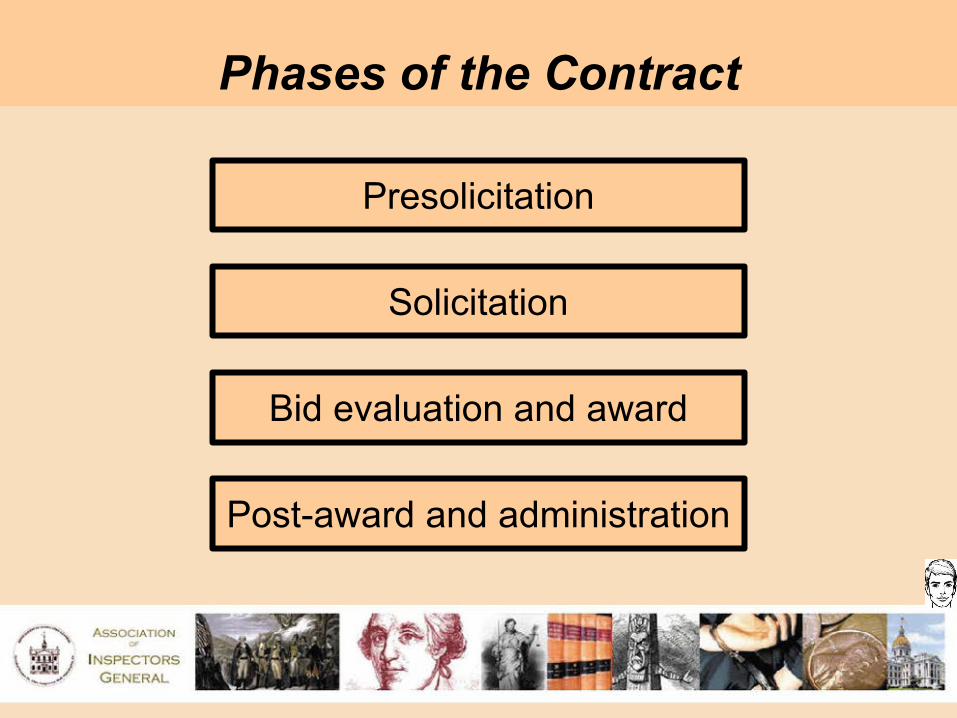

Phases of the Contract

Presolicitation

Solicitation

Bid evaluation and award

Post-award and administration

Contract Types

Firm Fixed Price – Low Risk to Government- Contract Not Subject to Adjustments

Cost Plus Type (flexible) Cost Reimbursement- Actual Costs and Allowable AdjustmentsPlus a Fee for Doing the Work

Contract Types

Level of Effort – High Risk to Government

Time & Materials

No Deliverables Required, only Best Effort(Usually used in Research, EnvironmentalCleanups, etc.)

These types of Contracts can be the mostdifficult to prove fraud.

Contract Types & Risks• Level of Effort - High Risk • Time and Materials• Cost Plus Fixed Fee• Cost Plus Award Fee• Cost Plus Incentive Fee• Cost No Fee• Cost Sharing• Fixed Price Award Fee• Fixed Price Incentive• Firm Fixed Price w/EPA• Firm Fixed Price – Low Risk

Contract

Types

Contractor Risk

Working Procurement Fraud Investigations

Presented byTom Caulfield & Sheryl Steckler

Fraud Scheme or Indicator

• Scheme – is a deliberate and purposefulundertaking designed to misrepresent andconceal an improper or illegal act.

• Indicator – is a symptom or characteristicon the existence of a potential scheme.

One indicator, normally in itself, does not mean a scheme has or has not occurred.

Fraud Scheme or Indicator

• Some indicators, such as a falsified or phonydocument, may be, in and of themselves, enough totrigger a referral or investigation.

• In other cases, you may need to recognize theinterrelationship of several seemingly unrelateddeficiencies or indicators, which when combined,warrant a referral or investigation.

• You must consider the total picture when decidingwhether to refer a suspected irregularity or initiate aninvestigation.

Fraud Scheme or IndicatorUndeniably, the universal and most significant threats to achieving and

maintaining honest, fair, impartial and legal contracting comes fromthe forty-four traditional schemes of procurement fraud or abuse andthe multitude of ways each of those schemes can be performed.

The success of these malicious acts are driven by the:

1. Motivation of the perpetrator(s);

2. Fraudsters ability to influence a decision point within aprocurement process;

3. Scheme they are deploying; and

4. Effectiveness of the entity’s procurement integritycontrols.

Rigged Specifications Collusive Bidding Excluding Qualified Bidders Unbalanced Bidding Leaking Bid Data Manipulation of Bids Unjustified Sole Source Change Order Abuse Split Purchases

Conflicts of Interest Defective Pricing Cost Mischarging Co-mingling of Contracts Defective Products Product Substitution Counterfeit Parts Phantom Vendor False Statements & Claims

Bribes – Gratuity – Kickbacks – Extortion

Just the Most Common

Available Resources

• Department of Defense – Office of Inspector GeneralFraud Indicators for Auditors

• United States Postal Service – Office of InspectorGeneral Contract Fraud Guidelines

• United States Air Force – Office of SpecialInvestigations Fraud Indicators and Schemes

• Association of Certified Fraud Examiners

After receiving a lead you developed a “fraudscheme theory” – basically you give it yourbest guess as to how the fraud scheme wascorrupting the processes and by who.

What allows you to be more effective is your knowledge of processes that the scheme might be corrupting.

Fraud Scheme Theory

You must understand your organizational acquisitionpolicies, the people involved in the processes, andhow the more traditional procurement fraud schemesoperate in order to do this.

Do you know your P-P-S?

POLICIES – PEOPLE – SCHEMES

When a fraud has occurred it will usually involve more then onestatute that has been violated. The purpose of a fraudexamination is to develop evidence that each of the elements ofa specific criminal or civil violation exists.

In addition to criminal penalties, individuals and corporationsmay be subject to civil monetary penalties and damages. Thevictimized organization may also seek administrative remedies.

A single set of facts may form the basis for a criminal case, acivil action, administrative remedies, and the implementation ofnew internal controls or an audit.

Damages

Contract provisions are a notorious area inwhich auditors and investigators believe theyhave clear evidence of theft only to discoverthat the money was taken in compliance with aprovision of the contract that the auditor orinvestigator failed to study and understand.

Read the CONTRACT!

Important to remember – The differencebetween authority and influence –

Sometimes in procurement fraud it is theinfluence over the authority that has thegreater impact.

Authority vs. Influence

Develop an Investigative Plan

1. Identifying sources of information

2. Collecting, organizing, and processing information

3. Conducting interviews

4. Analyzing information

5. Concluding the investigation

Identify Sources of Information

• Know where importantevidentiary informationmight be stored.

• Focus on identifyingsources that might berelevant to the incidentat issue.

Identify Sources of Information

• Hotline reports• Previous investigation

reports• Internal audit reports• Legal files• HR/Personnel files

• Ethics and compliance questionnaires

• Training records• Contracts!• Accounting records

External Sources of Information

• Public records• Nonpublic records (bank

records, credit reports)• Commercial databases• Internet sources• Social media sites• Media records• Third-party records

Collect, Organize, and Process Information

• Identify documents critical to the investigation.

• Know the options available for searching,analyzing, and reviewing digital data.

• Employ rigorous data collection and retentionpractices.

Analyze the Information

• Often involves analytical software

• Procurement fraud analysis typically focuses on:Customer account filesVendor master fileThird-party filesFinancial accounts and transaction recordsPayroll accountsGeneral ledger accountsInvoices

Conduct Interviews

• Plan for interviews!• Address practical

considerations.• Consider potential legal

issues.• Protect confidentiality.• Document interviews.

o Within how many days?

Conclude the Investigation • Analyze your documents

and interviews;• Outline your agency policy

violation(s) and/or law(s);• Draft your Findings and

Recommendations;• Do a quality control on work

papers; and• Enter all data into your

system (if applicable)

Investigative tools to consider during aprocurement or contract investigation are:

A. SubpoenasB. Search warrantsC. Mail covers

Tools to Consider

Review

Review