anglo pacific group plc - shares magazine

TRANSCRIPT

Anglo Pacific Group PLC

FINANCING INVESTMENT IN NATURAL RESOURCES TO ENABLE A SUSTAINABLE FUTURE

April 2021

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

IMPORTANT DISCLAIMER

This document has been prepared and issued by and is the sole responsibility of Anglo Pacific Group PLC (the “Company”) and its subsidiaries (the “Group”) for selected recipients. It comprises the written materials for a presentation to investors and/or industry professionals concerning the Group’s business activities. It is not an offer or invitation to subscribe for or purchase any securities and nothing contained herein shall form the basis of any contract or commitment whatsoever. This presentation does not constitute or form part of any offer or invitation to sell or issue, or any solicitation of any offer to purchase or subscribe for, any shares in the Company in any jurisdiction nor shall it or any part of it nor the fact of its distribution form the basis of, or be relied on in connection with, any contract commitment or investment decision in relation thereto nor does it constitute a recommendation regarding the securities of the Company. This presentation is for informational purposes only and may not be used for any other purposes.

Certain statements in this presentation are forward-looking statements based on certain assumptions and reflect the Group’s expectations and views of future events. Forward-looking statements (which includes any statement which constitutes ‘forward-looking information’ for the purposes of Canadian securities legislation) may include, without limitation, statements regarding the operations, business, financial condition, expected financial results, cash flow, requirement for and terms of additional financing, performance, prospects, opportunities, priorities, targets, goals, objectives, strategies, growth and outlook of the Group including the outlook for the markets and economies in which the Group operates, costs and timing of acquiring new royalties and making new investments, mineral reserve and resources estimates, estimates of future production, production costs and revenue, future demand for and prices of precious and base metals and other commodities and future demand for products which include precious and base metals and other commodities, for the current fiscal year and subsequent periods. Forward-looking statements include statements that are predictive in nature, depend upon or refer to future events or conditions, or include words such as, amongst others, ‘expects’, ‘anticipates’, ‘plans’, ‘believes’, ‘estimates’, ‘seeks’, ‘intends’, ‘targets’, ‘projects’, ‘forecasts’, ‘potential’, ‘positioned’, ‘strategy’, ‘outlook’, ‘predict’ or negative versions thereof and other similar expressions, or future or conditional verbs such as ‘may’, ‘will’, ‘should’, ‘would’ and ‘could’. These include statements regarding our intentions, beliefs or current expectations concerning, amongst other things, our results of operations, financial condition, liquidity, prospects, growth, strategies and the economic and business circumstances occurring from time to time in the countries and markets in which the Group operates.

Forward-looking statements are based upon certain material factors that were applied in drawing a conclusion or making a forecast or projection, including assumptions and analyses made by the Group in light ofits experience and perception of historical trends, current conditions and expected future developments, as well as other factors that are believed to be appropriate in the circumstances. The material factors and assumptions upon which such forward-looking statements are based include: the stability of the global economy; the stability of local governments and legislative background; the relative stability of interest rates; the equity and debt markets continuing to provide access to capital; the continuing of ongoing operations of the properties underlying the Group’s portfolio of royalties, streams and investments by the owners or operators of such properties in a manner consistent with past practice and/or with production projections, including the on-going financial viability of such operators and operations; no material adverse impact on the underlying operations of the Group’s portfolio of royalties, steams and investments from the global pandemic; the accuracy of public statements and disclosures (including feasibility studies, estimates of reserve, resource, production, grades, mine life and cash cost) made by the owners or operators of such underlying properties; the accuracy of the information provided to the Group by the owners and operators of such underlying properties; contractual terms honoured of the Group’s royalty and stream investments, together with those of the owners and operators of the underlying properties; no material adverse change in the price of the commodities produced from the properties underlying the Group’s portfolio of royalties, streams and investments; no material adverse change in foreign exchange exposure; no adverse development in respect of any significant property in which the Group holds a royalty or other interest, including but not limited to unusual or unexpected geological formations and natural disasters; successful completion of new development projects; planned expansions or additional projects being within the timelines anticipated and at anticipated production levels; and maintenance of mining title.

Forward-looking statements are provided for the purposes of assisting readers in understanding the Group’s financial position and results of operations as at and for the periods ended on certain dates, and of presenting information about management’s current expectations and plans relating to the future. It is believed that the expectations reflected in this presentation are reasonable but they may be affected by a wide range of variables that could cause actual results to differ materially from those currently anticipated. Readers are cautioned that such forward-looking statements may not be appropriate other than for purposes outlined in this presentation. Forward-looking statements are not guarantees of future performance and involve risks, uncertainties and assumptions, that may be general or specific, which could cause actual results to differ materially from those forecast, anticipated, estimated or intended in the forward-looking statements. Past performance is no guide to future performance and persons needing advice should consult an independent financial adviser. The forward-looking statements made in this presentation relate only to events or information as of the date on which the statements are made and, except as specifically required by applicable laws, listing rules and other regulations, the Group undertakes no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events.

No statement in this communication is intended to be, nor should it be construed as, a profit forecast or a profit estimate and no statement in this presentation should be interpreted to mean that earnings per share for the current or any future financial periods would necessarily match, exceed or be lower than the historical published earnings per share. Forward-looking statements involve estimates and assumptions that are subject to risks, uncertainties and other factors that could cause actual future financial condition, performance and results to differ materially from the plans, goals, expectations and results expressed in the forward-looking statements and other financial and/or statistical data within this presentation. . Such risks and uncertainties include, but are not limited to: the failure to realise contemplated benefits from acquisitions and other royalty and stream investments; the effect of any mergers, acquisitions and divestitures on the Group’s operating results and businesses generally; current global financial conditions; royalty, stream and investment portfolio and associated risk; adverse development risk; financial viability and operational effectiveness of owners and operators of the relevant properties underlying the Group’s portfolio of royalties, streams and investments; royalties, steams and investments subject to other rights; and contractual terms not being honoured, together with those risks identified in the ‘Principal Risks and Uncertainties’ section of our most recent Annual Report, which is available on our website. If any such risks actually occur, they could materially adversely affect the Group’s business, financial condition or results of operations. Readers are cautioned that the list of factors noted in the section herein entitled ‘Risk’ is not exhaustive of the factors that may affect the Group’s forward-looking statements. Readers are also cautioned to consider these and the other factors, uncertainties and potential events carefully and not to put undue reliance on forward-looking statements.

This presentation also contains forward-looking information contained and derived from publicly available information regarding properties and mining operations owned by third parties. This presentation contains information and statements relating to the Kestrel mine that are based on certain estimates and forecasts that have been provided to the Group by Kestrel Coal Pty Ltd (“KCPL”), the accuracy of which KCPL does not warrant and on which readers may not rely.

2

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

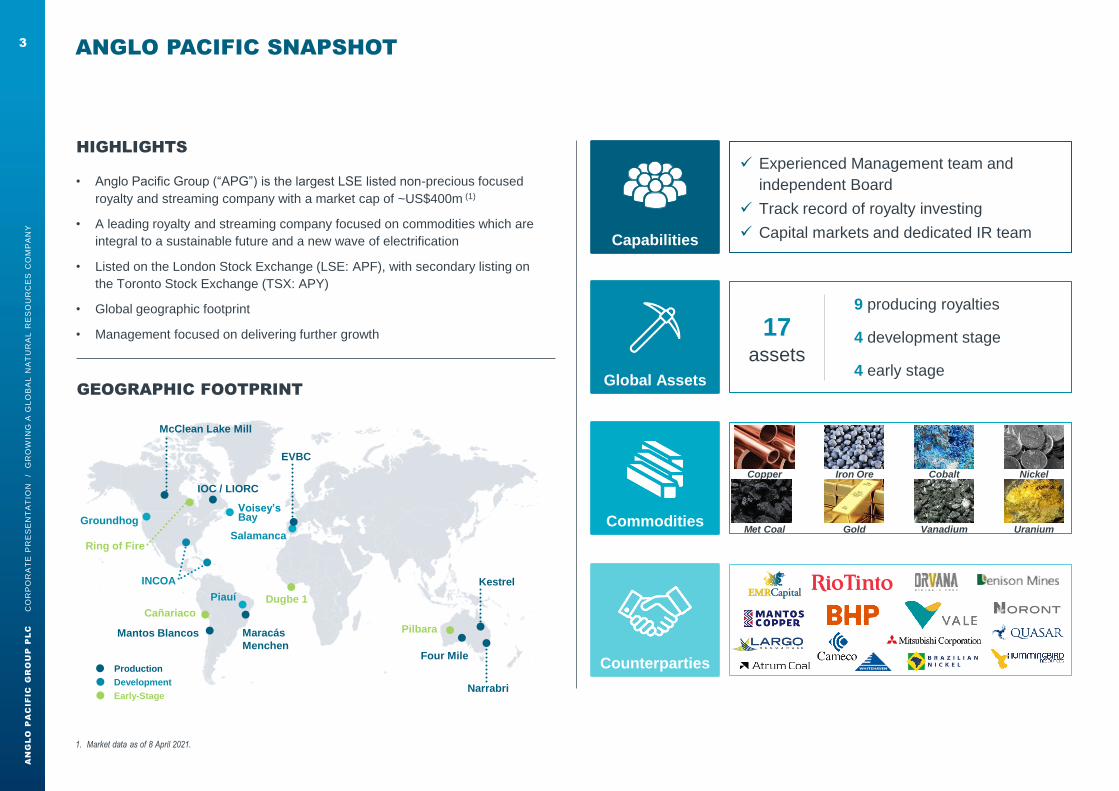

ANGLO PACIFIC SNAPSHOT3

1. Market data as of 8 April 2021.

GEOGRAPHIC FOOTPRINT

HIGHLIGHTS

• Anglo Pacific Group (“APG”) is the largest LSE listed non-precious focused

royalty and streaming company with a market cap of ~US$400m (1)

• A leading royalty and streaming company focused on commodities which are

integral to a sustainable future and a new wave of electrification

• Listed on the London Stock Exchange (LSE: APF), with secondary listing on

the Toronto Stock Exchange (TSX: APY)

• Global geographic footprint

• Management focused on delivering further growth

Capabilities

✓ Experienced Management team and

independent Board

✓ Track record of royalty investing

✓ Capital markets and dedicated IR team

Global Assets

9 producing royalties

4 development stage

4 early stage

17assets

Counterparties

Commodities

Copper Iron Ore Cobalt Nickel

Met Coal Gold Vanadium Uranium

McClean Lake Mill

EVBC

Salamanca

Groundhog

Ring of Fire

INCOA

Cañariaco

Dugbe 1

Mantos Blancos Maracás

Menchen

Piauí

Kestrel

Narrabri

Pilbara

Four MileProduction

Early-Stage

Development

IOC / LIORC

Voisey’s Bay

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

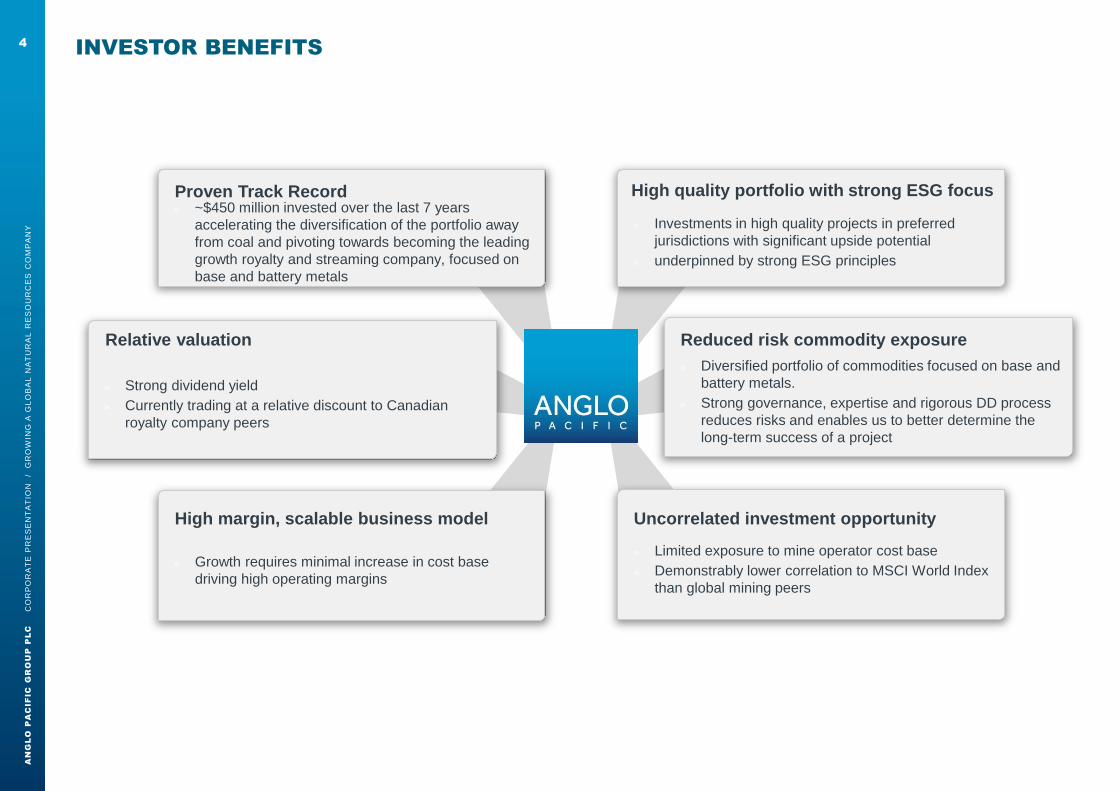

INVESTOR BENEFITS 4

» ~$450 million invested over the last 7 years

accelerating the diversification of the portfolio away

from coal and pivoting towards becoming the leading

growth royalty and streaming company, focused on

base and battery metals

» Strong dividend yield

» Currently trading at a relative discount to Canadian

royalty company peers

» Growth requires minimal increase in cost base

driving high operating margins

» Limited exposure to mine operator cost base

» Demonstrably lower correlation to MSCI World Index

than global mining peers

» Diversified portfolio of commodities focused on base and

battery metals.

» Strong governance, expertise and rigorous DD process

reduces risks and enables us to better determine the

long-term success of a project

» Investments in high quality projects in preferred

jurisdictions with significant upside potential

» underpinned by strong ESG principles

Relative valuation

High margin, scalable business model

Reduced risk commodity exposure

Uncorrelated investment opportunity

Proven Track Record High quality portfolio with strong ESG focus

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

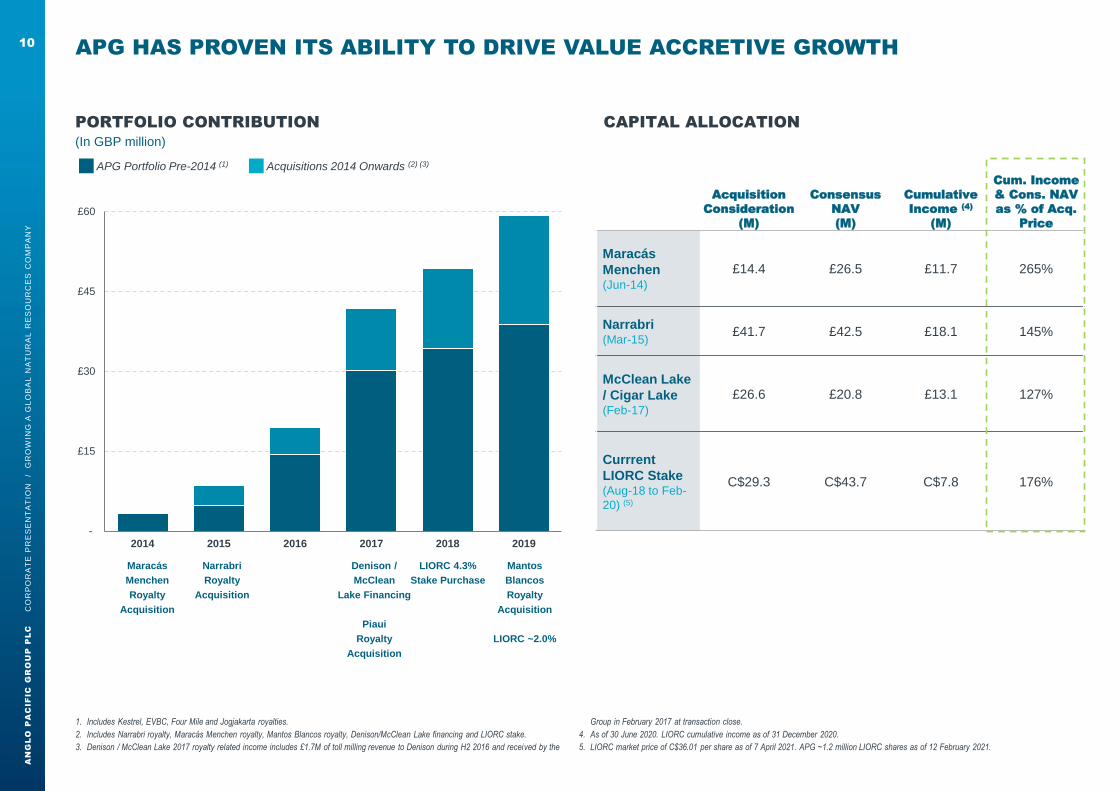

APG HAS PROVEN ITS ABILITY TO DRIVE VALUE ACCRETIVE GROWTH

Acquisition

Consideration

(M)

Consensus

NAV

(M)

Cumulative

Income (4)

(M)

Cum. Income

& Cons. NAV

as % of Acq.

Price

Maracás

Menchen(Jun-14)

£14.4 £26.5 £11.7 265%

Narrabri(Mar-15)

£41.7 £42.5 £18.1 145%

McClean Lake

/ Cigar Lake(Feb-17)

£26.6 £20.8 £13.1 127%

Currrent

LIORC Stake(Aug-18 to Feb-

20) (5)

C$29.3 C$43.7 C$7.8 176%

-

£15

£30

£45

£60

2014 2015 2016 2017 2018 2019

Maracás

Menchen

Royalty

Acquisition

Narrabri

Royalty

Acquisition

Denison /

McClean

Lake Financing

Piaui

Royalty

Acquisition

LIORC 4.3%

Stake Purchase

Mantos

Blancos

Royalty

Acquisition

LIORC ~2.0%

APG Portfolio Pre-2014 (1) Acquisitions 2014 Onwards (2) (3)

PORTFOLIO CONTRIBUTION CAPITAL ALLOCATION

(In GBP million)

10

1. Includes Kestrel, EVBC, Four Mile and Jogjakarta royalties.

2. Includes Narrabri royalty, Maracás Menchen royalty, Mantos Blancos royalty, Denison/McClean Lake financing and LIORC stake.

3. Denison / McClean Lake 2017 royalty related income includes £1.7M of toll milling revenue to Denison during H2 2016 and received by the

Group in February 2017 at transaction close.

4. As of 30 June 2020. LIORC cumulative income as of 31 December 2020.

5. LIORC market price of C$36.01 per share as of 7 April 2021. APG ~1.2 million LIORC shares as of 12 February 2021.

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

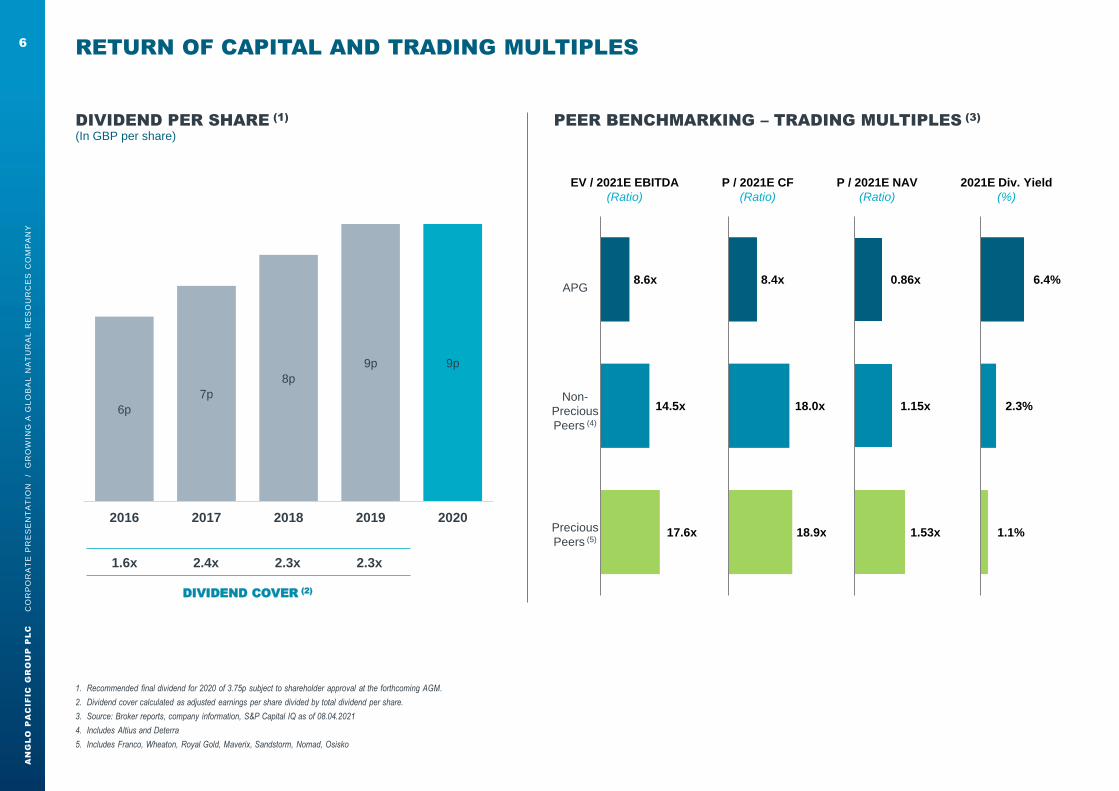

6p

7p

8p

9p 9p

2016 2017 2018 2019 2020

RETURN OF CAPITAL AND TRADING MULTIPLES6

DIVIDEND COVER (2)

1.6x 2.4x 2.3x 2.3x

DIVIDEND PER SHARE (1)

(In GBP per share)

PEER BENCHMARKING – TRADING MULTIPLES (3)

1. Recommended final dividend for 2020 of 3.75p subject to shareholder approval at the forthcoming AGM.

2. Dividend cover calculated as adjusted earnings per share divided by total dividend per share.

3. Source: Broker reports, company information, S&P Capital IQ as of 08.04.2021

4. Includes Altius and Deterra

5. Includes Franco, Wheaton, Royal Gold, Maverix, Sandstorm, Nomad, Osisko

APG

Non-

Precious

Peers (4)

EV / 2021E EBITDA

(Ratio)

P / 2021E CF

(Ratio)

P / 2021E NAV

(Ratio)

2021E Div. Yield

(%)

17.6x

14.5x

8.6x

Precious RoyaltyCo

Non-Precious Peers

APG

18.9x

18.0x

8.4x

Precious RoyaltyCo

Non-Precious Peers

APG

1.1%

2.3%

6.4%

Precious RoyaltyCo

Non-Precious Peers

APG

1.53x

1.15x

0.86x

Precious RoyaltyCo

Non-Precious Peers

APG

Precious

Peers (5)

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

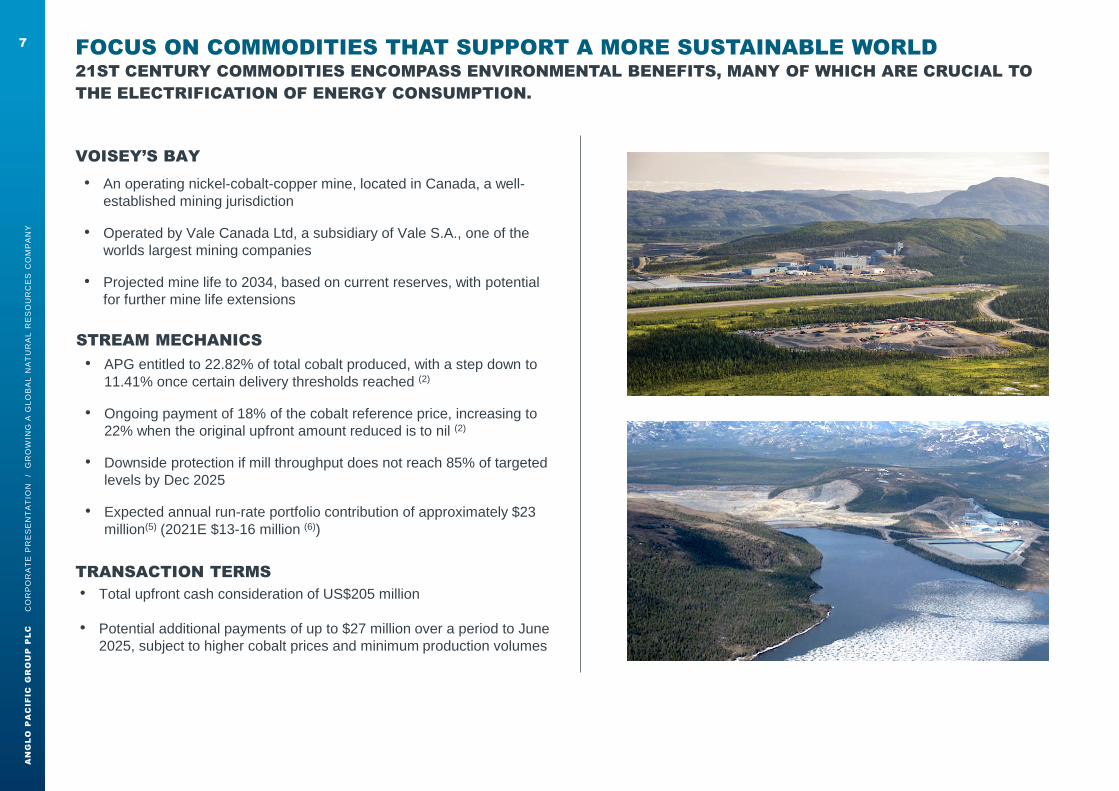

VOISEY’S BAY

• An operating nickel-cobalt-copper mine, located in Canada, a well-

established mining jurisdiction

• Operated by Vale Canada Ltd, a subsidiary of Vale S.A., one of the

worlds largest mining companies

• Projected mine life to 2034, based on current reserves, with potential

for further mine life extensions

• APG entitled to 22.82% of total cobalt produced, with a step down to

11.41% once certain delivery thresholds reached (2)

• Ongoing payment of 18% of the cobalt reference price, increasing to

22% when the original upfront amount reduced is to nil (2)

• Downside protection if mill throughput does not reach 85% of targeted

levels by Dec 2025

• Expected annual run-rate portfolio contribution of approximately $23

million(5) (2021E $13-16 million (6))

STREAM MECHANICS

TRANSACTION TERMS

• Total upfront cash consideration of US$205 million

• Potential additional payments of up to $27 million over a period to June

2025, subject to higher cobalt prices and minimum production volumes

7

21ST CENTURY COMMODITIES ENCOMPASS ENVIRONMENTAL BENEFITS, MANY OF WHICH ARE CRUCIAL TO

THE ELECTRIFICATION OF ENERGY CONSUMPTION.

FOCUS ON COMMODITIES THAT SUPPORT A MORE SUSTAINABLE WORLD

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

ANGLO PACIFIC’S COMMODITY EXPOSURE HAS BEEN TRANSFORMED…8

1. Book value of Anglo Pacific’s royalty related assets as of 31 December 2013, net of deferred tax where applicable, excluding the Cresso, Bulqiza and Amapá which have been impaired to nil carrying value, the Isua royalty which was subsequently disposed, and Jogjakarta which was subsequently bought back.

2. Book value of Anglo Pacific’s royalty related assets as of 31 December 2020 (net of deferred tax where applicable) adjusted for an illustrative US$205 million Voisey’s Bay Cobalt Stream acquisition and a ~75% monetisation of the LIORC stake..

3. Kestrel production primarily coking coal. Narrabri production primarily thermal coal.

4. South American exposure includes Brazil, Chile, and Peru. Europe exposure includes Spain.

YEAR END 2020 ADJUSTED FOR VOISEY’S BAY COBALT STREAM (2)

YEAR END 2013 (1)

Nil%

Battery

Metals

COMMODITY EXPOSURE

Coking coal (3) 76%

9%Iron Ore

Other

4%~60%

Battery

Metals

COMMODITY EXPOSURE

Cobalt 45%

Base metals 11%

Vanadium 4%

Coking coal (3) 12%

Thermal coal (3)

Iron ore

11%

9%

Uranium 7%

Canada 59%

Australia 25%

South America (4) 15%

Europe (4) 1%

GEOGRAPHIC EXPOSURE

Other <1%

GEOGRAPHIC EXPOSURE

Australia 87%

Europe (4) 9%

Canada 4%~93%

OECD

~95%

OECD

Uranium

11%

Other 2%

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

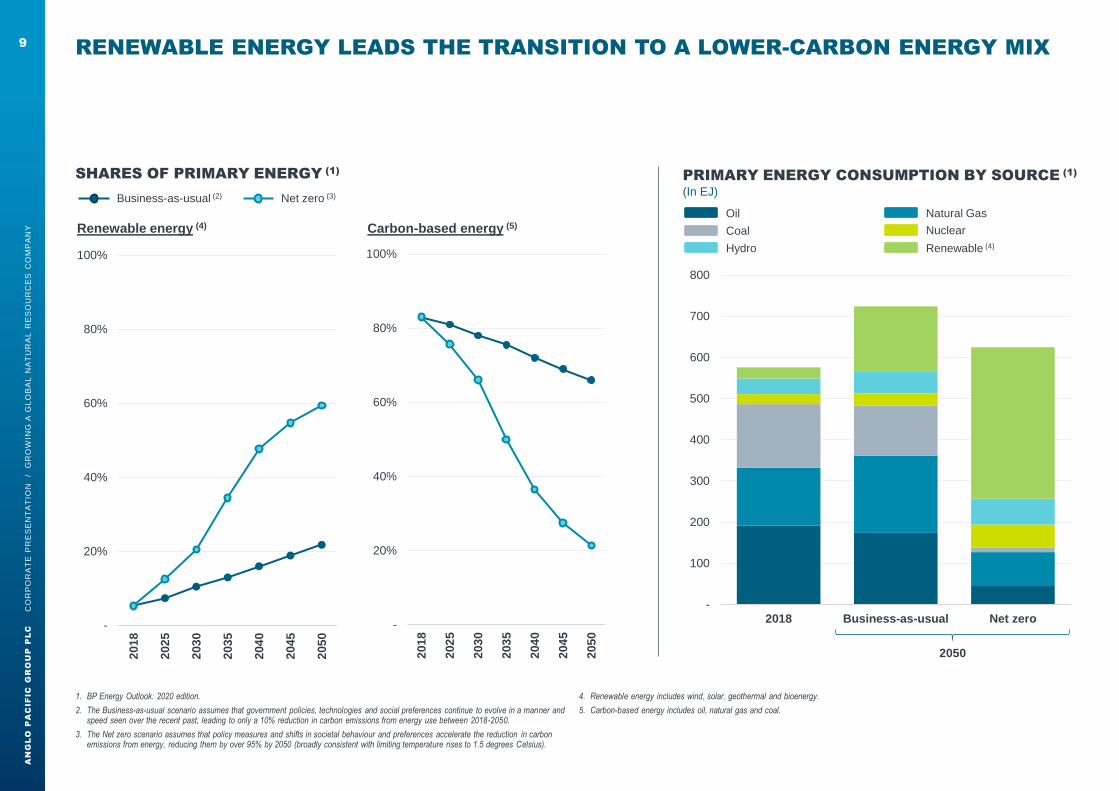

RENEWABLE ENERGY LEADS THE TRANSITION TO A LOWER-CARBON ENERGY MIX 9

1. BP Energy Outlook: 2020 edition.

2. The Business-as-usual scenario assumes that government policies, technologies and social preferences continue to evolve in a manner and speed seen over the recent past, leading to only a 10% reduction in carbon emissions from energy use between 2018-2050.

3. The Net zero scenario assumes that policy measures and shifts in societal behaviour and preferences accelerate the reduction in carbon emissions from energy, reducing them by over 95% by 2050 (broadly consistent with limiting temperature rises to 1.5 degrees Celsius).

4. Renewable energy includes wind, solar, geothermal and bioenergy.

5. Carbon-based energy includes oil, natural gas and coal.

PRIMARY ENERGY CONSUMPTION BY SOURCE (1)

(In EJ)

SHARES OF PRIMARY ENERGY (1)

-

20%

40%

60%

80%

100%

201

8

202

5

203

0

203

5

204

0

2045

2050

-

20%

40%

60%

80%

100%

201

8

202

5

203

0

203

5

204

0

204

5

205

0

Renewable energy (4) Carbon-based energy (5)

Natural GasOil

Hydro

NuclearCoal

Renewable (4)

Business-as-usual (2) Net zero (3)

-

100

200

300

400

500

600

700

800

2018 Business-as-usual Net zero

2050

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

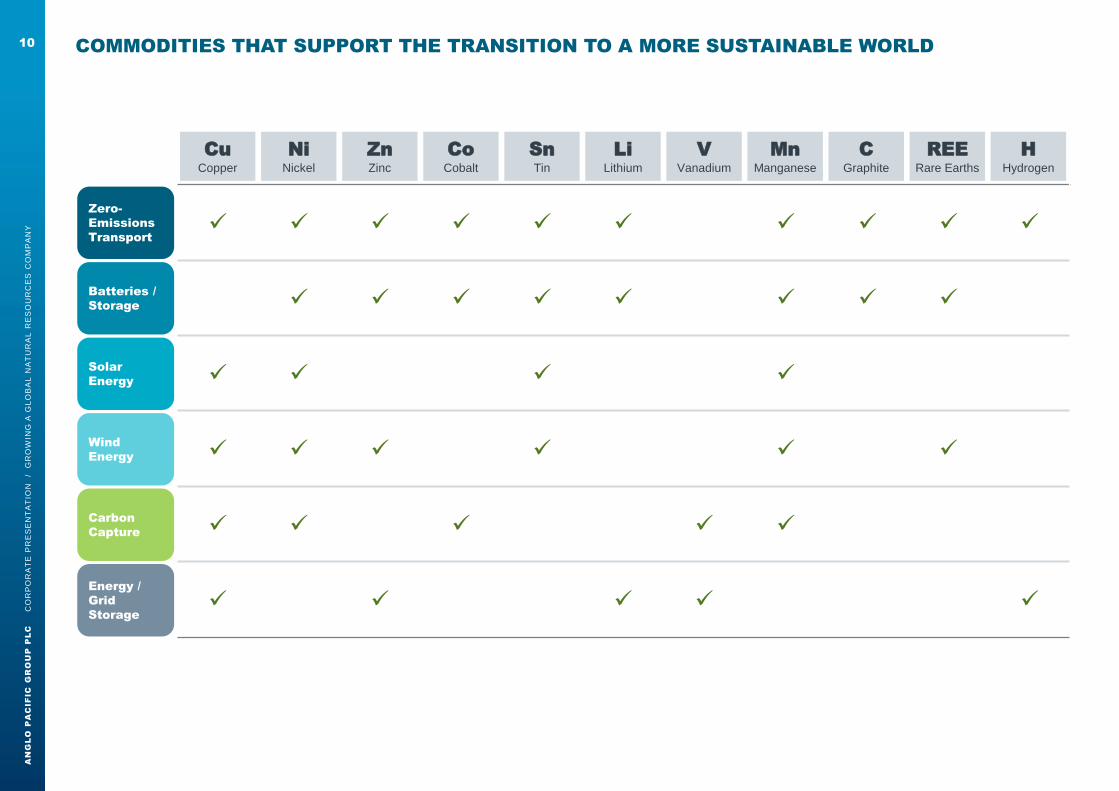

COMMODITIES THAT SUPPORT THE TRANSITION TO A MORE SUSTAINABLE WORLD 10

Copper Nickel Zinc Cobalt Tin Lithium Vanadium Manganese Graphite

Rare

Earths

Green

Hydrogen

Zero-

Emissions

Transport✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Batteries /

Storage ✓ ✓ ✓ ✓ ✓ ✓ ✓ ✓

Solar

Energy ✓ ✓ ✓ ✓

Wind Energy ✓ ✓ ✓ ✓ ✓ ✓

Carbon

Capture ✓ ✓ ✓ ✓ ✓

Energy /

Grid Storage ✓ ✓ ✓ ✓ ✓

Zero-

Emissions

Transport

Energy /

Grid

Storage

Carbon

Capture

Wind

Energy

Solar

Energy

Batteries /

Storage

CuCopper

NiNickel

ZnZinc

CoCobalt

SnTin

LiLithium

VVanadium

MnManganese

CGraphite

REERare Earths

HHydrogen

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

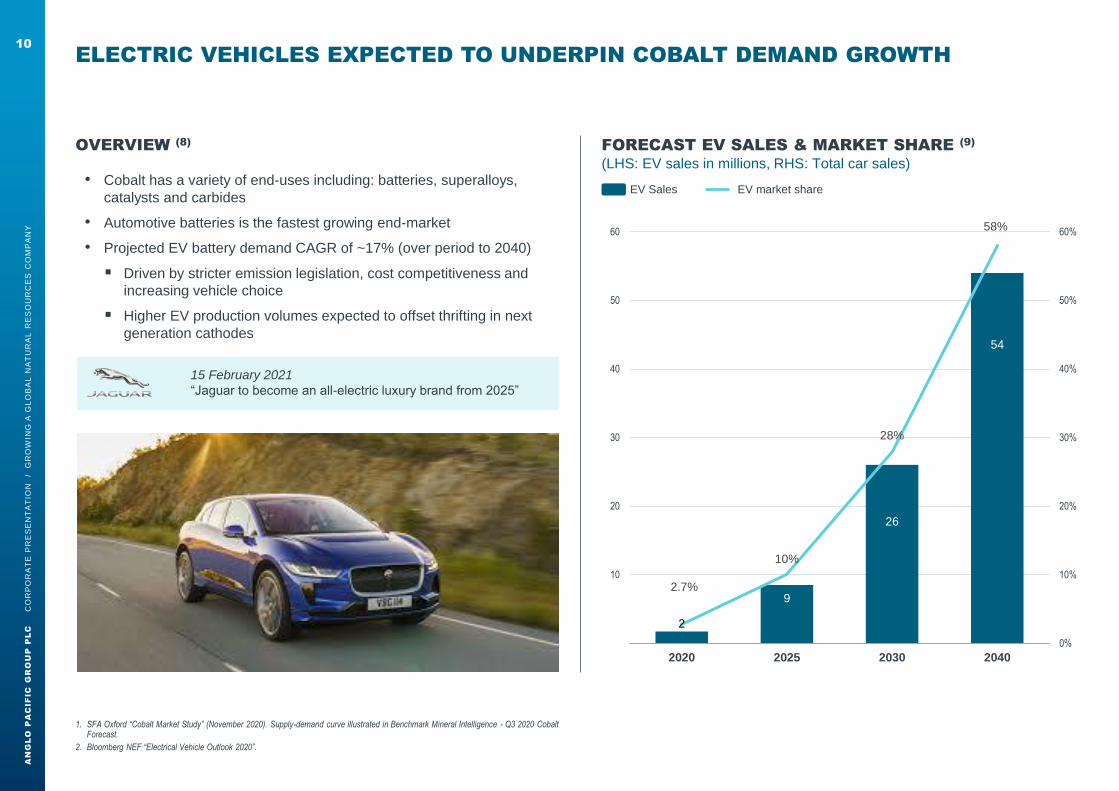

ELECTRIC VEHICLES EXPECTED TO UNDERPIN COBALT DEMAND GROWTH

FORECAST EV SALES & MARKET SHARE (9)

(LHS: EV sales in millions, RHS: Total car sales)

EV Sales EV market share

2

9

26

54

2.7%

10%

28%

58%

0%

10%

20%

30%

40%

50%

60%

10

20

30

40

50

60

2020 2025 2030 2040

OVERVIEW (8)

• Cobalt has a variety of end-uses including: batteries, superalloys,

catalysts and carbides

• Automotive batteries is the fastest growing end-market

• Projected EV battery demand CAGR of ~17% (over period to 2040)

▪ Driven by stricter emission legislation, cost competitiveness and

increasing vehicle choice

▪ Higher EV production volumes expected to offset thrifting in next

generation cathodes

15 February 2021

“Jaguar to become an all-electric luxury brand from 2025”

10

1. SFA Oxford “Cobalt Market Study” (November 2020). Supply-demand curve illustrated in Benchmark Mineral Intelligence - Q3 2020 Cobalt Forecast.

2. Bloomberg NEF “Electrical Vehicle Outlook 2020”.

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

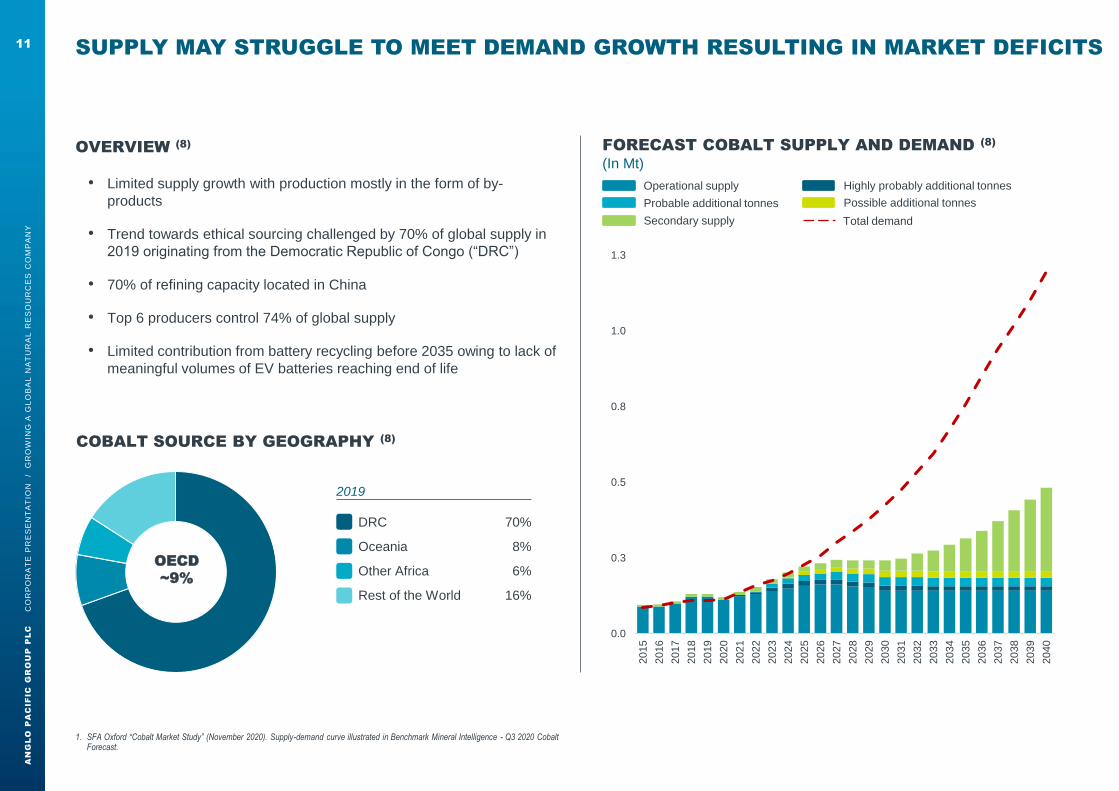

SUPPLY MAY STRUGGLE TO MEET DEMAND GROWTH RESULTING IN MARKET DEFICITS

FORECAST COBALT SUPPLY AND DEMAND (8)

(In Mt)OVERVIEW (8)

• Limited supply growth with production mostly in the form of by-

products

• Trend towards ethical sourcing challenged by 70% of global supply in

2019 originating from the Democratic Republic of Congo (“DRC”)

• 70% of refining capacity located in China

• Top 6 producers control 74% of global supply

• Limited contribution from battery recycling before 2035 owing to lack of

meaningful volumes of EV batteries reaching end of life

COBALT SOURCE BY GEOGRAPHY (8)

DRC 70%

Oceania 8%

Other Africa 6%

Rest of the World 16%

2019

OECD

~9%

0.0

0.3

0.5

0.8

1.0

1.3

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

Highly probably additional tonnesOperational supply

Secondary supply

Possible additional tonnesProbable additional tonnes

Total demand

11

1. SFA Oxford “Cobalt Market Study” (November 2020). Supply-demand curve illustrated in Benchmark Mineral Intelligence - Q3 2020 Cobalt Forecast.

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

HIGHLIGHTS AND OUTLOOK13

HIGHLIGHTS

• World class royalty and streaming portfolio

• Demonstrated ability to grow and diversify the portfolio

• Milestone cobalt stream acquired in March 2021, setting Anglo Pacific on the road to become the leading growth

royalty and streaming company, focused on base and battery metals

• Significant progress made on ESG

• Commitment made to make no further investment in thermal coal

OUTLOOK

• Closely monitoring and evaluating the impact of COVID-19

• At this time, the mines underlying the Company’s material royalty related revenue remain in production

• All Anglo Pacific staff members remain working remotely, and investment opportunities being pursued

• Commodity prices underpinning the Group’s revenues have seen mixed impact year to date, although most

have started recovering

• Healthy organic portfolio contribution growth expected in 2021

• Active pipeline and financial flexibility to continue to add to its world class royalty and streaming portfolio

• Strong dividend yield

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

MORE TO COME …

SOLID PLATFORM FOR INVESTORS

& WELL POSITIONED FOR GROWTH AND TO BECOME THE LEADING ROYALTY

AND STREAMING COMPANY IN BASE AND BATTERY METALS

14

MORE TO COME …

… THANK YOU

14

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

APPENDIX

15

• PORTFOLIO OVERVIEW

• ROYALTIES AND STREAMING EXPLAINED

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

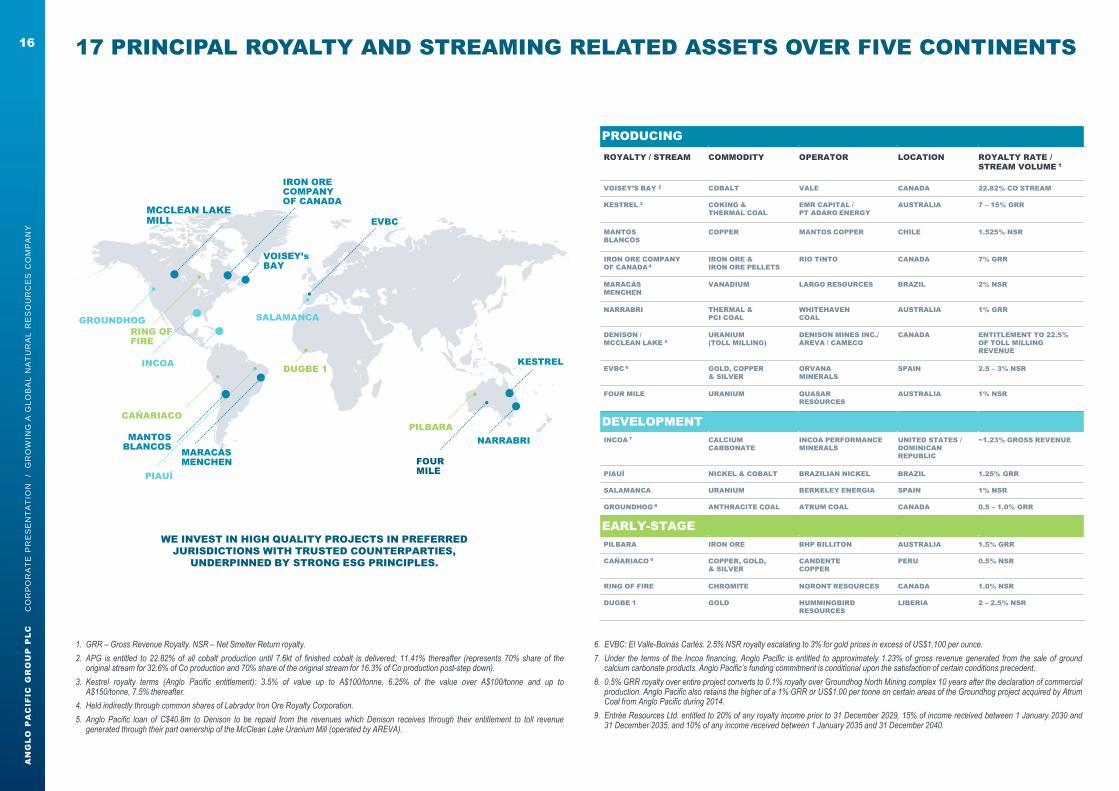

17 PRINCIPAL ROYALTY AND STREAMING RELATED ASSETS OVER FIVE CONTINENTS16

MCCLEAN LAKE MILL

GROUNDHOG

RING OF FIRE

CAÑARIACO

PIAUÍ

MARACÁS MENCHEN

DUGBE 1

PILBARA

FOUR MILE

NARRABRI

KESTREL

SALAMANCA

EVBC

MANTOSBLANCOS

PRODUCING

ROYALTY / STREAM COMMODITY OPERATOR LOCATION ROYALTY RATE /

STREAM VOLUME 1

VOISEY’S BAY 2 COBALT VALE CANADA 22.82% CO STREAM

KESTREL 3 COKING &

THERMAL COAL

EMR CAPITAL /

PT ADARO ENERGY

AUSTRALIA 7 – 15% GRR

MANTOS

BLANCOS

COPPER MANTOS COPPER CHILE 1.525% NSR

IRON ORE COMPANY

OF CANADA4

IRON ORE &

IRON ORE PELLETS

RIO TINTO CANADA 7% GRR

MARACÁS

MENCHEN

VANADIUM LARGO RESOURCES BRAZIL 2% NSR

NARRABRI THERMAL &

PCI COAL

WHITEHAVEN

COAL

AUSTRALIA 1% GRR

DENISON /

MCCLEAN LAKE 5URANIUM

(TOLL MILLING)

DENISON MINES INC./

AREVA / CAMECO

CANADA ENTITLEMENT TO 22.5%

OF TOLL MILLING

REVENUE

EVBC 6 GOLD, COPPER

& SILVER

ORVANA

MINERALS

SPAIN 2.5 – 3% NSR

FOUR MILE URANIUM QUASAR

RESOURCES

AUSTRALIA 1% NSR

DEVELOPMENT

INCOA 7 CALCIUM

CARBONATE

INCOA PERFORMANCE

MINERALS

UNITED STATES /

DOMINICAN

REPUBLIC

~1.23% GROSS REVENUE

PIAUÍ NICKEL & COBALT BRAZILIAN NICKEL BRAZIL 1.25% GRR

SALAMANCA URANIUM BERKELEY ENERGIA SPAIN 1% NSR

GROUNDHOG 8 ANTHRACITE COAL ATRUM COAL CANADA 0.5 – 1.0% GRR

EARLY-STAGE

PILBARA IRON ORE BHP BILLITON AUSTRALIA 1.5% GRR

CAÑARIACO 9 COPPER, GOLD,

& SILVER

CANDENTE

COPPER

PERU 0.5% NSR

RING OF FIRE CHROMITE NORONT RESOURCES CANADA 1.0% NSR

DUGBE 1 GOLD HUMMINGBIRD

RESOURCES

LIBERIA 2 – 2.5% NSR

INCOA

WE INVEST IN HIGH QUALITY PROJECTS IN PREFERRED

JURISDICTIONS WITH TRUSTED COUNTERPARTIES,

UNDERPINNED BY STRONG ESG PRINCIPLES.

VOISEY’sBAY

IRON ORE COMPANY OF CANADA

1. GRR – Gross Revenue Royalty. NSR – Net Smelter Return royalty.

2. APG is entitled to 22.82% of all cobalt production until 7.6kt of finished cobalt is delivered; 11.41% thereafter (represents 70% share of theoriginal stream for 32.6% of Co production and 70% share of the original stream for 16.3% of Co production post-step down).

3. Kestrel royalty terms (Anglo Pacific entitlement): 3.5% of value up to A$100/tonne, 6.25% of the value over A$100/tonne and up toA$150/tonne, 7.5% thereafter.

4. Held indirectly through common shares of Labrador Iron Ore Royalty Corporation.

5. Anglo Pacific loan of C$40.8m to Denison to be repaid from the revenues which Denison receives through their entitlement to toll revenuegenerated through their part ownership of the McClean Lake Uranium Mill (operated by AREVA).

6. EVBC: El Valle-Boinás Carlés. 2.5% NSR royalty escalating to 3% for gold prices in excess of US$1,100 per ounce.

7. Under the terms of the Incoa financing, Anglo Pacific is entitled to approximately 1.23% of gross revenue generated from the sale of groundcalcium carbonate products. Anglo Pacific’s funding commitment is conditional upon the satisfaction of certain conditions precedent.

8. 0.5% GRR royalty over entire project converts to 0.1% royalty over Groundhog North Mining complex 10 years after the declaration of commercialproduction. Anglo Pacific also retains the higher of a 1% GRR or US$1.00 per tonne on certain areas of the Groundhog project acquired by AtrumCoal from Anglo Pacific during 2014.

9. Entrée Resources Ltd. entitled to 20% of any royalty income prior to 31 December 2029, 15% of income received between 1 January 2030 and31 December 2035, and 10% of any income received between 1 January 2035 and 31 December 2040.

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

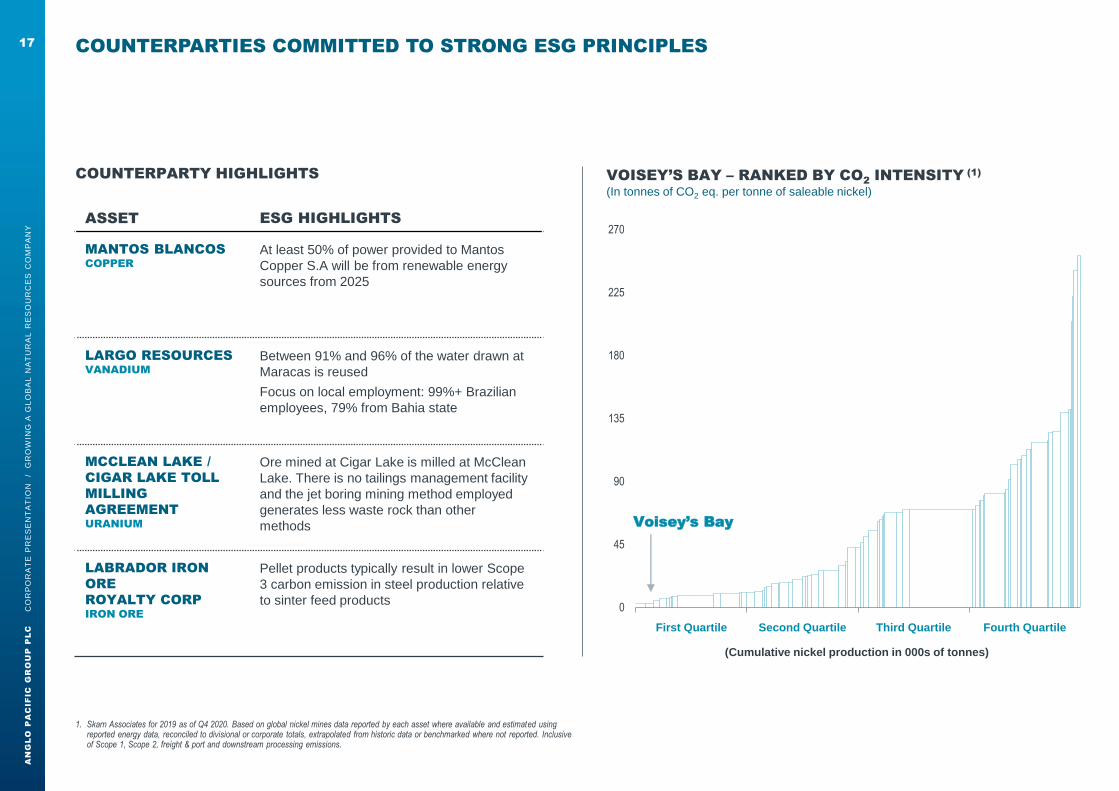

COUNTERPARTIES COMMITTED TO STRONG ESG PRINCIPLES 17

1. Skarn Associates for 2019 as of Q4 2020. Based on global nickel mines data reported by each asset where available and estimated using reported energy data, reconciled to divisional or corporate totals, extrapolated from historic data or benchmarked where not reported. Inclusive of Scope 1, Scope 2, freight & port and downstream processing emissions.

ASSET ESG HIGHLIGHTS

MANTOS BLANCOSCOPPER

At least 50% of power provided to Mantos

Copper S.A will be from renewable energy

sources from 2025

LARGO RESOURCESVANADIUM

Between 91% and 96% of the water drawn at

Maracas is reused

Focus on local employment: 99%+ Brazilian

employees, 79% from Bahia state

MCCLEAN LAKE /

CIGAR LAKE TOLL

MILLING

AGREEMENT URANIUM

Ore mined at Cigar Lake is milled at McClean

Lake. There is no tailings management facility

and the jet boring mining method employed

generates less waste rock than other

methods

LABRADOR IRON

ORE

ROYALTY CORP IRON ORE

Pellet products typically result in lower Scope

3 carbon emission in steel production relative

to sinter feed products

VOISEY’S BAY – RANKED BY CO2 INTENSITY (1)

(In tonnes of CO2 eq. per tonne of saleable nickel)

COUNTERPARTY HIGHLIGHTS

0

45

90

135

180

225

270

(Cumulative nickel production in 000s of tonnes)

Voisey’s Bay

First Quartile Second Quartile Third Quartile Fourth Quartile

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

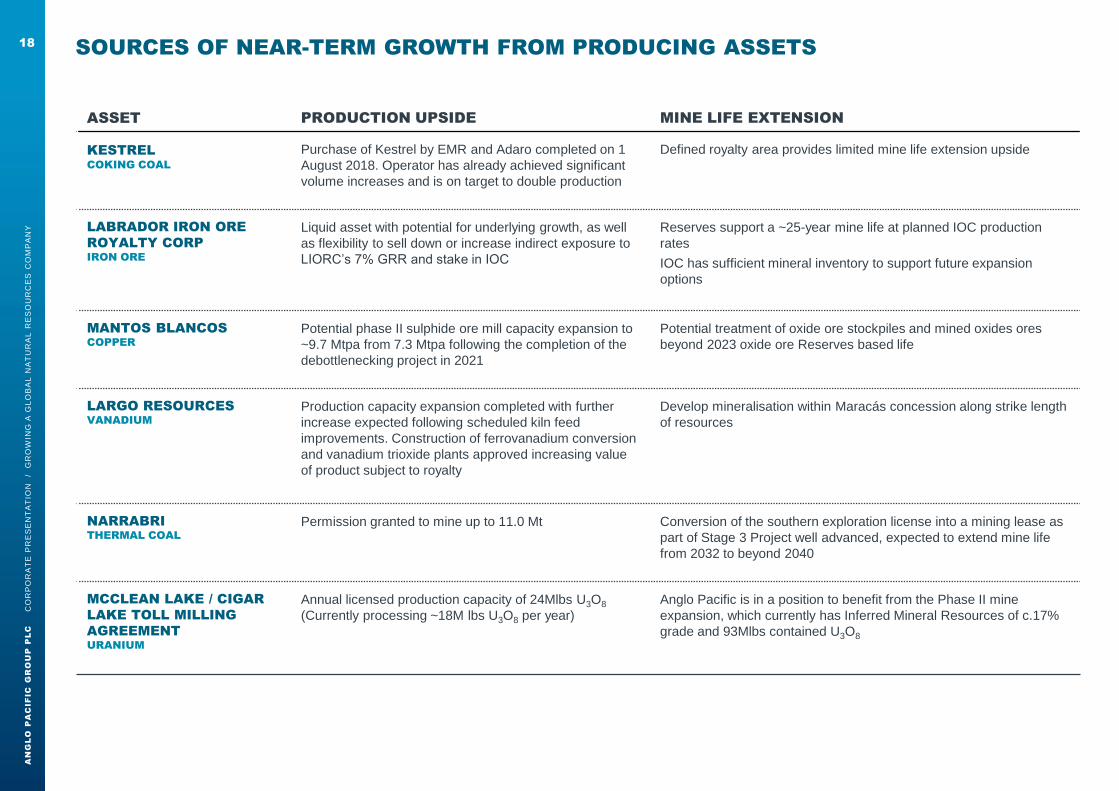

18 SOURCES OF NEAR-TERM GROWTH FROM PRODUCING ASSETS

ASSET PRODUCTION UPSIDE MINE LIFE EXTENSION

KESTRELCOKING COAL

Purchase of Kestrel by EMR and Adaro completed on 1

August 2018. Operator has already achieved significant

volume increases and is on target to double production

Defined royalty area provides limited mine life extension upside

LABRADOR IRON ORE

ROYALTY CORP IRON ORE

Liquid asset with potential for underlying growth, as well

as flexibility to sell down or increase indirect exposure to

LIORC’s 7% GRR and stake in IOC

Reserves support a ~25-year mine life at planned IOC production

rates

IOC has sufficient mineral inventory to support future expansion

options

MANTOS BLANCOSCOPPER

Potential phase II sulphide ore mill capacity expansion to

~9.7 Mtpa from 7.3 Mtpa following the completion of the

debottlenecking project in 2021

Potential treatment of oxide ore stockpiles and mined oxides ores

beyond 2023 oxide ore Reserves based life

LARGO RESOURCESVANADIUM

Production capacity expansion completed with further

increase expected following scheduled kiln feed

improvements. Construction of ferrovanadium conversion

and vanadium trioxide plants approved increasing value

of product subject to royalty

Develop mineralisation within Maracás concession along strike length

of resources

NARRABRI THERMAL COAL

Permission granted to mine up to 11.0 Mt Conversion of the southern exploration license into a mining lease as

part of Stage 3 Project well advanced, expected to extend mine life

from 2032 to beyond 2040

MCCLEAN LAKE / CIGAR

LAKE TOLL MILLING

AGREEMENT URANIUM

Annual licensed production capacity of 24Mlbs U3O8

(Currently processing ~18M lbs U3O8 per year)

Anglo Pacific is in a position to benefit from the Phase II mine

expansion, which currently has Inferred Mineral Resources of c.17%

grade and 93Mlbs contained U3O8

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

19

• ROYALTIES AND STREAMING EXPLAINED

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

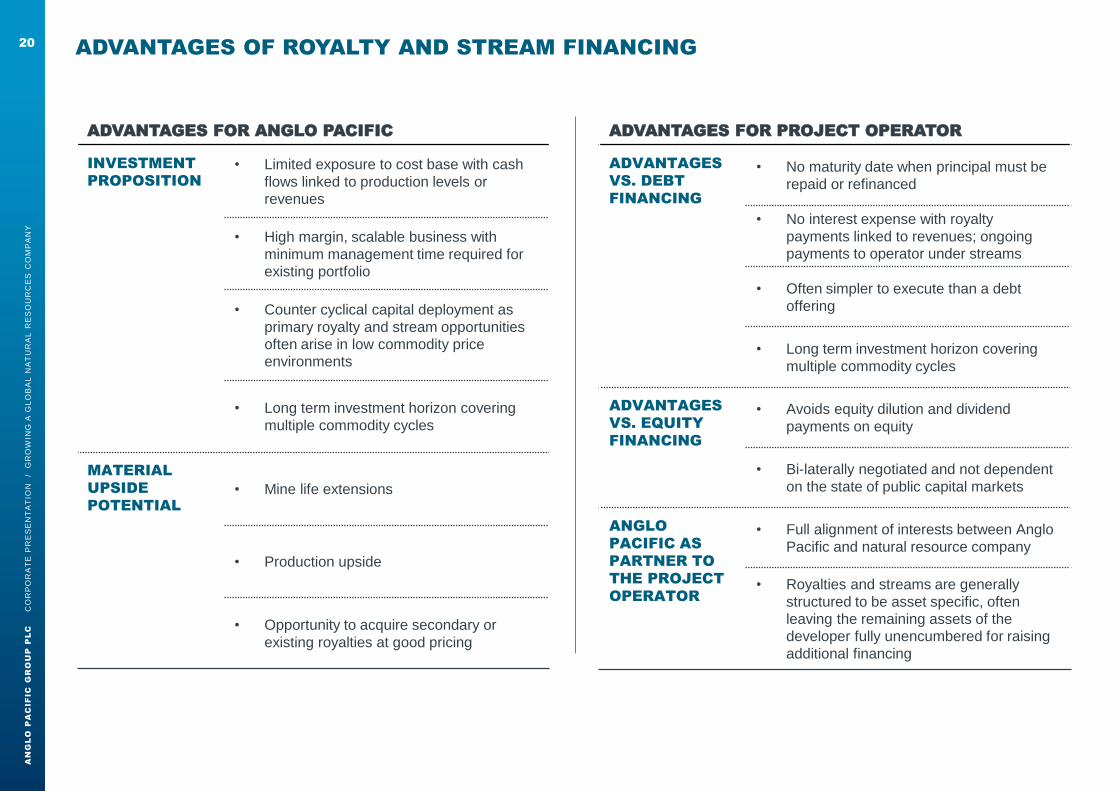

ADVANTAGES FOR ANGLO PACIFIC

INVESTMENT

PROPOSITION• Limited exposure to cost base with cash

flows linked to production levels or

revenues

• High margin, scalable business with

minimum management time required for

existing portfolio

• Counter cyclical capital deployment as

primary royalty and stream opportunities

often arise in low commodity price

environments

• Long term investment horizon covering

multiple commodity cycles

MATERIAL

UPSIDE

POTENTIAL• Mine life extensions

• Production upside

• Opportunity to acquire secondary or

existing royalties at good pricing

ADVANTAGES OF ROYALTY AND STREAM FINANCING20

ADVANTAGES FOR PROJECT OPERATOR

ADVANTAGES

VS. DEBT

FINANCING

• No maturity date when principal must be

repaid or refinanced

• No interest expense with royalty

payments linked to revenues; ongoing

payments to operator under streams

• Often simpler to execute than a debt

offering

• Long term investment horizon covering

multiple commodity cycles

ADVANTAGES

VS. EQUITY

FINANCING

• Avoids equity dilution and dividend

payments on equity

• Bi-laterally negotiated and not dependent

on the state of public capital markets

ANGLO

PACIFIC AS

PARTNER TO

THE PROJECT

OPERATOR

• Full alignment of interests between Anglo

Pacific and natural resource company

• Royalties and streams are generally

structured to be asset specific, often

leaving the remaining assets of the

developer fully unencumbered for raising

additional financing

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

ANGLO PACIFIC’S DISCIPLINED APPROACH TO ROYALTY/STREAM ACQUISITIONS

21

21

WE DILIGENTLY EVALUATE EACH PROJECT, ENSURING ITS VIABILITY FOR PRODUCTION AND POTENTIAL EXPLORATION UPSIDE. WE SELECT THE BEST OPERATIONS, DILIGENTLY GROWING REVENUE STREAMS.

THIS STABLE CASHFLOW ALLOWS US TO BUY MORE ROYALTIES AND STREAMS ON MORE MINES, PROVIDING OUR INVESTORS WITH A DIVERSIFIED PORTFOLIO

▪ Lighter, greener materials, which encompass environmental benefits and many of which form part of the

new wave of technologies around electrification, including renewable energy

▪ Examples include higher quality and more energy efficient iron ore and pellets, base metals linked to

energy storage or power transition, specialist alloying materials like niobium, vanadium and aluminium and

battery materials like lithium, cobalt and nickel

▪ No further investment in thermal coal assets

▪ High-quality and low-cost assets

▪ Well established natural resources jurisdictions

▪ Strong ESG credentials

▪ Strong operational management teams

▪ Long-life assets

▪ Diversification of royalty portfolio

▪ Production and exploration upside potential

▪ Strong returns

Commodity

Focus

Investment

Criteria

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

ANGLO PACIFIC

ANGLO PACIFIC

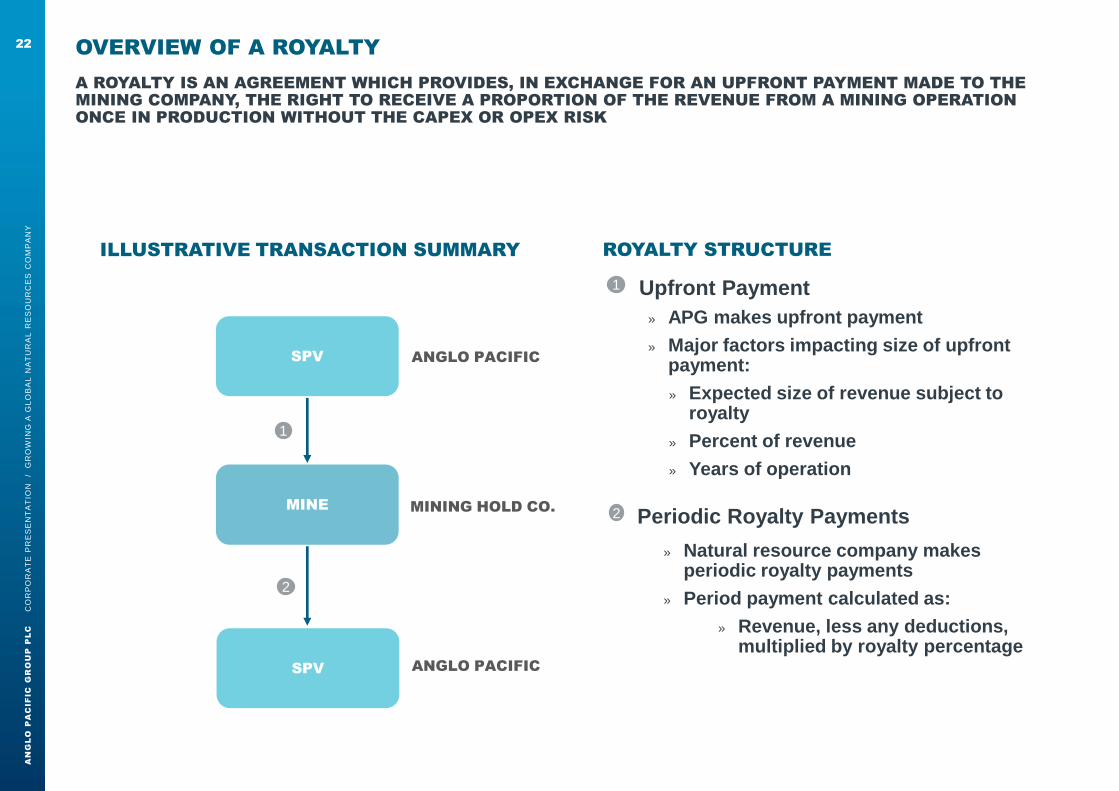

OVERVIEW OF A ROYALTY22

A ROYALTY IS AN AGREEMENT WHICH PROVIDES, IN EXCHANGE FOR AN UPFRONT PAYMENT MADE TO THE MINING COMPANY, THE RIGHT TO RECEIVE A PROPORTION OF THE REVENUE FROM A MINING OPERATION ONCE IN PRODUCTION WITHOUT THE CAPEX OR OPEX RISK

SPV

MINING HOLD CO.

ILLUSTRATIVE TRANSACTION SUMMARY

1

2

ROYALTY STRUCTURE

MINE

Upfront Payment

» APG makes upfront payment

» Major factors impacting size of upfront payment:

» Expected size of revenue subject to royalty

» Percent of revenue

» Years of operation

2 Periodic Royalty Payments

» Natural resource company makes periodic royalty payments

» Period payment calculated as:

» Revenue, less any deductions, multiplied by royalty percentage

1

SPV

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

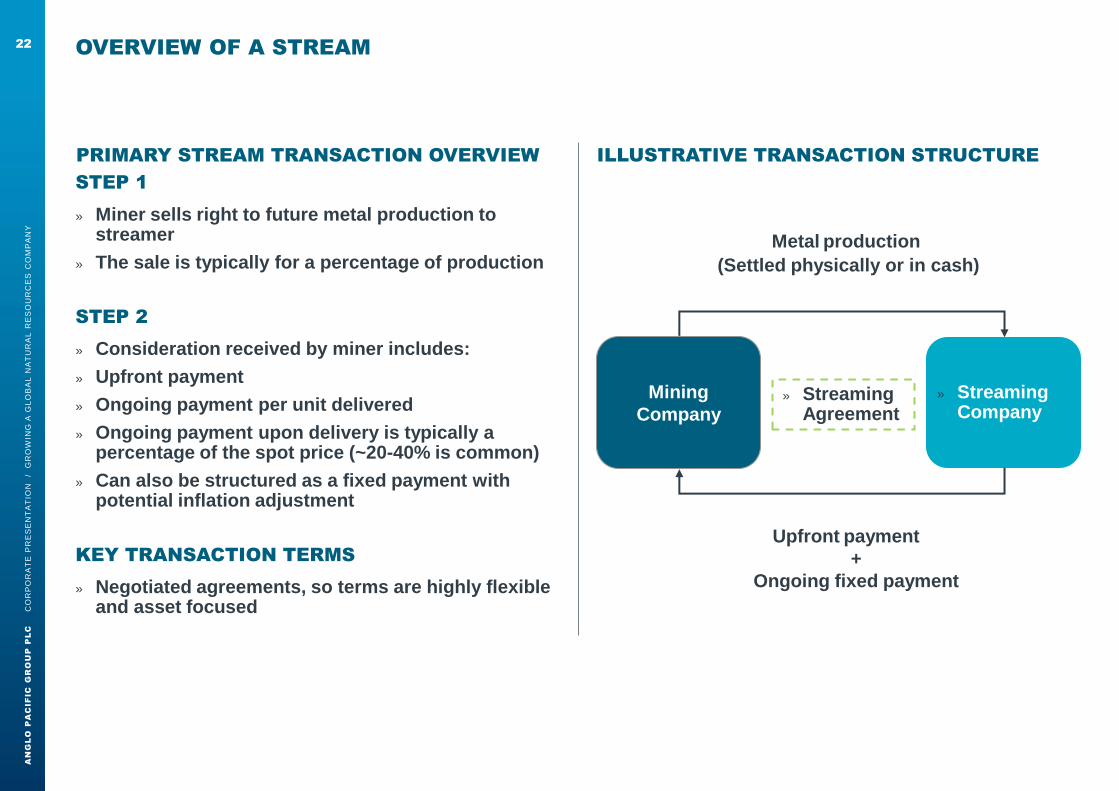

OVERVIEW OF A STREAM

STEP 1

» Miner sells right to future metal production to streamer

» The sale is typically for a percentage of production

STEP 2

» Consideration received by miner includes:

» Upfront payment

» Ongoing payment per unit delivered

» Ongoing payment upon delivery is typically a percentage of the spot price (~20-40% is common)

» Can also be structured as a fixed payment with potential inflation adjustment

KEY TRANSACTION TERMS

» Negotiated agreements, so terms are highly flexible and asset focused

PRIMARY STREAM TRANSACTION OVERVIEW ILLUSTRATIVE TRANSACTION STRUCTURE

Mining

Company

» Streaming Company

» Streaming Agreement

Metal production

(Settled physically or in cash)

Upfront payment

+

Ongoing fixed payment

22

AN

GL

O P

AC

IFIC

GR

OU

P P

LC

CO

RP

OR

AT

E P

RE

SE

NT

AT

ION

/

GR

OW

ING

A G

LO

BA

L N

AT

UR

AL

RE

SO

UR

CE

S C

OM

PA

NY

WHY COMPANIES ENGAGE WITH ANGLO PACIFIC

POTENTIAL DRIVERS FOR ENGAGING

WITH ANGLO PACIFIC

» Challenging financing environment

» Can be less dilutive than equity

» Less restrictive than debt

» Scope can be limited to a single asset or by-

product

PRIMARY ROYALTIES / STREAMS SECONDARY ROYALTIES / STREAMS

POTENTIAL DRIVERS FOR ENGAGING

WITH ANGLO PACIFIC

» Opportunity to monetise illiquid asset

» If privately held, risk can be highly concentrated

» Residual exposure possible via Anglo Pacific

shares

24

23