announcements gross margin ratio profit margin ratio 2014/210.9.24.8.30.pdf · before class starts...

TRANSCRIPT

Announcements

Gross Margin Ratio

Profit Margin Ratio

Before Class starts….(make sure your name is on all submissions)

Second Homework 14 Fall Inc. due 9/29.

No class 10/1.

First Exam Thursday 10/2 6pm-9pm ALL ALTERNATE ARRANGEMENTS DONE!

What questions do you have for me?

– TA Office Hours & Accounting Lab Hours on http://bus.emory.edu/scrosso

– File cabinet downstairs should now contain your mail folder and name cards

Measurement Fundamentals

BUS 210

Chapter 3

What do you know?

Valuation Input Market (purchase)-original, replacement Output Market (sell)-present, fair market

Financial Statements:• Original (Historic) Cost: Land, LT Invt

– Lower of Cost or Market: Inventory– Net Realizable Value: net AR– Net Book Value: PP&E, Intang.

• Face: Cash, Current liabilities • Fair Market Value (sales price): ST Invt• Present Value: LT NR & LTL

IFRS v. US GAAP Principles based Rules based

Financial Accounting Fundamentals

Financial Accounting FundamentalsAssumptions• Economic Entity (identified and measured)

• Fiscal Period (periodicity)

• Going Concern (life indefinite)

• Stable Dollar (across time)

Measurement Principles• Objectivity (Verifiable and documented)

• Revenue Recognition • Expense Recognition• Matching No More (costs & benefits)• Consistency (methods same across time)

• Two Exceptions– Materiality –little to no effect on user decisions

– Conservatism -understate assets, overstate liabilities, accelerate losses, and delay gains (due to legal liability)

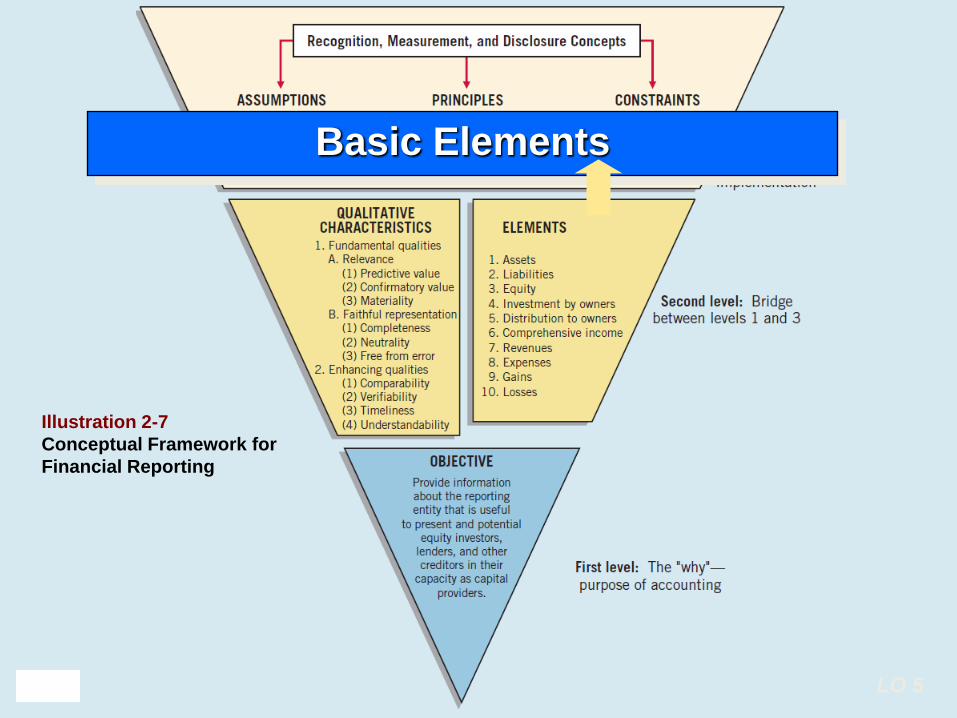

First Level = Basic Objectives

Second Level = Qualitative

Characteristics and Elements

Third Level = Recognition,

Measurement, and Disclosure

Concepts.

Overview of the Conceptual Framework

Conceptual Framework

LO 4

Conceptual Framework for

Financial Reporting

First Level: Basic Objectives

Objective of financial reporting:

To provide financial information about the reporting entity that

is useful to present and potential equity investors,

lenders, and other creditors in making decisions about

providing resources to the entity.

“The FASB identified the qualitative characteristics of

accounting information that distinguish better (more useful)

information from inferior (less useful) information for

decision-making purposes.”

Second Level: Fundamental Concepts

Qualitative Characteristics of Accounting

Information

Hierarchy of

Accounting Qualities

Second Level: Fundamental Concepts

LO 4

Conceptual Framework for

Financial Reporting

Relevance

Fundamental Quality—Relevance

To be relevant, accounting information must be capable of making

a difference in a decision.

Second Level: Fundamental Concepts

Financial information has predictive value if it has value as an input to

predictive processes used by investors to form their own expectations

about the future.

Second Level: Fundamental Concepts

Fundamental Quality—Relevance

Relevant information also helps users confirm or correct prior

expectations.

Second Level: Fundamental Concepts

Fundamental Quality—Relevance

Information is material if omitting it or misstating it could influence

decisions that users make on the basis of the reported financial

information.

Second Level: Fundamental Concepts

Fundamental Quality—Relevance

LO 4

Illustration 2-7

Conceptual Framework for

Financial Reporting

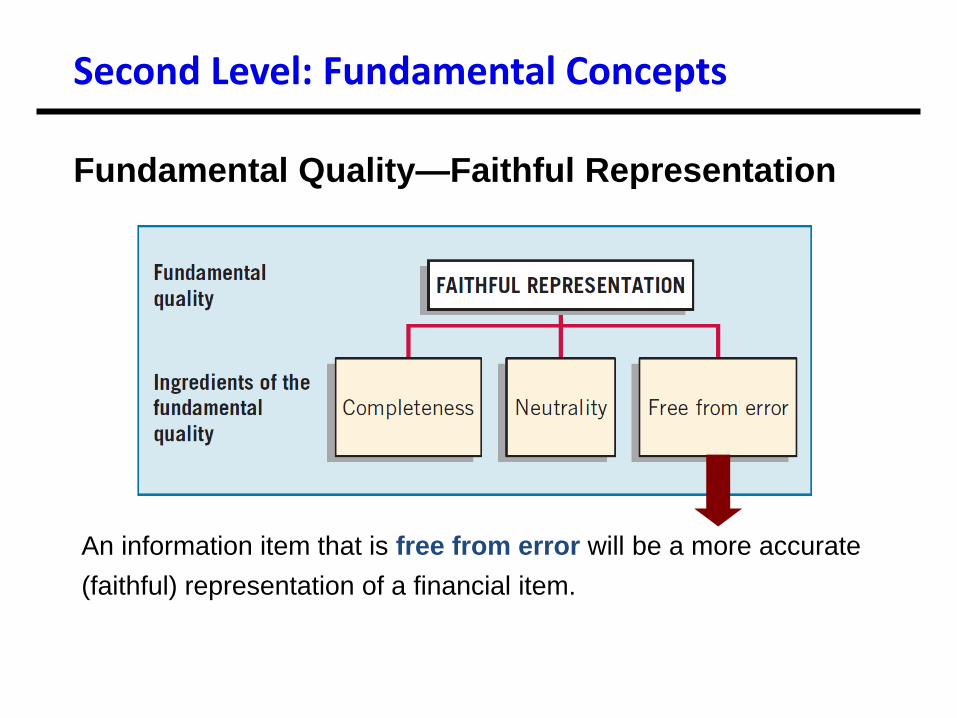

Faithful Representation

Fundamental Quality—Faithful Representation

Faithful representation means that the numbers and descriptions

match what really existed or happened.

Second Level: Fundamental Concepts

Completeness means that all the information that is necessary for

faithful representation is provided.

Second Level: Fundamental Concepts

Fundamental Quality—Faithful Representation

Neutrality means that a company cannot select information to favor

one set of interested parties over another.

Second Level: Fundamental Concepts

Fundamental Quality—Faithful Representation

An information item that is free from error will be a more accurate

(faithful) representation of a financial item.

Second Level: Fundamental Concepts

Fundamental Quality—Faithful Representation

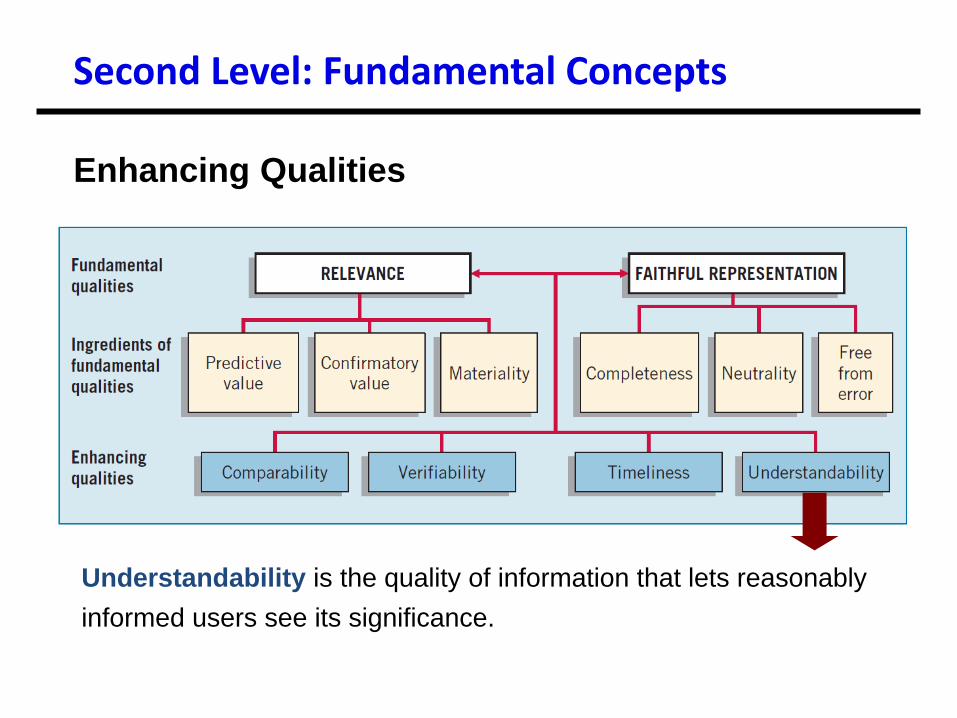

Enhancing Qualities

Information that is measured and reported in a similar manner for

different companies is considered comparable.

Second Level: Fundamental Concepts

Enhancing Qualities

Verifiability occurs when independent measurers, using the same

methods, obtain similar results.

Second Level: Fundamental Concepts

Enhancing Qualities

Timeliness means having information available to decision-makers

before it loses its capacity to influence decisions.

Second Level: Fundamental Concepts

Enhancing Qualities

Understandability is the quality of information that lets reasonably

informed users see its significance.

Second Level: Fundamental Concepts

LO 5

Illustration 2-7

Conceptual Framework for

Financial Reporting

Basic Elements

Investment by owners

Distribution to owners

Comprehensive income

Revenue

Expenses

Gains

Losses

Concepts Statement No. 6 defines ten interrelated elements

that relate to measuring the performance and financial status of

a business enterprise.

Assets

Liabilities

Equity

“Moment in Time” “Period of Time”

Second Level: Basic Elements

According to the FASB conceptual framework, an entity’s revenue

may result from

a. A decrease in an asset from primary operations.

b. An increase in an asset from incidental transactions.

c. An increase in a liability from incidental transactions.

d. A decrease in a liability from primary operations.

Second Level: Basic Elements

Question

Conceptual Framework

for Financial Reporting

The FASB sets forth most of these concepts in its Statement of

Financial Accounting Concepts No. 5, “Recognition and

Measurement in Financial Statements of Business Enterprises.”

Third Level: Recognition and Measurement

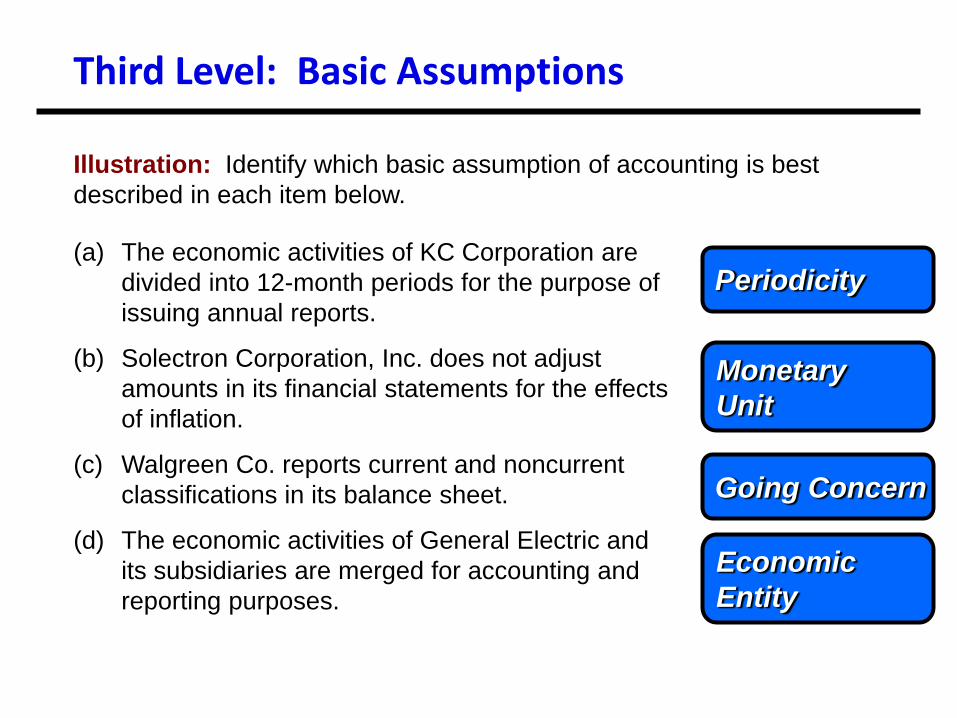

Economic Entity – company keeps its activity separate from

its owners and other businesses.

Going Concern - company to last long enough to fulfill

objectives and commitments.

Monetary Unit - money is the common denominator.

Periodicity - company can divide its economic activities into

time periods.

Third Level: Basic Assumptions

Illustration: Identify which basic assumption of accounting is best

described in each item below.

(a) The economic activities of KC Corporation are

divided into 12-month periods for the purpose of

issuing annual reports.

(b) Solectron Corporation, Inc. does not adjust

amounts in its financial statements for the effects

of inflation.

(c) Walgreen Co. reports current and noncurrent

classifications in its balance sheet.

(d) The economic activities of General Electric and

its subsidiaries are merged for accounting and

reporting purposes.

Periodicity

Going Concern

Monetary

Unit

Economic

Entity

Third Level: Basic Assumptions

Measurement Principle – The most commonly used

measurements are based on historical cost and fair value.

Issues:

Historical cost provides a reliable benchmark for measuring

historical trends.

Fair value information may be more useful.

Recently the FASB has taken the step of giving companies

the option to use fair value as the basis for measurement of

financial assets and financial liabilities.

Reporting of fair value information is increasing.

Third Level: Basic Principles

Revenue Recognition - requires that companies recognize

revenue in the accounting period in which the performance

obligation is satisfied.

Third Level: Basic Principles

Expense Recognition - “Let the expense follow the

revenues.” Illustration 2-6

Expense Recognition

Third Level: Basic Principles

Illustration: Assume the Boeing Corporation signs a contract to sell airplanes to Delta Air Lines for $100 million. To determine when to recognize revenue, use the five steps for revenue recognition shown at right.

Full Disclosure – providing information that is of sufficient

importance to influence the judgment and decisions of an

informed user.

Provided through:

Financial Statements

Notes to the Financial Statements

Supplementary information

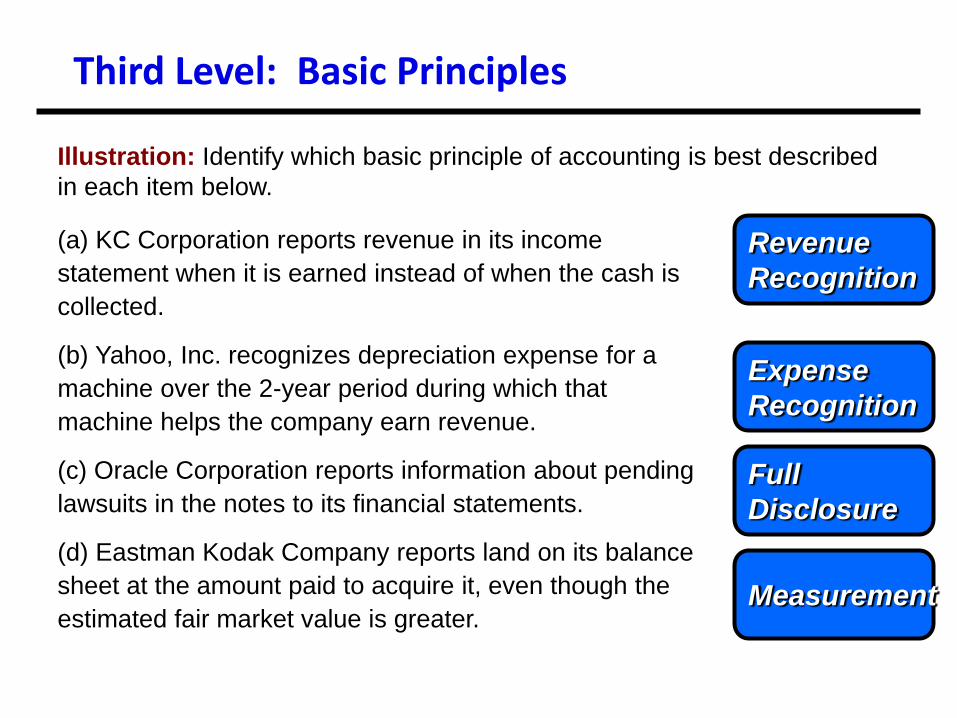

Third Level: Basic Principles

Illustration: Identify which basic principle of accounting is best described

in each item below.

(a) KC Corporation reports revenue in its income

statement when it is earned instead of when the cash is

collected.

(b) Yahoo, Inc. recognizes depreciation expense for a

machine over the 2-year period during which that

machine helps the company earn revenue.

(c) Oracle Corporation reports information about pending

lawsuits in the notes to its financial statements.

(d) Eastman Kodak Company reports land on its balance

sheet at the amount paid to acquire it, even though the

estimated fair market value is greater.

Revenue

Recognition

Expense

Recognition

Full

Disclosure

Measurement

Third Level: Basic Principles

Cost Constraint – cost of providing information must be

weighed against the benefits that can be derived from using it.

Third Level: Constraints

Illustration: The following two situations represent applications

of the cost constraint.

(a) Rafael Corporation discloses fair value information on its

loans because it already gathers this information internally.

(b) Willis Company does not disclose any information in the notes

to the financial statements unless the value of the information

to users exceeds the expense of gathering it.

Conceptual Framework for

Financial Reporting

Summary

of the

Structure

Cash Basis Accounting

• Primarily used by individuals and small businesses.

• Not permitted for revenue and expenses measurement and reporting under GAAP.

• Under cash basis accounting, revenues are recognized only in the period when cash is received.

• Under cash basis accounting, expenses are recognized only in the period when cash is disbursed.

• Cash basis accounting Income Statement reports the cash received as revenue and the cash expenses incurred.

Accrual Accounting

• Basic to financial reporting of corporations.• Concerned with the timing of revenue and expense

recognition.• Purpose is to accurately measure revenues and

expenses (and profits) for each accounting period.• Accrual accounting’s Income Statement attempts

to match revenues earned and the expenses incurred, NOT cash flows.

• Accrual accounting’s Statement of Cash Flows reports the cash inflows and outflows for the period.

Accrual Accounting Revenues

• Revenues are recognized and recorded when they are (1) earnedand are (2) realized or realizable.– Revenues are earned when the primary revenue generating activities

are substantially completed (usually the point of delivery of goods or completion of services, i.e., title passes).

– Revenues are realized when cash is collected. Revenues are realizablewhen a viable and measurable claim to cash is acquired. A viable claim is one that is expected to be collected under normal terms of collection.

• The actual receipt of cash is not required for revenue to be recognized, and in many cases the receipt of cash does not trigger an immediate recognition of revenue. Hence, under accrual accounting, depending on when both conditions (earned & realized) have been met, it may be necessary to recognize revenues either before, at the time, or after cash is collected, i.e. accruals, unearned.

Revenue Recognition:

Text 4 Steps v. Just Released 5 Steps

1. The company has completed a significant portion of the production and sales efforts.

2. The amount of revenue can be objectively measured.

3. The company has incurred the majority of costs, and remaining costs can be reasonably estimated, and

4. Cash collection is reasonably assured.

Matching ConceptsUnderlying the accrual accounting concept is the Matching concept. This concept holds that revenues recognized in a particular period should be accompanied by (or matched with) the recognition of expenses related to those revenues—costs should follow the revenues.• Some costs, such as cost of goods sold or cost of sales, have a direct

relation to specific revenues and should be recognized as expenses in the same period as the revenues to which they relate.

• Other costs, such as rent, depreciation, and some salaries, may not be directly traceable to specific revenues of the period, but they relate indirectly to the period’s revenue because they represent costs expired during the period in which revenues are recognized; hence they are an expense of the period.

• Some costs, such as research and development (R&D), have future expected benefits that cannot be determined objectively, so they are expensed in the period in which they are incurred.

• Implementing accrual accounting and the matching concept often requires adjusting entries at the end of the period to ensure that the books match all the appropriate revenues and expenses for the period.

Accruals and Deferrals

• An accrual asset or liability is created on the balance sheet any time revenue or expense is recognized (accrued) BEFORE the associated cash flow is received or paid. Examples: Accounts Receivable, Interest Receivable, Accounts Payable, Taxes Payable.[Expense now, Pay later. OR Receive later, Revenue now.]

• A deferral asset or liability is created on the balance sheet anytime cash is collected or paid BEFORE the associated expense or revenue is recognized (deferred). Examples: Inventories, Prepaid expenses, Equipment, Unearned revenues.

Accrual Balance Sheet

Assets on the Balance Sheet include:• Something that has future or potential value.

• Future expenses for which cash has already been paid.(Prepaid—i.e., deferred—Expenses)

• Past revenues for which cash has not been collected. (Accounts Receivable –i.e., accrued revenues)

Liabilities on the Balance Sheet include:• Responsibilities or promises to others• Past expenses for which cash has not been paid. (Accrued

Expenses Payable)• Future revenues for which cash has already been

collected. (Deferred or Unearned Revenues)

Accrual Income Statement

Reported revenues include:

• Revenues collected in a prior period deferred to the current period (reported previously on the balance sheet as a liability, Unearned Revenues)

• Revenues collected in the current period that were also earned currently.

• Revenues earned (and accrued) currently that will be collected in future periods (reported currently on the balance sheet as an asset, Accounts Receivable.

Accrual Income Statement

Reported expenses include:• The cost of goods or services consumed in the current

period that were paid for in a prior period, but deferred to the current period (reported previously on the balance sheet as an asset; i.e., Inventories, Prepaid Expenses).

• The cost of goods or services consumed in the current period that were also paid for in the current period.

• The cost of goods or services consumed in the current period that will be paid for in future periods (reported on the current balance sheet as a liability; i.e., Accounts Payable).

Subjective JudgmentsValuation Input Market (purchase)-original, replacementOutput Market (sell)-present, fair market

Financial Statements:• Original (Historic) Cost: Land, LT Invt

– Lower of Cost or Market: Inventory– Net Realizable Value: net AR– Net Book Value: PP&E, Intang.

• Face: Cash, Current liabilities • Fair Market Value (sales price): ST Invt• Present Value: LT NR & LTL

Bottom Line…..Accrual accounting fails to serve its intended purpose of matching revenues and expenses on the income statement and reporting appropriate amounts for accruals and deferrals on the balance sheet unless those responsible (Managers, Accountants, & Auditors) are people of integrity.

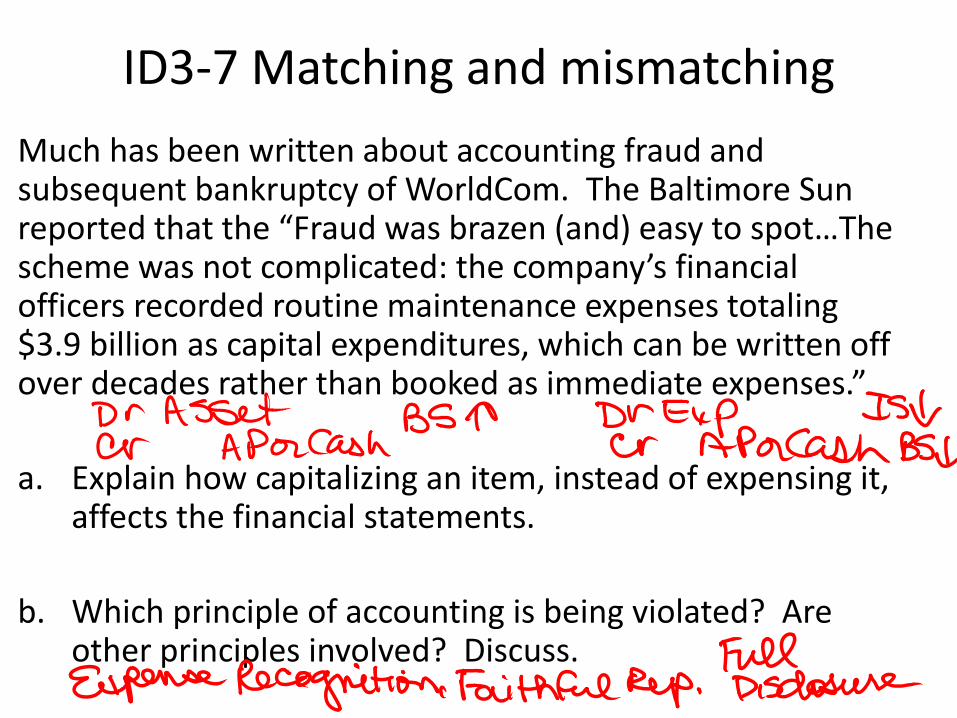

ID3-7 Matching and mismatching

Much has been written about accounting fraud and subsequent bankruptcy of WorldCom. The Baltimore Sun reported that the “Fraud was brazen (and) easy to spot…The scheme was not complicated: the company’s financial officers recorded routine maintenance expenses totaling $3.9 billion as capital expenditures, which can be written off over decades rather than booked as immediate expenses.”

a. Explain how capitalizing an item, instead of expensing it, affects the financial statements.

b. Which principle of accounting is being violated? Are other principles involved? Discuss.

P3-12 Revenue recognition and net incomea. Assuming that Hydra recognizes revenue when the toasters are produced, how much revenue should be recognized in each of the 3 years?b. Assuming Hydra recognizes revenue at delivery, how much revenue should be recognized in each of the 3 years?c. Calculate net income for the 3 periods under each of the two assumptions above.d. If Hydra’s management is paid an income-based bonus, which of the two assumptions would be preferred?

Hydra sells appliances to Seasons Department Store. A recent order requires Hydra to manufacture and deliver 500 toasters at a price of $100 per unit. Hydra’s manufacturing costs are approximately $40 per unit. The following schedule summarizes the production and delivery record of Hydra:

Year 1 2 3 Total

Toasters produced 200 200 100 500

Costs incurred $8,000 $8,000 $4,000 $20,000

Toasters delivered 150 200 150 500

Cash received $10,000 $15,000 $20,000 $45,000

P3-12

E3-5 Matching and Revenue recognition

Cascade Enterprises ordered 4,000 brackets from McKay and Company on 12.1.2011, for a contract price of $40,000. McKay completed manufacturing the brackets on 1.17.12 and delivered them to Cascade on 2.9.12. McKay received a check for $40,000 from Cascade on 3.14.12.a. Assume that McKay and Company prepare monthly income

statements. In which month should McKay recognize the $40,000 revenue from the sale?

b. Justify your answer in (a.) in terms of the 4 criteria of revenue recognition.

E3-5 Matching and Revenue recognition

Cascade Enterprises ordered 4,000 brackets from McKay and Company on 12.1.2011, for a contract price of $40,000. McKay completed manufacturing the brackets on 1.17.12 and delivered them to Cascade on 2.9.12. McKay received a check for $40,000 from Cascade on 3.14.12.

c. Are their conditions under which the revenue could be recognized in a different month than the month you chose?

d. Provide several reasons McKay’s management might be interested in the timing of the recognition of revenue.

MaterialityQ: Have you ever wondered why companies…• Sometimes do not restate for the prior period when a major event occurs,

such as an acquisition, that makes current and prior years non-comparable?• Can avoid recording losses on the income statement• Can capitalize (record as an asset) normal operating expenses• Fail to disclose one-time gains or losses as separate line items on the income

statement• In short—ignore the normal accounting conventions.Q: How can you convince your independent auditor to allow your company to circumvent normal accounting conventions?• Materiality exception—the impact of recording a transaction in a more

expedient (although technically improper) way has no significant impact on the investor, normal accounting conventions could be ignored.

• Thus, prior-period financial statements need not be restated if the change is deemed immaterial; and normal operating expenses could be capitalized if the amount is insignificant.

Adapted from: Center for Research and Financial Analysis, Inc.

Materiality Exception

• Due to the subjectivity in assessing materiality, over time certain quantitative thresholds (rules of thumb) have been used. Some use a 5% overstatement of net income as a threshold for materiality.– Securities and Exchange Commission (SEC) staff point out that exclusive

reliance on any percentage or numerical threshold has no basis in accounting literature.

• In SFAC No. 2 the Financial Accounting Standards Board (FASB) states the essence of materiality is: “The omission or misstatement of an item in a financial report is material if, in light of the surrounding circumstances, the magnitude of the item is such that it is probable that the judgment of a reasonable person relying upon the report would have been changed or influenced by the inclusion or correction of the item.”

• The Supreme Court has held that a fact is material if there is: “a substantial likelihood that the…fact would have been viewed by the reasonable investor as having significantly altered the total mix of information made available.”

Interpreting MaterialityRather than relying on a numerical threshold, materiality judgments should be based on all the facts, qualitative and quantitative. The SEC’s SAB No. 99 provides certain valuable insights to help investors make material judgments. Among the considerations that may well render material a quantitatively small misstatement of a financial statement item are whether the misstatement:• Arises from an item capable of precise measurement or whether it arises

from an estimate and, if so, the degree of imprecision inherent in the estimate

• Masks a change in earnings or other trends• Hides a failure to meet analysts’ consensus expectations for the enterprise• Changes a loss into income or visa versa• Concerns a segment or other portion of the registrant’s business that has

been identified as playing a significant role in the registrant’s operations or profitability

• Affects the registrant’s compliance with regulatory requirements• Affects the registrant’s compliance with loan covenants or other contractual

requirements• Has the effect of increasing management’s compensation—for example, by

satisfying requirements for the award of a bonus or other forms of incentive compensation whether the misstatement involves concealment of an unlawful transaction.

E3-8 The concept of materiality

All large U.S. companies have policies in which all expenditures under a certain dollar amount are expensed. Many of these expenditures are for assets, items that are useful to a company beyond the period in which they were purchased.

a. Explain the proper accounting treatment for expenditures for items that are expected to generate benefits in the future.

b. Explain why it might make economic sense to expense some of these items. Upon what exception to the principles of financial accounting would such a decision be based?

Conservatism

Conservatism in measurement and reporting –

–understate assets,

–overstate liabilities,

–accelerate losses, and

–delay gains (due to legal liability)

ID3-10 Income management and conservatism

Whitney Tilson, a noted analyst, warns investors in an article in The Motley Fool that more than any other type of company, financial companies have immense discretion regarding what earnings to report. The key is the rate of loan losses that they expect to experience, which must be estimated at the end of every period. By changing the estimate, which in turn changes one of the largest expenses on their income statement, financial companies can manage net income. Tilson specifically cites Farmer Mac, the agency created by the federal government to provide funds in the agricultural lending market, which many analysts believe smooths it earnings across time by simply changing its estimate of loss rates.a. What does it mean to “smooth earnings across time”? How might a financial

company practice this strategy, and why might it engage in this activity?

b. Earnings smoothing has also been associated with conservatism. Why?

Conceptual Framework for

Financial Reporting

Summary

of the

Structure