annexure j of appropriation accounts of indian railways

TRANSCRIPT

1

Presented By

M.Nageswara Rao, SSO(A)/Secunderabad

Presented By

M.Nageswara Rao, SSO(A)/Secunderabad

2

3

4

5

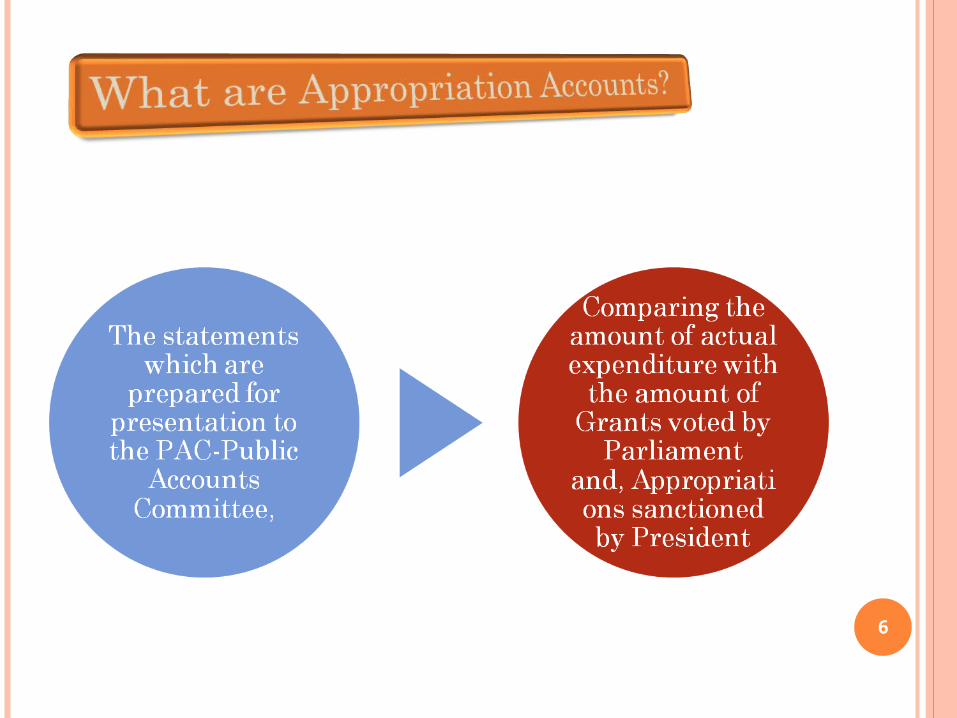

Before discussion on

Annexure J, lets have a look at significance of Appropriation

Accounts.

6

7

8

9

Appropriation Accounts - Annexures

10

Appropriation Accounts - Annexures

11

Appropriation Accounts - Annexures

12

Appropriation Accounts - Annexures

Appropriation Accounts - Annexures

13

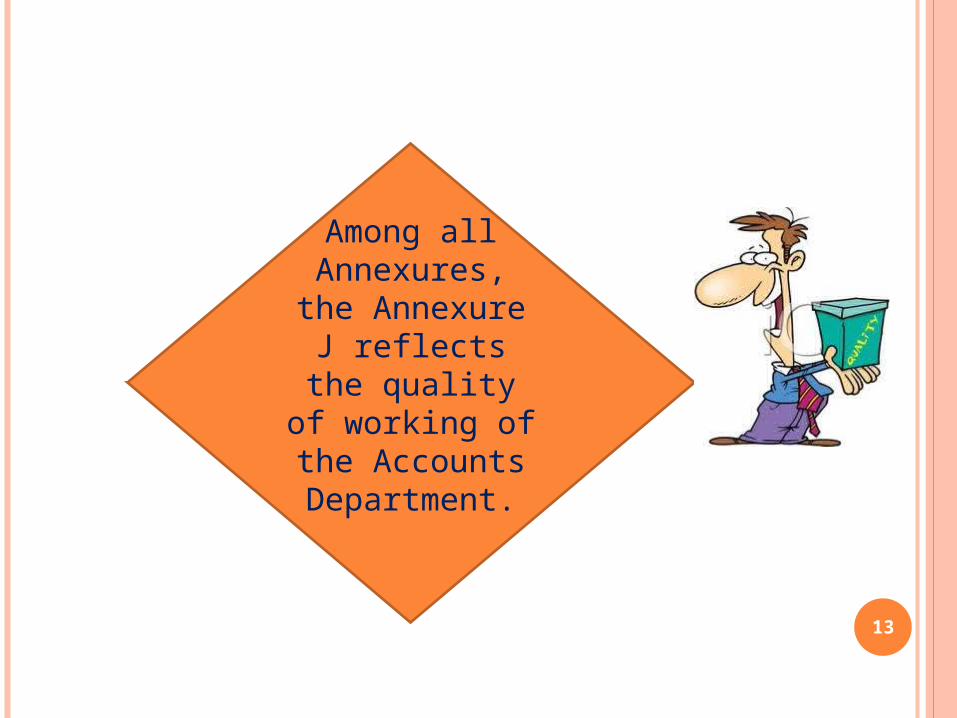

Among all Annexures, the

Annexure J reflects the quality of

working of the Accounts

Department.

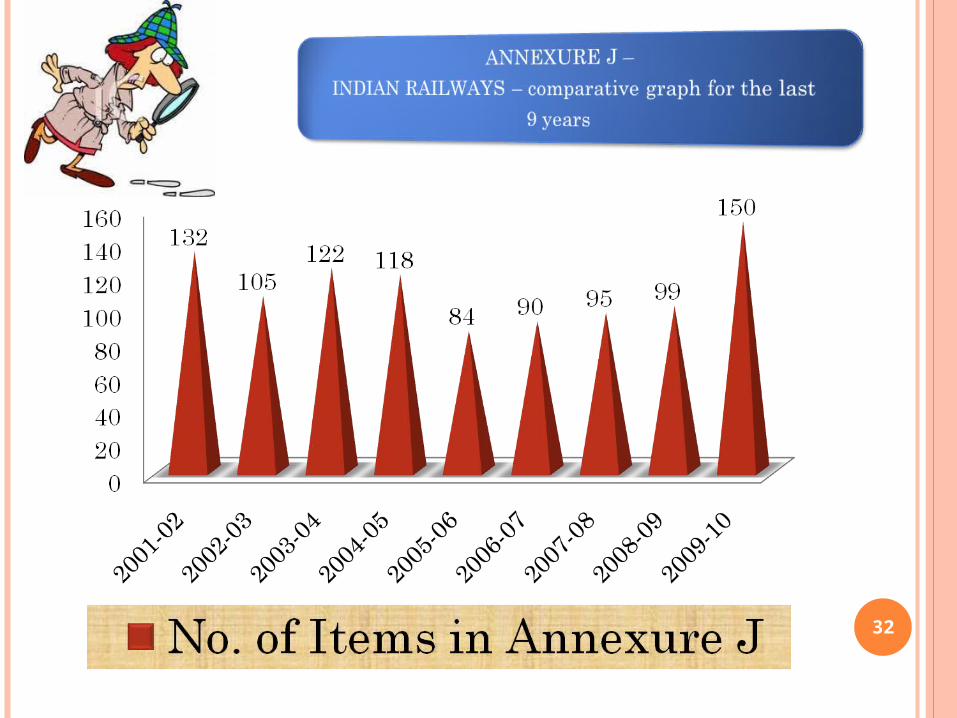

14

15

16

17

18

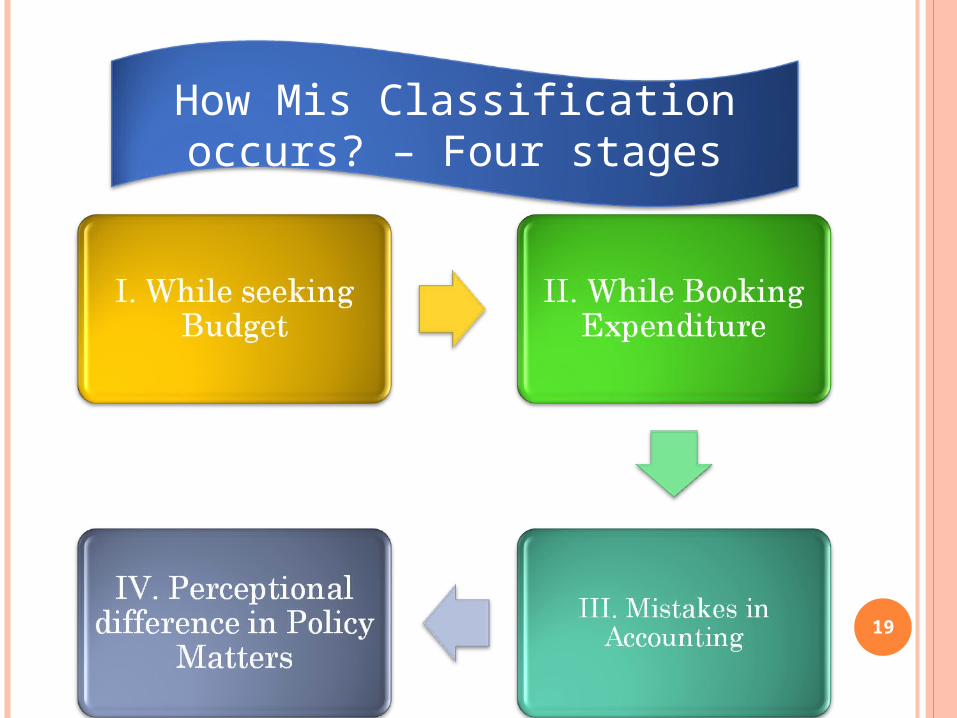

What is the mis - classification ?

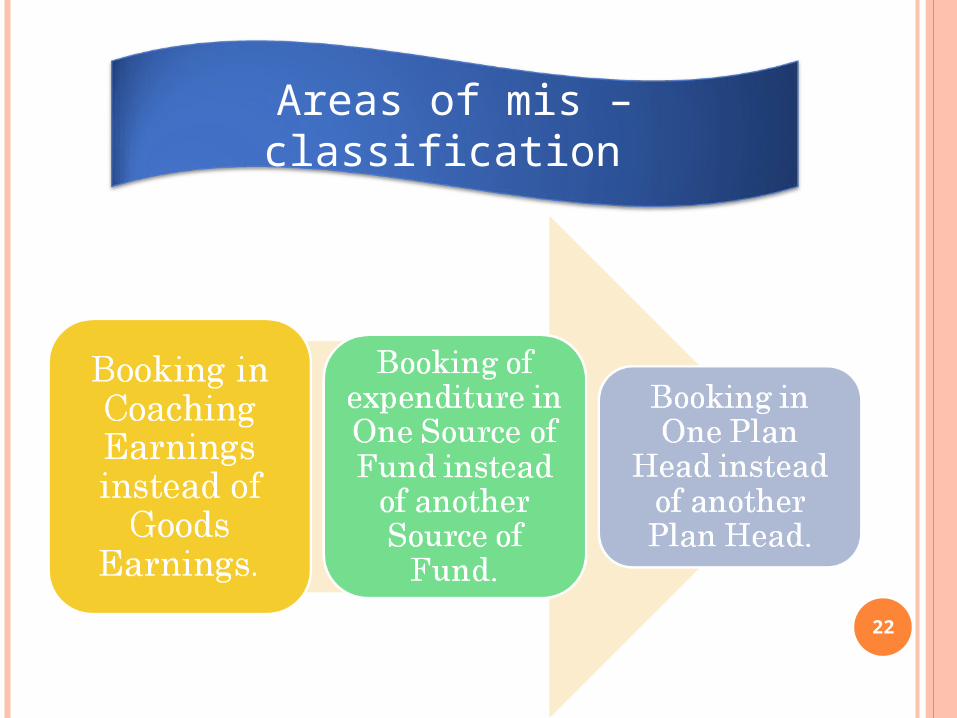

Examples are

19

How Mis Classification occurs? – Four stages

20

21

Areas of mis – classification

22

Areas of mis – classification

23

Areas of Mistakes

24

25

26

Demand No. 9

Demand No. 8

27

Demand No. 12

Demand No. 11 ( 11-120-25)

28

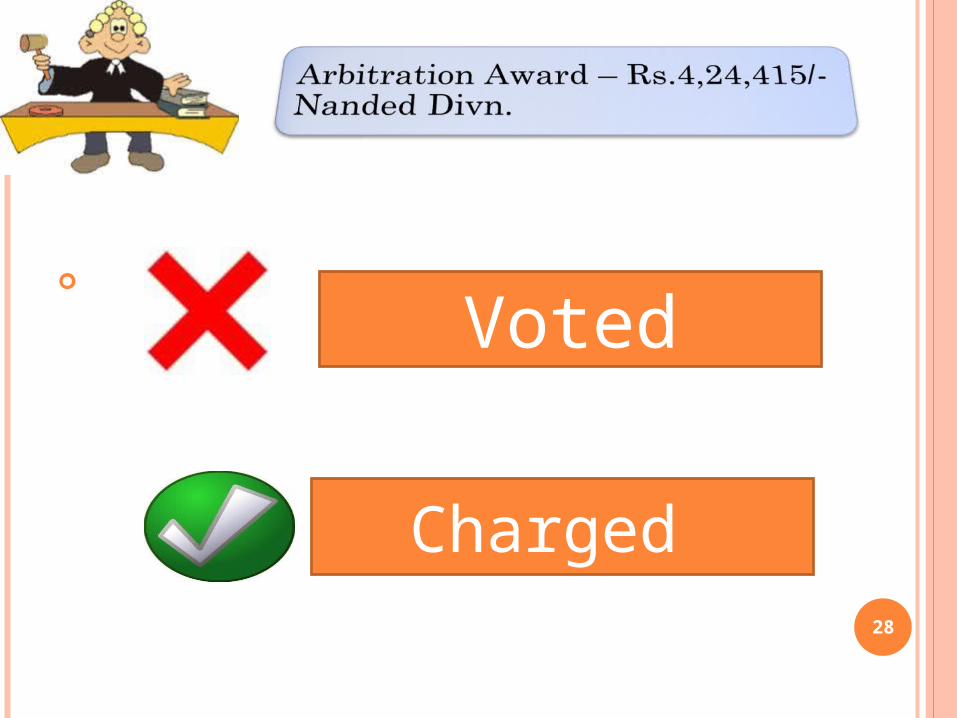

Voted

Charged

29

Development Fund (DF)

Depreciation Reserve Fund (D R F)

30

D R F – Depreciation Reserve Fund

CAPITAL

31

CAPITAL

D R F – Depreciation Reserve Fund

32

33

34

Demand No. 4

Demand No. 2

35

Demand No.7

Demand No. 12

36

Demand No. 6 (06-210) – It is a previous accepted allocation.

Demand No.8 (08 -531) – New allocation in place of 06-210

37

Demand No. 11

Demand No. 9

38

M A R

CAPITAL

39

VOTED

CHARGED

40

CAPITAL

D R F

41

42

Demand No. 4 – Minus Debit

Demand No. 4 - Credit Side as CRRM

43

Indian Rly. Misc. Deposits

Track Renewals Plan Head

44

Sundry Earnings – Abstract Z -650

Goods Earnings - Abstract Y

45

46

47

48

49

50

To percolate the

awareness of distinction

between Revenue

expenditure and capital

Expenditure.

51

By conducting refresher

courses among the staff, because

Prevention is better than

Cure.

52

The References cum General Areas to be

taken note of

53

54

55

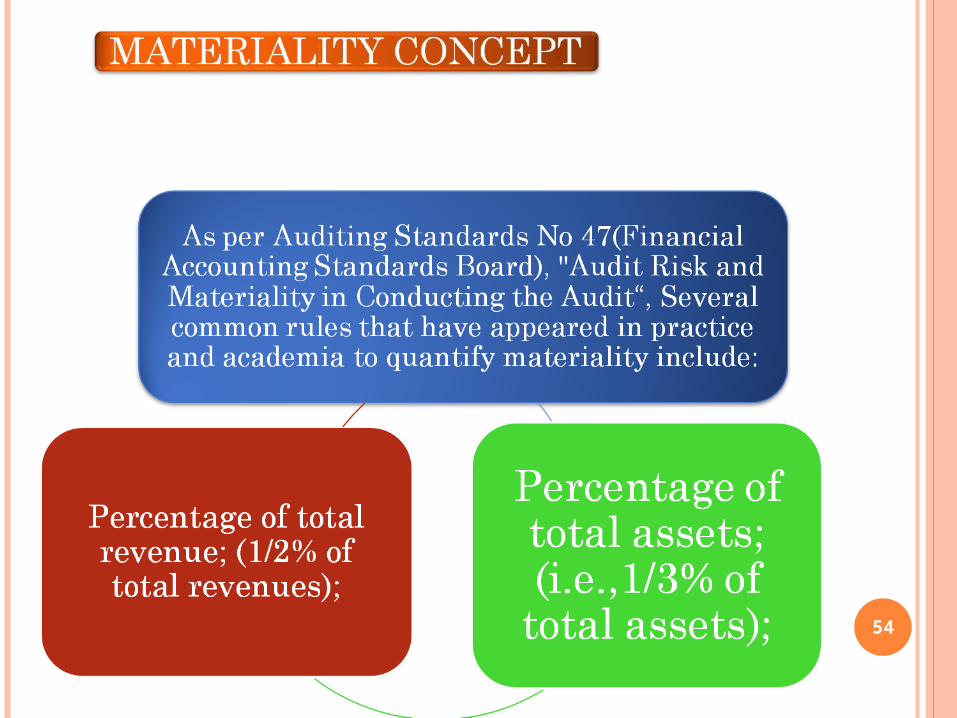

It is to suggest, that the materiality concept, which is applicable at present in the commercial concerns can be applied to Railways also.

Because there is no merit in excluding Government organizations from the scope of Materiality Concept.

56

57

58

59

60

61

NEW PENSION SCHEME

62While uploading to NSDL, the Head 000071 02 is operated on Debit Side for both Govt. and Employee contribution

While uploading to NSDL, the Head 000071 02 is operated on Debit Side for both Govt. and Employee contribution

63

64

65

66

67

68

69