annual financial report - abacus property group h2.pdf · annual financial report 30 june 2015 ......

TRANSCRIPT

ABACUS HOSPITALITY FUND

1

ANNUAL FINANCIAL REPORT 30 June 2015

Directory

Entity: Custodian: Abacus Funds Management Limited Perpetual Trustee Company Limited

ABN 66 007 415 590 Level 12 Angel Place Level 34, Australia Square 123 Pitt Street 264-278 George Street SYDNEY NSW 2000 SYDNEY NSW 2000 Tel: (02) 9253 8600 Auditor (Financial and Compliance Plan):

Fax: (02) 9253 8616 Ernst & Young Website: www.abacusproperty.com.au Ernst & Young Centre 680 George Street Directors of Responsible Entity and Abacus SYDNEY NSW 2000 Hospitality Limited: John Thame, Chairman Share Registry: Frank Wolf, Managing Director Boardroom Pty Limited William Bartlett Grosvenor Place Malcolm Irving Level 12, 225 George St Len Lloyd Sydney, NSW 2000 Myra Salkinder Tel: 1300 737 760 Peter Spira Fax: 1300 653 459 Company Secretary: Ellis Varejes

CONTENTS

DIRECTORS’ REPORT 2

AUDITORS INDEPENDENCE DECLARATION 6

CONSOLIDATED INCOME STATEMENT 7

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME 8

CONSOLIDATED STATEMENT OF FINANCIAL POSITION 9

CONSOLIDATED STATEMENT OF CASH FLOW 11

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY 12

NOTES TO THE FINANCIAL STATEMENTS 14

DIRECTORS’ DECLARATION 58

INDEPENDENT AUDIT REPORT 59

It is recommended that the report be considered together with any public announcements made by the Abacus Hospitality Fund in accordance with its continuous disclosure obligations arising under the Corporations Act 2001.

ABACUS HOSPITALITY FUND

2

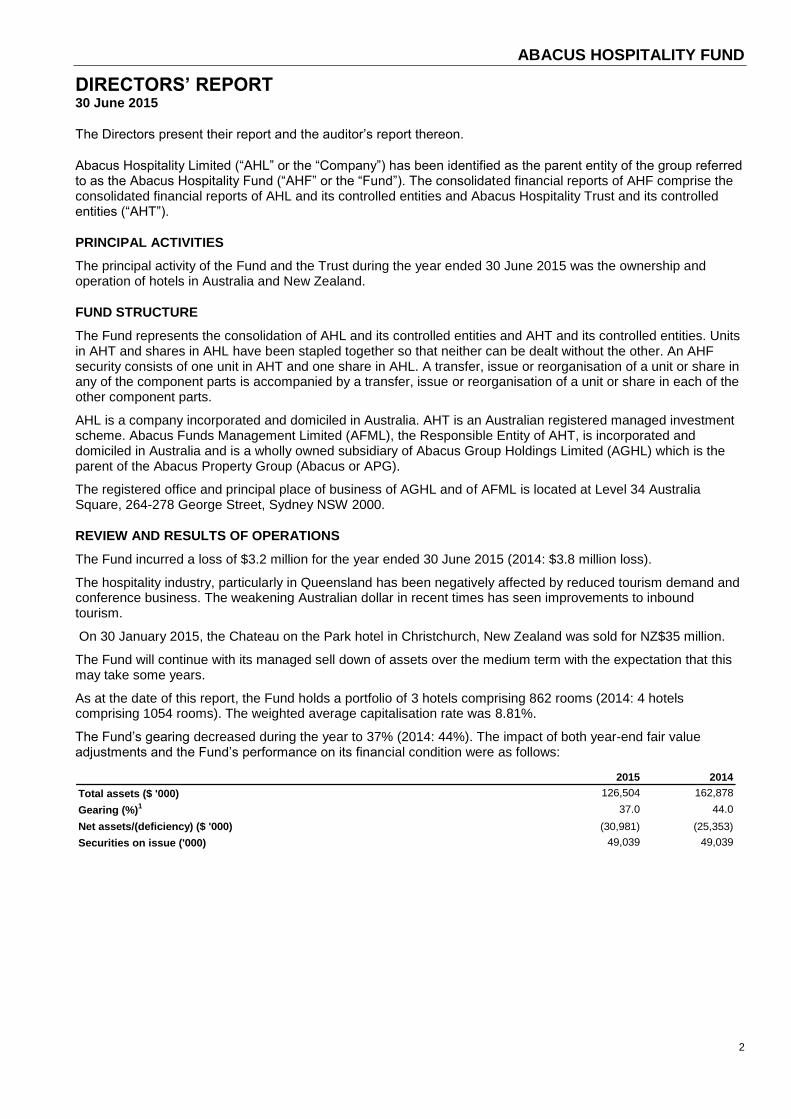

DIRECTORS’ REPORT 30 June 2015

The Directors present their report and the auditor’s report thereon.

Abacus Hospitality Limited (“AHL” or the “Company”) has been identified as the parent entity of the group referred to as the Abacus Hospitality Fund (“AHF” or the “Fund”). The consolidated financial reports of AHF comprise the consolidated financial reports of AHL and its controlled entities and Abacus Hospitality Trust and its controlled entities (“AHT”).

PRINCIPAL ACTIVITIES

The principal activity of the Fund and the Trust during the year ended 30 June 2015 was the ownership and operation of hotels in Australia and New Zealand.

FUND STRUCTURE

The Fund represents the consolidation of AHL and its controlled entities and AHT and its controlled entities. Units in AHT and shares in AHL have been stapled together so that neither can be dealt without the other. An AHF security consists of one unit in AHT and one share in AHL. A transfer, issue or reorganisation of a unit or share in any of the component parts is accompanied by a transfer, issue or reorganisation of a unit or share in each of the other component parts.

AHL is a company incorporated and domiciled in Australia. AHT is an Australian registered managed investment scheme. Abacus Funds Management Limited (AFML), the Responsible Entity of AHT, is incorporated and domiciled in Australia and is a wholly owned subsidiary of Abacus Group Holdings Limited (AGHL) which is the parent of the Abacus Property Group (Abacus or APG).

The registered office and principal place of business of AGHL and of AFML is located at Level 34 Australia Square, 264-278 George Street, Sydney NSW 2000.

REVIEW AND RESULTS OF OPERATIONS

The Fund incurred a loss of $3.2 million for the year ended 30 June 2015 (2014: $3.8 million loss).

The hospitality industry, particularly in Queensland has been negatively affected by reduced tourism demand and conference business. The weakening Australian dollar in recent times has seen improvements to inbound tourism.

On 30 January 2015, the Chateau on the Park hotel in Christchurch, New Zealand was sold for NZ$35 million.

The Fund will continue with its managed sell down of assets over the medium term with the expectation that this may take some years.

As at the date of this report, the Fund holds a portfolio of 3 hotels comprising 862 rooms (2014: 4 hotels comprising 1054 rooms). The weighted average capitalisation rate was 8.81%.

The Fund’s gearing decreased during the year to 37% (2014: 44%). The impact of both year-end fair value adjustments and the Fund’s performance on its financial condition were as follows:

2015 2014

126,504 162,878

37.0 44.0

(30,981) (25,353)

49,039 49,039

Total assets ($ '000)

Gearing (%)1

Net assets/(deficiency) ($ '000)

Securities on issue ('000)

ABACUS HOSPITALITY FUND

3

DIRECTORS’ REPORT 30 June 2015

INDIRECT COST RATIO

The Indirect Cost Ratio is the ratio of the Trust’s management costs over the Fund’s average net assets2

attributed for the year, expressed as a percentage. Management costs including management fees, custody fees and other expenses or reimbursements deducted in relation to the Trust, but do not include transactional or operational costs. The Indirect Cost Ratio for the Fund for the year ended 30 June 2015 was 2.25% (2014: 2.4%). 1 Abacus working capital facility is excluded in calculating net debt gearing ratio

2 Abacus working capital facility is excluded in calculating average net assets.

REVIEW OF FINANCIAL CONDITION

At 30 June 2015, the bank loan facility limit was AUD $55.0 million, and drawn amounts were AUD$51.2million. $94.7 million of the existing $150 million Abacus working capital facility was drawn as at 30 June 2015 and $10 million Abacus Finance Pty Ltd loan was fully repaid during the year.

The Fund manages the cash flow effect of interest rate risk by entering into interest rate swap arrangements that are used to convert floating interest rate borrowings to fixed interest rates. At 30 June 2015, approximately $30 million or 59% of total drawn bank debt were covered by interest rate swap arrangements at an average effective fixed interest rate (including bank margin) of 7.16%. The average term to maturity of the bank debt is 1.8 years and the average term to maturity of the swaps is 2.1 years.

The Fund’s net debt gearing ratio (calculated as total interest bearing liabilities less cash assets divided by total assets) excluding the Abacus working capital was 37% at 30 June 2015 (2014: 44%).

DISTRIBUTIONS

The Fund and the Trust distributions in respect of the year ended 30 June 2015 were $1 million (June 2014: $1.0 million), which is equivalent to 2.0 cents per stapled security (June 2014: 2.0 cents). This distribution includes 0.5 cents ($0.25 million) that was paid on 7th August 2015. Further details on the distributions are set out in note 10 of the financial statements.

STAPLED SECURITIES ON ISSUE

During the year no new stapled securities were issued and at 30 June 2015 there were 49.04 million stapled securities on issue (2014: 49.04 million).

SIGNIFICANT EVENTS AFTER BALANCE DATE

Other than as disclosed already in this report, there has been no matter or circumstance that has arisen since the end of the financial year that has significantly affected, or may affect, the Fund's operations in future financial periods, the results of those operations or the Fund's state of affairs in future financial periods.

LIKELY DEVELOPMENTS AND EXPECTED RESULTS

In the opinion of the Directors, disclosure of any further information on future developments and results than is already disclosed in this report or the financial statements would be unreasonably prejudicial to the interests of the Fund.

INFORMATION ON DIRECTORS AND OFFICERS

The Directors and Company Secretary of AHL and AFML (the Responsible Entity of AHT), in office during the financial year and until the date of this report are as set out below, with qualifications, experiences and special responsibilities.

ABACUS HOSPITALITY FUND

4

DIRECTORS’ REPORT 30 June 2015

INFORMATION ON DIRECTORS AND OFFICERS (continued)

John Thame AIBF, FCPA Chairman (non-executive)

Mr Thame has over 30 years’ experience in the retail financial services industry in senior management positions. His 26-year career with Advance Bank included 10 years as Managing Director until the Bank’s merger with St George Bank Limited in 1997. Mr Thame was Chairman (2004 to 2008) and a director (1997 to 2008) of St George Bank Limited and St George Life Limited.

Frank Wolf OAM, PhD, BA(Hons) Managing Director

Dr Wolf has over 25 years’ experience in the property and financial services industries, including involvement in retail, commercial, industrial and hospitality-related assets in Australia, New Zealand and the United States. Dr Wolf has been instrumental in over $3 billion worth of property related transactions, corporate acquisitions and divestments and has financed specialist property-based assets in retirement and hospitality sectors. He is also a director of HGL Limited, a diversified publicly listed investment company.

Malcolm Irving AM, FCPA, SF Fin, BCom, Hon DLitt

Mr Irving is a Non-Executive Director and has many years’ experience in company management, including 12 years as Managing Director of CIBC Australia Limited. He is also a director of O’Connell Street Associates Pty Ltd, Macquarie University Hospital.

Len Lloyd FAPI, WDA

Mr Lloyd is a licensed Real Estate Agent and a registered Real Estate Valuer. He has 40 years experience in the development, management and funding of commercial, retail and residential property. Mr Lloyd joined the Abacus Group in October 2000 and now holds the position of Managing Director of Abacus Property Services Pty Limited responsible for property administration and development opportunities in the Abacus portfolio. In previous positions Mr Lloyd held responsibility for the property portfolios of the Advance Bank and St George Bank and provided valuation and lending advice while with the Commonwealth Development Bank for 21 years.

William J Bartlett FCA, CPA, FCMA, CA(SA)

Mr Bartlett is a Non-Executive Director. As a partner at Ernst & Young for 23 years, he held the roles of Chairman of Worldwide Insurance Practice, National Director of Australian Financial Services Practice and Chairman of the Client Service Board. Mr Bartlett is a director of Suncorp Group Limited, GWA Limited, Reinsurance Group of America Inc and RGA Reinsurance Company of Australia Limited. Mr Bartlett is the Chairman of the Cerebal Palsy Foundation of Australia.

Myra Salkinder MBA, BA

Mrs Salkinder is a Non-Executive Director and is a senior executive of the Kirsh Group. She has been integrally involved over many years with the continued expansion of the Kirsh Group’s property and other investments, both in South Africa and internationally. Mrs Salkinder is a director of various companies associated with the Kirsh Group worldwide.

Peter Spira AM, B Arch (Appointed 27/05/2015)

Mr Spira is a Non-Executive Director. He has over 36 years’ experience in the Australian real estate sector with Meriton Group, Australia’s largest residential apartment developer. He was responsible for Meriton Group’s development projects while also leading the Meriton team in researching and developing new construction and remediation systems. Mr Spira was a director of Meriton Group from 2005 until 2015. In 2006 he received the Order of Australia (AM) for services to the development industry. He is a director of Retire Australia.

Ellis Varejes BCom, LLB Company Secretary and Chief Operating Officer

Mr Varejes has been the Company Secretary since September 2006. He has over 25 years’ experience as a corporate lawyer in private practice.

ABACUS HOSPITALITY FUND

5

DIRECTORS’ REPORT 30 June 2015

INFORMATION ON DIRECTORS AND OFFICERS (continued)

As at the date of this report, the relevant interests of the directors in the stapled securities of AHF were as follows:

Directors AHF securities held

F Wolf 169,778

L Lloyd 30,000

Directors’ Benefits

Since the end of the previous financial year, no director has received or become entitled to receive a benefit, other than any benefit disclosed in the financial statements as compensation or the fixed salary of key management personnel of the Fund or a related entity by reason of a contract made by the Fund or a related body corporate with the director or a with a firm of which he is a member, or with an entity in which he has a substantial financial interest.

Indemnification and Insurance of Directors and Officers

AFML has paid an insurance premium in respect of a contract insuring all directors, full time executive officers and secretary. The terms of this policy prohibit disclosure of the nature of the risks insured or the premium paid.

ENVIRONMENTAL REGULATION AND PERFORMANCE

The Fund’s and the Trust’s environmental responsibilities, such as waste removal and water treatment, have been managed in compliance with all applicable regulations and licence requirements and in accordance with industry standards. No breaches of requirements or any environmental issues have been discovered and brought to the board’s attention. There has been no known significant breaches of any environmental requirements applicable to the Fund and the Trust.

AUDITORS INDEPENDENCE DECLARATION

We have obtained an independence declaration from our auditor, Ernst & Young, and such declaration is shown

on page 6.

ROUNDING

The amounts contained in this report and in the annual financial report have been rounded to the nearest $1,000 (where rounding is applicable) under the option available to the group under ASIC Class Order 98/100. The Fund and the Trust are entities to which the Class Order applies.

Signed in accordance with a resolution of the directors.

John Thame Frank Wolf

Chairman Managing Director

Sydney, 21 August 2015

ABACUS HOSPITALITY FUND

7

CONSOLIDATED INCOME STATEMENT YEAR ENDED 30 JUNE 2015

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

Notes $'000 $'000 $'000 $'000

REVENUE

Rental income - - 9,734 10,568

Hotel income 55,577 58,832 - -

Finance income 141 205 60 91

Total Revenue 55,718 59,037 9,794 10,659

OTHER INCOME

Net change in fair value of hotel property, plant and equipment (74) 1,312 - -

Other income 1 1,133 1,296 1,174 1,291

Total Revenue and Other Income 56,777 61,645 10,968 11,950

Cost of sales (7,358) (7,739) - -

Property expenses & outgoings (476) (506) (206) (206)

Other hotel expenses (15,322) (15,882) - -

Depreciation and amortisation expense 2(a) (3,727) (3,889) - -

Finance costs 2(b) (5,929) (10,276) (5,929) (10,276)

Employee benefits expense 2(c) (21,945) (22,930) - -

Net change in fair value of financial instrument held at balance

date 255 (1,009) 255 (1,009)

Net change in fair value of financial instruments derecognised (1,589) (1,271) (1,589) (1,271)

Net change in fair value of hotel investment property held at

balance date - - (2,390) (1,636)

Net change in fair value of investment properties derecognised (1,548) - (1,421) -

Administrative and other expenses (1,403) (1,613) (1,398) (1,606)

PROFIT/(LOSS) BEFORE TAX (2,265) (3,470) (1,710) (4,054)

Income tax expense 3(a) (914) (291) (565) -

NET PROFIT/(LOSS) AFTER TAX (3,179) (3,761) (2,275) (4,054)

Net profit / (loss) attributable to:

AHL members (812) 229 - -

AHT members (2,367) (3,990) (2,275) (4,054)

NET PROFIT / (LOSS) (3,179) (3,761) (2,275) (4,054)

ABACUS HOSPITALITY FUND

8

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME YEAR ENDED 30 JUNE 2015

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

NET PROFIT / (LOSS) AFTER TAX (3,179) (3,761) (2,275) (4,054)

OTHER COMPREHENSIVE INCOME

Items that will not be reclassified subsequently to the income statement

Revaluation of assets, net of tax 351 (64) - -

Items that may be reclassified subsequently to the income statement

Foreign exchange translation adjustments, net of tax (1,819) 811 (1,539) 797

TOTAL COMPREHENSIVE INCOME/(LOSS) FOR THE YEAR (4,647) (3,014) (3,814) (3,257)

Total comprehensive income/(loss) attributable to:

Members of the parent entity (AHL) (833) 243 - -

Members of other stapled entity:

Non-Controlling interest - Abacus Hospitality Trust (3,814) (3,257) (3,814) (3,257)

TOTAL COMPREHENSIVE INCOME/(LOSS) FOR THE YEAR (4,647) (3,014) (3,814) (3,257)

ABACUS HOSPITALITY FUND

9

CONSOLIDATED STATEMENT OF FINANCIAL POSITION AS AT 30 JUNE 2015

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

Notes $'000 $'000 $'000 $'000

CURRENT ASSETS

Inventory 358 505 - -

Cash and cash equivalents 5 7,222 6,467 3,987 2,383

Trade and other receivables 13(a) 1,751 1,907 458 1,247

Other 346 545 - 219

TOTAL CURRENT ASSETS 9,677 9,424 4,445 3,849

NON-CURRENT ASSETS

Hotel property, plant and equipment 4 114,030 150,307 - -

Deferred tax assets 3(c) 2,797 3,147 4 -

Hotel Investment properties 12 - - 108,413 145,191

Related party receivables 13(b) - - 10,862 11,378

TOTAL NON-CURRENT ASSETS 116,827 153,454 119,279 156,569

TOTAL ASSETS 126,504 162,878 123,724 160,418

CURRENT LIABILITIES

Trade and other payables 7,411 6,044 473 423

Interest-bearing loans and borrowings 7(a) 5,069 5,919 5,069 5,919

Provisions 576 675 - -

TOTAL CURRENT LIABILITIES 13,056 12,638 5,542 6,342

NON-CURRENT LIABILITIES

Interest-bearing loans and borrowings 7(b) 140,559 164,581 140,559 164,581

Derivatives at fair value 2,598 9,675 2,598 9,675

Deferred tax liabilities 3(c) 202 147 - -

Provisions 1,070 1,190 - -

144,429 175,593 143,157 174,256

TOTAL LIABILITIES 157,485 188,231 148,699 180,598

NET LIABILITIES (30,981) (25,353) (24,975) (20,180)

TOTAL EQUITY (30,981) (25,353) (24,975) (20,180)

TOTAL NON-CURRENT LIABILITIES

ABACUS HOSPITALITY FUND

10

CONSOLIDATED STATEMENT OF FINANCIAL POSITION (continued) AS AT 30 JUNE 2015

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Equity attributable to members of AHL:

Contributed equity 2,459 2,459 - -

Reserves - 280 - -

Accumulated losses (8,465) (7,912) - -

Total equity attributable to members of AHL: (6,006) (5,173) - -

Equity attributable to members of AHT:

Contributed equity 43,152 43,152 43,152 43,152

Reserves 351 1,539 - 1,539

Accumulated losses (68,478) (64,871) (68,127) (64,871)

Total equity attributable to unitholders of AHT: (24,975) (20,180) (24,975) (20,180)

TOTAL EQUITY (30,981) (25,353) (24,975) (20,180)

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

Notes $'000 $'000 $'000 $'000

EQUITY

Contributed equity 9 45,611 45,611 43,152 43,152

Reserves 351 1,819 1,539

Accumulated losses (76,943) (72,783) (68,127) (64,871)

TOTAL EQUITY (30,981) (25,353) (24,975) (20,180)

ABACUS HOSPITALITY FUND

11

CONSOLIDATED STATEMENT OF CASH FLOW YEAR ENDED 30 JUNE 2015

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

Notes $'000 $'000 $'000 $'000

CASH FLOWS FROM OPERATING ACTIVITIES

Income receipts 48,785 54,064 11,701 11,367

Interest received 141 205 60 91

Income tax paid (564) - (625) -

Borrowing cost paid (6,476) (20,159) (6,476) (20,158)

Operating payments (37,054) (43,015) (1,461) (1,862)

NET CASH FLOWS FROM / (USED IN) OPERATING ACTIVITIES 5 4,832 (8,905) 3,199 (10,562)

CASH FLOWS FROM INVESTING ACTIVITIES

Purchase of property, plant and equipment (3,015) (4,409) (1,071) (3,437)

Disposal of investment property 32,699 - 32,709 -

Repayment of loans by related entities - - 554 2,089

NET CASH FLOWS FROM / (USED IN) INVESTING ACTIVITIES 29,684 (4,409) 32,192 (1,348)

CASH FLOWS FROM FINANCING ACTIVITIES

Repayment of borrowings (41,504) (64,824) (41,504) (64,824)

Proceeds from borrowings 8,733 74,259 8,733 74,259

Distributions paid (981) (981) (981) (981)

NET CASH FLOWS FROM / (USED IN) FINANCING ACTIVITIES (33,752) 8,454 (33,752) 8,454

NET INCREASE / (DECREASE) IN CASH AND CASH EQUIVALENTS 764 (4,860) 1,639 (3,456)

Net foreign exchange differences (9) 355 (35) 237

Cash and cash equivalents at beginning of year 6,467 10,972 2,383 5,602

CASH AND CASH EQUIVALENTS AT END OF YEAR 5 7,222 6,467 3,987 2,383

ABACUS HOSPITALITY FUND

12

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY YEAR ENDED 30 JUNE 2015

Consolidated AHF - 2015

Asset Foreign

Issued revaluation currency Retained Total

capital reserve translation earnings Equity

CONSOLIDATED $'000 $'000 $'000 $'000 $'000

At 1 July 2014 45,611 - 1,819 (72,783) (25,353)

Other comprehensive income / (loss) - 351 (1,819) - (1,468)

Net loss for the year - - - (3,179) (3,179)

Total comprehensive income / (expense) for the year - 351 (1,819) (3,179) (4,647)

Distribution to security holders - - - (981) (981)

At 30 June 2015 45,611 351 - (76,943) (30,981)

Consolidated AHF - 2014

Asset Foreign

Issued revaluation currency Retained Total

capital reserve translation earnings Equity

CONSOLIDATED $'000 $'000 $'000 $'000 $'000

At 1 July 2013 45,611 64 1,008 (68,041) (21,358)

Other comprehensive income / (loss) - (64) 811 - 747

Net loss for the year - - - (3,761) (3,761)

Total comprehensive income / (expense) for the year - (64) 811 (3,761) (3,014)

Distribution to security holders - - - (981) (981)

At 30 June 2014 45,611 - 1,819 (72,783) (25,353)

Attributable to the stapled security holder

Attributable to the stapled security holder

ABACUS HOSPITALITY FUND

13

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY YEAR ENDED 30 JUNE 2015

Consolidated AHT - 2015

Foreign

Issued currency Retained Total

capital translation earnings Equity

CONSOLIDATED $'000 $'000 $'000 $'000

At 1 July 2014 43,152 1,539 (64,871) (20,180)

Other comprehensive income / (loss) - (1,539) - (1,539)

Net loss for the year - - (2,275) (2,275)

Total comprehensive expense for the year - (1,539) (2,275) (3,814)

Distribution to unit holders - - (981) (981)

At 30 June 2015 43,152 - (68,127) (24,975)

Consolidated AHT - 2014

Foreign

Issued currency Retained Total

capital translation earnings Equity

CONSOLIDATED $'000 $'000 $'000 $'000

At 1 July 2013 43,152 742 (59,836) (15,942)

Other comprehensive income / (loss) - 797 - 797

Net loss for the year - - (4,054) (4,054)

Total comprehensive income / (expense) for the year - 797 (4,054) (3,257)

Distribution to unit holders - - (981) (981)

At 30 June 2014 43,152 1,539 (64,871) (20,180)

Attributable to the unit holder

Attributable to the unit holder

ABACUS HOSPITALITY FUND

14

CONTENTS 30 JUNE 2015

Notes to the financial statements

About this report Page 15

Results for the year

Operating assets and liabilities

Capital structure and financing costs

Group Structure Other Items

1. Revenue

4. Hotel Property, Plant and equipment

5. Cash and cash equivalents

11. Parent entity information

12. Investment properties

2. Expenses

6. Capital management

13. Trade and other receivables

3. Income tax 7. Interest bearing loans and borrowings

14. Commitments and contingencies

8. Financial instruments

15. Related party disclosures

9. Contributed equity

16. Key management personnel

10. Distributions paid and proposed

17. Deed of cross guarantee

18. Summary of significant accounting policies

19. Auditors remuneration

20. Events after balance sheet

Signed reports

Directors’ declaration Page 58

Independent auditor’s report Page 59

ABACUS HOSPITALITY FUND

15

NOTES TO THE FINANCIAL STATEMENTS – About this Report 30 JUNE 2015

AHF is comprised of Abacus Hospitality Limited and its controlled entities (AHL) and Abacus Hospitality Trust and its controlled entities (AHT).

The financial reports of the Abacus Hospitality Fund (the “Fund” or “AHF”) and Abacus Hospitality Trust (the "Trust" or "AHT") for the year ended 30 June 2015 are authorised for issue in accordance with a resolution of the Directors of Abacus Hospitality Limited (“the Company”) and Abacus Funds Management Limited on 21 August 2015.

Net asset deficiency

At 30 June 2015, AHF and AHT have a net asset deficiency of $31.0m and $25.0m respectively (2014: $25.4m and $20.2m respectively) and a net current asset deficiency of $3.4m and $1.1m respectively (2014: $3.2m and $2.5m respectively). AHF and AHT have obtained a letter from Abacus Property Group ("APG") that APG does not intend to request repayment of its loan for a period of 12 months from the date of this financial report and to the extent necessary APG intends to provide financial support to enable AHF and AHT to pay its debts as and when they fall due within the next 12 months.

The nature of the operations and principal activities of the AHF and AHT are described in the Directors’ Report.

SIGNIFICANT ACCOUNTING JUDGMENTS, ESTIMATES AND ASSUMPTIONS

In applying the Fund’s and the Trust’s accounting policies management continually evaluates judgements, estimates and assumptions based on experience and other factors, including expectations of future events that may have an impact on the Fund and the Trust. All judgements, estimates and assumptions made are believed to be reasonable, based on the most current set of circumstances available to management. Actual results may differ from the judgements, estimates and assumptions. Significant judgements, estimates and assumptions made by management in the preparation of these financial statements are outlined below:

(a) Significant accounting judgements

Recovery of deferred tax assets

Deferred tax assets are recognised for deductible temporary differences and tax losses on revenue account as management considers that it is probable that future taxable profits will be available to utilise those temporary differences and tax losses.

(b) Significant accounting estimates and assumptions

Fair value of derivatives

The fair value of derivatives is determined using closing quoted market prices (where there is an active market) or a suitable pricing model based on discounted cash flow analysis using assumptions supported by observable market rates. Where the derivatives are not quoted in an active market their fair value has been determined using (where available) quoted market inputs and other data relevant to assessing the value of the financial instrument.

Valuation of investment properties and property, plant and equipment - Hotels

The Fund and the Trust make judgements in respect of the fair value of investment properties (Note 18(l)) and (Note 18(m)). The fair value of these properties are reviewed regularly by management with reference to external independent property valuations and market conditions existing at reporting date, using generally accepted market practices. The assumptions underlying estimated fair values are those relating to the receipt of contractual rents, expected future market rentals, maintenance requirements, capitalisation rates and discount rates that reflect current market conditions and current or recent property investment prices. If there is any material change in these assumptions or regional, national or international economic conditions, the fair value of investment properties may differ and may need to be re-estimated.

ABACUS HOSPITALITY FUND

16

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

1. REVENUE

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Other Income

Foreign currency exchange gain - 338 - 338

Insurance recoveries 1,164 953 1,164 953

Sundry Income (31) 5 10 -

Total other income 1,133 1,296 1,174 1,291

2. EXPENSES

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

(a) Depreciation and amortisation expense

Depreciation of property, plant and equipment - hotels 3,727 3,889 - -

Total depreciation and amortisation expense 3,727 3,889 - -

(b) Finance costs

Interest on bank loans 4,666 4,681 4,666 4,681

Interest on related party loans 1,090 5,334 1,090 5,334

Amortisation of finance costs 173 261 173 261

Total finance costs 5,929 10,276 5,929 10,276

(c) Employee benefits expense

Wages and salaries 19,249 19,873 - -

Leave provisions 660 957 - -

Other 2,036 2,100 - -

Total employee benefits expense 21,945 22,930 - -

ABACUS HOSPITALITY FUND

17

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

3. INCOME TAX

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

(a) Income tax expense

The major components of income tax expense are:

Income Statement

Current income tax

Current income tax charge 554 231 565 -

Adjustments in respect of current income tax of previous years 69 123 - -

Deferred income tax

Movement in depreciable assets tax depreciation (24) (20) - -

Relating to origination and reversal of temporary differences 315 (43) - -

Income tax expense reported in the income statement 914 291 565 -

(b) Numerical reconciliation between aggregate tax expense

recognised in the income statement and tax expense

calculated per the statutory income tax rate

A reconciliation between tax expense and the product of

accounting profit before income tax multiplied by the

Fund's applicable income tax rate is as follows:

Profit/(loss) before income tax expense (2,265) (3,470) (1,710) -

Prima facie income tax expense/(benefit) calculated at 30% (AU) 101 (917) (160) -

Prima facie income tax expense calculated at 28% (NZ) (728) (116) (638) -

Less prima facie income tax expense/ (benefit) on loss / (profit)

from the Trust (144) 1,197 160 -

Prima Facie income tax of entities subject to income tax (771) 164 (638) -

Entertainment 6 9 - -

Foreign exchange translation adjustments - (5) - -

Adjustment of prior year tax applied 69 123 - -

Derecognition of deferred tax assets 315 - - -

Other items (net) 1,295 - 1,203 -

Income tax expense 914 291 565 -

Income tax expense reported in the consolidated income

statement 914 291 565 -

ABACUS HOSPITALITY FUND

18

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

3. INCOME TAX (continued)

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

(c) Recognised deferred tax assets and liabilities

Deferred income tax at 30 June 2015 relates to the following:

Deferred tax liabilities

Other 202 147 - -

Gross deferred income tax liabilities 202 147 - -

Deferred tax assets

Losses available for offset against future taxable income 3,022 3,247 - -

Derecognition of deferred tax assets (losses) (1,000) (1,000)

Employee provisions 494 547 - -

Other 281 353 4 -

Gross deferred income tax assets 2,797 3,147 4 -

Unrecognised temporary differences

At 30 June 2015, there are no unrecognised temporary differences associated with the Fund’s investments in subsidiaries, as the Fund has no liability for additional taxation should unremitted earnings be remitted (2014: $nil).

Losses available for offset against future gains

At 30 June 2015, the Fund has recognised a deferred tax asset of $2.0m (2014:$2.2m) from unutilised tax losses which are available indefinitely for offset against future taxable profits subject to continuing to meet relevant statutory tests. The utilisation of these losses is dependent on future taxable profits being generated within the entities subject to tax. The Fund has determined, based on a profit forecast prepared, that future taxable profits will be available to offset these losses.

Tax consolidation

AHL and its 100% owned Australian resident subsidiaries have formed a tax consolidated group. AHL is the head entity of the tax consolidated group. The head entity and the controlled entities in the tax consolidated group continue to account for their own current and deferred tax amounts. Members of the tax groups during the relevant periods have entered into tax sharing arrangements in order to allocate income tax expense to the head entity of the group. In addition, the agreement provides for the allocation of income tax liabilities between the entities should the head entity default on its tax payment obligations. At 30 June 2015, the possibility of default is remote.

Nature of the tax funding agreement

Members of the respective tax consolidated groups have entered into tax funding agreements. The tax funding agreements require payments to/from the head entity to be recognised via an inter-entity receivable (payable) which is at call. To the extent that there is a difference between the amount allocated under the tax funding agreement and the allocation under UIG 1052, the head entity accounts for these as equity transactions.

The amounts receivable or payable under the tax funding agreements are due upon receipt of the funding advice from the head entity, which is issued as soon as practicable after the end of each financial year. The head entity may also require payment of interim funding amounts to assist with its obligations to pay tax instalments.

ABACUS HOSPITALITY FUND

19

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

4. HOTEL PROPERTY, PLANT AND EQUIPMENT

The following table is a reconciliation of the movements of property, plant and equipment classified as Level 3 in accordance with the fair value hierarchy outlined in Note 8 for the year ended 30 June 2015.

AHF AHF

Consolidated Consolidated

2015 2014

$'000 $'000

Property

Australasian Hotels 114,030 150,307

114,030 150,307

Average market capitalisation rate 8.81% 9.57%

AHF AHF

Consolidated Consolidated

2015 2014

$'000 $'000

Land and buildings

At 1 July, net of accumulated depreciation 139,587 133,559

Additions 1,352 3,068

Fair value movement through the income statement (74) 1,312

Fair value movement through comprehensive income 351 (64)

Disposal (35,759) -

Effect of movements in foreign exchange 333 2,860

Depreciation charge for the year (1,416) (1,148)

At 30 June, net of accumulated depreciation 104,374 139,587

Cost or fair value less costs to sell 119,151 154,522

Accumulated depreciation (14,777) (14,935)

Net carrying amount at end of year 104,374 139,587

Plant and equipment

At 1 July, net of accumulated depreciation 10,720 12,061

Additions 1,662 1,341

Disposals (406) -

Effect of movements in foreign exchange (9) (24)

Depreciation charge for the year (2,311) (2,658)

At 30 June, net of accumulated depreciation 9,656 10,720

Cost or fair value 31,087 33,941

Accumulated depreciation (21,431) (23,221)

Net carrying amount at end of year 9,656 10,720

Total net carrying amount of Property, Plant & Equipment 114,030 150,307

If property, plant and equipment was carried under the cost model, the carrying amount would be $114.2m (2014:150.8m).

ABACUS HOSPITALITY FUND

20

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

4. HOTEL PROPERTY, PLANT AND EQUIPMENT (continued)

Revaluation gain on property, plant and equipment:

Property, plant and equipment held in AHF relate to hotel assets and are held at fair value at 30 June 2015. During the year a decrease in fair value to reflect the recoverable amount was recognised as a loss of $0.1m in the income statement (2014: a gain of $1.3m). Recoverable amount has been determined as the fair value of the property, plant and equipment by reference to internal and external valuations performed as detailed below.

The hotel property, plant and equipment are carried at the directors’ determination of fair value. The determination of fair value includes reference to the original acquisition cost together with capital expenditure since acquisition and either the latest full independent valuation, latest independent update or directors’ valuation. Total acquisition costs include incidental costs of acquisition such as property taxes on acquisition, legal and professional fees and other acquisition related costs.

In the year ended 30 June 2015, 0% (2014: 100%) by number of the property portfolio was subject to external valuation.

Sensitivity Information

Significant input Fair value measurement sensitivity to significant increase in input

Fair value measurement sensitivity to significant decrease in input

Net market EBITDA Increase Decrease

Optimal occupancy Increase Decrease

Adopted capitalisation rate Decrease Increase

The adopted capitalisation rate forms part of the income capitalisation approach.

When calculating the income capitalisation approach, the EBITDA has a strong interrelationship with the adopted capitalisation rate given the methodology involves assessing the total EBITDA generated from the property and capitalising this in perpetuity to derive a capital value. In theory, an increase in the EBITDA and an increase (softening) in the adopted capitalisation rate could potentially offset the impact to the fair value. The same can be said for a decrease in the EBITDA and a decrease (tightening) in the adopted capitalisation rate. A directionally opposite change in the EBITDA and the adopted capitalisation rate could potentially magnify the impact to the fair value.

- A weighted average capitalisation rate for the hotel properties is 8.81% (2014: 9.57%).

- The current weighted average occupancy rate for the hotel properties is 72% (2014: 72%).

External valuations are conducted by qualified independent valuers who are appointed by the Managing Director of Abacus Property Services Pty Ltd who is also responsible for the Fund’s and the Trust’s internal valuation process. He is assisted by one employee who holds relevant recognised professional qualifications and is experienced in valuing the types of properties in the applicable locations.

The hotel property, plant and equipment are independently valued on a staggered basis every two years unless the underlying financing requires a more frequent independent valuation cycle.

The hotel property, plant and equipment are used as security for secured bank debt.

ABACUS HOSPITALITY FUND

21

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

5. CASH AND CASH EQUIVALENTS

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Reconciliation to Cash Flow Statement

For the purposes of the Cash Flow Statement, cash and

cash equivalents comprise the following at 30 June 2015:

Cash at bank and in hand 1

7,222 6,467 3,987 2,383

1. Cash at bank earns interest at floating rates. The carrying amounts of cash and cash equivalents represent fair value.

Reconciliation of net profit after tax to net cash flows from operations

Net profit / (loss) (3,179) (3,761) (2,275) (4,054)

Adjustments for:

Depreciation and amortisation expense 3,727 3,889 - -

Amortisation of finance costs 173 261 173 261

Net change in fair value of financial instruments held at balance date (255) 1,009 (255) 1,009

Net change in fair value of financial instruments derecognised 1,589 1,271 1,589 1,271

Net change in fair value of hotel property, plant and equipment held at

balance date

74 (1,312) - -

Net change in fair value of investment property derecognised 3,456 - 3,070 -

Net change in fair value of investment property held at balance date - - 2,390 1,636

Foreign currency exchange difference (1,908) (336) (1,649) (336)

Increase/(Decrease) in payables 1,552 (11,328) (857) (9,574)

(Increase)/decrease in receivables and other assets (397) 1,402 1,013 (775)

Net cash from operating activities 4,832 (8,905) 3,199 (10,562)

(a) Disclosure of financing facilities

Refer to note 7d

ABACUS HOSPITALITY FUND

22

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

6. CAPITAL MANAGEMENT

The Fund and Trust seek to manage their capital requirements through a mix of debt and equity funding. It also ensures that Fund and Trust entities comply with capital and distribution requirements of their constitutions and/or Fund and Trust deeds, the capital requirements of relevant regulatory authorities and continue to operate as going concerns. The Fund and Trust also protect their equity in assets by taking out insurance. The Fund and Trust assess the adequacy of their capital requirements, cost of capital and gearing (i.e. debt/equity mix) as part of its broader strategic plan. In addition to tracking actual against budgeted performance, the Fund and Trust routinely review their capital structure to ensure sufficient funds and financing facilities, on a cost effective basis are available to implement the Fund’s and Trust’s strategy that adequate financing facilities are maintained and distributions to members are made within the stated distribution guidance (i.e. distributions are paid out of operating cashflows and to the extent where necessary, Abacus Finance Pty Limited will defer the payment of interest on its Working Capital Facility and/or management fees to support the distribution). The Fund and Trust can manage their capital via the following strategies: activating its distribution reinvestment plan, adjusting the amount of distributions paid to members, activating a security buyback program, divesting assets, active management of the Fund’s and the Trust’s fixed rate swaps or (where practical) recalibrating the timing of transactions and capital expenditure so as to avoid a concentration of net cash outflows. A summary of the AHF’s and the AHT’s key banking covenants is set out below. It is recognised that falling property prices could place pressure on compliance with the LVR. With financial support from APG to the extent necessary, AHF and AHT anticipate managing their covenant compliance by effecting the strategies set out above.

Covenant Measure Key details

Nature of facilities Secured, non recourse The Fund and the Trust have no unsecured facilities

Debt covenants Compliant Key covenants include Bank LVRs and Asset ICR

ABACUS HOSPITALITY FUND

23

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

7. INTEREST BEARING LOANS AND BORROWINGS

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

(a) Current

Loans from related parties 3

5,069 5,919 5,069 5,919

5,069 5,919 5,069 5,919

(b) Non-current

Bank loans - A$ 1,2

51,233 42,500 51,233 42,500

Bank loans - A$ value of NZ$ denominated loan - 23,759 - 23,759

Loans from related parties 3

89,666 98,696 89,666 98,696

Less: Unamortised borrowing costs (340) (374) (340) (374)

140,559 164,581 140,559 164,581

(c) Maturity profile of current and non-current interest

bearing loans

Due within one year 5,069 5,919 5,069 5,919

Due within two to five years 140,559 164,955 140,559 164,955

145,628 170,874 145,628 170,874

The Fund and the Trust maintain a range of interest-bearing loans and borrowings. The sources of funding are spread over a number of counterparties and the terms of the instruments are negotiated to achieve a balance between capital availability and cost of debt.

1 Bank loans – A$ are provided by a major bank at floating interest rates. The loans are denominated in Australian dollars and mature on 30 April 2017 with a term to maturity of 1.8 years. The interest on floating rate borrowings is paid quarterly based on existing swap and yield rates quoted on the rate reset date. The bank loans are secured by a charge over the investment properties and certain property, plant and equipment as detailed in note 4 and note 12.

2 AHF’s weighted average interest rate as at 30 June 2015 was 8.07% (2014: 7.7%).

3 Loans are provided by Abacus related entities to assist in funding the acquisition of hotels and to provide working capital. The interest rate on the borrowings is 8%, however, the rate was reduced to 2.0% for the year (2014: 3.25%). The loan matures in June 2019 and has a remaining term to maturity of 4 years. This loan ranks equally with other unitholders upon liquidation of AHF to the extent of a deficit/shortfall to issue price.

ABACUS HOSPITALITY FUND

24

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

7. INTEREST BEARING LOANS AND BORROWINGS (continued)

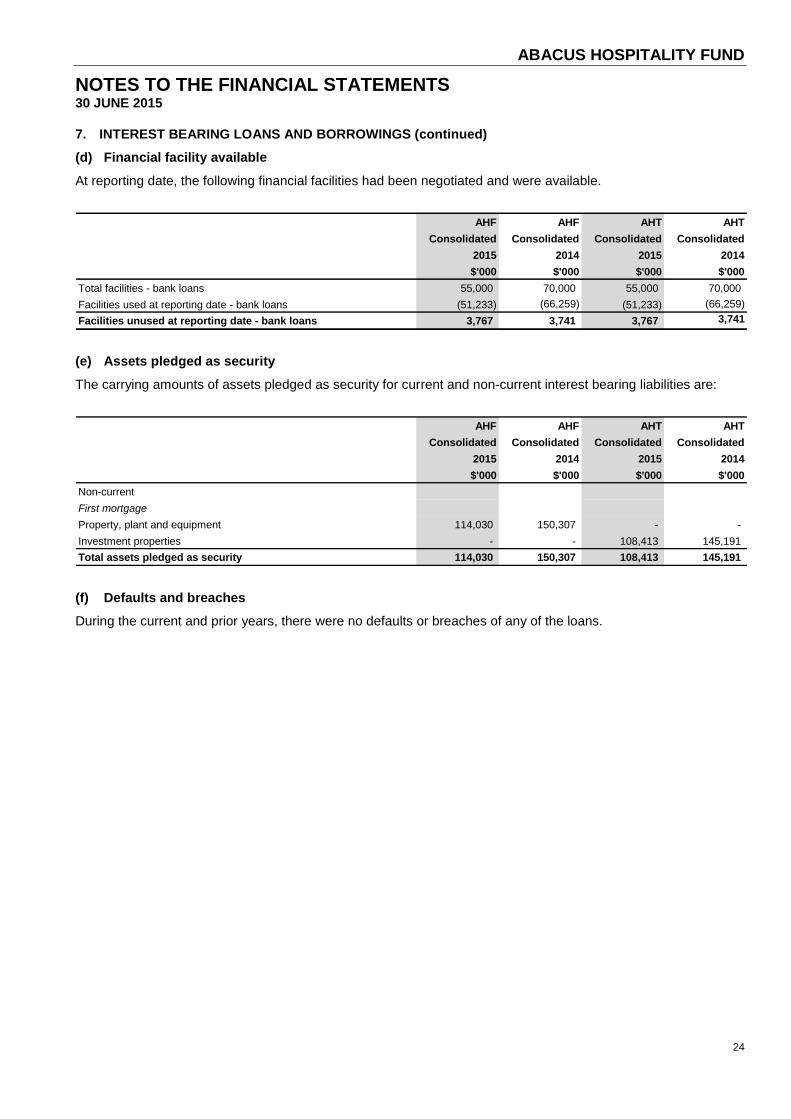

(d) Financial facility available

At reporting date, the following financial facilities had been negotiated and were available.

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Total facilities - bank loans 55,000 70,000 55,000 70,000

Facilities used at reporting date - bank loans (51,233) (66,259) (51,233) (66,259)

Facilities unused at reporting date - bank loans 3,767 3,741 3,767 3,741

(e) Assets pledged as security

The carrying amounts of assets pledged as security for current and non-current interest bearing liabilities are:

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Non-current

First mortgage

Property, plant and equipment 114,030 150,307 - -

Investment properties - - 108,413 145,191

Total assets pledged as security 114,030 150,307 108,413 145,191

(f) Defaults and breaches

During the current and prior years, there were no defaults or breaches of any of the loans.

ABACUS HOSPITALITY FUND

25

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS

Financial Risk Management

The risks arising from the use of the Fund’s and the Trust’s financial instruments are credit risk, liquidity risk and market risk (interest rate risk, price risk and foreign currency risk).

The Fund’s and the Trust’s financial risk management focuses on mitigating the unpredictability of the financial markets and its impact on the financial performance of the Fund and the Trust. The Board reviews and agrees policies for managing each of these risks, which are summarised below.

Primary responsibility for identification and control of financial risks rests with the Treasury Management Committee under the authority of the Board. The Board reviews and agrees policies for managing each of the risks identified below, including the setting of limits for trading in derivatives, hedging cover of interest rate risks and cash flow forecast projections.

The main purpose of the financial instruments used by the Fund and the Trust is to raise finance for the Fund and the Trust’s operations. The Fund and the Trust have various other financial assets and liabilities such as trade receivables and trade payables, which arise directly from its operations. The Fund and the Trust also enter into derivative transactions principally interest rate swaps. The purpose is to manage the interest rate exposure arising from the Fund and the Trust’s operations and its sources of finance.

Details of the significant accounting policies and methods adopted, including the criteria for recognition, the basis of measurement and the basis on which income and expenses are recognised, in respect of each class of financial asset, financial liability and equity instruments are disclosed in Note 18.

(a) Credit risk

Credit risk is the risk of financial loss to the Fund and the Trust if a customer or counterparty to a financial instrument fails to meet its contractual obligations, and arises principally from the Fund’s and the Trust’s receivables from customers, interest bearing loans and derivatives with banks.

The Fund and the Trust manage its exposure to risk by:

- derivative counterparties and cash transactions are limited to high credit quality financial institutions;

- policy which limits the amount of credit exposure to any one financial institution;

- regularly monitoring loans and receivables balances on an ongoing basis; and

- obtaining collateral as security (where required or appropriate).

With respect to credit risk arising from the other financial assets and liabilities of the Fund and the Trust, which comprise cash and cash equivalents and certain derivative instruments, the Fund’s and the Trust’s exposure to credit risk arises from default of the counter party, with a maximum exposure equal to the carrying amount of these instruments.

ABACUS HOSPITALITY FUND

26

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(a) Credit risk (continued)

Credit risk exposures

The Fund’s and the Trust’s maximum exposure to credit risk at the reporting date was:

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Receivables 1,751 1,907 458 1,247

Related party receivables - - 10,862 11,378

Cash and cash equivalents 7,222 6,467 3,987 2,383

8,973 8,374 15,307 15,008

As at 30 June 2015, the Fund and the Trust have the following concentrations of credit risk:

- Receivables: $1.3 million was represented by trading receivable by hotel operating companies in AHL.

The following table illustrates grouping of the Fund’s and the Trust’s trade and other receivables. As noted in disclosure note 3, the Fund and the Trust mitigate the exposure to this risk by evaluation of the credit submission before acceptance, ensuring security is obtained and consistent and timely monitoring of the financial instrument to identify and potential adverse changes in the credit quality. Also, the credit risks of the insurers are mitigated through the use of insurance brokers to seek, place and diversify insurance covers across various well rated insurers.

CONSOLIDATED AHF

Total Original term 1 Extended term Past due term 2 Impaired

30 June 2015 $'000 $'000 $'000 $'000 $'000

Trade and other receivables 1,751 1,473 273 5 -

less: provisioning - - - - -

Total 1,751 1,473 273 5 -

CONSOLIDATED AHF

Total Original term 1 Extended term Past due term 2 Impaired

30 June 2014 $'000 $'000 $'000 $'000 $'000

Trade and other receivables 1,919 1,380 535 4 -

less: provisioning (12) - (8) (4) -

Total 1,907 1,380 527 - -

1. Terms are extended typically in recognition of hotel trading conditions (peak season) and agreement with vendors. 2. For loans with past due terms all are less than one year old. Other than the provision raised, the Fund has assessed that the remaining

debtors are still recoverable.

ABACUS HOSPITALITY FUND

27

NOTES TO THE FINANCIAL STATEMENTS

30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(a) Credit risk (continued)

CONSOLIDATED AHT

Total Original term Extended term Past due term Impaired

30 June 2015 $'000 $'000 $'000 $'000 $'000

Trade and other receivables 458 458 - - -

less: provisioning - - - - -

Total 458 458 - - -

CONSOLIDATED AHT

Total Original term Extended term Past due term Impaired

30 June 2014 $'000 $'000 $'000 $'000 $'000

Trade and other receivables 1,247 1,247 - - -

less: provisioning - - - - -

Total 1,247 1,247 - - -

The movement in the allowance for impairment in respect of secured property loans and receivables during the year was as follows:

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Balance at 1 July 2014 12 15 - -

Impairment loss recognised 2 9 - -

Impairment loss utilised (14) (12) - -

Balance at 30 June 2015 - 12 - -

ABACUS HOSPITALITY FUND

28

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(b) Liquidity Risk

Prudent liquidity risk management implies maintaining sufficient cash and marketable securities, the availability of funding through an adequate and diverse amount of committed credit facilities, the ability to close out market positions and the flexibility to raise funds through the issue of new stapled securities or the distribution reinvestment plan.

The Fund’s and the Trust’s policy is to maintain an available loan facility with banks sufficient to meet expected operational expenses and to finance investment acquisitions for a period of 90 days, including the servicing of financial obligations. Current loan facilities are assessed and extended for a maximum period based on the Fund’s and the Trust’s expectations of future interest and market conditions.

As at 30 June 2015, the Fund and the Trust have undrawn committed facilities of $3.8 million and cash of $7.2 million which are adequate to cover short term funding requirements. Further information regarding the Fund’s and the Trust’s debt profile is disclosed in Note 7.

The table below shows an analysis of the contractual maturities of key liabilities which forms part of the Fund’s and the Trust’s assessment of liquidity risk.

CONSOLIDATED AHF Carrying

Amount

Contractual

cash flows 1 Year or less

Over 1 year to

5 years

Over 5

years

30 June 2015 $'000 $'000 $'000 $'000 $'000

Liabilities

Trade and other payables 7,411 7,411 7,411 - -

Interest bearing loans and borrowings # 148,226 183,326 11,244 172,081 -

Total liabilities 155,637 190,737 18,655 172,081 -

CONSOLIDATED AHF Carrying

Amount

Contractual

cash flows 1 Year or less

Over 1 year to

5 years

Over 5

years

30 June 2014 $'000 $'000 $'000 $'000 $'000

Liabilities

Trade and other payables 6,044 6,044 6,044 - -

Interest bearing loans and borrowings # 180,175 232,334 13,424 218,910 -

Total liabilities 186,219 238,378 19,468 218,910 -

CONSOLIDATED AHT Carrying

Amount

Contractual

cash flows 1 Year or less

Over 1 year to

5 years

Over 5

years

30 June 2015 $'000 $'000 $'000 $'000 $'000

Liabilities

Trade and other payables 473 473 473 - -

Interest bearing loans and borrowings # 148,226 183,326 11,244 172,081 -

Total liabilities 148,699 183,799 11,717 172,081 -

CONSOLIDATED AHT Carrying

Amount

Contractual

cash flows 1 Year or less

Over 1 year to

5 years

Over 5

years

30 June 2014 $'000 $'000 $'000 $'000 $'000

Liabilities

Trade and other payables 423 423 423 - -

Interest bearing loans and borrowings # 180,175 232,334 13,424 218,910 -

Total liabilities 180,598 232,757 13,847 218,910 -

# Carrying amount includes fair value of derivative liabilities. Contractual cash flows includes contracted debt and net swap payments using prevailing forward rates

ABACUS HOSPITALITY FUND

29

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

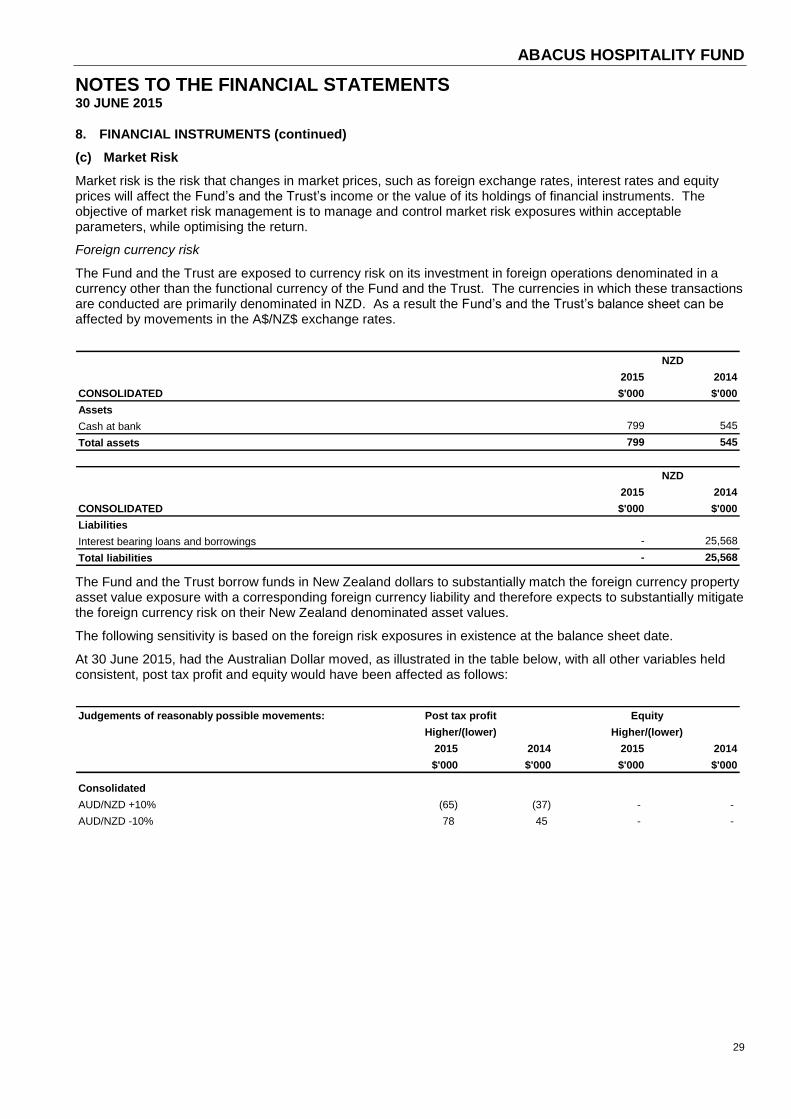

(c) Market Risk

Market risk is the risk that changes in market prices, such as foreign exchange rates, interest rates and equity prices will affect the Fund’s and the Trust’s income or the value of its holdings of financial instruments. The objective of market risk management is to manage and control market risk exposures within acceptable parameters, while optimising the return.

Foreign currency risk

The Fund and the Trust are exposed to currency risk on its investment in foreign operations denominated in a currency other than the functional currency of the Fund and the Trust. The currencies in which these transactions are conducted are primarily denominated in NZD. As a result the Fund’s and the Trust’s balance sheet can be affected by movements in the A$/NZ$ exchange rates.

2015 2014

CONSOLIDATED $'000 $'000

Assets

Cash at bank 799 545

Total assets 799 545

2015 2014

CONSOLIDATED $'000 $'000

Liabilities

Interest bearing loans and borrowings - 25,568

Total liabilities - 25,568

NZD

NZD

The Fund and the Trust borrow funds in New Zealand dollars to substantially match the foreign currency property asset value exposure with a corresponding foreign currency liability and therefore expects to substantially mitigate the foreign currency risk on their New Zealand denominated asset values.

The following sensitivity is based on the foreign risk exposures in existence at the balance sheet date.

At 30 June 2015, had the Australian Dollar moved, as illustrated in the table below, with all other variables held consistent, post tax profit and equity would have been affected as follows:

Judgements of reasonably possible movements:

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Consolidated

AUD/NZD +10% (65) (37) - -

AUD/NZD -10% 78 45 - -

Higher/(lower) Higher/(lower)

Post tax profit Equity

ABACUS HOSPITALITY FUND

30

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(c) Market Risk (continued)

Interest rate risk / Fair value interest rate risk

The Fund’s and the Trust’s exposure to the risk of changes in market interest rates relates primarily to its long-term bank debt obligations which are based on floating interest rates. The Fund and the Trust have a policy to maintain a mix of floating exposure and fixed interest rate hedging with fixed rate cover highest in years 1 to 5.

The Fund and the Trust hedge to minimise interest rate risk by entering variable to fixed interest rate swaps which also helps deliver interest covenant compliance and positive carry (net rental income in excess of interest expense) on the property portfolio. Interest rate swaps have the economic effect of converting borrowings from variable rates to fixed rates. Under the interest rate swaps, the Fund and the Trust agree to exchange, at specified intervals, the difference between fixed and variable rate interest amounts calculated by reference to the agreed notional principal amounts. At 30 June 2015, after taking into account the effect of interest rate swaps, approximately 58.6% of the Fund and the Trust’s drawn debt is subject to fixed rate hedges (2014: 64.8%). Hedge cover as a percentage of available facilities at 30 June 2015 is 54.5% (2014: 61.3%).

As the Fund and the Trust hold interest rate swaps against its variable rate debt there is a risk that the economic value of a financial instrument will fluctuate because of changes in market interest rates. The level of variable rate debt subject to interest rate swaps and fixed rate debt is disclosed in Note 7.

ABACUS HOSPITALITY FUND

31

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(c) Market Risk (continued)

Interest rate risk / Fair value interest rate risk (continued)

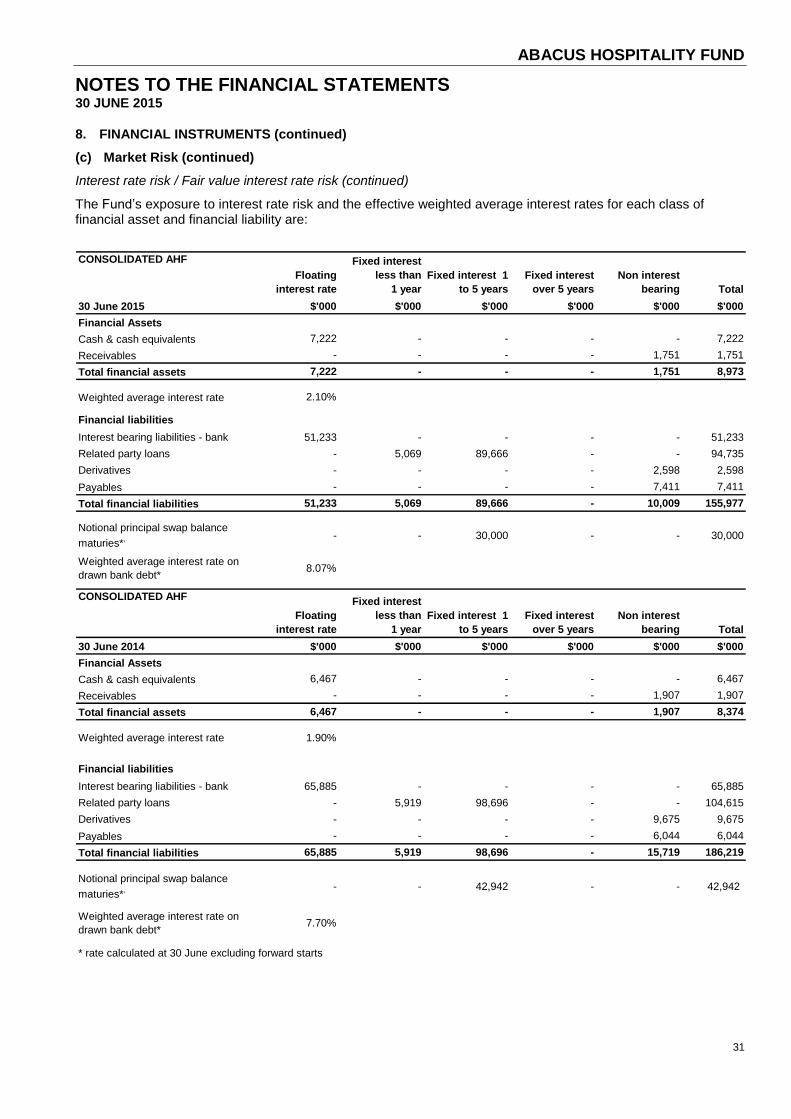

The Fund’s exposure to interest rate risk and the effective weighted average interest rates for each class of financial asset and financial liability are:

CONSOLIDATED AHF

Floating

interest rate

Fixed interest

less than

1 year

Fixed interest 1

to 5 years

Fixed interest

over 5 years

Non interest

bearing Total

30 June 2015 $'000 $'000 $'000 $'000 $'000 $'000

Financial Assets

Cash & cash equivalents 7,222 - - - - 7,222

Receivables - - - - 1,751 1,751

Total financial assets 7,222 - - - 1,751 8,973

Weighted average interest rate 2.10%

Financial liabilities

Interest bearing liabilities - bank 51,233 - - - - 51,233

Related party loans - 5,069 89,666 - - 94,735

Derivatives - - - - 2,598 2,598

Payables - - - - 7,411 7,411

Total financial liabilities 51,233 5,069 89,666 - 10,009 155,977

Notional principal swap balance

maturies*, - - 30,000 - - 30,000

Weighted average interest rate on

drawn bank debt*8.07%

CONSOLIDATED AHF

Floating

interest rate

Fixed interest

less than

1 year

Fixed interest 1

to 5 years

Fixed interest

over 5 years

Non interest

bearing Total

30 June 2014 $'000 $'000 $'000 $'000 $'000 $'000

Financial Assets

Cash & cash equivalents 6,467 - - - - 6,467

Receivables - - - - 1,907 1,907

Total financial assets 6,467 - - - 1,907 8,374

Weighted average interest rate 1.90%

Financial liabilities

Interest bearing liabilities - bank 65,885 - - - - 65,885

Related party loans - 5,919 98,696 - - 104,615

Derivatives - - - - 9,675 9,675

Payables - - - - 6,044 6,044

Total financial liabilities 65,885 5,919 98,696 - 15,719 186,219

Notional principal swap balance

maturies*, - - 42,942 - - 42,942

Weighted average interest rate on

drawn bank debt*7.70%

* rate calculated at 30 June excluding forward starts

ABACUS HOSPITALITY FUND

32

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(c) Market Risk (continued)

Interest rate risk / Fair value interest rate risk (continued)

The Trust’s exposure to interest rate risk and the effective weighted average interest rates for each class of financial asset and financial liability are:

CONSOLIDATED AHT

Floating

interest rate

Fixed interest

less than

1 year

Fixed interest

1 to 5 years

Fixed interest

over 5 years

Non interest

bearing Total

30 June 2015 $'000 $'000 $'000 $'000 $'000 $'000

Financial Assets

Cash & cash equivalents 3,987 - - - - 3,987

Receivables - - - - 458 458

Total financial assets 3,987 - - - 458 4,445

Weighted average interest rate 2.27%

Financial liabilities

Interest bearing liabilities - bank 51,233 - - - - 51,233

Related party loans - 5,069 89,666 - - 94,735

Derivatives - - - - 2,598 2,598

Payables - - - - 473 473

Total financial liabilities 51,233 5,069 89,666 - 3,071 149,039

Notional principal swap balance

maturies*, - - 30,000 - - 30,000

Weighted average interest rate on

drawn bank debt*8.07%

CONSOLIDATED AHT

Floating

interest rate

Fixed interest

less than

1 year

Fixed interest

1 to 5 years

Fixed interest

over 5 years

Non interest

bearing Total

30 June 2014 $'000 $'000 $'000 $'000 $'000 $'000

Financial Assets

Cash & cash equivalents 2,383 - - - - 2,383

Receivables - - - - 1,247 1,247

Total financial assets 2,383 - - - 1,247 3,630

Weighted average interest rate 2.60%

Financial liabilities

Interest bearing liabilities - bank 65,885 - - - - 65,885

Related party loans - 5,919 98,696 - - 104,615

Derivatives - - - - 9,675 9,675

Payables - - - - 423 423

Total financial liabilities 65,885 5,919 98,696 - 10,098 180,598

Notional principal swap balance

maturies*, # - - 42,942 - - 42,942

Weighted average interest rate on

drawn bank debt*7.70%

* rate calculated at 30 June excluding forward starts

#The Trust had interest rate swap positions which in notional terms exceeded the amount of debt borrowed, as a result of repaying bank

debt from hotel sales, including Diplomat in October 2012 and Swissotel in June 2010. .

ABACUS HOSPITALITY FUND

33

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(c) Market Risk (continued)

Interest rate risk / Fair value interest rate risk (continued)

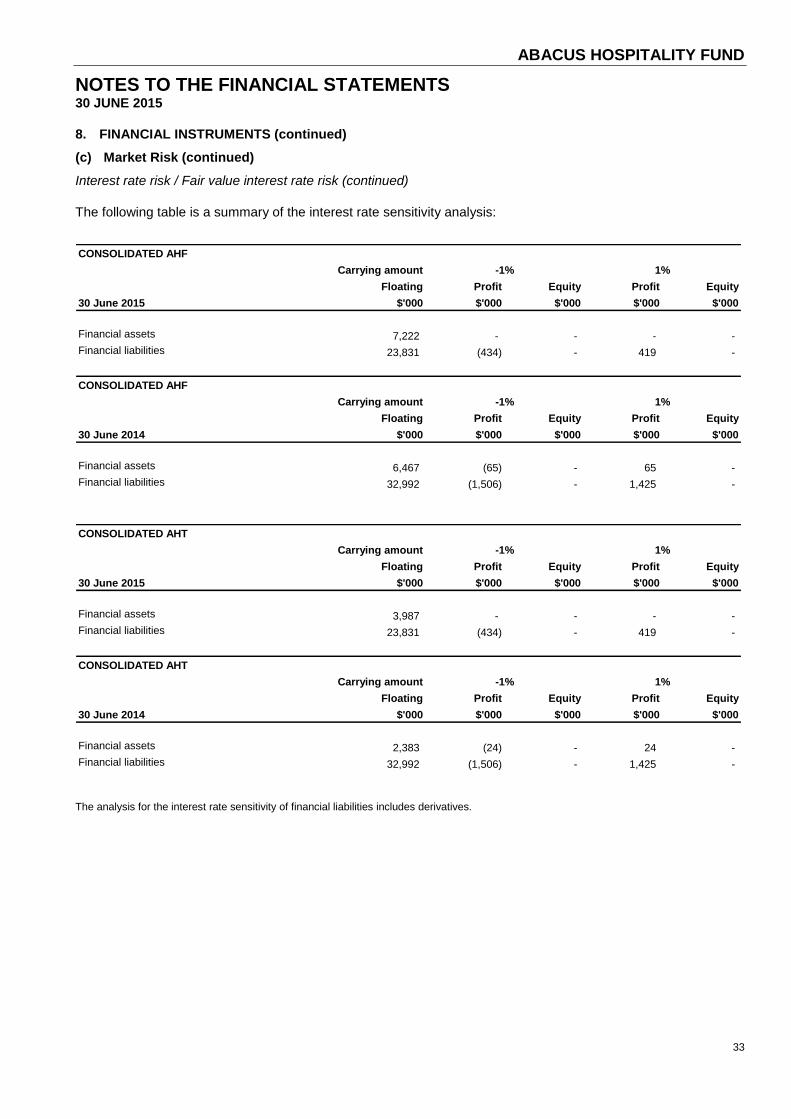

The following table is a summary of the interest rate sensitivity analysis:

CONSOLIDATED AHF

Carrying amount

Floating Profit Equity Profit Equity

30 June 2015 $'000 $'000 $'000 $'000 $'000

Financial assets 7,222 - - - -

Financial liabilities 23,831 (434) - 419 -

CONSOLIDATED AHF

Carrying amount

Floating Profit Equity Profit Equity

30 June 2014 $'000 $'000 $'000 $'000 $'000

Financial assets 6,467 (65) - 65 -

Financial liabilities 32,992 (1,506) - 1,425 -

CONSOLIDATED AHT

Carrying amount

Floating Profit Equity Profit Equity

30 June 2015 $'000 $'000 $'000 $'000 $'000

Financial assets 3,987 - - - -

Financial liabilities 23,831 (434) - 419 -

CONSOLIDATED AHT

Carrying amount

Floating Profit Equity Profit Equity

30 June 2014 $'000 $'000 $'000 $'000 $'000

Financial assets 2,383 (24) - 24 -

Financial liabilities 32,992 (1,506) - 1,425 -

-1% 1%

-1% 1%

-1% 1%

-1% 1%

The analysis for the interest rate sensitivity of financial liabilities includes derivatives.

ABACUS HOSPITALITY FUND

34

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(c) Market Risk (continued)

Interest rate risk / Fair value interest rate risk (continued)

Set out below, is a comparison by category of the carrying amounts and fair values of all the Fund’s and Trust’s financial instruments:

Carrying Fair Carrying Fair

Amount Value Amount Value

2015 2015 2014 2014

CONSOLIDATED AHF $'000 $'000 $'000 $'000

Financial assets

Cash and cash equivalents 1

7,222 7,222 6,467 6,467

Trade and other receivables (current) 1

1,751 1,751 1,907 1,907

Total financial assets 8,973 8,973 8,374 8,374

Financial Liabilities

Trade and other payables 1

7,411 7,411 6,044 6,044

Interest bearing loans and borrowings (current) 2

5,069 5,069 5,919 5,919

Interest bearing loans and borrowings (non-current) 2

140,559 140,559 164,581 164,581

Derivatives (non-current) 3

2,598 2,598 9,675 9,675

Total financial liabilities 155,637 155,637 186,219 186,219

Net financial assets / (liabilities) (146,664) (146,664) (177,845) (177,845)

Carrying Fair Carrying Fair

Amount Value Amount Value

2015 2015 2014 2014

CONSOLIDATED AHT $'000 $'000 $'000 $'000

Financial assets

Cash and cash equivalents 1

3,987 3,987 2,383 2,383

Trade and other receivables (current) 1

458 458 1,247 1,247

Total financial assets 4,445 4,445 3,630 3,630

Financial Liabilities

Trade and other payables 1

473 473 423 423

Interest bearing loans and borrowings (current) 2

5,069 5,069 5,919 5,919

Interest bearing loans and borrowings (non-current) 2

140,559 140,559 164,581 164,581

Derivatives (non-current) 3

2,598 2,598 9,675 9,675

Total financial liabilities 148,699 148,699 180,598 180,598

Net financial assets / (liabilities) (144,254) (144,254) (176,968) (176,968)

1. These financial assets and liabilities are not subject to interest rate or market risk and the fair value approximates carrying value.

2. The fair value of these financial liabilities (excluding derivative instruments and finance lease $2.2 million1) are determined at each

reporting date in accordance with generally accepted valuation techniques; these include the use of recent arm’s length transactions, reference to other assets that are substantially the same; or discounted cash flow analysis.

3. These financial assets and liabilities are subject to interest rate and market risks, the basis of determining the fair value is set out below in the fair value hierarchy.

ABACUS HOSPITALITY FUND

35

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

8. FINANCIAL INSTRUMENTS (continued)

(d) Market Risk (continued)

Interest rate risk / Fair value interest rate risk (continued)

In accordance with AASB 7 Financial Instruments: Disclosures and AASB13 Fair Value Measurement the Fund’s and Trust’s financial instruments are classified into the following fair value measurement hierarchy:

Level 1 Quoted prices (unadjusted) in active market for identical assets or liabilities;

Level 2 Inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

Level 3 Inputs for the asset or liability that are not based on observable market data.

Level 1 Level 2 Level 3 Total

30 June 2015 $'000 $'000 $'000 $'000

Current

Interest bearing loans and borrowings - 5,069 - 5,069

Total current - 5,069 - 5,069

Non-current

Derivative liabilities - 2,598 - 2,598

Interest bearing loans and borrowings - 140,559 - 140,559

Total non-current - 143,157 - 143,157

There were no transfers between levels 1,2 and 3 during the year.

Level 1 Level 2 Level 3 Total

30 June 2014 $'000 $'000 $'000 $'000

Current

Interest bearing loans and borrowings - 5,919 - 5,919

Total current - 5,919 - 5,919

Non-current

Derivative liabilities - 9,675 - 9,675

Interest bearing loans and borrowings - 164,581 - 164,581

Total non-current - 174,256 - 174,256

There were no transfers between Levels 1, 2 and 3 during the period.

Determination of fair Value

The fair value of interest rate swaps is determined using a generally accepted pricing model on a discounted cash flow analysis using assumptions supported by observable market rates.

ABACUS HOSPITALITY FUND

36

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

9. CONTRIBUTED EQUITY

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

(a) Issued securities

Issued securities 45,611 45,611 43,152 43,152

Total contributed equity 45,611 45,611 43,152 43,152

(b) Movement in stapled securities on issue

Number Value Number Value

'000 '000 '000 '000

At 1 July 2014 49,039 45,611 49,039 43,152

Securities on issue at 30 June 2015 49,039 45,611 49,039 43,152

AHF AHT

Issued securities Issued units

TERMS AND CONDITIONS OF STAPLED SECURITIES

Each security confers upon the security holder an equal interest in the Fund and the Trust, and is of equal value. A security does not confer any interest in any particular asset or investment of the scheme. security holders have various rights under the Constitution and the Corporations Act 2001, including the right to:

- Receive income distributions; - Attend and vote at meetings of security holders; - Participate in the termination and winding up of the scheme;

The Abacus working capital loan ranks equally with other security holders upon liquidation of AHF and AHT to the extent of a deficit/shortfall to issue price.

10. DISTRIBUTIONS PAID AND PROPOSED

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

(a) Distributions paid during the year

Jun 2014 quarter: 0.500 cents per security (2013: 0.500 cents) 245 245 245 245

Sep 2014 quarter: 0.500 cents per security (2013: 0.500 cents) 245 245 245 245

Dec 2014 quarter: 0.500 cents per security (2013: 0.500 cents) 245 245 245 245

Mar 2015 quarter: 0.500 cents per security (2014: 0.500 cents) 246 246 246 246

981 981 981 981

(b) Distributions proposed and not recognised as a liability^

Jun 2015 quarter: 0.500 cents per security (2014: 0.500 cents) 245 245 245 245

^ The final distribution of 0.50 cents per stapled security was declared on 1 July 2015. The distribution paid on 7 August 2015 was $0.245 million. No provision for the distribution has been recognised in the balance sheet at 30 June 2015 as the distribution had not been declared by the end of the year.

ABACUS HOSPITALITY FUND

37

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

11. PARENT ENTITY FINANCIAL INFORMATION

AHF AHF AHT AHT

PARENT PARENT PARENT PARENT

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Results of the parent entity

Profit/(loss) for the year (59) (3) 198 (6,283)

Other comprehensive income - - - -

Total comprehensive expense for the year (59) (3) 198 (6,283)

Financial position of the parent entity at year end

Current assets 1 1 4,489 3,020

Total assets 1,438 1,413 120,493 152,344

Current liabilities 2,043 1,909 5,337 6,253

Total liabilitites 2,043 1,959 148,834 180,883

Net deficiency (605) (546) (28,341) (28,539)

Total equity of the parent entity comprising of:

Issued capital 2,459 2,458 43,152 43,152

Retained earnings/(accumulated losses) (3,064) (3,004) (71,493) (71,691)

Total equity (605) (546) (28,341) (28,539)

(a) Parent Entity contingencies

There are no contingencies with the parent entity as at 30 June 2015 (2014: $Nil).

(b) Parent Entity capital commitments

The parent entity has not entered into any capital commitments as at 30 June 2015 (2014: $Nil).

(c) Parent Entity guarantees in respect of debts of its subsidiaries

The parent entity has entered into a Deed of Cross Guarantee with the effect that the Company guarantees debts in respect of its subsidiaries.

Further details of the Deed of Cross Guarantee and the subsidiaries subject to the deed are disclosed in Note 17.

ABACUS HOSPITALITY FUND

38

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

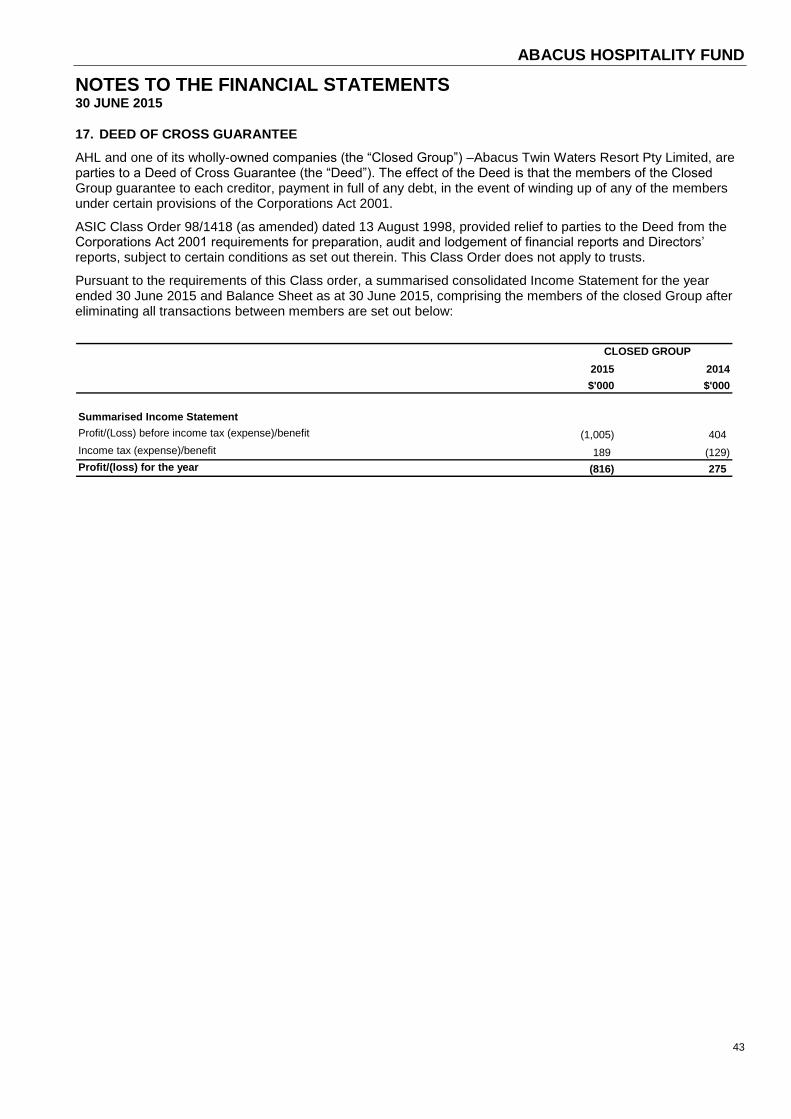

12. INVESTMENT PROPERTIES

Reconciliation

A reconciliation of the carrying amount of the hotel investment properties at the beginning and end of the period is as follows. All investment properties are classified as Level 3 in accordance with the fair value hierarchy outlined in Note 8(d):

AHF AHF AHT AHT

Consolidated Consolidated Consolidated Consolidated

2015 2014 2015 2014

$'000 $'000 $'000 $'000

Carrying amount at beginning of the financial period - - 145,191 140,594

Additions and capital expenditure - - 1,069 3,436

Fair value adjustments for properties held at balance date - - (2,390) (1,636)

Disposal - - (35,779) -

Effect of movements in foreign exchange - - 322 2,797

Carrying amount at end of the financial year - - 108,413 145,191

Investment properties are carried at the Directors’ determination of fair value. The determination of fair value includes reference to the original acquisition cost together with capital expenditure since acquisition and either the latest full independent valuation, latest independent update or directors’ valuation. Total acquisition costs include incidental costs of acquisition such as property taxes on acquisition, legal and professional fees and other acquisition related costs.

Sensitivity Information

Significant input Fair value measurement sensitivity to significant increase in input

Fair value measurement sensitivity to significant decrease in input

Adopted capitalisation rate Decrease Increase

Optimal occupancy Increase Decrease

Adopted discount rate Decrease Increase

The adopted capitalisation rate forms part of the income capitalisation approach.

When calculating the income capitalisation approach, the net market rent has a strong interrelationship with the adopted capitalisation rate given the methodology involves assessing the total net market income receivable from the property and capitalising this in perpetuity to derive a capital value. In theory, an increase in the net market rent and an increase (softening) in the adopted capitalisation rate could potentially offset the impact to the fair value. The same can be said for a decrease in the net market rent and a decrease (tightening) in the adopted capitalisation rate. A directionally opposite change in the net market rent and the adopted capitalisation rate could potentially magnify the impact to the fair value.

When assessing a discounted cash flow, the adopted discount rate and adopted terminal yield have a strong interrelationship in deriving at a fair value given the discount rate will determine the rate in which the terminal value is discounted to the present value.

During the year ended 30 June 2015, 0% (30 June 2014: 100%) of the number of investment properties in the portfolio was subject to external valuations, the remaining 100% (30 June 2014: nil) was subject to internal valuation.

External valuations are conducted by qualified independent valuers who are appointed by the Managing Director of Abacus Property Services Pty Ltd who is also responsible for the Fund’s and the Trust’s internal valuation process. The Managing Director is assisted by one employee who holds relevant recognised professional qualifications and is experienced in valuing the types of properties in the applicable locations.

Investment properties are independently valued on a staggered basis every two years unless the underlying financing requires a different valuation cycle.

The majority of the investment properties are used as security for secured bank debt outlined in Note 7(e).

ABACUS HOSPITALITY FUND

39

NOTES TO THE FINANCIAL STATEMENTS 30 JUNE 2015

13. TRADE AND OTHER RECEIVABLES